Sofia Mateo-La Rosa1, Odaliz Ferreyra-Mejia1, Elizabeth Mayuri-Ramos1 and Franklin Cordova-Buiza2

1 Business Faculty, Universidad Privada del Norte, Lima, Peru

2 Research, Innovation and Social Responsibility Department, Universidad Privada del Norte, Lima, Peru

Volume 2024,

Article ID 955925,

IBIMA Business Review,

16 pages,

DOI: https://doi.org/10.5171/2024.955925

Received date: 21 November 2023; Accepted date: 28 January 2024; Published date: 20 June 2024

Cite this Article as:

Sofia Mateo-La Rosa, Odaliz Ferreyra-Mejia, Elizabeth Mayuri-Ramos and Franklin Cordova-Buiza (2024)," User Loyalty through Technological Means in the Financial Sector: A Systematic Review ", IBIMA Business Review, Vol. 2024 (2024), Article ID 955925,

https://doi.org/10.5171/2024. 955925

Technology has been the best ally for the financial sector because it allows the development of new processes to build user loyalty. The objective of this systematic review was to determine what has been written in the scientific literature on user loyalty through technological means in the financial sector within the years 2018 – 2023. On the other hand, this review was conducted under the PRISMA method strategy, the databases used were: Scopus, Science Direct, ProQuest and Dialnet, from which 25 scientific articles were systematized; and it was obtained as a result that the banking sector has greater adaptability in technological functions to build user loyalty, unlike cooperatives and savings banks that use the same method but at a slower pace; it was also identified that technological tools facilitate the task of knowing the customer and thus achieve satisfaction, such as advertising in social networks, the incorporation of easily accessible applications, chatbots and mainly the registration of their data in the cloud; finally, it is evident that digitalization has positioned itself positively in the financial sector. It is concluded, by confirming the influence of technological strategies on customer loyalty in the banking sector, technological tools are being modernized according to the characteristics of the markets.

Keywords: Financial marketing, digitalization, financial loyalty, digital media, financial system.

Introduction

In recent years, technology has been constantly evolving and is causing a significant effect on all aspects of human activity, this has been reaffirmed with the arrival of the COVID-19 pandemic, all sectors are implementing measures to be able to reestablish their economic stability and technology cooperating as storage, advertising, etc., assuming that the world is being digitized day by day and people are part of this change (Boufounou et al., 2022; Gomez-Pino et al., 2023; Machuca Vílchez et al., 2023). Currently, technological media have a partial role since they make consumer loyalty feasible by connecting the entity with the customer from wherever they are and at whatever time, but at the same time they give them the power to publicly express their liking or disliking for the entity; the financial sector uses technological media as allies for their marketing strategies, achieving greater reach (Basem Masud, 2019; Orellana-Treviños et al., 2023; Mayuri-Ramos et al., 2023).

In this sense, entities have been adapting to the consumer’s lifestyle since the new market is now looking for security, efficiency and mainly time savings; with more emphasis when the increase in the number of people infected by COVID-19 was lost control of, given that interactions and physical contact were restricted (Medina -Quintero et al., 2022; Salazar-Rebaza et al., 2022). In this context, although the scope of services became one of the primary factors for public preference, the importance of the service experience cannot be underestimated, since it is considered a very influential factor in customer loyalty and satisfaction, highlighting that they are responsible for mobilizing the country’s economy with all the financial operations they perform on a daily basis (Dehnert & Schumann, 2022; Cordova-Buiza et al., 2022; Arce-Cruz et al., 2023).

The importance of this systematic review lies in the influence that digital financial marketing has on the customer-entity relationship; although it is true that marketing focuses on customer satisfaction, it cannot fail to take into account the activities carried out by the competition; likewise, it must take into consideration that the information provided about financial products will have an effect on the behavior and purchase decision; for this reason, Enamul et al. (2018) state that the principle of transparency and symmetry of information must prevail, assuming that creating trust in the user contributes positively to building the image and reputation of a company. Therefore, this research aims to identify what has been written in the scientific literature on user loyalty through technological means in the financial sector between the years 2018-2023?

Loyalty in the banking sector is an essential process for the solidity and validity of the company, defined as the existence of a good relationship between the company and consumers with the certainty that if they have acquired a financial product once, they will tend to do it again and that company will be their first choice; but its importance is not only limited to ensuring future sales but to the recommendations and positive comments shared by users, taking the role of “advertising” from their own experience and it is assumed to be a priority for the financial sector as it is considered one of the most competitive. The investments made by companies are aimed at attracting potential customers, but this does not ensure their loyalty but will depend on the differentiated quality between one institution and another (Naranjo & Vásquez, 2021; Balbin-Romero et al., 2022).

The use of technological means implies the migration of the financial business from the physical to the digital environment, from contracting in branches to online contracting, from face-to-face procedures to the use of applications such as mobile banking, from waiting in long lines to the “token” as confirmation of the transaction from the comfort of your home. The boom of these means is unstoppable since it would be very close to a consolidation stage considering that their use is rapidly becoming the public’s favorite means of transaction (Reboiro, 2020). In this line, the acceptance of the public has been good, however, there is a small percentage that continues to opt for traditional media and still resort to face-to-face and physical interaction, refusing to be part of the digitalization, but this situation is a consequence of the insecurity they feel about digital channels (B., Ly & R., Ly, 2022; Aguayo-Villodas et al., 2024; Hernandez-Padilla et al., 2023).

