Fiorella Nicole, MORALES-CHAVEZ, Joberth, VARGAS-FIGUEROA, Melva, LINARES-GUERRERO and Sindulfo Javier DIAZ-ANGULO

Graduate, School of Business, Universidad Privada del Norte, Peru

Volume 2025,

Article ID 256237,

IBIMA Business Review,

11 pages,

DOI: https://doi.org/10.5171/2025.256237

Received date: 26 August 2024; Accepted date: 2 December 2024; Published date: 2 January 2025

Academic Editor: Nelly Rosario Moreno-Leyva

Cite this Article as:

Fiorella Nicole, MORALES-CHAVEZ, Joberth, VARGAS-FIGUEROA, Melva, LINARES-GUERRERO and Sindulfo Javier DIAZ-ANGULO (2025)," Tax Evasion in the Grocery Sector: Effects on Tax Collections in Peru", IBIMA Business Review, Vol. 2025 (2025), Article ID 256237, https://doi.org/10.5171/2025.256237

The objective of the research was to determine the impact of tax evasion generated by grocery wholesalers in Peru on tax collection, since there are some gaps in the literature that addresses these issues in local markets concerning wholesale companies from medium to large companies. The study sample consisted of 25 local companies; the technique used was the survey, using the questionnaire as a data collection instrument; this instrument was validated by expert judgment and reliability analysis. The study is of basic type, quantitative approach, descriptive-correlational level and non-experimental design. Obtaining results, that wholesale grocery merchants have low tax knowledge due to lack of information and knowledge about tax payments by intentionally failing to pay the taxes due as taxpayers, obtaining a negative relationship of -0.060 of Spearman’s Rho, demonstrating that tax evasion by merchants has a negative effect on tax collection. It is concluded that there is a moderate negative relationship between the variable tax evasion and the variable tax collection, which means that the higher the cases of tax evasion, the lower the tax collection that is used for public services for the citizens.

Currently, tax evasion has impacted and continues to generate less tax collection in a way that harms state revenues, with a negative effect on tax resources, which are considered one of the largest revenue generating sources in a country, since they contribute to the achievement of the objectives set by governments to safeguard the benefits of society. On the other hand, tax evasion is presented as a phenomenon that, in addition to generating a loss in government revenues, also deteriorates the entire social and economic structure, undermining the legitimacy of governments. Thus, Pedroni et al. (2022) set out to identify the microeconomic determinants of corporate tax evasion in emerging economies: the case of Argentina, for which they identified a multi-causal phenomenon, in which taxes lose their importance thanks to these determinants, such as corruption, regulation, bureaucracy, quality of public services, informality of the sector and political instability. To speak of an informal economy is to speak of private companies and companies that are not registered with the different regulatory bodies, as well as some companies that file their tax returns with a lower level of sales, thus reducing their tax burden.

Showing some statistics, in 2016 the value added tax (VAT) was the main creator of tax revenue in most countries in the world; this increase in the rate of VAT evasion in the period 2000-2014 is high: Uruguay in 2012 obtained 13.4% and Peru in 2001 obtained 49.5% and in Argentina the values were between 19.8% and 34.8% in the period 2007-2011; these recent estimates indicate the level of tax evasion. Around 46% – 52% are legal entities in Argentina World Bank statistics (2018), this is among the thirty countries with the highest tax evasion worldwide in addition to other factors that increase the effective tax pressure in Argentina motivating the crime of evasion. Due to this bad practice, the world loses around $400 billion dollars in taxes every year (State of Tax Justice, 2020).

