Research Institute for Agricultural Economics and Rural Development (I.C.E.A.D.R), Bucharest, Romania

Volume 2022,

Article ID 536123,

Research in Agriculture and Agronomy,

16 pages,

DOI: 10.5171/2022.536123

Received date: 18 October 2021; Accepted date: 3 February 2022; Published date: 5 May 2022

Academic Editor: Adela Sorinela Safta

Cite this Article as:

Ana URSU and Ionut Laurentiu PETRE (2022), “Profitability of Sugar Beet Cultivation, Comparative Analysis between Conventional and Organic Agriculture in Romania”, Research in Agriculture and Agronomy, Vol. 2022 (2022), Article ID 536123,

DOI: 10.5171/2022.536123

Romania’s ecological and environmental diversity offers opportunities for sugar beet cultivation, both in conventional and organic farming systems. The study aims to highlight the economic benefits that farmers can get. The study reveals the comparative techno-economic and financial context of two agricultural systems and two production systems. Profitability indicators for the production year 2020/2021 were examined. The results of the study showed that organically grown non-irrigated sugar beet provided a return of 50.1% of gross profit, compared to 30.3% for conventionally grown sugar beet. In an irrigated system, conventional beet had a profit of 32% of gross profit, compared to 13.1% for organically grown beets. The conventional/organic ratio can only maintain a positive rate of return if the beet is subsidized. The resulting differences are due to different levels of yield and capitalization prices. Organic sugar beet may not be favored by conventional producers due to lower yields, but capitalization prices and financial support for producers to maintain arable land can offset lost revenue. Based on these assumptions, precise rationalizations are provided, which can create decision-making opportunities for producers in the selection and expansion of sugar beet areas and / or their introduction into cultivation.

In Romania, the organically cultivated areas and the areas under conversion must meet all the production conditions established in Council Regulation (EC) no. 834/2007 of 28 June 2007 on organic production and labelling of organic products and repealing Regulation (EEC) No 2092/91, and the detailed implementing rules are laid down in Commission Regulation (EC) No 889/2008 of 5 September 2008 laying down detailed rules for the implementation of Council Regulation (EC) No 834/2007. The area occupied by organic farming is one of the EU’s indicators of sustainable development. Organic farming is a production method that protects the environment, avoiding or reducing the use of synthetic chemicals (fertilizers, pesticides, etc.). The European Green Agreement with the two related strategies From Farm to Consumer and Biodiversity aims, by 2030, to reduce the risk of using chemical fertilizers, and pesticides, reducing nutrient losses, reducing the use of antibiotics, as well as using 10% of the land for biodiversity. Eurostat, (2021).

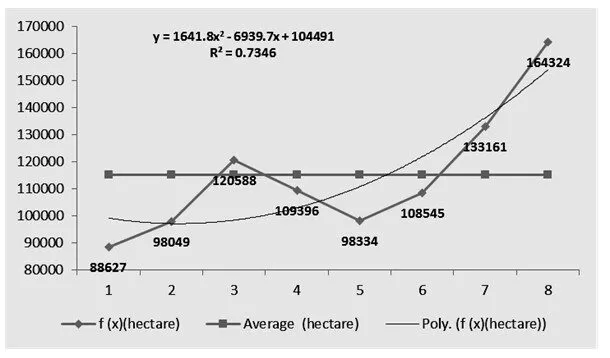

Romania is one of the countries where organic farming is practiced. The area under organic farming, in the period 2012-2019, decreases, on average by 6939.7 hectares / year. The coefficient of determination (R2) shows how much 100% of the variation of one variable (area) is explained by the variation of the other variable (agricultural year). In this context, the independent variable, area, is explained by the agricultural year in a percentage of 73.46%. Figure no. 1. Other factors that contributed to the reduction of the ecological surface in Romania, in a percentage of 26.54%, are those that refer to the low demand on the market for ecological products, due to the reduced purchasing power, etc.

Fig. 1: Romania – Fully converted to organic farming (hectare), 2012-2019

Source: Eurostat (2021), Organic crop area by agricultural production methods and crops,

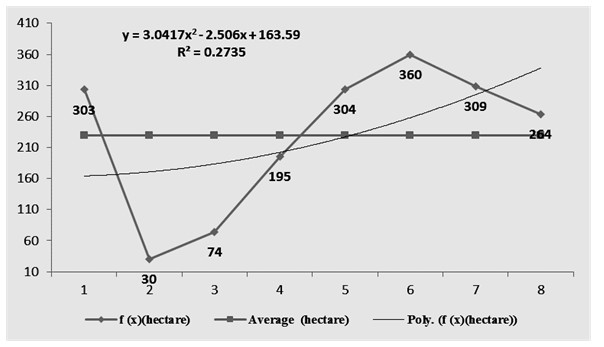

The area of sugar beet, the fully converted to organic farming, represents 0.15% of the fully converted area to organic farming in Romania. Eurostat, (2021). The coefficient of the regression equation shows that, in the period 2012- 2019, the area occupied by organic sugar beets has decreased, on average, by 2.506 hectares / year. Figure no. 2.

The study is conducted for sugar beet cultivation, and the results are determined by the ecological and socio-economic context of the production year 2020-2021. As a result, these results are indicative for sugar beet growers and need to be adapted to the specifics of the geographical area and the type of farm. The aim is to determine the profitability of sugar beet cultivation in organic farming compared to the conventional cropping system, for the agricultural year 2020-2021.

