Mila APAZA-CHULLUNQUIA, Michael VILLOSLADA-COSINGA, Andrea TORRES-VASQUEZ Yessica ERAZO-ORDOÑEZ And Roberto MACHA-HUAMÁN

Universidad Peruana Unión, Lima, Perú

Volume 2025,

Article ID 440552,

IBIMA Business Review,

18 pages,

DOI: https://doi.org/10.5171/2025.440552

Received date: 1 November 2024; Accepted date: 23 February 2025; Published date: 15 May 2025

Cite this Article as:

Mila APAZA-CHULLUNQUIA, Michael VILLOSLADA-COSINGA, Andrea TORRES-VASQUEZ Yessica ERAZO-ORDOÑEZ And Roberto MACHA-HUAMÁN (2025)," Digital Marketing Strategies in Loyalty: Satisfaction as a Mediating Element with Bank Clients, Lima - Peru", IBIMA Business Review, Vol. 2025 (2025), Article ID 440552, https://doi.org/10.5171/2025.440552

In Peru, the strong competition in the banking sector in the digital context has made customer loyalty essential, which is why the use of well-defined digital marketing strategies is important as a differentiating point in a competitive market. Although customer satisfaction has been widely studied, there is little research that places it as a mediator between digital marketing strategies and customer loyalty. The objective of the research is to analyze to what extent digital marketing strategies influence brand loyalty, the mediating role of satisfaction. This research has a quantitative approach with a non-experimental design, at an explanatory level, with the use of structural equations. The sample was made up of 300 bank clients, with a non-probabilistic sampling for convenience. The results of the theoretical model were adequate, due to the values of RMSEA= 0.057 and SRMR=0.045, CFI=0.939 and TLI=0.932, chi-square (X^2) =724 and (df)=363. The results show that marketing strategies influence customer loyalty with customer satisfaction as a mediator. However, these strategies must be reviewed periodically due to changes in technology and artificial intelligence.

Keywords: Digital marketing, strategies, loyalty, satisfaction.

Introduction

Digital marketing has become an essential tool for businesses in the modern era, especially in the banking sector. The pandemic prompted the closure of bank branches, forcing customers to use their banks’ digital channels. As a result, 50% of customers now interact with their bank through mobile applications or websites at least once a week, compared to 32% two years ago (López and Lagunas, 2021). In Lima, Peru, competition between banks is fierce, and customer loyalty has become a primary objective. The number of digital operations in Peru has increased significantly. Digital payments per capita in the country increased by 56% compared to 2021, reaching a total of 156 digital payments per capita in 2022 (Banco Central de Reserva del Perú [BCRP], 2022). Well-implemented digital marketing strategies can be a key differentiator in a saturated market. Today’s consumers expect personalized and convenient experiences.

According to Deloitte (2021), digital use among millennials and generation Z increased from 25% to 70%. This research will not only benefit banking institutions by providing them with clear and effective strategies to improve customer loyalty, but will also contribute to the academic and practical development of digital marketing in the financial sector. Although there are various studies on the influence of digital marketing in various sectors, there is little research focused on strategies that influence loyalty within the banking sector in Peru; satisfaction has also been widely studied, however there are few investigations that place it as a mediator between marketing strategies and loyalty, therefore that is the gap that is intended to be filled: providing information that can help banks optimize their digital marketing strategies to improve both customer satisfaction and loyalty.

The objective is to analyze to what extent digital marketing strategies influence brand loyalty, a mediating role in satisfaction.

Literature Review

Digital marketing refers to marketing over the Internet using websites, advertising, online promotions, and social media (Kotler and Armstrong, 2018). The implementation of digital marketing in companies is vital to be competitive in the market by offering their products and services through digital tools (Gasca et al., 2022). Likewise, it is important to apply digital marketing strategies in organizations, these support customer satisfaction, the creation of products and reaching the target market (Viteri et al., 2018). On the other hand, digital marketing is a competitive advantage over other companies that do not adapt to constant changes (Alonso and Tena, 2019). Meanwhile, those responsible for marketing must apply strategies to improve customer loyalty and satisfaction (Guo, Zhang and Xia, 2023). Likewise, implementing digital marketing strategies means innovating every day, improving communication and achieving customer loyalty (Lozano et al., 2021). Therefore, companies must apply marketing strategies with innovation and actively adapt to constant change to excel in constant competition (Ma and Gu, 2024).

Loyalty is the customer’s tendency to choose one brand over another (Usman, Iselmi and Fidhyallah, 2024). Likewise, loyal consumers are usually satisfied, however, satisfaction is not necessarily consumer loyalty (Oliver, 1999). Maintaining customer loyalty is often given more priority than attracting new customers, retaining existing customers is cheaper than attracting new consumers (Amiruddin, Paly and Abdullah, 2023). Usually, customer loyalty has been defined as a behavioral indicator (Kumar, Ramani and Bohling, 2004). Furthermore, brand loyalty manifests itself as a visible behavior, evidenced in repeated purchases of the same product, brand or supplier, regardless of the customer’s stated intentions about future purchases. This approach defends the random nature of the phenomenon and, therefore, provides an inductive and observational explanation, explaining the frequency of occurrence. (Páramo, 2020).

Customer satisfaction is defined as the extent to which customers’ expectations about a product or service are met or exceeded. This variable is crucial in evaluating business performance and has a significant impact on customer loyalty, retention and long-term profitability of the company (Anderson, Fornell and Rust, 1997). Likewise, customer satisfaction not only refers to the perception of the value received, but also to the general experience with the company, which includes aspects such as customer service and interaction at key contact points. This reflects positively in greater customer retention and an increase in recommendations, which is vital for the organic growth of the company (Eskildsen, 2009). On the other hand, companies that invest in improving customer satisfaction often see a positive return on their investment due to decreased customer churn and increased customer lifetime value (Homburg, Jozić and Kuehnl, 2017). Also, customer satisfaction contributes significantly to productivity and profitability, differentiating between goods and services (Anderson, Fornell and Rust, 1997). Additionally, customer satisfaction can be effectively assessed using surveys that measure specific aspects of the customer experience, such as perceived quality and perceived value (Babin and Zikmund, 2015).

