Introduction

Performance is the major concern of managers who regularly seek the means to compete and differentiate from competitors.

Performance has been the subject of various management studies (Choi et al., 2006) trying to define and delineate the construct. These studies agreed that performance refers to the achievement of firm objectives (earnings, market share, profitability, innovation, etc…) (Drew, 1997) and helps to improve firm cost-value data (Lorino, 1997). Performance looks also as a global construct and is judged on the basis of its time periodicity, hence, it has multiple dimensions (economic, financial, social, societal, human, etc.).

Moreover, performance represents many facts and involves research instrument or measurement indicators that make these facts “measurable”. These facts are from several organizational, but also contextual factors mainly related to firm scope. Firm scope construct outlines the scope of firm activities and its geographical areas. Firm scope implies that all performance dimensions are important, however, this importance degree differs depending on whether the firm is diversified or focused (product scope), international or national (geographical scope) and belonging to a firm group or independent (interaction with other firms scope).

Most studies that have examined the diversification-performance link have focused so much on financial performance and neglected other equally important dimensions of performance, hence we consider similar, both overall and financial performance.

Hence, our research question is: What is manager’s perceived importance of performance dimension’s in firms operating in different product and geographic scopes?

Our aim is to discover which performance dimension to be the primary managers’ concern in diversified product and geographic firms. Consequently, managers will be informed about the right strategic choices leading to achieve firm strategic goals and how to develop a successful diversification.

The article is divided three parts: Literature review (part 1), research design and methodology (part 2) and results and discussion (part 3).

Literature Review

Firm Scope

Firm scope has been the subject of two different, but complementary lines of research (Peng and Delios, 2006), the first one consider performance dimensions; the second deals with performance measurement. Commonly, these two lines of research both kept the separation between the two dimensions. Firm scope refers to the number of economic activities, industries, market segments, product lines in which firm is involved (Jones and Hill, 1988). Firm scope is defined as the number of business activities and its geographic scope. Geographic scope refers to the number of competitive systems in which a firm is involved (Caloriand al., 1994).

According to these firm scope definitions, three dimensions of scope are emphasized: (Calori et al., 1994; Robins and Wiersema, 2003; Peng and Delios, 2006):

- Product scope refers to firm location in one or more markets as strategic choices of diversifying either from one or more resources or skills related to its main activity area (Rumelt, 1974), or from existing skills creating potential value for target markets. We refer to “diversified” firms- as opposed to “focused” firms- and firms whose principal activity is dominant over other elementary or secondary ones (Rumelt, 1977), by wide range of activities.

- Geographical scope is defined as the international operation firm scope (Delios and Beamish, 1999) and limits of firm served markets (regional, national or international) possibly representing opportunities for current or future firm products. In this context, international firms or even firms present in some national and foreign markets illustrate aspects of a broad geographic firm scope while national firms illustrate the narrow geographic scope.

- Scope of firm interaction with business partners or other firms appeal to the firm growth modes and its concentration degrees. Growth is a process that leads to increasing firm size and then to structure transformation (Strategor, 1988). There are three types of growth: horizontal, vertical and conglomerate growth. Horizontalgrowth means the development of activities at the same stage of production; vertical growth is the development of current firm activities using upstream or downstream integration. Finally, conglomerate growth implies the development of other activities (Porter, 1985). Growth can be internal-i.e. firms innovate with their own means and learn from the new trade- or external i.e. firms buy or partner with other competing or complementary firms) (Strategor, 1988). Concentration is the processes by which firms are grouped in one sector and become more powerful, and have an increasingly important market share (Porter, 1985). Firm concentration can be vertical (integration) (firm grouping manufacturing the same product or having upstream or downstream activities) or conglomerate (diversification) (firm grouping manufacturing different products) (Porter, 1985). Both aspects (growth and concentration) suggest a firm to be part of firm group (national or multinational group) as opposed to independent firms.

