Volume 2021,

Article ID 404252,

Journal of Accounting and Auditing: Research & Practice,

11 pages,

DOI: 10.5171/2021.404252

Received date: 2 September 2020; Accepted date: 21 January 2021; Published date: 27 July 2021

Academic Editor: Małgorzata Macuda

Cite this Article as:

Ewa W. BABUSKA (2021), " The Changes of Polish Accounting Regulations after the 1989 Political Transformation Incorporation of Global Solutions", Journal of Accounting and Auditing: Research & Practice, Vol. 2021 (2021), Article ID 404252, DOI: 10.5171/2021.404252

The aim of the article is to present the changes in Polish accounting regulations in the last thirty years of the ongoing systemic transformation from socialism to capitalism, which began in Poland in 1989. The changes consisted in adjusting Polish regulations to the Directives of the European Union and to the International Accounting Standards and International Financial Reporting Standards. There are no synthetic studies on this subject in the available literature. The article partially fills this gap and is therefore original. The introduction provides a background followed by a retrospective outline of Polish and international accounting regulations. The main part describes the most important changes introduced to the Polish Accounting Act of 1994 over the last 25 years. The research method was a review of Polish, European and international accounting regulations in that period. The hypothesis related to the question whether the amendments to the Accounting Act were regular, immediate and adequate to the amendments of the EU and IAS / IFRS laws. The answer to the question was positive.

JEL classification: M41, K20, K29

Keywords: Keywords: regulations of accounting and financial reporting, the Polish Act on Accounting European Union Directives, International Standards IAS / IFRS.

Introduction

Accounting, which was developed over the centuries, in today’s socio-economic reality has gained the unquestionable and honorable name of the business language. It is an expression of the ennoblement of accounting in terms of theory, practice and policy. Fundamental accounting principles have been shaped in its historical development which is still going on (Surdykowska, 1999; Jaruga ed., 2002). Accounting development is international, for the reason that different countries have contributed to accounting advances. Accounting is subject to different legal systems in which are big differences, mainly in Europe. Therefore, apart from the existing specific national accounting systems, universal systems are created on a regional, international and world scale. The systems are the result of the ongoing processes of standardization and harmonization of accounting norms and practices. Standardization is associated with the standards of the International Accounting Standards Board (IASB) and harmonization with the directives of the European Union, (Alexander and Nobes, 2010). The accounting of highly developed countries has been standardized on the basis of international accounting standards [IAS – issued until 2001 by International Accounting Standards Committee (IASC)] and international standards of financial reporting [ISFR – issued since 2001 by IASB with its headquarters in London]. Standardization and harmonization of accounting and financial reporting resulted from the necessity to standardize various solutions found in accounting theory, practice and policy in particular countries and from the need to develop and implement international patterns of conduct in accounting, as well as in order to make financial reports in global economies comparable (Olchowicz, Tłaczała, 2015). The standards are not strictly provisions of law, but they are reflected in legal regulations of national states referring to the accounting and the financial reporting used there. The aim of the article is to present the changes in the Polish accounting regulations in connection with the transformations that have taken place in the Poland over the past thirty years. The chiefly section is preceded by an outline of Polish and international accounting regulations. The originality of the article lies in tracing the evolution in the Polish accounting laws during the systemic and economic transformation, adjusting them to the EU and IAS/IFRS solutions. The research method consists in reviewing the legal regulations: national, European and international, as the related literature on the subject does not synthetically and comprehensively reflect all changes introduced to the Polish Accounting Act during the period. The article is an attempt to fill this gap. The research hypothesis was verified by checking what changes and at what time were introduced to the Polish Accounting Act in accordance with the amendments of EU and IAS / IFRS laws. It was shown that changes to the Act were introduced regularly and adequately to European law and International Standards. The Act was frequently amended and adapted to new regulations on an ongoing basis, and the hypothesis was positively verified.

The retrospective outline of Polish and international accounting regulations

The Polish economy in 1945-1989 was a centrally-steered economy, with social (state) ownership, deprived of private ownership. The socialized economy was in opposition to the capitalist economy. It was modeled on the Soviet economy, in close connection with it and the economies of other Central and Eastern European countries, which were imposed on socialism and a “planned” economy. In that system, accounting was a tool of central planning, its purpose and addressees were different than in the market economy, and the informative function of financial statements was also different.

