National and Kapodistrian University of Athens, Athens, Greece

Volume 2020,

Article ID 668702,

Journal of Accounting and Auditing: Research & Practice,

16 pages,

DOI: 10.5171/2020.668702

Received date: 1 October 2019; Accepted date: 28 November 2019; Published date: 23 January 2020

Academic Editor: Aliya Isiksal

Cite this Article as:

Dimitris BALIOS and Theodora ZAROULEA (2020), " Corporate Governance, Internal Audit and Profitability: “Evidence from P.I.G.S. Countries” ", Journal of Accounting and Auditing: Research & Practice, Vol. 2020 (2020),

Article ID 668702, DOI: 10.5171/2020.668702

This paper aims to explore whether and how specific corporate governance and internal audit determinants affect the profitability of businesses in the countries internationally called P.I.G.S. (Portugal, Italy, Greece, Spain, respectively). The sample consists of listed companies of the Southern European countries P.I.G.S. The survey data covers the period 2011-2016. Statistical analysis was based on a panel data regression model. In contrast to many research studies, this paper finds that internal managers are more suitable to perform the duties of the audit committee effectively, that there is a positive effect in profitability by increasing the Board Size with new members and that frequent meetings of the boards entail additional costs that outweigh any benefits. In addition, there is evidence that firms’ profitability may behave differently in countries with similar macroeconomic and cultural characteristics and for specific examined periods.

Firm profitability is a crucial factor for both a) long term firm survival – success and b) countries growth and unemployment rates. To date, a large amount of empirical research has examined the factors determining profitability focusing on accounting information; information extracted by financial statements. Besides, the relationship between firm performance and corporate governance characteristics is well established. Researchers and managers are very interested in the factors affecting firm performance and work in that direction.

Although we have a growing body of research on the above issues, the question remains open in the empirical literature. Not only contradicted results on the effect of specific factors on firm profitability have been found (see Section 2), but our knowledge on the behaviour of these determinants, especially in countries facing economic instability, is limited. Little attention has been paid to firm profitability determinants in periods of financial crisis and political instability.

This study examines the influence of a set of variables on firm profitability. We focus on Southern Europe countries called P.I.G.S., more specifically, Portugal, Italy, Greece, and Spain. We pick these countries in a time that P.I.G.S. faced macroeconomic instability in a country level and the European Commission asked for specific measures to converge to the other countries. Besides, the cultural characteristics of these countries such as individualism, uncertainty avoidance, power distance, masculinity, long term orientation are at the same level (Hofstede Insights Culture Compass). Because of these characteristics, we aim to explore whether and how specific corporate governance and internal audit characteristics affect the performance of businesses in the countries internationally called P.I.G.S.

We try to fill the gap on the effect of firm performance determinants in a sample of companies with similar country macroeconomic and cultural characteristics. We use variables such as the Audit Committee Independence, the Board Size and the Number of Board Meetings in a panel data regression model and we conclude on whether these variables react as the majority of researchers’ support.

This study consists of 4 more sections. A literature review, which leads to the paper’s research propositions, is presented in Section 2. Section 3 contains a summary of the data and methods used. Section 4 presents the findings resulting from the primary analysis. Section 5 concludes the paper with a discussion of these findings and their implications, limitations of the work and suggestions for further inquiry.

Literature Review and Research Proposition

The impact of the board of directors on corporate performance has attracted the interest of many researchers, over time. It is considered that the board is one of the most critical control mechanisms of corporate governance, as it has the authority to monitor and supervise senior management, to advise and to prevent the adoption and implementation of decisions (Weisbach, 1988). A significant number of surveys have studied the relationship between corporate performance and the various features of the board of directors. Indicatively, previous studies have shown that performance is positively affected by the existence of small-sized boards (Conyon and Peck, 1998; Eisenberg et al., 1998; O’ Connell and Cramer, 2010; Yermack, 1996), high frequency of board meetings (Chou and Buchdadi, 2017; Chou et al., 2013; De Andres and Vallelado, 2008; Ntim and Osei, 2011; Vafeas, 1999), and high board gender diversity, with an appreciable participation of women in them (Campbell and Minguez-Vera, 2008; Carter et al., 2003; Erhardt et al., 2003; Krishnan and Park, 2005; Lűckerath-Rovers, 2013; Terjesen et al., 2016; Xie et al., 2018).

Another issue that researchers have been preoccupied with, in the broader subject of corporate governance, is the impact of the composition of the audit committee and the individual characteristics of its members as well, on the performance of an economic entity. Despite conflicting views, the main conclusions of the existing literature are related to the positive impact of audit committees on the performance of organisations, under certain conditions. The boards’ basic characteristics have to be the high degree of independence (Alqatamin, 2018; Chan and Li, 2008; Kallamu and Saat, 2015; Rosenstein and Wyatt, 1990; Williams et al., 2015). In addition, their members need to have financial/accounting experience/expertise (Aldamen et al., 2012; Chan and Li, 2008; Davidson et al., 2004; Defond et al., 2005; Sellami and Fendri 2017).

The 2008 financial crisis affected credit markets, and many researchers studied the impact of the crisis on corporate governance and bank performance (Hau and Thum, 2009; Aebi et al., 2012; Erkens et al., 2012). Ayadi et al. (2019) analyzed the effects of governance mechanisms on banks’ profitability (ROA as the dependent variable) before and after the 2008 crisis and concluded that banks undertake tradeoffs between different governance mechanisms and that internal mechanisms have a significant impact on bank performance. These studies focus on banks. To our knowledge, there are no references on non-financial companies in the period we examine in this paper, and especially on P.I.G.S.