Material and Method

To carry out the study, we will define the aspects that define the technical and economic parameters used to determine the economic profitability of the agricultural product sugar beet obtained in the conventional system and organic farming. The calculations refer to the area of 1 hectare, and the results obtained can be taken as sources of guidance for all types of farms organized in various forms: individual households, family associations or companies. To assess economic profitability, the main indicators are formulated based on assumptions, designed to simplify the evaluation process.

These hypotheses are:

Hypothesis I (H1): The market price for sugar beet is high enough for the revenue obtained to cover the cost of production and to make a profit;

Hypothesis II (H2): The increase in revenue due to direct payments is large enough to cover the cost of production and to make a profit;

Hypothesis III (H3): The increase in revenue due to coupled support is large enough to cover the cost of production and to make a profit.

Hypothesis IV (H4): The increase in revenues, determined by ANT 6, is large enough to cover the cost of production and to make a profit.

Hypothesis V (H5): The increase in revenues, determined by Sub-Measure 11.2, is large enough to cover the cost of production and to make a profit.

The technical framework for the quantification of technological expenditure is called the estimate or technological file in which the activities specific to sugar beet cultivation, activities grouped in mechanized works, manual works and materials and materials are distributed chronologically. Each category is costly. From their sum, there are technological expenses for the unfinished production (unfinished production starts from the release of the land from the previous plant and lasts until December 31 of the current year), as well as expenses for the plan year (expenses made from 1 January of the following year until the sugar beet harvest). Agricultural machinery can be rented (in the case of individual households) or owned by family associations or companies.

The irrigation system is ensured by the existing irrigation arrangements, the system is still based on pumping.

Defining Result Indicators

Gross profit (euro) reflects the absolute size of the return:

Gross profit = Total income – Total expenses

The rate of return on gross profit (%), reflects the relative size of return, is an indicator that measures the degree to which the use of various resources (including income) brings profit:

R (%) = Gross profit / Total expenses *100

The two mentioned quantities are related to each other having a correlative character, as claimed by Cojocaru, C. (2000).

Profit losses are decreases in economic benefits and in this respect do not differ in nature from other types of expenses, as claimed by Zahiu, L., Leonte, J., Stoian, M., Dobre, I., (1999).

Defining the Reference Indicators

Variable expenditure (CV) is directly proportional to the level of production and includes expenditure on materials and supplies, expenditure on mechanized works, irrigation, supply, temporary labor, and those on crop insurance.

Fixed expenses (CF), independent of the level of activity, are incurred for the purpose of normal operation of the farm and include expenses for permanent labor, general and management expenses, credit interest, rent (if the farmer is not the owner of the land) , as well as depreciation for buildings and utilities.

Total expenditure (TC): the sum of fixed and variable expenditure forms the total cost CT=CF+CV, as claimed by Hotea C. R., (2002) and Vintila G., (1999).

The methodology used takes into account the area of sugar beet in organic farming, because the financial assessment takes into account the amount of 218 euro / ha, support provided to farmers through EAFRD (European Agricultural Fund for Rural Development) who have the total land converted, compared with farmers who are in the conversion period and who receive an amount of 293 euro / ha.

Production yields and unit prices provided by the Eurostat statistical database were taken into account in determining yields and capitalization prices on the domestic market. Also, for the estimation of total revenues, the level of subsidies taken into account in determining the indicators from the Revenue and Expenditure Budget (BVC) was the one related to 2019. The lei-euro exchange rate taken into account was 4.7496 lei / euro, established by the European Central Bank on September 30, 2019. The financial support granted to Romanian sugar beet producers consists of: single area payment scheme (SAPS) = 98.7381 euro / ha; redistributive payment (PR) = 5 euros for the first 5 hectares; payment for greening (PI) = 57.8255 euro / ha; transitional national aid (ANT 1 = 13.3202 euro / ha) and (ANT 6 = 73.8219 euro / ha); coupled support (SC) = 829.34 euro / ha; Sub-measure 11.2 – Support for the maintenance of organic farming practices = 218 euro / ha. Total conventional = 1078.0457 euro / hectare; Ecological total = 1296.0457 euro / hectare.

