Aymane CHEMMAA, Mohammed IBRAHIMI and Mohammed AMINE

Hassan II University of Casablanca, ENCG Casablanca, Casablanca, Morocco

Volume 2025,

Article ID 997800,

IBIMA Business Review,

19 pages,

DOI: https://doi.org/10.5171/2025.997800

Received date: 3 April 2025; Accepted date: 20 June 2025; Published date: 31 July 2025

Academic Editor: Kamal Abou El Jaouad

Cite this Article as:

Aymane CHEMMAA, Mohammed IBRAHIMI and Mohammed AMINE (2025)," Do Boards of Directors Influence Earnings Management Practices ? The Case of Moroccan Listed Firms", IBIMA Business Review, Vol. 2025 (2025), Article ID 997800, https://doi.org/10.5171/2025.997800

Although many countries have implemented corporate governance reforms, empirical assessments of their effectiveness remain scarce, particularly in emerging economies like Morocco. This study aims to bridge this gap by examining the impact of Morocco’s 2008 Corporate Governance Code on earnings management practices among firms listed on the Casablanca Stock Exchange over the period 2018–2022. Using the Generalized Method of Moments (GMM) on a panel dataset of 34 firms, the findings reveal that board independence and the Moroccan nationality of the board chair are negatively and significantly associated with earnings management, suggesting their effectiveness in mitigating opportunistic financial reporting. Conversely, gender diversity and the frequency of board meetings are positively and significantly related to earnings manipulation, indicating that, under certain conditions, these governance attributes may inadvertently enable such behavior. Furthermore, board size shows a positive but statistically insignificant relationship, suggesting that increasing board membership does not necessarily curtail earnings management. Overall, this research provides new empirical evidence on the outcomes of governance reforms in Morocco and enriches the understanding of corporate governance mechanisms in emerging market contexts.

Keywords: Earnings management; Board of directors; Cultural values; Morocco; Emerging markets; COVID-19.

Introduction

As of 2024, mitigating fraud-related risks, including earnings management, remains a global priority for firms. According to the Association of Certified Fraud Examiners (2024), 58% of fraud cases are detected through proactive board oversight, underscoring boards’ pivotal role in risk prevention. This highlights the necessity of ethical practices and transparent environments to safeguard shareholder and stakeholder interests (García-Olalla and Vázquez-Ordás, 2024). Earnings management has emerged as a critical concern in emerging markets. Almarayeh and al. (2024) argue that corporate governance mechanisms often fail to align with institutional context-specific nuances, which explains the prevalence of earnings management in emerging markets. Furthermore, 56% of publications on corporate governance and earnings management have been produced between 2018 and 2024, reflecting a growing academic interest in this topic over the past six years (Chemmaa and Ibrahimi, 2025).

Similar to Western companies, accounting scandals have also affected the African continent. Kaituko and al. (2023) showed that financial statement fraud has become common in many manufacturing companies listed on the East African Stock Exchange Association. Likewise, in Morocco, several companies have been accused of manipulating their financial results (Ibrahimi and Baghdadi, 2024). These accounting scandals have shaken investor confidence in the accuracy of the accounting and financial information provided by the Moroccan stock market, thus questioning the effectiveness of governance mechanisms. In addition to these scandals, the Moroccan stock market has experienced several events, such as the adverse effects of the 2008 global financial crisis, the Arab Spring in the MENA region in 2011, and various geopolitical events, leading to a loss of approximately 6.40% of its market capitalization in 2015 and 6.70% in 2020 (Ibrahimi and El Baghdadi, 2023). Consequently, future research should prioritize examining the relationship between corporate governance and earnings management, especially in emerging economies within the Middle East and North Africa (MENA) region(Afifa and al., 2022; Chemmaa and Ibrahimi, 2025).

To restore stakeholder confidence in the Moroccan stock market, the National Commission for Corporate Governance (CNGE) developed the first Moroccan Code of Good Corporate Governance Practices in 2008. The main objective of this code was to enhance governance mechanisms, improve transparency, and mitigate risks. However, to date, no study has provided evidence on the effectiveness of this governance code in improving the quality of financial reporting following crises such as the COVID-19 pandemic and the 2018 boycott movement. Similarly, Ibrahimi and Baghdadi (2024) highlighted the need to assess the code’s effectiveness in mitigating risks related to earnings management. These findings emphasize the crucial role of boards of directors in strengthening financial transparency and control mechanisms.

In this context, our study aims to assess the effectiveness of the 2008 Moroccan Corporate Governance Code by analyzing the impact of board characteristics on earnings management practices among companies listed on the Casablanca Stock Exchange between 2018 and 2022. It examines factors such as board size, board independence, CEO duality, gender diversity, and financial expertise of board members, drawing on the recommendations of Almarayeh and al. (2024) and Saleh and al. (2022), who explored these issues in the MENA region.

This study has important implications for academics, practitioners, and policymakers. For the academic community, this research contributes to the literature by analyzing governance mechanisms in an emerging market like Morocco. Unlike studies primarily focused on developed economies, it highlights board characteristics such as size, independence, gender diversity, board meetings, and the nationality of the board chair, providing a detailed analysis in response to suggestions from researchers such as Ibrahimi and Baghdadi (2024), Attia and al. (2022) and Al-Haddad and Whittington (2019). Additionally, our study paves the way for future comparative research exploring differences in governance mechanisms between developed and emerging economies. For practitioners, the results highlight the importance of enhancing board diversity, strengthening board independence, and improving the financial expertise of directors to enhance the quality of strategic decisions and financial reporting. In the African context, where emerging financial markets face challenges such as economic volatility and evolving regulatory frameworks, these recommendations are particularly relevant. They can help mitigate opportunistic earnings management practices, improve financial transparency, and boost investor confidence—crucial factors for attracting capital and supporting economic development in the region.

For regulators and policymakers, particularly regulatory authorities in emerging economies, this study highlights the importance of board chair nationality, board independence, and gender diversity in enhancing the effectiveness of corporate governance mechanisms. These factors play a crucial role in strengthening transparency and the quality of financial reporting, especially in an economic context shaped by the COVID-19 pandemic and the 2018 boycott movement. The study also underscores the need to align corporate practices with national regulations to ensure stable and equitable governance.

The paper proceeds as follows: Section 2 develops the theoretical framework and hypotheses, Section 3 outlines the sample, variables, and research methodology, Section 4 presents the empirical results, Section 5 discusses the findings, and Section 6 concludes.

Literature Review

Context

Over the past decades, the MENA region has undergone significant transformations, with major reforms aimed at modernizing institutional and financial infrastructures (Ibrahimi and al., 2021). In this context, Morocco has distinguished itself through ambitious initiatives to strengthen its institutional framework and modernize its financial sector. Since the 2000s, the country has undertaken a series of reforms to align its practices with international standards, enhance transparency, and increase its global attractiveness (Ibrahimi and Baghdadi, 2024). These efforts have intensified in recent years, with measures focused on consolidating macroeconomic stability and strengthening resilience against international crises, paving the way for sustainable and inclusive growth. In 2023, Morocco demonstrated remarkable economic resilience in the face of multiple shocks, including the COVID-19 pandemic, drought, and inflation. The country recorded a growth rate of 3.4%, while inflation was reduced to 1.7% in 2024 (Word Bank, 2024). This performance was supported by major structural reforms, such as the restructuring of state-owned enterprises and the rationalization of public spending. These initiatives aim to enhance governance and stimulate employment, particularly for SMEs, further consolidating macroeconomic stability (IMF, 2024). At the same time, Morocco has strengthened its attractiveness to foreign direct investment (FDI), positioning itself as a regional hub in strategic sectors such as automotive, aerospace, and renewable energy. The rise of Greenfield projects, particularly in green hydrogen, has contributed to this momentum (EY Attractiveness Africa, 2023);

On the financial front, the Casablanca Stock Exchange posted strong performance in 2023, with the MASI index rising by 12.80% and the MASI.20 index by 15.44%. This growth was driven by the finance, energy, and construction materials sectors. Market capitalization reached 626 billion dirhams, reflecting the stock market’s resilience despite a volatile international environment (Casablanca Stock Exchange, 2023). In terms of governance, Morocco ranks among the top 20 African countries according to the Ibrahim Index of African Governance (IIAG), with a score of 62/100 in 2024. While the country performs well in security and economic development, further efforts are needed to improve transparency and human rights to align with leading African nations such as Mauritius and Seychelles (Bangoura, 2024).

