Introduction

The impact of small and medium enterprises (SSEs) to every nation has been documented to include job generation, poverty alleviation, wealth creation and economic vitality. As a result, SSEs has recorded to be the engine of economic growth and development. They contribute more than 80% of the GDP, 60% of the total employment creation and 70% of the total raw materials of large cooperation of both developed and developing countries (Ogunleye , 2004). They also provide the platform for technological and manpower development required by both private and public enterprises of a particular nation. This observation formed the major basis in the comments of Hoselitz, (1959); Staley and Morse, (1966); World Bank, (1978a, 1978b) who categorically emphasized that Small-scale enterprises (SSEs) generate more direct jobs of investment than large enterprises. They serve as a training ground for developing technical and entrepreneurial skills and by virtue of their greater use of indigenous technological capabilities, they promote local inter-sectoral linkages (particularly in agriculture) and contribute to the dynamism and competitiveness of the economy.

Small Scale Enterprises have attracted the attention of several researchers, NGOs and governments in formulating strategies on how best they can be assisted in the achievement of their entrepreneurial objectives. The significance of SSEs has been recognized by the government of most developing countries, and many have introduced special support programmes in an attempt to boost their activities and harness the benefits embeded in their existence. A large number of such programmes have concentrated on the provision of small industry credit, frequently associated with technical advice (Brunton, 1997), in Nigeria, both the federal and state governments have initiated policies and schemes to support the survival and substance of this sector. Emmanuel (2012), opined that the Nigerian governments had at one time or the other developed set of policies to enhance the development of SSEs after identifying its role in boosting the economy of the nation. The efforts of the Nigerian governments towards SSEs development can be traceable to 1946 when the government made the first attempt to be committed to industrial development whose functions among others include; (i) To promote and develop village crafts and industries hence develop Nigerian products (ii) To set up and operate an experimental undertaking for the testing of Nigerian industrial products; (iii) To engage in other suitable projects approved by the governor-in-council geared towards development of the economy. Most of these policies and schemes centered on to finance the operations of SSEs, with several provisions made for how well business owners can raise their initial capital outlay through either the conventional banks or establishment of specialized loan schemes to ensure that adequate funds are available for them when needed. To meet up with this responsibility, the Nigerian government at one point or the other, had voted special fund allocation in its budget to ensure speedy development and effective operation of SSEs in Nigeria.

Business organisations have diverse objectives, among which is the objective of profit maximization, survival, which will enable them to continue to contribute to the economic development of the nation (Obigbemi, 2010). However, it is sad to note that in spite of the efforts of the government to support this subsector, evidences have shown that majority of them do not survive their first five years of existence and if peradventure they survived, the issue of inadequate finance has been noted to be a ‘thorn in their flesh’. It has been observed that although the intentions of the government is good, the implementation of some of these policies was saddled with serious administrative bottle necks that have frustrated their efforts towards achieving their objectives in providing support to SSEs. The poor performance of some of these credit programmes in various parts of the developing world is an ample testimony to the ineffectiveness of the administration aspect of the credit schemes. This has called for more research and investigation for an alternative and better way of meeting the entrepreneurial objectives of the SSEs operators. On this regards, several researchers have provided different suggestions and comments on how best to solve this challenge. These include; Osuntogun and Adeyemo (1981), Ojo (1982); Akanji, (1994); Akanji (1998), Aluko (1980),Chandanvaker (1985); Falegan (1987) and (Alabi , Alabi, Akrobo, (2007); Oloyede, (2008) but only few of these studies focused on the indigenous way of providing credit to the small scale enterprises towards helping them to achieve their entrepreneurial objectives. This study, therefore is aimed at examining the effectiveness of Esusu scheme as a strategy for achieving the entrepreneurial objectives of SSEs in Nigeria using Ado-Odo Otta, Ogun State Nigeria, as case study. To achieve this objective, this paper is divided into five parts; introduction, literature review/conceptual framework, methodology, data analysis, conclusion and recommendations.

Literature Review/Conceptual Framework

The Concept of SSEs

The concept of SSEs is dynamic and relative (Olorunshola 2003; Ogunleye 2004). Several institutions and agencies defined SSEs differently with parameters such as employee’s size, asset base, turnover, financial strength, working capital and size of the business. These definitions include; Nigerian Industrial Policy 1989 defined SSEs as enterprise whose investment in working capital is between N100,000 and N2m excluding cost of land. CBN Monetary Policy Circular No. 22 of 1998 defined SSEs as any enterprise whose investments include land and working capital is less than 300,000 and annual turnover is less than N5m. The Nigerian Industrial Development Bank (NIDB) also defined small enterprise as an enterprise that has investment and working capital not exceeding N750,000 and medium enterprise as one with N750,000 to N3m. The Federal Ministry of Industry Guidelines to NBCI also defined as business with a total cost not exceeding N500,000 (excluding cost of land but including working capital). Centre for Industrial Research and Development (CIRD) of the Obafemi Awolowo University, Ile-Ife defined SSEs as an enterprise with capital base not exceeding N25,000 and employing capital base not exceeding N250,000 and employing on full time basis, 50 workers or less.

