Irina Nikolaevna Dmitrieva, Tatyana Nikolaevna Myznikova, Aleksey Fedorovich Chernenko and Anna Vladimirovna Shishkina

South Ural State University, Russia

Volume 2019,

Article ID 430681,

Journal of Accounting and Auditing: Research & Practice,

11 pages,

DOI: 10.5171/2019.430681

Received date: 20 March 2019; Accepted date: 9 September 2019; Published date: 18 October 2019

Academic Editor: Elena Iadrennikova

Cite this Article as:

Irina Nikolaevna Dmitrieva, Tatyana Nikolaevna Myznikova, Aleksey Fedorovich Chernenko and Anna Vladimirovna Shishkina (2019), " Analysis of Efficiency of Financial Leasing ", Journal of Accounting and Auditing: Research & Practice, Vol. 2019 (2019), Article ID 430681, DOI: 10.5171/2019.430681

The article substantiates the necessity of periodic relevance monitoring of effectiveness assessing methods of leasing operations due to the constantly changing management analysis information base and continuous improvement of management analysis methods. The problem is that the existing analytical methods objectively require constant improvement because of the growth of quality and transparency of the economic analysis information base. The purpose of the study was to create a methodology for analyzing the effectiveness of leasing operations based on indicators compiled on the current requirements of international financial reporting standards. The authors of the study suggest the effect of the leasing agreement to be defined as the difference between the potential costs of the lessee enterprise when acquiring fixed assets under the leasing agreement and the potential costs of the borrowing enterprise when acquiring property under a purchase and sale contract at the expense of a credit or a loan. The relative efficiency of leasing is proposed to be defined as the ratio of the effect of the leasing contract to the potential costs of the lessee. Lists of potential expenses of the lessee and the borrower are drawn up in accordance with the applicable regulatory legal acts, with consideration of the tax consequences of transactions and the inflation component. The methodology developed by the authors of the article will help enterprise managers make the right managerial decisions regarding the choice of financing source when updating fixed production assets, increase transaction efficiency, and optimize enterprise expenses.

The need to update the fixed production assets of enterprises exists under any state of economy. Repurposing the production during the period of economic growth allows increasing the productivity and quality of products, which enables enterprises to become more competitive. The renewal of fixed assets also allows setting the foundation for the forthcoming growth in a period of stagnation or crisis. However, selecting the right source of financing within the volatile economic environment appears to be one of the most important factors in deciding upon renewal the means of production.

Among the possible sources of financing for the fixed assets renewal are internal funds (shares issue, borrowed funds or financial lease). As a rule, economic entities lack their own sources for updating fixed productive assets, so the choice between types of borrowing is a critical task for them.

Accuracy and quality of financial data used by economic entity to make a decision about borrowing funds, whether it is a credit or a lease, is strictly regulated by the set of international standards. IAS 1: Presentation of Financial Statements, IAS 10: Events after the Reporting Period, IAS 21: The Effects of Changes in Foreign Exchange Rates, IAS 32: Financial Instruments: Presentation, IAS 37: Provisions, Contingent Liabilities and Contingent Assets, and IAS 39: Financial Instruments: Recognition and Measurement give the definition of the terms “credit” and “credit-related contingency”. IAS 39 regulates the terms of initial recognition and subsequent loans evaluation, as well as impairment of the credit claims. IAS 39: Financial Instruments: Recognition and Measurement establishes the procedure of acknowledging the interest income and defining non-market interest rate. IAS 23: Borrowing Costs describes the accounting treatment of capitalized interests for loans not connected with acquisition and construction of fixed assets, but used for these purposes in practice anyway.

Deep elaboration of the rules for accounting and reporting on transactions related to the use of financial leases sets the solid foundation for conducting analytical research in this field.