Poland has “always” used the continental (German) accounting model in its practice, preferring the valuation of assets and liabilities according to their historical cost. It was only in 1994, when the first Polish Act on Accounting was passed, that Poland started to implement the solutions contained in the Anglo-Saxon accounting model and apply international standards. Already the first version of the Act incorporated some solutions of this model and contained references to international standards.

At some point the establishment of accounting norms was the subject of the state intervention. In the European area this occurred directly in the legal form, in the English and American area stakeholders ordered directly the creation of professional standards. The European mode relied on political will, while the American one requires participation of all interested parties and legitimization that is broader than political will. That is why at the beginning of the 1970s the USA became home to the first board in the world i.e., Financial Accounting Standards Board (FASB) which represented interests of economic entities more fully and whose task was to establish financial accounting standards. The Board was also forced to solve the problem of its own legitimization on the intellectual platform and needed theory that would justify the content of standards and the way of establishing them. However, since accounting has never had a generally accepted scientific theory, the Board formulated it independently in the shape of a concept framework of financial accounting in the mid-1960s. It was then that the main focus shifted from measuring income to generating information for stakeholders who needed it to take economic decisions. This direction is still developing along with the process of globalizing world economies. In Polish one can read “The Concept Assumptions of Financial Accounting” formulated by IASB with its registered seat in London, which establishes financial accounting and reporting standards. Both Boards originate from English and American areas. Financial statements and corresponding measurement, structure and communication patterns, that is financial reporting standards, are the major products of the current stage of development of accounting (Nowak, 2010, pp. 15-20).

It must be remembered that in the searching for generally accepted principles of accounting in the USA there was a significant change and the major focus was shifted to searching conceptual assumptions as the theoretical foundation for standards that have become their major part. “Concept Assumptions”, as FASB document, was called the “constitution”, on which standards were to rely, while the choice of vocabulary emphasized the political essence of standards. However, the “Concept Assumptions” were not referred to financial accounting, but to financial reporting. The assumptions, contrary to expectations, did not become a generator in the process of developing standards, but their significance gradually decreased and they became only a source of concepts, preserving their political characteristics (Hendriksen and van Breda 2002, pp.138-148).

The recent study of The Routledge Companion (2015 ed. by S. Jones), devoted to the theory of financial accounting, draws attention to the fact that this theory finds many applications in the accounting practice of many entities and also has political implications. The authors of the new standards rely extensively on theoretical assumptions of accounting, and the regulatory bodies in corporations behave in a similar way when establishing regulations and evaluating existing accounting solutions in practice. The theory of accounting deals with formulating and analyzing rules on which the accounting practices rely and supporting them. In the USA these are Generally Accepted Accounting Principles – GAAP (Delaney et al, 2003). The IASB and the FASB have made some attempt to collaborate in the global financial reporting convergence process to align IAS / IFRS and US GAAP smoothly, and then align with other legal systems.

Changes in accounting and financial reporting regulations in Poland adjusting them to European and international solutions

Financial reporting is an integral part of accounting, since the financial reports are the final products of accounting. Accounting and financial reporting are subject to continuous changes as they try to adjust to the developing global economy as well as regional and national economies. The growing flow of goods, services, capital and people attributed to the progressing process of globalization – in the 1990s brought about a change in the purpose of companies’ activities and contributed to the increased demand for new information, necessary for management and investment purposes. Since then the top priority has been seen not in increasing short-term profits, but in increasing the value of the company in the long term, whereas financial and non-financial data included mainly in financial reports are used when making strategic decisions and checking their implementation, as well as when managing risk in an enterprise. They are also used by other stakeholders, primarily investors, when choosing an optimal way of allocating capital in selected investment ventures.