The National Council on Industry (NCI 2001) offered the following definitions for micro, small and large scale enterprises in Nigeria. Small or cottage industry is industry with a labour size of not more than 10 workers, or total cost of not more than N1.50 million, including working capital but excluding cost of land, and /or, a workforce of not more than 10 workers. Small-Scale Industry An industry with a labour size of 11-100 workers or a total cost of not more thanN50 million, including working capital but excluding cost of land, and /or, a workforce of 11-100workers.

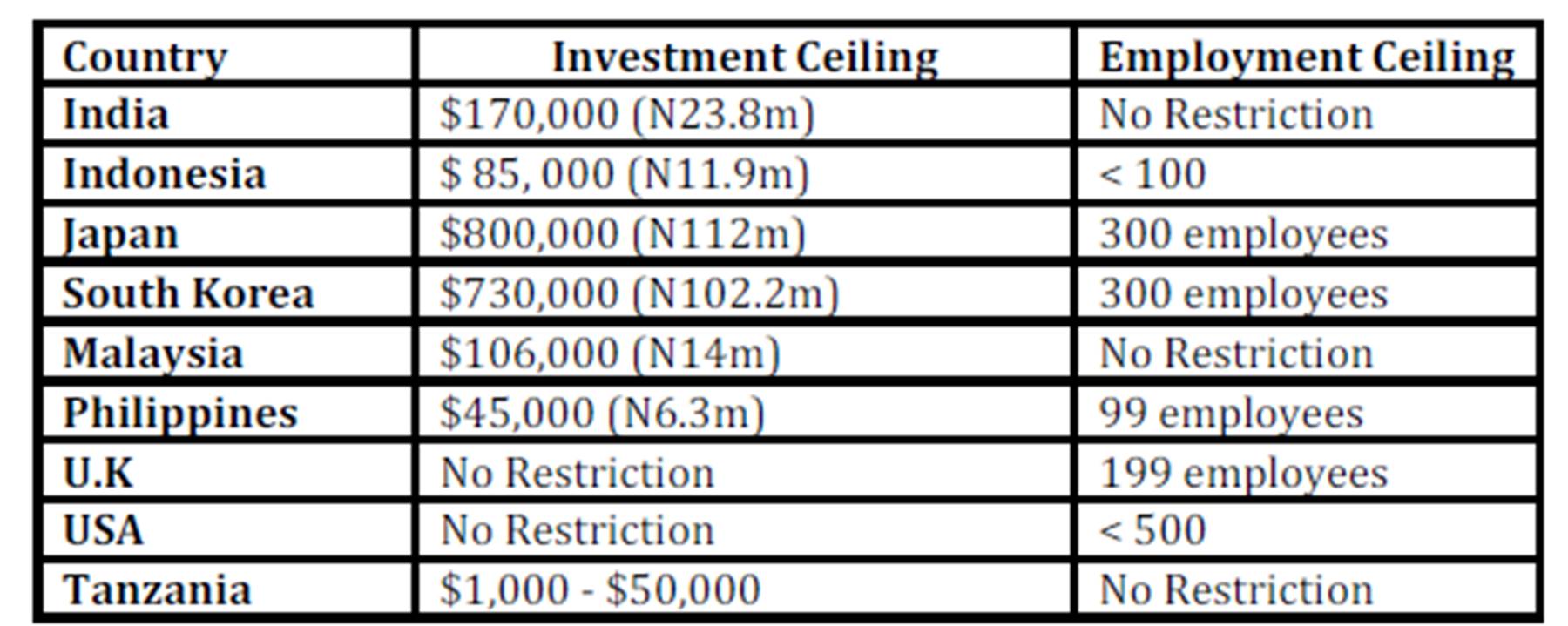

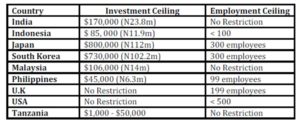

Table 1 : Definition of SSEs in other Nations

Source: (i) Confederation of Asia Pacific Chamber of Commerce and Industry – Journal of Commerce and Industry, Vol. 11, 1994.

The above definitions show that there is no universal definition of SSEs however, for the purpose of this write up the definition of SSEs according to SMIES can be adopted which defined SSEs as establishment with less than N20m (exclude cost of land and working and has more than 10 employees and less than 300 employees.

Characteristics of SSEs

The peculiar characteristics of SSEs have helped in enhancing their entrepreneurial performance in the economy. By their nature, SSEs constitute the most viable and veritable vehicle for self-sustaining industrial development. They possess common capability to grow an indigenous enterprise culture more than any other strategy (Udechukwu 2003). Adeleja (2005) enumerated the following as the peculiar attributes of SSEs; creativity, provision of inputs and or material components for large enterprises, mainly found everywhere especially in the local communities and fasted tools for job creation. Olorunshola (2004) in his work identified simple management structure result from the fusion of ownership and management by one man as another characteristic of SSEs. According to (Udechukwu 2003) SSEs are characterized by labour intensive production processes, centralized management, have limited access to long term capital, use local resources, and closely attached to the products that launched them. The peculiarity of SSEs in enhancing economic development can be best described in this statement;

SSEs constitute the most dynamic segment of many transition and developing economies. They are more innovative, faster growing, family/individual ownership and subjective in decision making and possibly more profitable as compared to larger sized enterprises (World Bank 2001; Ogunleye, 2004).

