Faculty of Finance and Banking, Bucharest University of Economic Studies, Bucharest, Romania

Volume 2025,

Article ID 491635,

IBIMA Business Review,

12 pages,

DOI: https://doi.org/10.5171/2025.491635

Received date: 25 November 2024; Accepted date: 27 December 2024; Published date: 27 February 2025

Academic Editor: Florin Cornel Dumiter

Cite this Article as:

Alexandra Ioana VINTILĂ (2025)," Do the Performance and Value of the Companies Influence Corporate Taxation? Empirical Study on Standard & Poor’s 500 Companies", IBIMA Business Review, Vol. 2025 (2025), Article ID 491635, https://doi.org/10.5171/2025.491635

The effective corporate tax rate represents an important tool which could help the management take the best financial decisions within the company. The paper analyzes whether the company performance and the company value influence the effective corporate tax rate, used as a proxy for the corporate taxation. The firm performance is represented by Return on Assets and Return on Equity, while the firm value is expressed as Tobin’s Q and Price-to-Book ratio. The sample consists of the non-financial companies included in the Standard & Poor’s 500 index, over the period 2014-2023. Based on the literature review, there are selected the most relevant factors that could impact the tax burden of the US companies, and the empirical results suggest that, to reduce the corporate taxation, it is necessary to increase the performance and the value of the company, and, furthermore, bigger and older firms register lower effective tax rates.

Keywords: corporate taxation; effective tax rate; company performance; company value; S&P 500 companies.

Introduction

The corporate income tax represents a fundamental tool and a highly debated component of the fiscal system of a country, due to the impact that it could have on the financial decisions within a company (Delgado et al., 2014; Delgado et al., 2018). The effective corporate tax rate, used as a proxy for corporate taxation, measures the overall corporate tax burden and it could provide policymakers with information to help them improve the corporate tax policies, as well as to assess the fairness of the fiscal system (Cao and Cui, 2017).

Over the last decades, two competing theories regarding the effective corporate tax rate have been put forward, namely: the political cost theory and the political power theory. On the one hand, the political cost theory (Watts and Zimmerman, 1978; Zimmerman, 1983) predicts a positive relationship between the firm size and the effective tax rate, meaning that the greater visibility of large and successful companies exposes them to greater regulatory actions by the government and, consequently, the firms are the target of tax provisions which impact them more aggressively. Given the fact that taxes represent a part of the total political costs borne by the companies, the political cost theory claims that larger firms have higher effective tax rates. On the other hand, the political power theory (Siegfried, 1972; Porcano, 1986) suggests a negative relationship between the firm size and the effective tax rate. This influence is explained by the fact that larger companies have substantial resources for tax planning and for the adoption of accounting practices that lower their effective tax rate. Moreover, larger companies can hire professionals which could help them reduce the tax burden of the company, and, thence, the effective corporate tax rate.

In the literature review, there are identified studies which highlight both the political cost theory (Zeng, 2010; Fernández-Rodríguez and Martínez-Arias, 2012; Huang et al., 2013; Delgado et al., 2014; Lazăr, 2014; Cao and Cui, 2017; Vintilă et al., 2018; Panda and Nanda, 2020; Fernández-Rodríguez et al., 2021; Hendayana et al., 2024) and the political power theory (Richardson and Lanis, 2007; Fernández-Rodríguez et al., 2019; Bubanić and Šimović, 2021). Moreover, there are a multitude of factors that can influence the effective corporate tax rate, such as: financial leverage (Gupta and Newberry, 1997; Liu and Cao, 2007; Richardson and Lanis, 2007; Zeng, 2010; Fernández-Rodríguez and Martínez-Arias, 2012; Huang et al., 2013; Delgado et al., 2014; Fernández-Rodríguez and Martínez-Arias, 2014; Lazăr, 2014; Cao and Cui, 2017; Chen et al., 2018; Delgado et al., 2018; Vintilă et al., 2018; Fernández-Rodríguez et al., 2019; James, 2020; Panda and Nanda, 2020; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021; Hendayana et al., 2024; Wang, 2024), capital intensity (Gupta and Newberry, 1997; Liu and Cao, 2007; Richardson and Lanis, 2007; Zeng, 2010; Fernández-Rodríguez and Martínez-Arias, 2012; Huang et al., 2013; Delgado et al., 2014; Fernández-Rodríguez and Martínez-Arias, 2014; Lazăr, 2014; Cao and Cui, 2017; Chen et al., 2018; Delgado et al., 2018; Vintilă et al., 2018; Fernández-Rodríguez et al., 2019; James, 2020; Panda and Nanda, 2020; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021; Hendayana et al., 2024; Wang, 2024), inventory intensity (Gupta and Newberry, 1997; Richardson and Lanis, 2007; Zeng, 2010; Fernández-Rodríguez and Martínez-Arias, 2012; Huang et al., 2013; Delgado et al., 2014; Fernández-Rodríguez and Martínez-Arias, 2014; Chen et al., 2018; Vintilă et al., 2018; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021), research and development intensity (Gupta and Newberry, 1997; Richardson and Lanis, 2007; Fernández-Rodríguez et al., 2019; James, 2020), liquidity (Vintilă et al., 2018), performance (Gupta and Newberry, 1997; Liu and Cao, 2007; Richardson and Lanis, 2007; Zeng, 2010; Fernández-Rodríguez and Martínez-Arias, 2012; Huang et al., 2013; Delgado et al., 2014; Fernández-Rodríguez and Martínez-Arias, 2014; Lazăr, 2014; Cao and Cui, 2017; Chen et al., 2018; Delgado et al., 2018; Vintilă et al., 2018; Fernández-Rodríguez et al., 2019; James, 2020; Panda and Nanda, 2020; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021; Hendayana et al., 2024; Wang, 2024), firm value (James, 2020), firm age (Fernández-Rodríguez et al., 2019; Panda and Nanda, 2020), statutory corporate tax rate (Zeng, 2010; Delgado et al., 2014; Vintilă et al., 2018; Fernández-Rodríguez et al., 2021).