One of the benefits of digitizing the financial sector is the ease of being able to stand out from the competition since nowadays options can be compared immediately either based on the interest rate, solvency, quality of services, term, practicality, promotions, etc. Daily, people perform operations through mobile applications and the failure of these can be known from anywhere in the world. Currently, the information travels through the Internet in a matter of seconds having as intermediaries the users; assuming this, the reputation and soundness of the entity would be affected (Baena, 2022; Mesta-Cabrejos et al., 2023). In relation to the above, it can be stated that user trust in banking terms differs from trust in emotional terms; emotional trust firmly believes in personal interaction and unquestionably doubts the security that the advancement of technology can provide, and, on the other hand, in the financial sphere, trust is based mainly on functional components such as the skills and capacity of the counterparty, based on this, they also choose the entity with which they will go hand in hand so that both parties benefit partially (Pelgander et al., 2022).

Gilsanz (2021) states that every day there are more customers who use digital devices and media for constant investment advice or to obtain unified information on their global position; the digital environment is overtaking the physical environment as the main channel of attention, which allows the entity to have greater access to the information of its consumers so that the products they offer are more tailored to their needs, their services are personalized and the company becomes more attractive to the customer. We all demand a good service and with much more reason if it is our money.

This is why greater attention must be paid to the protection of financial consumers in the use of digital channels, since their personal information must be treated with care and its use should only be for transactions authorized by the owners, assuming that they are fully aware of their rights and obligations regulated by the law; in this sense, each entity has the obligation to train and instruct the public on the use of the technology they are implementing in each process, either by publishing tutorials on the Internet, through their commercials and social networks, providing advice within the agencies, etc., so that they cooperate with the security protection schemes (Anaya, 2020; Pelgander et al., 2022).

All companies that comprise the financial sector have to ensure the privacy and security of their consumers to encourage a sense of trust. It is also evident that the acquisition of knowledge about technology by the public positively influences the acceptance of digitization of the financial sector. The digital capability with the ability to ask and answer questions empowers companies to both understand the customer in a timely manner and to have an advantage in competition within the market (Adiguzel et al., a2022). Today, millennials are facilitating this task because they are on the lookout for cutting-edge technology and are driving the transformation of the financial industry landscape (Hashem, 2022).

Sang-Bong and Ki-Chang (2023) point out that there is a difference in the sales growth rate between companies that use digital marketing and non-digitized companies, because the latter do not have enough reach with the public and continue to risk using traditional media as advertising, knowing that digital media are largely the favorites of customers; the recurrence of the same ad every time we turn on a device manages to arouse curiosity in the user that if his experience was good, he will return. In that sense, Agarwal et al. (2022) express that customer experience and satisfaction, as well as security, have a significant impact on their loyalty to the institution; if one of these aspects fails or is provided in a different proportion, the result will still be negative for the company.

The objective of this systematic review was to determine the most important thing that has been written in the scientific literature about user loyalty through technological means in the financial sector within the years 2018 – 2023.

Methodology

The PRISMA method used for the systematic review works through a flow that supports a correct systematization and choice of scientific articles that seeks to answer the problem posed under its own pre-established criteria (Moher et al., 2009).

Databases that contributed to the development of the problem and objective of the systematic review were identified; the main criterion taken into account was the scientific journals since they provide accurate information on the research topic, and, therefore, it was decided to work with four databases where outstanding articles were found that followed the line of research of the work and provided us with scientific reading material; in addition, they provided more information results compared to other databases considered and subsequently discarded.

The search engines used to obtain accurate and reliable information were: Scopus, which is a database of abstracts of scientific articles, citations and journals in technology, medicine and social sciences; ProQuest, which provides access and resources for libraries and researchers to manage information; WOS, which provides access to multiple databases that provide relevant information on different academic disciplines; and Sciencie Direct, which is a digital platform and database where publications with scientific, social, and technological criteria can be consulted.

A time range between 2018 and 2023 was used, thus providing up-to-date research articles with relevant information for the systematic review. The filters provided the sensitization to ideally execute the selection of the databases and to successfully complete the extraction process of scientific articles. The strategy used in the search for scientific articles in the database was through keywords, coincidence with the titles or in the summary, also called abstract, of which the search criteria were different for each database, and it was possible to search for articles in English as well as in Spanish. In the Scopus database, the term “financial marketing” was assigned, while, in the ProQuest database, “loyalty” and “financial system” and “digital media” were used; on the other hand, in Science Direct, “financial loyalty” was used, and finally, in WOS, “financial system” and “digital media” were used. In addition, the Boolean connector “And” was used for each search as a whole, in order to obtain results that were coherent and congruent with the topic and respond to the problem of the systematic review.