Moreover, Morocco has strengthened its strategic position in Africa, becoming the continent’s second-largest investor, with foreign direct investments exceeding $800 million in 2021. This growth has been particularly driven by its reintegration into the African Union in 2017, further solidifying its role as a regional economic and financial hub (Ibrahimi and Baghdadi, 2024). This dynamic is also supported by South-South cooperation and the implementation of the African Continental Free Trade Area (AfCFTA) (IFC, 2021).

In this evolving landscape, studying corporate governance in Moroccan firms is particularly relevant. The impact of board characteristics on earnings management remains a critical area requiring further exploration, especially regarding accounting manipulations and the evolution of governance practices within the country. Ibrahimi and Baghdadi (2024) have shown that Moroccan firms engage in earnings management practices. They suggest that examining the effectiveness of governance systems in preserving financial information quality is essential. The 2008 Moroccan Corporate Governance Code introduced key recommendations to enhance corporate governance, particularly concerning board structures. It advocates for at least one-third of board members to be independent, ensuring objective decision-making and mitigating conflicts of interest. Additionally, it encourages gender diversity on boards, enriching perspectives and expertise. The Code also recommends regular board meetings to ensure effective oversight and strategic decision-making. These principles align with the “comply or explain” mechanism, allowing companies to deviate from recommendations as long as they provide justifications, thereby encouraging the adoption of best governance practices. This framework balances flexibility with accountability, ultimately reinforcing transparency and improving corporate governance quality.

Hypotheses

Earnings management is defined as a process where managers adjust financial information while complying with accounting standards to achieve the organization’s desired objectives (Davidson and al., 1987). According to Schipper (1989), this practice is often used by managers to avoid losses or declines in results. Persakis and Iatridis (2015) argue that earnings management is used by managers to mitigate negative reactions from investors, particularly when their financial performance deteriorates. Hsu and Yang (2022) emphasize that earnings management played a key role during the economic crisis related to the pandemic by helping companies temporarily mask their financial difficulties. Finally, Haw and al. (2005) show that companies tend to report positive results to maintain the stability of their stock prices, prepare for operations such as IPOs, or avoid sanctions like delisting.

Lo (2008) shows that earnings management includes two forms: accounting earnings management and real earnings management. Accounting earnings management occurs when managers take advantage of the flexibility provided by accounting standards to make discretionary adjustments, either to improve or worsen the income statement. Real earnings management is defined as decisions made by managers to influence the actual activities of the company, such as abnormal cash flows, abnormal production costs, and abnormal discretionary expenses.

Board Size

The literature provides mixed results regarding the impact of board size on earnings management. The first category suggests that a large board is effective in limiting earnings management practices and beneficial in terms of sharing knowledge and opinions among directors (Rajeevan and Ajward, 2020). For instance, Hunjra and al. (2025) demonstrate that in South Asian listed companies, a larger board has a significant negative effect on earnings management, indicating that larger boards contribute to reducing such practices. Similarly, Lu and Boateng (2018) argue that a large board can enhance board effectiveness in supervision and control, thus helping to limit earnings management, especially during periods of crisis (Hsu and Yang, 2022). However, another strand of research supports a small-sized board. In this regard, (Abdou and al., 2020) show that a small board is effective in reducing earnings management practices because it fosters communication, coordination, and quicker decision-making. Thus, a large board seems to be less effective due to bureaucracy and conflicts that may arise among directors (Jamaludin and al., 2015). Finally, some researchers report a non-significant relationship between board size and earnings management (Almarayeh and al. 2024; Le and Nguyen, 2022), suggesting that the board size does not directly influence the ability to limit earnings management practices. In this study, we consider that board size is negatively associated with earnings management. This hypothesis is based on the 2018 report from the Moroccan Institute of Directors, which states that the board of directors is responsible for evaluating internal control mechanisms, preventing opportunistic behavior, and improving the quality of financial reporting.

H1: Board size has a negative relationship with earnings management in Moroccan companies.

Independence of the board of directors

According to agency theory, the independence of the board of directors is considered an effective control mechanism to limit earnings management practices and reduce agency conflicts (Fama and Jensen, 1983). In this regard, Almubaydeen and Al-Eyasrah (2025) showed that board independence significantly reduces earnings management practices in industrial companies listed on the Amman Stock Exchange. This suggests that external directors play a key role in overseeing management’s actions by offering valuable advice based on their experience (Saona and al. 2020). Furthermore, Attia and al. (2022) and Paul and al. (2023) found a negative relationship between board independence and earnings management. They concluded that the presence of independent directors strengthens the control and oversight system, thereby reducing these practices. Similarly, Beasley (1996) demonstrates that the probability of detecting financial fraud is lower in companies with a higher proportion of external directors. However, Saleh and al. (2022) suggest a positive relationship between board independence and earnings management in a sample of 480 non-financial companies from MENA countries between 2012 and 2019. They explain this finding by the power of large shareholders to appoint friends or family members as external directors, which could influence the board’s effectiveness. Finally, Almarayeh and al. (2024) and Paul and al. (2020) did not find a significant relationship between board independence and earnings management in the MENA region and Nigerian companies, respectively. Additionally, Park and Shin (2004) argue that external directors fail to reduce earnings management, particularly in cases of income smoothing or loss avoidance. In this study, we hypothesize that the presence of independent directors is likely to strengthen the control system and reduce earnings management practices. This hypothesis aligns with the recommendations of the Moroccan Corporate Governance Code of March 2008, which emphasizes the importance of non-executive directors possessing the objectivity and independence necessary to perform their duties effectively and impartially (Moroccan Capital Market Authority, 2008).

H2: Board independence has a negative relationship with earnings management in Moroccan companies.

Gender Diversity

Gender diversity, particularly the representation of women on boards of directors, continues to be a topic of debate in the literature, especially regarding its impact on earnings management practices. Several studies suggest that gender diversity is negatively associated with earnings management (Almubaydeen and Al-Eyasrah, 2025; Huang and al., 2021; Mensah and Boachie, 2023). In this regard, Almubaydeen and Al-Eyasrah (2025) demonstrated that gender diversity improves the quality of financial outcomes in large listed companies in India. Furthermore, Mensah and Boachie (2023) found that an increased presence of women on boards enhances the effectiveness of management control, thereby better meeting stakeholder expectations. Female directors are also perceived to possess specific skills in overseeing management, adopting more conservative strategies, and avoiding earnings management practices to protect the company’s reputation (García Lara and al., 2017). However, another strand of research supports a positive relationship between gender diversity and earnings management practices (Biswas and al., 2022; Fan and al., 2019). Biswas and al. (2022) observed that gender diversity does not mitigate earnings management practices in Indian commercial banks, attributing this to the predominance of men and a highly masculinized organizational culture (Sheedy and Lubojanski, 2018). Finally, some studies report an insignificant relationship between gender diversity and earnings management (Almarayeh and al., 2024; Kalantonis and al., 2021). In our research, we hypothesize that gender diversity is negatively associated with earnings management. This hypothesis is consistent with the findings of a report by the International Finance Corporation (2022), which analyzes the impact of gender diversity on board effectiveness in Morocco, particularly within the framework of reforms mandating female representation of 30% by 2024 and 40% by 2027.

H3: Gender diversity has a negative relationship with earnings management in Moroccan companies.