The empirical research analyzes whether the company performance and the company value could affect the effective corporate tax rate. The sample consists of the non-financial companies included in the Standard & Poor’s 500 index, over a period of 10 years, from 2014 to 2023. Based on the literature review, there are selected the most relevant factors that could affect the tax burden of the US companies. Thus, the dependent variable is represented by the effective tax rate, used as a proxy for the corporate taxation, the independent variables are Return on Assets and Return on Equity, as proxies for the firm performance, and Tobin’s Q and Price-to-Book ratio, as proxies for the firm value, and there are also used control variables which highlight the indebtedness, capital intensity, liquidity, firm age, and firm size. There are several estimated unbalanced panel data regression models, with fixed effects and with random effects, using Stata 18 software, and the empirical results are interpreted from both a statistical and an economic standpoint.

Literature Review

The international specialized literature on corporate taxation is focused on the factors that could influence the effective corporate tax rate. Several empirical studies have been carried out on samples of companies from the same country, such as China (Liu and Cao, 2007; Zeng, 2010; Huang et al., 2013; Cao and Cui, 2017; Chen et al., 2018; Wang, 2024), Germany (Delgado et al., 2018), Spain (Fernández-Rodríguez et al., 2019), United States of America (Gupta and Newberry, 1997), Croatia (Bubanić and Šimović, 2021), Indonesia (Hendayana et al., 2024), India (Panda and Nanda, 2020), Romania (Lazăr, 2014), Australia (Richardson and Lanis, 2007), whereas a few econometric studies have analyzed the determinants of effective tax rate in multiple countries, respectively European countries (Delgado et al., 2014; Vintilă et al., 2018), BRICS countries (Fernández-Rodríguez and Martínez-Arias, 2014; Fernández-Rodríguez et al., 2021), MINT countries (Fernández-Rodríguez et al., 2021).

Two of the first researchers that analyzed the effective corporate tax rate are Gupta and Newberry (1997) who focused on six factors that could affect the corporate tax burden, namely: firm size, capital structure, capital intensity, inventory intensity, research and development intensity, and firm performance. The empirical results suggested that financial leverage used as a proxy for capital structure, inventory intensity, and return on assets used as a proxy for firm performance have a positive impact on effective tax rate, capital intensity and research and development intensity negatively affect the tax burden, while firm size was found to be statistically insignificant.