In the Peruvian reality, tax evasion is a serious problem, to the extent that there is no tax awareness, the structure of the tax system is not adequate, thus affecting tax collection, with a harmful effect on society. It is worth mentioning that tax evasion occurs in all economic sectors, the trade sector being a notorious example of evasion. In this sense, the present research focused on this sector specifically in wholesale traders, in which there is evasion at all levels of the buying and selling process. In this sense, Carranza and Colmenares de Zavala (2021) mention that for Peru this is not a strange issue. It was analyzed that tax evasion in the country, informality and little information on tax culture on the part of taxpayers, generates that the country collects 52.8% in its totality; this means that it is far below the maximum possible collection according to its current economic situation. This results in a very low average for Latin America as a whole by OECD standards. 41.5% of this revenue is used to pay the salaries of public officials and 35.2% is used to finance infrastructure and 25.8% to finance social programs. Therefore, we must try to raise awareness among all Peruvians, whether natural or legal persons, of the importance of paying taxes on time and being responsible for their taxes in order to contribute to the economic development of the country.

Within this broad national sector, there is a representative reality in the city of Cajamarca located in northern Peru, since the lack of tax culture among taxpayers generates a situation known as tax evasion or tax resistance for most taxpayers. The merchants of the food market located in the center of the city are among these taxpayers who evade their taxes by not issuing their customers any payment vouchers or issue vouchers that do not generate tax credit for their tax return; it was also perceived that the sales made are not declared in their entirety.

It is specified that the funds collected are used inadequately; therefore, basic needs are not covered, which causes taxpayers to avoid paying taxes, fail to comply with their obligations and show their unwillingness to pay taxes properly. Patiño, Mendoza, Quintanilla and Diaz (2019) point out in their research that citizens perceive that the tax system is not adequate and that the government is unfair with the rates imposed since these are too high, therefore there is a great inability to pay; likewise, they think that much of the money ends up in the pockets of corrupt politicians or their friends and relatives being a cause for tax evasion.

Tax evasion involves key components such as tax culture, which Quispe and Arellano (2020) mention that it is the main cause of evasion, which results mainly in the deterioration of the tax collection system and a high increase in evasion and fraud, as well as citizens’ lack of knowledge to comply with their formal duties and abide by the different tax laws. In turn, tax culture is closely linked to three aspects: first, lack of knowledge of regulations, understood as a set of rules that limit the taxing power, constitutes the framework of the tax activity, such as the principle of legality, contributive capacity; second, ethical conduct, tax education cannot be reduced to a learning experience that teaches people to meet the demands of the tax system, it must be an education aimed at cultural change and a re-evaluation of ethics within social groups (Vargas, et al… 2023); third, tax responsibility, understood as a set of rules that limit the tax power, constitutes the framework of the tax activity, such as the principle of legality, contributive capacity, etc. (Vargas, et al., 2023); fourth, tax responsibility identifies that taxes cause citizens to cooperate in solidarity with the government in order to provide it with the necessary resources.

Another component of tax evasion is Informality, and Acosta and Capa (2023) state it as a serious problem that occurs worldwide, where workers or entrepreneurs opt for this option in order to evade tax payments; in addition, 85% of informal employees end up with precarious and undignified jobs, the percentage of labor informality in the year 2021 was 76.8%, which is a very high percentage in the last 11 years, resulting in almost 700 thousand employees entering the informal sector. From here it is understood that informality is present in several activities such as: Registration in the tax administration; it mentions that people do not want to formalize their businesses due to the costs of the formalization process that the state requires from all entrepreneurs which causes demotivation in formalizing their business; Ambulatory trade, whose activity is developed mainly among certain sectors of the Peruvian population that have few economic resources, little knowledge of commercial law and lack of defined physical spaces to carry out commercial activities; Economic instability, in which the presence of informal jobs causes a reduction in tax collection, with the result that the high level of evasion reduces tax revenues and therefore the state’s capacity for public investment such as education, roads and health, harming the performance of economic agents.

As a last component, tax fraud which, according to Zevallos (2018), causes corruption by companies that take advantage of the defective control and inspection by the Tax Administration – SUNAT, this directly affects the tax fund since they act with deception, cheating, among other ways, to evade the total of their tax payments and thus obtain a particular benefit that does not correspond to them. Within tax fraud is observed: Omission of payment, it is identified that some businessmen totally or partially hide their assets, income or revenues, in order to reduce or eliminate the payment of taxes and make it look like a sufficient payment (Merino, 2004); Concealment of income, some companies file returns that include fictitious facts or operations or false amounts, omitting totally or partially the income, rents or assets of any kind that must be considered in the determination of the tax debt.Omission of the Sworn declaration is the non-compliance by the companies in their monthly or annual sworn declaration in which the tax to be paid is determined (Lira, et al,. 2023).