Contributions of SSEs to Economic Development

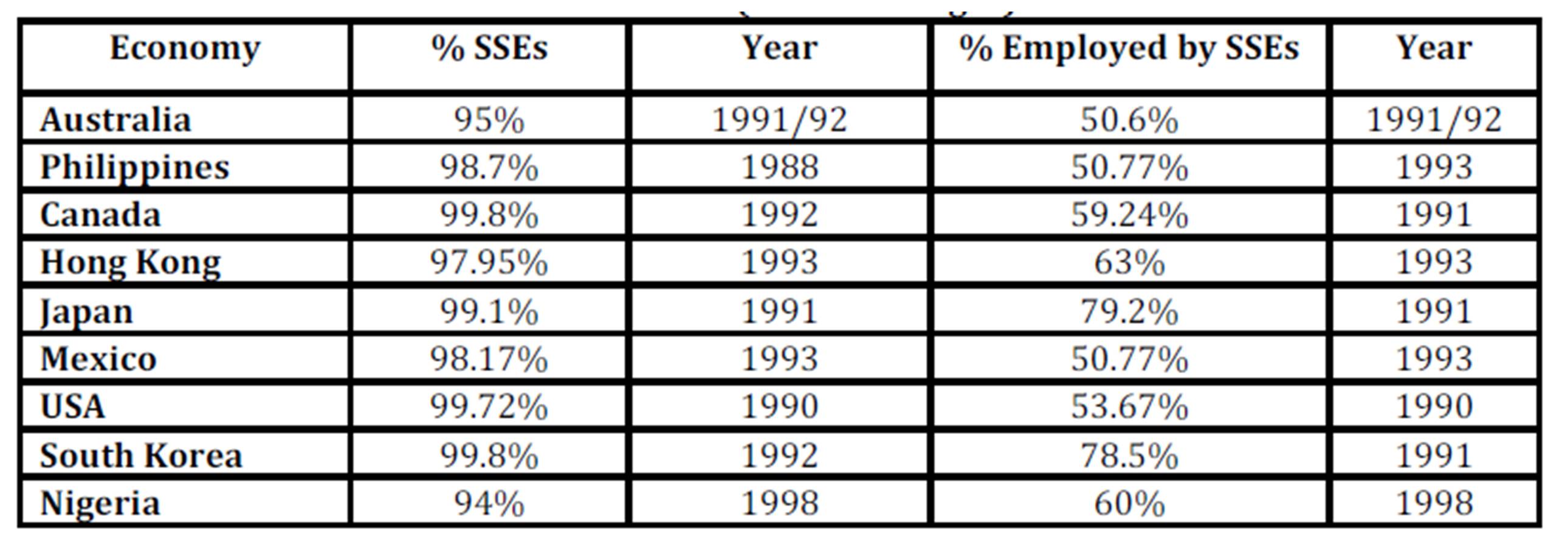

The contributions of SSEs to economic development of both developed and less developed countries have been obvious in these nations’ GDP, industrial output, employment, poverty alleviation and export promotion. Statistically, the Nigerian GDP by sector shows that agriculture contributes about 32%, industry 41% and 27% (Weller et al 1999). In most cases, of the industry figure, SSEs usually dominate all other sub-sectors. For instance, in Japan, 80% of the total industrial labour force belongs to SSEs sector, 50% in Germany and 46% in USA are employed in SSEs. In USA, SSEs contribute nearly 39% to their national Income (Udechukwu, 2003). Also in less developed countries such as Nigeria, India, Indonesia, Mali etc., SSEs have been identified to constitute more than 95% of establishments in the organized manufacturing sector and have become a vibrant core sub-sector making substantial contribution in terms of employment generation and industrial output and export (Udechukwu, 2003). This means that SSEs play important role in the economies of both developing and developed countries.

The table below shows the contributions of SSEs in some countries including Nigeria.

Table 2: Contributions of SSEs to Overall Economy And on Employment

Generation ( in Percentages)

Source: Oyekanmi (2004) Concepts of Equity Financing and its implication for SMIEIS

The above performance of SSEs in developed and less developed economies was identified as a result of the following reasons; well-defined and complementary roles of the private and public sectors in SSEs promotion, Structure of credit/capital provided to the SSEs, nature of the incentives directed at SSEs, and Identification and implementation of factors driving such programs (Oyekanmi, 2004).