Moreover, in a scientific paper (Cao and Cui, 2017), there are analyzed the determinants of the effective tax rate of Chinese companies over the period 2008-2015; the reason why Cao and Cui (2017) chose 2008 as the first year was that 2008 was the year that China introduced a new corporate income tax law and decreased the statutory tax rate from 33% to 25%. The authors identified a positive impact of firm size and non-operating expense, while leverage, capital intensity, return on assets, preferential tax rate and investment gain have a negative influence on effective tax rate. Chen et al. (2018) and Zeng (2010) consider that state ownership and ownership concentration have a significant impact on tax reporting practices in China, given the fact that Chinese listed firms have high levels of state ownership and ownership concentration. The studies show that companies with more shares held by the largest, respectively the five largest shareholders, pay low taxes. However, Liu and Cao (2007) identified a positive influence of ownership concentration on effective tax rate of Chinese companies. The tax burden of Chinese listed companies is also analyzed by Huang et al. (2013), who identified four key determinants, respectively firm-specific attributes, ownership structure, industry upgrading, and tax reforms. The findings suggest that while there is a positive linear relation between firm size, capital intensity, inventory intensity and effective tax rate, between financial leverage and effective tax rate there is a non-linear relation, meaning that tax rates are negatively related to leverage, but the relationship becomes less negative as leverage keeps increasing. A positive impact of firm size and a negative influence of financial leverage was also disclosed by Lazăr (2014), using a sample of Romanian non-financial companies listed on the Bucharest Stock Exchange. Contrary to Huang et al. (2013), Lazăr (2014) identified that capital intensity has a negative influence, and return on assets has a positive impact on effective tax rate. The political cycle of Provincial Party Congresses has also an important impact on the effective tax rate in China (Wang, 2024). Thus, effective tax rate rises in the year before and during the Provincial Party Congresses, and then declines. Wang (2024) also indicates a positive influence of the debt level of the company, and the negative impact of fixed assets and return on assets on the effective tax rate of Chinese companies.

In two interesting empirical research studies, there are investigated, on the one hand, the determinants of the effective tax rate of the companies from the European Union (Delgado et al., 2014), and, on the other hand, the relationship between company size and effective tax rate of German companies (Delgado et al., 2018), over the period 1992-2009, using quantile regression models. The studies disclose a positive impact of the leverage (Delgado et al., 2014; Delgado et al., 2018), the company size (Delgado et al., 2014), the capital intensity (Delgado et al., 2014), the inventory intensity (Delgado et al., 2014), contrary to return on assets which impacts positively (Delgado et al., 2014) or negatively (Delgado et al., 2018) the effective tax rate. The determinants of effective tax rate are also analyzed in the BRICS and MINT countries (Fernández-Rodríguez et al., 2021), and the empirical results relieve a positive influence of firm size, inventory intensity and government effectiveness, and a negative impact of leverage, capital intensity, profitability, firm growth, on the tax burden for firms in emerging countries. Fernández-Rodríguez and Martínez-Arias (2014) have similar approaches, studying the factors affecting the effective tax rate of companies from BRIC countries, over the period 2000-2009, using a generalized method of moments estimation. The same group of authors (Fernández-Rodríguez and Martínez-Arias, 2012) identified the factors affecting tax burden of companies in China and the United States and concluded that US firms have higher effective tax rates than Chinese firms, and there is a non-linear relationship between firm size, firm leverage, respectively capital intensity, and effective tax rate. Moreover, Fernández-Rodríguez et al. (2019) found out that ownership structure and firm size have a meaningful influence on tax burden of Spanish companies. Thus, state-owned enterprises present lower effective tax rates than non-state-owned enterprises, and firm size negatively affects tax burden, meaning that larger companies have a lower effective tax rate.

According to Vintilă et al. (2018), liquidity represents another factor that could influence the effective corporate tax rate. The study is carried out on a sample of companies listed on five Eastern European stock exchanges, covering the period 2000-2016. The empirical results suggest that companies with higher liquidity rates, capital and inventory intensity, profitability, and more indebtedness, register a higher effective tax rate. Furthermore, Hendayana et al. (2024) also identified a positive influence of firm size and financial leverage on the effective tax rates of the LQ45 companies listed on the Indonesia Stock Exchange, over the period 2019-2022. However, a negative impact of firm size and financial leverage and a positive influence of inventory intensity on the effective tax rate was identified by Richardson and Lanis (2007), and Bubanić and Šimović (2021). Moreover, asset profitability positively affects the effective tax rate of Australian companies (Richardson and Lanis, 2007), and negatively impacts the tax burden of the Croatian firms (Bubanić and Šimović, 2021).

The receptiveness of effective tax rate to firm characteristics is analyzed by Panda and Nanda (2020), on a sample of Indian manufacturing companies, from 2007 to 2017. Thus, firm size, non-debt tax shield, return on assets, and firm growth rate have a positive impact on effective tax rate, as opposed to asset tangibility which negatively affects the corporate taxation. James (2020) examined the relation between CEO age and tax planning, and considered that CEO age positively affects the cash and GAAP effective tax rates, and negatively influences the permanent book‐tax difference, suggesting that the older the CEO is, the less likely he is to take measures to reduce the company tax burden.

