Volume 2024,

Article ID 544979,

IBIMA Business Review,

18 pages,

DOI: https://doi.org/10.5171/2024.544979

Received date: 20 June 2024; Accepted date: 17 July 2024; Published date: 6 September 2024

Academic Editor: Stephen Aro-Gordon

Cite this Article as:

Heba N. ASSAD (2024)," Enhancing Financial Performance through Social Responsibility Disclosure: A Study of Industrial Companies in Palestine", IBIMA Business Review, Vol. 2024 (2024), Article ID 544979, https://doi.org/10.5171/2024.544979

Social responsibility disclosure (SRD) has become a pivotal topic in various economic sectors as it develops firms’ reputations, attracts new customers, and raises their market shares. Therefore, many entities are concerned with clarifying their role in their communities by providing voluntarily financial support to achieve their goals, especially with the persistence of competitors in the market. However, institutions still have an awareness scarcity of the social responsibility importance and the return they can obtain from it, which can affect their performance and market indicators. Besides, there is limited research on its influence on financial performance in the context of Palestinian firms. Therefore, this study investigates how disclosing social responsibility activities can impact the financial performance of the industrial companies listed on the Palestine Stock Exchange (PEX) from 2018 to 2022. Panel data from annual reports are analyzed using SPSS. SRD is measured using an index from four main categories and 20 subcategories, while financial performance is assessed using Tobin’s Q and return on assets (ROA). The results indicate that SRD significantly impacts financial performance, evidenced by ROA and Tobin’s Q. However, no significant differences in SRD are found among Palestinian industrial companies during the study period. These results suggest that increasing SRD improves financial performance, leading to recommendations for promoting SRD practices through workshops and legislation.

Disclosure is the company’s announcement of all information that permits the financial statement users to evaluate the nature of the commercial activities in which it participates and the economic and environmental effects in which it operates. Its diverse activities have social dimensions, and the financial statements are suitable for evaluating them (Onuora, 2022).

All disclosures of the financial statements are essential for the sustainability of economic institutions. Notably, social responsibility disclosure has become a vital topic from an accounting viewpoint for researchers and specialists in the social, economic, and environmental science fields, especially after the economic recession in 1938 (Bag and Omrane, 2022).

After expanding the economic and business environment, many sectors support social responsibility disclosure as it effectively improves the company’s reputation and attracts new customers. Besides, the competition expands, leading the commitment to society to become one of the companies’ essential goals, and so organizations are interested in highlighting their role in the community in which they operate by disclosing their commitment to cover social responsibility and implementing projects or providing voluntarily financial support to achieve their goals, especially with the persistence of competitors in the market. Many motives are influencing that. The most important of them are enhancing opportunities for the organization’s development, promoting ethical ideals among employees, achieving a good reputation, increasing efficiency, supporting the implementation of environmental strategies, and maximizing the realization of the ecological issue.

Social responsibility disclosure can achieve many advantages for economic organizations, including obtaining a distinguished tax treatment in exemptions or reducing taxes paid due to the institution’s commitment to social responsibility. Besides, measuring the environmental and social performance of the institution is an essential rule of social analysis that avoids incurring penalties and fines due to non-disclosure of social activity information (Onuora, 2022).

Creating several NGOs and special groups that protect the environment and are interested in the rights of workers and employees affects the interest in social responsibility. However, there is still a scarcity of awareness among firms and economic institutions of the importance of social responsibility and the return businesses can obtain from involvement. It can positively affect fiscal performance and market indicators and maximize investors’ wealth (Bussoli and Conte, 2018).

This study aims to examine the impact of SRD on the financial performance of industrial firms listed on the PEX from 2018 to 2022. The specific objectives are:

Measure the level of SRD in the annual reports of the industrial companies listed on the PEX.

Analyze how SRD affects financial performance using Tobin’s Q and return on assets (ROA).

Identify significant differences in SRD practices among these companies over the study period.

Provide recommendations related to SRD practices in Palestine.

SRD is very important for companies today. It means sharing information about a firm’s social, environmental, and economic actions that can improve its reputation, attract customers, and boost financial performance.

This study derives its importance from dealing with a vital topic: examining the influence of SRD on financial performance. There is a growing concern about SRD in the Palestinian environment, which may positively affect the capital market by increasing stock liquidity and maximizing market growth. Therefore, this study highlights the necessity of SRD and the benefits enterprises may gain by considering it for all parties involved, both inside and outside the company.

Industrial firms play a crucial role in building the economy. This study provides valuable data for those interested in SRD in Palestine and its effect on financial performance. It helps all parties make informed decisions and contributes to the Palestinian library, which lacks studies on this subject. This research aims to be a crucial addition to the literature on SRD.

Therefore, this study aims to show the importance of SRD and how it can influence the fiscal performance of industrial companies listed on the PEX.

Literature Review and Hypotheses Development

Theoretical Framework

Several theories explain the influence of SRD on fiscal performance, such as legitimacy and stakeholder theories.

The most relevant theory is the legitimacy theory, which supposes that the action of an institution is appropriate or proper in a social and organizational framework of values, definitions and criteria. Thus, according to Dowling and Pfeffer (1975), the company should comply with social standards and law provisions to promote confidence. If they do not respect these laws and standards, they may confront several problems and challenges and not obtain the bolster of society to stay in the market (Platonova et al., 2018).

Furthermore, Suchman (1995) defines legitimacy as a generalized conception that an organization is valid within a social system’s values and beliefs. This theory suggests that companies always try to confirm that they work within the standards and boundaries of their societies. In other words, the legal theory states that there is a social contract between the firm and the community in which it works (Guthrie et al., 2007).

Tilling (2004) argues that firms aim to balance social activities and their activities. If they can’t achieve this balance, their legitimacy is threatened. On the other hand, the failure of the organization to achieve an adequate level of legitimacy leads to negative consequences for the organization in the business environment. In this regard, Lindblom (1994) suggests that organizations’ quest to gain legitimacy is achieved by carrying out social activities and then disclosing them as a primary goal to improve performance. In this regard, Margolis and Walsh (2003) contend that disclosure of social responsibility can enhance company performance. As a result, their research concludes a positive relationship between SRD and financial performance.