Board Meetings

The frequency of board meetings is considered an effective control mechanism aimed at enhancing the board’s efficiency in performing its duties, particularly in overseeing management’s actions (Almarayeh, 2021). A strand of literature supports a negative relationship between the frequency of board meetings and earnings management (Bajra and Cadez, 2018; Eze, 2017; Hunjra and al., 2025). In this regard, Hunjra and al. (2025) showed that a higher frequency of board meetings significantly reduces earnings management, suggesting that a more active board helps limit discretionary earnings management practices. Similarly, Eze (2017) demonstrated that the board of directors is expected to plan meetings to address the most critical issues related to company management and fulfill its oversight and management tasks. However, Menon and Williams (1994) emphasized that a low frequency of board meetings significantly reduces its effectiveness in control. Another strand of literature suggests a positive relationship between board meetings and earnings management (Almuzaiqer and al., 2022; Attia and al., 2022). Frequent board meetings present an opportunity for executives to manipulate earnings figures (Attia and al., 2022a), meaning that board members may waste time in meetings rather than focusing on their primary function of overseeing and controlling management’s actions (Almuzaiqer and al., 2022). Some studies, however, suggest no significant relationship between board meetings and earnings management (Chatterjee and Rakshit, 2022; Kjærland and al., 2020). The results of these studies indicate that board meetings may not influence the limitation of earnings management practices, which could be justified by the lack of expertise within the board (Chatterjee and Rakshit, 2022). In this study, we consider that the frequency of board meetings is positively associated with earnings management. This hypothesis is supported by the findings of a report on governance and gender equality in Morocco conducted by the International Finance Corporation (2022), revealing that 82% of respondents indicate that their board regularly discusses the company’s strategy, suggesting that meetings are more focused on strategic management and performance monitoring rather than strict oversight of management’s actions.

H4: The frequency of board meetings has a positive relationship with earnings management in Moroccan companies.

Nationality Of the Chairman of the Board

The nationality of the chairman of the board, as a carrier of cultural values, plays a significant role in corporate governance practices. Amin and al. (2025) demonstrated that the nationality of the chairman reflects his or her cultural values, which contributes to improving financial transparency and significantly influences earnings management, particularly in contexts where formal institutions are underdeveloped. Kato and Rockel (1992) showed that cultural differences between American and Japanese CEOs influence their management styles and financial decisions, including earnings management practices. Jalbert and al. (2007) also highlighted that the nationality of the CEO affects key aspects of corporate governance, such as compensation, performance, and management approaches, underscoring the impact of national culture on managerial and financial decisions. Bouaziz and al. (2020) revealed that the nationality of the CEO has a positive and significant relationship with the quality of financial information, suggesting that national culture influences the transparency and reliability of financial reporting. Our paper argues that the nationality of the chairman of the board is negatively associated with earnings management. Our idea is based on the findings of a PwC (2021) conducted in 2021, titled “Global Culture Survey,” which emphasizes the importance of cultural values in promoting transparency and mitigating risks within organizations, particularly in the context of the COVID-19 pandemic.

H5: The nationality of the chairman of the board has a negative relationship with earnings management in Moroccan companies.

Data and Methodology

Data And Variables

Our initial sample consists of 76 companies listed on the Casablanca Stock Exchange between 2018 and 2022. After excluding 13 financial companies due to the specificity of their regulations, and 29 companies with missing data, our final sample consists of 34 listed companies over the 5-year period, totaling 170 data points. The financial data and information related to the governance bodies of these companies were manually collected from the companies’ annual reports.

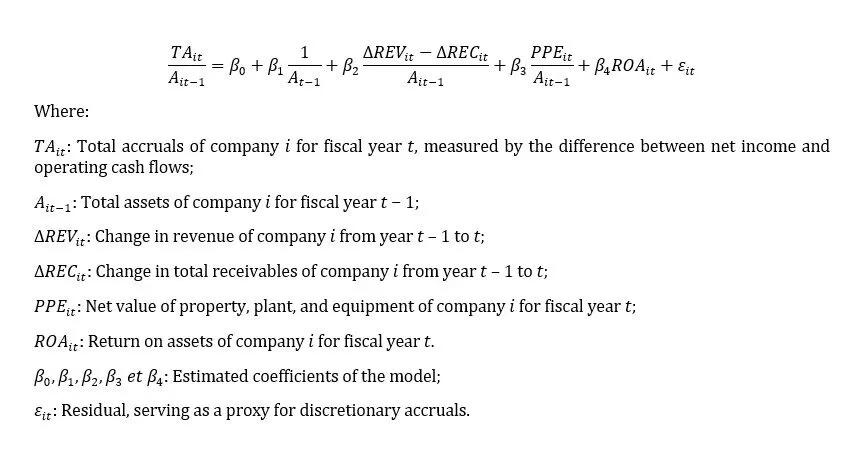

The main dependent variable used in this study is the discretionary accruals account, which serves as an indicator of earnings management, following the Kothari and al. (2005) model. This model is preferred for its ability to accurately capture discretionary accruals in non-financial companies, unlike other models (Costa and Soares, 2022). Additionally, it incorporates return on assets (ROA) to control for extreme operating performance, which reduces bias in estimating discretionary accruals (Al-Shaer and Zaman, 2021). Moreover, the Kothari and al. (2005) model provides superior explanatory power compared to the Dechow and al. (1995) and Caylor (2010) models, particularly because it accounts for both past and present performance of the company (Uddin, 2023). Therefore, this model remains a widely used tool by researchers for its effectiveness and simplicity (Almarayeh, 2024; Bilal and al., 2024).

We estimate discretionary accruals using the Kothari and al. (2005) model as follows:

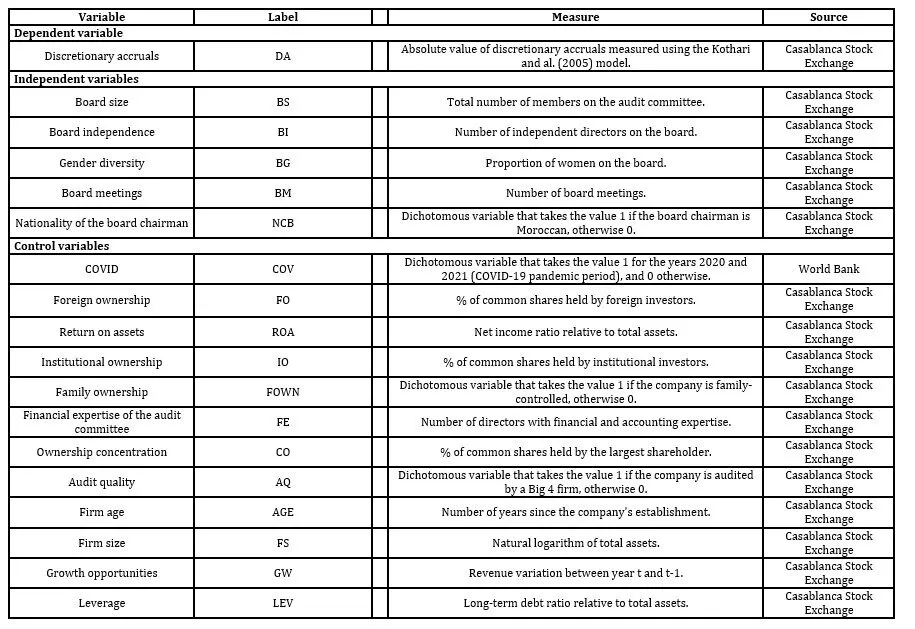

This study incorporates a range of independent and control variables to examine the determinants of earnings management. The first key independent variable, board size (BS), represents the total number of members on the board of directors. The second independent variable, board independence (BI), is measured by the number of independent directors on the board. The third variable, gender diversity (BG), is measured by the proportion of women on the board of directors. The frequency of board meetings (BM) is measured by the number of meetings held by the board. Finally, the nationality of the chairman of the board is a binary variable taking the value 1 if the chairman is Moroccan, and 0 otherwise. The data for these variables come from the annual management reports filed with the Casablanca Stock Exchange. In addition to these independent variables, we incorporate several control variables that account for structural and contextual factors influencing earnings management practices. These include the health crisis (COV), which takes the value of 1 for the years 2020 and 2021, corresponding to the COVID-19 pandemic period, and 0 otherwise; foreign ownership (FO), measured by the percentage of shares held by foreign investors; return on assets (ROA), calculated as the ratio of net income to total assets; institutional ownership (IO), representing the percentage of shares held by institutional investors; family ownership (FOWN), which takes the value 1 if the company is controlled by a family and 0 otherwise; and the financial expertise of the audit committee (FE), measured by the number of directors with financial and accounting expertise.

