1Putu Sugiartha SANJAYA and 2Wimpie Yustino SETIAWAN

Universitas Atma Jaya Yogyakarta, Daerah Istimewa Yogyakarta, Indonesia

Volume 2023,

Article ID 672101,

IBIMA Business Review,

13 pages,

DOI: https://doi.org/10.5171/2023.672101

Received date: 2 May 2023; Accepted date: 21 July 2023; Published date: 21 September 2023

Academic Editor: Abdul Hadi Zulkafli

Cite this Article as:

Putu Sugiartha SANJAYA and Wimpie Yustino SETIAWAN (2023)," Do Independent Directors Affect Real Earnings Management Practices? The Case of Indonesian Two-Tier Board System ", IBIMA Business Review, Vol. 2023 (2023), Article ID 672101, https://doi.org/10.5171/2023.672101

The question regarding the role of independent directors in corporate governance in general and in limiting real earnings management practices in particular has long been debated. This study, therefore, attempts to address this question by investigating the influence of independent directors on real earnings management (REM) from the perspective of Indonesian two-tier board system. Examining the data of manufacturing firms listed on the Indonesia Stock Exchange during the 2014-2018 period and employing the model developed by Roychowdhury (2006) to measure REM, the findings of this study indicate that independent directors positively affect REM practices, suggesting the under-performance of independent directors which may put minority shareholders at a disadvantage. The insight provided by these findings may be of important value to regulators and policy makers, especially in formulating future policies with regard to the role of independent directors in the two-tier board system adopted in Indonesia in order to improve good corporate governance.

Keywords: independent directors, real earnings management, two-tier system, corporate governance.

Introduction

In the Indonesian context, the board consists of the board of directors as the management and the board of commissioners which supervises the board of directors. Both boards are accountable to shareholders. Each board also has independent members as independent directors and independent commissioners. As stated in the Appendix I of the BEI Kep-00001/BEI/01-2014, publicly listed companies are required to have independent directors as a counterweight when top managers make decisions. With independent parties on both boards, as part of good corporate governance, unhealthy practices by managers could be prevented. This is important because managers have control on earnings such as through covenants of debt, avoidance of losses, and compensation. Managers may conduct earnings management to protect the interests of controlling shareholders.

This study aims to investigate whether independent directors on the board influence real earnings management (REM). This study is especially important because, unlike in other countries, the existence of independent directors, formerly called unaffiliated directors, in Indonesia is a new phenomenon. In the one-tier system, the board of directors comprises executive directors and non-executive directors. The two-tier system, however, is made up of two separate bodies, namely directors and commissioners.

The presence of independent directors in Indonesia is of crucial importance due to the involvement of controlling shareholders in the board of directors. Siregar (2006) found that 33.56% of controlling shareholders were part of directors, with evidence showing that the board was occupied by ultimate shareholders themselves, their children, or their relatives.

Due to its role as a counterweight in the process of decision-making, an independent director in the context of Indonesia is different from a non-executive director in countries adopting the one-tier who typically monitors the executive directors. The supervisory duties in Indonesian public companies are carried out by the board of commissioners, which is comprised of commissioners and independent commissioners. Nevertheless, referring to the Indonesian Law on Limited Companies, directors are appointed and dismissed through the meeting of shareholders. This means that controlling shareholders may still be dominant when appointing an independent director.

The contribution of this paper is fourfold. First, this study has an economic contribution. The findings of this study show the under-performance of independent directors in preventing or reducing REM. Shareholders may use their voting rights to dismiss an independent director if he/she is not playing a positive role in the mechanisms of corporate governance. The presence of independent directors will otherwise be an economic burden on the company. Second, this study’s results may be of value to the Indonesian Financial Services Authority in formulating policies regarding the existence of independent directors. Third, this study contributes to the development of agency theory. In the context of Indonesia, the conflict mainly occurs between controlling shareholders and non-controlling ones, because the former are often involved in the management team of a company. The results of this study can be used as a reference for future design and implementation of supervisory mechanisms that would enhance the financial reporting quality and reduce REM. Fourth, the results of this study are of value to practitioners, in general, and investors, in particular. Investors need to pay attention to the list of names presented at the meeting of shareholders and check the background of each name appearing at the meeting.

After this introduction section, section 2 reviews literatures and develops hypothesis. Section 3 describes research methods. Section 4 describes results and discussions. The last section provides conclusions and opportunities for next research.

Theoretical Framework, Literature Review and Hypothesis Development

Earnings Management

Activities of earnings management through accruals mainly use pure accounting decisions (Dechow et al., 1995; Peasnell et al., 2000; Osma and Noguer, 2007), while real earnings management is concerned about selling assets (Bartov, 1993) and managing R&D expenditure (Bushee, 1998; Cheng, 2004). Accrual-based earnings management is less expensive for managers to meet their target. A study carried out by Graham, Harvey and Rajgopal (2005) finds evidence that real earnings management is widely used, with more than 80 percent of the financial executives using this method by decreasing R&D to meet their targets. Zang (2012), Braam et al. (2015), and Ho et al. (2015) point out that, instead of managing accruals, real-based earnings management is performed by managing normal activities. Various accounting methods are employed by managers to improve the earnings baseline through accruals. This method, however, will revert in next periods and it does not influence the cash flows of the firm (Dechow et al., 1995; Healy and Wahlen, 1999). Real earnings management, on the contrary, is conducted by managing real activities, such as normal operations, which will consequently affect the company’s cash flows (Zang, 2012). A literature review by Dutzi and Rausch (2016) suggest that, during times of crisis, managers may employ either income-increasing or income-decreasing techniques. Prior to bankruptcy, however, most companies carry out income-decreasing earnings management.