Based on the research framework, the following hypotheses are formulated:

Hypothesis 1: Company performance negatively impacts the effective tax rate (Huang et al., 2013; Cao and Cui, 2017; Chen et al., 2018; Delgado et al., 2018; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021; Wang, 2024).

Hypothesis 2: Company indebtedness has a negative influence on the effective tax rate (Liu and Cao, 2007; Richardson and Lanis, 2007; Huang et al., 2013; Lazăr, 2014; Cao and Cui, 2017; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021).

Hypothesis 3: Capital intensity negatively affects the effective tax rate (Gupta and Newberry, 1997; Richardson and Lanis, 2007; Lazăr, 2014; Cao and Cui, 2017; Chen et al., 2018; Panda and Nanda, 2020; Fernández-Rodríguez et al., 2021; Wang, 2024).

Hypothesis 4: Liquidity exerts a positive impact on the effective tax rate (Vintilă et al., 2018).

Hypothesis 5: Company size has a negative influence on the effective tax rate (Richardson and Lanis, 2007; Fernández-Rodríguez et al., 2019; Bubanić and Šimović, 2021).

These hypotheses are tested within the empirical models regarding the determinants of the effective tax rate of the S&P 500 companies.

Research Methodology

Database and Research Variables

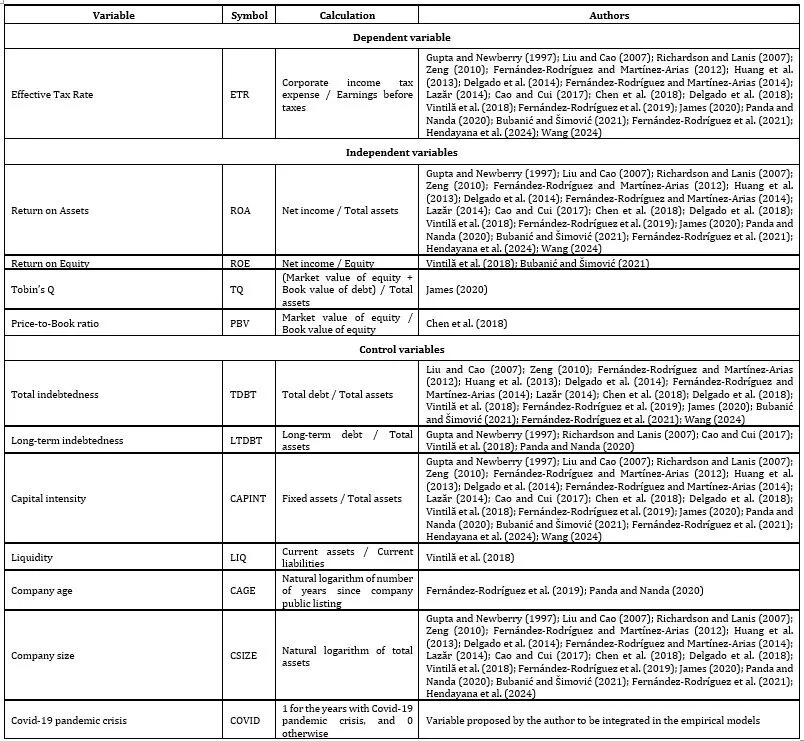

To analyze whether the company performance and the company value, along with other factors, affect the effective corporate tax rate, there were sampled data from Thomson Reuters Eikon platform, for the non-financial companies included in the Standard & Poor’s 500 index, over the period 2014-2023, cumulating a total number of 4420 statistical observations. The dependent variable is represented by the effective tax rate, while the independent variables are represented by financial indicators that measure the company performance (expressed both as Return on Assets and Return on Equity) and the company value (expressed both as Tobin’s Q and Price-to-Book ratio). The detailed presentation of all the variables is highlighted in Table 1.

Table 1. Variables description

Source: author’s own processing

Alongside the variables included in the previous studies, there was proposed and used a new control variable represented by a dummy variable which analyzes the impact that Covid-19 pandemic crisis had on the effective tax rate of the S&P 500 companies, given the fact that the analyzed period also includes the Covid-19 pandemic crisis.