Financing of SSEs

Funding has been identified as a very important factor to the survival of SSEs (Jimoh, 2004). Every business operation is financed through (i) owner’s equity, (ii) debt. It is the sole responsibility of the entrepreneur to consider the features of the various sources of funds before taking the decision on the source or the mix of finance to be used for his or her business. Oyekanmi (2004) identified the following as the different features of sources of funds; Owner’s Equity- commitment to the business, capital for promoting growth and expansion, while debt features include- lower cost of capital, leverage on the equity return, enforced fiscal discipline, and preoccupation with collateral security. Critical analysis of the features of equity and debt sources of finance will enable SSEs operators to take appropriate decision on the best mix of finance. This is to say that all the sources of finance for SSEs fall within owner’s equity, debt and government funding schemes and institutions. Sources of financing SSEs include; plough back, bank loan, overdraft, banker’s acceptance, accrual accounts and some government schemes which include; Central Bank of Nigeria’s Support And Schemes For SSEs Financing, the National Economic Reconstruction Fund (NERFUND), Agricultural Credit Guarantee Scheme Fund, Refinancing and Rediscounting Facility, The Small and Medium Industries Equity Investment Scheme (SMIEIS), Nigerian Agricultural, Cooperative and Rural Development Bank (NACRDB), Bank of Industry (BOI) etc. (Ogunleye, 2004).

Esusu Scheme Operation in Nigeria

ESusu is one of the African most ancient traditional banking systems which has over the years been the mode of fund mobilization for initiation, sustenance and in some cases development of SSEs (Alabi, Alabi, Tei Akrobo, 2007). The concept of Esusu has different names from different tribes of Nigeria. For instance, in Igbo land it is called ‘Itu,utu’, in Yoruba tribe it is called ‘Esusu or Ajo’ while in Hauas land it is called ‘Adache’, in Ghana is called “Susu” or ‘Esu’ in Bahamas, ‘Susu’ in Tobago or Sou in Trinidad ( Okafor, 2008). The Esusu system is so popular that among the Yorubas and Igbos in Nigeria today, it has been noted that there is hardly a single adult who is not a member of one or even several Esusu schemes (Seibel and Damachi, 1982; Alabi, Alabi, Tei Akrobo, 2007). The system is virtually in all the tribes in West Africa as well as in many other parts of the world. Its importance has made it to be integrated in the credit system for the financing of micro, small and medium businesses especially in the rural areas. Due to the problems the entrepreneurs are encountering with the formal financial institutions, the Esusu system has now been extended to the urban areas. Some of them now operate like microfinance Bank. This was the observation of Barclays (2005) cited in Norwood ( 2005); Alabi, Alabi, Tei Akrobo (2007) when he emphasized that with the expansion of the money economy, these informal financial institutions (IFIs) have not lost their vigor. Quite to the contrary, they have multiplied, both in numbers and diversity. Its simple structure and modus operands has earned it wide recognition and it seems to have proven to be a dependable and cost effective mechanism of emphasizing state participation and encouragement of the domestic indigenous sector( Alabi , Alabi, Tei Akrobo, 2007). In the IMF working paper, the Esusu system is classified into three categories based on the classification according to Basu et al.( 2004). These include Esusu Clubs and Esusu Associations, Mobile collectors and Cooperatives societies Alabi, Alabi, Ahiawodzi, 2006).

Entrepreneurial Objectives of SSEs and Esusu System

The entrepreneurial requirements of any enterprise, whether small, medium or large, can be categorised under four broad headings; marketing, financial, production and human resource. The entrepreneurial objectives of the SSEs focus on the ability of the SSEs operators to identify the needs in their immediate environment bring together the resources towards meeting the needs so to attain their set objectives. The marketing function emphasizes on meeting objectives that have to do with branding, advertising, promotion etc, financial objectives refer to the economic lives of the SSEs which extend for the medium to long term, production objectives focus on ensuring that raw materials are processed into finished goods, the human resources objectives ensure that the right employees are being recruited and appropriately remunerated. All these entrepreneurial objectives require both fixed and working capital. Fixed capital is concerned with investment in assets such as land, buildings and equipment, working capital on the other hand, consists mainly of cash, inventories of raw materials, work-in progress and finished goods, and accounts receivable. Implicit in this definition is the notion that the working capital of the financial objectives of SSEs are ‘self-liquidating’ over the short-term – a period approximating the enterprise’s production cycle – while their funds invested in fixed capital are only recovered from cash-flow surpluses over the medium to long term (Brunton,1997; Alabi, Alabi, Ahiawodzi, 2006; Oloyede, 2007). This shows that adequate funding is required to operate the enterprise over the production period. Thus the financial objectives constitute more than 60% of the total entrepreneurial objectives of SSEs as majority of their operators see lack of finance as the main challenge their enterprises (Norwood, 2005; Oloyede, 2007).

The study of Kihiko (2012) revealed this clearly. This study showed that t among all the small business entrepreneurs basic needs, financial needs constitute about 119(70%) of the businesses needs and the findings also showed that 145(86%) of all the small-scale businesses depend on credit for business capital (Kihiko, 2012). The findings showed that most entrepreneurs, 131 (90%) with credit get it from informal financial institutions such as rotating credit and savings associations. The relative importance of these financial requirements of SSEs depends on a number of factors, the most important being the size of the enterprise, the industry group in which it operates and the nature of the technology employed (Brunton, 1997). While there are significant differences between countries, regions and sectors, in general, small scale enterprises tend to have lower relative financial requirements for both fixed and working capital because of the high degree of labour intensity exhibited (Brunton, 1997).