Business Performance

Organizational performance covers concepts as diverse as the effectiveness, efficiency, productivity, etc.

Performance concept has been defined in several ways: “management performance is the achievement of organizational goals” (Bourguignon, 1995). For Lorino (2003), “… performance is in the firm all that, and only that which contributes to improving the net creation of value”, i.e., better cost-value. Performance is not a mere observation, it is constructed. It is the achievement of something for a given purpose and is the result of a causal process and an indication of potential future results. It must be relative to the competitive and organizational context in which strategy is developed (Lebas, 1995).

Most research discussed and debated performance concept terminology, its analysis level (individual, work unit or organization) and theoretical foundations supporting its evaluation (Ford and Schellenberg, 1982). Hence, literature on performance subject was abundant, however, there’s a small hope of reaching an agreement on its terminology and definitions (Venkatraman and Ramanujam, 1986). Some researchers were frustrated: Kanter and Brinkerhoff (1981) for example, have articulated this pessimism by encouraging academics to urgently focus their attention on more fruitful areas of research.

This has encouraged other researchers to focus on performance measurement option (Steers, 1975). However, some performance measures have been criticized because of their incompleteness and irrelevance. Some researchers have suggested that a critical evaluation of the proposed measurement approaches being made to expand and improve the understanding of the constructs underlying the concept (Cameron and Whetten, 1983b). Venkatraman and Ramanujam (1986) defined three performance fields:

Financial performance is a reduced conception of firm performance (Venkatraman and Ramanujam, 1986). This type of performance is centered on the use of financial indicators reflecting firm economic goals (Venkatraman and Ramanujam, 1986) as well as accounting and stock market measures (Hax and Majluf, 1984). This approach remainders a very financial-oriented one and assumes the prevalence and legitimacy of financial objectives in the firm objective system.

Operational performance is a broader conceptualization of firm performance in addition to financial and operational (non-financial) indicators (market share, new product introduction, product quality, marketing effectiveness, value-added production, etc…) and other measures of technological efficiency (Venkatraman and Ramanujam, 1986). This approach may be advantageous for researchers in bringing them out of “black box” approach, which is characterized by the exclusive use of financial indicators focusing on key success factors leading to financial performance (Venkatraman and Ramanujam, 1986).

Organizational effectiveness is a broader field of firm performance with different nature of strategic objectives (Venkatraman and Ramanujam, 1986) involving multiple stakeholders, and implying the establishment of interdependent relationships between them.

Hoque (2005) defines three performance perspectives (see figure below):

Fig.2: Performance Perspectives (Hoque, 2005)

We will use these perspectives to examine firm scope and performance relationship.

Firm Scope– Performance Link: Research Hypotheses

Firms that are seeking to expand their activity scope offer customers a complete product line corresponding to their implicit and explicit needs. To facilitate resource allocation and access to information sources, firms choose to internalize their transactions (Alchian and Demsetz, 1972), and to separate between strategic and operational control to resolve coordination problems that afflict large firms (Williamson, 1981). In addition, managers in these companies have major concern for costs issue and seek to be competitive (prices, market share, customer loyalty, etc.). They try then to exploit potential synergy between different activities (R& D, distribution system, brand, know-how of production, etc.) (Allaire and Firsirotu, 1993). Accordingly, firms have subsidiaries linked by factors related mainly to customers.

Hence, we note the importance of performance customer dimension for managers of diversified firms that we illustrate through the first hypothesis H1:

H1. Diversified firms or firms with dominant principal activity have superior performance on the customer dimension

The second dimension of firm scope is the geographic one. Large geographic scope (internationalization), allows organizational learning, it also helps to develop knowledge and to be operationally flexible (Garbe and Richter (2009). Consequently, firms with a wide geographic scope (international firms) continuously seek to obtain technology knowledge and physical assets that they can internalize and transform into a source of competitive advantage. The expansion into new geographic markets is a source of firm success since it motivates personnel to exploit or extend businesses to new markets (Caves, 1996). This expansion involves business activity adaptation (including production) to price differentials to exploit other location advantages (Dunning, 1993).