Analysis of the state of the problem of choosing the type of borrowing when it is necessary to renew fixed assets

A comparison of the appropriateness of credit and leasing was examined in (Arevalo, O., Saman, D.M., Bonaime, A., and Skelton, J., 2010, Séverin, E., 2010, Clausen, C.C., Bauer, M., Saleh, A., and Picker, O., 2008, Miroshnikova, T., 2015, Miroshnikova, T., 2015). In addition to financial leasing, the literature analyzes the impact of operating income on operating income (to interest expenses) and on net income (Imhoff Jr., E.A., Lipe, R.C., and Wright, D.W., 1997). Prospectivity and benefits of using leasing are justified in publications (Conbeer, G.P., 1990, Simons, R.A., 1994, Nash, C.Y., and Flesher, D.L., 2005, Lazar, A., Avram, M.M., Duinea, E.M., Nita, M.M., and Gurau, M., 2010, Islam, M.A., Islam, M.R., and Siddiqui, M.H., 2014).

The number of articles and Russian authors is devoted to the issues of expediency of renewal of fixed assets due to credits. For example, in paper by Agibalov, A.V., and Gorelkin M.V. (2016) it is justified that for enterprises there are no clear recommendations on how to evaluate the effectiveness of credit. The authors proposed to allocate the target and economic efficiency of the loan. They established that evaluation of economic effectiveness of a loan for an enterprise using the traditional methods is unacceptable, that is why they have invented a proprietary technique of a loan effectiveness evaluation based on the interest margin rate with certain adjustments in calculation. As a credit resource rate authors recommend to use the banking loan price index, and as an interest yield rate – a return on equity. An interpretation of possible results of a comparison between the profitability of capital and the price of borrowed capital is presented in case study. The received positive value means the possibility of using the remaining part of the profit for expenditure and accumulation, and a negative value indicates that the target efficiency of borrowing is not accompanied by the necessary level of economic effect.

Considerable place in the economic literature is given to the consideration of the conditions for the effectiveness of leasing operations. In paper by Naumkina, N.A. (2012) it is shown that the loan is beneficial only for the replenishment of current assets, and it is more rational to use leasing to acquire fixed assets. In paper by Tsarkov, V.A., Malikova, O.S., and Takshaitov, Т.А. (2013), an investment transaction model is proposed that contains the initial data under a leasing agreement, settlement results, leasing payment flows and loan repayment flows by the lessor. The authors also describe the possibilities of applying this model to coordinate the interests of participants in the financial lease agreement.

A large number of works are devoted to clarification of terminology and accounting of leasing (for example, (Kovalev, V.V., and Kovalev, V.V., 2016, Holt, A., Eccles, T., and Bond, P., 2012, Michelman, J.E., Gorman, V., and Trompeter, G.M., 2011)). In paper by Kovalev, V.V., and Kovalev, V.V. (2016) the problem of definition of concepts “financial” and “operational leasing” in the accounting legislation is considered. The authors suggested ways of solving this problem through studying the genesis of concepts from the 1930s to the appearance of international financial reporting standards.

The dynamics of accounting practice of leasing is considered in paper by Holt, A., Eccles, T., and Bond, P. (2012). The authors analyzed the principles of accounting for fees for servicing commercial real estate and found that the current practice of accounting for leasing operations does not meet the interests of users.

In paper by Michelman, J.E., Gorman, V., and Trompeter, G.M. (2011) it is proved that by manipulating the indicators of financial statements, it is possible to create a false idea about the financial position of the enterprise. This, in its turn, calls into question the effectiveness of the management decision taken on the way of financing the renewal of fixed assets. The Sarbanes-Oxley Act adopted on 30.07.2002 in the United States facilitated the solution of this problem. The goal of this act was to increase the reliability of financial statements of enterprises. One of the directions regulated by this law is the existence of a model of internal control of the enterprise. The model consists of blocks that relate to all groups of business objectives of the organization: strategic, operational, reporting and legislative, and also includes an assessment of possible risks in selecting a funding source.

The work by Dmitrieva I.N. (2010) presents the technique of evaluation of financial rent operations efficiency in comparison to a loan (credit). The developed methodological foundations allow determining the most rational way of attracting borrowed funds for the acquisition of capital assets. They also take into account such factors as the tax consequences arising when concluding a contract and purchasing property, inflation (deflation), and the variability of accounting for leased property.