Descriptive Statistics and Correlation Analysis

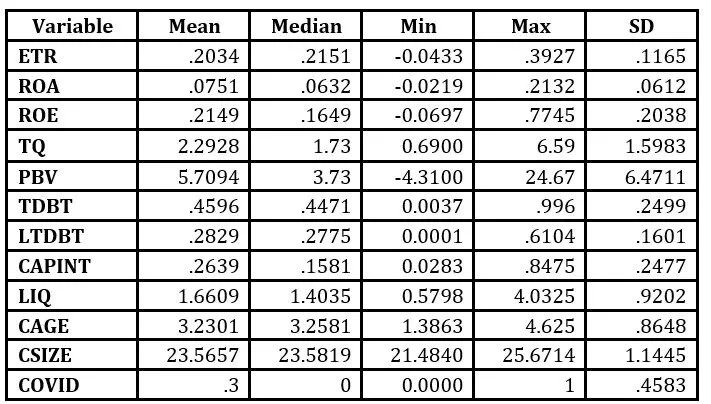

Table 2 reports the descriptive statistics, namely the mean, median, minimum, maximum and standard deviation, for all the variables included in the econometric analysis. The variables are winsorized at the 5th and 95th percentiles, to reduce the effects of the outliers. The descriptive statistics indicate that the mean of the effective tax rate of the S&P 500 companies, over the period 2014-2023, is 20.34%, while the median is 21.51%. Regarding the firm performance, the average return on equity is greater than the average return on assets, while the firm value expressed as Tobin’s Q has a mean of 2.29, and expressed as Price-to-Book ratio has an average of 5.71.

Table 2. Descriptive statistics

Source: author’s own processing

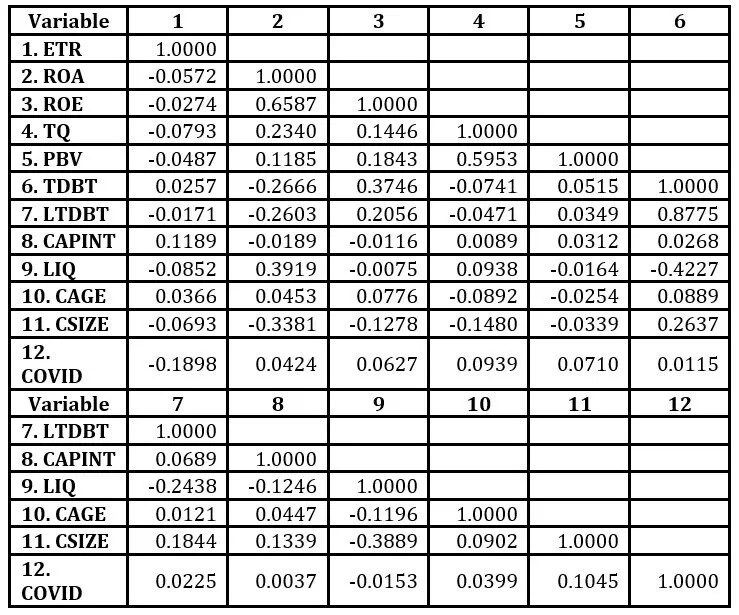

Table 3 presents the correlation matrix of the variables used in the empirical models.

Table 3. Correlation matrix

Source: author’s own processing

There can be observed positive and strong correlations only between the company performance variables, the firm value variables, and the company indebtedness variables, meaning that these indicators will be used in distinct regression models.