In the following paragraphs, we present the relevant literature on each of these relationships, and we develop the research hypotheses of the paper. We focus in Section 2.1 on Audit Committee Independence, Audit Committee Background and Skills in Section 2.2, Board Size in Section 2.3, the Frequency of Board Meetings and the Participation of Women on the boards in Sections 2.4 and 2.5 respectively.

Audit Committee Independence

One of the factors that have gathered the attention of researchers is the establishment of the audit committee and, in particular, the “independence” of its members. Despite the existence of several different definitions, in general, a committee is classified as “independent” when the majority of its members are executives who do not come from within the company and its management, but it consists of outside managers. (Fuzi et al., 2016)

A significant number of surveys have focused on the impact of the audit committee independence on corporate performance, both in terms of stock market performance and operating performance. The main feature of these surveys is that, in their majority, they support the particular positive effect of an independent audit committee on corporate performance. Rosenstein and Wyatt (1990) noted that the announcement of the placement of an additional external manager on the board would increase the company’s market value. Likewise, Chan and Li (2008) advocate that the audit committee independence enhances firm value. This effect is more robust when the majority of members come from the outside environment of the business (Williams et al., 2015). In addition, Kallamu and Saat (2015) argue that the participation of independent managers in the audit committee leads to an improvement of the company’s performance, whereas Alqatamin (2018) found a positive relationship between the independence of the members of the audit committee and the company’s profitability.

On the other hand, Vafeas (2000) failed to demonstrate a statistically significant relationship between the participation of more external members, in the various committees of a company and its performance. Finally, Klein (1998) pointed out that the participation of internal managers on the board and the individual administrative committees favourably affects the various performance indices, including the ROA index. In conclusion, the existence of independent managers from the external environment of the company is expected to contribute to corporate profitability positively.

Audit Committee Background and Skills

The financial / accounting background, experience and expertise of the members of the Audit Committee are equally important for the effective operation of the internal control (Carcello et al., 2006). Defond et al. (2005) reported that the investors react very positively when a company announces the recruitment of external executives with financial / accounting background and experience, in order to staff its audit committee. Furthermore, the investigation of Davidson et al. (2004) in a significant number of companies of the NASDAQ index reached the same conclusion, i.e. the announcement of hiring executives with financial / accounting expertise to the audit committee is followed by positive stock returns for these companies. Chan and Li (2008) claim that the participation of executives with financial / accounting background and expertise is not sufficient when it comes to increasing a company’s performance in the market. This finding changed when the financial / accounting expertise was combined with the existence of an independent committee. It became clear that the integration of external members with financial / accounting training and experience in the audit committee leads to higher performance. Similarly, according to Aldamen et al. (2012) and Sellami and Fendri (2017), the higher the percentage of experienced executives that compose an audit committee, the higher the performance is expected to be. It, therefore, appears that financial / accounting expertise positively affects a company’s profitability in the market.

Board Size

Over time, the existing literature links the board’s growth to some negative side effects (Eisenberg et al., 1998; Jensen, 1993; Yermack, 1996). Firstly, the more the number of members grows, the more difficult it gets to have effective direct communication. Meanwhile, Yermack (1996) pointed out that the large boards anticipate greater participation of outside managers, who generally oppose the implementation of very risky administrative actions, for fear of possible negative consequences. In this sense, therefore, it is not excluded that a large board will block the implementation of lucrative moves. Indicatively, Jensen (1993) strongly supports that the benefits of expanding the board are outweighed by the costs associated with increasing its membership. More specifically, he claims that the more the board’s size increases, the more inefficient is the exchange of ideas. Similarly, Vafeas (2000) reported that investors assess positively the profits declared by companies with small-sized boards. The same conclusions were drawn by Yermack’s survey (1996), which focused on multimember boards of companies belonging to the Fortune 500 index.

Additionally, Eisenberg et al. (1998) conducted a study on a sample of Finnish small and medium-sized companies. They found that the negative relationship between the board size and the corporate performance, as measured by the ROA ratio, not only applies to large companies with large boards, but also extends to small companies with small boards. O’Connell and Cramer (2010) underlined the negative relationship between the board size and ROA, in a sample of Irish businesses. Particularly interesting were their findings on the fact that this negative relationship is less intense in smaller businesses. By studying European companies, Conyon and Peck (1998) reached the same conclusion. Moreover, Zabri et al. (2016) found an inversely proportional relationship between the board size and corporate performance, as measured by ROA. Based on the above analysis, it appears that the increase in board size is inversely proportional to corporate profitability.

The frequency of Board Meetings

A typical indication of the level of activity and the active participation of the board of a company in its operation is the frequency of board meetings. The relationship between the frequency of meetings and corporate profitability is not clear. Frequent meetings involve notable benefits, but significant costs as well (Vafeas, 1999). The increased activity of the board, which is evident from the frequency of board meetings, has beneficial effects on the operating profitability of the business (Vafeas, 1999). In particular, Vafeas (1999) showed that the increase in the frequency of board meetings is linked to a rise in profitability ratio, such as ROA index, which may apply up to three years. At the same time, Vafeas (1999) supports that the increase of the meetings is often associated with the previous low performance of the company, and therefore the board is motivated to resolve any problems. Similarly, de Andres and Vallelado (2008) clarified that the number of board meetings favours corporate profitability.

In turn, Chou et al. (2013) defended the positive impact of the meetings through a study in the Taiwan market, but have set an essential prerequisite. Specifically, they characterized the board meetings as successful, in terms of company performance, when their members attend these meetings.