Despite the large number of conducted analytical studies and the existence of various ways to assess the effectiveness of leasing operations, the developed methods require adjustments in case the company applies international standards of financial reporting. Therefore, the authors of this article have set themselves the task to state, in their opinion, the actual method of assessing leasing operations, which was developed on the basis of modern regulatory legal acts.

Methodical Foundation of Financial Rent Efficiency Evaluation

The authors of this article propose to determine the effect of the lease contract as the difference between the potential costs of the property-receiving enterprise when acquiring property under a financial lease (PL) and the potential costs of the borrowing enterprise when acquiring property under a purchase-sale contract using the fund of a loan (PC) upon making a managerial decision in favor of a loan or a financial lease. Thus, the efficiency of leasing (EL) is proposed to be defined as the ratio of the effect of the lease contract (PC – PL) to the potential costs of the lessee (PL).

A choice in favor of a financial lease in comparison with a bank loan or a banking rate loan is obvious (when PL < PC or PL / PC PC), and, therefore, there are conditions of equality of the two alternatives (PC = PL).

Because of the fact that IFRS 16: Lease as opposed to IFRS 17: Lease, does not allow the lessee to classify the lease in two ways: as operational and financial, all rentals will be accounted for as a finance lease. Therefore, the subject of a lease contract can only be booked on the balance of the lessee.

Potential costs of the lessee in the acquisition of property under a financial lease PL in accordance with IFRS. As a result of settling the financial lease agreement, the asset will be recorded on the lessee’s balance sheet in accordance with paragraph 24 of IFRS 16 in the amount of the lease obligation and other expenses related to the lease and the obligation in accordance with paragraph 26 of IFRS 16 in the amount of the present value of the obligation to pay future rental payments (Bezzateeva, T., 2017).

The potential costs of the lessee are:

– the present value of lease payments;

– the influence of inflation on the cost of VAT payments due to changes in the timing of their payment;

– the amount of property tax that will be paid by the organization before the asset is fully depreciated.

The lease obligation is estimated at the present value of the lease payments that have not yet been made at the lease commencement date (paragraphs 26, 27 of IFRS 16). Lease payments are discounted using the interest rate laid down in the lease agreement or the rate of additional borrowing by the lessee.

In accordance with paragraph 27 of IFRS 16, lease payments consist of the following payments:

fixed payments excluding any incentive payments for rent (compensation) to the receipt;

variable lease payments, depending on some index or rate;

amounts that will be paid by the lessee as a guarantee of residual (liquidation) value;

the cost of the repurchase of the asset (if there is a sufficient degree of confidence in the exercise of the contractual right to such an opportunity);

fines for refusal (termination) from the lease (if such possibility is provided for by the terms of the contract) (Bezzateeva, T., 2016).

In accordance with paragraph 24 of IFRS 16, the initial cost of an asset should include the following:

the amount of the original estimate of the lease obligation;

lease payments on the date of commencement of the lease or until such date, less the incentive payments received for the lease;

any initial direct costs incurred by the lessee;

an estimate of the costs incurred by the lessee in the dismantling and transfer of the underlying asset, the restoration of the site on which it is located, or the restoration of the underlying asset to the condition required under the lease conditions (unless such costs are incurred to produce inventories).

In accordance with paragraph 55 of IAS 16 Fixed Assets, the accrual of depreciation for the asset begins when it becomes available for use, that is, when it is put into operation. Depreciation of an asset is made over its useful life, which is determined based on the estimated usefulness of the asset for the organization. In this case, the useful life of the asset may be shorter than its economic life. In our case, this is due to the expiry of the terms of the relevant lease contracts (paragraph 56 IAS 16). The same procedure for calculating depreciation exists in the tax accounting. However, unlike accounting, the amount of depreciation for tax purposes is determined by taxpayers on a monthly basis.

The tax base for property tax is the average annual value of the property. In this case, it is necessary to calculate the depreciation in accordance with the norms of accounting legislation, since “when determining the tax base, the property recognized as the object of taxation is accounted for at its residual value formed in accordance with the established accounting procedures approved in the accounting policy of the organization”.

