Ika Iryanti, Wisnu Mawardi, Harjum Muharam and Sugeng Wahyudi

Universitas Diponegoro, Erlangga Tengah , Semarang, Central Java, Indonesia

Volume 2022,

Article ID 530892,

IBIMA Business Review,

10 pages,

DOI: 10.5171/2023.530892

Received date: 8 September 2022; Accepted date: 29 December 2022; Published date: 10 January 2023

Academic Editor: Wan Norhayati Mohamed

Cite this Article as:

Ika Iryanti, Wisnu Mawardi, Harjum Muharam and Sugeng Wahyudi (2023)," Gender Diversity of Board and Debt: Firm size moderating Role (Evidence from Indonesia)", IBIMA Business Review, Vol. 2023 (2023), Article ID 530892, DOI: 10.5171/2023.530892

This research verifies the relationships between gender diversity in the boardroom, firm size, and debt. The research was conducted based on panel data from non-financial enterprise listed on the Indonesia Stock Exchange for the 2015-2020 period. Our study results propose that board gender diversity has a negative impact on capital structure. However, the relation between gender diversity on board and the size of a firm is significantly positive for capital structure. This paper is different from prior studies in that it uses a contingency theory to research the connection between gender diversity in the boardroom and debt. The current paper’s result sheds light on the reference in the emerging market.

Keywords: Emerging market, Gender diversity of the board, Firm size, Debt

Introduction

In the world, the female workforce is approximately 49 percent. In Indonesia, the female workforce rate rises over time (Klasen et al., 2020). Yet, there are under-presentation females on company boards in emerging and advanced countries (Darmadi, 2013). This phenomenon is called the “glass ceiling” (Bertrand et al., 2018).

The firm faces decisions that impact financing and investment policies (Rossi et al., 2017). The board of directors’ role monitors opportunistic managerial behavior (Fama & Jensen, 1983; Jensen & Meckling, 1976). Gender diversity supports decision-making because of preference viewpoints (Zahra & Pearce, 1989). Women directors have perspectives and skills of problem-solving that are diverse from men (Tanaka, 2014). The controversy as to whether board gender diversity influences debt. At the same time, several studies propose that board gender diversity positively correlates with debt (e.g., Rossi et al., 2017; Mehedi et al., 2020). Several other studies show a negative connection (e.g., Huang & Kisgen, 2013; Briozzo, 2019; Faccio et al., 2016; Adusei, 2018; Elmagrhi et al., 2018).

Contingency theory states that the effect characteristics of the board may be limited or amplified relying on the contexts of the organization (Boyd et al., 2011). Van Knippenberg et al. (2004) suggested moderating variables to examine the impact of diversity on the firm decision. Contingency variables of firm size influence decision-making (Hannan & Freeman, 1984).

Literature review and hypothesis development

Gender diversity of board and leverage

Derived from agency theory, separating a firm’s control and ownership increases conflicts of interest (Berle & Means, 1932). Agency theory states board’s role is to control and monitor managers (Fama & Jensen, 1983; Jensen & Meckling, 1976). The board serves as monitoring to preserve the behalf of shareholders and managers (Hillman & Dalziel, 2003). Diversity of the board increases transparent information, therefore supporting corporate governance (Upadhyay & Zeng, 2014).

Board gender diversity can be a mechanism to minimize agency costs (Hillman and Dalziel 2003). Gender diversity in the boardroom enhances monitoring functions (Adams & Ferreira, 2009). Board diversity generates more independence of the board, increases effective problem-solving, and diversity of perspectives to assess more preferences and more conscientiously investigate the consequences of this preference (Carter et al., 2003). In turn, board gender diversity exacerbates decision-making from more alternative angles (Zahra & Pearce, 1989). From the decision-making perspective, different groups should perform better than homogeneous groups. Diverse groups have broader distance skills, knowledge, and opinion (Van Knippenberg et al., 2004).

The resource dependence theory by Hillman & Dalziel (2003) states that the board provides (1) counsel and advice, (2) a link between the company and outboard firms, (3) legitimacy, and (4) a preferable link to support from necessary factors outside the company. Pfeffer and Salancik (1978) stated that resources minimize dependency among the firm and outboard contingencies and alleviate unpredictability for a company (Pfeffer, 1972). Board provision of resources embraces a particular activity, for instance, providing the enterprise’s legitimacy (Selznick, 1949), ease of obtaining funds (Mizruchi & Stearns, 1988). Board’s ability to bring resources to the enterprise becomes a weakness or strength of the firm (Wernerfelt, 1984: 172). Diversity in the boardroom increases networks, communication channels, and corporate links (Kilic, 2015). The presence of females in the boardroom increases obtaining the enterprise debt (Reguera-Alvarado et al., 2017).