Roychowdhury (2006), Zang (2012) and Chan et al. (2015) point out that real-activity manipulations are chosen by managers when tighter scrutiny on flexibility in accounting occurs. Managing real activities, nevertheless, is most costly for companies, although it is less costly for managers (Gunny, 2005; 2010). On the other hand, accruals manipulation, in general, is considered a less detectable and less expensive method and, therefore, preferred by managers to meet their target income. Kuo et al. (2014) find that Chinese companies moved manipulating earnings from accruals to real-activity earnings management after the Split-Share Structure Reform, because it is less detectable and less scrutinised. Zang (2012) finds that, during a fiscal year, the manager prefers manipulating earnings by real activities and subsequently adjusting accruals at year-end, depending on the effectiveness of real activities manipulation in increasing the reported earnings.

Kim et al. (2010) find that companies manage earnings by real activities, particularly when they are in position of near debt covenant breaches. In a separate study, Ge and Kim (2014) find that companies perform real-activity earnings management in the year of issuing their new bonds to reduce bond yield spread and mislead rating agencies. Meanwhile, Chan et al. (2015), Cohen and Zarowin (2010), Cohen et al. (2008), and Roychowdhury (2006), finds that, compared to accruals manipulation, real-activity earnings management is more costly for shareholders, as this method could decrease future cash flows and damage the firm’s viability. As a matter of fact, a truthful disclosure of accounting information is less likely to draw auditor and regulatory scrutiny (Cohen et al., 2008). On the other hand, real-activity earnings managem ent will decrease a firm’s value, because it negatively affects its future cash flows (Mellado-Cid et al., 2018; Roychowdhury, 2006).

Previous research has also suggested that independent directors affect corporate decision making. The studies by Weisbach (1988) and Byrd and Hickman (1992) find that independent directors influence board decisions. Dechow et al. (1996) and Peasnell et al. (2005) report that independent directors limit accrual earnings management practices. Klien (2002) finds a negative relationship between discretionary accruals and the percentage of independent directors on the board of directors. However, there is no previous study that has given empirical evidence that independent directors can limit real-activity earnings management.

Real Earnings Management

As argued by Roychowdury (2006), managers prefer to manage earnings by real-activity earnings management than accrual-based earnings management, because the latter is riskier than the former and could easily be discovered by auditors. Roychowdhury (2006) suggests that real-activity earnings management is a tool to manage earnings by conducting normal business practices to meet profit targets. It is frequently carried out in three forms, namely discounted prices, overproduction, and discretionary costs reduction.

One- and Two-Tier Systems

Nestor and Thompson (2000) mention two models of corporate governance commonly adopted by companies. The first model is called the one-tier model or unitary system. This model is also known as the outsider model or Anglo-Saxon model and is widely adopted in, among others, the USA, the UK, and Canada. The second model is called the two-tier model or insider model. This model is generally applied in countries with the Continental European System such as Germany. It is also predominantly used in Indonesia.

Independent Directors in One-Tier System

Independent directors in one-tier system are more popular in countries adopting the common law. The system only recognises the board of directors, which consists of executive directors and non-executive directors. In the 1950s, independent directors were formed voluntarily by companies in the USA with the aim of creating well-managed companies. Independent directors are now required by law (Varottil, 2011). The New York Stock Exchange requires companies to have independent directors in the audit committee (Clarke, 2007). Meanwhile, in the UK, independent directors first appeared in 1992 in a Cadbury Committee report as a significant part of good corporate governance in that country (Varottil, 2011). An independent director is a member of the board of directors who has no relationship with the company and the company manager in his/her capacity as a director (Varottil, 2011). Independent directors are often called independent board of directors or external directors because they supervise the executive directors. The word “independent” suggests that these directors are the representatives of minority shareholders.

According to the regulations of the NYSE and Nasdaq approved by the Security Exchange Committee (SEC) in 2003, an independent director is a director who has no relationship with a listed company, either directly or indirectly, such as a partnership, shareholder, or an official in an organisation related to the company (Duchin et al., 2009). On the New York Stock Exchange, an independent director is considered independent if he/she has announced and stated that he/she has no material relationship with the company (Clarke, 2007). While an independent director has the duties of overseeing management on behalf of shareholders, developing strategic plans, and collecting all forms of resources, the purpose of having an independent director is more aimed at monitoring executive performance and reducing the divergence between the interests of shareholders and management (Lawrence and Stapledon, 1999).

Independent Directors in Indonesia

Law Number 40 of 2007 Republic of Indonesia has no reference about independent directors. The Law addresses independent commissioners as follows:

(1) The existence of one or more independent commissioners and one representative commissioner.

(2) Independent commissioner is elected by shareholders on meeting of shareholders.