In 80. years of XX age the harmonization of financial reports has been greatly affected by the UE directives. These were: Directive IV from 25th July 1978 on principles of making, publishing and auditing annual financial reports, Directive VII from 13th July 1983 on principles of making, publishing and auditing consolidated financial reports, and Directive VIII from 10th April 1984 on professional qualifications of persons authorized to audit annual financial reports and requirements to be met by auditing companies in order to be able to audit annual financial reports. However, since Directives IV and VII, in spite of numerous modifications, did not help to achieve the desired state of comparability and transparency of financial reports, the European Commission implemented a new directive on accounting, aimed at decreasing administrative burden, mainly of small companies, and improving clarity (transparency) of financial reports. It is Directive of the European Parliament and of the Council of 26th June 2013 on the annual financial statements, consolidated financial statements and related reports of certain undertakings. This Directive amended the Directive of the European Parliament and of the Council 2006/43/EC and repealed the Directives of the Council 78/660/EEC and 83/349/EEC (OJ of EU 29.06.2013, item L182/19). In 2002, the European Parliament adopted Regulation No 1606/2002 on the application of International Accounting Standards in the European Union. The regulation included the order to use IAS/IFRS in making consolidated financial reports for issuers of securities allowed for public trade since 2005. Since January 2005 banks and capital groups operating in the EU, including those operating in Poland, are obliged to make annual financial reports in accordance with the IAS/ISFR. It should be emphasized that accounting in Europe, as in other regions of the world, has been shaped by various social, economic and political factors for centuries. These factors have marked significant differences deeply rooted in the practice of making financial reports. These factors include: various legal and tax systems, different perception of goals of financial reporting and various sources of financing economic activity (Bonham et al, 2006, p. 66).

Accounting in Poland, as mentioned, was based on the continental model and was subject to various legal regulations which covered all its issues, namely bookkeeping, cost accounting and financial reporting. As the Polish state underwent constitutional transformation, accounting was governed by new acts of law in order to adjust it to the free market economy conditions and the information needs of both external and internal users. The first of them was the regulation of the Minister of Finance from 15th January 1991 on principles of accounting, which normalized the accounting records and the new financial reporting, whereas in other issues (including mostly cost accounting) it referred interested parties to the principles developed by the accounting science and to accounting practice and customs (Regulation of the Minister of Finance, Journal of Laws No 10, item 35, § 3 point 6).