Email marketing and satisfaction

Email marketing has established itself as an essential tool in digital marketing strategies, especially in sectors such as banking, where personalization and direct communication are essential for customer satisfaction. According to Chaffey and Ellis-Chadwick (2019), email marketing allows companies to effectively segment their customers, personalize messages and measure the impact of their campaigns, which significantly contributes to improving the customer experience. In the banking context, this translates into greater satisfaction when receiving relevant and timely information, which reinforces the positive perception of the financial institution (Ali et al., 2021). The influence of email marketing on customer loyalty and satisfaction is evident in studies such as that of Valente and Alturas (2023), who found that well-executed email marketing campaigns can strengthen customer loyalty, a key component of customer satisfaction. Furthermore, Assensoh-Kodua (2016) points out that, in the banking industry, email marketing not only improves satisfaction by keeping customers informed about products and services, but also increases customer retention, an indicator of long-term satisfaction. Another relevant aspect is the integration of email marketing with customer relationship management (CRM) systems. El Hail (2024) highlights that this combination allows for more effective and personalized communication, which contributes to greater customer satisfaction. Along these lines, Ellis-Chadwick and Doherty (2012) argue that email marketing, when implemented correctly, can be a powerful tool to improve customer satisfaction by offering relevant and personalized content that responds to the specific needs of banking customers. Personalization is one of the main factors that link email marketing with customer satisfaction. According to Sagar et al. (2022), the ability to personalize messages according to customer preferences not only increases the email opening rate, but also improves the customer’s perception of the brand, which in turn raises their level of satisfaction. This personalized approach is particularly relevant in the banking sector, where clients value the relevance and timeliness of the information received. Finally, recent studies, such as that of Alalwan (2018), show that email marketing characteristics, such as personalization and segmentation, significantly influence purchase intention and customer satisfaction. These findings suggest that banks using personalized email marketing strategies can not only increase customer satisfaction but also improve long-term loyalty.

Affiliate marketing has become a key strategy for companies seeking to increase customer satisfaction through strategic collaborations with third parties. In the banking sector, this practice allows financial institutions to expand their reach and offer complementary products and services that improve the customer experience. According to Singh (2017), affiliate marketing allows banks to leverage their affiliate partners’ audiences to offer promotions and products that better align with customer needs, increasing overall satisfaction. Recent studies, such as that of Zangana et al. (2024), suggest that affiliate marketing is not only effective in attracting new customers, but also in improving the satisfaction of existing customers by providing them with access to exclusive and personalized offers. In the banking context, this approach can translate into higher customer retention rates, as satisfaction is a key driver of customer loyalty (Kumar, 2021). The trust generated by affiliate recommendations also plays a crucial role in customer satisfaction. According to Syrdal et al. (2023), customers tend to trust affiliate recommendations more than the company’s direct advertising, which reinforces their positive perception and, therefore, their satisfaction with the financial institution. In this sense, the credibility and trust generated through affiliate marketing can be decisive in improving the banking customer experience (Garepasha et al., 2020). On the other hand, Mangiò and Di Domenico (2022) highlight that transparency in affiliate marketing practices is essential to maintain customer satisfaction. When customers are aware of the relationship between the bank and its affiliates, and perceive that the offers are relevant and fair, their level of satisfaction increases considerably. This aspect is particularly important in the financial sector, where trust and transparency are fundamental to the relationship with the client. Additionally, strategic alliances established through affiliate marketing can improve the perception of value among banking customers. According to Kumar et al. (2024), promotional offers and additional benefits provided through affiliates can increase the customer’s perception of value, which in turn raises their level of satisfaction. These types of synergies are especially relevant in the competitive banking market, where customers continually look for options that offer them the greatest possible value. Finally, a study by Leeflang et al. (2014) points out that affiliate marketing can be an effective strategy to improve customer satisfaction by allowing greater personalization and relevance in the offers presented. In summary, affiliate marketing, when implemented strategically in the banking sector, not only has the potential to attract new customers, but also to significantly increase the satisfaction of existing customers by providing them with offers and products that respond to their specific needs.

Search engine marketing is one of the digital marketing strategies, which is a practice that allows visualization in the search for information about a product or service (Khushi, 2023). Likewise, search engine marketing positively influences satisfaction and the purchase decision (Khanfar et al., 2024; Diwanji et al., 2023). Similarly, search engine marketing is significantly related to customer satisfaction to generate loyalty in its customers (Ikeni, 2024). However, Altarifi et al. (2024) in their study found that search engine marketing does not have significant acceptance among customers.

There are already different social networks in the market and although social networks are very dynamic, it is difficult not to refer to one in particular and how it has influenced marketing: WhatsApp, Facebook, YouTube, Instagram and Twitter are the most used social networks without forgetting that the social network that has grown with the most trend in recent years is Tik Tok (Sicilia et al., 2022). In the same way, the content generated on social networks by brands and users where products or services and recommendations are made known is vital to consumers for their purchasing decision (Adistsany and Wikartika, 2022). Social media marketing promotes brands and products (Mude and Undale, 2023). Likewise, the use of social networks is an effective digital marketing strategy to attract potential customers, strengthen relationships with followers and customers to provide a satisfactory experience, thereby generating customer loyalty (Handal et al., 2024). Furthermore, the use of social networks is positive and significant in company performance (Winarso et al., 2023). According to Al-Weshah et al. (2021), digital marketing strategies, especially the social media strategy, positively influence patient satisfaction at the health center in Jordan. On the other hand, Alfaro et al. (2023) obtained as a result in their research that digital marketing strategies have not been able to satisfy customer expectations because the company is just on the path to adapting digital media and does not interact with its customers through social networks, which is why it has a low positive relationship. Likewise, Rashwan et al. (2019) in their research work found that satisfaction with electronic banking does not act as a mediator in the relationship between the dimensions of the E-CRM, therefore managers must enhance customer satisfaction by offering technological security mechanisms for online banking transactions.

H4: Social media marketing influences banking customer satisfaction.

Mobile marketing and satisfaction

The growth of mobile marketing has increased the importance of banking services through mobile devices (Yang, 2004). Currently, users must use their phones to carry out transactions on electronic commerce platforms, although they must complete these operations using mobile banking applications; this includes actions such as transfers, withdrawals, payments and investments (Öztaş, 2015). Therefore, banks must take advantage of this opportunity to provide services that fit the needs of their mobile customers, particularly relating customer satisfaction, thus obtaining a corrective result of mobile marketing and satisfaction (Baptista and León, 2013). Also, Scharl et al. (2005) defined m-marketing as the use of wireless media to offer m-consumers personalized and relevant information in time and place, promoting products and services. Likewise, Akgün et al. (2018) indicate that m-marketing includes marketing activities carried out through mobile phones in mobile commerce.