Results and Discussions

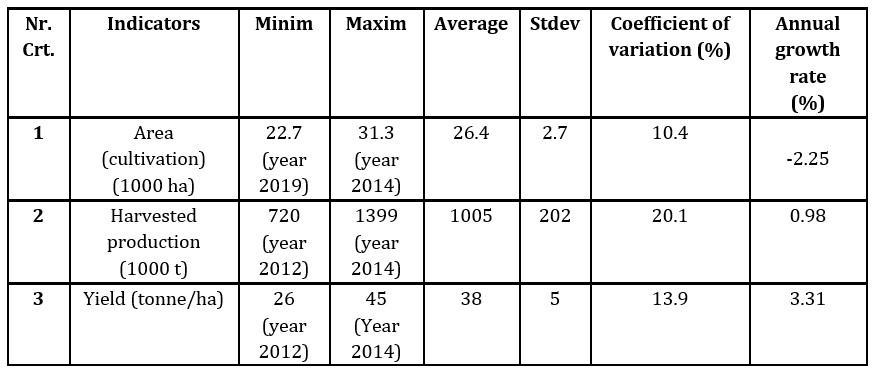

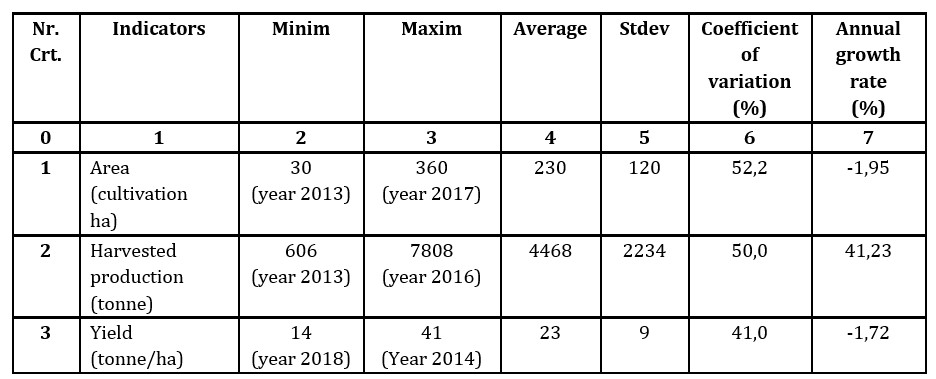

Technical indicators of production from a statistical point of view: to determine the profitability, we will present the technical indicators of production of sugar beet cultivation, conventional and ecological, from the perspective of cultivated areas, total production and yield per hectare. To determine the differences between the technical production indicators for the sugar beet crop, conventionally grown and in organic farming, the following statistical indicators were determined: minimum, maximum, average, standard deviation, coefficient of variation (CV%) and rate annual growth in terms of cultivated area, total production and yield per hectare. The analysis of the mentioned statistical indicators was performed based on EUROSTAT statistical data, for the period 2012-2020.

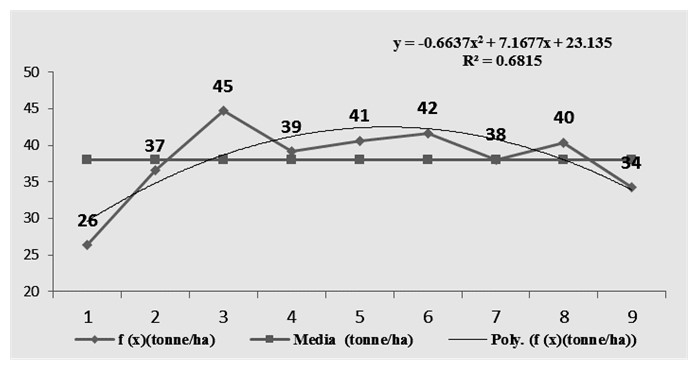

The values of the coefficient of variability, calculated as the ratio between the standard and average deviation for sugar beet in the conventional system, define the threshold for the samples cultivated area (10.4%), total production (20.1%) and yield per hectare (13, 9%), their values being below the threshold of 20% which means that the dispersion of data around the averages is relatively homogeneous, and the sample is statistically representative. Regarding the annual growth rate, it is negative, revealing reductions of the cultivated area, on average, by 2.25% / year. Table no. 1.

Table 1: Sugar beet variability in the conventional system 2012-2020

Source: Eurostat (2021), Crop production in national humidity [apro_cpnh1], CROPS, Sugar beet (excluding seed), STRUCPRO Area (cultivation/harvested/production)/Harvested production (1000 t) (1000 ha)/Yield (tonne/ha), https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=apro_cpnh1&lang=en (extracted on 14/10/2021); Authors’ own calculations.

Regarding the production yield per hectare, for conventional beet, the coefficient of the regression equation shows an average increase of 7.1677 tons / ha / year. Figure no.3.

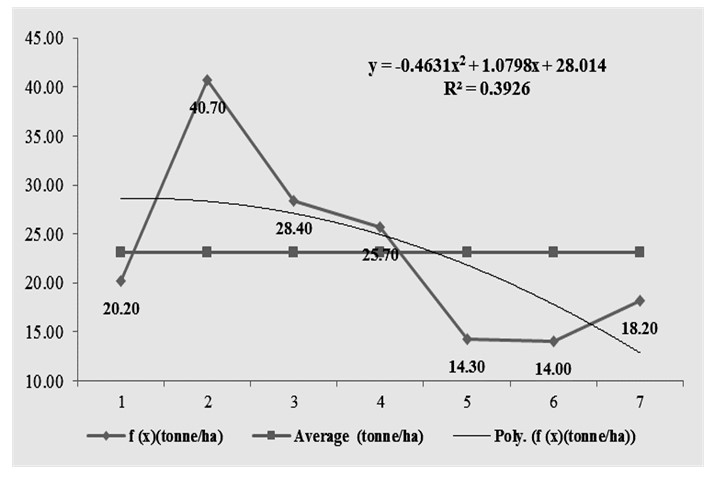

The coefficient of variability, for sugar beet in organic farming, defines the threshold for the samples of the three indicators as heterogeneous (CV> 35%), their values being above the threshold of 35%, which means that the dispersion of data around the averages is heterogeneous, and the sample is not statistically representative. Table no. 2.