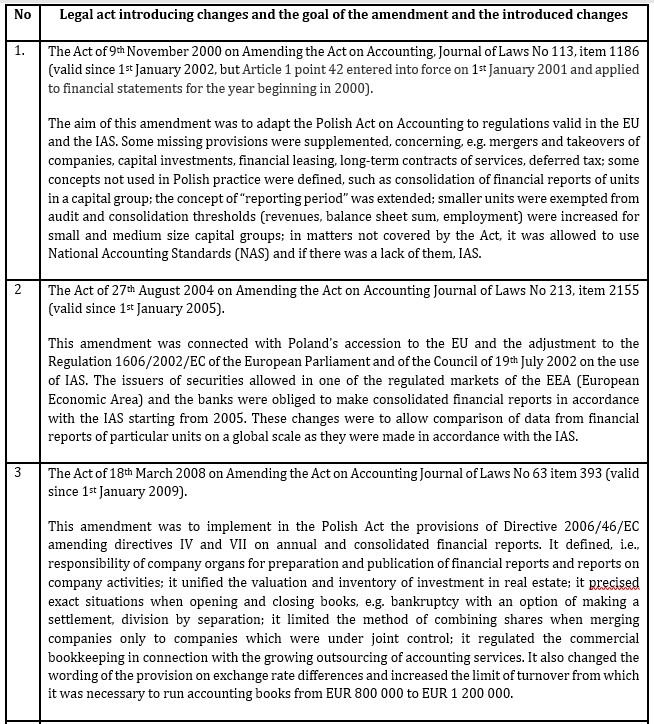

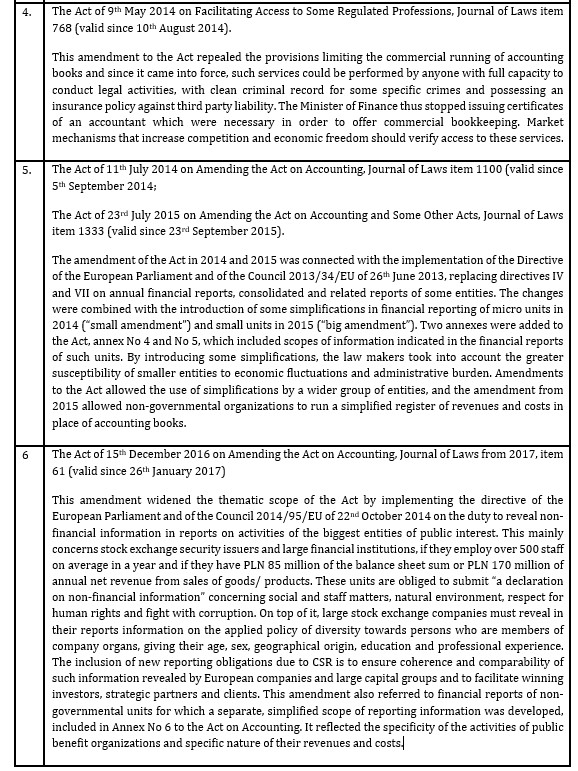

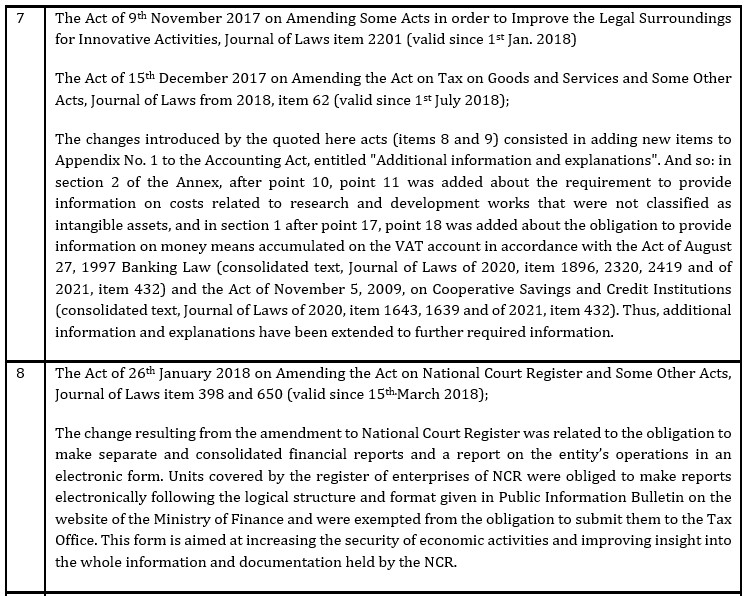

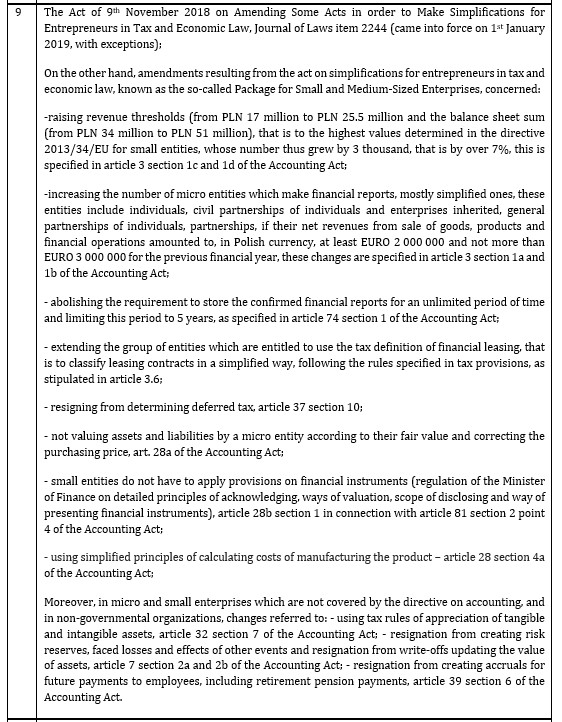

The key legal act, however, has been the Act on Accounting of 29th September 1994 (Journal of Laws No 121, item 591). The Act was passed when the legal order of the IV Directive of the Council of 25th July 1978 on annual reports (78/660/EEC) was implemented into the Polish law. The Act includes provisions concerning financial accounting and financial reporting (Article 4 section 3). The issue of costs, that is managerial accounting (in German-speaking countries known as controlling), however, was neglected and the provision on applying principles of the accounting science and its practice and customs in matters not regulated by the Act was not repeated, i.e., § 3 point 6 of the aforesaid regulation of the Minister of Finance. According to Sobańska and Walińska (2018, p. 155), this created „regulation and terminology confusion in the subject literature and in accounting practice”. The act which regulated accounting and financial reporting while ignoring managerial accounting was called “inadequate to the subject scope” (Sobańska, 2012, p. 179). The Accounting Act has been amended many times in order to adjust it to social, economic and legal changes and to the EU and IAS regulations. The harmonization of the Polish accounting law with the EU directives started 12 years before Poland’s accession to the EU. From the very beginning the Act combined provisions of the IV and VII Directives, while the European Commission did so only in 2013 (Dadacz 2018, p. 5-8). The Act also introduced some solutions from the international standards. The first significant amendment was introduced in the Act of 9th November 2000. It was so-called “big amendment”, which brought expended definitions, simplified inventory, changes to report templates and adjustment of accounting principles to the requirement of computer bookkeeping (Gnich, 2002, p. 14). This amendment of the Polish Accounting Act for the most part took into account the provisions of the International Accounting Standards containing solutions used in international practice. It also took into account the needs specific to the developing market economy, in particular with regard to the standardization of the content and scope of information presented in financial statements. New regulations were adopted on issues not regulated by the previous act. At that time, the following was introduced into the law: the principle of “substance over form” and “fair value” as a new parameter for the valuation of certain assets and liabilities, including goodwill and badwill. Detailed provisions of all changes to the Act on Accounting are presented in Table 1 below.

Table 1: Amendments to the Polish Act on Accounting, presented chronologically

Source: Author’s own elaboration.

Table 1 presents the most important amendments to the Polish Accounting Act so far, however, on November 25, 2020, the assumptions of a new draft amendment to the Accounting Act and certain other acts were published in the list of legislative and program works of the Council of Ministers. The amendments are envisaged in the draft Act on December 2020 which is currently being processed. The changes relate to the principles of preparing financial statements and reports on operations, as well as the principles of signing reports. The draft introduces new file formats for electronic financial statements and reports on operations (XHTML and XBRL) and allow signing of reports by only one member of the multi-person management board. In addition, it also provides for a number of changes for statutory auditors and audit firms. These changes correspond to the draft technical standards adopted by the European Commission Delegated Regulation 2019/815 of 17 December 2018. This regulation supplemented Directive 2004/109 / EC of the European Parliament and of the Council