On the other hand, when the delegates attend the meetings instead of the actual members, the corporate performance is affected. In addition, Ntim and Osei (2011) confirmed the proportional relationship between the company’s frequency of meetings and performance. Similar results came from Chou and Buchdadi (2017) in a survey they conducted in Indonesian companies. Briefly, they found that the number of board meetings is positively related to Return on Assets (ROA). In a further study of the relationship between corporate performance and frequency of board meetings, Brick and Chidambaran (2010) identified that the increased supervisory activity of the board had no significant impact on the performance of the companies, but resulted in higher market value. On the contrary, Johl, Kaur and Cooper (2015), who studied a large number of Malaysian listed companies, claimed that very frequent board meetings affect ROA. Based on the above, the conclusion is that the larger the number of meetings, the more favourable is the repercussion on corporate profitability.

The Participation of Women on the Boards

One of the most popular issues the researchers have been preoccupied with over time is the impact of gender. Many researchers have studied the women’s participation and the effective operation of the board and, as a result, the improvement of the performance of the companies. For example, Miller and del Carmen Triana (2009) have argued that the increased participation of women in a company’s board, leads on the one hand to more innovative decisions, and on the other hand it contributes to the organisation’s reputation. Both these effects of diversity are associated with higher performance. Their analysis on a sample of Fortune 500 firms has indeed confirmed that the more noticeable participation of women in the board has an indirect positive impact on performance, through the adoption of pioneering concepts.

At the same time, several scholars have argued that the stronger participation of women on the boards has an immediate positive impact on corporate performance (Erhardt et al., 2003; Terjesen et al., 2016). In particular, Krishnan and Park (2005) stated that the greater participation of the female gender in the management of a company leads to higher performance, as measured by the ROA index. Also, Lückerath-Rovers (2013) found that companies that staff their boards with women outweigh companies that have no women on the board, both in terms of performance (ROE) and profitability (EBIT), but also in terms of growth rate of the stock price.

Also, Xie et al. (2018) reported that the increased participation of women on the board is associated with greater performance (ROA) and higher market value. Similarly, according to Carter et al. (2003), the participation of women in boards is also associated with the higher performance of organisations in the stock market. Consequently, Campbell and Minguez-Vera (2008), examining a sample of Spanish companies, found that greater female gender participation in the board means higher market value. A respectively positive relationship between the number of women participating in the board and the corporate performance (ROA) was also highlighted by Carter et al. (2010), in a study of major American businesses.

Some studies question this beneficial effect of women. In a survey carried out by Rose in a sample of Danish enterprises, it has not been possible to prove the existence of a positive relationship between performance and female representation in the management. Accordingly, Dimovski and Brooks (2006) have failed to demonstrate the existence of a direct and statistically significant relationship, either positive or negative, on the participation of female gender in the board and the effect on corporate performance.

Many studies have argued that greater female participation in the board has negative financial results for the company. For example, Shrader et al. (1997) pointed out that women’s participation on boards has a negative impact on corporate performance. Similarly, in a survey that focused on US companies, Adams and Ferreira (2009) reported that there is a negative correlation between the highest proportion of women in the board and the value of the company. Overall, the majority of surveys have supported a favourable relationship between women’s presence on boards and corporate profitability.

Simply stated, our research investigates how the audit committee independence and the audit committee background and skills, as well as the board size, the frequency of board meetings and the board gender diversity, affect corporate profitability measured by Return on Assets.

Data and Methodology

This research focuses on the role of five main corporate governance variables in the performance of a sample of 74 companies from Portugal, Italy, Greece, and Spain (P.I.G.S.). The current study proposes and examines research on the impact of the audit committee independence and the audit committee background and skills on the performance of a company. On the other hand, we take into consideration the board size, the frequency of board meetings and the board gender diversity. To our knowledge, this is the first research that examines the relationship between corporate governance and internal audit characteristics and profitability, in the environment of the so-called P.I.G.S. (Portugal, Italy, Greece, Spain).

Sample Selection

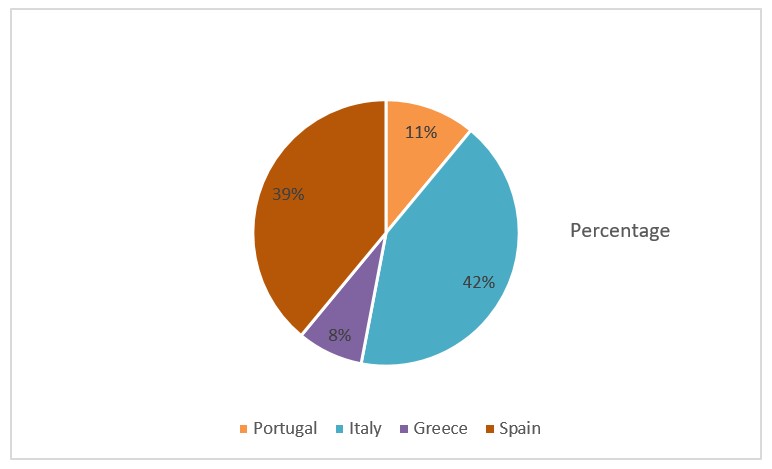

We used the Thomson Reuters Eikon database to collect our data. We initially examined 593 listed companies. Forty-seven from Portugal, 231 from Italy, 171 from Greece and 144 from Spain (3.813 observations in total). We excluded the financial sector’s entities for reasons of heterogeneity on their balance sheet. Besides, we omitted 76 companies with no corporate governance and audit committee. Outliers in 2 companies were observed and removed by diagrammatic analysis. The final sample includes 359 observations. The time horizon for each company consists of the years between 2011 and 2016. The above observations correspond to 74 companies from 4 Southern European countries which are our final sample. More specifically 31 based in Italy (42%), 29 in Spain (39%), 8 in Portugal (11%) and 6 in Greece (8%). Figure 1 illustrates the business rates that correspond to the sample countries.