Therefore, mobile marketing is a medium that allows business organizations to interact with their customers in a personalized way (Gana and Koce, 2016) ensuring that customers’ needs are met and promoting greater interaction and communication that helps satisfy their desires, which increases their satisfaction (Al-Hawary and Obiadat, 2019). This aspect is crucial to foster customer loyalty towards the organization (Hallowell, 1996)

H5: Mobile marketing influences banking customer satisfaction.

Customer satisfaction and loyalty

The growing advancement of financial services related to customer behavior has been a highly studied topic in recent years, particularly in satisfaction and loyalty to an entity (Baptista and León, 2013). In this sense, loyalty is seen as the viable path to profitability, helping to reduce customer loss and increase income in companies (Reichheld, 1993; Osayawe, 2006). Satisfaction is seen as the response of the consumer’s fulfillment. Bolton and Drew (1991, p. 377) and Oliver (1999) reinforce this concept by defining it as the satisfaction given by certain characteristics of a product or service and the pleasant result of its use in relation to the expectation (Lévy Mangin et al., 2020). While customer loyalty focuses specifically on the dimensions of the service (Zárraga, Morejón and Sandoval, 2018)

H6: Satisfaction influences bank customer loyalty.

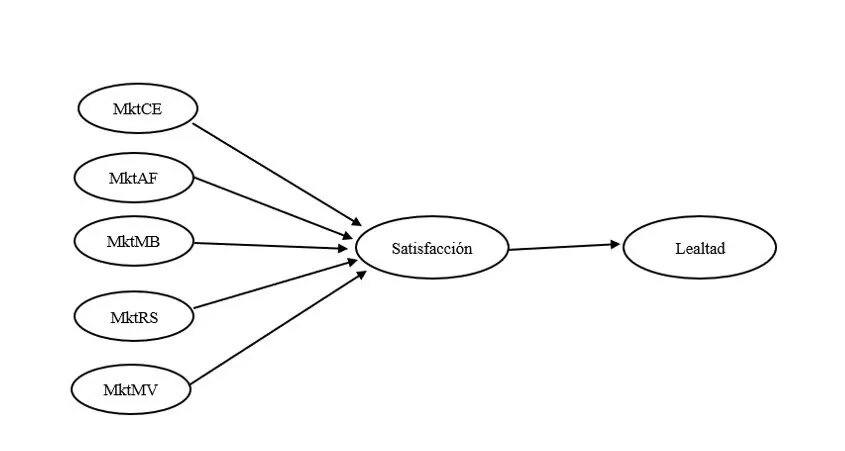

Fig 1. Theoretical model

Materials and Methods

This study will be carried out under a quantitative approach, characterized by the collection and analysis of numerical data to establish patterns and test predefined hypotheses (Ato, López-García and Benavente, 2013). Likewise, the research design is non-experimental where the variables are not manipulated; the variables are observed as they occur in their natural environment. Cross-sectional since data collection is carried out at a single moment in time (Hernández and Mendoza, 2018). Furthermore, the research will be of an explanatory level because it focuses on understanding and explaining the causal relationships between the variables investigated, with the use of SEM equations (Hernández et al., 2014). The study sample is made up of 300 bank clients. Inclusion criteria: People of legal age who are clients of a bank. Exclusion criteria: people who are not clients of a bank. Non-probabilistic convenience sampling will be used. This type of sample was chosen due to the ease and speed of accessing participants who meet the inclusion criteria, allowing data to be collected in an efficient and practical manner.

The technique used was the survey and the questionnaire as an instrument. The specific questionnaires used to measure each of the study variables are described below: To measure the digital marketing strategies, the instrument by Dhankhar et al. (2023) was used and to measure the loyalty variable, the instrument by Shi et al. (2014) was used, and, finally, to measure the satisfaction variable, the questionnaire (American Customer Satisfaction Index [ACSI], 2018) will be used. The three questionnaires use a 5-point Likert scale, where 1 represents “totally disagree” and 5 represents “totally agree. The reliability of the instruments is greater than 0.7 considering the instruments reliable. The final survey was subsequently carried out. Jamovi software version 2.3.28 was used for data processing.

Results

Table 1 shows the sociodemographic results, prioritizing the age between 25-34 with a percentage of 43.7%, mostly men with 61.3%, with a higher degree of university education of 57%, and the highest percentage of respondents were from Banco BCP with 42.3%.

Table 1. Sociodemographic data

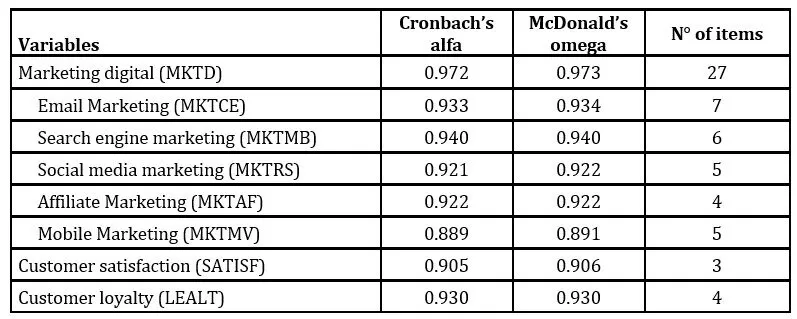

Table 2 shows the reliability of the instruments used in the present study. That is, both Cronbach’s alpha and McDonald’s omega measure the internal consistency of an instrument. Therefore, for an instrument to be considered reliable, the coefficient must be greater than 0.7.