To strengthen the robustness of our results and limit potential estimation biases, we conduct additional analyses by including alternative control variables commonly used in the literature. These include ownership concentration (CN), measured by the percentage of shares held by the largest shareholder; audit quality (AQ), which takes the value of 1 if the company is audited by a Big 4 firm, and 0 otherwise; firm age (AGE), measured by the number of years since the company was founded; firm size (FS), measured by the logarithm of total assets; growth opportunities (GW), measured by the change in revenue from t-1 to t; and leverage (LEV), measured as the ratio of long-term debt to total assets.

Table1 provides a detailed presentation of the dependent, independent, and control variables, including their definitions, measurement methods, and data sources. Additionally,

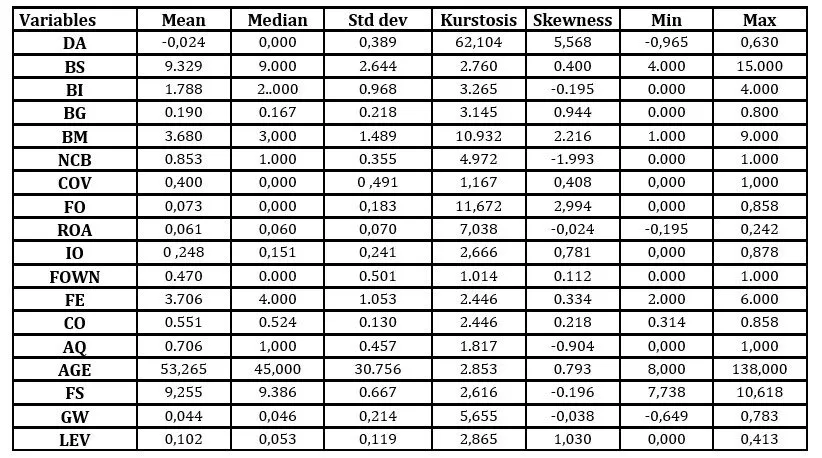

Appendix 1 presents the descriptive statistics of the variables used in the analysis.

Table 1. Variables, measures, and sources

Methodology

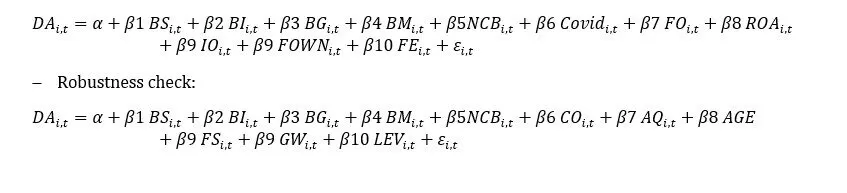

This study examines earnings management practices using discretionary accruals (DA) as the dependent variable to identify whether executives adopt an upward or downward earnings management strategy. The dataset covers a five-year period and is structured as a panel, which allows for simultaneous consideration of both cross-sectional and time dimensions. To analyze these data, the Generalized Method of Moments (GMM) with the two-step estimator of Arellano and Bond (1991) is chosen due to its efficiency in handling the specifics of panel data and controlling for endogeneity issues. This method is widely preferred for dynamic panel data analysis, particularly due to its ability to address endogeneity problems, especially when the dependent variable is correlated with the error term in the differenced equation, rendering fixed effects (FE) and random effects (RE) models inappropriate (Baltagi and al., 2009). The GMM estimator overcomes this limitation by using lagged values of both dependent and independent variables as instruments, ensuring their correlation with the explanatory variables while remaining uncorrelated with the error term (García-Herrero and al., 2009). Furthermore, the two-step GMM estimation handles heteroscedasticity and provides robust results, even in the presence of over-specified moment conditions (Fève and Langot, 1995). This method is also widely adopted in academic literature (Jawadi and al., 2025; Ganda, 2024) due to its robustness and efficiency in analyzing dynamic panel data.

In our analysis, we consider the following regression equations:

Main regression analysis:

Where α and β_i are the parameters of the equations, and ε_it is the error term.

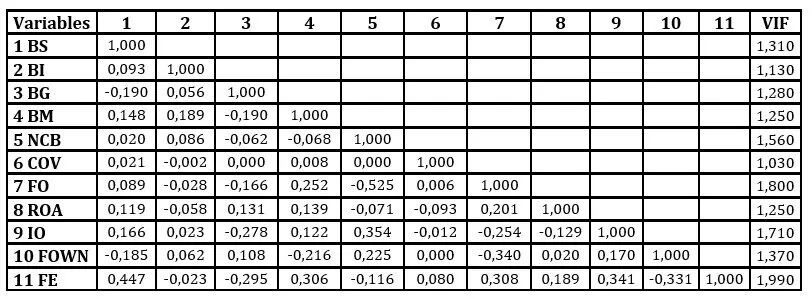

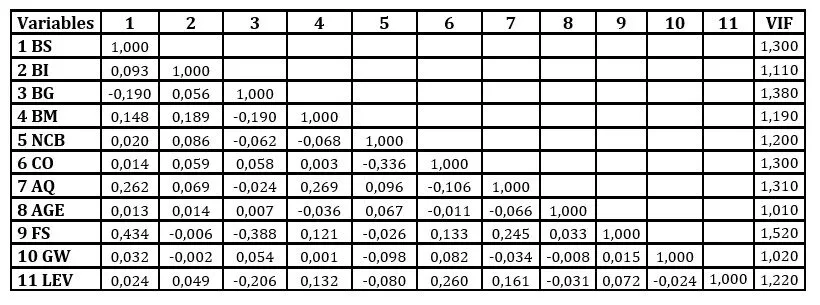

Our empirical analysis relies on six regression models. The correlation matrices of the variables (

Appendix 2) indicate low correlation levels, and the Variance Inflation Factor (VIF) tests show values below 10. These results confirm the absence of multicollinearity issues in our analysis.

Results

Descriptive Analysis

Appendix 1 presents the descriptive statistics of companies listed on the Casablanca Stock Exchange for the period 2018-2022. The average value of discretionary accruals is -0.9653, with a minimum value of -0.9653 and a maximum value of 0.6295. These results indicate that executives of companies listed on the Casablanca Stock Exchange tend to favor downward earnings management rather than upward earnings management. These results are consistent with the findings of Ibrahimi and Baghdadi (2024) in the Moroccan context for the period 2012-2021, as well as with the work of Hsu and Yang (2022) conducted in the UK during the health crisis. Thus, these elements reinforce the relevance of our results within the existing literature on earnings management. The average number of board members is between 9 and 10 directors, with a minimum of 4 and a maximum of 15. Although the Moroccan Governance Code of 2008 allows companies the freedom to determine the size of their board, this average indicates general adherence to best practices, thereby contributing to the strengthening of the governance system and the transparency of financial information. The average number of independent directors on the board is between 1 and 2, on a scale from 0 to 4, indicating a relatively low presence of independent members. This observation highlights the need to strengthen board independence to better align local practices with international corporate governance standards. Regarding gender diversity, while the observed 19% female representation (range: 0%-80%) shows partial adherence to Morocco’s 2008 Governance Code, significant progress remains necessary to achieve equitable participation. These results collectively indicate: (1) insufficient implementation of independent director standards, and (2) nascent but inadequate efforts toward gender-inclusive governance.

The average number of board meetings per year ranges from 3 to 4, with a minimum of 1 and a maximum of 9. These results align with the recommendations of the Moroccan Governance Code of 2008, which encourages regular meetings to strengthen oversight and transparency. The nationality of the board chairman shows that 85.3% of chairmen are Moroccan, indicating a strong predominance of local leaders at the head of Moroccan companies. This trend reflects the importance of cultural values and local networks in corporate governance in Morocco. Regarding control variables, the average value for COVID-19 is 40%, indicating that 40% of the observations pertain to the post-pandemic period. Foreign ownership represents an average of 7.3%, indicating relatively low participation by international investors in the capital of companies listed on the Casablanca Stock Exchange. Institutional ownership represents an average of 24.8%, indicating significant participation by institutions in Moroccan companies. This presence enhances stability and governance, while opening up prospects for increasing their role in financing and the country’s economic development. Finally, the average values for asset returns and family ownership are 6.1% and 47%, respectively, while the average number of directors with financial and accounting qualifications and skills ranges from 3 to 4.