Trade-Off theory with tax states debt increase enterprise value (Modigliani & Miller, 1963). Debt benefit is a tax shield (Miller, 1977). Debt cost is the cost of financial distress (Kraus & Litzenberger, 1973). Gender diversity on board minimizes debt costs by alleviating agency conflict among managers and lenders (Pandey et al., 2019).

Free cash flow theory proposes that enterprise cash flow in excess increases conflicts of interest among agents and shareholders (Jensen, 1986). A manager could participate in an inefficient project (Jensen and Meckling, 1976). Debt as managers incentivize to minimize abuse of resources and create preferable investment decisions (Elmaghri et al, 2018).

The presence of women directors increases attendance at the meetings of the board (Adams and Ferreira, 2009). Because of its advising capability, effective monitoring role, and strategic orientation from the board with gender diversity minimize default risk. In turn, creditors charge less for a firm’s debt (Usman et al., 2019). Consequently, a firm with board gender diversity tends to increase debt (Rossi, 2018). Board gender diversity is an accelerated factor in getting more debt (Zaid et al., 2020).

H1: Gender diversity on board increases the enterprise debt level.

Firm size moderating role

Prior research on the effect of gender diversity in the boardroom and leverage has generated mixed results.

Contingency theory proposes that the size of an enterprise is the contingency organizational factor. Firm size is a moderating variable that facilitates or constrains a company’s decision-making (Zona et al., 2013; Child, 1975). The influence of board gender diversity on enterprise decision-making is connected with enterprise size (Nahavandi et al., 1993). A larger company has a broader distribution of power and decentralized structure, which minimizes the influence of gender diversity of the board on enterprise decision-making. Small firms have more leveraged than larger firms because it is more expensive to issue new equity and less asymmetric information (Smith, 1977; Rajan et al., 1995).

It is plausible to assume that the firm size moderates the influence of gender diversity on the boardroom and debt.

H2: The impact of gender diversity on the board on debt is moderated by firm size

Research Methods

Sample and data collection

This paper’s population consists of non-financial enterprises listed on the Indonesia Stock Exchange. Secondary data were acquired from a company’s yearly report period 2015 to 2020.

Companies have to fulfill the following criteria to be entered into the ending sample:

– annual reports of companies are provided for the entire sample period;

– companies’ annual reports can be accessed for the entire sample period;

– companies have to be persistently listed on the Indonesia Stock Exchange period 2015 to 2020.

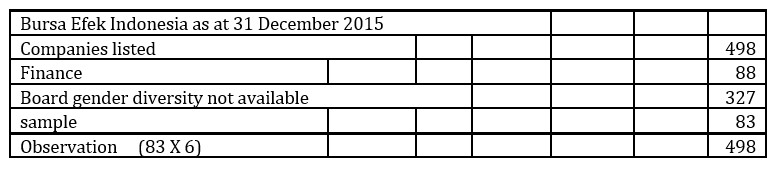

This paper uses data from 83 non-financial enterprises in Indonesia-listed firms from 2015 to 2020, so 498 observations are obtained. This study used a purposive sampling method.

Table 1. Sample selection

Variable Definitions

The dependent variable debt to asset (DTA) is the ratio of total debt to total asset. In prior studies (Detthamrong et al., 2017; Garcia et al., 2021), DTA has been widely used to measure financial leverage. Accordingly, DTA has been adopted in this paper as the variable of a dependent.

This paper has preferred one of the most general dimensions of board diversity. Gender diversity of board (BGEN) is the explanatory variable. It measured the sum of women directors as a proportion of total directors (Usman et al., 2019; Rossi et al., 2017; Dwaikat et al., 2021).

We made a difference between indirect and direct methods to analyze the effect of gender diversity in the boardroom and debt. Enterprise size has been verified as a moderator variable on such a link. Firm size (FZ) is measured as a logarithm of total assets (Mishra et al., 2018; Tariq et al., 2019).

Control variables are board size and board independence. Bigger boards are positively associated with monitoring effectiveness (Adams and Mehran, 2003). The size of the board is a negative link with the enterprise cost of debt (Lorca et al.,2011). The size of the board (BZ) is the total number of the firm’s directors (Bansal et al., 2021).