On the other hand, tax collection is the process through which the tax authorities collect taxes from taxpayers, where Cáceres and Soto (2017) mention that tax collection is of great importance because the more it is collected, the better the investment of the state throughout the country can be improved, resulting in better sustainable development at the national level. Within the collection, tax revenues have been considered in the first place, understood as the total amount of monetary resources received by the public sector through taxes and has the following indicators such as: Value Added Tax, which is a tax that the state does not compensate directly to taxpayers; Contributions is a tax that generates income whose obligation arises from the execution of public works or services (Pérez & Fol, 2022).

Secondly, tax pressure which Carhuapoma and Perez (2023) indicate that it varies according to the type of economy in each country but can bring advantages or disadvantages to be high and low; when there is a higher tax pressure, taxpayers seek ways to evade it, however, in other developed countries, taxpayers translate this high level of pressure as better opportunities for the country. This dimension has the following indicators: Tax revenues, which represent the total amount of monetary resources received by the public sector through taxes, tributes, fees or other types of contributions; Gross domestic product, which represents the value of final goods and services produced in an area in a given period (Colombia, 2012).

Finally, the Laffer Curve which, according to Otárola and Robledo (2019), is a tool which shows the relationship between tax revenues collected by the government and tax rates paid by citizens. Through this econometric comparative static analysis, we see a microeconomic specification which has the following indicators: Tax rate, which identifies the form of the economy of a government as it affects the fact that the income depends on the taxes that are collected; Tax collection, this process identifies how the government incorporates the collection of taxes, ensuring that contributions are made in accordance with the stipulations of the tax code.

It is necessary to present some background information that contextualizes and presents results and important contributions regarding tax evasion and the relationship it generates in tax collection, which becomes relevant information to initiate this study. It should be noted that the background information is presented at the international, national, and local levels.

In the international context, Tixi (2016), in his study “Tax evasion and income tax collection” the objective was to determine the incidence of evasion in tax collection; the methodology was quantitative approach, descriptive and hypothetical-deductive scope and the sample consisted of 397 individuals. The results show that more than 30% of the cases are not registered with the tax administration and therefore do not have a taxpayer identification number (NIT) and that 60% of the taxpayers are informally registered in the sales records.In this way, he concludes that one of the problems is the bad image of the state in the use of resources, the little tax orientation to people with business, which has repercussions in the lower payment of their tax obligations.

The objective of the research “Tax evasion and its effect on the economic development of the country” by López (2016) was to identify and describe tax evasion and the serious consequences that affect the economic development of the country. It is a bibliographic and descriptive research at the study level, the result of which shows that 70% of Peru’s economy is informal and only 30% formal, which translates into less income to the state for taxes due to the high level of business informality.. Concluding that it is possible to reduce tax evasion with state policies and taxpayers becoming aware of the importance of paying taxes.

Solis and Valverde (2018), in their thesis entitled “Tax Evasion and its impact on the State Budget of Ecuador in 2014 – 2018”, analyzed the levels of tax revenue for the general budget of the State. The research was of mixed approach, with non-experimental design in addition to longitudinal cut and obtaining results of growth from 20.39% in 2018 to 39.37% for 2019 due to public policies. Concluding that the increase in collection is due to cultural actions and state policies where taxpayers become more aware citizens.

In the national context, there is Carrillo (2023), “Tax culture and its impact on the fulfillment of tax obligations of Mypes commercial enterprises in Piura, 2021”, whose objective was to determine the relationship between tax culture and the responsibility of tax obligations in Mypes commercial enterprises. This quantitative research, non-experimental design, cross-sectional and a descriptive correlational level applied to a sample of 35 owners of Mypes commercial enterprises, obtained a result of considerable positive relationship, its significance level is 0, 000 and a 0.579 correlation coefficient. It is concluded that the higher the level of tax culture within an organization, the higher tax compliance will increase.