Regression Analysis

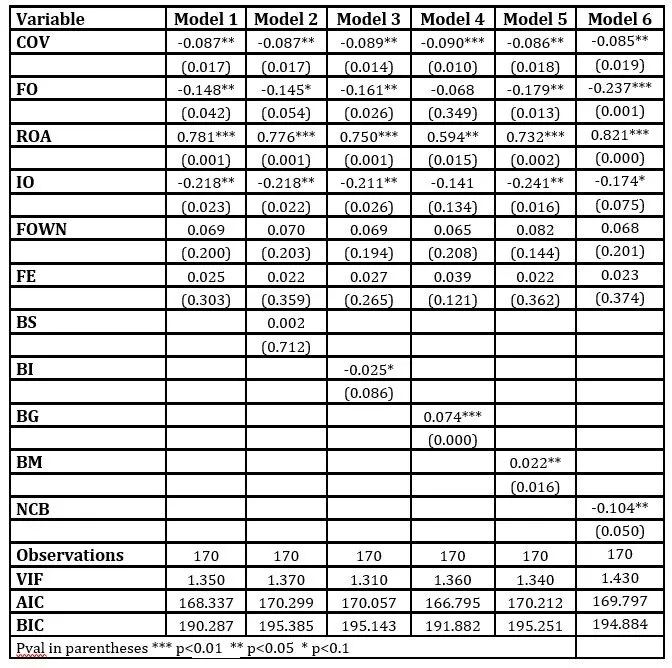

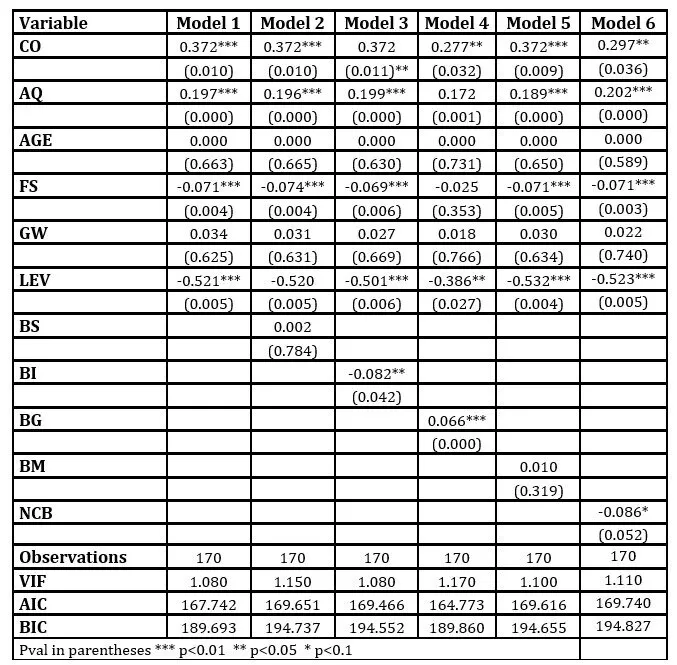

Error! Reference source not found. presents the results of our analysis on the impact of board characteristics on earnings management. In Model 2, board size has a positive but non-significant effect on earnings management (0.002). This result suggests that larger boards do not appear to be effective in reducing earnings management practices. Furthermore, board independence has a negative and significant effect on earnings management (-0.025). This suggests that an increased presence of independent directors strengthens the oversight of financial reporting practices, thereby reducing executives’ ability to manipulate earnings. Model 4 highlights a positive and significant effect between gender diversity and earnings management (0.074). This means that the presence of women on the board does not limit executives’ use of manipulative techniques. Model 4 also shows a positive and significant association between board meeting frequency and earnings management (0.022). This indicates that as the frequency of board meetings increases, executives find greater freedom to manipulate earnings. Finally, Model 5 examines the effect of the board chairman’s nationality on earnings management. The coefficient is negative and significant (-0.104), indicating that Moroccan board chairmen effectively reduce earnings management practices.

Table 2.Main regression analysis

Robustness Check

The robustness check presented in Table 3 extends the main analysis by incorporating additional variables. In Model 2, board size has a positive but non-significant effect on earnings management (0.002). Model 3 highlights a negative and significant relationship between board independence and earnings management (-0.082), indicating that a higher presence of independent directors translates into better financial reporting quality. In Model 4, gender diversity has a positive and significant effect on earnings management (0.066), meaning that the participation of women on the board does not contribute to reducing manipulative techniques. Model 5 reveals that board meeting frequency has a positive but non-significant effect on earnings management (0.010), suggesting that an increase in meeting frequency does not necessarily reduce earnings management practices. Finally, Model 6 highlights a negative and significant relationship between the board chairman’s nationality and earnings management (-0.086), confirming the role of Moroccan board chairmen in maintaining the quality of financial reports. Overall, the robustness check confirms the main findings of the initial analysis, indicating that board independence, gender diversity, meeting frequency, and the chairman’s nationality significantly influence earnings management practices in non-financial companies listed on the Casablanca Stock Exchange. Regarding the hypotheses, our results confirm H2, H4, and H5, while H1 and H3 are not supported.

Table 3. Robustness check

Discussion

Our results indicate the absence of a significant relationship between board size and earnings management, meaning that board size is not capable of curbing earnings management. This result is similar to that of Almarayeh and al. (2024) regarding MENA countries, which can be explained by the presence of large shareholders who hold a high percentage of shares, potentially preventing the board from effectively supervising the management team (Le and Nguyen, 2022). Regarding board independence, it has a negative and significant effect on earnings management, suggesting that the higher the proportion of independent directors, the less motivated executives are to engage in earnings management techniques. This result aligns with that of Mokrani and Alami (2021) in the Moroccan context, confirming the role of independent directors in improving corporate governance and reducing bankruptcy and financial fraud risks. Gender diversity has a positive and significant effect on earnings management, meaning that the inclusion of women on the board has not significantly contributed to reducing opportunistic behaviors among executives. This result is similar to that of Almarayeh (2021) in the MENA region, which shows that institutional and cultural barriers hinder women’s access to leadership positions, limiting their participation compared to their male counterparts.

Turning to the board meeting frequency, our results suggest that it has a positive and significant effect on earnings management. This means that the more often the board meets, the more freedom executives have to manipulate earnings. This observation is consistent with several studies, such as that of Almuzaiqer and al. (2022) in the United Arab Emirates and that of Attia and al. (2022) in Egypt. This relationship can be explained by the fact that board members spend too much time in meetings at the expense of their primary function, which is to monitor executives and protect corporate assets. Regarding the nationality of the board chairman, we found it to be negatively associated with earnings management, highlighting the role of Moroccan board chairmen in preserving financial reporting quality. This result is similar to that of Amin and al. (2025), which suggests that nationality reflects the chairman’s cultural values, playing a key role in limiting earnings management practices.

Our findings also reveal a correlation between control variables and earnings management. The COVID-19 pandemic, foreign ownership, and institutional ownership show a negative and significant association with earnings management, suggesting that in crisis contexts, such as the health crisis, foreign and institutional investors play a crucial role by imposing increased transparency and disclosure requirements, thereby limiting manipulative techniques. Conversely, return on assets exhibits a positive and significant association with earnings management, indicating that highly performing companies engage in earnings management. This behavior can be explained by the informational perspective, according to which earnings management serves as a signaling tool to financial markets. Executives often manipulate earnings to present a favorable image of the company’s financial situation, influencing investor perceptions and maximizing shareholder value.