Empirical Analysis and Regression Results

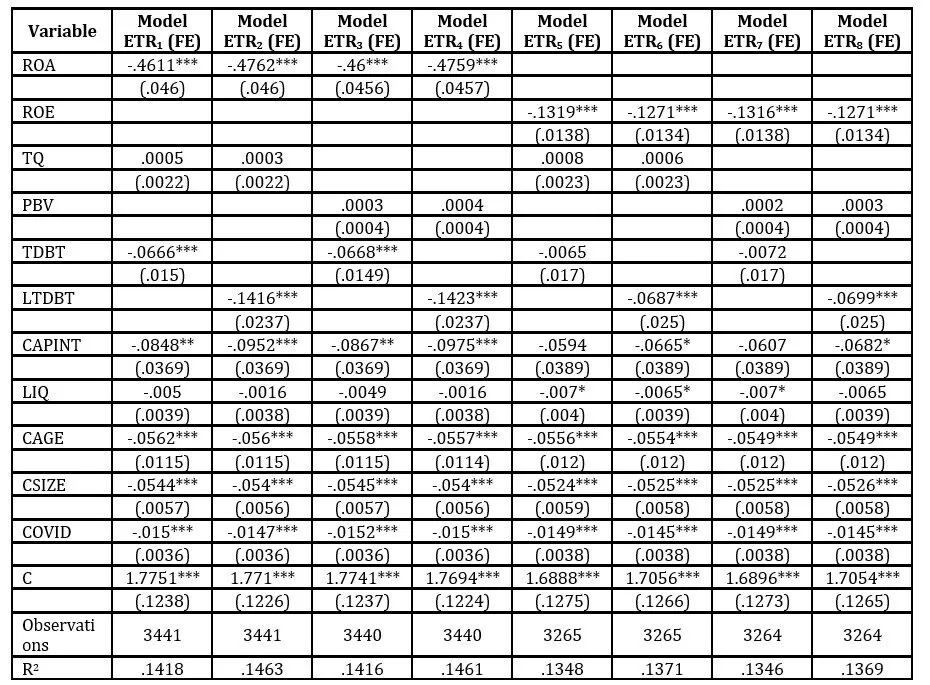

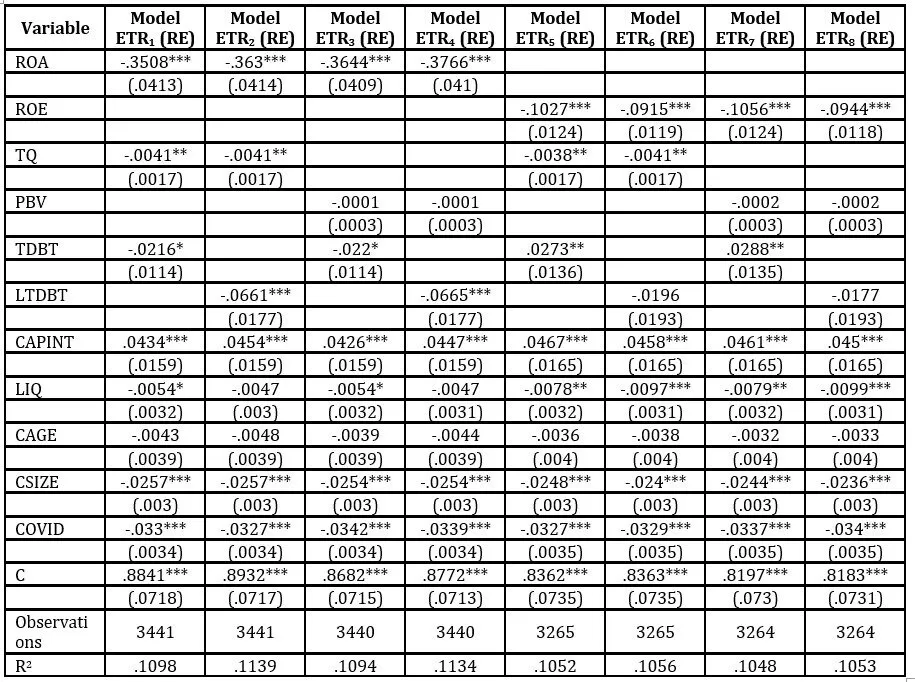

To analyze the impact of the determinants on the effective tax rate of the S&P 500 companies, from the period 2014-2023, there are estimated multiple regression models, with unbalanced panel data, with fixed effects and random effects, using Stata 18 software. In Table 4, there are highlighted the empirical results for the fixed effects (FE) regression models, and, in Table 5, there are presented the econometric results for the random effects (RE) regression models.

Table 4. Determinants of the effective tax rate (fixed effects models)

Source: author’s own computation using Stata 18 software. Significance level: *** p<.01, ** p<.05, * p<.1. Standard errors are displayed in brackets.

Table 5. Determinants of the effective tax rate (random effects models)

Source: author’s own computation using Stata 18 software. Significance level: *** p<.01, ** p<.05, * p<.1. Standard errors are displayed in brackets.

The company size represents one of the most used factors in the analysis of the determinants of the corporate tax burden. The company size has a negative influence on the tax burden, being in accordance with the political power theory, that suggests a negative relationship between firm size and effective tax rate. Thus, hypothesis 5 is accepted (Richardson and Lanis, 2007; Fernández-Rodríguez et al., 2019; Bubanić and Šimović, 2021), meaning that the S&P 500 companies, which are larger companies, have more resources for tax planning, and also have a greater influence on regulators, trying to lower their effective tax rate. Alongside the company size, the company performance, represented by Return on Assets and Return on Equity, and the company value, expressed as Tobin’s Q, negatively affect the effective tax rate. More profitable and more valuable firms are more efficient and have more tax planning instruments to reduce the tax burden. Therefore, hypothesis 1 is accepted (Huang et al., 2013; Cao and Cui, 2017; Chen et al., 2018; Delgado et al., 2018; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021; Wang, 2024).