Table 2: Instrument Reliability

Note: Reliability results prepared with Jamovi

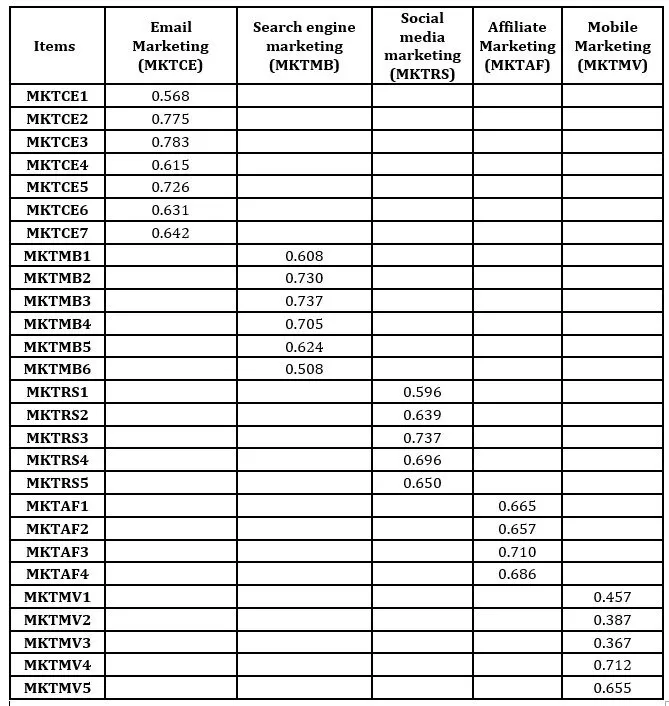

Exploratory Factor Analysis (EFA) allows measuring the Kaiser-Meyer-Olkin (KMO), which must be greater than 0.6. Likewise, it allows us to obtain the Bartlett test of sphericity, which is composed of Chi-square (X^2), degree of freedom (df) and p value that must be less than 0.05 to be significant. Furthermore, the explained variance must be greater than 50%. In this sense, the KMO was 0.963, the Chi-square (X^2)=7545, df=351 and p<0.001. Finally, through the maximum likelihood extraction method and varimax rotation, 5 factors were extracted with a cumulative explained variance of 70.7%, as shown in Table 3.

Table 3: Factor loadings of the dimensions of the digital marketing variable

Note: factor loadings taken from the EFA

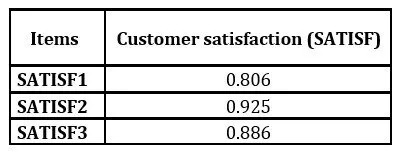

For the customer satisfaction variable, the KMO was 0.740, the Chi-square (X^2)=596, df=3 and p<0.001. Finally, through the maximum likelihood extraction method and varimax rotation, 1 factor was extracted with a cumulative explained variance of 76.3%, as shown in Table 4.

Table 4: Factor loadings of the customer satisfaction variable

Note: factor loadings taken from the AFE

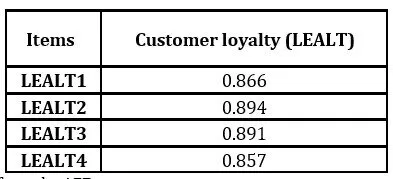

For the customer loyalty variable, the KMO was 0.854, Chi-square (X^2)=966, gl=6 and p<0.001. Finally, through the maximum likelihood extraction method and varimax rotation, 1 factor was extracted with a cumulative explained variance of 76.9%, as shown in Table5.

Table 5: Factor loadings of the customer loyalty variable

Note: factor loadings taken from the AFE

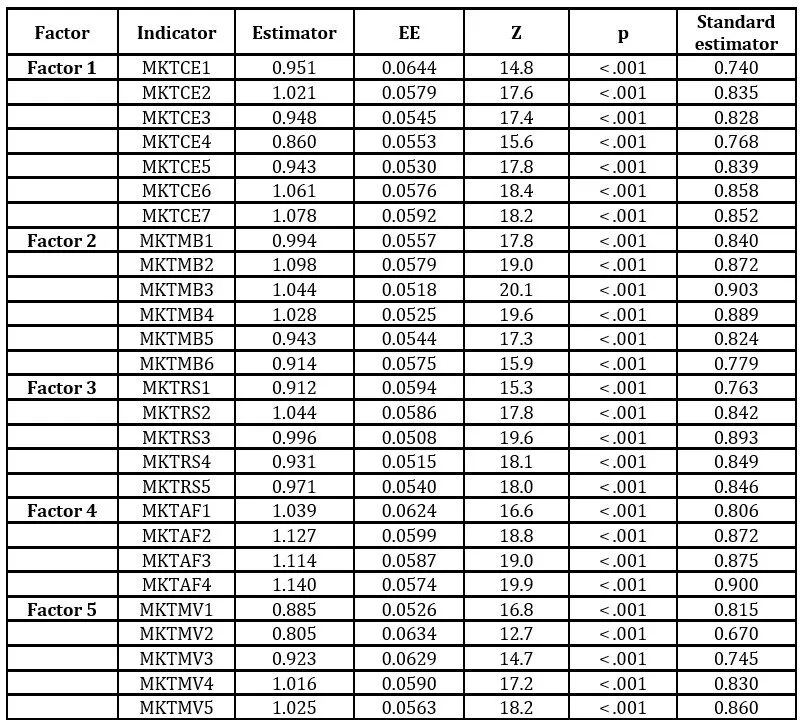

After the Exploratory Factor Analysis (EFA), Confirmatory Factor Analysis (CFA) was used in order to confirm the theories. For the digital marketing variable, 5 factors were confirmed as shown in Table 5. Also, the Chi-square (X^2)=802; gl: 314 and p<0.001. In addition, the fit measures resulted adequate because they are above 0.90 and the errors of unexplained variance are less than 0.08: CFI=0.935, TLI=0.927, SRMR=0.0405 and RMSEA=0.0718.

Table 6: Loadings of the factors of the digital marketing variable

Note: factors taken from the AFC

For the variables customer satisfaction and customer loyalty, Confirmatory Factor Analysis (CFA) has not been carried out because both variables only have one factor, as demonstrated in the EFA.

The Structural Equation Model (SEM) is a multivariate statistical technique for testing hypotheses and validating a theoretical model. This technique allows measuring the relationship between dependent and independent latent variables. In this sense, to obtain the results of the theoretical model, the Robust Maximum Likelihood (MLR) estimation method was used. The results were the following: Chi-square (X^2)= 724, degree of freedom (df)=363 and p<0.001. Likewise, the CFI=0.939 and the TLI=0.932 greater than 0.90 considered adequate. On the other hand, the RMSEA= 0.057 and the SRMR=0.045, less than 0.08 respectively, are considered adequate.