Fig. 1: Graphic depiction of the sample companies per country (percentages)

The data for each company is complete, and there are no missing values in all variables collected. There are also some diversifications in the set of data available for each business.

We analysed data based on the eViews 9 econometric software. Given the longitudinal observations of each company, we chose a panel data regression model. Moreover, the Hausman test was used to select between random and fixed effects of the regression model (Hausman, 1978). The results of the Hausman test led to the selection of a fixed effects model. Finally, heteroscedasticity control was performed using the White test (White, 1980). We set the statistical significance level at 5%.

Research Design

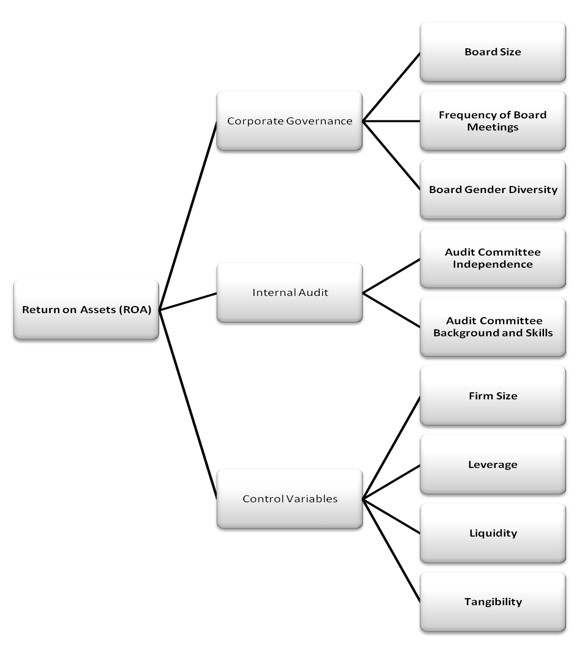

Firm profitability – as a dependent variable – is generally regarded as an essential precondition for long-term firm survival and success. Moreover, the variable significantly affects the firm’s achievement of other financial goals. We studied firm performance by using market-based measure or accounting based figures. ROA was used as a dependent variable, as the literature widely uses it. In general, we follow the literature and the variables generally used in order to make our results totally comparable. According to theory, the variables that might explain firm profitability can be classified into three main categories of independent variables: corporate governance, internal audit and control variables. Corporate governance is characterised by the board size, the frequency of board meetings and the women’s participation on board. Internal audit operates based on the Audit Committee Independence and the Audit Committee Background and Skills. Control variables consist of the Size, the Leverage, the Liquidity, and the Tangibility. Figure 2 depicts our research design.

Fig. 2: Dependent and independent variables of the model

ROA is the dependent variable in our model as a measure of the performance. We calculate ROA as the net accounting profit before interest, tax, depreciation, and amortisation (EBITDA), divided by total assets.

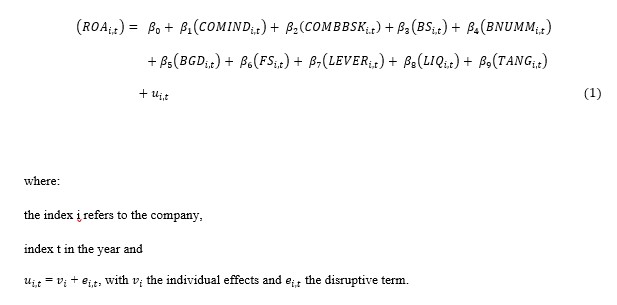

We concluded to the following empirical regression model:

Variable Definitions

The study takes into account specific determinants that affect the efficiency of an organism (dependent variable). The ROA measures this variable.

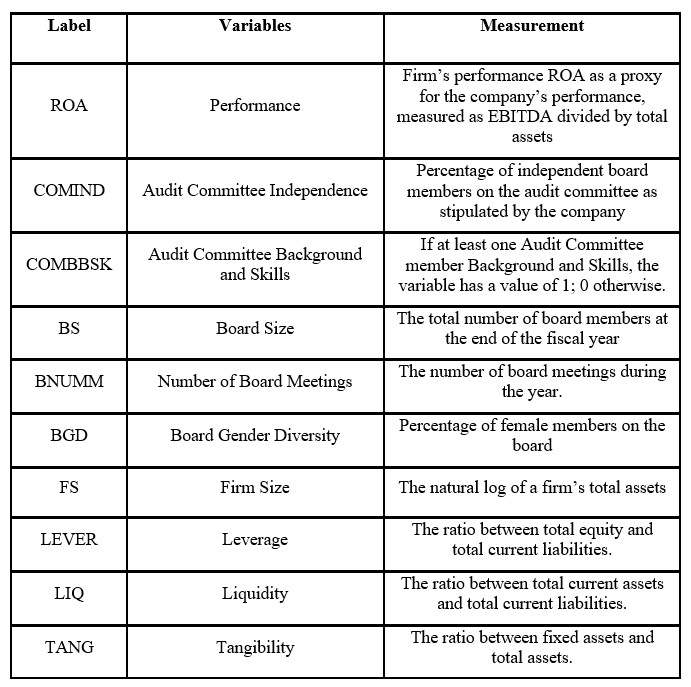

ROAi,t : Corporate performance, ROA as a proxy for the company’s performance, measured as EBITDA divided by total assets.

The defining parameters that constitute the independent variables of this paper are discussed below. Particularly:

COMMINDi,t: The Audit Committee Independence is defined as the percentage of independent Board members in the Audit Committee.