Regarding the company indebtedness, it is observed a negative influence of long-term debt on the effective tax rate. Given the fact that interest expenditures, associated with debt financing, are tax deductible, while dividends, associated with equity financing, are not, companies with higher long-term debt have a lower effective tax rate (Richardson and Lanis, 2007; Cao and Cui, 2017). However, total debt has both a positive and a negative impact on tax burden, meaning that hypothesis 2 is rejected. Moreover, fixed assets are also important in the context of taxation, because depreciation and amortization are tax-deductible expenses. In the empirical analysis, capital intensity negatively affects the tax burden only in the fixed effects models, showing that, the greater the investment in tangible assets, the greater the tax saving from the depreciation and amortization expenses, and the lower the effective corporate tax rate (Gupta and Newberry, 1997; Richardson and Lanis, 2007; Lazăr, 2014; Cao and Cui, 2017; Chen et al., 2018; Panda and Nanda, 2020; Fernández-Rodríguez et al., 2021; Wang, 2024). Thus, hypothesis 3 cannot be accepted. Hypothesis 4 is also rejected, because liquidity negatively impacts the effective tax rate of the S&P 500 companies. The company age also negatively affects the effective tax rate. Older companies have more experience and are expected to bear a lower tax burden. Besides, older companies tend to use more debt financing, and an increased level of debt reduces the tax burden. Relating to the new control variable proposed, it can be observed that the Covid-19 pandemic crisis had a beneficial effect on the company taxation, because, during the Covid-19 period, the effective tax rate of the S&P 500 companies decreased.

Conclusion

The paper investigated whether the company performance and the company value affect the effective tax rate, using a sample of non-financial companies included in the Standard & Poor’s 500 index, over the period 2014-2023. Based on the literature review, there were selected the most relevant variables which could influence the tax burden and, because the period analyzed includes the Covid-19 pandemic crisis, there was also included a new control variable which determined whether the Covid-19 period had an impact on the corporate taxation.

The empirical results highlighted, mainly, the negative influence of the factors on the effective tax rate. The factors which negatively affect the tax burden are represented by company performance (Huang et al., 2013; Cao and Cui, 2017; Chen et al., 2018; Delgado et al., 2018; Bubanić and Šimović, 2021; Fernández-Rodríguez et al., 2021; Wang, 2024), company value expressed as Tobin’s Q, long-term indebtedness (Richardson and Lanis, 2007; Cao and Cui, 2017), liquidity, company age, company size (Richardson and Lanis, 2007; Fernández-Rodríguez et al., 2019; Bubanić and Šimović, 2021), and the Covid-19 pandemic crisis. However, the total indebtedness and the capital intensity had both a positive and a negative influence on the effective tax rate, while Price-to-Book ratio, used as a proxy for firm value, was statistically insignificant.

In conclusion, the results of the empirical study showed that US companies can reduce their effective tax rate through a multitude of factors, and the pandemic period helped firms reduce their corporate taxation.

References

Bubanić, M. and Šimović, H. (2021). Determinants of the effective tax burden of companies in the Telecommunications activities in the Republic of Croatia. Zagreb International Review of Economics and Business, 24(2), 59-76. doi:10.2478/zireb-2021-0011

Cao, J. and Cui, Y. (2017). An Alternative View on Determinants of the Effective Tax Rate: Evidence from Chinese Listed Companies. Emerging Markets Finance and Trade, 53(5), 1001-1014. doi:10.1080/1540496X.2016.1256113

Chen, X., Lin, X., Ding, W. and Zhu, K. (2018). State ownership, performance evaluation and tax avoidance. China Journal of Accounting Studies, 6(1), 84-105. doi:10.1080/21697213.2018.1494109

Delgado, F. J., Fernández-Rodríguez, E. and Martínez-Arias, A. (2014). Effective Tax Rates in Corporate Taxation: a Quantile Regression for the EU. Engineering Economics, 25(5), 487-496. doi:10.5755/j01.ee.25.5.4531