In summary, our findings provide insights into the effectiveness of corporate boards. The 2008 Moroccan Code of Good Governance Practices emphasizes that the board plays a role in strengthening governance mechanisms, maintaining financial transparency, and promoting ethics and social responsibility. Our study shows that board independence and the nationality of the board chairman are key determinants in preserving financial reporting quality. These results align with the recommendations of the 2008 Moroccan governance code and the findings of several researchers. For example, Almubaydeen and Al-Eyasrah (2025) demonstrated that independent directors are effective in detecting manipulative techniques in the Jordanian context. Similarly, Amin and al. (2025) highlight the importance of the board chairman’s nationality in improving financial transparency, particularly in contexts where formal institutions are less developed. However, although listed companies comply with the recommendations of this code, these efforts remain insufficient to ensure effective control and transparent governance. Other studies, such as those by Ibrahimi and Baghdadi (2022), have shown that the institutional, political, and financial environment in MENA countries is ineffective, encouraging executives to engage in earnings management practices.

Conclusion

The objective of our study was to explore the relationship between board characteristics and earnings management. To do so, a regression using the GMM was employed to analyze data from 34 companies listed on the Casablanca Stock Exchange over the period 2018 to 2022. The results of our study show that boards composed mainly of independent directors and that prioritize national cultural values—such as Moroccan board chairpersons—are more effective in reducing earnings management practices. This increased effectiveness can be attributed to the adoption of Law No. 20-19, which requires publicly traded companies to appoint one or more independent directors to their board, in order to strengthen governance and transparency in Moroccan companies.

Moreover, the study conducted by PwC (2021), titled ‘Global Culture Survey’, highlights the importance of cultural values in promoting transparency and risk prevention within organizations, particularly in the context of the COVID-19 pandemic. Moroccan regulators should adopt various measures to strengthen the governance system and improve financial information transparency. These include: encouraging companies to adopt the 2008 Moroccan Corporate Governance Code to enhance their performance and corporate image; introducing a public disclosure approach that involves publishing the names of companies engaged in earnings manipulation so that the market can sanction these practices and encourage greater transparency; and reinforcing the “comply or explain” approach by making it mandatory for listed companies, with penalties for non-compliance.

Our study makes a significant contribution by exploring the role of boards of directors in reducing earnings management practices, particularly in the context of emerging markets such as Morocco. The results offer concrete recommendations for different stakeholders. For regulators, they highlight the need to strengthen governance mechanisms by promoting diverse and dynamic boards while integrating the country’s cultural values. This approach would improve corporate governance and enhance financial transparency. For practitioners, the results emphasize the importance of independent directors and Moroccan board chairpersons in reinforcing governance effectiveness and investor confidence. Furthermore, a balanced gender representation within boards of directors helps strengthen corporate governance by promoting conservative strategies and limiting earnings management practices, thereby preserving the company’s reputation.

This study stands out for its in-depth analysis of the impact of the 2008 Moroccan Corporate Governance Code on earnings management, highlighting the strategic role of boards of directors. It sheds light on governance practices in Africa, where institutional, structural, and cultural challenges differ from those in developed economies. In a post-COVID-19 context, the conclusions underscore the importance of strong governance mechanisms that integrate local cultural values to ensure transparency and ethical disclosure of information.

However, the study has certain limitations, particularly regarding the observation period and the range of board characteristics analyzed. Future research could deepen the analysis by incorporating additional factors, such as audit committee characteristics, CEO duality, and other contextual dimensions, including audit quality, institutional environment, ownership concentration, the predominance of family businesses, corporate social responsibility, and national cultural values. Additionally, examining the combined effect of two governance mechanisms on limiting earnings management practices would provide a more comprehensive understanding of their interaction and effectiveness. Moreover, adopting a qualitative approach through in-depth interviews with executives and directors would help better understand the underlying mechanisms that contribute to board effectiveness. This approach would offer complementary perspectives by exploring the perceptions, practices, and challenges faced by corporate governance actors.

Funding

This work was supported by the National Center for Scientific and Technical Research (CNRST) as part of the “PhD-Associate Fellowship – PASS” program, awarded to Aymane Chemmaa.

References

Abdou, H., Ellelly, N., Elamer, A., Hussainey, K. and Yazdifar, H. (2020), “Corporate governance and earnings management nexus: Evidence from the UK and Egypt using neural networks”, International Journal of Finance & Economics, Vol. 26, doi: 10.1002/ijfe.2120.

Afifa, M.A., Saleh, I., Al-shoura, A. and Van, H.V. (2022), “Nexus among board characteristics, earnings management and dividend payout: evidence from an emerging market”, International Journal of Emerging Markets, Emerald Publishing Limited, Vol. 19 No. 1, pp. 106–133, doi: 10.1108/IJOEM-12-2021-1907.

Al-Haddad, L. and Whittington, M. (2019), “The impact of corporate governance mechanisms on real and accrual earnings management practices: evidence from Jordan”, CORPORATE GOVERNANCE-THE INTERNATIONAL JOURNAL OF BUSINESS IN SOCIETY, Emerald Group Publishing Ltd, Bingley, Vol. 19 No. 6, pp. 1167–1186, doi: 10.1108/CG-05-2018-0183.

Almarayeh, T. (2024), “Audit committees’ independence and earnings management in developing countries: evidence from MENA countries”, Journal of Financial Reporting and Accounting, doi: 10.1108/JFRA-11-2023-0652.

Almarayeh, T., Aibar-Guzmán, B. and Suárez Fernández, Ó. (2024a), “Does the board of directors play a role in mitigating real and accrual-based earnings management in the MENA context?”, Corporate Governance: The International Journal of Business in Society, Vol. 24, pp. 1103–1136, doi: 10.1108/CG-04-2022-0192.

Almarayeh, T., Aibar-Guzmán, B. and Suárez Fernández, Ó. (2024b), “Does the board of directors play a role in mitigating real and accrual-based earnings management in the MENA context?”, Corporate Governance: The International Journal of Business in Society, Vol. 24, pp. 1103–1136, doi: 10.1108/CG-04-2022-0192.

Almarayeh, T., Aibar-Guzman, B. and Suarez-Fernandez, O. (2024), “Does the board of directors play a role in mitigating real and accrual-based earnings management in the MENA context?”, CORPORATE GOVERNANCE-THE INTERNATIONAL JOURNAL OF BUSINESS IN SOCIETY, Emerald Group Publishing Ltd, Leeds, doi: 10.1108/CG-04-2022-0192.

Almarayeh, T.S. (2021), “Do board characteristics mitigate real and accrualbased earnings management activities? Evidence from MENA countries”.

Almubaydeen, T. and Al-Eyasrah, M.Z. (2025), “The Impact of Board Characteristics on Earnings Management in Industrial Companies Listed in Amman Stock Exchange”, in Musleh Al-Sartawi, A.M.A., Al-Okaily, M., Al-Qudah, A.A. and Shihadeh, F. (Eds.), From Machine Learning to Artificial Intelligence: The Modern Machine Intelligence Approach for Financial and Economic Inclusion, Springer Nature Switzerland, Cham, pp. 1115–1130, doi: 10.1007/978-3-031-76011-2_82.

Almuzaiqer, M.A., Fatima, A.H. and Ahmad, M. (2022), “Royal Family Members and Corporate Governance Characteristics: The Impact on Earnings Management in Uae”, International Journal of Business and Society, Univ Malaysia Sarawak, Fac Economics & Business, Sarawak, Vol. 23 No. 2, pp. 689–713, doi: 10.33736/ijbs.4834.2022.

Al-Shaer, H. and Zaman, M. (2021), “Audit committee disclosure tone and earnings management”, Journal of Applied Accounting Research, Vol. 22 No. 5, pp. 780–799, doi: 10.1108/JAAR-12-2020-0243.

Amin, H.M.G., Mohamed, E.K.A., Abdallah, A.S. and Elamer, A.A. (2025), “National culture, formal institutions and structure of board of directors: theory and empirical evidence”, Journal of Financial Reporting and Accounting, Emerald Publishing Limited, Vol. ahead-of-print No. ahead-of-print, doi: 10.1108/JFRA-07-2024-0431.