The high proportion of independent directors allows monitoring agents more effectively (Ahmed Sheikh et al., 2012). Lorca et al. (2011) stated that boards with a high level of independent directors have less cost of debt. Board independence (BIND) is the sum of independent directors divided by the sum of directors (Kao et al., 2019).

Empirical Model Of Research

To explore the influence of gender diversity in the boardroom on debt, panel regression is used.

The paper regression equation is modeled as follows:

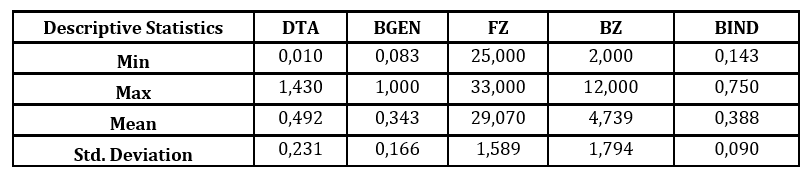

Table 1 exhibits that the maximum value of DTA is 1,430, while the minimum value of DTA is 0,010. The mean DTA is 0,492. Also, BGEN is 0,343. Therefore FZ is 29,070. The next BZ is 4,739. Additionally, BIND is 0,388.

Table 3: Panel Data Regression

Source: Processing results by STATA software

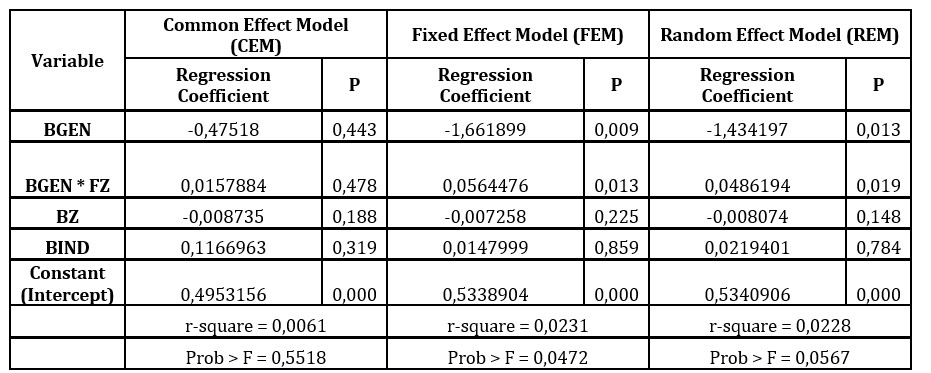

Based on the results shown in Table 2, the common effect model (CEM) results show that all variables, namely BGEN, BGEN*FZ, BZ, and BIND, each has no significant effect on DTA, with all p values > 0.05. Meanwhile, in the fixed effect model (FEM), BGEN and BGEN*FZ variables have a significant effect on DTA, with each a probability value of p = 0.009 < 0.05 and p = 0.013 < 0.05. In the random-effects model (REM), the variables BGEN and BGEN*FZ, each has a significant effect on DTA, with the respective probability values p = 0.013 < 0.05 and p = 0.019 < 0.05. The model of fixed effect (FEM) and the model of random effect (REM) gave better results compared to the model of common effect (CEM) because the model of fixed effect (FEM) and the model of random effect (REM) gave two significant results. However, statistical testing was necessary to determine which model was appropriate. To determine the estimation model with the Chow test, CEM or FEM would be used to form the regression model. The hypotheses tested were as follows.

H0: the model of CEM is better than the model of FEM.

H1: The model of FEM is better than the model of CEM.

Below are the results based on the Chow test using STATA

Table 4. Results of the Chow Test

Source: Processing results by STATA software

The rules for making decisions are as follows.

If the Chow test results are below 0.05, H1 is accepted, and H0 is rejected.

If the Chow test results are above or equal to 0.05, H0 is accepted, and H1 is rejected.

Based on the value of the Chow test presented

in Table 3, the Chow test results are less than 0.05. Therefore, the approximation model used was the fixed effect model (FEM). Next, it was tested again to select between FEM and REM. The test was carried out using the Hausman test.