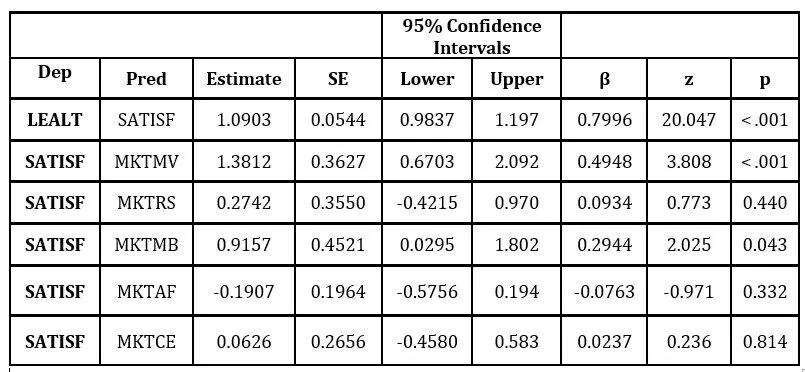

Figure 2 shows the path diagram of the measurement model. This figure shows that the variables email marketing (MKTCE), affiliate marketing (MKTAF), search engine marketing (MKTMB), social media marketing (MKTRS) and mobile marketing (MKTMV) are independent exogenous variables. Likewise, these independent variables have high correlation with each other, which are above 0.70. Furthermore, the variables MKTCE, MKTAF, MKTMB, MKTRS and MKTMV are influential independent variables: β=0.0237, β=-0.0763, β=0.2944, β=0.0934 and β=0.4948 on customer satisfaction (SATISF) and in turn customer satisfaction has a high influence on customer loyalty with a β=0.80

Figure 2. Model path diagram

Table 7 shows the dependent variables and the independent or predictor variables. That is, the influence (β) and the significance (p) are observed; although it is true that there is influence of the predictor variables, however, they are not significant given that the “p” value in almost all the causal relationships is greater than 0.05, except for the mobile marketing and customer satisfaction variables which are significant given that the p<0.001.

Table 7: Estimated parameters

Note: Theoretical model prepared with Jamovi

Discussion

According to the first hypothesis proposed, a low influence of Email Marketing on banking customer satisfaction has been evidenced in Lima, Peru. These findings are not consistent with previous studies such as Ali et al. (2021) who mention that the application of email marketing translates into greater satisfaction when receiving relevant and timely information. Valente and Alturas (2023) also mention that well-executed email marketing campaigns strengthen customer loyalty, a key component of satisfaction. For its part, Assensoh-Kodua (2016) mentions that the email marketing strategy increases retention, a key indicator of satisfaction.

According to the second hypothesis proposed, a negative influence of Affiliate Marketing on banking customer satisfaction has been evidenced in Lima, Peru. These findings are inconsistent with previous research such as the work of Singh (2017), which indicates that affiliate marketing strategy allows banks to leverage their affiliate audiences to offer promotions and products that better align with customer needs, thereby increasing overall satisfaction. Also, Syrdal et al. (2023) mention that customers tend to trust affiliate recommendations more than the company’s direct advertising, which reinforces their positive perception and, therefore, their satisfaction with the financial institution (Kumar et al., 2004).

According to the third hypothesis proposed, a significant influence of Search Engine Marketing on bank customer satisfaction has been evidenced in Lima, Peru. Coinciding with previous research such as that of Ikeni (2024) where he mentions the relationship between the variables, in the same way (Khanfar et al., 2024; Diwanji et al., 2023). On the other hand, Altarifi et al. (2024) found that content marketing is not accepted by customers.

According to the fourth hypothesis proposed, a low influence of social network Marketing on bank customer satisfaction has been evidenced in Lima, Peru. The results coincide with the study by Handal et al. (2024) who mention the effectiveness of the digital marketing strategy to attract potential customers, strengthen relationships and to provide a satisfactory experience to customers; likewise, it is supported by Al-Weshah et al. (2021). However, the research by Alfaro et al. (2023) indicates that digital marketing strategies have failed to meet customer expectations.

According to the fifth hypothesis proposed, a significant influence of Mobile Marketing on bank customer satisfaction has been evidenced in Lima, Peru. The results coincide with previous research such as that of Baptista and León (2013) who indicate that there is a correlation between mobile marketing and satisfaction. Also, the research by Al-Hawary and Obiadat (2019) mentions that mobile Marketing promotes greater interaction and communication that helps satisfy customer desires, which increases customer satisfaction.

According to the sixth hypothesis proposed, a significant influence of satisfaction on bank customer loyalty has been evidenced in Lima, Peru. The results are aligned with previous research such as those of Baptista and León (2013) who have been studying the relationship between them. Also, Reichheld, (1993) and Osayawe (2006) support the same results.

Conclusions

The results showed that the email marketing strategy as it is being implemented has a low influence on customer satisfaction. This result may indicate that, although this communication tool is widely used, it does not always translate into a higher level of customer satisfaction. It is possible that the email marketing strategy, when it is not properly personalized by identifying specific needs, does not become a source of added value.

The results showed that the affiliate marketing strategy can be key to generating sales but not necessarily to creating customer satisfaction; perhaps because they do not perceive value in terms of customer service or support. The incorporation of more direct and personalized interaction strategies could have a greater effect on satisfaction.

The results showed that the search engine marketing strategy can be important to increase brand visibility; but it does not directly contribute to customer satisfaction, perhaps if focuses on attraction rather than support.and not on support, key elements to increase customer satisfaction.

The results showed that, although the social media marketing strategy allows companies to interact with their audience and improve their visibility, its impact on customer satisfaction is limited. This suggests that, although social networks are an effective means of disseminating promotions, news and brand content, they alone fail to produce high levels of customer satisfaction.

The results showed a significant influence of the mobile marketing strategy on customer satisfaction. The goodness of the mobile marketing strategy to offer immediate, relevant, and timely content improves the user experience and strengthens their relationship with the brand. Unlike other strategies, mobile marketing facilitates constant and contextualized interaction, which helps customers perceive greater value.

The results showed a significant influence of satisfaction on customer loyalty; this shows that a satisfied customer is more likely to establish a lasting relationship with the brand. Therefore, if we manage to consistently respond to customer expectations and demands, their loyalty is reinforced, which drives retention and generates favorable recommendations.

The theoretical implication of the research is to expand the existing theory on how digital marketing strategies influence customer loyalty in the banking sector, highlighting the key role of satisfaction as a mediator. The study offers a new look by locating satisfaction as a mediator between digital marketing strategies and bank customer loyalty. Adding theoretical value to previous studies, which have considered it in isolation

Practical implication, the results offer banks a guide to improve their digital strategies, focusing on how to improve satisfaction to encourage loyalty. This could include personalization of content and agile digital channels that improve the customer experience. Banks would have at their disposal what type of digital strategies are most effective, resulting in differentiated strategy proposals to improve loyalty in various demographic groups.

This study has certain limitations. The study focuses exclusively on Lima, Peru, which may limit the generalization of the results to other countries, even within Latin America. Digital marketing is constantly changing, with new technologies and platforms constantly emerging; that is why new tools must be considered in the analysis.