Therefore, when compared to the above-mentioned Indonesian company law, the concept of independent directors (non-executive directors) in countries applying common law is similar to the concept of independent commissioners in countries with the legal systems of Continental Europe which adopt the two-tier system. In Indonesia, the concept of independent directors was first recognised and confirmed in the Circular Letter of the Indonesian Stock Exchange Number SE-00001/BEI/02-2014 explaining the terms of independent commissioners and independent directors of public companies, in which the term “independent director” replaces the term “unaffiliated director”.

The Decree of the Director of the Indonesian Stock Exchange Number Kep-00001/BEI/01-2014 addresses Amendments to Rule No. I-A. There are several listing requirements, including:

An unaffiliated director of at least one person on board of directors is elected through meeting of shareholders.

Unaffiliated directors must meet the following requirements:

No affiliation with the controlling shareholder;

There is no affiliation with other Commissioners or Directors of the public firm;

Currently not working as a director in another firm;

No insider in an institution-related capital market.

The appointment of an independent director of a company must refer to Article 94 paragraph 1 of the Act of Limited Companies, that the members of the board of directors are elected by shareholders in the general meeting. Furthermore, Part III 1.5.2 of BEI Rule Number 1-A also stipulates that the independent director must meet the requirements as follows (Gupta et al., 2011):

Has no affiliation with the main shareholder not more than 6 months prior to the appointment;

Has no affiliation with Board of Directors and Board of Commissioners;

Not serving as a director or Board of Commissioners in another listed or non-listed firm;

No insider in institution who has been employed by the Issuer.

Section III.1.5.1 of Rule Number 1-A requires every public company to have at least one independent director elected by shareholders in general meeting who will begin to act effectively as independent director after shares are registered in capital market. The independent director is only allowed to serve, as stipulated in section V.4.2. Rule Number 1-A, no more than two consecutive terms.

Hypothesis of Independent Directors and Real Earnings Management

Amongst the essential elements of good governance, board of director characteristics are often considered effective tools in reducing earnings management practices (Cho and Chung, 2022; Iqbal et al., 2022; Aleqab and Ighnaim, 2021; Peasnell et al., 2005; Uzun et al., 2004; Xie et al., 2003; Klein, 2002; Beasley, 1996). A study by Klien (2002) finds a significantly negative influence of outside directors on the board on discretionary accruals. Osma (2008) finds board independence reduces the probability of managers cutting R&D spending due to previous period disappointments and earnings management to meet the current targets. Kang and Kim (2012) find that when the size of independent directors is larger, real-activity earnings management decreases. The negative impact of board members’ independence on earnings management is also found by Aleqab and Ighnaim (2021), who examine 131 companies listed on the Amman Stock Exchange. The findings of a study by Iqbal et al (2022) also confirm the significant role of the size and independence of the company board in limiting earning management practices in Malaysia. Studying the influence of board characteristics on earnings management in Vietnamese publicly listed companies, Cho and Chung (2022) find evidence that the board size and the percentage of external directors on the board negatively influence earnings management.

Visvanathan (2008) shows that only independence of the board negatively and significantly affects abnormal production. Visvanathan (2008) further explains that the lack of relationship between governance mechanisms and real-activity earnings management may be due to the fact that real activity-based earnings management is more complex and difficult to detect. In another study, Osma (2008) finds empirical evidence that independent board can detect and limit real-based earnings management. Examining the listed firms on the Bombay Stock Exchange, Kapoor and Goel (2019) also find evidence that independent directors may restrain practices of earnings management. However, Fallatah (2021) finds that the independence level of the board of directors has no influence on earnings management in Saudi Arabia’s financial sector.

Kang and Kim (2012) find that board independence and board size have negative impact on real earnings management. In a study by Talbi et al. (2015), higher board independence is associated with lower levels of real activities manipulation. Ali et al. (2014), Cheng et al. (2013), Demsetz and Lehn (1985) indicate a weaker role of the independent board of directors. Due to the higher noise and information asymmetry in concentrated markets, managers’ behaviour is more difficult to be monitored by independent board members. The findings of a study of family-controlled companies in Italy by Lippolis and Grimaldi (2020) suggest that the effectiveness of board of directors in limiting earning management may be hindered by family presence.

While the presence of an independent director may strengthen corporate governance, their selection process is largely determined by the control rights of controlling shareholders, which are likely to diminish independent directors’ role in creating good corporate governance. Based on these pros and cons of the role of independent directors in the corporate governance, the hypothesis of the present study is non-directional. Therefore, the research hypothesis is formulated as follows.

Ha1: Independent directors influence real earnings management.

Methodology

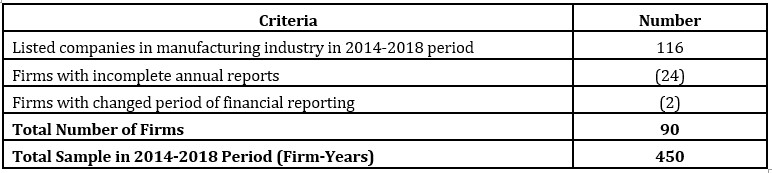

Sampling Technique

The sample of this study consists of manufacturing industry on the Indonesia Stock Exchange from 2014 until 2018. The sample selection is presented in the following table.