The choice of articles was based on criteria previously analyzed to solve the problem of the systematic review; in addition, we worked with the Prisma diagram model that contributed to the selection of required articles; the terms of inclusion considered for the systematic review were scientific articles, excluding theses, books, conferences or dissertations; in addition, the articles had to be open access; another criterion that was taken into account was the time range that was managed between 2018 and 2023, in addition to being open access. Regarding exclusion criteria, it was defined that the systematic review follows a clear and concise line of research, therefore, articles that were not related in the abstract were discarded, in addition to duplicate scientific articles.

Results

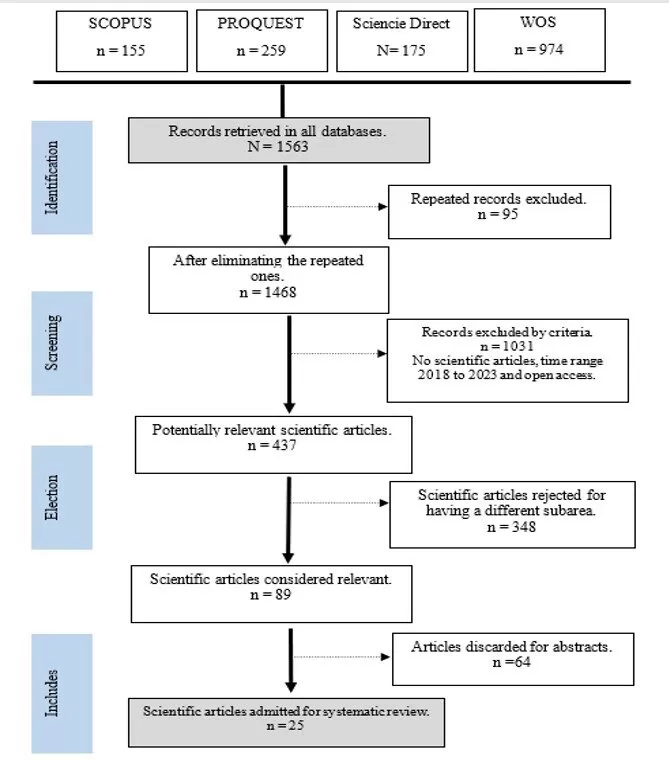

Through the Prisma diagram, 30 scientific articles were selected that are suitable for the systematic review; in the first section, the number of articles in the chosen databases was identified, which was a total of 1563, then the duplicate articles were discarded, which were 95 articles, leaving a total of 1468 articles in general; in the next step, the inclusion criteria were considered in which it was requested that they be scientific articles of open access and that they are in a period of time between 2018 and 2023, therefore, 1031 articles that did not meet the inclusion criteria were excluded, obtaining an overall of 437 articles. Continuing with the systematization process, the exclusion criterion was applied in which 348 articles that were not related to the line of research were discarded, resulting in a total of 89 articles. Finally, considering that there should be a certain number of articles for the present systematic review, 64 articles were excluded due to summaries with low impact of the topic, thus 25 articles were selected, which will be part of the research.

Figure 1: Prism Diagram Flow – Article Selection

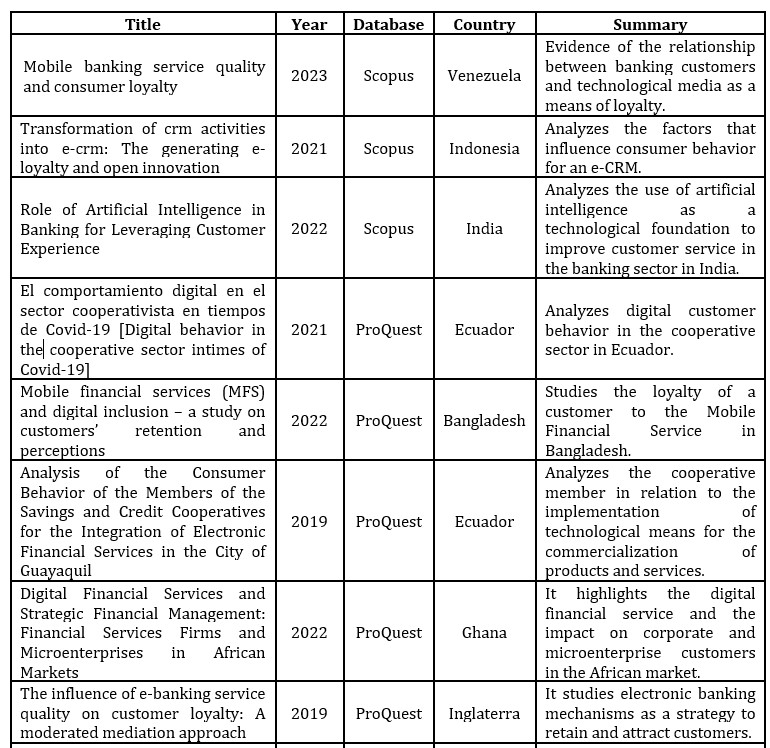

Expanding on the information regarding the articles selected for this systematic review, the criteria used will be presented, such as year, database, abstracts, title, and name of the journal. The intention of the results is to verify in detail the fulfillment of the criteria exposed in the methodology section.