The thesis “La cultura y la evasión tributaria en las pequeñas empresas de lima metropolitana 2020”, by Pineda (2022), had as objective to know the link between tax culture and the causes of tax evasion. It is a bibliographic and descriptive research at the study level, the result of which shows that 70% of the Peruvian economy is informal and only 30% is formal, which translates into less income for the state in terms of taxes collected due to the high level of business informality.It is concluded that SUNAT does not correctly inform about tax regulations, but also taxpayers did not take due importance to their tax payments.

Cornejo (2017), in his research “Tax evasion and its impact on tax collection in Peru”, determined how tax evasion influences tax collection in Peru in a way that harms public investment and therefore the common welfare of citizens. This research is basic, explanatory level, non-experimental-transversal design and quantitative approach. It obtained a result of a negative relationship with a significance of less than 0.05 (p-value), the estimate of the tax evasion variable on the tax collection variable is negative -5,187, demonstrating that there is no relationship between these two variables; therefore, the higher the levels of tax evasion, the lower the tax collection.

At the local level we have, Peña (2023), in his study entitled “La informalidad en el mercado de frutas de Cajamarca, como factor determinante en el delito de hurto simple”, tax evasion persists in regions where high levels of informality, ignorance, and lack of standards to identify the causes of such cases and simple theft are determinants. This study has a quantitative approach, non-experimental, cross-sectional design. Following the survey, 98.6% of the respondents cited the lack of implementation of national policies as the cause of public informality and distrust. It was concluded that informal labor employed by traders generates disreputable people, leading to crimes that affect citizens such as theft and tax evasion.

Montoya (2019), in his research “tax evasion and its influence on the tax collection of mypes”, determined the influence of tax evasion of mypes on tax collection, with a quantitative approach, non-experimental design, cross-sectional, whose population was made up of merchants from a local market; obtaining results that 59% of taxpayers do not declare all their income, 32% do not issue payment receipts and 8% are not registered in SUNAT. It is concluded that the merchants of the said local market have a high tax evasion, which affects the state’s tax collection.

Díaz and Obregón (2018), in their research “Tax evasion and its influence on the tax collection of merchants in a local market, 2017”, found out to what extent tax evasion influences the VAT tax collection in the grocery merchants of the mega market of the city of Huamantanga. This research, being a quantitative, non-experimental, cross-sectional approach applied to a sample of 50 individuals obtained results that 80% of the respondents are unaware of the tax regimes and 90% do not know the use of the said taxes by the state. It is concluded that the lack of tax knowledge intervenes in the high level of tax evasion, and lack of awareness to contribute to the state.

The research is justified in three important areas: theoretically, because it provides theories, norms, and concepts that guide the reader to have a better understanding of how tax evasion negatively influences tax collection since it afflicts the state, causing large losses in tax revenue; in the practical part, it will allow the tax administration to develop policies to reduce tax evasion and obtain greater tax collection; and finally, on the scientific side, it will allow the presentation of results and conclusions obtained under a rigorous process with the application of an appropriate methodology for the achievement of the research objectives. From this, the objective is set: to determine the relationship that causes tax evasion in tax collection in wholesale grocery merchants in a local market, and the specific objectives are to: a) Determine the relationship between tax culture and tax revenue in wholesale grocery merchants in a local market, b) Determine the relationship between informality and tax pressure in wholesale grocery merchants in a local market, and c) Determine the relationship between tax fraud and the Laffer curve in wholesale merchants in a local market.