The other theory is the stakeholder theory, which supposes that a firm must meet the stakeholders’ predictions and protect the interest of all of them, including employees, shareholders, lenders, and the general public at large, as the balance of the competing demands determines the performance of management (Ogden and Watson, 1999). The attribution between the emergence of social responsibility and the stakeholder theory states that achieving the firms’ economic goals (such as maximizing profit ) and non-economic goals related to the stakeholders’ benefits (such as firms` social performance) reflects the success of organizations ( Pirsch et al., 2007 ).

Stakeholder theory states managers have a fiduciary relationship with stakeholders rather than only fiduciary duties to shareholders. Stakeholder theory explains how companies appropriately deal with stakeholders related to social responsibility. According to this theory, the corporation cannot be devoid of its social responsibility. Therefore, social responsibility disclosure assists companies in maintaining stakeholder legitimacy and supporting them within the framework of policies and decision-making, which contributes to achieving the firm’s goals, growth of its performance, stability and continuity in the business environment (Prihatiningtias and Dayanti, 2014).

SRD and Financial Performance

Social responsibility clarifies that any entity, whether an organization or an individual, must act in society’s interests (Isa, 2012). It is defined as all the actions of organizations that comply with the community and are ethically in compliance with international standards of behavior to achieve integration in all the organization’s practices (Verboven, 2011). The European Commission defines social responsibility as uniting an organization’s environment and society with its internal operations (Barin Cruz and Avila Pedrozo, 2009). Also, social responsibility is identified as the firm’s adherence to participating in economic developments and improving the lifestyles of individuals and society through doing business well and seeking comprehensive growth in all activities that the organizations provide to all stakeholders (Tilling, 2004).

Social responsibility disclosure is to provide quantitative and non-quantitative financial data to the users in a complete, correct, appropriate, and non-misleading manner relating to everything the company does towards the internal and external environment in which it operates. It refers to this responsibility in its annual reports and includes responsibility towards the environment, employees, society, and improving services (Bag and Omrane, 2022). Besides, Kamaliah (2020) defines social responsibility disclosure as communicating the environmental and social influences of the firm’s economic activities on society.

SRD aligns with the rapid development in the accounting disclosure process, which meets stakeholders’ requirements and seeks to decrease the gap between social and legal dimensions and the organization’s actions with the distinction of disclosing information related to the organization’s role socially. It is also essential to raise competitiveness and reduce risks resulting from non-compliance in disclosures.

Furthermore, organizations strive to maintain a good reputation in their operating environment, preserve their image in the market, and improve their fiscal performance by benefiting from increasing SRD. Many studies have investigated the influence of SRD on financial performance.

Hoang and Tran (2021) found a positive and significant effect of SRD on the financial performance of construction firms in Vietnam from 2014 to 2018. The data were obtained from 27 listed firms. Likewise, Sang Tang My (2022) confirmed the positive impact of social responsibility disclosure on the financial performance measured by the return on assets of listed banks in Vietnam from 2015 to 2019. Also, Shukla and Geetika (2022) confirmed a significant impact between social responsibility expenditures and the financial performance of energy firms in India.

Nguyen et al. (2021) identified the significant variables influencing the SRD of listed firms in Vietnam and examined their influence on financial performance. The study analyzed the impact of firm size, industry sensitivity, and business age on SRD in 2019. The data were obtained from the companies’ reports. ROA was used as a proxy of financial performance. The results confirmed a significant and positive effect of the organization size and industry sensitivity on social responsibility disclosure. In contrast, firm age had an insignificant impact on social responsibility disclosure. Besides, SRD significantly positively impacted ROA.

Platonova et al. (2018) demonstrated a positive and significant effect of SRD on the financial performance of Islamic banks in Gulf Council Countries from 2000 to 2014. Likewise, Onuora (2022) estimated the impact of SRD on the performance of gas and oil corporations in Nigeria from 2016 to 2020. The results revealed that SRD significantly positively impacted firm performance. Wijaya et al. (2022) indicated that social responsibility disclosure significantly impacted financial performance, as measured by Tobin’s Q. The study sample included non-financial companies in Indonesia from 2015 to 2019. It also revealed that leverage negatively impacted the financial performance measured by Tobin’s Q, while firm size and age positively impacted it.

Jitaree (2015) investigated the influence of SRD on financial performance in Thailand. The study used data from 323 firms from 2009 to 2011. An improved index measured social responsibility disclosure, while ROA and Tobin’s Q evaluated financial performance. The finding revealed a positive and significant relationship between SRD with ROA and Tobin’s Q. Besides, firms’ characteristics, including firm size, leverage, and age, significantly impacted financial performance.

Eventually, Bussoli and Conte (2018) investigated the effect of SRD on financial performance measured by the ROA of 71 listed banks in Europe from 2011 to 2015. The results indicated that SRD positively affected return on assets. Also, bank size had a significant and positive impact on financial performance.

Margaretha and Rachmawati (2016) investigated the impact of SRD on financial performance in Indonesia from 2010 to 2013. Social responsibility disclosure was evaluated through indicators. On the other hand, ROA and Tobin’s Q were used to assess financial performance. The study found that disclosure of social responsibility towards the community positively and significantly impacted ROA and Tobin’s Q.

Oware and Mallikarjunappa (2019) found that SRD positively affected the financial performance of Indian companies from 2010 to 2017. Besides, the study found a negative relationship between financial leverage and financial performance measured by ROA.

Ellili and Nobanee (2023) found a low level of commitment to the sustainability disclosure of banking institutions in the UAE. The critical implication of this research was that the central bank in UAE had to issue instructions and guidelines to increase the involvement of banking institutions in sustainability disclosure and to decrease information asymmetry. Furthermore, the study found that SRD significantly influenced fiscal performance. Likewise, Bag and Omrane (2022) demonstrated a significant impact of SRD on the fiscal performance of 100 companies in India. Besides, these companies had the potential to achieve better financial performance through increasing social responsibility practices and activities.