Table 1: Sample of Research

Research Variables

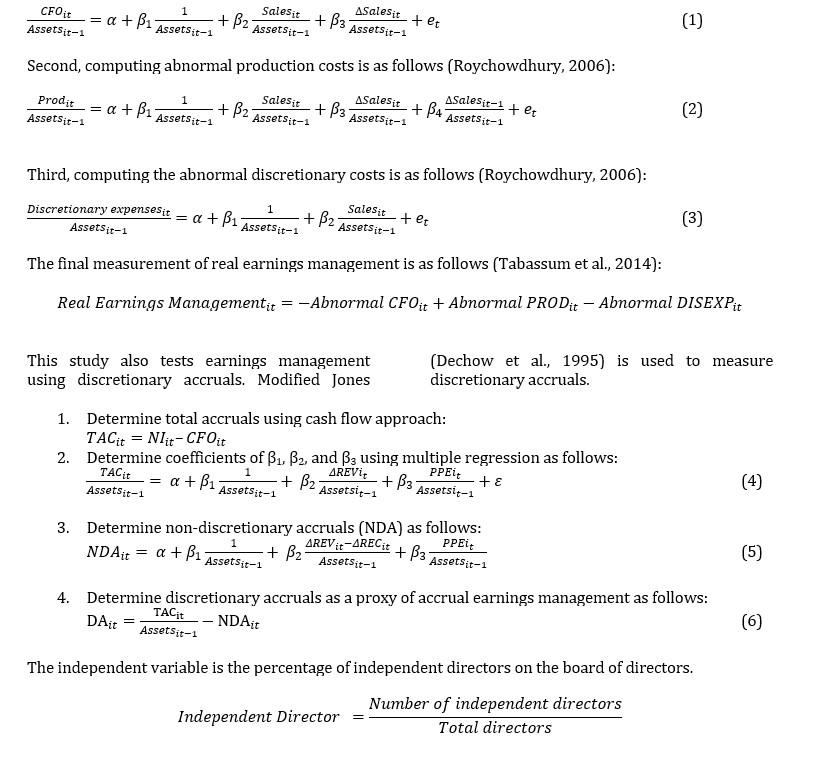

The dependent variable is real earnings management (REM), which is measured by three abnormal or unexpected activities, namely, unexpected operating cash flow, unexpected production, and unexpected discretionary costs (Roychowdhury, 2006). First, computing unexpected operating cash flows (Roychowdhury, 2006) is as follows.

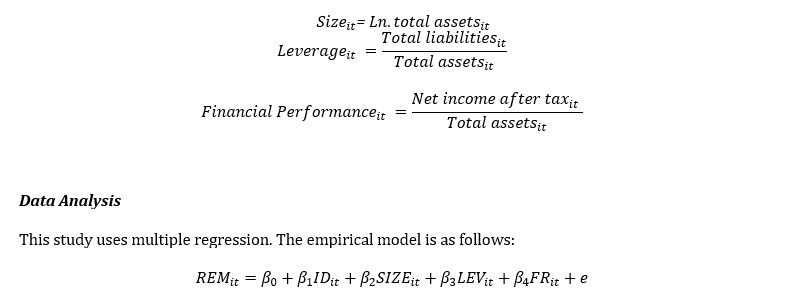

Based on the studies by Vorst (2016) and Filip et al. (2015), firm size is a variable that consistently affects earnings management. The present study, therefore, uses company size as a control variable. Company size is the logarithmic value of total assets (Qi et al., 2018). Three other control variables used in the present study are: size, leverage, and financial performance.

Results of Data Analysis

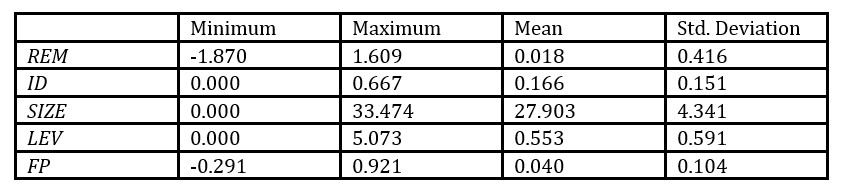

Descriptive Statistics

The following table summarises the descriptive statistics.

Table 2: Descriptive Statistics

As shown by Table 2, the mean value for REM was 0.018 (or 1.80 percent of total assets), indicating that the companies in the sample undertook real earnings management. The mean value for ID was 0.166, showing that the independent directors, on average, were 16.6 percent of total directors. It was found that one or two companies in the sample had two independent directors and even an independent director who became the main director. However, there were some companies in this sample which did not have independent directors. Most of the companies in this sample had only one president director. Meanwhile, the average levels of leverage and firm performance were 55.30 percent and 4 percent, respectively, of total assets.

Correlation

The relationships amongst variables are presented in the following table.

Table 3: Correlation

Table 3 shows the matrix of correlation of the variables used in regression. Consistent with the hypothesis that independent directors are related to real earnings management, a positive correlation between independent director (ID) and real earnings management (REM) was found. However, there were negative correlations between ID and SIZE, and ID and FP. To check whether the sample suffered from multicollinearity, the Variance Inflation Factors (VIFs) for each of the independent variables were also examined. The results showed that all VIF values were relatively small, and none exceeded 10. Therefore, it was concluded that there was no problem of multicollinearity.