Materials and Methods

The approach of the research is quantitative, because it shows statistical results of the study, being of an applied type, because theories are not being created, but rather the existing ones are applied to reality and of a descriptive level, because they describe the relationship that exists between evasion fiscal and collection and cross-sectional when applied in a single period of time. This study considers a finite population, made up of 595 wholesale merchants in the food market, who were granted operating licenses. The sample was determined under the non-probabilistic method for convenience for which the individuals were selected, making a total of 25 companies and people who are dedicated to the wholesale purchase of groceries. It should be noted that inclusion criteria were adopted (natural and legal persons who carry out commercial activity in the said market), and exclusion criteria (companies that refuse to provide information, that are not wholesalers) that are outside the jurisdictional radius of the investigation.

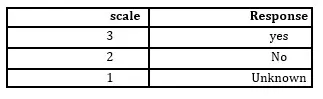

The data collection techniques were the survey and the structured questionnaire with 16 questions, divided into two parts, used as instruments. The first part consists of 8 questions that evaluate the importance of complying with the taxes by wholesale grocery merchants; the second part consists of 8 questions that evaluate the tax collection of wholesale merchants and whose answers are organized on a scale of 3 answers which are: yes, no and don’t know; the scale used for the analysis was as shown in Table 1.

Table 1:Survey measurement scaleNote. Table 1 shows the rating intervals used for the analysis of the information.

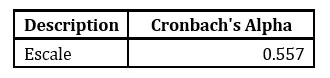

The instrument was validated based on expert judgment. To measure the reliability of the instrument, Cronbach’s Alpha coefficient was used, the results of which are shown in the following table:

Table 2: Reliability Statistics for the Tax Evasion variable and the Tax Collection variable

Table 2 shows the value obtained through the JAMOVI program that the reliability of the instrument is regular, with a Cronbach’s alpha value of 0.557; since it is in the interval [0.5 – 0.7], it indicates that the reliability of this instrument presents a good level of confidence for the variables Tax evasion and Tax collection, therefore it can be applied and accepted Regarding the ethical part of the research, it is based on moral principles and values, with results as they are collected and statistically verified without any alteration.

Results

Next, the results obtained in the research on tax evasion and its relationship with the tax collection of wholesale merchants in a local market are explained, in relation to the objectives and hypotheses proposed, To determine the normality test, a 95% confidence level and a 5% margin of error were applied, so the p-reference value is 0.05.

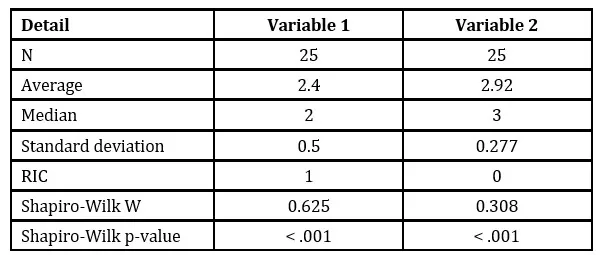

Table 3: Normality of the Tax Evasion and Tax Collection variables

According to the Shapiro-Wilk results, the normality test of 0.625 was obtained for variable 1 and 0.308 for variable 2 with a significance level less than 0.001. Therefore, to check whether the hypothesis is met or not, Spearman’s Rho was used, which is used in samples of less than 50 individuals to determine if the said variables have a normal distribution. The tests used in the general hypothesis and specific hypotheses are shown below.

Inferential Analysis

Compliance with general objective

Determine the impact of tax evasion generated by wholesale grocery merchants in Peru on tax collection 2023

Table 4: Relationship between Tax Evasion and Tax Collection

Table 4 shows that there is a moderate negative relationship between the tax evasion variable and the tax collection variable, because a Spearman’s Rho correlation coefficient was obtained -0.060 and a significance level of 0.775 indicating that p-value is greater than 0.05 (p>0.05). Therefore, the stated objective is determined, which means that there is a negative relationship between these two variables since tax evasion brings unfavorable consequences for the state, causing little tax collection.

Compliance with specific objective 1

Determine the relationship between tax culture and tax revenue in wholesale grocery merchants in a local market.