Table 5. The results of the Hausman test

Source: Processing results by STATA software

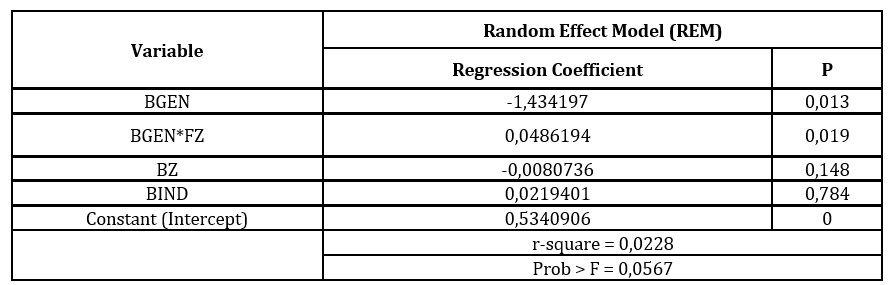

The value of the Hausman test shown in Table 4 was 0.9061 > 0.05, so the model elected was the random effect model (REM). The random-effect model (REM) was selected as the model. Based on statistical tests, the selected model was the random effect model (REM).

Table 6. Selected Model: Random Effect Model (REM)

Source: Processing results by STATA software

Based on the random effect model (REM) results presented in Table 5, BGEN has a significant negative effect on DTA, with p = 0.013 <0.05. BGEN*FZ has a significant positive effect on DTA, with p-value = 0.019 < 0.05. This means that FZ significantly moderates the effect of BGEN on DTA. While BZ and BIND, each has no significant effect on DTA, with each a probability value of p = 0.148 > 0.05 and p = 0.784 > 0.05. It is known that the value of r-square = 0.0228, which means that BGEN, BGEN*FZ, BZ, and BIND, together, can explain DTA by 2.28%.

Conclusion

Our study considers if diversity of the board affects the capital structure and examines whether firm size transforms this connection. The size of an enterprise may provide a moderating role based on contingency theory in the link between gender diversity of the board and leverage.

This study supports gender diversity in the boardroom literature by serving a preferable concept of enterprise size, moderating the connection between gender diversity in the boardroom and capital structure. Prior studies on this connection have found positive results (e.g., Rossi et al., 2017; Mehedi et al., 2020), negative results (e.g., Garcia et al., 2021; Adusei et al., 2018; Alves et al., 2015), no link (e.g., Detthamrong et al., 2017).

The study finds evidence size of the firm is a moderating factor in the gender diversity of the board and capital structure, which might explain the inconsistent result in the effect of gender diversity of the board on leverage, also, enrich the concept impact of gender diversity in the boardroom and capital structure in emerging economies. This research examines how gender diversity in the boardroom may increase debt. Based on a sample of 83 Indonesia-listed firms from 2015 to 2020, our study results propose that board gender diversity positively impacts the capital structure under variable moderating. Small firms have more leveraged than larger firms because it is more expensive to issue new equity and less asymmetric information (Smith, 1977; Rajan et al., 1995). This finding inline with agency theory states that gender diversity in the boardroom increases monitoring role (Adams & Ferreira, 2009). Consequently, borrowers charge cheap for debt (Usman et al., 2019); In turn, this accelerates the factor of getting more debt (Zaid et al., 2020). And the resource dependence theory, Hillman & Dalziel (2003) states that the board becomes a resource provider for the company. The presence of females in the boardroom increases obtaining the enterprise debt (Reguera-Alvarado et al., 2017).

The influence between gender diversity on board and the size of an enterprise is significantly positive for capital structure. This evidence suggests that the size of an enterprise significantly improves the negative link between gender diversity in boardroom and capital structure. This finding also inlines the trade-off theory with tax, which states debt increase enterprise value (Modigliani & Miller, 1963). Gender diversity on board minimizes debt costs by alleviating agency conflict among managers and lenders (Pandey et al., 2019). And Free cash flow theory proposes that enterprise cash flow in excess increases conflicts of interest among agents and shareholders (Jensen, 1986). Board gender diversity is an accelerated factor in getting more debt (Zaid et al., 2020). From the contingency theory perspective, this study enriches our knowledge of how board gender diversity is connected to leverage.

Acknowledgment

There is no conflict of interest to declare

References

Adams, R., & Mehran, H. (2003). Is corporate governance different for bank holding companies?. Federal Reserve Bank of New York. Economic Policy Review, pp. 123-42.

Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94, 291–309.