For the most accurate analysis, it is reasonable to take into account all the tax consequences associated with the implementation of the lease agreement, since “the taxpayer reduces the revenues received by the amount of expenses incurred”. In accordance with the tax accounting, the potential costs of the lessee are:

– the accrued amount of depreciation under tax legislation, which relates to expenses related to the production and sale;

– the amount of lease payments less the amount of depreciation for the asset accrued in accordance with tax legislation that relates to other expenses related to the production and (or) sale;

– the amount of the accrued property tax also relates to other expenses related to the production and sale.

The above mentioned amounts will reduce the taxable base for income tax. Accordingly, the amount of income tax reduction due to depreciation, rental payments, and property tax must be deducted when determining the total costs of the lessee.

Therefore, the aggregate leasing expenses incurred by the lessee will be determined as a difference between the present value of VAT exclusive lease payments for the period of the financial leasing contract (P(L)), the change in the current value of VAT payments due to the changes in the timing of their payment (ΔP(VAT)), the discounted value of the property tax that will be paid by the organization before the asset is fully depreciated (P(PT)), and the discounted amount of income tax reduction due to the following: depreciation of the asset during the whole period of its depreciation (P(ITD)); property tax (P(ITPT)); accrual of VAT exclusive and asset amortization exclusive leasing payments (P(ITPL-D)). The sum P(ITPL-D) will reduce the taxable base for income tax in the event that the amount of accrued lease payments in the reporting period will be greater than the amount of depreciation accrued on this asset. Otherwise, this index will be zero.

In determining the total costs, the present value of lease payments should be reduced by the value of the value-added tax. This is explained by the fact that VAT is an indirect tax and the lessee later presents it to a deduction from the budget when it is paid to the lessor, as part of the lease payment. Accordingly, at the time the lease payment, cash outflow from the turnover is effected for the period from the moment of transfer to the lessor when the lease payment is paid, until the debt to the budget for VAT for the current period is paid off. However, with significant inflation, the lessee in this regard will incur losses.

The present value of lease payments P(L) or the period of the leasing agreement is determined as the sum of the products of lease payments without VAT for the i-th period in accordance with the payment schedule (Lwithout VAT i) and the discount rate (Fdisc), which is determined by the interest rate , laid down in the lease. In the event that such a rate cannot be easily determined, the lessee must use the rate of borrowing additional borrowed funds by the lessee.

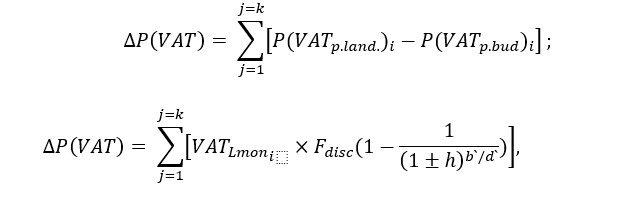

Depending on the timing of the transfer of rental payments to the lessor and the payment of debts to the budget for VAT, the discount multiplier will be calculated differently. Let us give the final formula for calculating the current cost of payments for VAT, omitting the order of mathematical transformations:

where P(VATp.land.)i is the VAT rate paid to the lessor on the day b within the i-th number of rents, with due account to inflation (deflation);

P(VATp.bud.)i is the discounted amount of reduction of the lessee’s VAT tax liability for the i-th month, subject to redemption on the b-th day (i + 1)-th month, by VAT amount already paid to the lessor as part of i-th lease payment;

k is a period of validity of the agreement, in months;

j is a conditional number of the current month of the financial lease agreement;

h is an average monthly rate of inflation (deflation), in the number of times;

VALLmoni is the amount of VAT of the monthly i-th lease payment;

b`is a calendar day of the month in which the amount of VAT is transferred to the budget, in days;

d`is a number of days in the month in which the amount of VAT is transferred to the budget, in days.

The amount of income tax reduction due to the accrued depreciation of the asset P(ITD) during the period of its depreciation is determined as the sum of the depreciation deductions for the i-th month (IC × D)i and the tax rate for the income tax (RIT). The amount of depreciation for the i-th month is determined by the sum of the initial value of the asset (IC) and the annual depreciation rate (D).