COMBBSKi,t: The Audit Committee Background and Skills is determined based on the participation of at least one member, with a similar background.

BSi,t: The Board Size results from the total number of its members at the end of each financial year.

BNUMMi,t: The Frequency of Board Meetings is determined by the number of meetings of its members during each year.

BGD i,t: The Board Gender Diversity is defined as the percentage of women participating in it.

Control Variable Definitions

In order to test the effect of the determinants on the dependent corporate performance variable, the analysis included four control variables related to the characteristics of the sample companies.

FS i,t: The Firm Size, which is the natural logarithm of its total assets.

LEVERi,t: The Leverage is measured by the ratio between total equity and total current liabilities.

LIQ i,t: The Liquidity results from dividing total current assets to total current liabilities.

TANG i,t: The Tangibility of business comes as a result of the fixed assets fraction to total assets.

Table 1 shows in detail the dependent and independent variables of the model, as well as their performance metrics.

Table 1: Variables definition

Descriptive Statistics

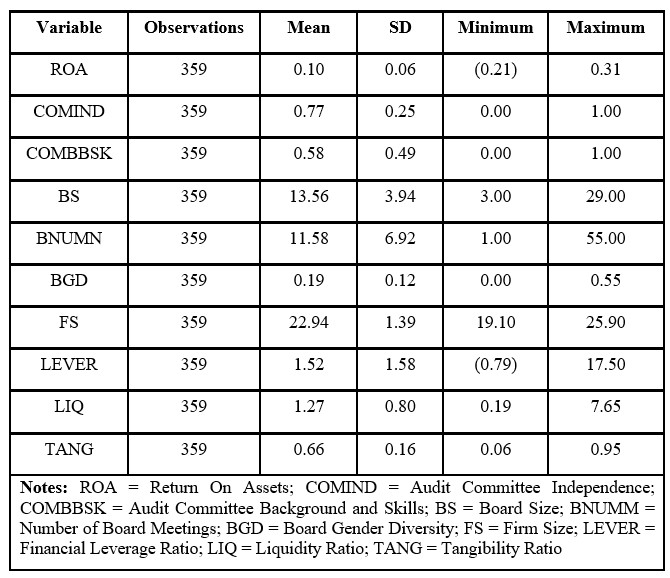

Initially, descriptive measures are presented for all the variables included in the fixed effects regression model. The average value, the standard deviation, the minimum, and the maximum values are given for each of the continuous variables, as shown in Table 2.

Table 2: Descriptive statistics

Table 2 shows that the dependent variable (ROA), which measures the performance of each company for the period of 2011 – 2016, varies with 10% average, between a minimum value of (21)% and a maximum value of 31%. Regarding the Audit Committee Independence, 77% of its members, on average, come from the external business environment and therefore have a high degree of independence. Also, as an average, 58% of its members have financial / accounting expertise. We discuss the parameters for the Board Meeting below. It appears that the average size of the Board Meeting is 14 members. At the same time, there are as much numerous Board Meetings of 29 members, as small ones with only three members. Concerning the Frequency of Board meetings, the Boards meet approximately 12 times per year. Certainly, there are very active Board Meetings, which reach 55 meetings per year. Table 2 shows that, in general, female participation in the Boards is relatively low, reaching 20%, that is, only 1 out of 5 members are women. Surely, in exceptional cases, women represent the majority of the Board, while in other Boards they are absent. Concerning the control variables, the sample companies are characterised by high assets, relatively low liquidity compared to the widely accepted value (1.27 vs > 2) and high consolidation. We conclude that there is no high volatility in almost all variables, as standard deviations are significantly lower than the corresponding average values.

Correlation Analysis

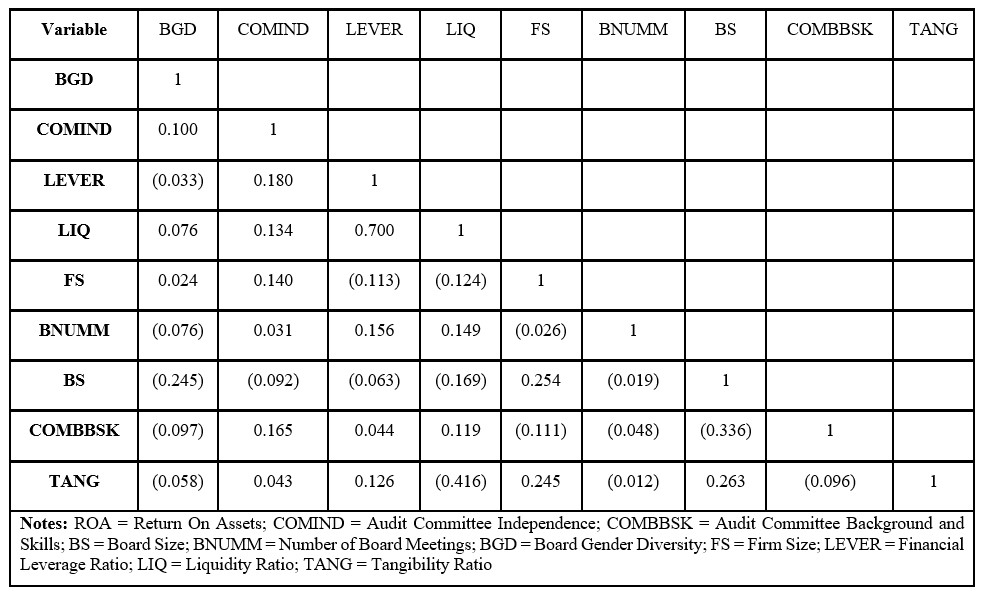

Table 3 presents non-parametric Spearman correlation coefficients among all the independent variables.