Table 2: Sugar beet variability in organic farming 2012-2019

Source:Eurostat (2021): Organic crop area by agricultural production methods and crops [org_cropar] and Organic crop production by crops [org_croppro] https://appsso.eurostat.ec.europa.eu/nui/setupDownloads.do (extracted on 08.10.2021); Authors’ own calculations

The annual growth rate registers negative values, both for the area in organic farming (-1.95% / year) and for the production yield in organic farming (-1.72% / year).

Fig. 4: Sugar beet – Organic crop production by crops (tonne/ha)

Source: Eurostat (2021), Organic crop production by crops [org_croppro], Sugar beet (excluding seed), https://appsso.eurostat.ec.europa.eu/nui/show.do (extracted on 15/10/2021); Authors’ own calculations

Regarding the yield per hectare, for organic beets, the coefficient of the regression equation shows an average increase of 1.0798 tons / ha / year. Figure no. 4.

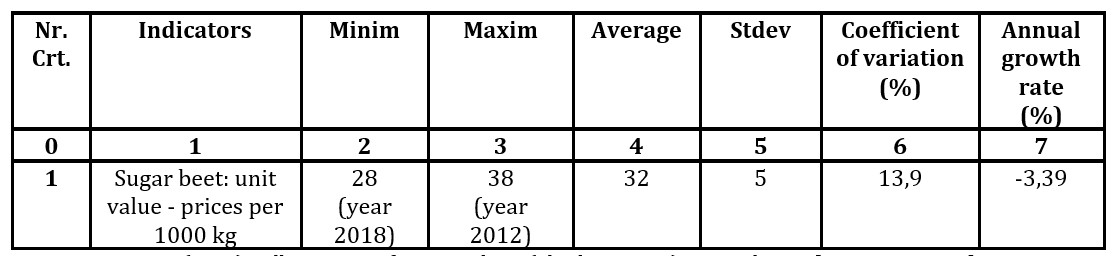

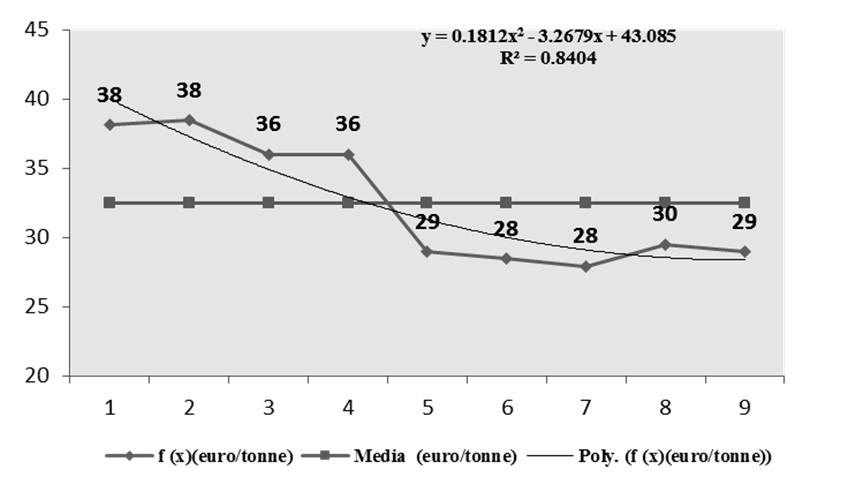

Unit value statistics – the market price for conventional sugar beet cultivation

The values of the coefficient of variability, calculated as the ratio between the standard deviation and the average, for sugar beet in the conventional system, define the threshold for the unit price sample (13.9%); its value is below the threshold of 20% which means that the dispersion data around the averages is relatively homogeneous, and the sample is statistically representative. Regarding the annual growth rate, it is negative, revealing price reductions, on average, by 3.39% / year. Table no.3.

The unit price for sugar beet decreased between 2012 and 2020, on average by 3.2679 euro / ton / year. The coefficient of determination (R2) shows how much 100% of the variation of one variable (price) is explained by the variation of the other variable (year of production). In the present context, the independent variable, the capitalization price, is explained by the agricultural year in a percentage of 84.04%. Other factors that contributed to the formation of prices, in percentage of 15.96%, are those that refer to the levels of prices and tariffs existing on the market, as well as to the situation of supply and demand of sugar beet, etc.

The market price, determined for the production year 2020-2020, was 32 euro / tonne, for conventional beet and 43 euro / ha for organic beet.