Methodology

The sample design of this paper was based on a simple sampling approach. To carry out this study, one hundred (100) entrepreneurs were randomly selected from Ado-Odo Ota Local Government Area in Ogun State which is the population of the study was purposively selected (Singleton, Straits, and Straits, 1993), while snowball sampling techniques were used to select members of the Esusu scheme (Neuman, 2003). All participants are dwellers of Ota village in Ado-Ota Local Government Area in Ogun State. The activities of the small scale entrepreneurs were captured using some demographic items such as age, sex, nature of their business, year they started the business structure and other variables. The instrument of structured questionnaire was used to obtain the necessary data required for this study. The use of questionnaire was necessitated so as to enable the respondents to be objective and precise in responding to the research questions. The questionnaire was sectionalized into three parts with more than twenty five (25) items which include information on the profile of the entrepreneurs. A five-point Likert- scale that ranges from strongly agree to strongly disagree of point scale of (5 to 1) was used to capture the activities of the Esusu scheme with the respondents. A statistical model of single regression was used to test the hypothesis of this study. The use of regression is important so as to test the relationship between the independent and dependent variable.

Survey Results

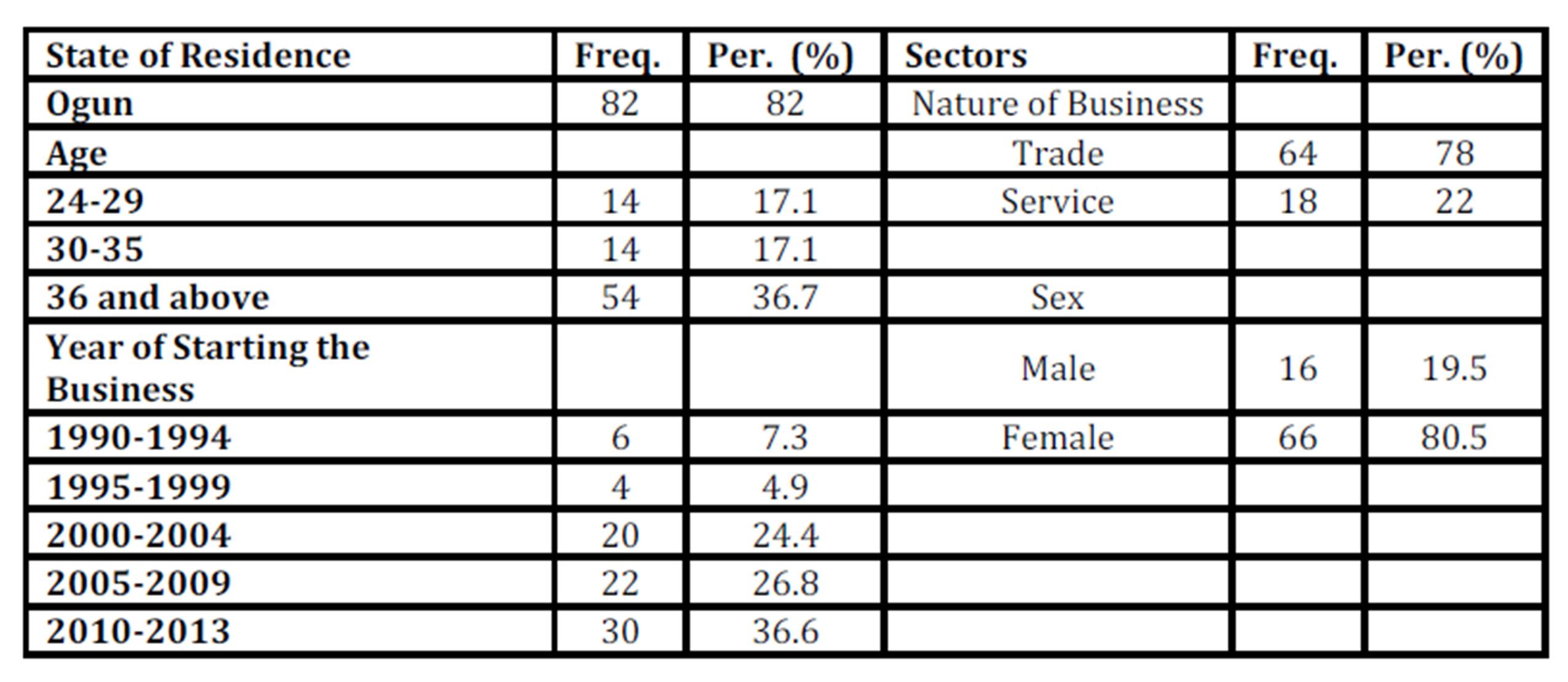

To analyze the data of this study, SPSS 12 (SPSS, Inc., 2003) statistical program was used. Descriptive statistics which include percentage distributions, mean and standard deviation were calculated based on the respondent’s responses for each item on the demographic information of the respondents and this includes their age, sex, the nature of business, year they stated business and their the Esusu scheme. Table 3 depicted that out of the 100 questionnaires distributed, 82 or 82.00% of the questionnaire were retrieved from the respondents and this forms the sample size of this study.