Table 1: Systematization of articles

Analysis of the number of articles found per database and year

The articles selected for the present systematic review are based on the most recognized databases, therefore, they will be visualized through the different criteria that have been established for the analysis and to demonstrate the contributions to the present research.

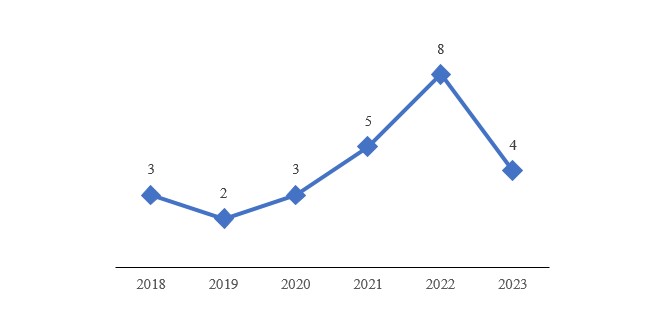

In the research, it is important to verify if the selected topic is found in the chosen databases; for this, it is necessary to show how many articles per year have been published in the time range of the present research, therefore, it was obtained that the number of published articles has been increasing as the years go by, being in 2022 the year with the highest number of published articles (8), and so far in 2023 there are 4 published articles (Figure 2).

Figure 2: Articles published by year

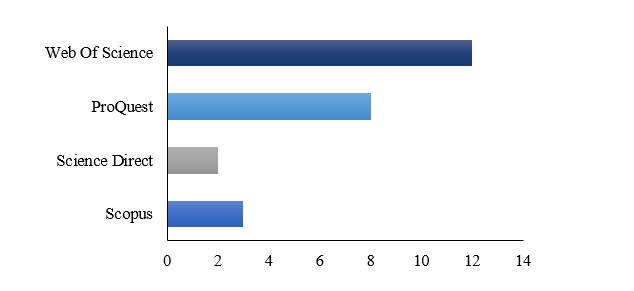

The number of articles found in each database was also analyzed, with Web of Science having 12 articles, followed by ProQuest with 8 published articles, Scopus with 3 articles and Science Direct with 2 articles (Figure 3).

Figure 3: Articles published in each database

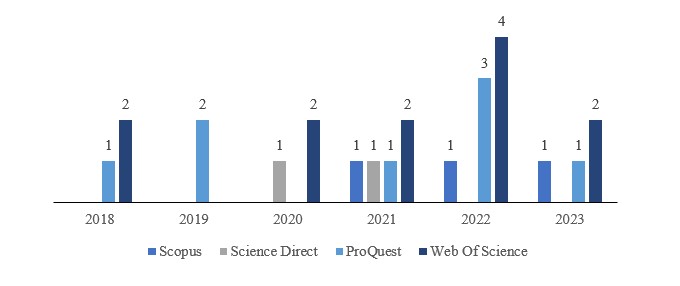

The constancy of the information regarding the topic in the databases is a valid point to analyze, therefore, it is shown that Web of Science and ProQuest are the databases that manage to maintain articles related to the research topic between the years 2018 to 2023, while Scopus has a constancy from 2021 and Science Direct was only found in the years 2020 and 2021 (Figure 4).

Figure 4: Articles published by year and database

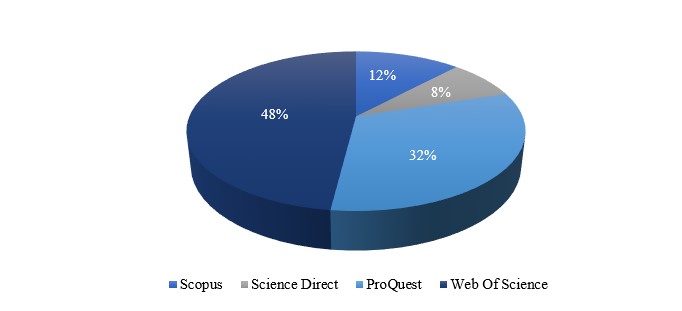

Another criterion found within is the database that predominates in the research: Web of Science comprises 48% of the 25 articles selected, ProQuest 32%, Scopus 12% and Science Direct 8% (Figure 5).

Figure 5: Percentage of articles per database

Analysis of the number of articles found per country

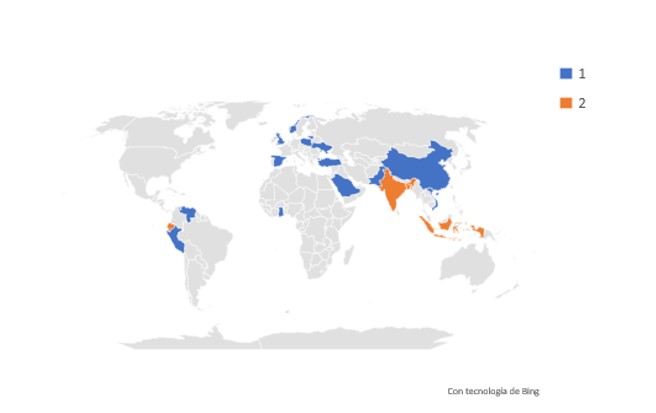

Different articles were viewed worldwide in order to find out if the topic is of global interest: 2 articles were found in the countries of Indonesia, India, Ecuador, Bangladesh, England, while 1 article was found in Peru, Venezuela, Ecuador, Ghana, Kosovo, Turkey, Vietnam, Lithuania, Ukraine, Saudi Arabia, China, Poland, Norway, Spain, Pakistan and the United Kingdom (Figure 6).