Arellano, M. and Bond, S. (1991), “Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations”, The Review of Economic Studies, Vol. 58 No. 2, pp. 277–297, doi: 10.2307/2297968.

Association of Certified Fraud Examiners. (2024), Occupational Fraud 2024: A Report to the Nations.

Attia, E., Ismail, T. and Mehafdi, M. (2022a), “Impact of board of directors attributes on real-based earnings management: further evidence from Egypt”, Future Business Journal, Vol. 8, doi: 10.1186/s43093-022-00169-x.

Attia, E.F.F., Ismail, T.H.H. and Mehafdi, M. (2022b), “Impact of board of directors attributes on real-based earnings management: further evidence from Egypt”, FUTURE BUSINESS JOURNAL, Springer, New York, Vol. 8 No. 1, p. 56, doi: 10.1186/s43093-022-00169-x.

Bajra, U. and Cadez, S. (2018), “The Impact of Corporate Governance Quality on Earnings Management: Evidence from European Companies Cross-listed in the US”:, Australian Accounting Review, doi: 10.1111/auar.12176.

Baltagi, B.H., Demetriades, P.O. and Law, S.H. (2009), “Financial development and openness: Evidence from panel data”, Journal of Development Economics, Vol. 89 No. 2, pp. 285–296, doi: 10.1016/j.jdeveco.2008.06.006.

Bangoura, M. (2024), “IIAG 2024: la gouvernance sur le continent africain a cessé de progresser”, com, 24 October, available at: https://mosaiqueguinee.com/2024/10/iiag-2024-la-gouvernance-sur-le-continent-africain-a-cesse-de-progresser/ (accessed 29 March 2025).

Beasley, M.S. (1996), “An Empirical Analysis of the Relation between the Board of Director Composition and Financial Statement Fraud”, The Accounting Review, American Accounting Association, Vol. 71 No. 4, pp. 443–465.

Bilal, Ezeani, F., Usman, M., Komal, B. and Gerged, A.M. (2024), “Impact of ownership structure and cross-listing on the role of female audit committee financial experts in mitigating earnings management”, Business Ethics, the Environment & Responsibility, Vol. n/a No. n/a, doi: 10.1111/beer.12705.

Biswas, S., Bhattacharya, M., Sadarangani, P.H. and Jin, J.Y. (2022), “Corporate governance and earnings management in banks: An empirical evidence from India”, COGENT ECONOMICS & FINANCE, Taylor & Francis As, Oslo, Vol. 10 No. 1, p. 2085266, doi: 10.1080/23322039.2022.2085266.

Bouaziz, D., Salhi, B. and Jarboui, A. (2020), “CEO characteristics and earnings management: empirical evidence from France”, Journal of Financial Reporting and Accounting.

Casablanca Stock Exchange. (2023), Le Marché Des Capitaux En Chiffres 2023.Pdf.

Caylor, M.L. (2010), “Strategic revenue recognition to achieve earnings benchmarks”, Journal of Accounting and Public Policy, Vol. 29 No. 1, pp. 82–95, doi: 10.1016/j.jaccpubpol.2009.10.008.

Chatterjee, R. and Rakshit, D. (2022), “Association Between Earnings Management and Corporate Governance Mechanisms: A Study Based on Select Firms in India”, Global Business Review, Vol. 24 No. 1, pp. 152–170, doi: 10.1177/0972150919885545.

Chemmaa, A. and Ibrahimi, M. (2025), “Two Decades of Research on Earnings Management and Corporate Governance: Insights from a Bibliometric Review”, Journal of Accounting and Auditing: Research & Practice, pp. 1–15, doi: 10.5171/2025.320461.

Costa, C.M. and Soares, J.M.M.V. (2022), “Standard Jones and Modified Jones: An Earnings Management Tutorial”, Revista de Administração Contemporânea, Vol. 26 No. 2, p. e200305, doi: 10.1590/1982-7849rac2022200305.en.

Davidson, S., Stickney, C.P. and Weil, R.L. (1987), Accounting: The Language of Business, 7th ed., T. Horton, Sun Lakes, Ariz.

Dechow, P.M., Sloan, R.G. and work(s):, A.P.S.R. (1995), “Detecting Earnings Management”, The Accounting Review, Vol. 70 No. 2, pp. 193–225.

EY Attractiveness Africa. (2023), “EY Africa Attractiveness Report 2023: South Africa, Egypt at forefront of FDI project”, available at: https://www.ey.com/en_za/services/consulting/ey-africa-attractiveness-report-2023–south-africa–egypt-at-for (accessed 29 March 2025).

Fama, E. and Jensen, M.C. (1983), “Agency Problems and Residual Claims”, The Journal of Law & Economics, Vol. 26 No. 2, pp. 327–349.

Fan, Y., Jiang, Y., Zhang, X. and Zhou, Y. (2019), “Women on boards and bank earnings management: From zero to hero”, Journal of Banking & Finance, Vol. 107, p. 105607, doi: 10.1016/j.jbankfin.2019.105607.

Fève, P. and Langot, F. (1995), “La méthode des moments généralisés et ses extensions : théorie et applications en macro-économie”, Économie & prévision, Vol. 119 No. 3, pp. 139–170, doi: 10.3406/ecop.1995.5737.

Ganda, F. (2024), “The interplay between technological innovation, financial development, energy consumption and natural resource rents in the BRICS economies: Evidence from GMM panel VAR”, Energy Strategy Reviews, Vol. 51, p. 101267, doi: 10.1016/j.esr.2023.101267.

García Lara, J.M., García Osma, B., Mora, A. and Scapin, M. (2017), “The monitoring role of female directors over accounting quality”, Journal of Corporate Finance, Vol. 45, pp. 651–668, doi: 10.1016/j.jcorpfin.2017.05.016.

García-Herrero, A., Gavilá, S. and Santabárbara, D. (2009), “What explains the low profitability of Chinese banks?”, Journal of Banking & Finance, Vol. 33 No. 11, pp. 2080–2092, doi: 10.1016/j.jbankfin.2009.05.005.

García-Olalla, M. and Vázquez-Ordás, C.J. (2024), “Introduction to the special issue: ‘Current challenges of corporate governance: Reputation, risk and sustainability’”, Global Policy, Vol. 15 No. S1, pp. 5–7, doi: 10.1111/1758-5899.13319.

Haw, I.-M., Qi, D., Wu, D. and Wu, W. (2005), “Market Consequences of Earnings Management in Response to Security Regulations in China”, Contemporary Accounting Research, Vol. 22 No. 1, pp. 95–140, doi: 10.1506/9XVL-P6RR-MTPX-VU8K.

(2006), “Methodological Issues in Accounting”, Scribd.

Hsu, Y.-L. and Yang, Y.-C. (2022), “Corporate governance and financial reporting quality during the COVID-19 pandemic”, Finance Research Letters, Vol. 47, p. 102778, doi: 10.1016/j.frl.2022.102778.

Huang, H.-L., Liang, L.-W., Chang, H.-Y. and Hsu, H.-Y. (2021), “The Influence of Earnings Management and Board Characteristics on Company Efficiency”, Sustainability, Multidisciplinary Digital Publishing Institute, Vol. 13 No. 21, p. 11617, doi: 10.3390/su132111617.

Hunjra, A.I., Deari, F., Mehmood, R. and Al-Faryan, M.A.S. (2025), “Do board and audit characteristics affect earnings management in times of Covid-19?”, International Journal of Accounting, Auditing and Performance Evaluation, Inderscience Publishers (IEL).

Ibrahimi, M., Amine, M. and Taghzouti, A. (2021), “Determinants of value creation through mergers and acquisitions in the MENA region”, International Journal of Business Performance Management, Vol. 22 No. 2/3, p. 273, doi: 10.1504/IJBPM.2021.116404.

Ibrahimi, M. and Baghdadi, F. (2022a), “Gestion Des Résultats Pour Eviter Des Pertes Et Des Baisses De Résultats : Cas Des Sociétés Marocaines Cotées”.