Table 3 showed that majority of the businesses owned by the entrepreneurs are in the distribution as 64(78%) in trade and 18(22%) in service sector. Considering the respondents’ year of starting the business, majority of them, about 70(87.8%) of them started the business between 2000 and 2013.

Table 3: Descriptive Statistics of Entrepreneurs by Age, Nature of Business n=82,

Source: Field Study (2013)

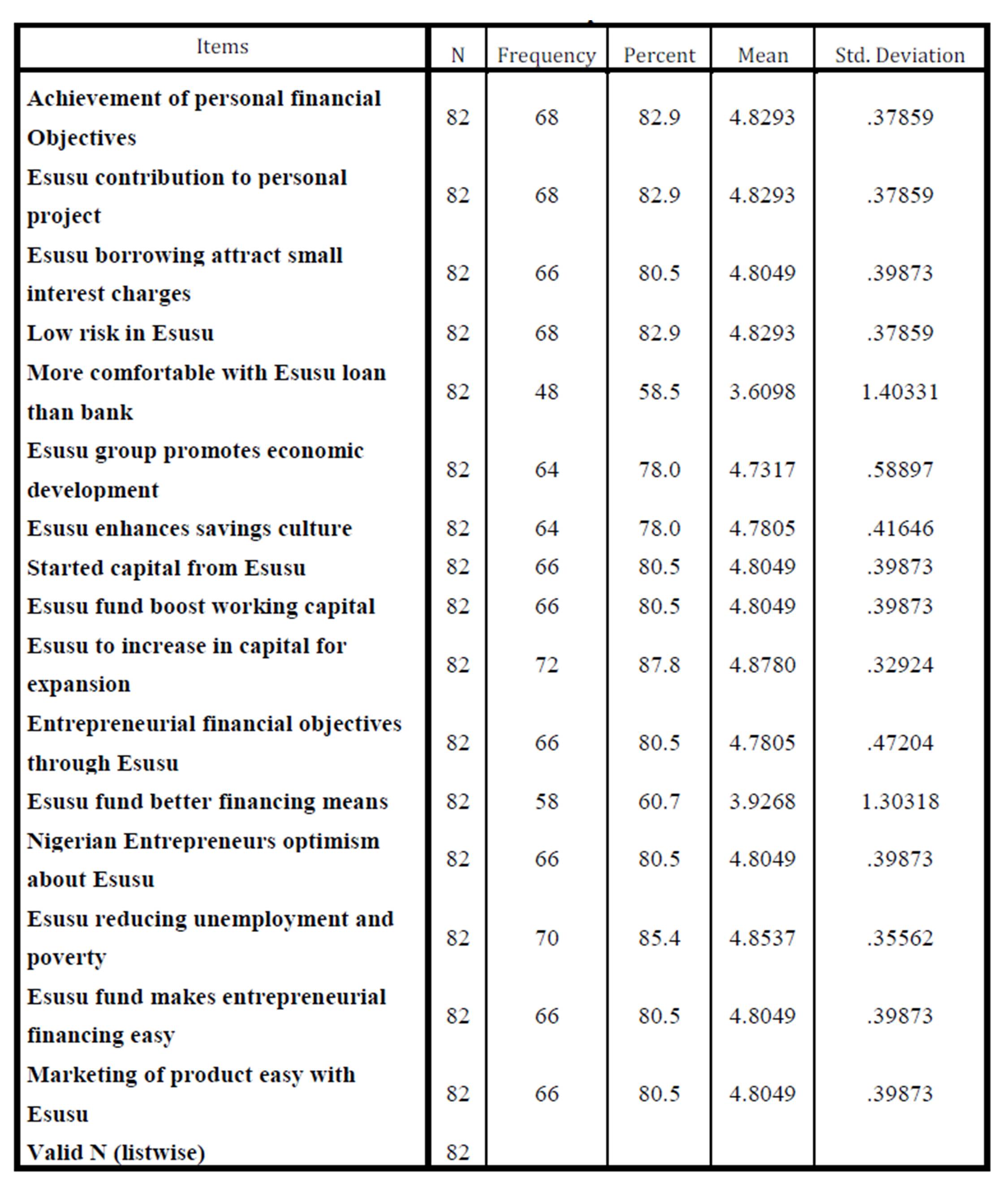

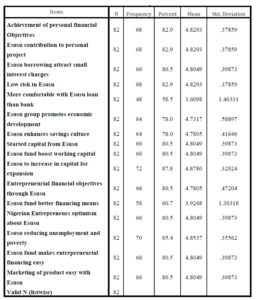

The entrepreneurs under this study were asked questions like whether Esusu scheme has helped them to “achieve personal financial objective”, majority of them 68(82%) were in affirmation with the question. Other questions that rated high point include; if Esusu has helped to increase their capital for business expansion, the impact of Esusu in reducing unemployment and poverty among the beneficiaries, whether Esusu makes entrepreneurial financing and marketing easy. The frequency and percentage of these items scored 72(87.8%), 70(85.5%) and 66(80.5%).