Figure 6: Number of articles published by country

Discussion

The analysis of what has been written regarding the loyalty of users through technology gives us an idea of the process of digitalizing financial transactions for the most part, with the aim of speeding up time, avoiding physical contact and prioritizing user convenience; however, there are still gaps that do not allow this process to be more accessible, the basic lack of knowledge about the operation of a cell phone, the lack of implementation of certain technologies in different emerging sectors and the absence of financial education, are the factors considered important to meet the objective of digitizing society and also to make it more loyal (Afroze & Rista, 2022).

Le (2021) disagrees with the above stating that digital media also have factors that can affect the process of technological integration in the traditional financial system, thus giving access to technological finance or better known as Fintech, which is a star-up that offers financial services of a digital nature; in the case of Peru, they have the support of the Superintendence of Banking and Insurance; on the other hand, it is analyzed whether customers have a positive behavior towards these new financing modalities, the highest participation was found in the Covid-19 pandemic where physical contact and agglomerations were forbidden, in addition to the need to obtain financing or secure and reliable income.

On the other hand, they also include more specific characteristics such as the image of the organization, the customer experience and the performance of the product or service provided to the consumer. All factors are part of the study conducted to know what motivates the digital consumer to be loyal to a financial institution, in addition to knowing the perception through which different data collection tools contribute to further improving the digital and also face-to-face service, as they are related in terms of user loyalty (Akhgari et al., 2018). In the same line, Baena-Graciá (2022) disagrees and determines that the emotional factor influences user loyalty more than a visual perception; an application that is effective, fast, and functional has a greater chance of loyalty, since we are in the digital era.

The advance of technology not only stands out in the financial system, but also in other sectors that are part of the economy of a country, which is why technological innovation in the rural sector is established as a point of exception; the relationship is based on the development of the sector that generates an opportunity for financial institutions to create loyalty and access to financing tools through technology (Liu et al., 2021). Another point of exception that is established is the level of risk of technological means; the client will always have a level of distrust since he/she watches over the interest of his/her finances and information, that is why it is analyzed through models, the impact that this risk exerts on client loyalty, resulting in a high and fundamental relationship between client and technological risk (Beqaj & Baca, 2022).

The financial system is broad, therefore the information is also broad, but the same study or research is not conducted for all sectors that make up the financial market; coincidentally, Paskevicius and Keliuotyte-Staniuleniene (2018) indicate that studies on technological innovation specifically of capital markets are scarce, because there is no model or system established to measure the impact of different variables, in this case technological innovation; consequently, there is no information with which to build customer loyalty or opt as new financing tools and attract customers.

The banking sector is one of the best known and most commercialized. Oruna et al. (2023); Shankar and Jebarajakirthy (2019); Taka and Bayarcelik (2023) agree on the need to employ indicators and strategies to measure user loyalty and satisfaction, in addition to having trained personnel to be able to guide people who do not find it easy to learn how to use digital tools, since it influences the perception, experience, and impact on the final results when verifying profitability or other aspects of measurement that are not purely monetary, on the other hand, also indicate that although there is currently a large participation of young people who dominate the use of technology, we must prioritize adaptability and create a culture of inclusion for all factors contribute to the purpose of loyalty.

Elliot et al. (2022) and Guzmán (2019) agree that the cooperative and microfinance sector is also affected by the development of technological innovations and should be used as a tool to build member and client loyalty, and that the behavior, need, and access to technology should be evaluated. They also mention the importance of having statistical models as a measurement system to study the main characteristics that determine the behavior of the member, who would be the eventual customer and continue to be part of the cooperative. If you do not have a measurement system and do not adapt to change despite being a small sector, it can be reflected in the process of loyalty and satisfaction, hence the growth of the sector itself, which is why the perception of this specific case is through the institution and also through the cooperative member.

Artificial intelligence is an important factor in the technological innovation process. Bhattacharya and Sinha (2022) and Gasiorkiewicz et al. (2020) agree that the use of artificial intelligence is an operational opportunity for financial institutions and avoids the implementation of costly programs that will be used only for one purpose, however, AI has different functionalities including the study of customers for loyalty and measuring the levels of this criterion, since customers seek personalized attention. In addition, it seeks to replace traditional transactions by digital ones, such as payment of services, bank transfers, payment of fees, digital statement of account and currency exchange. The operations mentioned above are the most used by customers and performing them from their mobiles generates a point in favor by the value of time and generates customer loyalty.