Future lines of research would be studies with other mediating elements, such as customer trust, value perception, omnichannel experience or service quality. Also expanding the study to other departments, to see if satisfaction continues to play a determining mediating role. The emergence of artificial intelligence would be important to investigate how it impacts customer satisfaction and, therefore, loyalty.

References

Adistsany Salwanisa, E. and Wikartika, I. (2022) ‘Digital marketing analysis on the consumer decision-making process of millennials and Gen Z generation groups on the TikTok application | Salwanisa | EQUILIBRIUM : Jurnal Ilmiah Ekonomi dan Pembelajarannya’, Equilibrium:Jurnal Ilmiah Ekonomi dan pembelajaranya, 11, pp. 112–125.

Akgün, A., Barutçu, S. and Dincer Aydın, H. (2018) ‘Drivers of Customer Satisfaction from the Mobile Commerce and Mobile Marketing:The Case of Mobile Shopping Applications’, in. Conferencia: 1er Congreso Internacional de Investigación en Ciencias Sociales, Sarajevo / Bosnia y Herzegovina. Available at: https://www.researchgate.net/publication/326177165_Drivers_of_Customer_Satisfaction_from_the_Mobile_Commerce_and_Mobile_MarketingThe_Case_of_Mobile_Shopping_Applications.

Alalwan, A.A. (2018) ‘Investigating the impact of social media advertising features on customer purchase intention’, International Journal of Information Management, 42, pp. 65–77. Available at: https://doi.org/10.1016/j.ijinfomgt.2018.06.001.

Alfaro Hernández, C.J. et al. (2023) ‘Incidencia de las Estrategias del Marketing Digital en la Fidelización de clientes en un Restaurante de comida oriental, Trujillo, 2023’, LACCEI International Multiconference on Entrepreneurship, Innovation and Regional Development – LEIRD 2023 [Preprint]. Available at: https://dx.doi.org/10.18687/LEIRD2023.1.1.223.

Al-Hawary, S. and Obiadat, A. (2019) ‘Impact of Mobile Marketing on Customer Loyalty in Jordan’, International Journal of Web Applications, 11(4), p. 136. Available at: https://doi.org/10.6025/ijwa/2019/11/4/136-152.

Ali Algnaidi, A.I., Kumar Tarofder, A. and Ferdous Azam, S.M. (2021) ‘E-MARKETING AND ITS EFFECT ON CUSTOMER SATISFACTION IN THE COMMERCIAL BANKS – LIBYA’, Psychology and Education Journal, 58, pp. 2589–2601. Available at: https://doi.org/10.17762/pae.v58i1.1140.

Alonso, A. and Tena, A. (2019) ‘EVOLUCIÓN DEL MARKETING DIGITAL EN EL ÁMBITO EMPRESARIAL, Y SUS IMPLICACIONES EN LA ACTUALIDAD’, 2019, p. 42.

Altarifi, S. et al. (2024) ‘Customers’ acceptance of digital marketing techniques: the impact of search engine, e-mail, and social media marketing’, International Journal of Business Innovation and Research, 34(3), pp. 327–341. Available at: https://doi.org/10.1504/IJBIR.2024.139230.

AL-WESHAH, G.A., KAKEESH, D.F. and AL-MA’AITAH, N.A. (2021) ‘Digital marketing strategies and international patients’ satisfaction: An empirical study in Jordanian health service industry’, Studies ok Applied Economics, 39–7. Available at: https://doi.org/10.25115/eea.v39i7.4811.

American Customer Satisfaction Index (ACSI) (2018) The American Customer Satisfaction Index (ACSI) – National Cross-Industry Measure of Customer Satisfaction, The American Customer Satisfaction Index. Available at: https://theacsi.org/ (Accessed: 19 July 2024).

Amiruddin, K., Paly, M.B. and Abdullah, M.W. (2023) ‘CUSTOMER LOYALTY ISLAMIC BANKS IN INDONESIA: SERVICE QUALITY WHICH MEDIATED BY SATISFACTION AND CUSTOMER TRUST’, International Journal of Professional Business Review, 8(4). Available at: https://doi.org/10.26668/businessreview/2023.v8i4.1286.

Anderson, E.W., Fornell, C. and Rust, R.T. (1997) ‘Customer Satisfaction, Productivity, and Profitability: Differences Between Goods and Services’, Marketing Science [Preprint]. Available at: https://doi.org/10.1287/mksc.16.2.129.

Assensoh-Kodua, A. (2016) ‘Marketing potentials of the social media tools in the banking market of an emerging country’, Risk Governance and Control: Financial Markets & Institutions, 6. Available at: https://doi.org/10.22495/rgcv6i4c2art2.

Ato, M., López-García, J.J. and Benavente, A. (2013) ‘Un sistema de clasificación de los diseños de investigación en psicología’, Anales de Psicología / Annals of Psychology, 29(3), pp. 1038–1059. Available at: https://doi.org/10.6018/analesps.29.3.178511.

Banco Central de Reserva del Peru (2022) Reporte de Estabilidad Financiera. Banco Central de Reserva del Peru, p. 89. Available at: https://www.bcrp.gob.pe/docs/Publicaciones/Reporte-Estabilidad-Financiera/2022/noviembre/ref-noviembre-2022.pdf.

Baptista, M.V. and León, M.D.F. (2013) ‘Estrategias de lealtad de clientes en la banca universal’, Estudios Gerenciales, pp. 189–203. Available at: https://doi.org/10.1016/j.estger.2013.05.007.

Bolton, R. and Drew, J. (1991) ‘A Multistage Model of Customers’ Assessments of Service Quality And Value’, Journal of Consumer Research, 17, pp. 375–84. Available at: https://doi.org/10.1086/208564.

Chaffey, D. and Ellis-Chadwick, F. (2019) Digital marketing. Sixth edition. Harlow London New York NY Boston, Mass. San Franzisco Toronto: Pearson (Always Learning).

Deloitte (2021) La ruta hacia una Banca Digital. Available at: https://www2.deloitte.com/pe/es/pages/financial-services/articles/la-ruta-hacia-una-banca-digital.html.

Dhankhar, D. et al. (2023) ‘The Impact of Digital Marketing Practices on Tourist Buying Behavior: A Study of Indian Tourism Industry’, 16.