Table 4 : Descriptive Statistics

Source: Field Study (2013)

Data Analysis

To achieve the objective of this study a research hypothesis was formulated and the model of simple regression was employed to test the hypothesis. However, a descriptive analysis on the demographic and nature of the business of the respondents was first conducted before statistical inference is drawn as to ascertain the relationship between the independent and dependent variables.

Hypothesis

H0: Esusu is not an effective strategy for achieving the entrepreneurial objectives of SSEs

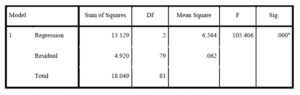

Table 5 :(a) Model Summary

a. Predictors: (Constant), Esusu fund boost woring capital, Started capital from Esusu

Table 5:(b) ANOVAb

b. Dependent Variable: Entrepreneurial objectives through Esusu

Source: Field Study (2013)

In Table 5(a) and (b) above, we observed that the explanatory variable (involvement of SSEs in Esusu scheme for financing entrepreneurial venture) has a significant effect on the achievement of the entrepreneurial objectives. The P-value is significant at 0.000. This means that the research hypothesis (Hi) is statistically significant and the null hypothesis which states that Esusu is not an effective strategy for achieving the entrepreneurial objectives of SSEs is rejected. The result of the analysis of this study implies that the involvement of entrepreneurs in SSEs in Esusu scheme significantly explained only 72.7% of the achievement of their entrepreneurial objective. This means that about 72.7% achievement of their entrepreneurial objectives resulted from their involvement in Esusu scheme. This result shows that R2 (independent variables) of 72.7% is strong in explaining the change in the dependent variable. This reveals that the independent variable (Esusu scheme ) has a positive effect on the dependent variable (achievement of the entrepreneurial objectives) of the SSEs under our study.

Conclusion

This study has examined the role of the indigeniuos contribution scheme known as Esusu in Nigeria in helping Small Scale Enterprises in the achievement of their enterpreneurial objectives. From the result of the analyses conducted, this study concluydes that there is a positive relationship between the Esusu scheme and the achievement of the SSEs entrepreneurial objectives. This shows that Esusu scheme can be used as a medium for financing SSEs towards the economic development of the nation Nigeria.

Recommendations

Based on the results of the analysis, the paper made the following recommendations (i) The Nigerian government should consider the issue of regulating the informal financing system (Esusu scheme) by enacting appropriate legislations, laws, and regulations just like what is obtainable in existing banks such as Agricultural Credit Guarantee Scheme Fund (ACGSF) and Microfinance banks. This will help to control the operation of the Esusu scheme and check mate their activities. (ii) There is need to organize training and workshop programmes for the Esusu scheme operators so as to educate them on different strategies to achieve their entrepreneurial objectives and best practices as regard SSEs. This will help to equip them with the knowledge and skills required for the operation of their business. (iii) The SSEs operators should also be given attention in terms of funds raising and management. This will help to mitigate the obstacles of mismanagement of funds, irregular repayments and loan delinquency by SSEs beneficiaries. (iv) Esusu scheme collectors must be insured to regulate their operations. Here lessons can be learnt from the Credit Union Scheme and Credit Unions Association (CUA) system in Ghana. This will help to weed out fraudulent individuals who may want to defraud the vulnerable, such as the illiterates and less educated members of the scheme. There is need for NGOs and Social Interest groups to be involved in integrating capacity building programmes into the activities of the Esusu scheme. Organizing training and short courses such as entrepreneurial marketing,, people management, book keeping, basic business management and accounting principles should become a pre-requisite for accepting SSEs into the Esusu scheme and other type of rotation credit associations. This will help to improve and build the capacity of both Esusu operators and small scale entrepreneurs.

(adsbygoogle = window.adsbygoogle || []).push({});

References

1. Akanji, O. O. (1994). Towards a viable rural financial market in Nigeria. Bullion, Central

Bank of Nigeria, 18(4): 22 – 38.

2. Akanji, O. O. (1998). Policy issues in informal financial sector development. Bullion, CentralBank of Nigeria, July/September

3. Aluko, S. (1980). The management of the rural economy. Management in Nigeria, Nigerian Institute of Management: 18.

4. Alabi, G., Alabi, J. Akrobo, S. (2007). The Role Of “Susu” A Traditional Informal Banking System In The Development, Of Micro And Small Scale Enterprises (MSEs) In Ghana, International Business & Economics Research Journal – December 2007 Volume 6, Number 12.

5. Alabi, G., Alabi, J. Ahiawodzi, A. (2006). Effects of ““susu”” – A Traditional Micro-Finance Mechanism On Organized And Unorganized Micro And Small Enterprises (Mses) in Ghana, African Journal of Business Management Vol. 1 (8), pp. 201-208, November, Available online at http://www.academicjournals.org/AJBM, ISSN 1993-8233.

6. Adelaja, M.A. (2005), “Women’s empowerment Strategies in Nigeria: How feasible for sustainable development?” A Paper Presented at the Launching of Young Business and Professional Women at Airport Hotel, Ikeja, August, 27.