Ibrahimi, M. and Baghdadi, F. (2022b), “Qualité institutionnelle des cibles et gestion des résultats lors des fusions- acquisitions : Cas des acquéreurs ciblant la région MENA”.

Ibrahimi, M. and Baghdadi, F. (2024), “Value relevance of accounting information in Morocco: impact of profitability and earnings management strategies”, Managerial Finance, Vol. 51, doi: 10.1108/MF-03-2024-0147.

Ibrahimi, M. and El Baghdadi, F. (2023), “Pertinence de la valeur des informations comptables : Cas des sociétés marocaines cotées”, Recherches en Sciences de Gestion, ISEOR, Ecully, Vol. 158 No. 5, pp. 219–241, doi: 10.3917/resg.158.0219.

(2021), “Les investissements du Maroc en Afrique, un atout pour le continent”, IFC, Text/HTML, , available at: https://www.ifc.org/fr/stories/2024/moroccos-southward-investment-push-win-for-africa?utm_source=chatgpt.com (accessed 29 March 2025).

(2024), “Le Conseil d’administration du FMI a achevé les consultations de 2024 au titre de l’article IV, la revue à mi-parcours relative à l’accord de recours à la ligne de crédit modulable, la première revue relative à la facilité pour la résilience et la durabilité, et la modification du calendrier défini dans le cadre de la facilité pour la résilience et la durabilité en ce qui concerne le Maroc”, IMF, available at: https://www.imf.org/fr/News/Articles/2024/05/01/pr24132-morocco-imf-exec-board-2024-art-iv-consult-midterm-rev-fcl-first-rev-rephasing-access-rsf (accessed 29 March 2025).

International Finance Corporation. (2022), Enquête Gouvernance et Parité — Women on Boards in Morocco.

Jalbert, T., Chan, C., Jalbert, M. and Landry, S. (2007), “The Interrelationship Of CEO Nationality With Financial Management, Firm Performance, And CEO Compensation”, Journal of Diversity Management (JDM), Vol. 2, doi: 10.19030/jdm.v2i2.5007.

Jawadi, F., Pondie, T.M. and Cheffou, A.I. (2025), “New challenges for green finance and sustainable industrialization in developing countries: A panel data analysis”, Energy Economics, Vol. 142, p. 108120, doi: 10.1016/j.eneco.2024.108120.

Kaituko, L.E., Githaiga, P.N. and Chelogoi, S.K. (2023), “Board structure and the likelihood of financial statement fraud. Does audit fee matter? Evidence from manufacturing firms in the East Africa community”, Cogent Business & Management, Cogent OA, Vol. 10 No. 2, p. 2218175, doi: 10.1080/23311975.2023.2218175.

Kalantonis, P., Schoina, S. and Kallandranis, C. (2021), “The impact of corporate governance on earnings management: Evidence from Greek listed firms”, Corporate Ownership and Control, Vol. 18 No. 2, pp. 140–153, doi: 10.22495/cocv18i2art11.

Kato, T. and Rockel, M. (1992), “The importance of company breeding in the U.S. and Japanese managerial labor markets: A statistical comparison”, Japan and the World Economy, Vol. 4 No. 1, pp. 39–45, doi: 10.1016/0922-1425(92)90024-K.

Kjærland, F., Haugdal, A., Søndergaard, A. and Vågslid, A. (2020), “Corporate Governance and Earnings Management in a Nordic Perspective: Evidence from the Oslo Stock Exchange”, Journal of Risk and Financial Management, Vol. 13 No. 11, p. 256, doi: 10.3390/jrfm13110256.

Kothari, S.P., Leone, A.J. and Wasley, C.E. (2005), “Performance matched discretionary accrual measures”, Journal of Accounting and Economics, Vol. 39 No. 1, pp. 163–197, doi: 10.1016/j.jacceco.2004.11.002.

Le, Q.L. and Nguyen, H.A. (2022), “The impact of board characteristics and ownership structure on earnings management: Evidence from a frontier market”, Cogent Business & Management, Cogent OA, Vol. 10 No. 1, p. 2159748, doi: 10.1080/23311975.2022.2159748.

Lo, K. (2008), “Earnings management and earnings quality”, Journal of Accounting and Economics, Vol. 45 No. 2, pp. 350–357, doi: 10.1016/j.jacceco.2007.08.002.

Lu, J. and Boateng, A. (2018), “Board composition, monitoring and credit risk: evidence from the UK banking industry”, Review of Quantitative Finance and Accounting, Vol. 51 No. 4, pp. 1107–1128, doi: 10.1007/s11156-017-0698-x.

Menon, K. and Deahl Williams, J. (1994), “The use of audit committees for monitoring”, Journal of Accounting and Public Policy, Vol. 13 No. 2, pp. 121–139, doi: 10.1016/0278-4254(94)90016-7.

Mensah, E. and Boachie, C. (2023), “Corporate governance mechanisms and earnings management: The moderating role of female directors”, Cogent Business & Management, Cogent OA, Vol. 10 No. 1, p. 2167290, doi: 10.1080/23311975.2023.2167290.

Mokrani, Y.E. and Alami, Y. (2021), “The effects of corporate governance mechanisms on earnings management: Empirical evidence from Moroccan listed firms”, International Journal of Financial, Accounting, and Management, Vol. 3 No. 3, pp. 205–225, doi: 10.35912/ijfam.v3i3.538.

Moroccan Capital Market Authority. (2008), Code Marocain de Bonnes Pratiques de Gouvernance d’Entreprise.

Park, Y.W. and Shin, H.-H. (2004), “Board composition and earnings management in Canada”, Journal of Corporate Finance, Vol. 10 No. 3, pp. 431–457, doi: 10.1016/S0929-1199(03)00025-7.

Paul, O., Francis, I. and Ben-Caleb, E. (2020), “Corporate Governance and Creative Accounting Practices in The Listed Companies in Nigeria”, Academy of Accounting and Financial Studies Journal, Allied Business Academies, Vol. 24 No. 4.

Paul, O., Olayinka, E. and Dorcas, A. (2023), “Do corporate governance mechanisms restrain earnings management? Evidence from Nigeria”, International Journal of Business Governance and Ethics, Inderscience Enterprises Ltd, Vol. 17 No. 5, pp. 544–572.

Peasnell, K.V., Pope, P.F. and Young, S. (2001), “Board Monitoring and Earnings Management: Do Outside Directors Influence Abnormal Accruals?”, SSRN Electronic Journal, doi: 10.2139/ssrn.249557.

Persakis, A. and Iatridis, G.E. (2015), “Cost of capital, audit and earnings quality under financial crisis: A global empirical investigation”, Journal of International Financial Markets, Institutions and Money, Vol. 38, pp. 3–24, doi: 10.1016/j.intfin.2015.05.011.

(2021), Global Culture Survey 2021: The Link between Culture and Competitive Advantage.

Rajeevan, S. and Ajward, R. (2020), “Board characteristics and earnings management in Sri Lanka”, Journal of Asian Business and Economic Studies, Emerald Group Publishing Ltd, Bingley, Vol. 27 No. 1, pp. 2–18, doi: 10.1108/JABES-03-2019-0027.

Saleh, I., Abu Afifa, M. and Alkhawaja, A. (2022), “Internal corporate governance mechanisms and earnings manipulation practices in MENA countries”, Economic Research – Ekonomska Istraživanja, Routledge Journals, Taylor & Francis Ltd, Abingdon, doi: 10.1080/1331677X.2022.2134902.

Saona, P., Muro, L. and Alvarado, M. (2020), “How do the ownership structure and board of directors’ features impact earnings management? The Spanish case”, Journal of International Financial Management & Accounting, Vol. 31 No. 1, pp. 98–133, doi: 10.1111/jifm.12114.

Schipper, K. (1989), “Commentary on earnings Management”, Accounting Horizons.

Uddin, M. (2023), “The moderating role of COVID-19 pandemic on the relationship between CEO characteristics and earnings management: evidence from Bangladesh”, Cogent Business & Management, Vol. 10, doi: 10.1080/23311975.2023.2190196.

Word Bank. (2024), Economic Monitoring Report on Morocco.