A systematic analysis by Ali et al. (2024) highlights that firms engage in various activities to disclose their social responsibility efforts. These activities include reporting on environmental impact, community engagement programs, ethical sourcing practices, labor standards, and governance structures. Companies disclose these activities to enhance their reputation, improve financial performance, manage stakeholders effectively, and increase corporate accountability.

Wang et al. (2024) analyzed CSR in China. They found that firms with better CSR disclosure attract more attention in the media, and high CSR disclosure is positively related to corporate financial performance, partially mediated by media coverage. The strategic use of CSR disclosure to create economic benefits for firms may be of value to directors and investors who desire to comprehend the influence of CSR and media coverage on the firm fiscal performance.

Furthermore, Escamilla‐Solano et al. (2024) reported that the disclosure of social and environmental actions aligned with appropriate standards in the economic dimension can lead to an improvement in the FP of the company.

Activities of SRD

There are several activities of social responsibility disclosure, including:

SRD of activities towards society: It is the disclosure of all activities that the organization performs towards supporting infrastructure, considering traditions and customs, not violating general behavior and rules, supporting civil society organizations, supporting scientific and educational centers, supporting social activities, and making donations to associations. There are many benefits to interest and investing in these activities; the most important is achieving the community’s needs by the organization as the organization seeks to provide and adapt them through the previous programs and activities, and so the organization becomes a partner with the governments towards society when it adopts support for cultural, health, educational and charitable programs at an adequate level.

SRD of activities towards employees: It is the disclosure of what the company offers to its employees of an appropriate environment for work (Tuodolo, 2009), suitable and rewarding pensions, job promotions, training, and health insurance, in addition to vacations, transportation, housing, and housing benefits. The interest in these activities also contributes to providing job opportunities, reducing unemployment in society, and enhancing the organization’s competitiveness. It means that when the organization adopts this concept, a reciprocal relationship arises between social responsibility in promoting employees and considering the administrative and financial aspects through the commitment towards human resources, which leads to attracting highly skilled workers, gaining their loyalty, satisfying them, and positively affecting the organization’s performance.

SRD of activities towards developing services: The disclosure of everything the company performs to improve its products and services so that customers can meet their desires and satisfy them (Bag and Omrane, 2022). Besides, the organization strives to achieve the highest level of quality by meeting customers’ demands and providing services or products that meet their needs, which leads to improving the corporate reputation, attracting new capital resources and funds, attracting customers and maximizing the organization’s profitability and value (Sang Tang My, 2022).

SRD of activities towards the environment: It is the disclosure of what the company offers towards the environment, what it provides towards afforestation, gardens, and increasing green areas in the community in which it operates, and what it is doing towards reducing pollution of water, soil, and air.

Depending on the previous discussion and the empirical results, the main hypothesis is developed:

H1: Social responsibility disclosure significantly positively impacts the financial performance of industrial companies listed on the PEX.

Depending on this main hypothesis, the following specific hypotheses are developed :

H1.1: Social responsibility disclosure significantly positively impacts the return on assets of industrial companies listed on the PEX.

H1.2: Social responsibility disclosure significantly positively influences Tobin’s Q of industrial companies listed on the PEX.

Methodology

Study Data

The panel data are gathered from the annual reports of the industrial companies listed on the PEX from 2018 to 2022, and the deductive approach is used. Table 1 shows the industrial companies listed on the PEX.

The primary reason for selecting companies from the industrial sector is their significant role in the economy and their substantial contributions to industrial innovation and technological advancements, aligning closely with the study objectives to analyze and understand innovation practices and their impact within a significant economic sector.

Industrial sector companies generally maintain comprehensive records of their operational and financial data, which is crucial for the study’s detailed analysis. Access to reliable data sources is critical in ensuring the findings’ validity and robustness.

Focusing on a specific sector provides more in-depth insights and recommendations tailored to the unique challenges and opportunities within that sector. This specificity can enhance the practical applicability of the research findings.

Table 1: Industrial Companies Listed on the PEX

Data Collection

The study uses the yearly reports of the industrial companies listed on the PEX to obtain the variables’ values. The annual reports on each industrial company’s website are comprehensive sources for the required data as the industrial listed companies publish the accounting statements for all users.

Sampling Frame

This study aims to determine the impact of SRD on the financial performance of industrial companies listed on the PEX from 2018-2022. The study population includes all the firms listed on the PEX. The study sample is limited to the industrial firms listed on the PEX, whose financial reports are available during the study period. Table 2 illustrates the sampling frame of the study, including total observations.

Table 2: Sampling Frame of the Study Including Total Observations

Although the sample size of 13 companies might appear limited, it represents a significant portion of the key players within PEX. These companies were selected based on their market capitalization, innovation index, and overall influence in the industry.

To overcome the concerns about sample size, robust statistical techniques for smaller sample sizes are suggested, such as t-tests, Mann-Whitney U test, ruskal-Wallis test, Bootstrapping, Spearman’s rank correlation and Kendall’s tau correlation coefficient (Giner-Sorolla et al., 2024).

Study Models

The following two OLS regression models are developed to examine the impact of SRD on the financial performance of industrial companies listed on the PEX. The study uses two indicators to measure financial performance: the market indicator, represented by Tobin’s Q, and the accounting indicator, measured by Return on Assets (ROA).

ROAit: Return on Assets of the firm )i( in the year )t(.

TQit: Tobin’s Q of the firm )i( in the year )t(.

β0: Constant of the model.

SRDit: Social Responsibility Disclosure of the firm )i( in the year )t(.

SIZEit: Size of the firm )i( in the year )t(.

LEVit: Leverage of the firm )i( in the year )t(.

AGEit: Age of the firm )i( in the year )t(.

εit: Error term.