Fig. 5: Sugar beet: unit value – prices per 1000 kg (euro) – 2012-2020

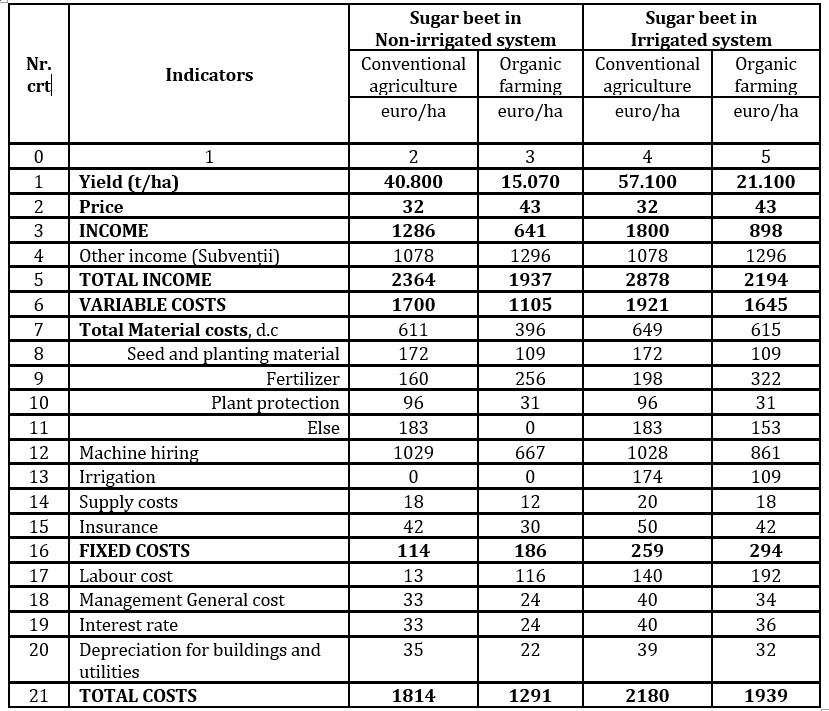

Sugar beet – non-irrigated system: for sugar beet in the conventional system was established an average production of 40.8 t / ha, while in organic farming, the determined yield was 63% lower. To obtain these productions, it is necessary to spend 1653 euro / ha on the cultivation of beet grown (non-irrigated) in a conventional system, while for organic sugar beet, it is about 29% lower. Expenditures on mechanized works have a share of 62% in total technological works, 35% higher than organic sugar beet. Manual labor costs account for 0.8% in conventional and 10% in organic farming, with manual labor spending being about 8 times higher on sugar beet (non-irrigated) in organic farming. Expenditure on materials and materials has a share, out of total technological expenditure, of 37% in the conventional system and 34% in organic farming, the effort on expenditure on consumption of materials and materials being 35% higher in conventional agriculture. Table no. 4.

Table 4: Distribution of technological costs for sugar beet – non-irrigated system, 2020-2021

Source: Authors’ own calculations; Project ADER 23.1.1.

Sugar beet – irrigated system: for sugar beet grown under irrigated agrotechnics, in the conventional system, was established an average production of 57.1 t / ha, while in organic farming, the determined yield was 63% higher little bit. To obtain these productions, expenses in the amount of 1992 euro / ha are necessary, for the cultivation of beet irrigated in conventional system, while for the cultivation of beet irrigated in organic agriculture, they are approximately 11% lower. Expenditures on mechanized works have a share, in total technological expenditures, of 52% for beets grown in conventional agriculture and 48% for beets grown in organic farming. The expenses with manual works occupy a weight in the total technological expenses of 7%, for the irrigated beet in conventional system and of 11% in the ecological agriculture; the effort regarding this category of expenses being 37% higher for the culture of beet irrigated in ecological system. Expenditures on materials have a share of total technological expenditures, of 41% in both cropping systems; the effort on expenditures on consumption of materials being 12% higher for the cultivation of beet irrigated in a conventional system. Table no. 5.

Table 5: Distribution of technological costs for sugar beet – irrigated system, 2020-2021

Source: Authors’ own calculations; Project ADER 23.1.1.

Indicators – production costs per hectare

Sugar beet production costs in non-irrigated system

Total costs: for non-irrigated sugar beet, in conventional agriculture, are necessary costs of 1814 euro / ha, 29% more than sugar beet grown in organic farming, because the production is higher.

Variable costs are 35% higher than organic sugar beet, and fixed costs are 63% lower, because the effort on labor consumption is higher for sugar beet grown in organic farming. Table no. 6, col. 2 et al 3

Production costs for sugar beet in irrigated system

Total costs: for sugar beet grown under irrigated agrotechnics, in conventional agriculture, are necessary costs of 2180 euro / ha, 11% more than sugar beet grown in organic farming.

Variable costs are 14% higher than organic sugar beet, and fixed costs are 14% lower, as the effort on labor consumption is higher for sugar beet grown in organic farming. Table no. 6, col. 4 et seq. 5

Table 6: Indicators – production costs / ha

Source: Authors’ own calculations; Project ADER 23.1.1

In order to determine the profitability of the sugar beet product, cultivated in a conventional system and in organic farming, profit indicators were calculated, based on the formulated assumptions, both in absolute and relative values.

Determination of result indicators for sugar beet cultivation in non-irrigated system