Table 5: Relationship between Tax Culture and Tax Revenue

Table 5 shows that there is a moderate negative relationship between the tax culture dimension and the tax revenue dimension, because a Spearman’s Rho correlation coefficient was obtained -0.067 and a significance level of 0.750 indicating that p-value is greater than 0.05 (p>0.05). Therefore, the stated objective is determined, which means that the level of tax culture has a negative relationship in wholesale grocery merchants, generating an unfavorable impact on tax revenues.

Compliance with specific objective 2

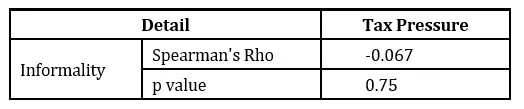

Determine the relationship between informality and tax pressure on wholesale grocery merchants in a local market.

Table 6: Relationship between Informality and Tax Pressure

Table 6 shows that there is a moderate negative relationship between the informality dimension and the tax collection dimension, because a correlation coefficient -0.067 and a significance level of 0.750 were obtained, indicating that p-value is greater than 0.05 (p>0.05). Therefore, it is possible to determine the stated objective that generates informality in merchants. Grocery wholesalers have an impact on tax pressure, which is the amount of money that the state receives from families and taxpayers.

Compliance and specific objective 3

Determine the relationship between tax fraud and the Laffer curve in wholesale merchants in a local market.

Table 7: Relationship between Tax Fraud and Laffer Curve

Table 7 shows that there is a moderate negative relationship between the tax fraud dimension and the Laffer curve dimension; this is because a Spearman’s Rho correlation coefficient was -0.333 and a significance level of 0.103 indicating that p-value is greater than 0.05 (p>0.05). Therefore, it is possible to determine the stated objective, indicating that tax fraud is negatively related to the level of increase in the tax rate, generating a negative Laffer curve, as the coefficient of the tax fraud variable is higher, the Laffer curve variable will be lower.

Descriptive Analysis

Quiz results

After processing the information obtained from the study through the use of the questionnaire, the following descriptive results are obtained.

Table 8: Total variables

Table 8 shows a total of 25 respondents who are wholesale grocery merchants with a statistical error for the tax culture variable of 0.1000 and the tax collection variable of 0.0554, with a median value that occupies the intermediate position of the data set, with 2 for tax culture and 3 for Tax collection, a standard deviation for the tax culture variable of 0.500 and the tax collection variable of 0.277, the coefficient of variation for tax culture is 0.2500 and of tax collection is 0.0767 comparing the degree of dispersion of variables measuring in units, also with a minimum value of 2 for the two variables and a maximum of 3.

Discussion

The objective of this investigation was to determine the relationship that causes tax evasion in tax collection in wholesale grocery merchants in a local market. In the following lines, the findings of the research and the theoretical sources are presented and what was obtained in this research is compared.

In relation to the general objective and using the Rho Spearman test in table 4, a correlation coefficient of -0.060 resulted, which specifically means a moderate negative correlation between the research variables. This indicates that the tax evasion variable generates negative consequences for the tax collection variable; likewise, regarding its significance, it is 0.775. These results agree with those found by Díaz and Obregón (2019) who found that 80% of those surveyed are unaware of the tax regimes and 90% do not know the use of the said taxes made by the state; as a result, there is a high level of tax evasion and a low level of tax collection. According to these results, the hypothesis is verified, the level of negative incidence between tax evasion and tax collection is identified, pointing out that citizens are not satisfied with the work of the state and therefore the refusal to pay their taxes and an increase in the level of income.

In relation to specific objective 1: Determine the relationship between tax culture and tax revenue in wholesale grocery merchants in a local market. It is evident in table 5, with a confidence level of 95% using Spearman’s Rho test, that tax culture has a very low negative relationship with tax revenue, since there is a correlation coefficient level of -0.067 and a level of significance of 0.750, which means that the tax culture of wholesale grocery merchants generates a negative impact on tax revenues. Therefore, in a certain way it agrees with Carrillo (2023), whose result was that there is a considerable relationship with a significance of 0.000 and a correlation coefficient of 0.579, concluding that, the greater the knowledge of the tax culture of an entrepreneur, the greater will be the level of compliance with their duties, increasing tax revenues. According to these results, the hypothesis is tested and the level of relationship generated by the tax culture is identified since it is important for people with businesses to comply with their tax obligations established in the regulations, obtaining more resources for the growth of the country.