The following figure shows the study models:

Figure 1. Study Models

Study Variables

Social Responsibility Disclosure

SRD is the independent variable in this study. The study categorizes SRD into four main areas: activities towards society, the environment, employees, and developing services or products. The study uses five categories to measure each area, forming the basis of the index used to measure SRD (Barakat et al., 2015).

The content analysis method measures the disclosed items related to SRD. Besides, the study uses the dichotomous approach to calculate social responsibility disclosure by giving 1 for each disclosed item in the index and 0 for non-disclosed items. Then, the scores are summed up to get the total score of SRD for each firm as follows:

SRD = Total points of the SRD the firm has disclosed/ Total social responsibility disclosure index items.

Financial Performance

Financial performance is the dependent variable measured using the market indicator represented by Tobin’s Q and the accounting indicator measured by ROA. Table 3 shows the study variables and their measurements with their expected signs.

Table 3: Study Variables

And so, the models’ equations with the expected signs of the variables are as follows:

The study uses SPSS version 24 to analyze the obtained data by using the following tests and tools:

The study uses descriptive statistics: mean, standard deviation, maximum and minimum values. Descriptive statistics is part of statistics science that is concerned with providing summative data measures. The function of descriptive statistics is the description of all data without reaching the final results, which is considered one of the limitations of descriptive statistics. In other words, one of the limitations of descriptive statistics is presenting data in a simplified manner without providing understanding or results related to the interaction of variables in a set of data.

Normality test. The normality test determines whether data are modeled using a normal distribution. This study uses the Skewness and Kurtosis test to see if the study data are subject to a normal distribution. One of the limitations of this test is its outstanding suitability for nonparametric tests. In the literature, there are many techniques available to check the normality of data; the most well-known methods are the Shapiro-Wilk test, Kolmogorov-Smirnov test, skewness, kurtosis, histogram, P-P plot, and Q-Q plot (Mishra et al., 2019). The skewness and kurtosis test is relied on due to its suitability to the size and nature of the study sample. Generally, the literature provides guidance when selecting an appropriate test for normal data distribution.

Multicollinearity test. The study uses multiple regression analysis using the Pearson correlation coefficient to estimate the relationship between each pair of the investigated variables and determine if there is a multicollinearity problem among independent variables. It draws a line through the data of two variables to present their relationship. This linear relationship can be positive or negative. The difficulty distinguishing between independent and dependent variables is a main limitation of Pearson’s correlation. Therefore, Pearson correlation does not assign which variable is “the cause” and which is “the effect.” In the literature, the correlation value depends on the Pearson correlation, Variance Inflation Factor value, and tolerance value, which are the most used tests to examine the multicollinearity problem in the study model (Wondola et al., 2020). This study uses these two methods to investigate multicollinearity problems in the study model.

Homogeneity test. The homogeneity test is used in linear regression to examine the hypothesis of homogeneity of variance, which requires the availability of conditions to be applied. If one of these conditions is violated, inaccurate results will be obtained. The Breusch-Pagan Test is used in this study to ensure that this condition is met. In the literature, the White Test, Breusch-Pagan Test, and F Test are the most used for testing Heteroskedasticity in the regression model.

The study uses ordinary least squares (OLS) to estimate the effect of the independent variable, social responsibility disclosure, on the dependent variable, the fiscal performance of industrial firms listed on the PEX. Regression analysis is used to clarify the relationship between the variables through a set of mathematical equations such as the regression equation. This analysis type appeared by Francis Galton. One of the limitations of this analysis method is that it doesn’t consider the time factor in the multiple regression analysis models. In other words, it doesn’t work well for many real-world applications. In the literature, simple and multiple linear tests are relied on to determine the relationship between the variables. This study uses multiple linear tests to find the relationship between the SRD and fiscal performance in the presence of some controlling variables. This test is chosen due to its compatibility with the study data. Also, the sensitivity test for robustness is applied.

One-way analysis of variance (ANOVA) is used to determine if there are any statistically significant differences in the means of three or more independent groups. In the literature, several tests are used for the same purpose, such as mean, one sample t-test, independent samples t-test, partied sample t-test, and one-way ANOVA. This study uses ANOVA as an additional test to see if there is a statistically significant difference in the disclosure of social responsibility among industrial companies during the specified study period. This test was chosen to compare 13 companies. In general, this test is used for two or more samples.

Results

Descriptive Statistics

The following Table presents the descriptive statistics, including minimum value, maximum value, mean, and standard deviation of the variables (independent, dependent, and control variables).

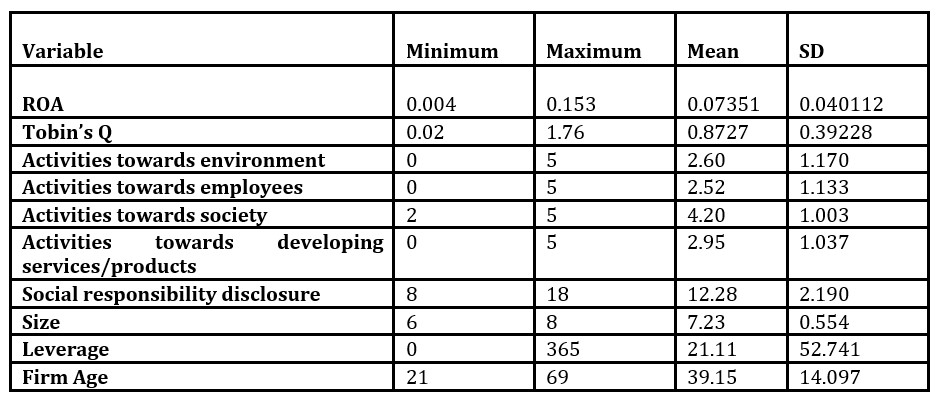

Table 4: Descriptive Statistics

Table (4) shows positive indicators for the variables of the study sample. Concerning financial performance measured by ROA and Tobin’s Q, it is clear that the mean for it is 0.07351 and 0.8727, respectively. Besides, descriptive statistics show that the companies’ disclosures regarding all dimensions of SRD are good, as the mean confirms that the study sample companies disclose most of the elements regarding the dimensions of social responsibility. In general, companies’ SRD is also suitable as its mean amounted to (12.28) items out of the total number of (20), which means that companies disclose social responsibility well.