Regression

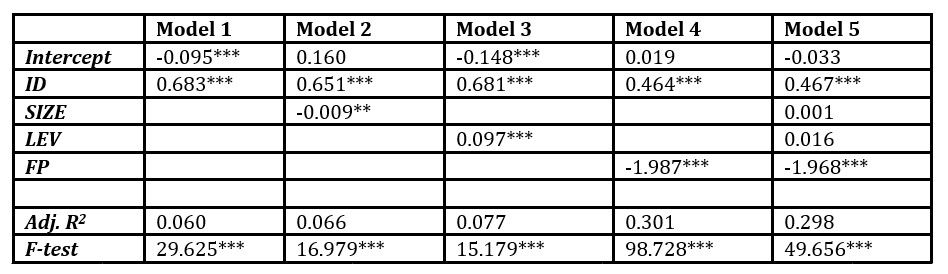

Table 4: Hypothesis Testing

Based on Table 4, the research hypothesis is supported. The ID coefficients are 0.683, 0.651, 0.681, 0.464, and 0.467 in models 1, 2, 3, 4 and 5, respectively, significant at an alpha of 0.01. This indicates that, as the percentage of independent directors increases, real-activity earnings management practices increase, implying that the presence of independent directors in Indonesia has not supported good corporate governance and signifying the failure of the independent directors in playing their balancing role in the process of decision-making.

Empirical evidence of this study has suggested that the existence of an independent director in a publicly-listed company is only a burden on the company, instead of a benefit, as the presence of independent directors does not support efficient corporate governance. The salaries and benefits paid by the company to the independent director have become a financial burden on the company and its shareholders, since these expenses decrease the company’s income and, consequently, reduce the amount of dividends distributed to the shareholders. The empirical evidence of this study may raise the question about the effectiveness of the presence of independent directors in the corporate governance mechanisms in Indonesia.

This result may be due to the process of electing independent directors by shareholders in the general meeting, where the controlling shareholder’s voting rights tend to overpower the voting rights of the non-controlling ones. Typically, at such a meeting, the session chairperson only reads out the names of the board of directors, including the independent director, to the meeting participants, and inquires the meeting participants if there are any suggestions or objections. If there is no objection raised, the session chairperson will then finalise the agenda of the board of directors’ choice and ask the notary to read out the results of the vote counting the number of “agree”, “disagree”, and “abstain” votes. A voting process like this is susceptible to the significant influence of the controlling shareholder, who generally has the largest votes, on the decision-making process of appointing the independent director.

This may cause the public to doubt the independence of the elected independent director, especially in protecting the interest of minority investors, and to think that the whole voting process is just a mere formality. Since the independent director is elected by the majority vote and the controlling shareholder has the largest votes, the independent director may only appear independent but they are not independent in fact. Moreover, independent directors may not act independently when making decisions, because they are afraid to be dismissed by the controlling shareholder. The phenomenon of most controlling shareholders placing themselves or their relatives on the boards of directors and commissioners may discourage the independent director from taking corrective measures and balancing the conflicting interest in the company, unless the independent director is ready to lose his/her job.

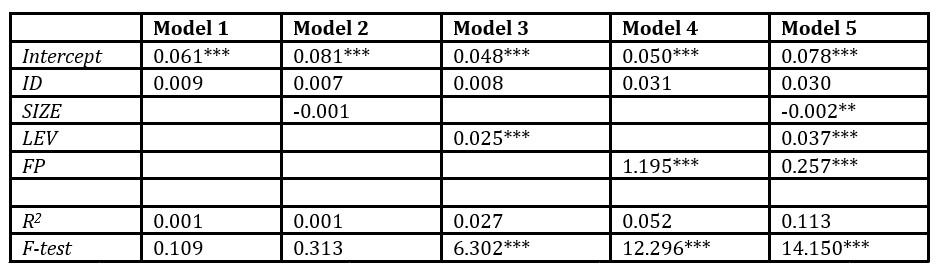

Test Using Accrual-Based Earnings Management

The study also carries out a test using discretionary accruals (in absolute accruals) as the dependent variable. The results are as presented in Table 5.

Table 5: Accrual-Based Earnings Management

As shown in Table 5, managers prefer more to use real activities than accruals to manage earnings. This preference towards real-activity earnings management may be because this method, despite its impact on the cash flows of the company and being costly to the company and shareholders, is not costly to the managers and less detectable. The policy of selling at huge discount, for example, will influence current and future cash flows, such as reducing cash and net income of the company and increasing the expenses to maintain the inventory resulting from excessive production. It, consequently, may also negatively impact stock price, thereby reducing the value of the firm in capital market. These arguments are supported by the findings of prior studies. A study by Zang (2012), for example, reports that real activity-based earnings management affects firms’ cash flows. Roychowdhury (2006), Zang (2012) and Chan et al. (2015) suggest that when increased scrutiny on accounting flexibility occurs, a manager will use real activity-based manipulations. Gunny (2005; 2010) finds evidence that managing real activities is more costly to companies and their stakeholders but is less expensive to managers. Roychowdhury (2006), Cohen et al. (2008), Cohen and Zarowin (2010), and Chan et al. (2015) find that real activity-based earnings management becomes huge costs in the long run borne by shareholders. In addition to its harmful impact on future cash flows, real earnings management could also damage a company’s viability. As found by Mellado-Cid et al. (2018) and Roychowdhury (2006), real activity-based manipulations reduce firm value, as the measures taken by managers in the present period to boost earnings may adversely affect future cash flows. Nevertheless, as pointed out by Kuo et al. (2014), managers often move from accrual earnings management to real earnings management because it is less scrutinised and detectable. It is consistent with Dechow et al. (1995) and Healy and Wahlen (1999) who suggest that accrual discretionary is less used by managers because, although it does not affect the firm cash flow, it will be reverted in future periods. This method is typically considered unnoticeable and less costly.