Table 3: Correlation analysis

We first calculate the Pearson correlation coefficients between the dependent and independent variables (Table 3) and we conclude that there are no high correlations between the variables of the regression model. The correlation coefficient between the leverage and liquidity ratios is 0.70, smaller than 0.80, which is the limit line drawn by Kennedy (1985). Since multicollinearity problems in regression models can occur if the correlation coefficient between independent variables exceeds 0.80 in absolute value, we assumed that all variables could remain in the model.

Empirical Results

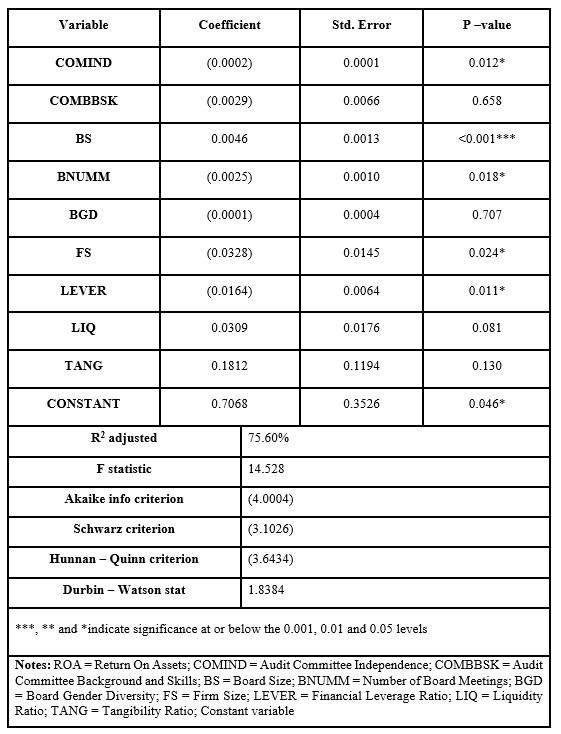

We used a regression model for panel data to investigate the determinants of the impact of corporate governance on the profitability of an organization. The Hausman test rejected the null hypothesis (P value <0.001) and therefore a fixed effects model was adopted. The F test rejected the null hypothesis (P <0.001), and the use of a fixed effects model against the corresponding OLS model was confirmed. The White Test rejected the null hypothesis (P value <0.001) of homoscedasticity. For weighted results in the presence of heteroskedasticity, the Huber / White estimators were used to evaluate the standard errors of the model coefficients. Table 4 shows in detail the results of the regression model.

Table 4: The results of the Regression Model

The regression model is overall statistically significant (F statistic = 14.528, P <0.001), meaning it interprets statistically a significant part of the variability of the dependent variable. The coefficient of determination (R2) is 0.812, and the corresponding adjusted coefficient of determination (R2 adjusted) is 0.756. Given the plurality of independent variables, the adjusted coefficient of determination determines that the regression model explains 75.6% of the variability of the dependent variable. This percentage is very satisfactory and certifies that the appropriate independent variables have been included in the model to study the changes in the dependent variable.

The results reported in Table 4 suggest that the variables, Audit Committee Independence, Board Size and Number of the Board Meeting, have statistically significant effects (P <0.05) on corporate performance. The impact of the Audit Committee Independence on corporate performance is found negative and statistically significant [β = (0.00017), p = 0.012]. A statistically significant and positive association between Board Size and corporate performance is found (β = 0.0046, p <0.001). Finally, the Number of Board Meetings has a negative and statistically significant effect on company performance [β = (0.0025), p = 0.018].

Although the Audit Committee Background and Skills positively affect corporate performance, the results showed a negative relationship between the two [β = (0.0029), p = 0.6584], which is not statistically significant. Although the percentage of Female Board Members is positively correlated with corporate performance, the effects of regression showed a negative relationship [β = (0.00015), p = 0.707], but statistically insignificant.

Referring to the control variables, two out of the four included in the regression model (Firm Size, Financial Leverage, Liquidity, and Tangibility) had a statistically significant relation with corporate performance. More specifically, the Firm size [β = (0.0328), p = 0.024] and Leverage have a negative effect [β = (0.0164), p = 0.011] on corporate performance. On the other hand, Liquidity and Tangibility ratios are statistically insignificant.

Robustness Tests

Finally, we performed robustness tests in separate models with dummy variables in terms of years and countries respectively. Conclusions remain unchanged in terms of p-values. We do not report the results for the sake of brevity.

Discussion

The paper analyzes the effect of internal audit and corporate governance on firms’ profitability. Our empirical analysis is conducted using a sample of 74 firms from the countries internationally called P.I.G.S. during the 2011-2016 period. We adopt a fixed effects panel data regression model that links internal audit, corporate governance and profitability. This research contributes to the literature dealing with the determinants of profitability as we focus on corporate governance and internal audit effects in firms from countries that face macroeconomic instability in a country level.

The obtained results show a negative impact of the high Audit Committee Independence on ROA ratio. This result is in contrast to the initial hypothesis, according to which, as the number of the external independent managers in the audit committee increases, the corporate performance strengthens. This result seems to question the proposals of a significant number of previous investigations on the audit committee independence (Alqatamin, 2018; Chan and Li, 2008; Kallamu and Saat, 2015; Rosenstein and Wyatt, 1990), which highlight the need to increase the independence of the audit committees, in order to better perform their tasks and ultimately improve corporate performance.