Diwanji, V.S., Lee, J. and Cortese, J. (2023) ‘Future-proofing Search Engine Marketing: An Empirical Investigation of Effects of Search Engine Results on Consumer Purchase Decisions’, Journal of Strategic Marketing, 0(0), pp. 1–21. Available at: https://doi.org/10.1080/0965254X.2023.2229343.

El Hail, C. (2024) ‘A Comparative Study on the Adoption of Customer Relationship Management (CRM) Technologies by Family and Non-Family Small and Medium Enterprises (SMEs)’, in Inteligencia artificial, Big Data, IoT y Blockchain en la atención sanitaria: de los conceptos a las aplicaciones. A Comparative Study on the Adoption, pp. 90–102. Available at: https://doi.org/10.1007/978-3-031-65018-5_9.

Ellis-Chadwick, F. and Doherty, N.F. (2012) ‘Web advertising: The role of e-mail marketing’, (1) Scientific Muddling (2) Executional Elements In Advertising, 65(6), pp. 843–848. Available at: https://doi.org/10.1016/j.jbusres.2011.01.005.

Eskildsen, J. (2009) ‘The satisfied customer: Winners and losers in the battle for buyer preference’, Total Quality Management & Business Excellence, 20(5), pp. 581–582. Available at: https://doi.org/10.1080/14783360902925421.

Gana, M. and Koce, H. (2016) ‘Mobile Marketing: The Influence of Trust and Privacy Concerns on Consumers’ Purchase Intention’, International Journal of Marketing Studies, 8, p. 121. Available at: https://doi.org/10.5539/ijms.v8n2p121.

Garepasha, A. et al. (2020) ‘Relationship dynamics in customer loyalty to online banking services’, Journal of Islamic Marketing, ahead-of-print. Available at: https://doi.org/10.1108/JIMA-09-2019-0183.

Gasca Herrera, L.A.G., Mejia Gracia, C.A.M. and Ramos, J.H. (2022) ‘Análisis del marketing digital versus marketing tradicional. Un estudio de caso en empresa tecnológica’, Cuadernos Latinoamericanos de Administración, 18(35), pp. 1–11.

Guo, J., Zhang, W. and Xia, T. (2023) ‘Impacto del diseño de sitios web de compras en la satisfacción y lealtad del cliente: el papel mediador de la usabilidad y el papel moderador de la confianza’, 2023, p. 16.

Hallowell, R. (1996) ‘The relationships of customer satisfaction, customer loyalty, and profitability: an empirical study’, International Journal of Service Industry Management, 7(4), pp. 27–42. Available at: https://doi.org/10.1108/09564239610129931.

Handal Gomez, A.J., Alvarado Pineda, C.G. and Isabel Rivera, M. (2024) ‘Enhance digital marketing to achieve the growth and development of the microenterprise.’, LACCEI International Multi-Conference for Engineering, Education, and Technology [Preprint]. Available at: https://laccei.org/LACCEI2024-CostaRica/meta/FP1158.html (Accessed: 8 October 2024).

Hernández Sampieri, R., Fernández Collado, C. and Baptista Lucio, P. (2014) Metodología de la investigación. 6th edn. McGraw Hill España. Available at: https://dialnet.unirioja.es/servlet/libro?codigo=775008 (Accessed: 14 July 2024).

Hernández Sampieri, R. and Mendoza Torres, C.P. (2018) Metodología de la investigación: las rutas: cuantitativa ,cualitativa y mixta. Mc Graw Hill educación. Available at: http://repositorio.uasb.edu.bo/handle/54000/1292 (Accessed: 14 July 2024).

Homburg, C., Jozić, D. and Kuehnl, C. (2017) ‘Customer experience management: toward implementing an evolving marketing concept’, Journal of the Academy of Marketing Science, 45(3), pp. 377–401. Available at: https://doi.org/10.1007/s11747-015-0460-7.

Ikeni, O. (2024) ‘SEARCH ENGINE MARKETING AND CUSTOMER SATISFACTION OF DOMESTIC AIRLINE IN RIVERS STATE’, 25.

Khanfar, I.A.A. et al. (2024) ‘Impact of online marketing tools on customers’ purchasing decisions’, International Journal of Data and Network Science, 8(4), pp. 2285–2290. Available at: https://doi.org/10.5267/j.ijdns.2024.6.003.

Khushi, Jain (2023) ‘Search engine marketing’, in An SEO Guide for Start-Ups. Nova Science Publishers, Inc., pp. 85–106. Available at: https://www.scopus.com/record/display.uri?eid=2-s2.0-85171953315&origin=resultslist&sort=plf-f&src=s&sid=e7207f20c64f45d09765a75e9d3c5444&sot=b&sdt=cl&cluster=scosubjabbr%2C%22BUSI%22%2Ct&s=TITLE-ABS-KEY%28%22Search+Engine+Marketing%22+AND+%22marketing%22%29&sl=59&sessionSearchId=e7207f20c64f45d09765a75e9d3c5444&relpos=11 (Accessed: 15 October 2024).

Kotler, P. and Armstrong, G. (2018) Principles of marketing. Seventeenth edition. Hoboken: Pearson Higher Education.

Kumar, A. (2021) ‘Study on customer relationship management in banking sector’, in El papel de los recursos humanos y la gestión de las relaciones con los clientes en el escenario actual. AGAR Publications, pp. 448–463. Available at: https://doi.org/10.5281/zenodo.6625001.

Kumar, D. et al. (2024) ‘Understanding the Impact of Affiliate Marketing on Consumer Behavior: A Comprehensive Analysis’. Available at: https://doi.org/10.1007/978-3-031-67434-1.

Kumar, V., Ramani, G. and Bohling, T. (2004) ‘Customer lifetime value approaches and best practice applications’, Journal of Interactive Marketing, 18(3), pp. 60–72. Available at: https://doi.org/10.1002/dir.20014.

Leeflang, P.S.H. et al. (2014) ‘Challenges and solutions for marketing in a digital era’, European Management Journal, 32(1), pp. 1–12. Available at: https://doi.org/10.1016/j.emj.2013.12.001.

Lévy Mangin, J.-P. et al. (2020) ‘La influencia de la confianza y satisfacción del cliente en la intención de uso de los servicios bancarios por internet: un modelo estructural’, CIENCIA ergo-sum, 27(2). Available at: https://doi.org/10.30878/ces.v27n2a3.

López Abellán, D. and Lagunas, J. (2021) Estudio del consumidor bancario: Hacia una digitalización más humana | Accenture, Accenture. Available at: https://www.accenture.com/es-es/insights/banking/consumer-study-making-digital-banking-more-human (Accessed: 21 July 2024).