Normality Test

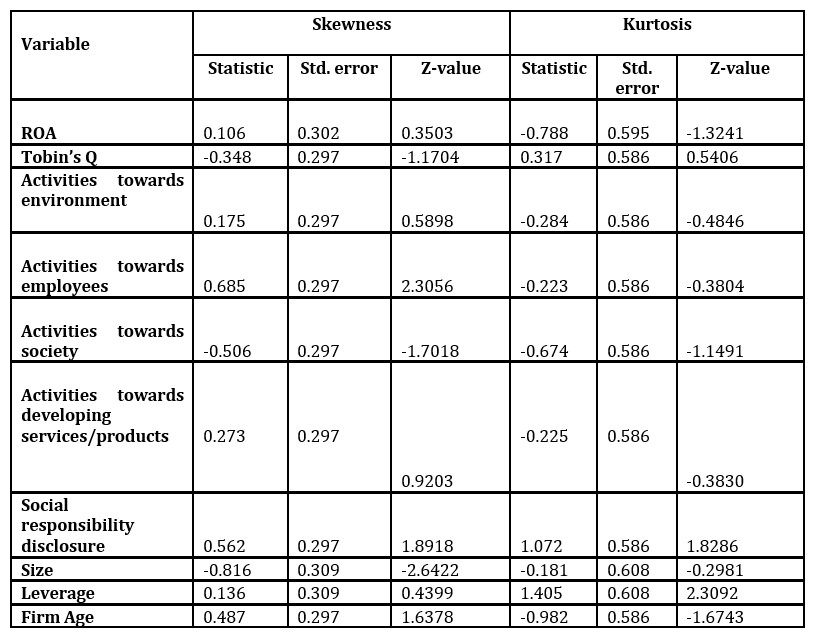

The normal distribution of the data is one of the conditions for the validity of the regression model. The data’s lack of a normal distribution may cause a loss of the ability of the correlation to interpret the phenomenon under study. This study uses the Skewness and Kurtosis test to check how near the data are to the normal distribution. The test’s null hypothesis is accepted when the absolute z value of skewness and kurtosis is less than or equal to 3.29, indicating that the data are subject to a normal distribution (Kim, 2013). The following Table presents the results of this test.

Table 5: Skewness and Kurtosis Test

The Z-value for all the study variables is less than (3.29). Therefore, it is concluded that the study variables are subject to a normal distribution and are valid for the regression analysis model.

Homogeneity Test

This study uses the Breusch-Pagan Test to examine the Heteroscedasticity in the linear regression analysis. The following Table shows the results.

Table 6: Results of the Breusch-Pagan Test

The Table above shows that the Sig is less than (0.05), indicating no heteroscedasticity problem in regression study models.

Multicollinearity

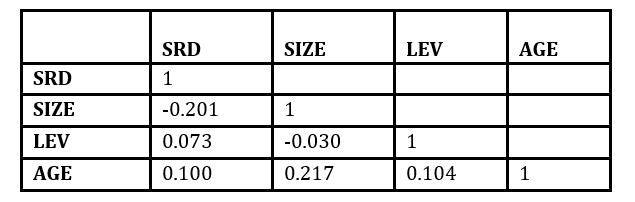

Multicollinearity is defined as the existence of a linear relationship between the independent variables. It contradicts one of the assumptions of the multiple linear regression model. This assumption is that the independent variables must be linearly independent, meaning no relationship exists between them. Table (7) presents the regression analysis using the Pearson correlation coefficient to show the collinearity among independent variables.

Table 7: Pearson Correlation

The correlation coefficients between the independent variables are less than 60%, indicating that the regression analysis models in this study are free from the problem of multicollinearity.

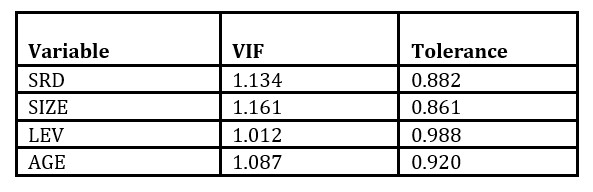

Furthermore, the Value Inflation Factor and Tolerance are used to examine the multicollinearity problem in the study models, as shown in Table (8):

Table 8: Results of VIF and Tolerance

As shown in the above Table, the values of VIF for study variables are all less than (10), and the values of Tolerance for all study variables are above (0.05). Therefore, it is concluded there is no multicollinearity problem in the study models.

Regression results

This section presents the results of the regression analysis to investigate the relationship between SRD and financial performance. The study uses least squares analysis (OLS) with two models to examine this relationship.

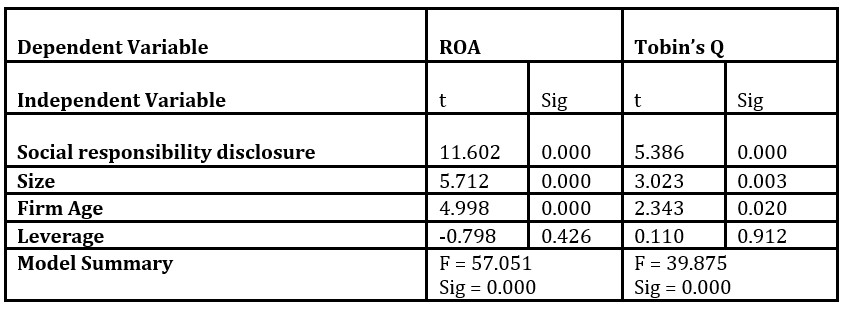

Table 9: Regression Results

The above Table shows the results of the regression analysis. These results confirm a significant positive relationship between SRD and the company’s financial performance using ROA (t = 11.602, Sig = 0.000) and Tobin’s Q (t = 5.386, Sig = 0.000). The regression also shows a significant positive relationship between size and fiscal performance using ROA (t = 5.712, Sig = 0.00) and Tobin’s Q (t =3.023, Sig = 0.003). Furthermore, firm age significantly positively impacts financial performance using ROA (t = 4.998, Sig = 0.000) and Tobin’s Q (t = 2.343, Sig = 0.020). However, the regression indicates an insignificant relationship between leverage and financial performance using ROA (t = -0.798, Sig = 0.426) and Tobin’s Q (t = 0.110, Sig = 0.912).