with regard to regulatory technical standards concerning the specification of a single electronic reporting format. The adopted standards are an act delegated by the directive, so after being adopted, they are directly applicable in all European Union countries. Under this Regulation 2019/815, issuers are required to prepare their annual financial reports (which also include financial statements) in XHTML format. Where this report will contain consolidated financial statements prepared in accordance with IAS, issuers are required to tag these statements using the Inline XBRL markup language (iXBRL). The XBRL technology has already been implemented in many countries around the world and the European Union has been interested in it for over 10 years. Currently in Poland pursuant to article 45 section 1f of the Accounting Act financial statements are prepared in electronic form and equipped with a qualified electronic signature, a trusted signature or a personal signature. Moreover, according to article 45 section 1g of the Accounting Act entities entered in the register of entrepreneurs of the National Court Register prepare financial statements in a logical structure and format made available in the Public Information Bulletin on the website of the Ministry of Finance [in XML format (Extensible Markup Language)]. On the other hand, according to article 45 section 1h of the Accounting Act financial statements prepared in accordance with IAS are prepared in a logical structure and format, if they are made available in the Public Information Bulletin on the website of the Ministry of Finance – this means that currently these statements can be prepared in any electronic format, e.g., PDF. The new draft is justified by the argument that keeping the current wording of the Accounting Act, while the provisions of Regulation (EU) 2019/815 are in force, would result in the need to use different formats for the same financial statements. This solution was supported by the European Parliament already in 2008 (Resolution 2007/2254 (INI)). The European Commission has also endorsed XBRL. The obligation to prepare financial statements and submit them to supervisory authorities in a standardized format for companies listed on the regulated markets of the European Union is regulated by Directive 2013/50 / EU of the European Parliament and of the Council. It obliged issuers to prepare annual reports in a single electronic reporting format (ESEF – European Single Electronic Format). ESMA (European Securities and Markets Authority) has been required to develop draft regulatory standards to define an electronic reporting format. ESMA is an independent body of the European Union that aims to improve investor protection and promote stable and efficient financial markets (ESMA, 2020a). ESMA proposed several solutions, including the XBRL technology. The proposed amendment is to adapt the currently applicable provisions on financial reporting and auditing to the current legal and economic situation and to technological possibilities. The dynamic development of digital technologies, which we are currently dealing with, has a significant impact also on accounting and auditing. The possibility of using modern IT tools and digital technologies makes it easier for entities applying the Accounting Act to fulfill their obligations in the field of bookkeeping, preparation of financial statements or remote controls in audit firms. On the other hand, users of these reports can quickly download, analyze and interpret the data they need. The digital transformation of economic life was accelerated by the pandemic caused by the spread of the SARS-CoV-2. Annual reports in the uniform European reporting format (ESEF) were to be prepared for the financial years beginning on or after 1 January 2020. However, in connection with Covid 19, this obligation was postponed by Regulation 2021/337 of February 16, 2021. The decision on this matter rests with the Member States.