The evaluation criteria are fundamental to determine the loyalty study and this is confirmed by Amoroso et al. (2023); Iqbal et al. (2021); Manyanga et al. (2022) and Rashid et al. (2020) who mention that the determination of variables allows obtaining a clear and concise study to build customer loyalty, therefore, customer experience and service quality are determining factors for the customer to achieve customer loyalty, since an optimal attention and a good financial product or service generate a positive impact of the service and are related to customer satisfaction. This challenge is used through digital media, where there is no physical and direct contact with the customer, on the contrary, an artificial attention is generated and must be taken into account for the customer, the didactic use and easy use, so that the experience is better or equal to a face-to-face attention.

On the other hand, Algamdi et al. (2021), Farmania et al. (2021), and Ramirez et al. (2020) indicate that the incorporation of programs and software helps the study of customer behavior. CRM and SERVQUAL are optimal mechanisms to measure the relationship of the loyalty process, also through the program are estimated and designed strategies to achieve the goal, in addition to having a feedback after executing some tactic with the customer and obtaining opportunities for improvement to meet the goal.

Fernández et al. (2022) and Kurnia et al. (2023) agree that financial inclusion is an important factor and that it is related to customer loyalty, since when the loyalty management process begins, different digital tools are used to incorporate the customer; this inclusion occurs mostly in remote populations or to microentrepreneurs who do not trust, however, it is where technological means are incorporated to attract, include, and build customer loyalty.

The subject of the review is based on the customer’s perspective and their behavior, however, the vision from the institution also contributes to the achievement of loyalty. Managers indicate that analyzing strategies, having an optimal working environment, and a staff trained in all digital aspects contribute to the customer experience to continue with the entity, in addition to the fact that the digital impact that banks have had on the financial system provides a clear vision of the future (Mbama et al., 2018). On the other hand, Manzhura et al. (2022) indicate that customer loyalty through digital media not only applies to the financial sector but to all others, in order to reduce the gaps for customers or citizens and achieve loyalty, in general, to the country’s economy.

Conclusion

The objective of the research was to determine the most important thing that has been written in the scientific literature on user loyalty through technological means in the financial sector within the years 2018 – 2023; from there, twelve articles point out the increase in revenue for companies in the financial sector that have been integrating technology in their operations. The recurrence of advertisements in digital media manages to capture the user’s attention, inviting them to try the service and/or product offered. In ten of the articles analyzed, it is highlighted that the key to the relationship between technological media and consumer loyalty is the ease with which you can collect customer data, which consequently allows knowing and customizing the service, managing to meet their needs in the best way.

Likewise, three of the twenty-five articles that focused on banking point out that it is the sector that has been best integrating cutting-edge technology, taking advantage of its advances to be ever closer to its customers wherever they may be. The results of this systematic review confirm the relationship between technological means and loyalty. It was observed that currently these means provide the financial sector with a greater reach to the public and influence user behavior, since people opt for services that take less time, but with the same quality and evidence of this are the digital transactions that are used daily through a mobile device

References

Adiguzel, Z., Aslan, B. and Sonmez, F. (2022), ‘The bank’s effect on digital capability and knowledge acquisition within the performance and digital native’s perception of mobile marketing. Revista de Estudios Empresariales, 22(2), 292-313.

Afroze, D. and Rista, F. (2022), ‘Mobile financial services (MFS) and digital inclusion – a study on customers retention and perceptions,’ Qualitative Research in Financial Markets, 14(5), 768-785.

Agarwal, S., Malik, P. and Gautam, S. (2022), ‘Analysis of Customer Satisfaction and the Customer Experience in Digital Payments: A Meta-Analysis Review,’ International Journal of Business Science and Applied Management, 18(1), 1-17.

Aguayo-Villodas, B.A., Reyes-Gomez, S.E., Cordova-Buiza, F., and Auccahuasi, W. (2024),‘Consumer Interaction in the Digital Environment: A Systematic Review,’ Lecture Notes in Networks and Systems, 774, 71-80.

Akhgari, M., Bruning, E., Finlay, J. and Bruning, N. (2018), ‘Image, performance, attitudes, trust, and loyalty in financial services,’ The International Journal of Bank Marketing, 36(4), 744-763.

Algamdi, A., Brika, S., Laamari, I. and Chergu, K. (2021), ‘CRM system and potential customer loyalty trends: Some evidence of customer engagement,’ International Journal of Advanced and Applied Sciences, 8(5), 44-52.

Amoroso, D., Lim, R., Lei, J. and Saxena, A. (2023), ‘A Study of Satisfaction and Loyalty for Continuance Intention of Mobile Wallet in India,’ International Journal of E- Adoption, 15(1).

Anaya-Saade, C. (2020), ‘Protección del consumidor financiero en Colombia, en el uso de canales electrónicos bancarios [Financial consumer protection in Colombia, in the use of electronic banking channels].,’Vniversitas, 69, 1-12.

Arce-Cruz, G. O., Valencia-Mayuri, J. C., Jimenez-Rivera, W. O., Rivera, W. M. J. and Cordova-Buiza, F. (2023), ‘Financial Literacy and its Relationship to the Indebtedness of a Bank’s Customers,’ In ECKM 2023 24th European Conference on Knowledge Management, 1, 67-73.