Together, these factors underline the importance of the company’s resources to achieve its objectives, including major contribution of human resources to successful expansion into foreign markets through geographic skills development and firm internal growth modes (improving production processes, increasing distribution channels, developing personnel…). Then, we propose the second hypothesis H2:

H2. International firms and national firms present in some foreign countries have superior performance on the personnel development and growth dimension

A firm may also have a wide range of interactions (multinational or transnational corporations) (Prahalad and Doz, 1987; Bartlett and Ghoshal, 1989) with worldwide operations. In this case, managers, through their interactions with foreign firms, face not only a diversity of markets, but also, a diversity of management practices.

Most often, firms with a wide range of interactions on world scale, choose a matrix structure in which local units are organized according to efficiency production objective and personnel knowledge development through its various geographic markets. These effectiveness and efficiency objectives are pushing managers to seek cheap labor, relocate their manufacturing or outsource their production. Managers constantly seek to exploit economies of scope through tangible and intangible assets (technological innovation, brand reputation, production know-how). They opt sometimes for the internalization of activities which allow, in addition, production rationalization through a large production volume. In addition, firms are extending their relational scope to new countries by expanding opportunities for innovation (Hitt et al., 1997) and reinforcing exploitation of host country technological expertise (Kogut and Chang, 1991).

All these factors explain the importance of factors related to productivity and improving manufacturing processes to benefit from economies of scale and improve production. Hence, performance in these firms follows the perspective of internal processes which is the subject of our third hypothesis H3:

H3. Firms belonging to business groups (national or multinational groups) have superior performance on the firm internal process dimension

Research Design and Methodology

Sample

The sample in this research consists of managers or chief executive officers operating in the Tunisian industrial sector. We constituted our sample using the technique of “snowball” that allowed us to get forty-eight firms distributed among nine industry sectors. Data about firm scope and performance were collected using a questionnaire. We completed data about firm scope from the website of Agence de Promotion de l’Industrie (API) (Tunisian Agency for the Promotion of Industry).

Variable Measurement

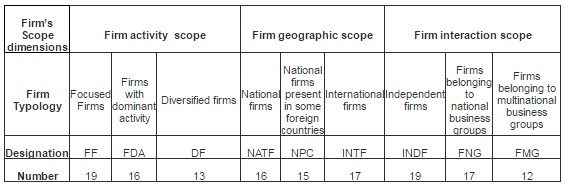

Firm scope was measured using Ward’s hierarchical clustering aggregation method which allowed us to obtain three types of firms:

Table 1: Type of Firms according to their Scope

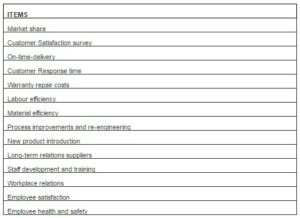

Performance was measured using fourteen items adapted from Hoque (2005). Respondents were asked, on a five-point scale Likert Scale ranging from 1 (declined sharply) to 5 (increased sharply), to indicate their perception of the relative growth of the fourteen items of the competitor’s performance (Table 2).

Table 2: Item Performance

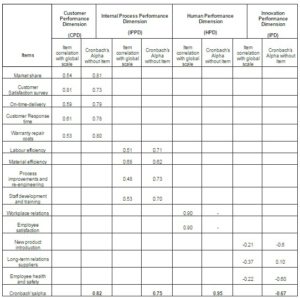

A principal Component Analysis (PCA) with varimax rotation of the forty items yielded four factors with an eigen value greater than 1. They explained 66.07% of the total variance. A reliability check for this measure was produced a Cronbach alpha (Cronbach, 1951) of 0.7, which is considered to be far above the lower limits of normal acceptability (Nunally, 1978). The four factors obtained corresponded to four performance dimensions which are: Customer (CPD), internal processes (IPPD), human resources (HPD) and innovation (IPD) performance dimension. Item correlation with global scale and Cronbach’s Alpha without item for each item performance dimension appear in Table 3.