Sensitivity Test for Robustness

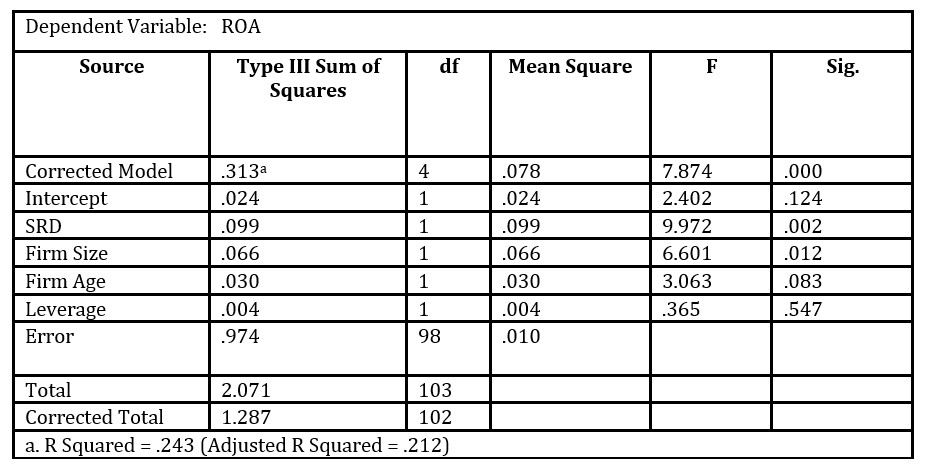

Sensitivity analysis assesses the results’ robustness by applying the analysis under various plausible assumptions about the procedures, models, or information that deviate from those used in the preliminary study as indicated in advance. Table (10) shows the results of the sensitivity test for robustness for (ROA):

Table 10: Sensitivity Test for Robustness (ROA)

As shown in the Table above, using the sensitivity test for robustness, all results of OLS regression are confirmed, which gives confidence in the study results.

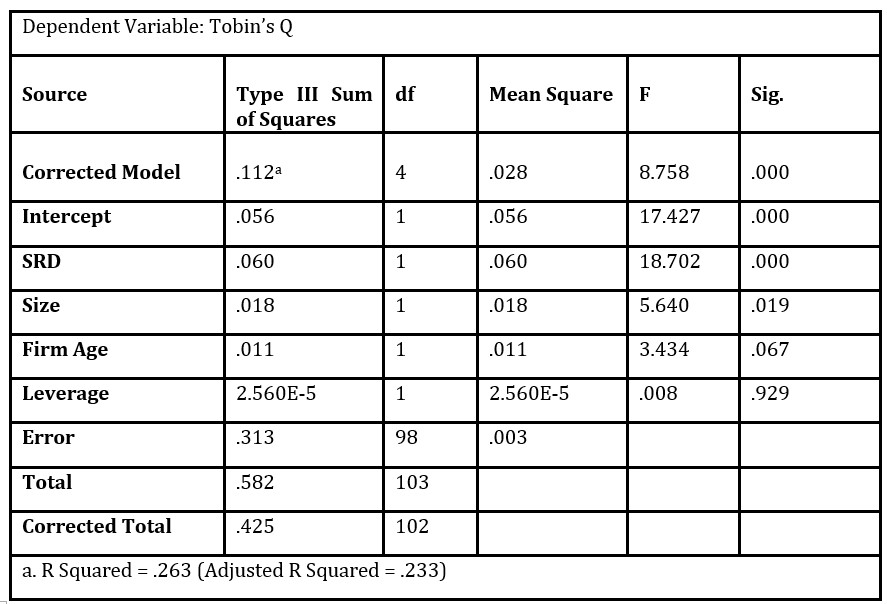

Table 11: Sensitivity Test for Robustness (Tobin’s Q)

According to Table (11), using the sensitivity test for robustness shows that all results of OLS regression are confirmed, which gives confidence in the study results.

One-way ANOVA

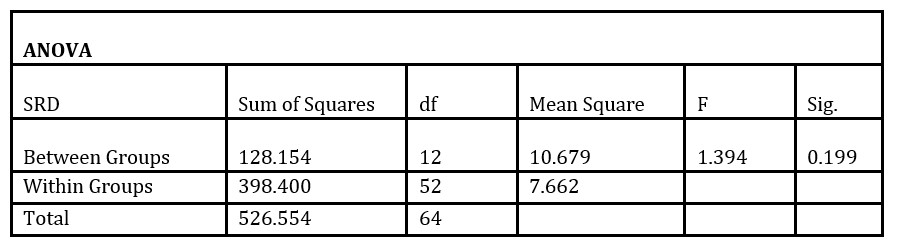

ANOVA is used to investigate if there are statistically significant differences in social responsibility disclosure. The following Table shows the results :

Table 12: ANOVA Results

Table (12) shows that (F = 1.394, Sig = 0.199) indicates no statistically significant differences in SRD among Palestinian industrial companies during the study period. Thus, the study concludes that the industrial companies listed on the PEX disclose social responsibility at the same level.

Discussion

The study explores the relationship between SRD and financial performance among industrial companies listed on the PEX. The findings reveal a significant positive correlation between SRD and financial performance, measured by ROA and Tobin’s Q. Regression analysis demonstrates that SRD strongly influences financial outcomes (ROA: t = 11.602, Sig = 0.000; Tobin’s Q: t = 5.386, Sig = 0.000), indicating that companies engaged in SRD activities experience enhanced financial performance.