The amount of income tax reduction due to the accrual of the amount of VAT excluded lease payments deducing the amount of depreciation for this asset is defined as the sum of the products of VAT exclusive lease payments, deducing the amount of depreciation and the tax rate for income tax (RIT).

The value of the property tax (RIT) accrued over the useful life of the asset is determined in accordance with the norms of the tax law as the sum of the products of the average annual (average) value of the asset calculated for the k-th reporting period of the 20n year (AAVk, 20n) and tax rate for property tax (RPT). Reporting periods are the first quarter, six months and nine months of the calendar year, and the tax period is the calendar year. If the amount of the advance payment for the corresponding reporting period is calculated, the tax rate (RPT) must be multiplied by 1/4.

The average annual value of an asset for a tax (reporting) period is determined as a quotient from dividing the amount obtained as a result of adding the values of the residual value of the asset to the 1st day of each month of the tax (reporting) period and the 1st day of the moth followed by the tax (reporting) period, by the number of months in the tax (accounting) period, increased by one.

The amount of the discounted amount of income tax reduction due to property tax P(ITPT) is calculated as the sum of the works of property tax payable for the k-th quarter of 20n year (PTk,20n) and the tax rate for income tax (RIT).

Thus, after calculating all potential costs associated with the acquisition of an asset under a finance lease agreement, the economic entity will determine the real value of this contract.

Potential costs of the enterprise when acquiring property under a contract of sale or purchase at the expense of a loan. Under a loan agreement, one party (a lender) transfers money or other things specified by generic characteristics to the property of the other party (a borrower), and the borrower undertakes to return to the lender the same amount of money (loan amount) or an equal number of other things of the same kind and quality received by him . However, during the analysis loan agreement will be applied, which is provided only in cash. As can be seen from the definition, borrowed funds can be borrowed without accrual of interest, but this is not a prerequisite for this agreement, and the lender has the right to receive interest from the borrower at the loan amount.

Assets purchased under a contract of sale are the property of an economic entity are recorded on the balance sheet as fixed assets. Property, plant and equipment items are evaluated at historical cost. In accordance with the paragraph 16 of IAS 16: Property, plant and equipment, the initial value of property, plant and equipment includes:

the price of its purchase, including import duties and non-refundable purchase taxes, less trade discounts and concessions;

all the costs that directly relate to the delivery of the asset to the intended location and bring it into a state necessary for operation in accordance with the intentions of the organization’s management, namely:

site preparation costs;

initial shipping and handling costs;

installation costs;

the amounts of remuneration for professional services provided and other costs.

When a fixed asset becomes available for use, depreciation begins to accrue on it (paragraph 55 of IAS 16). There are tax consequences that also need to be taken into account in the analysis – property tax, value added tax and changes in the taxable base for income tax.

When acquiring an asset under a purchase and sale contract, the supplier issues an amount of VAT to the enterprise, which it can present for deduction from the budget.

In accordance with IAS 23 Borrowing Costs, an entity must capitalize interest and other costs incurred in connection with the receipt of borrowed funds and directly related to the acquisition of the asset by including them in the cost of the asset. The capitalization of borrowing costs ceases when almost all the work necessary to prepare a qualifying asset for its intended use is completed (paragraphs 8, 22 of IAS 23).

Thus, the composition of costs incurred by an enterprise when raising funds under a credit (loan) agreement and acquiring an asset under a sales contract will be as follows:

the amount of the principal debt under a loan or credit agreement (in our case it is equal to the value of the acquired object);

the amount of accrued interest in full;

the influence of inflation on the amount of VAT in connection with the change in the period of its payment to the supplier and to the budget;

the amount of property tax on the acquired asset.

In accordance with the tax legislation, interest on loans and borrowings of the borrower for tax purposes are related to non-operating expenses, regardless of the fact for what aims these borrowed funds were obtained, most importantly, that they are used in entrepreneurial activities aimed at generating income.

When an entity adds a fixed asset to its cost breakdown in determining the tax base for income tax it is qualified as:

expenses related to production and sale, – the accrued amount of depreciation;

other expenses related to production and sales, – the amount of the assessed property tax;

non-operating expenses – the amount of interest on credit or loan agreements.