Tableau 3: Cronbach’s Alphas between the Four Performance Dimension Items

In order to make this analysis simpler, we will not keep innovation performance dimension (IPD) because it showed a very low Cronbach’s alpha (0.43) and had minimal contribution in explaining performance. The table below presents the three dimensions of performance:

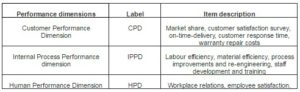

Tableau 4: Item Description of the Three Performance Dimensions

Results and Discussion

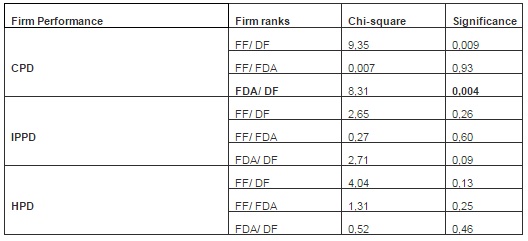

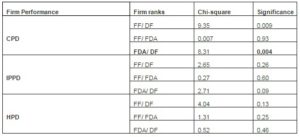

We used non-parametric tests methodto verify our research hypotheses. The results of Chi-square tests on H1 are presented in the table below:

Tableau 5: Activity Scope and Business Performance

The Chi-square tests show that firms with a wide range of activities (DF and FDA) have superior customer dimension performance. Therefore, H1 is confirmed. In fact, because of the diversity of their activities, these firms develop continuously marketing skills to successfully market and sell products. They try to adapt to their customer’s behavior frequently, tastes, preferences, habits, etc.

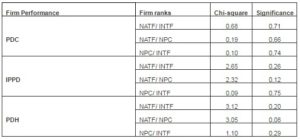

The second hypothesis states that firms with a wide geographical scope are performing on employee learning and growth performance dimension (human dimension). The results of the nonparametric tests are presented below:

Tableau 6: Geographic Scope and Business Performance

The chi-square value obtained (3.05) was not very strong or significant (0.08 close to 0.05). However, it focuses on PDH rather than other dimensions of performance. This confirms conceptually, but not statistically H2 hypothesis. Thus, H2 is invalid. Hence, conceptually, firms with wide geographic scope consider of a great importance to the human resource performance dimension which represents a factor to adjust managerial activities and management practices to different firm’s contexts and consequently allows achieving growth. The key is that this dimension is best suited to their performance strategies.

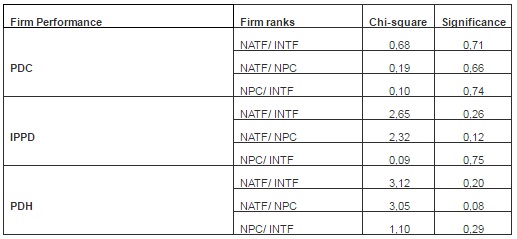

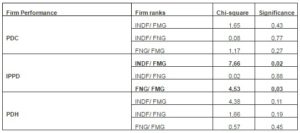

Table 7 presents the results of H3 non-parametric tests:

Table 7: Interaction with Other Firm’s Dimension and Business Performance

The table above shows that internal processes performance dimension is very important in firms with wide geographic scope (FMG and FNG). Thus, H3 is confirmed. In fact, these firms increase production to achieve economies of scale and productivity gains purposes. Consequently, they can resist to international competition and easily access to research, development and innovation.

Conclusion

In this research, we address the issue of manager’s perceived importance of performance dimensions depending on activity and geographic scope. Our aim was to show that managers, although belonging to the same industry sector, do not share the same business performance dimension perceptions in making strategic choices of developing one or more specific performance dimension.