Lozano Torres, B.V., Toro Espinoza, M.F. and Calderón Argoti, D.J. (2021) ‘El marketing digital: herramientas y tendencias actuales Digital marketing: current tools and trends Marketing digital: ferramentas e tendências atuais’, Ciencias Técnicas y Aplicadas, 7, pp. 907–921.

Ma, X. and Gu, X. (2024) ‘New marketing strategy model of E-commerce enterprises in the era of digital economy’, Heliyon, 10(8), p. e29038. Available at: https://doi.org/10.1016/j.heliyon.2024.e29038.

Mangiò, F. and Di Domenico, G. (2022) ‘All that glitters is not real affiliation: How to handle affiliate marketing programs in the era of falsity’, SPECIAL ISSUE: MANAGING IN AN ERA OF FALSITY, 65(6), pp. 765–776. Available at: https://doi.org/10.1016/j.bushor.2022.07.001.

Mude, G. and Undale, S. (2023) ‘Scopus – Detalles del documento – Uso de las redes sociales: una comparación entre la Generación Y y la Generación Z en la India | Iniciar sesión’, International Journal of E-Business Research, 19, pp. 1–20. Available at: https://doi.org/10.4018/IJEBR.317889.

Oliver, R.L. (1999) ‘Whence Consumer Loyalty?’, Journal of Marketing, 63(4_suppl1), pp. 33–44. Available at: https://doi.org/10.1177/00222429990634s105.

Osayawe Ehigie, B. (2006) ‘Correlates of customer loyalty to their bank: a case study in Nigeria’, International Journal of Bank Marketing, 24(7), pp. 494–508. Available at: https://doi.org/10.1108/02652320610712102.

Öztaş, Y.B.B. (2015) ‘The Increasing Importance of Mobile Marketing in the Light of the Improvement of Mobile Phones, Confronted Problems Encountered in Practice, Solution Offers and Expectations’, Procedia – Social and Behavioral Sciences, 195, pp. 1066–1073. Available at: https://doi.org/10.1016/j.sbspro.2015.06.150.

Páramo Morales, D.P. (2020) ‘Lealtad a la marca’, Pensamiento & Gestión, (49), pp. 1–3.

Rashwan, H.H.M., M. Mansi, A.L. and Hassan, H.E. (2019) ‘The impact of the E- CRM (expected security and convenience of website design) on E- loyalty field study on commercial banks’, Journal of Business & Retail Management Research, 14(01). Available at: https://doi.org/10.24052/JBRMR/V14IS01/ART-10.

Reichheld, F.F. (1993) ‘Loyalty-based management’, Harvard business review, 71(2), pp. 64–73.

Sagar, H., Mohite and Mohite, S. (2022) ‘EMAIL MARKETING ROLE IN IMPROVING CUSTOMER RETENTION RATES (ABDC)’.

Scharl, A., Murphy, J. and Dickinger, A. (2005) ‘Diffusion and success factors of mobile marketing’, Electronic Commerce Research and Applications, 4, pp. 159–173. Available at: https://doi.org/10.1016/j.elerap.2004.10.006.

Shi, Y., Prentice, C. and He, W. (2014) ‘Linking service quality, customer satisfaction and loyalty in casinos, does membership matter?’, International Journal of Hospitality Management, 40, pp. 81–91. Available at: https://doi.org/10.1016/j.ijhm.2014.03.013.

Sicilia, M. et al. (2022) Marketing en redes sociales. Primera Edicion. Colombia: Alpha Editorial. Available at: https://books.google.com.pe/books?hl=es&lr=&id=vtavEAAAQBAJ&oi=fnd&pg=PA5&dq=marketing+de+redes+sociales+y+satisfacci%C3%B3n+articulos+cientificos&ots=Dfg5tAemrU&sig=tnn1Yz4HlsBv3topBIj-hVrRgwE#v=onepage&q&f=f.

Singh, S. (2017) ‘Affiliate Marketing and Customer Satisfaction’, in Driving Traffic and Customer Activity Through Affiliate Marketing, pp. 1–10. Available at: https://doi.org/10.4018/978-1-5225-5187-4.ch057.

Syrdal, H.A. et al. (2023) ‘Influencer marketing and the growth of affiliates: The effects of language features on engagement behavior’, Journal of Business Research, 163, p. 113875. Available at: https://doi.org/10.1016/j.jbusres.2023.113875.

Usman, O., Iselmi, P.A. and Fidhyallah, N.F. (2024) ‘Factors affecting loyalty in mobile banking: A case study on BSI mobile customers’, International Journal of Applied Economics, Finance and Accounting, 18(1), pp. 180–191. Available at: https://doi.org/10.33094/ijaefa.v18i1.1341.

Valente, N. and Alturas, B. (2023) ‘Marketing Business Processes in a Multinational Organization: A Case Study of an Information System Implementation’, in, pp. 28–49. Available at: https://doi.org/10.4018/978-1-6684-8958-1.ch002.

Viteri Luque, F., Herrera Lozano, L.A. and Bazurto Quiroz, A.F. (2018) ‘Importancia de las Técnicas del Marketing Digital’, RECIMUNDO: Revista Científica de la Investigación y el Conocimiento, 2(1), pp. 764–783.

Winarso, W. et al. (2023) ‘The Impact of Social Media and Innovation Strategy on the Marketing Performance of Small and Medium Sized Enterprises (Smes) in Bekasi City, Indonesia’, International Journal of Professional Business Review, 8(5), pp. e01688–e01688. Available at: https://doi.org/10.26668/businessreview/2023.v8i5.1688.

Yang, I.L. (2004) ‘Customer service and organizational learning in the context of strategic marketing’, Marketing Intelligence & Planning, 22(6), pp. 652–662. Available at: https://doi.org/10.1108/02634500410559033.

Zangana, H., Omar, M. and Ali, N. (2024) ‘HARNESSING ARTIFICIAL INTELLIGENCE IN MODERN MARKETING: STRATEGIES, BENEFITS, AND CHALLENGES’, 2, pp. 70–82.

Zárraga, L., Morejón, V.M.M. and Sandoval, E.C. (2018) ‘La satisfacción del cliente basada en la calidad del servicio a través de la eficiencia del personal y eficiencia del servicio: un estudio empírico de la industria restaurantera’, Revista de Estudios en Contaduría, Administración e Infomática, 7. Available at: https://www.redalyc.org/articulo.oa?id=637968306002 (Accessed: 31 October 2024).