On the contrary, our study seems to be in line with Klein’s (1998) one, which emphasises the importance of staffing the committee with internal managers working in the business. There is evidence that internal managers are more suitable to perform the duties of the audit committee effectively. However, a lot of companies tend to replace internal managers with external ones, many of whom have little or no participation in the company’s growth until their hiring. It is speculated that this is due to external pressures (for example, the Business Roundtable, the American Law Institute, the share activists and the financial press), supporting the tangible benefits resulting from independent audit committees. Possibly, the study partly simulates Vafeas’ hypothesis (2000), who failed to associate independence with positive or negative performance. In any case, the findings highlight the need for more research, to better define this relationship.

Subsequently, a conclusion drawn from the results of this analysis is the positive effect in profitability by increasing the Board Size with new members. Although there is a limited number of surveys of the same direction (Adams and Mehran, 2012; Coles et al., 2008; de Andres and Vallelado, 2008), this result contradicts both the initial hypothesis and the vast majority of articles referring to this relationship (Conyon and Peck, 1998; Eisenberg et al., 1998; O’ Connell and Cramer, 2010; Yermack, 1996; Zabri et al., 2016). Researchers mentioned above have argued that particularly negative effects on performance accompany the increase in size. A possible explanation for the positive effect in profitability is the increased supervision by an abundant board. The increased supervision limits the wastage of money. Moreover, adding members in a board contributes to better decisions, as more views and knowledge are provided. Finally, in inefficient markets, board members may be a way of getting access to specific profitable projects.

The result of our study regarding the impact of the Board Meetings on corporate performance differs from the majority of research studies conducted previously. Many researchers support that frequent meetings of the boards entail additional costs that outweigh any benefits and burden on their performance. In line with Johl et al. (2015), we conclude on a negative relationship between board meetings and company performance. In an environment of economic and political instability, the board is expected to be more active in dealing with potential problems. For example, each additional meeting includes travel costs, extra members’ compensation, and valuable time expense. Of course, meetings allow managers to discuss crucial management issues and conduct a more thorough control function which is very important in a period of economic and political fluctuations.

On the other hand, the impact of the Audit Committee Background and Skills and the effect of the Board Gender Diversity on corporate performance, are statistically insignificant.

Equally remarkable findings emerged from the control variables, included in the regression analysis. High Leverage (debt burden) has been found to lead to a lower return, probably due to the higher entailed costs. Additionally, Liquidity is positively related to performance. On the other hand, we find that the large Firm Size is associated with a lower return, which is expected, given that larger-scale organisations are directly affected by negative economic developments.

Limitations and Opportunities for Future Inquiry

Researchers wishing to advance the current research are suggested to focus on one country, with a lot of companies providing the appropriate data, in order to draw more reliable conclusions. Thus, it would be useful to conduct comparative studies, in completely different geographical areas, something particularly appealing. Finally, an equally interesting proposal is to investigate more corporate governance variables. The independence and educational background of the board, the nationality of its members, the size, the compensation, the number of meetings and the participation of the CEO in the Audit Committee, are some factors worth analyzing.

Adams R. B. and Ferreira D. (2009) ‘Women in the boardroom and their impact on governance and performance’ Journal of Financial Economics, 94 (2), 291–309.

Aebi, V., Sabato, G. and Schmid, M. (2012) ‘Risk management, corporate governance, and bank performance in the financial crisis’ Journal of Banking and Finance, 36 (12), 3213-3226.

Aldamen H., Duncan K., Kelly S., McNamara R. and Nagel S. (2012) ‘Audit committee characteristics and firm performance during the global financial crisis’ Accounting and Finance, 52 (4), 971-1000.

Alqatamin R.M. (2018) ‘Audit committee effectiveness and company performance: evidence from Jordan’ Accounting and Finance Research, 7 (2), 48-60.

Ayadi M. A., Ayadi N. and Trabelsi S. (2019) ‘Corporate governance, European bank performance and the financial crisis’ Managerial Auditing Journal, 34 (3), 338-371.

Brick Ι.Ε. and Chidambaran N.K. (2010) ‘Board meetings, committee structure, and firm value’ Journal of Corporate Finance, 16 (4), 533-553.

Campbell K. and Minguez-Vera A. (2008) ‘Gender diversity in the boardroom and firm financial performance’ Journal of Business Ethics, 83, 435–451.

Carcello J.V., Hollingsworth C.W., Klein A. and Neal T.L. (2006) ‘Audit committee financial expertise, competing corporate governance mechanisms and earnings management’ New York University. Stern School of Business Accounting Working Papers, available at: https://archive.nyu.edu/handle/2451/27455

Carter D.A., D’Souza F., Simkins B.J. and Simpson W.G. (2010) ‘The gender and ethnic diversity of US boards and board committees and firm financial performance’ Corporate Governance: An International Review, 18 (5), 396–414.

Carter D. A., Simkins B. J. and Simpson W. G. (2003) ‘Corporate governance, board diversity and firm value’ The Financial Review, 38 (1), 44–53.

Chan K.C. and Li J. (2008) ‘Audit committee and firm value: evidence on outside top executives as expert-independent directors’ Corporate Governance, 16 (1), 16-31.

Chou H.I., Chung H. and Yin X. (2013) ‘Attendance of board meetings and company performance: evidence from Taiwan’ Journal of Banking and Finance, 37 (11), 4157–4171.

Chou Τe-Kuang and Buchdadi A.D. (2017) ‘Could independent board, board meeting, audit committee and risk committee improve the asset quality and operational performance? A study of listed banks in Indonesia’ Research Journal of Business and Management, 4 (3), 247-254.

Conyon M. J. and Peck S. I. (1998) ‘Board size and corporate performance: Evidence from European countries’ European Journal of Finance, 4 (3), 291–304.