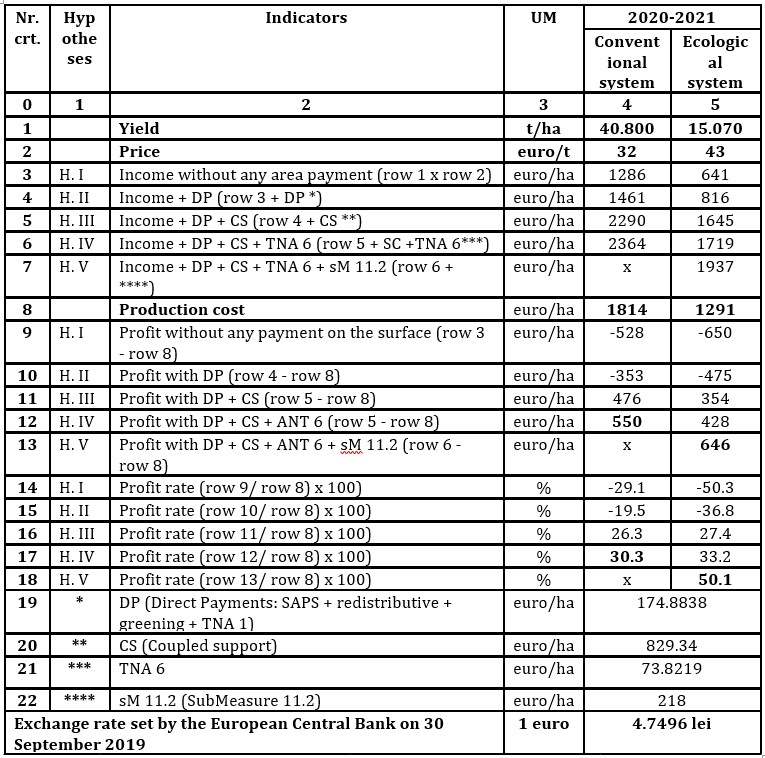

Table 7 : Indicators of profitability for sugar beet – non-irrigated system- 2020/2021

Source: Authors’ own calculations; Project ADER 23.1.1

H 1. The market price for sugar beet is high enough for the revenue obtained to cover the cost of production and to make a profit. By deducting the total costs from the value of production, there is a loss of 528 euro / ha, for sugar beet grown in conventional system and 650 euro for sugar beet grown in organic farming; the loss rate being 29.1% for conventional beet and 50.3% for organic sugar beet. Table no. 7, row 9 – col. 4 and col.

H1. – The hypothesis is not confirmed.

H 2. The increase in revenue due to direct payments is large enough to cover the cost of production and make a profit.

Direct payments (in the amount of 174.8838 euro / ha) contribute to the income by 7.4%, to conventional sugar beet and by 9.0% to organic sugar beet, but do not ensure the profitability of sugar beet cultivation. The profit obtained represents a loss of 353 euro / ha, for conventional sugar beet and 475 euro for organic sugar beet; the profit loss rate being 19.5% for conventional sugar beet and 36.8% for beet organic sugar. Table no. 7, row 10 – column 4 and column 5.

H2. – The hypothesis is not confirmed.

H3.The increase in revenue due to coupled support is large enough to cover the cost of production and make a profit

The coupled support (in the amount of 829.34 euro / ha) contributes to the achievement of revenues by 35.1%, for conventional sugar beet, and by 42.8% for organic sugar beet, ensuring the profitability of sugar beet cultivation. The profit obtained is 476 euro / ha for conventional sugar beet and 354 euro / ha for organic sugar beet. The profit rate is 26.3% for conventional sugar beet and 27.4% for organic sugar beet. Table no. 7, row 11 – col. 4 and col 5. H3. – The hypothesis is confirmed.

H4.The increase in revenues, determined by TNA 6, is large enough to cover the cost of production and make a profit.

Transitional National Aid (TNA) 6 (amounting to EUR 73.8219 / ha) contributes to the revenue of 3.1% for conventional sugar beet and 3.8% for organic sugar beet, ensuring the profitability of sugar beet. The profit obtained is 550 euro / ha for conventional beet and 428 euro / ha for organic sugar beet, the profit rate being 30.3% for conventional sugar beet and 33.2% for organic sugar beet. Table no. 7, row 12 – col 4 and col 5.

H4. – The hypothesis is confirmed.

H5.The increase in revenues, determined by Sub-Measure 11.2, is large enough to cover the cost of production and make a profit. Sub-measure 11.2 (in the amount of 218 euro / ha) contributes to the achievement of revenues by 11.3%, ensuring the profitability of organic sugar beet cultivation. The profit obtained is 646 euro / ha, and the profit rate is 50.1%. Table no. 7 rd. 13 – col 4 and col 5.

H5.– The hypothesis is confirmed.

Determination of result indicators for sugar beet cultivation in irrigated system