Baena-Graciá, V. (2022), ‘Vinculación emocional hacia la marca y marketing digital como estrategia de éxito en tiempos de Covid-19 [Emotional brand bonding and digital marketing as a strategy for success in times of Covid-19],’ Revista de Marketing y Publicidad, 6, 35-36.

Basem-Masud, A. (2019), ‘Religiosity and customer trust in financial services marketing relationships,’ Journal of Financial Services Marketing, 24(1-2), 31-43.

Beqaj, B. and Baca, G. (2022), ‘Consumer evaluations of e-services: A perceived risk perception in financial institutions,’ Ekonomski Vjesnik, 35(1), 113-123.

Bhattacharya, C. and Sinha, M. (2022), ‘Role of Artificial Intelligence in Banking for Leveraging Customer Experience,’ Australian Accounting, Business and Finance Journal, 16(5), 89-105.

Boufounou, P., Mavroudi, M., Toudas, K. and Georgakopoulos, G. (2022), ‘Digital Transformation of the Greek Banking Sector in the COVID Era,’ Sustainability, 14, 11855.

Cordova-Buiza, F. and Paredes-Vasquez, R.D.P. (2022), ‘Loyalty Strategies in Latin American SMEs: a Systematic Review of Scientific Literature Between 2012 and 2021,’ IEEE International Professional Communication Conference, 2022-July, 298-302.

Dehnert, M. and Schumann, J. (2022), ‘Uncovering the digitalization impact on consumer decision – making for cheking accounts in banking,’ Electroniks Markets, 32(3), 1503–1528.

Elliot, E., Cavazos, C. and Ngugi, B. (2022), ‘Digital financial services and strategic financial management: Financial services firms and microenterprises in African markets,’ Sustainability, 14(24).

Enamul-Joque, M., Hazrul-Nik Hashim, N. and Bin-Azmi, M. (2018), ‘Moderating effects of marketing communication and financial consideration on customer attitude and intention to purchase Islamic banking products: A conceptual framework,’ Journal of Islamic Marketing, 9(4), 799-822.

Farmania, A., Elsyah, D. and Touri, M. (2021), ‘Transformation of crm activities into e-crm: The generating e loyalty and open innovation,’ Journal of Open Innovation: Technology, Market and Compleity, 7(109), 2.

Fernández, B., González, G., Sierra, O. and Ortega, E. (2022), ‘Financial Inclusion as Enabler for Innovation in Banking,’ Foresight and STI Governance, 16(3), 95-105.

Gasiorkiewicz, L., Monkiewicz, J. and Monkiewicz, M. (2020), ‘Technology-driven innovations in financial services: The rise of alternative finance,’ Foundations of Management, 12(1).

Gilsanz-Muñoz, M. (2021), ‘El impacto de la inteligencia artificial en la sociedad y su aplicación en el sector financiero [The impact of artificial intelligence on society and its application in the financial sector],’ Revista Diecisiete, 12(4), 167-174.

Gomez-Pino, L. B., Huertas-Vilca, K. S., Maguiña-Rivero, O. F. and Cordova-Buiza, F. (2023), ‘Customer loyalty and administrative management of e-commerce in the telecommunications sector in Latin America,’ Problems and Perspectives in Management, 21(3), 330-342.

Guzmán, E. (2019), ‘Analysis of the consumer behavior of the members of the savings and credit cooperatives for the integration of electronic financial services in the city of Guayaquil,’ International Journal of Business and Administrative Studies, 5(5), 303-311.

Hashem-Abdullah, A. (2022), ‘Determinants of digital banking adoption in the Kingdom of Saudi Arabia: A technology acceptance model approach,’ Digital Business, 2(2).

Hernandez-Padilla, J. D., Donayre-Gallo, A., Cordova-Buiza, F. and Auccahuasi, W. (2023, September), ‘Innovative Digital Marketing Strategies to Increase Demand in a Hotel Company,’ In ECIE 2023 18th European Conference on Innovation and Entrepreneurship, 1, 365-374.

Iqbal, K., Munawar, H., Inam, H. and Qayyum, S. (2022), ‘Promoting Customer Loyalty and Satisfaction in Financial Institutions through Technology Integration: The Roles of Service Quality, Awareness, and Perceptions,’ Sustainability, 13(23).

Kurnia, S., Budiarti, I., Waluya, D. and Onegina, V. (2023), ‘Digitalization and informal MSME digital financial inlusion for MSME development in the formal economy,’ Journal of Eastern European and Central Asian Research, 10(1), 9-19.

Le, M. (2021), ‘Examining factors that boost intention and loyalty to use Fintech post-COVID-19 lockdown as a new normal behavior,’ Heliyon, 7(8).

Liu, Y., Ji, D., Zhang, L., An, J. and Sun, W. (2021), ‘Rural Financial Development Impacts on Agricultural Technology Innovation: Evidence from China,’ International Journal of environmental research and public health, 18(3).