Davidson W.N., Xie B. and Xu W. (2004) ‘Market reaction to voluntary announcements of audit committee appointments: The effect of financial expertise’ Journal of Accounting and Public Policy, 23 (4), 279–293.

De Andres P. and Vallelado E. (2008) ‘Corporate governance in banking: The role of the board of directors’ Journal of Banking & Finance, 32 (12), 2570–2580.

Defond M.L., Hann R.N. and Hu X. (2005) ‘Does the market value financial expertise on audit committees of boards of directors? ’ Journalof Accounting Research, 43 (2), 153-193.

Dimovski W. and Brooks R. (2006) ‘The gender composition of boards after an IPO’ Corporate Governance, 6 (1), 11–7.

Eisenberg T., Sundgren S. and Wells M. (1998) ‘Larger board size and decreasing firm value in small firms’ Journal of Financial Economics, 48 (1), 35-54.

Erhardt N. L., Werbel J. D. and Shrader C. B. (2003) ‘Board of director diversity and firm financial performance’ Corporate Governance, 11 (2), 102–111.

Erkens, D. H., Mingyi, H. and Pedro, M. (2012) ‘Corporate governance in the 2007-2008 financial crisis: evidence from financial institutions worldwide’ Journal of Corporate Finance, 18 (2), 389-411.

Fuzi S.F.S, Halim S.A.A. and Julizaerma M.K. (2016) ‘Board independence and firm performance’ Procedia Economics and Finance, 37, 460 – 465.

Hau, H. and Thum, M. (2009) ‘Subprime crisis and board (in-) competence: private vs. public banks in Germany’ Economic Policy, 24 (60), 701-751.

J. A. (1978) ‘Specification Tests in Econometrics’ Econometrica. 46(6): 1251–1271.

Jensen M. (1993) ‘The modern industrial revolution, exit, and the failure of internal control systems’ The Journal of Finance, 48 (3), 831-880.

Kallamu B.S. and Saat N.A.M. (2015) ‘Audit committee attributes and firm performance: evidence from Malaysian finance companies’ Asian Review of Accounting, 23 (3), 206-231.

Kaur Johl S., Kaur S. and Cooper B.J. (2015) ‘Board characteristics and firm performance: evidence from Malaysian public listed firms’ Journal of Economics, Business and Management, 3 (2), 239 – 243.

Kennedy, P. (1985) ‘A Guide to Econometrics’ 2nd ed., MIT Press, Cambridge, MA.

Klein A. (1998) ‘Firm performance and board committee structure’ Journal of Law and Economics, 41 (1), 275-303.

Krishnan H. A. and Park D. (2005) ‘A few good women: On top management teams’ Journal of Business Research, 58 (12), 1712–1720.

Lűckerath-Rovers Μ. (2013) ‘Women on boards and firm performance’ Journal of Management Governance, 17 (2), 491–509.

Miller T. and del Carmen Triana M. (2009) ‘Demographic diversity in the boardroom: mediators of the board diversity – firm performance relationship’ Journal of Management Studies, 56 (5), 755-786.

Ntim C. G. and Osei K. A. (2011) ‘The impact of corporate board meetings on corporate performance in South Africa’ African Review of Economics and Finance, 2 (2), 83-103.

O’ Connell V. and Cramer N. (2010) ‘The relationship between firm performance and board characteristics in Ireland’ European Management Journal, 28 (5), 387– 399.

Rose C. (2007) ‘Does female board representation influence firm performance? The Danish evidence’ Corporate Governance, 15 (2), 404–413.

Rosenstein S. and Wyatt J.G. (1990) ‘Outside directors, board independence and shareholder wealth’ Journal of Financial Economics, 26 (2), 175-191.

Sellami Y. M. and Fendri H. B. (2017) ‘The effect of audit committee characteristics on compliance with IFRS for related party disclosures: Evidence from South Africa’ Managerial Auditing Journal, 32 (6), pp.603-626

Shrader C. B., Blackburn V. B. and Iles P. (1997) ‘Women in management and firm financial performance: an exploratory study’ Journal of Managerial Issues, 9 (3), 355–73.

Terjesen S., Couto E. B. and Francisco P. M. (2016) ‘Does the presence of independent and female directors impact firm performance? A multicountry study of board diversity’ Journal of Management and Governance, 20, 447–483.

Vafeas N. (2000) ‘Board structure and the informativeness of earnings’ Journal of Accounting and Public Policy, 19 (2), 139-160.

Vafeas N. (1999) ‘Board meeting frequency and firm performance’ Journal of Financial Economics, 53 (1), 113-142.

Weisbach M. S. (1988) ‘Outside directors and CEO turnover’ Journal of Financial Economics, 20 (1), 431-460.

White H. (1980) ‘A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity’ Econometrica, 48(4): 817–838.

Williams B. R., Bingham S. and Shimeld S. (2015) ‘Corporate governance, the GFC and independent directors’ Managerial Auditing Journal, 30 (4), pp.324-346.

Xie J., Nozawa W., Yagi M., Fujii H. and Managi S. (2018) ‘Do environmental, social, and governance activities improve corporate financial performance?’ Business Strategy and the Environment, 28 (2), 1–15.

Yermack D., (1996) ‘Higher market valuation of companies with a small board of directors’ Journal of Financial Economics, 40 (2), 185-213.

Zabri S.M., Ahmad K. and Wah K.K. (2016) ‘Corporate governance practices and firm performance: evidence from Top 100 public listed companies in Malaysia’ Procedia Economics and Finance, 35, 287 – 296.

Notes

P value: Conducting Hausman test for random effects, p value is 0.004, result overruled (Ho: p value < 0.001). On the contrary, verification with cross section test for fixed effects results in p value 0.000