Conclusions

This study shows there is a positive effect of independent directors on real earnings management, indicating that as the number of independent directors increases, real activity-based earnings management practices increase. The increased practices of accounting engineering which could prove detrimental to non-controlling shareholders may consequently lead to the worsening quality of financial reports, since the financial statements may not be faithfully represented, making it difficult for the minority investors to use information therein in their decision-making process. This should be of concern to regulators and the Institute of Indonesia Chartered Accountants (IAI) in making efforts to reduce such practices in the preparation of financial reports. The case of PT Garuda Indonesia Tbk, in which the national airline was forced to restate the 2018 financial statements, shows how the board of directors could manage reported earnings to turn a loss into a profit. When the case was brought up, the company’s share price dropped sharply, causing financial losses for investors who bought the company’s stock at high prices before the airline’s practice was revealed.

The limitation of the present study is the incomplete data on the board of directors. If these data had been obtained, they could have increased the number of observations and improved the power of the test of this study.

Since its outbreak in the late December 2019, nearly every company has been affected by COVID-19. It is suggested, therefore, that future research examines whether listed companies apply conservative or optimistic accounting during the pandemic, by using the 2019 and 2020 financial reports, in order to take a closer look at the role of independent directors in the good corporate governance in Indonesia. The results of such studies can provide valuable information for the Indonesian Financial Services Authority (OJK) and the Indonesia Stock Exchange for developing policies and regulations and for evaluating whether the existing policies on corporate governance are beneficial or burdensome to public companies. Further studies on independent directors and earnings management may also provide insights for the policy makers in revising the existing regulations, based on the findings of those studies for the effect of real activity-based earnings management on the firm value, market reactions, cost of equity and value relevance.

References

Aleqab, M. M., and Ighnaim, M. M. (2021). ‘The impact of board characteristics on earnings management’, Journal of Governance & Regulation, 10(3), 8–17.

Ali, A., Klasa, S., and Yeung, E. (2014), ‘Industry concentration and corporate disclosure policy’, Journal of Accounting and Economics, 58(2-3), 240-264.

Bushman, R.M., and Smith, A.J. (2003), ‘Transparency, Financial Accounting Information, and Corporate Governance’, FRBNY Economic Policy Review, April, 65-87.

Bartov, E. (1993), ‘The Timing of Asset Sales and Earnings Manipulation’, The Accounting Review, 68(4), 840-855.

Beasley, M. (1996), ‘An empirical analysis of the relation between the board of director composition and financial statement fraud’, The Accounting Review, 71, 443 – 465.

Bozec, Y., and Laurin, C. (2008), ‘Large Shareholder Entrenchment and Performance: Empirical Evidence from Canada’, Journal of Business Finance & Accounting, 35(1-2), 25–49.

Braam, G., Nandy, M., Weitzel, U., and Lodh, S. (2015), ‘Accrual-based and real earnings management and political connections’, The International Journal of Accounting, 50(2), 111–141.

Bushee, B.J. (1998), ‘The influence of institutional investor on myopic R&D investment behavior’, The Accounting Review, 73(3), 305-333.

Byrd, J.W. and Hickman, K.A. (1992), ‘Do outside directors monitor managers? Evidence from tender offer bids’, Journal of Financial Economics, 32(2), 195-221.

Chan, L.H., Kevin C. W. Chen, K.C.W., Chen, T.Y., and Yu, Y. (2015), ‘Substitution between Real and Accruals-Based Earnings Management after Voluntary Adoption of Compensation Clawback Provisions’, The Accounting Review, 90(1), 147–174.

Chen, X., and Cheng, Q. (2002), ‘Abnormal accrual-based anomaly and managers’ motivations to record abnormal accruals’, Suader School of Business Working Paper.

Cheng, S. (2004), ‘R&D expenditures and CEO compensation’, The Accounting Review, 79, 305–328.

Cheng, P., Man, P., and Yi, C.H. (2013), ‘The Impact of Product Market Competition on Earnings Quality’, Accounting and Finance, 53, 137–162.

Cho, S., and Chung, C. (2022). ‘Board Characteristics and Earnings Management: Evidence from the Vietnamese Market’, Journal of Risk and Financial Management, 15(9), 1-16.

Claessens, S., and Fan, J. P. H. (2002), ‘Corporate Governance in Asia: A Survey’, International Review of Finance, 3(2), 71–103.

Clarke, D.C. (2007), ‘Three Concepts of Independent Director’, Delaware Journal of Corporate Law, 32(1), 73-111.

Cohen, D., Dey, A., and Lys, T. (2008), ‘Real and accrual-based earnings management in the preand post-sarbanes-oxley periods’, The Accounting Review, 83(3), 757-787.

Cohen, D., and Zarowin, P. (2010), ‘Accrual-based and real earnings management activities around seasoned equity offerings’, Journal of Accounting and Economics, 50(1), 2–19.

Dechow, P.M., Sloan, R.G., and Sweeny, A.P. (1995), ‘Detecting earnings management’, The Accounting Review, 70(2), 193-225.