In relation to specific objective 2: Determine the relationship between informality and tax pressure on wholesale grocery merchants in a local market. It is evident in table 6, with a confidence level of 95% using Spearman’s Rho test, that informality is related to tax pressure since there is a moderate negative relationship between the variables, having a correlation coefficient of -0.067 and a significance level of 0.750 compared to what was mentioned, the level of informality that wholesale grocery merchants have is high, which generates a negative impact on the state’s tax pressure on the amount of money collected. Therefore, it coincides with Peña (2023), where the result was that 98.6% of those surveyed responded that non-compliance with national policies is the cause of public informality and mistrust. He concluded that the merchants operated informally, mostly selling on the streets of the markets, which led to people of dubious reputation causing crimes of theft and tax evasion affecting citizens. According to these results, the research hypothesis is verified and the level of negatively moderate incidence between the variable informality and tax pressure is identified, considering that businessmen accuse the state of not managing the taxes collected well, which is why they violate the rules, causing a high level of informality and creating negative tax pressure.

In relation to specific objective 3: Determine the relationship between tax fraud and the Laffer curve in wholesale merchants in a local market. It is evident in Table 7, with a confidence level of 95% using Spearman’s Rho test, since there is a moderate negative relationship between the variables, having a correlation coefficient of -0.333 and a significance level of 0.103, which means that the higher the tax fraud that wholesale grocery merchants have, the lower the tax revenue results will be shown in the Laffer curve graph. This coincides with Cornejo (2017), who points out that tax evasion has several causes, one of them being tax fraud, resulting in a significance level of less than 0.05 and a negative correlation coefficient of -0.204, determining that there is no relationship between these two variables, causing a decrease in tax collection and obtaining a negative Laffer curve for the state. According to these results, the research hypothesis is verified and with the aforementioned author the negative influence caused by tax fraud is shown, due to which the level of tax revenue is declining for the state, generating setbacks in the country.

Conclusions

In relation to the general objective, it was determined that tax evasion has a moderate negative relationship so that it generates a negative impact on tax collection by wholesale grocery merchants in the district of Cajamarca 2023, according to the statistician Spearman. The confidence level is 95% with a correlation coefficient of -0.060, which means that the greater the increase in tax evasion, the less tax revenue there will be for the state.

In relation to specific objective 1, it was determined that there is a moderate negative relationship between tax culture and tax collection by wholesale grocery merchants in the district of Cajamarca 2023, according to results obtained through Rho Spearman. It has a correlation coefficient of -0.067, with a confidence level of 95%. In this way, it is verified that the majority of merchants consider it not important to know the tax regulations, which causes a negative impact on the collection of taxes by the state.

In relation to specific objective 2, it was determined that there is a moderate negative relationship between informality and tax collection by wholesale grocery merchants in the district of Cajamarca 2023, being one of the main causes that affects tax collection, according to the statistician. Spearman has a correlation coefficient of -0.067, with a confidence level of 95%, thus demonstrating that informality seriously affects income by generating a small amount of goods and services provided by the state.

In relation to specific objective 3, it is concluded that there is a moderate negative relationship between tax fraud and tax collection by wholesale grocery merchants in the district of Cajamarca 2023, according to the Spearman statistic. The result is a correlation coefficient of -0.333 , with a confidence level of 95%, since wholesale grocery merchants do not present their sworn statements on time since this generates an expense for which they hide information or declare false data.