Adams, R.B., & Funk, P. (2012). Beyond the glass ceiling: does gender matter? Management Science 58(2):219–235

Adusei, M., & Obeng E. Y. T. (2018). Board gender diversity and the capital structure of microfinance institutions: A global analysis. The Quarterly Review of Economics and Finance 71: 258-269.

Alves, P., Couto, E. B., & Francisco, P. M. (2015). Board of directors’ composition and capital structure. Research in International Business and Finance, 35, 1–32.

Anderson, R. C., Mansi, S. A., & Reeb, D. M. (2004). Board characteristics, accounting report integrity, and the cost of debt. Journal of Accounting and Economics, Vol. 37, pp. 315-42.

Bansal, D., & Singh S. (2021). Does board structure impact a firm’s financial performance? Evidence from the Indian software sector. American Journal of Business.

Berle, A., & Means, G. (1932). The modern corporation and private property. New York: Macmillan.

Briozzo, A., Cardone-Riportella, C., & García-Olalla, M. (2019). Corporate governance attributes and listed SMES’ debt maturity. Corporate Governance: The International Journal of Business in Society 19(4): 735-750.

Boyd, B. K., Haynes, K. T., & Zona, F. (2011). Dimensions of CEO–board relations. Journal of Management Studies, 48(8), 1892–1923.

Carter, D. A., Simkins, B. J., & Simpson, W.G. (2003). Corporate Governance, Board Diversity, and Firm Value. Financial Review 38(1): 33-53.

Carter, D. A., D’Souza, F., Simkins, B. J., & Simon, W. G. (2010). The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review, 18(5), 396–414.

Child, J. (1975). Managerial and organizational factors associated with company performance-part II: A contingency Analysis. Journal of Management Studies, 12(1–2), 12–27.

Darmadi, S. (2013). Do women in top management affect firm performance? Evidence from Indonesia. Corporate Governance: The International Journal of Business in Society 13(3): 288-304.

Detthamrong, U., Chancharat, N., Vithessonthi, C. (2017). Corporate governance, capital structure and firm performance: Evidence from Thailand. Research in International Business and Finance 42: 689-709.

Dwaikat, N., Qubbaj I. S., & Queiri, A. (2021). Gender diversity on the board of directors and its impact on the Palestinian financial performance of the firm. Cogent Economics & Finance 9(1): 1948659.

Elmagrhi, M. H., Ntim, C. G., Malagila, J., Fosu, S., & Tunyi, A. A. (2018). Trustee board diversity, governance mechanisms, capital structure, and performance in UK charities. Corporate Governance: The International Journal of Business in Society 18(3): 478-508.

Faccio, M., Marchica, M-T., & Mura, R. (2016). CEO gender, corporate risk-taking, and the efficiency of capital allocation. Journal of Corporate Finance 39:193–209.

Fama, E., & Jensen, M. (1983). Separation of ownership and control. Journal of Law and Economics, 26: 301-325.

García, C. J., & Herrero, B. (2021). Female directors, capital structure, and financial distress. Journal of Business Research 136: 592-601.

Hannan, M. T., & Freeman, J. (1984). Structural inertia and organizational change. American Sociological Review, 49(2), 149–164.

Hillman, A. J., & Dalziel, T. (2003). Board of directors and firm performance: Integrating agency and resource dependence perspectives. Academy of Management Review, 28(3), 383–396.

Jensen, M., & Meckling, W. (1976). Theory of the firm: Managerial behavior, agency costs, and ownership structure. Journal of Financial Economics, 3: 305-360.

Jensen, M.C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review 76(2):323– 329.

Kao, M-F., Hodgkinson, L., & Jaafar, A. (2019). Ownership structure, board of directors and firm performance: evidence from Taiwan. Corporate Governance: The International Journal of Business in Society 19(1): 189-216.

Kilic, M. (2015). The effect of board diversity on the performance of banks: Evidence from Turkey. International Journal of Business and Management, 10(9), 182–192.

Kraus, A., & Litzenberger, R. H. (1973). A state-preference model of optimal financial leverage. The JournalofFinance, Vol. 28No. 4, pp. 911-922.

Lorca, C., Sanchez-Ballesta, J. P., & Garcia-Meca, E. (2011). Board effectiveness and cost of debt. Journal of Business Ethics, Vol. 100, pp. 613-631.

Mehedi, S., et al. (2020). The relationship between corporate governance, corporate characteristics and agricultural credit supply: evidence from Bangladesh. International Journal of Social Economics 47(7): 867-885.