Dechow, P. M., Sloan, R. G., and Sweeney, A. P. (1996), ‘Causes and consequences of earnings manipulations: An analysis of firms subject to enforcement actions by the SEC’, Contemporary Accounting Research, 13(1), 1–36.

Demsetz, H., and Lehn, K. (1985), ‘The structure of corporate ownership causes and consequences’, Journal of Political Economy, 93, 115– 1177.

Ding, Y., Hope, O., Jeanjean, T., and Stolowy, H. (2007), ‘Differences between domestic accounting standards and IAS: Measurement, determinants, and implications’, Journal of Accounting & Public Policy, 26, 1–38.

Duchin, R., Matsusaka, J.G., and Ozbas, O. (2009), When are outside directors effective? Ann Arbor, University of Michigan.

Dutzi, A., and Rausch, B. (2016). ‘Earnings Management before Bankruptcy: A Review of the Literature’, Journal of Accounting and Auditing: Research & Practice (IBIMA Publishing), 2016, 1-21.

Eisenhardt, K. M. (1989), ‘Agency Theory: An Assessment and Review’, Academy of Management Review, 14(1), 57–74.

Fallatah, R. (2021). ‘Earning Management and the Independence of Board Directors: A Study of Financial Sectors in Saudi Arabia’, Academy of Accounting and Financial Studies Journal, 25(1), 1-9.

Fama, E.F., and Jensen, M.C. (1983), ‘Separation of ownership and control’, Journal of Law and Economics, 26, 301 – 325.

Fan, J. P., and Wong, T. (2002), ‘Corporate ownership structure and the informativeness of accounting earnings in East Asia’, Journal of Accounting and Economics, 33(3), 401–425.

Filip, A., Jeanjean, T., and Paugam, L. (2015), ‘Using Real Activities to Avoid Goodwill Impairment Losses: Evidence and Effect on Future Performance’, Journal of Business Finance & Accounting, 42(3-4), 515–554.

Ge, W., and Kim, J. B. (2014), ‘Real earnings management and the cost of new corporate bonds’, Journal of Business Research, 67(4), 641-647.

Graham, J. R., Harvey, C.R., and Rajgopal, S. (2005), ‘The economic implications of corporate financial reporting’, Journal of Accounting and Economics, 40(1), 3–73.

Gunny, K.A. (2005), ‘What are the consequences of real earnings management?’, Working Paper, University of Colorado, USA.

Gunny, K.A. (2010), ‘The relation between earnings management using real activities manipulation and future performance: Evidence from meeting earnings benchmarks’, Contemporary Accounting Research, 27(3), 855–888.

Gupta, S.L., Hothi, B.S. and Gupta, A. (2011), ‘Corporate: Independent Directors in the Board’, Global Journal of Management and Business Research, 11(1), 57-74.

Healy, P. M., and Wahlen, J. M. (1999), ‘A review of the earnings management literature and its implications for standard setting’, Accounting Horizons, 13, 365-383.

Ho, L.C.J., Liao, Q., and Taylor, M. (2015), ‘Real and Accrual-Based Earnings Management in the Pre- and Post-IFRS Periods: Evidence from China’, Journal of International Financial Management and Accounting, 26(3), 294-335.

Iqbal, A., Sharofiddin, A., Farooq, Z., Khan, S.A., Bilal, F., Kamran, M., Rehman, S.U. (2022). ‘Corporate Governance And Earnings Management Practices: Moderating Role Of Audit Committees’, Journal of Positive School Psychology, 6(12), 57-72.

Jensen, M. (1993), ‘The modern industrial revolution, exit, and the failure of internal control systems’, The Journal of Finance, 48(3), 831–880.

Jensen, M. C., and Meckling, W. H. (1976), ‘Theory of the firm: Managerial behavior, agency costs and ownership structure’, Journal of Financial Economics, 3(4), 305–360.

Kang, S.A., and Kim, Y.S. (2012), ‘Effect of corporate governance on real activity-based earnings management: based from Korea’, Journal of Business Economics and Management, 13(1), 29–52.

Kapoor, N., and Goel, S. (2019), ‘Do diligent independent directors restrain earnings management practices? Indian lessons for the global world’, Asian Journal of Accounting Research, 4(1), 52-69.

Kim, J.B., Song, B.Y., and Zhang, L. (2010), ‘Earnings management through real activities and bank loan contracting’, Working Paper, City University of Hong Kong.

Kim, J-B., and Sohn, B. (2013), ‘Real earnings management and cost of capital’, Journal of Accounting and Public Policy, 32(6), 518-543.

Klien, A. (2002), ‘Audit committee, Board of directors’ characteristics and earnings management’, Journal of Accounting and Economics, 33(3), 375-400.

Kuo, J. M., Ning, L., and Song, X. (2014). ‘The Real and Accrual-based Earnings Management Behaviors: Evidence from the Split Share Structure Reform in China’, The International Journal of Accounting, 49(1), 101–136.

La Porta, R., Lopez-De-Silanes, F., and Shleifer, A. (1999), ‘Corporate Ownership Around the World’, The Journal of Finance, 54(2), 471–517.

Lawrence, J., and Stapledon, G. (1999), ‘Do Independent Directors Add Value?’ Research Report. Center for Corporate Law and Securities Regulation. The University of Melbourne.