From a methodological point of view, we adopted hypothetical and deductive approach so we confirmed two out of three research hypotheses linking firm scope to business performance. Performance dimensions were adapted from Hoque’s (2005) performance scale and tested on Tunisian industrial firms’ sample.

Research results confirmed our suspicions about manager’s heterogeneous behavior with respect to performance. In fact, we found that diversified firms performed particularly on customer dimension, however, international firms performed successfully (although approximately) on human one and finally, multinational firms have been performing on internal process dimension.

In light of these results, we recommend that firms-depending on their scope extent (activities or geographic)-should focus attention on only profitable areas without neglecting the other ones, instead of dispersing efforts means and resources on several performance areas. These firms must also consider their context characteristics impacting the way to achieve success.

Assuming that performance is a multidimensional concept, one should, therefore, deal with this multidimensionality. Then firms should opt for specialization strategy to achieve performance objectives.

Our research has conceptual, managerial and practical contribution. Conceptually, we discussed thoroughly two important concepts: firm scope and business performance. Using quantitative analysis and adopting hypothetical-deductive approach, we methodologically tested three research hypotheses using various statistical tests and methods. From a managerial and practical point of view, we have shown the importance of going beyond the financial performance framework adopted in most diversification- performance link and treating performance as a multidimensional concept. In doing so, we have specified what performance dimension to consider relating to each type of firm scope.

However, this research has limitations mainly related to firms sample size. Therefore, future research should be drawn from a larger sample which would be interesting and possibly make comparative analyses.

(adsbygoogle = window.adsbygoogle || []).push({});

References

Alchian, A. A. & Demsetz, H. (1972). “Production, Information Costs, and Economic Organization,” American Economic Review, 62, 777-795.

Publisher – Google Scholar

Bartlett, C. A. & Ghoshal, S. (1989). Managing across borders. The Transnational Solution, Boston, Mass: Harvard Business School Press.

Publisher – Google Scholar

Bourguignon, A. (1995). ‘Peut-on Définir la Performance?,’ Revue Française de Comptabilité, 269, 61-66

Google Scholar

Calori, R., Johnson, G. & Sarnin, P. (1994). “CEO’s Cognitive Maps and the Scope of the Organization,” Strategic Management Journal, 15, 437-457.

Publisher – Google Scholar

Cameron, K. S. & Whetten, D. A. (1983b). ‘Some Conclusions about Organizational Effectiveness,’ In K. S. Cameron & D. A. Whetten (Eds.), Organizational Effectiveness; a Comparison of Multiple Methods (pp. 261-277). NY: The Academic Press.

Google Scholar

Caves, R. E. (1996). Multinational Enterprise and Economic Analysis, 2nd edition. Cambridge (United Kingdom). Cambridge University Press.

Publisher – Google Scholar

Choi, B., Poon, S. K. & Davis, J. G. (2006). ‘Effects of Knowledge Management Strategy on Organizational Performance: A Complementary Theory-Based Approach,’ The International Journal of Management Science, 10, 1-17.

Delios, A. & Beamish, P.W. (1999). “Geographic Scope, Product Diversification, and the Corporate Performance of Japanese Firms,” Strategic Management Journal, 20 (8), 711-727.

Publisher – Google Scholar

Drew, S. A. W. (1997). “From Knowledge to Action: The Impact of Benchmarking on Organizational Performance,” Long Range Planning, 30 (3), 427-441.

Publisher – Google Scholar

Dunning, J. H. (1993). ‘Multinational Enterprises and the Global Economy,’ Addison-Wesley, Harlow, Essex.

Ford, J. D. & Schellenberg, D. A. (1982). “Conceptual Issues of Linkage in the Assessment of Organisational Performance,” Academy of Management Review, 7, 49-58.

Publisher – Google Scholar

Garbe, J.- N. & Richter, N. F. (2009). “Causal Analysis of the Internationalization and Performance Relationship Based on Neural Networks-Advocating the Transnational Structure,” Journal of International Management, 15 (4), 413-431.