Miller, M. H. (1977), Debt and taxes. The Journal of Finance, Vol. 32No. 2, pp. 261-275.

Mishra, R. K., & Kapil S. (2018). Effect of board characteristics on firm value: evidence from India. South Asian Journal of Business Studies 7(1): 41-72.

Mizruchi, M. S., & Stearns, L. B. (1994). A longitudinal study of borrowing by large American corporations. Administrative Science Quarterly, 39: 118-140.

Modigliani, F. & Miller, M. (1963). Corporate income taxes and the cost of capital: a correction. American Economic Review, Vol. 53, pp. 433-443.

Nahavandi, A., & Malekzadeh, A. R. (1993). Leader style in strategy and organizational performance: An integrative framework. Journal of Management Studies, 30(3), 405–425.

Pandey, R., Biswas, P. K., Ali, M. J., & Mansi, M. (2019). Female directors on the board and cost of debt: Evidence from Australia. Accounting & Finance, 60, 4031–4060.

Pfeffer, J. (1972). Size and composition of corporate boards of directors: The organization and its environment. Administrative Science Quarterly, 17: 218-228.

Pfeffer, J.: (1973). Size, Composition and Function of Hospital Boards of Directors: A Study of Organization Environment Linkage, Administrative Science Quarterly 18, 349-363.

Pfeffer, J., & Salancik, G. (1978). The external control of organizations: A resource dependence perspective. New York: Harper & Row.

Rajan, R., & Zingales, L. (1995). What do we know about the capital structure? Some evidence from international data. Journal of Finance, 50, 1421–1460.

Reguera-Alvarado, N., de Fuentes, P., & Laffarga, J. (2017). Does Board Gender Diversity Influence Financial Performance? Evidence from Spain. Journal of Business Ethics 141(2): 337-350.

Rossi, F., Cebula, R.J., & Barth, J.R. (2017). Female representation in the boardroom and firm debt: empirical evidence from Italy. Journal of Economics and Finance 42(2): 315-338.

Selznick, P. (1949). TVA and the grassroots: A study of the sociology of formal organizations. New York: Harper & Row.

Sheikh, N. A., & Wang, Z. (2012). Effects of corporate governance on capital structure: empirical evidence from Pakistan. Corporate Governance: The International Journal of Business in Society 12(5): 629-641.

Siciliano, J. I. (1996). The relationship of board member diversity to organizational performance. Journal of Business Ethics, 15(12), 1313–1320.

Singh, M., & Davidson III, W. N. (2003). Agency costs, ownership structure and corporate governance mechanisms. Journal of Banking & Finance 27:793–816.

Smith Jr., C. W. (1977). Alternative methods for raising capital right versus underwritten offerings. Journal of Financial Economics, 5, 273–307.

Tanaka, T. (2014). Gender diversity in the boards and the pricing of publicly traded corporate debt: evidence from Japan. Applied Financial Economics 24(4): 247-258.

Tariq, H., Shahzad, F., Anwar, A., & Rehman, I. U. (2019). Economic Consequences of Insider-ownership: An Emerging Market Perspective. Asia-Pacific Contemporary Finance and Development, Emerald Publishing Limited. 26: 117-139.

Usman, M., Farooq, M. U., & Zhang, J. (2019). Female directors and the cost of debt: does gender diversity in the boardroom matter to lenders? Managerial Auditing Journal 34(4): 374-392.

Van Knippenberg, D., De Dreu, C. K. W., & Homan, A. C. (2004). Workgroup diversity and group performance: An integrative model and research agenda. Journal of Applied Psychology, 89(6), 1008.

Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management Journal, 5: 171-180.

Zaid, M. A. A., Wang, M., Abuhijleh, S. T. F., Issa, A., Saleh, M. W. A., & Ali, F. (2020). Corporate governance practices and capital structure decisions: the moderating effect of gender diversity. Corporate Governance: The International Journal of Business in Society 20(5): 939-964.

Zald, M. N. (1969). The Power and Function of Boards of Directors, A Theoretical Synthesis, American Journal of Sociology 75, 97-111.

Zahra, S., & Pearce, J. (1989). Boards of directors and corporate financial performance: a review and integrative model, Journal of Management, Vol. 15, pp. 291-334.

Zona, F., Zattoni, A., & Minichilli, A. (2013). A contingency model of boards of directors and firm innovation: The moderating role of firm size. British Journal of Management, 24(3), 299–315.