Thus, the potential costs of an enterprise for the acquisition of an asset under a purchase-sale contract at the expense of a loan will be determined as the difference between the discounted amount of payments on the loan (loan), provided that its size will be equal to the cost of the acquired asset (P(C)), and the current amount of the property tax that would be paid by the organization until the full amortization of the acquired asset, with consideration of the inflation (deflation) (P(PT)), the inflation (deflation) adjusted amount of VAT specified in the relevant tax document; the inflation (deflation) adjusted amount of income tax reduction due to depreciation of the acquired asset during the period of its depreciation (P(ITD)); the discounted amount of income tax reduction due to property tax (P(ITPT)) and discounted amount of the reduction in the profit tax due to the attribution to expenditure of the amount of interest under the loan or credit contracts (P(ITGR)).

Interest on loans is calculated using the effective interest method in accordance with IFRS 9. During the reporting period, interest income is calculated by applying the effective interest rate to the amortized cost of the financial asset in accordance with paragraph 5.4.1 (b) of the standard. In subsequent reporting periods, interest income must be calculated by applying the effective interest rate to the gross book value if the credit risk for a financial instrument is reduced to such an extent that the financial asset is no longer credit-impaired and this reduction can be objectively related to an event that occurred after the application of the requirements of item 5.4.1 (b) (for example, with an improvement in the borrower’s credit rating). The discounted value of payments on a credit (loan) is defined as the amount of the present value of the acquired asset under a sale and purchase agreement with VAT (IC) and interest on the credit (loan). Interest on the credit (loan) is calculated by multiplying the discounted value of the acquired property (IC) by the interest rate for the use of the loan (credit) for the j-th period (ij).

The value of inflation (deflation)-adjusted VAT P (VAT) is defined as the product of the VAT amount paid to the property provider and the discount factor (Fdisc).

The discounted amount of income tax reduction due to depreciation of the acquired property P(ITD) is determined as the sum of the products of accrued depreciation for this property for the i-th month, the tax rate for the profit tax RIT and the discount factor (Fdisc). In accordance with the tax legislation, depreciation is calculated as the product of either the original value of the property when applying the linear method or the total balance of the depreciation group (subgroup) into which the property will be included when applying the nonlinear method and the depreciation rate.

The current value of the property tax that will be paid by the organization before the full depreciation of the acquired property P(PT), and the discounted amount of income tax reduction due to property tax P(ITPT), will be determined as well as for the asset purchased under the financial lease.

The inflation (deflation)-adjusted amount of the reduction in the profit tax due to attributing the amount of interest under loan or loan agreements P(ITGR), to expenses is determined as the sum of the products of interest under the loan or loan agreements for the j-th month of GRj, the tax rate for the profit tax (RIT) and the discount factor (Fdisc).

Sources of information for calculating the potential costs of an enterprise when acquiring property under a purchase and sale contract at the expense of a loan are the information of a seller and a credit organization in a form of an information letter, price list and other documents.

Thus, the calculation and comparison of the amounts of potential costs for the acquisition of property under a financial lease agreement and under a purchase and sale contract at the expense of a loan or a loan justifies the choice of the type of borrowing as a source of financing, if it is necessary to update the fixed production assets in case of a deficit in the company’s own funds.

Conclusion

The result of the research is in developing a methodology for management analysis of the effectiveness of financial leasing operations based on indicators adjusted to meet the requirements of international accounting standards. At the heart of the methodology proposed by the authors is a comparison of the amounts of potential expenses of an enterprise depending on the type of borrowing: lending or lease. The lists of potential expenses are compiled in accordance with the applicable regulatory legal acts, taking into account the tax consequences of transactions and the inflation component. The choice of the source of borrowing is determined by the result of a comparison of potential costs when acquiring property under a financial lease agreement and under a purchase or sale contract at the expense of a loan. The decision is made in favor of the source of borrowing, whose potential costs will be the least. The method of management analysis developed by the authors of the article allows to achieve the main goal of accounting, that is, to make the right management decisions regarding the choice of the source of financing when updating the organization’s means of production, improve the efficiency of transactions, and optimize the costs of the enterprise.