Ly, B. and Ly, R. (2022), ‘Internet banking adoption under Technology Acceptance Model-Evidence from Cambodian users,’ Computers in Human Behavior Reports, 7(1).

Machuca Vílchez, J. A., Ramos Cavero, M. J. and Cordova Buiza, F. (2023), ‘Knowledge management in financial education in Peruvian government programs focused on women: Progress and challenges,’ Knowledge and Performance Management, 7(1), 1-14.

Manyanga, W., Makanyeza, C. and Muranda, Z. (2022), ‘The effect of customer experience, customer satisfaction and word of mouth intention on customer loyalty: The moderating role of consumer demographics,’ Cogent Business & Management, 9(1).

Manzhura, O., Pochenchuk, G. and Kraus, N. (2022), ‘Innovative changes in financial and tax systems in the conditions of digital transformation,’ Baltic Journal of Economic Studies, 8(1), 94-102.

Mayuri-Ramos, E., Almazan-Rivera, E. S., Jesus-Cardenas, M. A. and Cordova-Buiza, F. (2023), ‘Innovative Strategies to Maximize Customer Loyalty in the Banking System: A Systematic Review,’ In 18thEuropean Conference on Innovation and Entrepreneurship, 18(1), 587-595.

Mbama, C., Ezepue, P., Alboul, L. and Beer, M. (2018), ‘Digital banking, customer experience and financial performance: UK bank managers’ perceptions,’ Journal of Research in Interactive Marketing, 12(4), 432-451.

Medina-Quintero, J., Rios-Echevarría O. and Ortiz-Rodríguez, F. (2022), ‘Confianza y calidad de la información para la satisfacción y lealtad del cliente en el e-Banking con el uso del teléfono celular [Trust and quality of information for customer satisfaction and loyalty in e-Banking using cell phones],’ Contaduría y administración, 67(1), 283-304.

Mesta-Cabrejos, V. F., Huertas-Vilca, K. S., Wong-Aitken, H. G. and Cordova-Buiza, F. (2023), ‘Corporate social responsibility in the banking sector: a focus on Latin America and the Caribbean,’ Humanities and Social Sciences Communications, 10(1), no 668.

Moher, D. (2009), ‘Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement,’ Annals of Internal Medicine, 151(4), 264.

Naranjo, E. and Vásquez, Mario. (2021), ‘Financial marketing as a tool for customer loyalty in national banking,’ Revista Minerva, 2(6), 43-49.

Orellana-Treviños, E. L., Perez-Iglesias, M. J., Barsheva, C., Gonzales-Paucarcaja, F. C. B. and Olavarria-Benavides, H. L. (2023), ‘Relationship Marketing as an Innovative Strategy for Customer Loyalty in Customized Arrangements Companies,’ In 18th European Conference on Innovation and Entrepreneurship, 2, 694-703.

Oruna, A., Oruna, M., Aranguren, P. and Sánchez, J. (2023), ‘Mobile banking service quality and consumer loyalty,’ Revista Venezolana de Gerencia, 28(102), 855-871.

Paskevicius, A. and Keliuotyte-Staniuleniene, G. (2018), ‘The evaluation of the impact of financial technologies innovations on CEECs capital markets,’ Marketing and Management of Innovations, 3, 241-252.

Pelgander, L., Öberg, C. and Barkenäs, L. (2022), ‘Trust and the sharing economy,’ Digital business, 2(2), 100048.

Ramírez, E., Maguina, M. and Huerta, R. (2020), ‘Attitude, satisfaction, and loyalty of customers in Municipal Savings Banks of Perú,’ Retos-Revista de Ciencias de la Administración y Economía, 10(20), 329-342.

Rashid, H., Nurunnabi, M., Rahman, M. and Masud, A. (2020), ‘Exploring the Relationship between Customer Loyalty and Financial Performance of Banks: Customer Open Innovation Perspective,’ Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 108.

Reboiro-Gutierrez, P. (2020), ‘Digitalización del Sector Financiero [Digitalization of the Financial Sector],’ Boletín de Estudios Económicos, 75(229), 53-77.

Salazar-Rebaza, C., Aguilar-Sotelo, F., Zegarra-Alva, M. and Cordova-Buiza, F. (2022), ‘Financing in the alternative securities market: Economic and financial impact on SMEs,’ Investment Management and Financial Innovations, 19 (2), 1-13.

Sang-Bong, An and Ki-Chang, Yoon. (2023), ‘Los efectos de los cambios en el desempeño financiero en la creación de valor en la transformación digital: una comparación con las empresas no digitalizadas [The effects of changes in financial performance on value creation in digital transformation: a comparison with non-digitized firms.],’ Sustainability, 15(3).

Shankar, A. and Jebarajakirthy, C. (2019), ‘The influence of e-banking service quality on customer loyalty: A moderated mediation approach,’ The International Journal of Bank Marketing, 37(5), 1119-1142.

Taka, M. and Bayarcelik, E. (2023), ‘Sustainable digital transformation of financial institutions,’ Business & Management Studies: An International Journal, 11(1), 253-269.