Descriptive statistics show that these companies exhibit high levels of SRD, particularly in societal activities, with an average SRD score of 12.28 out of 20, emphasizing their commitment to social responsibility. This transparency likely boosts corporate reputation and stakeholder trust, improving financial performance.

These findings corroborate existing literature on the positive impact of SRD on financial performance. They extend prior research by demonstrating these effects within the Palestinian industrial sector, underscoring the broad applicability of SRD benefits across various contexts and industries.

For practitioners, the study offers robust evidence supporting the integration of SRD into corporate strategies. It suggests that industrial firms should prioritize and enhance their SRD practices, focusing on comprehensive reporting across societal, environmental, employee, and service domains. Such practices meet regulatory requirements and bolster corporate reputation and investor confidence, contributing to improved financial performance.

The findings have significant implications for policymakers advocating for frameworks promoting SRD adoption. Regulatory incentives could encourage transparency and accountability in SRD, ensuring companies contribute positively to social and environmental sustainability. Policy initiatives might also reward firms excelling in SRD practices, further motivating widespread adoption.

While providing valuable insights, the study suggests avenues for future research. It proposes exploring SRD impacts across different sectors and regions to enhance generalizability. Longitudinal studies could assess the enduring effects of SRD on financial performance, while detailed analyses could pinpoint which specific SRD components yield the most significant financial benefits.

Conclusion

SRD has become a vital topic from the viewpoint of researchers and specialists in social, economic, and environmental sciences, especially after the economic recession in 1938. Furthermore, expanding the financial and business environment motivates many sectors to improve their SRD and adopt it. On the other hand, financial performance is considered one of the most critical topics in financial accounting as it is a general measure of the firm’s fiscal position during a specific period.

However, the lack of awareness of some institutions of the necessity of SRD and the return they can obtain is the primary motive for this study, which aims to examine the impact of SRD on the financial performance of the industrial companies listed on the PEX.

The study’s results indicate that SRD significantly positively impacts financial performance, as measured by ROA. This result is consistent with the findings of Hoang and Tran (2021). Also, the results show that SRD significantly positively impacts fiscal performance, as measured by Tobin’s Q. This result is consistent with the findings of Margaretha and Rachmawati (2016). Besides, the results indicate no statistically significant differences in SRD among Palestinian industrial companies, concluding that these companies disclose social responsibility at the same level.

These results of the study are explained by the fact that SRD increases the community’s confidence in the strength of the companies and the sincerity of their transactions, thus increasing the desire to financially deal and transact with them, which supports the companies’ stability, growth, competitiveness, sustainability and maximizes the companies’ financial indicators such as return on assets which will be reflected in increasing their financial performance.

Also, SRD maximizes the disclosure of more detailed data about the company, its operations, and the effects of those operations on society and the company. Besides, it increases the transparency of the financial reports, which will meet the needs of the stakeholders and the users of financial statements. This will maintain existing customers, attract new customers, develop the company’s reputation, maximize its value, increase its market share, and maximize its market indicators, especially those related to Tobin’s Q, reflected in improving its fiscal performance.

The study is limited to one sector, the industrial sector, as this sector has distinctive features. So, the findings can’t be generalized for all listed companies on the PEX. On the other hand, this study relates to Palestine as one of the developing countries; therefore, the results can’t be generalized to the developed countries.

This study has several implications for firms, decision-makers, regulators, and researchers concerned with increasing SRD. Thus, it is necessary to hold conferences and workshops to motivate the firms’ management to participate in social responsibility, disclose it, and inform them about the benefits that can be obtained, which will be reflected in their financial performance. On the other hand, it is essential to enact legislation and laws related to increasing SRD due to the importance of this information to the stakeholders, including shareholders, partners, suppliers, distributors, customers, employees and society. Thus, the regulators should put clear policies and legislation in place to obligate companies to expand their social responsibility disclosure in their published reports since it is an effective tool for achieving political, economic, social, and environmental stability for the business community. This research is an extension for researchers to conduct future research in this field, such as conducting several similar studies on different sectors in the PEX or investigating similar studies using other financial performance indicators to measure the impact of SRD on them.

References

Ali, W., Bekiros, S., Hussain, N., Khan, S. A. and Nguyen, D. K. (2024),’ Determinants and consequences of corporate social responsibility disclosure: A survey of extant literature,’ Journal of Economic Surveys, 38, 793-822.

Bag, S., and Omrane, A. (2022), ‘Corporate social responsibility and its overall effects on financial performance: Empirical evidence from Indian companies,’Journal of African Business, 23(1), 264-280.

Barakat, F. S., López Pérez, M. V., and Rodríguez Ariza, L. (2015), ‘Corporate social responsibility disclosure (CSRD) determinants of listed companies in Palestine (PXE) and Jordan (ASE),’Review of Managerial Science, 9, 681-702.

Barin Cruz, L., and Avila Pedrozo, E. (2009), ‘Corporate social responsibility and green management: Relation between headquarters and subsidiary in multinational corporations,’ Management Decision, 47(7), 1174-1199.

Bussoli, C., and Conte, D. (2018),’ The Virtuous Circle” Between Corporate Social Performance and Corporate Financial Performance in the European Banking Sector,’International Journal of Business Administration, 9(2), 80-92.

Dowling, J., and Pfeffer, J. (1975), ‘Organizational legitimacy: Social values and organizational behavior,’Pacific sociological review, 18(1), 122-136.

Ellili, N. O. D., & Nobanee, H. (2023), ‘Impact of economic, environmental, and corporate social responsibility reporting on financial performance of UAE banks,’ Environment, Development and Sustainability, 25(5), 3967-3983.