Leuz, C., Nanda, D., and Wysocki, P. (2003), ‘Earnings management and investor protection: An international comparison’, Journal of Financial Economics, 69, 505–527.

Lippolis, S., and Grimaldi, F. (2020). ‘Board Independence and Earnings Management: Evidence from Italy’, International Journal of Business and Management, 15(8), 26-28.

McNulty, T., Florackis, C., and Ormrod, P. (2012), ‘Corporate Governance and Risk: A Study of Board Structure and Process’, Research Report 129. The Association of Chartered Certified Accountants.

Meini, Z., and Siregar, S.V. (2014), ‘The effect of accrual earnings management and real earnings management on earnings persistence and cost of equity’, Journal of Economics, Business, and Accountancy Ventura, 17(2), 269 – 280.

Mellado-Cid, C., Jory, S.R., and Ngo, T.N. (2018), ‘Real activities manipulation and firm valuation’, Review of Quantitative Finance and Accounting, 50, 1201–1226.

Mizik, N., and Jacobson, R. (2007), ‘Myopic Marketing Management: Evidence of the Phenomenon and Its Long-Term Performance Consequences in the SEO Context’, Marketing Science, 26(3), 361–379.

Nestor, S., and Thompson, J.K. (2000), ‘Corporate Governance Patterns in OECD Economies: Is Convergence Under Way?’, The Conference on Corporate Governance in Asia: A Comparative Perspective, Seoul, March 1999.

Osma, B.G. (2008), ‘Board independence and real earnings management: the case of R&D expenditure’, Corporate Governance: An International Review, 16(2), 116-131.

Osma, B. G., and Noguer, B. G. (2007), ‘The Effect of the Board Composition and its Monitoring Committees on Earnings Management: Evidence from Spain’, Corporate Governance an International Review, 15(6), 1413-1428.

Peasnell, K. V., Pope, P.F. and Young, S. (2000). ‘Accrual management to meet earnings targets: U.K. evidence pre- and post-Cadbury’, British Accounting Review, 32, 415-445.

Peasnell, K. V., Pope, P. F., and Young, S. (2005), ‘Board Monitoring and Earnings Management: Do Outside Directors Influence Abnormal Accruals?’, Journal of Business Finance and Accounting, 32(7-8), 1311–1346.

Qi, B., Lin, J.W., Tian, G., and Lewis, H.C.X. (2018), ‘The Impact of Top Management Team Characteristics on the Choice of Earnings Management Strategies: Evidence from China’, Accounting Horizons, 32(1), 143-164.

Roychowdhury, S. (2006), ‘Earnings management through real activities manipulation’, Journal of Accounting and Economics, 42, 335-370.

Sanjaya, I.P.S. (2010), ‘The effects of entrenchment and alignment on earnings management’, Dissertation. Universitas Gadjah Mada.

Shleifer, A., and Vishny, R. W. (1997), ‘A survey of corporate governance’, Journal of Finance, 52(2), 737–783.

Siregar, B. (2006), ‘The separation of cash flow and controlling rights in ultimate ownership’, Dissertation. Universitas Gadjah Mada.

Supriatna, A., and Ermond, B. (2019), ‘The role of independent directors in good corporate governance’, Jurnal Yuridis, 6(1), 67 – 93.

Tabassum, N., Kaleem, A., and Nazir, M.S. (2015), ‘Real Earnings Management and Future Performance’, Global Business Review, 16(1), 21–34.

Talbi, D., Omri, M. A., Guesmi, K., and Ftiti, Z. (2015), ‘The Role of Board Characteristics in Mitigating Management Opportunism: The Case of Real Earnings Management’, Journal of Applied Business Research, 31(2), 661-674.

Uzun, H., Szewczyk, S.H., and Varma, R. (2004), ‘Board Composition and Corporate Fraud’, Financial Analysts Journal, 60(3), 33-43.

Watts, R., and Zimmerman, J.L. (1986), Positive Accounting Theory. Prentice-Hall.

Weisbach, M.S. (1988), ‘Outside directors and CEO turnover’, Journal of Financial Economics, 20 (January-March), 431-460.

Varottil, U. (2011), ‘Independent Director and their Constraints in China and India’, Jindal Global Law Review, 2(2), 127-140.

Villalonga, B., and Amit, R. (2006), ‘How do family ownership, control, and management affect firm value?’, Journal of Financial Economics, 80(2), 385–417.

Visvanathan, G. (2008), ‘Corporate governance and real earnings management’, Academy of Accounting and Financial Studies Journal, 12(1), 9-22.

Vorst, P. (2016), ‘Real Earnings Management and Long-Term Operating Performance: The Role of Reversals in Discretionary Investment Cuts’, The Accounting Review, 91(4), 1219–1256.

Xie, B., Davidson III, W.N., and DaDalt, P. J. (2003), ‘Earnings management and corporate governance: the role of the board and the audit committee’, Journal of Corporate Finance, 9, 295-316.

Zang, A. (2012), ‘Evidence on the trade-off between real activities manipulation and accrual-based earnings management’, The Accounting Review, 87(2), 675–703.

Zhao, Y., Chen, K., Zhang, Y., and Davis, M. (2012), ‘Takeover protection and managerial myopia: Evidence from real earnings management’, Journal of Accounting and Public Policy, 31, 109-135.