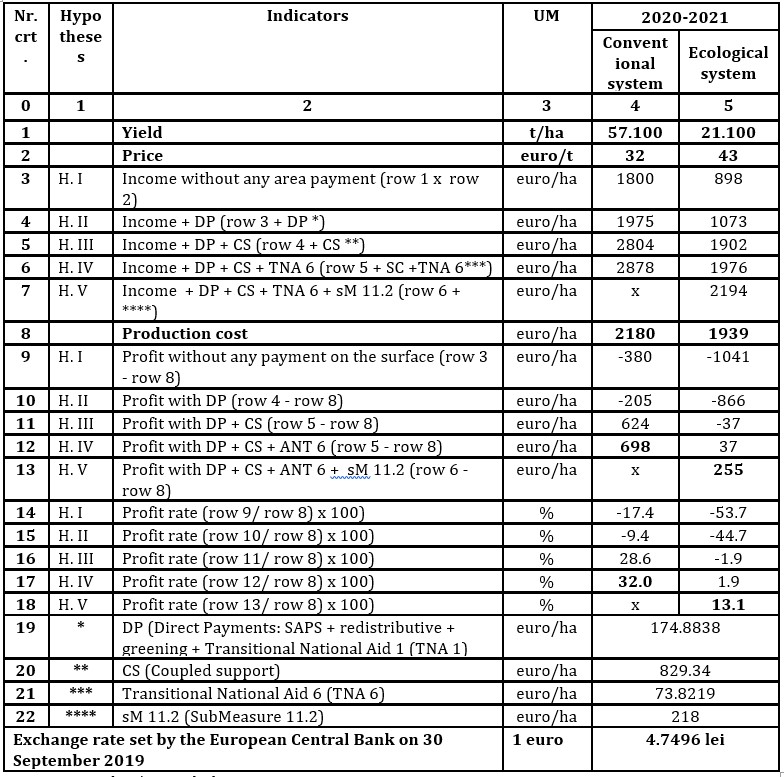

H1. The market price for sugar beet is high enough for the revenue obtained to cover the cost of production and to make a profit. By deducting the total costs from the value of production, there is a loss of 380 euro / ha, for sugar beet grown in conventional system and 1041 euro / ha for sugar beet grown in organic farming. The loss rate being 17.4% for conventional beets and 53.7% for organic beets. Table no. 8, row 9 – col 4 and col 5.

H1.– The hypothesis is not confirmed.

H2.The increase in revenue due to direct payments is large enough to cover the cost of production and make a profit.

Direct payments (amounting to 174.8838 euro / ha) contribute to the revenue of 6.1% for conventional sugar beet and 8.0% for organic sugar beet, but do not ensure the profitability of sugar beet cultivation. The profit obtained represents a loss of 205 euro / ha, for conventional sugar beet and 866 euro / ha for organic sugar beet. The profit loss rate being 9.4% for conventional sugar beet and 44.7% for organic sugar beet.

H2. – The hypothesis is not confirmed.

Table 8 : Indicators of profitability for sugar beet– irrigated system- 2020/2021

Source: Authors’ own calculations; Proiect ADER 23.1.1

H3.The increase in revenue due to coupled support is large enough to cover the cost of production and make a profit.

The coupled support (in the amount of 829.34 euro / ha) contributes to the achievement of revenues by 28.8% for conventional sugar beet and by 37.8% for organic sugar beet, ensuring the profitability of the crop only for conventional sugar beet. The profit obtained is 624 euro / ha for conventional sugar beet and a loss of 37 euro / ha for organic sugar beet. The profit rate is 28.6% for conventional sugar beet and -1.9% for organic sugar beet. Table no. 8, row 11 – col 4 and col 5.

H3. – Partially confirmed hypothesis – to conventional sugar beet.

H4.The increase in revenues, determined by ANT 6, is large enough to cover the cost of production and make a profit.

Transitional National Aid (NTA) 6 (in the amount of 73.8219 euro / ha) contributes to the revenue of 2.6% for conventional sugar beet and 3.4% for organic sugar beet, ensuring profitability for sugar beet. The profit obtained from conventional sugar beet is 698 euro / ha, and the rate of return is 32%. The profit obtained from organic sugar beet is 37 euro / ha, and the rate of return is 1.9%. Table no. 8, row 12 – col 4 and col 5.

H4. – The hypothesis is confirmed.

H5.The increase in revenues, determined by Sub-Measure 11.2, is large enough to cover the cost of production and make a profit.

Sub-measure 11.2 (in the amount of 218 euro / ha) contributes to the achievement of revenues by 9.9%, ensuring the profitability of organic sugar beet cultivation. The profit obtained is 255 euro / ha, and the profit rate is 13.1%. Table no. 8 rd. 13 – col 4 and col 5.

H5. – The hypothesis is confirmed.

Conclusions

The study on the profitability of sugar beet cultivation in conventional and organic agriculture showed that the most favorable economic and financial results are obtained for sugar beet grown in non-irrigated organic farming, by confirming hypotheses III, IV and V. Gross profit obtained is 646 euro / ha, ensuring a rate of return of 50.1%. Production yield is 63% lower than sugar beet grown in conventional agriculture; production costs are 28.8% lower than conventional sugar beet; and the market price is 34.4% higher than the price charged in conventional agriculture. Profit losses, confirmed by hypotheses I and II, certify that this crop must be supported in the future, and that agricultural policies must find solutions to increase financial support for beet growers, especially organic farmers.

In the case of sugar beet grown under irrigated agrotechnical conditions, profitability is ensured by conventional sugar beet. The profit obtained is 698 euro / ha, ensuring a rate of return of 32%. Profit losses are confirmed by hypotheses I and II, and profitability by hypotheses III and IV. Irrigated sugar beet is a crop with high production costs in both farming systems. It is one of the reasons why sugar beet is no longer in the preferences of growers.

We mention that the study has its limits, in the sense that the presented estimates are related to the production year 2020-2021, but the research on the approached topic enters our current concerns and we will continue them.

Acknowledgment

We thank the Ministry of Agriculture and Rural Development for the financial support provided for the publication of the paper. The study is part of the research conducted in phase no. 2/2020/2021 of the ADER project 23.1.1, entitled “Technical-economic substantiation of production costs and estimates regarding the capitalization prices of the main plant and animal products, obtained in conventional system and in organic agriculture”. The project is funded by the Ministry of Agriculture and Rural Development and is coordinated by the Research Institute for Agricultural Economics and Rural Development, Bucharest. The authors are part of the project research team.