Delgado, F. J., Fernández-Rodríguez, E. and Martínez-Arias, A. (2018). Corporation effective tax rates and company size: evidence from Germany. Economic Research-Ekonomska Istraživanja, 31(1), 2081-2099. doi:10.1080/1331677X.2018.1543056

Fernández-Rodríguez, E., García-Fernández, R. and Martínez-Arias, A. (2019). Influence of Ownership Structure on the Determinants of Effective Tax Rates of Spanish Companies. Sustainability, 11(5), 1-19. doi:10.3390/su11051441

Fernández-Rodríguez, E., García-Fernández, R. and Martínez-Arias, A. (2021). Business and institutional determinants of Effective Tax Rate in emerging economies. Economic Modelling, 94, 692-702. doi:10.1016/j.econmod.2020.02.011

Fernández-Rodríguez, E. and Martínez-Arias, A. (2012). Do Business Characteristics Determine an Effective Tax Rate? The Chinese Economy, 45(6), 60-83. doi:10.2753/CES1097-1475450604

Fernández-Rodríguez, E. and Martínez-Arias, A. (2014). Determinants of the Effective Tax Rate in the BRIC Countries. Emerging Markets Finance and Trade, 50(sup3), 214-228. doi:10.2753/REE1540-496X5003S313

Gupta, S. and Newberry, K. (1997). Determinants of the variability in corporate effective tax rates: Evidence from longitudinal data. Journal of Accounting and Public Policy, 16(1), 1-34. doi:10.1016/S0278-4254(96)00055-5

Hendayana, Y., Arief Ramdhany, M., Pranowo, A. S., Abdul Halim Rachmat, R. and Herdiana, E. (2024). Exploring impact of profitability, leverage and capital intensity on avoidance of tax, moderated by size of firm in LQ45 companies. Cogent Business & Management, 11(1), 1-13. doi:10.1080/23311975.2024.2371062

Huang, D. F., Chen, N. Y. and Gao, K. W. (2013). The tax burden of listed companies in China. Applied Financial Economics, 23(14), 1169-1183. doi:10.1080/09603107.2013.786163

James, H. L. (2020). CEO age and tax planning. Review of Financial Economics, 38(2), 275-299. doi:10.1002/rfe.1072

Lazăr, S. (2014). Determinants of the Variability of Corporate Effective Tax Rates: Evidence from Romanian Listed Companies. Emerging Markets Finance and Trade, 50(sup4), 113-131. doi:10.2753/REE1540-496X5004S4007

Liu, X. and Cao, S. (2007). Determinants of Corporate Effective Tax Rates: Evidence from Listed Companies in China. The Chinese Economy, 40(6), 49-67. doi:10.2753/CES1097-1475400603

Panda, A. K. and Nanda, S. (2020). Receptiveness of effective tax rate to firm characteristics: an empirical analysis on Indian listed firms. Journal of Asia Business Studies, 15(1), 198-214. doi:10.1108/JABS-11-2018-0304

Porcano, T. M. (1986). Corporate tax rates: progressive, proportional or regressive. The Journal of the American Taxation Association, 7, 17-31.

Richardson, G. and Lanis, R. (2007). Determinants of the variability in corporate effective tax rates and tax reform: Evidence from Australia. Journal of Accounting and Public Policy, 26(6), 689-704. doi:10.1016/j.jaccpubpol.2007.10.003

Siegfried, J. J. (1972). The relationship between economic structure and the effect of political influence: empirical evidence from the Federal Corporation Income Tax Program. Ph.D. dissertation, University of Wisconsin.

Vintilă, G., Gherghina, Ş. C. and Păunescu, R. A. (2018). Study of Effective Corporate Tax Rate and Its Influential Factors: Empirical Evidence from Emerging European Markets. Emerging Markets Finance and Trade, 54(3), 571-590. doi:10.1080/1540496X.2017.1418317

Wang, L. (2024). Political cycle and effective corporate tax rate: evidence from China. Applied Economics, 56(9), 1035-1048. doi:10.1080/00036846.2023.2174937

Watts, R. L. and Zimmerman, J. L. (1978). Towards a Positive Theory of the Determination of Accounting Standards. The Accounting Review, 53(1), 112-134.

Zeng, T. (2010). Ownership Concentration, State Ownership, and Effective Tax Rates: Evidence from China’s Listed Firms. Accounting Perspectives, 9(4), 271-289. doi:10.1111/j.1911-3838.2010.00014.x

Zimmerman, J. L. (1983). Taxes and firm size. Journal of Accounting and Economics, 5, 119-149. doi:10.1016/0165-4101(83)90008-3