Polish accounting regulations have been linked to the content of IAS / IFRS and EU Directives by introducing standards and regulations to the Accounting Act. This content was usually simplified to facilitate the work and make it easier to perform. At the same time, the Act contains an important provision, namely that in matters not regulated by the provisions of this Act, and provided that the accounting principles (policy) are applied, entities may apply National Accounting Standards issued by the Accounting Standards Committee. In the absence of a relevant national standard, entities may apply IAS / IFRS, except for entities for which these standards are law. So far, the National Accounting Standards have been issued as outlined below. 1. Cash flow statement, 2. Income tax, 3. Unfinished construction services, 4. Impairment of assets, 5. Leasing, rental, lease, 6. Provisions, passive cost accruals, temporary liabilities, 7. Changes to the rules (policy) accounting, estimated values, correcting errors, events after the balance sheet date – recognition and presentation, 8. Development activities, 9. Report on activities, 10. Public-private partnership agreements and concession contracts for construction works or services, 11. Fixed assets, 12. Agricultural activity, 13. Manufacturing cost as the basis for product valuation. National Accounting Standards are to facilitate the application of accounting principles by entities by making them more precise and providing interpretations helpful in the practical implementation of regulations. Entities operating in Poland, for which international standards are law, obligatorily apply all these standards, without exception, together with the interpretations issued for them. Other entities apply only those regulations that were included in the Accounting Act. IAS / IFRS are the leading accounting standards adapted to economic changes in the world, while national regulations are usually traditional. However, the Polish Accounting Act is changing dynamically, introducing immediately the appropriate solutions contained in subsequent international standards and EU directives.

Conclusions

In the period of 25 years which passed since the passing of the first text of the Polish Accounting Act, many significant amendments have been introduced to it. All these changes resulted from the need to adjust the Polish Act of Accounting to the global and European tendencies in accounting, elevated as “the language of business”: in international economic relations. These tendencies reflect the processes of standardizing this language on a global scale and harmonizing and standardizing financial reports as the basic carrier of financial information. Every change in newly-implemented solutions in theory, practice and policy of accounting, exerts some influence on the financial reporting of entities, constituting the final product and an integral part of accounting. Referring to the purpose of the article, it can be stated that a detailed study of frequent changes to the Polish Accounting Act over the last 30 years of the political and economic transformation in Poland shows that the act is being gradually and immediately adapted to the IAS / IFRS international standards and directives of the European Union. It can also be hoped that the article filled the gap in the literature on the subject in terms of a synthetic and comprehensive presentation of the changes introduced in the Polish Accounting Act in order to adjust it to the EU Directives and the MRS / IFRS standards. The research hypothesis as to whether the changes to the Polish Accounting Act are implemented frequently, regularly and adequately, to the changes introduced in EU directives and in international accounting and financial reporting standards has been positively verified. That explains why Poland belongs to a group of countries which update their national provisions on accounting in accordance with arrangements and norms promoted and adopted in the world. Thanks to the updates, the Polish Act on Accounting includes modern trends in decisions concerning accounting and does not lag behind the world solutions in this field. On the other hand, this act reflects the specificity of the Polish economy and its further development prospects. The implemented provisions are deeply analyzed by numerous Polish theoreticians and practitioners in order to ensure their best adjustment to the reality of the economic life in Poland.

Foot Notes

XHTML (Extensible Hypertext Markup Language), an extensible hypertext markup language, does not require separate mechanisms to be presented in a human-readable format – XHTML reports can be opened and viewed using a standard web browser. As it is not proprietary, it can be used freely.