Acknowledgments

The work was supported by the Act 211 of the Government of the Russian Federation, contract No 02.A03.21.0011.

Agibalov, A.V., and Gorelkin M.V. (2016) «On the evaluation of the effectiveness of the loan», Bulletin of the Voronezh State Agrarian University, 4(51), 240-246.

Arevalo, O., Saman, D.M., Bonaime, A., and Skelton, J. (2010) «Mobile dental units: Leasing or buying? A dollar-cost analysis», Journal of Public Health Dentistry, 70(3), 253-257.

Bezzateeva, T. (2016) «IFRS 16 Lease», International Financial Reporting Standards, 5 [Online]. [Retrieved February 21, 2018]. Available: http://www.profmedia.by/pub/msfo/].

Bezzateeva, T. (2017) «Accounting for leases according to IFRS» [Online]. [Retrieved February 21, 2018]. Available: http://www.cfin.ru/ias/msfo/IFRS_16_Leases.shtml.

Clausen, C.C., Bauer, M., Saleh, A., and Picker, O. (2008) «Financing problems of capital goods: Part 2: Procedure for investment appraisal» [Finanzierungsproblematik von investitionsgütern: Teil 2: Verfahren der investitionsrechnung], Anaesthesist, 57(7), 711-716.

Conbeer, G.P. (1990) «Leasing can add flexibility to asset management», Healthcare Financial Management, 44(7), 27-32.

Dmitrieva I.N. (2010) «Leasing and credit: a comparative analysis applied to strategic analysis», Financial analytics: problems and solutions, 10(34), 29-40.

Holt, A., Eccles, T., and Bond, P. (2012) «Changing practice in accounting for service charges in commercial property: A longitudinal analysis», Journal of Accounting and Organizational Change, 8(2), 186-209.

Imhoff Jr., E.A., Lipe, R.C., and Wright, D.W. (1997) «Operating leases: Income effects of constructive capitalization», Accounting Horizons, 11(2), 12-32.

Islam, M.A., Islam, M.R., and Siddiqui, M.H. (2014) «Lease financing of Bangladesh: A descriptive analysis», International Journal of Economics, Finance and Management Sciences, 1(2), 33-42.

Kovalev, V.V., and Kovalev, V.V. (2016) «Accounting for lease: History, development and challenges», Proceedings of the 27th International Business Information Management Association Conference, IBIMA, 1, 457-465.

Lazar, A., Avram, M.M., Duinea, E.M., Nita, M.M., and Gurau, M. (2010) «Knowledge Management and Innovation: A Business Competitive Edge Perspective», Proceedings of the 15th International Business Information Management Association Conference, IBIMA, 1, 200-205.

Michelman, J.E., Gorman, V., and Trompeter, G.M. (2011) «Accounting fraud at CIT computer leasing group, Inc», Issues in Accounting Education, 26(3), 569-591

Miroshnikova, T. (2015) «Formation of an Effective Mechanism of Financial and Credit Support Reproduction Process», Mediterranean Journal of Social Sciences, 5(6), 84-92.

Nash, C.Y., and Flesher, D.L. (2005) «Employee leasing. The antebellum 1800s and the twenty-first century: A historical perspective of the contingent labour force», Accounting, Business and Financial History, 15(1), 63-76.

Naumkina, N.A. (2012) «Efficiency of the acquisition of fixed assets through leasing», Bulletin of the Samara State University of Communications, 1(15), 51-54.

Séverin, E. (2010) «Self organizing maps in corporate finance: Quantitative and qualitative analysis of debt and leasing», Neurocomputing, 73(10-12), 2061-2067.

Simons, R.A. (1994) «Public Real Estate Management and the Planner’s Role», Journal of the American Planning Association, 60(3), 333-343.

Tsarkov, V.A., Malikova, O.S., and Takshaitov, Т.А. (2013) «Investment model of the leasing transaction», Finances and credit, 14, 62-68.

Zaridis, A.D. (2017) «Comparative Analysis of Leasing’s Evaluation as a Method of Financing Investments in Greek Agribusiness Sector Before and During Greek Economic Crisis», Journal of Business and Economic Development, 2(2), 79-86.