Escamilla‐Solano, S., Fernández‐Portillo, A., Sánchez‐Escobedo, M. C., and Orden‐Cruz, C. (2024), ‘Corporate social responsibility disclosure: Mediating effects of the economic dimension on firm performance,’ Corporate Social Responsibility and Environmental Management, 31(1), 709-718.

Giner-Sorolla, R., Montoya, A. K., Reifman, A., Carpenter, T., Lewis Jr, N. A., Aberson, C. L., … and Soderberg, C. (2024),’ Power to detect what? Considerations for planning and evaluating sample size,’ Personality and Social Psychology Review, 28(3), 276-301.

Guthrie, J., Cuganesan, S., and Ward, L. (2007),’ Legitimacy theory: A story of reporting social and environmental matters within the Australian food and beverage industry,’ In Asia Pacific Interdisciplinary Research in Accounting Conference (5th: 2007) (pp. 1-35). APIRA 2007 Organising Committee.

Hoang, B. A., & Tran, T. T. H. (2021, October),’ Corporate social responsibility disclosure and financial performance of construction enterprises: Evidence from Vietnam,’ In CIGOS 2021, Emerging Technologies and Applications for Green Infrastructure: Proceedings of the 6th International Conference on Geotechnics, Civil Engineering and Structures (pp. 1505-1514). Singapore: Springer Nature Singapore.

Isa, S. M. (2012) ‘Corporate social responsibility: what can we learn from the stakeholders? ,’ Procedia-Social and Behavioral Sciences, 65, 327-337.

Jitaree, W. (2015) ‘Corporate social responsibility disclosure and financial performance: Evidence from Thailand.’

(2020) ‘Disclosure of corporate social responsibility (CSR) and its implications on company value as a result of the impact of corporate governance and profitability,’ Int’l JL and Mgmt., 62, 339.

Kim, H. Y. (2013) ‘Statistical notes for clinical researchers: assessing normal distribution (2) using skewness and kurtosis,’ Restorative dentistry and endodontics, 38(1), 52-54.

Lindblom, C. K. (1994) ‘The implications of organizational legitimacy for corporate social performance and disclosure,’ In Critical Perspectives on Accounting Conference, New York, 1994.

Margaretha, F., and Rachmawati, B. (2016),’ The effect of corporate social responsibility on the financial performance of the company in Indonesia,’ OIDA International Journal of Sustainable Development, 9(04), 11-18.

Margolis, J. D., and Walsh, J. P. (2003), ‘Misery loves companies: Rethinking social initiatives by business,’ Administrative science quarterly, 48(2), 268-305.

Mishra, P., Pandey, C. M., Singh, U., Gupta, A., Sahu, C., and Keshri, A. (2019),’ Descriptive statistics and normality tests for statistical data,’Annals of cardiac anaesthesia, 22(1), 67-72.

Nguyen, T. H., Vu, Q. T., Nguyen, D. M., & Le, H. L. (2021),’ Factors influencing corporate social responsibility disclosure and its impact on financial performance: the case of Vietnam,’ Sustainability, 13(15), 8197.

Ogden, S., and Watson, R. (1999), ‘Corporate performance and stakeholder management: Balancing shareholder and customer interests in the UK privatized water industry,’ Academy of Management Journal, 42(5), 526-538.

Onuora, J. K. J.’ Evaluation of the Impact of Corporate Social Responsibility Cost on Financial Performance of Non-Financial Firms in Nigeria,’

Oware, K. M., and Mallikarjunappa, T. (2019), ‘Corporate social responsibility investment, third-party assurance and firm performance in India: The moderating effect of financial leverage,’ South Asian Journal of Business Studies, 8(3), 303-324.

Pirsch, J., Gupta, S., and Grau, S. L. (2007),’ A framework for understanding corporate social responsibility programs as a continuum: An exploratory study,’ Journal of business ethics, 70, 125-140.

Platonova, E., Asutay, M., Dixon, R., & Mohammad, S. (2018),’ The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector,’ Journal of business ethics, 151, 451-471.

Prihatiningtias, Y. W., and Dayanti, N. (2014), ‘Corporate Social Responsibility Disclosure and Firm Financial Performance in Mining and Natural Resources Industry,’ The International Journal of Accounting and Business Society, 22(1).

Sang Tang My, H. T. M. (2022) ‘Relationship between corporate social responsibility and bank performance of listed banks in Vietnam,’ Journal of Hunan University Natural Sciences, 49(1).

Shukla, A., and Geetika. (2022), ‘Impact of Corporate Social Responsibility on Financial Performance of Energy Firms in India,’ International Journal of Business Governance and Ethics, 16(1), 88-105.

Suchman, M. C. (1995) ‘Managing legitimacy: Strategic and institutional approaches,’ Academy of management review, 20(3), 571-610.

Tilling, M. V. (2004) ‘Some thoughts on legitimacy theory in social and environmental accounting,’ Social and Environmental Accountability Journal, 24(2), 3-7.

Tuodolo, F. (2009) ‘Corporate social responsibility: Between civil society and the oil industry in the developing world,’ ACME: An International Journal for Critical Geographies, 8(3), 530-541.

Verboven, H. (2011) ‘Communicating CSR and Business Identity in the Chemical Industry Through Mission Slogans,’ Business Communication Quarterly, 74(4), 415-431.

Wang, L., Li, Y., and Li, X. (2024), ‘Corporate social responsibility disclosure, media coverage and financial performance: An empirical analysis in the chinese context,’ The Singapore Economic Review, 69(01), 251-268.

Wijaya, L. I., Herlambang, A., and Evans, B. (2022), ‘Corporate social responsibility and leverage level on high profile industries at Indonesian stock exchange of 2015-2019 period,’ Media Ekonomi dan Manajemen, 37(1), 1-16.

Wondola, D. W., Aulele, S. N., and Lembang, F. K. (2020, February),’ Partial least square (PLS) method of addressing multicollinearity problems in multiple linear regressions (case studies: cost of electricity bills and factors affecting it),’ In Journal of Physics: Conference Series (Vol. 1463, No. 1, p. 012006). IOP Publishing.