XBRL (Extensible Business Reporting Language) is a markup language used to describe (mark) data sets in such a way that they can be processed automatically (Regulation 2019/815).

Inline XBRL (iXBRL for short) is a technology that provides embedding of XBRL tags in HTML / XHTML documents. It combines the advantages of data tagging in XBRL and the advantages of presenting a report in a human-readable format (ESMA, 2019).

Ministry of finance

However, on the website of RP is a note: “Ministry of Finance informs that the logical structures and the format of financial statements prepared in accordance with IAS will not be published in the Public Information Bulletin of the Ministry of Finance” https://www.gov.pl/web/kas/struktury-e-sprawozdan [Date of access 2021-07-19]

References

Act on Accounting of September 29, 1994, Journal of Laws No 121, item 591; consolidated text Journal of Laws of 2021, item 217.

Alexander, D., Nobes, Ch., (2010), Financial Accounting. An International Introduction, Pearson Education Limited, England.

Bonham, M. et al., (2006), Międzynarodowe Standardy Sprawozdawczości Finansowej w interpretacjach i przykładach, Wydawnictwo Prawnicze LexisNexis, Warszawa.

Commission Delegated Regulation (EU) 2019/815 of 17 December 2018 supplementing Directive 2004/109 / EC of the European Parliament and of the Council with regard to regulatory technical standards concerning the specification of a single electronic reporting format, OJ L 143, 29.5.2019.

Dadacz, J. (2018), Polskie przepisy o rachunkowości po transformacji – historia, stan obecny, kierunki rozwoju, „Rachunkowość” 11/2018, SKwP, Warszawa.

Delaney, P. R., Epstein, B. J., Nash, R., Weiss Budak S., (2003) Wiley GAAP 2003 Interpretation and Application of Generally Accepted Accounting Principles 2003, John Wiley & Sons, Inc., Hoboken, New Jersey, USA.

Directive 2013/50 / EU of the European Parliament and of the Council of 22 October 2013 amending Directive 2004/109 / EC of the European Parliament and of the Council on the harmonization of transparency requirements in relation to information about issuers whose securities are admitted to trading on a regulated market, 2003/71 / EC of the European Parliament and of the Council on the prospectus published in connection with the public offering or admission to trading of securities and Commission Directive 2007/14 / EC laying down detailed rules for the implementation of certain provisions of Directive 2004/109 / EC, Journal L 294 of 6 November 2013.

European Parliament Resolution of 21 May 2008 on a simplified business environment for enterprises in the fields of company law, accounting and auditing (2007/2254 (INI)).

ESMA (2020a), https://www.esma.europa.eu/about-esma/esma-in-brief, accessed March 18, 2021.

Gnich, J. (2002), Komentarz do znowelizowanej ustawy o rachunkowości. Poradnik dla małych i średnich przedsiębiorstw, Polska Agencja Rozwoju Przedsiębiorczości, Warszawa.

Hendriksen, E.A., van Breda, M.F. (2002), Teoria rachunkowości, Wyd. Naukowe PWN, Warszawa.

Międzynarodowe regulacje rachunkowości. Wpływ na rozwiązania krajowe, (2002), pod red. A. Jarugi, Wydawnictwo C.H. BECK, Warszawa.

IAS 1 Presentation of financial statements [in:] International Financial Reporting Standards (2016), SKwP, IFRS, Warszawa.

Nowak, W. A. (2010), Teoria sprawozdawczości finansowej. Perspektywa standardów rachunkowości, Oficyna a Wolters Kluwer business, Warszawa.

Olchowicz, I., Tłaczała, A. (2015), Sprawozdawczość finansowa według krajowych i międzynarodowych standardów, wydanie III zmienione i rozszerzone, Difin, Warszawa.

Regulation (EU) 2021/337 of the European Parliament and of the Council of 16 February 2021 amending Directive 2004/109 / EC as regards a single electronic reporting format for annual financial reports to support recovery after the COVID-19 crisis, Journal Laws L 68 of January 26, 2021.

Sobańska, I., Walińska, E., (2018) Przyczynek do postrzegania struktury współczesnego systemu rachunkowości, ‘Zeszyty Teoretyczne Rachunkowości’ tom 96 (152), SKwP, Warszawa.