References

Academy of Agricultural and Forestry Sciences „Gheorghe Ionescu Șișești”, Paper “Tariffs for contract work, related to agricultural, horticultural and zootechnical works, provided by the staff of the research-development units within ASAS”, for the year 2019-2020.

ADER Project, number code 23.1.1, Year of start: 2019 Year of completion: 2022, Duration: 36 months. „The technical-economic substantiation of the production costs and estimates regarding the capitalization prices of the main vegetal and animal products, obtained in conventional system and in ecological agriculture”, Research Institute for Agricultural Economics and Rural Sustainability A.S.A.S. Bucharest. Retrieved from https://www.madr.ro/attachments/article/335/ADER-2311-faza-2.pdf, http://www.iceadr.ro/proiecte.

Area under organic farming (sdg_02_40), Explanatory texts, Eurostat (2021), Metadata Relevance, the statistical office of the European Union, (ORG_CROPAR, ORG_CROPAR_H2). Retrieved from https://ec.europa.eu/eurostat/cache/metadata/en/sdg_02_40_esmsip2.htm

C. (2000). Economic-financial analysis of agricultural and forestry holdings, Economic Publishing House, Bucharest.

Emergency Ordinance no. 3 of March 18, 2015 for the approval of the payment schemes that are applied in agriculture in the period 2015-2020 and for the modification of art. 2 of Law no. 36/1991 on agricultural companies and other forms of association in agriculture. Retrieved from http://legislatie.just.ro/Public/DetaliiDocument/166545

FAO – Food and Agriculture Organization of the United Nations (2000) – Economic and Financial Comparison Organic and Conventional Citrus – growing Systems, Study prepared for FAO by Juan Fco. Julia Igual, Ricardo J. Server Izquierdo, Departament of Economics and Social Sciences, University of Valencia. Retrieved from https://www.fao.org/3/Y2746E/Y2746E00.htm

Georgeta Waqas Aslam, Chen Hong, (2018). Comparative Profitability Analysis of Conventional and Organic Vegetable Farming in Khyber Pakhtunkhwa and Azad Jammu Kahsmir, Pakistan, Journal of Economics and Sustainable Development iiste.org, ISSN 2222-1700 (Paper) ISSN 2222-2855 (Online) Vol.9, No.8.

Government Decision no. 1174/2014 on the establishment of a state aid scheme for the reduction of excise duty on diesel used in agriculture, with subsequent amendments and completions; Retrieved from http://legislatie.just.ro/Public/DetaliiDocument/164301

Hotea C. R., (2002). Profitability analysis in family farms, Publishing House of the Academic Foundation for Rural Progress Terra Noastra, Iași.

MARD, (2015). Ministry of Agriculture and Rural Development – “Order no. 619/2015 for the approval of the eligibility criteria, the specific conditions and the manner of implementation of the payment schemes provided in art. 1 para. (2) and (3) of the Government Emergency Ordinance no. 3/2015 for the approval of the payment schemes that are applied in agriculture in the period 2015-2020 and for the amendment of art. 2 of Law no. 36/1991 on agricultural companies and other forms of association in agriculture, as well as the specific implementation conditions for the compensatory rural development measures applicable on agricultural lands, provided in the National Rural Development Program 2014-2020”, Retrieved from http://legislatie.just.ro/Public/DetaliiDocument/184794.

Ministry of Agriculture and Food Industry, (1985) – General Economic Directorate for Agricultural Mechanization, Norms for production and consumption of diesel – Mechanism Remuneration Rates, I.P. Publishing House Information C. 109.

National Rural Development Plan (NRDP), 2014-2020, Measure 11 – Organic farming, Sub-measure 11.1- Support for conversion to organic farming practices and methods Measure 11 – Organic farming, Sub-measure 11.1- Support for conversion to organic farming practices and methods, Retrieved from https://www.pndr.ro/implementare-pndr-2014-2020/pndr-2014-2020-versiune-aprobata.html.

Organic crop area by agricultural production methods and crops (from 2012 onwards) [org_cropar], Eurostat, (2021). Retrieved from https://ec.europa.eu/eurostat/data/database.

Regulation (EU) 2018/848 of the European Parliament and of the Council of 30 May 2018 on organic production and labelling of organic products and repealing Council Regulation (EC) No 834/2007. Retrieved from https://eur-lex.europa.eu/eli/reg/2018/848/oj.

Ursu, A., Petre, I., (2021). Practical technical-economic guide for vegetable agricultural products obtained in conventional system and in organic farming, Year of production 2020-2021, Economic Publishing House, Bucharest, ISBN 978-973-709-974-7, 41 – 42.

Ursu, A., Surca, E., Petre, I., (2018). Practical technical-economic guide for conventional agriculture and ecological agriculture, Economic Publishing House, Bucharest, ISBN 978-973-709-856-6.

Ursu, A. and coll. (2008). The farmer’s notebook for vegetable production, Publishing House, Bucharest.

Vintilă , (1999). Financial management of the enterprise, Second edition, Didactic and Pedagogical Publishing House, Bucharest.

Zahiu, L., Leonte, J., Stoian, M., Dobre, I., (1999). Agricultural management – Book of practical works and case studies, Romania of Tomorrow Foundation Publishing House, Bucharest.