7. Basu A, Blavy R, and Yulek M, 2004, Microfinance in Africa: Experience and Lessons from IMF – International Monetary Fund

Google Scholar

8. Brunton, D. (1997). Financing small-scale rural manufacturing enterprises. Caribbean Development Bank, (CDB)Barbados, Small-Scale Forest-Based Processing Enterprise, Rome.

9. Chandavarkar, A. G. (1985). The non-institutional financial sector in developing countries:

Macroeconomic implication for savings policies”, Savings and Development, Finafrica Quarterly Review, No. 2.

10. Confederation of Asia Pacific Chamber of Commerce and Industry (1994.) Journal of Commerce and Industry,

Vol. 11.

11. Emmanuel (2012). Entrepreneurship: A Conceptual Approach, Pumark, Lagos.

12. Falegan, S. B. (1987). Redesigning Nigeria’s financial system, University Press Limited,Ibadan.

13. Hoselitz, B.F., 1959 “Small Industry in Developing Countries,” Journal of Economic History, 19. Reprinted in Development Economics and Policy: Readings., I. Livingston, ed., London: Alien and Unwin.

14. Jimoh, B. (2004), “Funding is Very Important to the Survival of Small Business Enterprises” Contribution In How to Improve Access to Finance for Small Firms? Organization: Banking. World Bank, On line Discussion , Hot topics for a Global Community.

15. Kihiko, G. N. (2012). Factors influencing the performance of small-scale businesses in Bungoma municipality-Kenya, http://erepository.uonbi.ac.ke:8080/xmlui/handle/123456789/6970

16. Neumann, W. L. (2002). Social Research Methods, Qualitative and Quantitative Approaches. Pearson Eduation Inc.

17. Ndubusi, F. (2004). Bankers List Financing Alternatives For SSEs, In CBN Seminar On Small and Medium Industries Equity Investments Scheme, Maritime. Nigerian Agriculture/ Micro Enterprise Field Visit – A Summary report designed to assist in implementation of the USAID/Nigeria Transition Strategy SO2

18. Norwood, C. (2005). Macro Promises of Microcredit: A Case of a local eSusu in Rural Ghana, Journal of International Women’s Studies, Vol. 7, Issue 1.

19. Obigbemi, I.F. (2010). The role of competition on the pricing decision of an organisation and the attainment of the organisational objective. Annals of the University of Petroşani, Economics, Vol. 10. No. 1,Pp. 229-248.

Google Scholar

20. Ogunleye, G. A. (2004). “Small and Medium Scale Enterprises as Foundation for Rapid Economic Development in Nigeria” In Small and Medium Enterprises Development and SMIEIS, Effective Implementation Strategies (Ed.), By Ojo A. T. , Maryland Finance Company and Consultancy Service Ltd, Lagos.

21. Ojo, J. A. T., and Adewumi Wole (1982). Banking and finance in Nigeria. Graham Burn.

22. Okafor, C. (2008). “Informal Financing, Micro/Small Enterprises and Achievement of Vision 2020 in Nigeria: Challenges and Opportunities”. Lagos Journal of Banking, Finance and Economic Issues. University of Lagos, Vol. 2, No 1. Pp 162-174.

23. Osuntogun, A., and Adeyemo, R. (1981). Mobilization of rural savings and credit extensions by pre-cooperative organizations in the Southwestern Nigeria. Savings andDevelopment, Finafrica Quarterly Review, No. 4.

Google Scholar

24. Olorunshola, J. A. (2004) “Problems and Prospects of Small and Medium- Scale Industries in Nigeria In CBN Seminar On Small and Medium Industries Equity Investments Scheme, Maritime.

25. Oyekanmi (2004), “Concepts of Equity Financing and Its Implication For SMIEIS”In CBN Seminar On Small and Medium Industries Equity Investments Scheme, Maritime.

26. Oloyede, J. A. (2007). Informal financial sector, savings mobilization and rural development in Nigeria: Further evidence from Ekiti state of Nigeria, African Economic and Business Review Vol. 6 No. 1, Spring 2008.

Google Scholar

27. Seibel, H.D, & U.G. Damachi, (1982): Self-Help Organizations: Guidelines and Case Studies for Development Planners and Field Workers ─ a Participative Approach. Bonn, Friedrich-Ebert-Stiftung.

28. Singleton, R. A, Straits, B. C. and Straits, M. M. (1993). Approaches to Social Research. 2nd Ed. New York: Oxford University Press.

Google Scholar

29. SPSS, Inc. (2003). SPSS 12.0 for Windows. [Statistical Analysis Computer Software] Chicago.

30. Udechukwu, (2003), “Survey of Small and Medium Scale Industries and their Potentials in Nigeria” In CBN Seminar On Small and Medium Industries Equity Investments Scheme, Maritime.

31. World Bank Group (2001), “Microfinance and Small and Medium –Sized Enterprises”, www.worldbank.org/worldbank/microfinance

32. World Bank, 1978a “Employment and Development of Small Enterprises”, Washington, D.C., Sector Policy Paper (February).

Google Scholar

33. World Bank, 1978b “Rural Enterprise and Non-Farm Employment”, Washington, D.C., A World Bank Paper (January).