Cáceres, JM & Soto, JN (2020) ‘Levels of tax collection and public investment at the departmental level in Peru, 2008-2017’, UNEMI Science Magazine, 13(33), pp. 108-119. Available at: https://dialnet.unirioja.es/descarga/articulo/8375326.pdf

Carrillo, AL (2023) Tax culture and its impact on compliance with tax obligations of commercial companies mypes of the organs, Piura, 2021. thttps ://hdl.manejar.neto//11537//335

Carhuapoma Inga, YK & Perez Vidal, AS (2023) Tax pressure and public spending in Peru, 1990-2021. Available at:http://repositorio.unac.edu.pe/bitstream/handle/20.500.12952/7811/TESIS-carhuapoma-perez.pdf?sequence=1

Córdova, RCL (2014) ‘Tax evasion and its consequence on the economic development of the country’, In Crescendo

Díaz, MD & Obregón, KE (2018) Tax evasion and its influence on VAT tax collection by grocery merchants at the Huamantanga Mega Market in 2017. http://hdl.handle.net/11537/13929

Doila Cortez & Peregrino, J. (2021) Incidence of tax evasion on tax collection in the hotel sector in the Cajamarca district, 2021. https://repositorio.upn.edu.pe/bitstream/handle/11537/32833/ Cortez%20Leiva%2c%20Doila%20Aydee%20-%20Peregrino%20Mestanza%2c%20Jhonatan%20Manuel.pdf?sequence=1&isAllowed=y

Lennin Rodríguez, (2018) Business culture and tax evasion in the city of Cajamarca: https://repositorio.unc.edu.pe/bitstream/handle/20.500.14074/2239/CULTURA%20EMPRESARIAL%20Y%20EVASI%C3%93N %20tributaria%20EN%20LA%20ciudad%20de%20cajamarca.pdf?sequence=1

Lira, ZR et al. (2023) ‘Personnel attraction processes in Ecuadorian family and non-family businesses’, Revista de Ciencias Sociales (Ve), XXIX (Special Issue 7)https://elibro.bibliotecaupn.elogim.com/es/lc/upnorte/ titles/53661

Merino Antigüedad, JM (2004) Master, is it legal to pay tribute to Caesar? d.https://elibro.bibliotecaupn.elogim.com/es/lc/upnorte/titulos/53661

Montoya, KI (2019) Tax evasion and its influence on the tax collection of MYPES in the San Antonio market, Cajamarca 2018. http://hdl.handle.net/11537/22366

Otalora, JCV, Saavedra, JPH & Robledo, JAC (2021) Taxation in Colombia: A theoretical and empirical approach to the Laffer Curve. Available at: https://hal.science/hal-03114284/document

Pedroni, FV, Briozzo, A. & Pesce, G. (2022) ‘Firm-level determinants of corporate tax evasion in emerging economies: the case of Argentina’, Journal of Quantitative Methods for Economics and Business, https:/ /www.upo.es/revistas/index.php/RevMetCuant/article/download/5277/6326/29038

Peña, LP (2023) Informality in the Cajamarca fruit market, as a determining factor in the crime of simple theft. thesis.https://hdl.handle.net/11537/33533

Tixi Lucero, YJ (2016) Tax Evasion and its impact on the collection of the Income Tax of Natural Persons in the Riobamba Canton period 2014. http://dspace.unach.edu.ec/handle/51000/2750

Triana, EDV, Arriaga, LIS & Valenzuela, PPA (2019) ‘Tax Evasion and its impact on the General Budget of the Ecuadorian State in the years 2014-2018’, Pro Sciences: Magazine of Production, Sciences and Research, 3

Varela, KJ (2021) Factors of tax evasion of Mypes in the district of Pacasmayo – 2020. thesis.https://hdl.handle.net/11537/29443

Vargas Figueroa, J. et al. (2023) ‘The deduction system as a tax compliance strategy: a Peruvian case’, IBIMA Business Review. 2023 (2023), Article ID 239727 https://doi.org/10.5171/2023.239727Zevallos Rivarola, PC (2018) SUNAT and tax fraud in Peru. Available at:http://dist.udh.edu.pe/flujo de bits/manejar//123/1091 /ZE%20RIVAROLA %2C%%20Paulo%20C.pdf?secuencia =1&es=