Publisher – Google Scholar

Hax, A. C. & Majluf, N. S. (1984). Strategic Management: An Integrative Perspective, Englewood Cliffs, NJ Prentice-Hall.

Publisher – Google Scholar

Hitt, M. A., Hoskisson, R. E. & Kim, H. (1997). “International Diversification: Effects on Innovation and Firm Performance in Product-Diversified Firms,” Academy of Management Journal, 40 (4), 767-798.

Publisher – Google Scholar

Hoque, Z. (2005). “Linking Environmental Uncertainty to Non-Financial Performance Measures and Performance: A Research Note,” The British Accounting Review, 37, 471-481.

Publisher – Google Scholar

Jones, G. R. & Hill, C. W. L. (1988). “Transaction Cost Analysis of Strategic- Structure Choice,” Strategic Management Journal, 9,159-172.

Publisher – Google Scholar

Kanter, R. M. & Brinkerhoff, D. (1981). “Organizational Performance: Recent Developments in Measurement,” Annual Review of Sociology, 7, pp. 322-349.

Publisher – Google Scholar

Kogut, B. & Chang, S. J. (1991). “Technological Capabilities and Japanese Foreign Direct Investment in the United States,” Review of Economic and Statistics, 73, 401-413.

Publisher – Google Scholar

Lebas, M. (1995). ‘Oui, il Faut Définir la Performance,’ Revue Française de Comptabilité, 269, 66-72.

Google Scholar

Lorino, P. (1997). ‘Méthodes et Pratiques de la Performance,’ le Guide de Pilotage, Editions d’Organisations.

Google Scholar

Lorino, P. (2003). Méthodes et Pratiques de la Performance. Le Pilotage par les Processus et les Compétences, Editions d’Organisation, 3ème édition.

Publisher – Google Scholar

Peng, M. W. & Delios, A. (2006). “What Determines the Scope of the Firm over Time and around the World? An Asia Pacific Perspective,” Asia Pacific Journal of Management, 23, 385-405.

Publisher – Google Scholar

Porter, M. (1985). ‘Competitive Advantage: Creating and Sustaining Performance,’ New York: Free Press.

Prahalad, C. K. & Doz, Y. L. (1987). The Multinational Mission, Balancing Local Demands and Global Vision, Free Press: New York.

Publisher – Google Scholar

Robins, J. A. & Wiersema, M. F. (2003). “The Measurement of Corporate Portfolio Strategy: Analysis of the Content Validity of Related Diversification Indexes,” Strategic Management Journal, 24, 39-59

Publisher – Google Scholar

Rumelt, R. P. (1974). Strategy, Structure and Economic Performance, Harvard University Press: Boston, USA.

Publisher – Google Scholar

Rumelt, R. P. (1977). ‘Diversity and Profitability,’ Unpublished paper presented at The Annual Meeting of The Western Division, Academy of Management, Sun Valley, Idaho, 1977.

Steers, R. M. (1975). “Problems in the Measurement of Organizational Effectiveness,” Administrative Science Quarterly, 20, 546-558.

Publisher – Google Scholar

Strategor, J. P. (1988). ‘Politique Générale d’Entreprise,’ Ed. INTEREDITIONS.

Google Scholar

Thiétart, R.- A.& Coll. (1999). ‘Méthodes de Recherche en Management,’ Dunod, Paris, 1999, 535p.

Google Scholar

Venkatraman, N. et Ramanujam, V. (1986). “Measurement of Business Performance in Strategy Research: A Comparison of Approaches,” Academy of Management Review, 1(4), 801-814.

Publisher – Google Scholar

Williamson, O. E. (1981). “The Modern Corporation: Origins, Evolution, Attributes,” Journal of Economic Literature, 19, 1537-1568.

Publisher – Google Scholar