Faculty of Economics & Business Administration, West University of Timisoara, Timișoara, Romania

Volume 2023,

Article ID 153211,

Journal of Accounting and Auditing: Research & Practice,

20 pages,

DOI: https://doi.org/10.5171/2023.153211

Received date: 23 May 2023; Accepted date: 22 September 2023; Published date: 12 October 2023

Academic Editor: Maria Moraru

Cite this Article as:

Andrei-Marius OLARIU (2023), " Audit Challenges amidst COVID-19 and Evolving Auditor Reporting Trends in Romania: A Comprehensive Analysis and Research Prospects", Journal of Accounting and Auditing: Research & Practice, Vol. 2023 (2023), Article ID 153211, https://doi.org/10.5171/2023.153211

This research paper sets out to examine the auditing in the unprecedented era of the COVID-19 pandemic. It systematically investigates the prevailing trends in auditor reporting for companies that are listed on the Bucharest Stock Exchange, focusing on the critical period from 2018 to 2021. The main objective of this paper revolves around the synthesis of the existing literature that relates to audit reporting. It takes a magnifying lens to the specter of uncertainty and the associated risks related to the “going concern” status of Romanian companies that find themselves ensconced within the realm of the Bucharest Stock Exchange. It also presents a brief overview of the array of audit opinions that were disseminated to Romanian firms listed on the stock exchange during the defined timeframe. The rationale behind choosing the 2018-2021 period is rooted in the historical evidence that suggests significant fluctuations and changes in audit practices. The years 2018 to 2021 were characterized by persistent economic uncertainty in the Romanian landscape, reflecting to some extent the conditions witnessed during the 2007 crisis, largely propelled by the far-reaching and profound impacts of the COVID-19 pandemic. In essence, this research highlights the imperative need for further in-depth exploration into the substantive content and the practical utility of the enhanced auditor’s reports. The shadow cast by global events, such as the COVID-19 pandemic, further accentuates the urgency of this endeavor, which should serve as a rallying point for both researchers and practitioners within the field of auditing.

The role of the audit of the financial statements finds its correspondent in providing a reasonable assurance about the credibility of financial reporting and the information presented in it.

In this context, a very important aspect regarding the development of the audit profession is the one related to the consolidation of the credibility offered by the auditor.

The duty of the financial auditor is to provide his personal judgment regarding the financial statements’ compliance with the financial reporting framework in order to ensure the quality of the financial information released by the listed firms (Deliu, 2013). This opinion must be developed by the auditor while taking into account the specific requirements of competence, judgment, professionalism, and ethics – in order to be considered a reliable one.

The trend of audit opinions at the national and international level is a subject that is constantly analyzed in order to produce statistics and forecasts for the following periods.

This study is based on a sample of audit opinions of the companies listed on the Bucharest Stock Exchange, for the period 2018-2021. The main scope of the study is to investigate the frequency of auditors’ rotations. From one point of view, the period 2018-2021 was chosen because this included a major global event (the COVID-19 pandemic), which could have had a significant impact on the financial statements and audit engagements of many companies (Deliu, 2020b).

In addition, from another point of view, studying the frequency of auditors’ rotations in Romania can provide valuable insights into the state of the country’s accounting and auditing practices, and the financial health of Romanian companies, due to the fact that Romania is considered to be an emergent market (Deliu, 2019; Deliu, 2020a).

Numerous businesses in such developing markets as Romania are affiliated with a worldwide group and, as a result, their consolidated financial statements are included in the financial statements published by the entire company. Therefore, it can be said that the Big 4/Non-Big 4 dichotomy is insufficient for the purposes of this study.

All of the Big 4 corporations and a few more businesses affiliated with international networks of accounting firms may be found in Romania on the audit market. There are also a lot of regional audit firms that are not a part of any global network. Joint audits are not yet required. Beginning in 2012, the regulation required practically all listed companies (on the Bucharest Stock Exchange) to adopt IFRS. Previously, they were expected to report in accordance with Romanian GAAP and only submit IFRS financial statements if they were presenting consolidated financial statements or for the purposes of investors. Berinde (2013) split Romanian auditors into three categories (Big 4, Non Big 4, and individuals), and discovered that Big Four auditors will see an ascending trend in terms of market share compared to local audit firms. Grosanu & Berinde (2013) discovered that the Big 4 firms only covered 18% of the entities in their sample for a number of significant companies from North-West Romania. They also identified a few elements that they believe strongly influence why audited companies request the Big 4 auditors, including investors (domestic or foreign) and managers’ need for confidence.

Hence, some potential benefits of studying audit opinions in Romania include:

Understanding the quality of financial reporting: Studying audit opinions can provide insight into the quality of financial reporting in Romania, including any areas of improvement that may be needed.

Evaluating the effectiveness of auditing: Audit opinions can be used to evaluate the effectiveness of auditing practices in Romania and to identify any areas that may need improvement.

Monitoring the financial health of companies: Audit opinions can provide insight into the financial health of companies in Romania, including any potential risks or challenges that they may face.

Identifying regulatory trends: Studying audit opinions can help to identify regulatory trends in Romania, including any changes to accounting standards or audit requirements that may impact the financial statements of companies in the country.

Improving transparency and accountability: By providing information on the financial health of companies, audit opinions can improve transparency and accountability in Romania’s financial markets.

Henceforth, the main objectives of this study include:

OB1: Identifying the trends in the issuance of unqualified vs. qualified audit opinions over time.

OB2: Evaluating the role of auditors in providing assurance on the accuracy and reliability of financial reporting.

OB3: Comparing the trends of audit opinions across different industries or countries, to identify any differences or similarities in the financial reporting practices of these groups.

The paper is structured as follows: the Introduction sets the scene as regards the current market context that prompted the research theme, while the Literature Review presents the theoretical background in reference to studies focusing on audit reporting of going-concern uncertainty. The Materials and Methods section, respectively the Results section will further assess findings, while the Discussions and Conclusions and Future Directions sections will deep-dive into comparing the results with existing research and drawing relevant conclusions and practical implications of the study.

Literature Review

Currently, the global economy is in a continuous process of change, being still drastically affected by the effects of the COVID-19 pandemic. A very important element for increasing confidence regarding the quality of the information presented in the financial statements is the audit.

Following the work performed by the auditor based on the collection of audit evidence, an audit opinion is issued as mentioned in the independent auditor’s report (ISA 700).

There is a considerable increase in terms of interest in the form and content of audit reports, based on the investors’ reaction to the financial scandals and the pandemic context of recent years, thus justifying the increase in investors’ interest in the audit report (Felix et al., 1982; Wines, 1994; Wu et al., 2006; Carey et al., 2008; Monroe & Hossain, 2013; Barnes et al., 2018; Fulop, 2018; Hirst et al, 2018; Lu, 2020; Dionisijev, 2021; Purnama, 2021; Hidayat, 2022).

According to the International Standards on Auditing (ISA), the audit report is assigned a triple role, as follows: (i) Communication tool with users of financial statements in order to justify decisions; (ii) Tool for increasing user confidence in financial statements; respectively (iii) Tool for identifying the responsibilities of auditors and company management.

The opinion issued by the independent auditor presents in a synthesized form his conclusion regarding the fact that the financial statements prepared by the client comply with the financial reporting standards (Bunget et al., 2022). Thus, the opinion can be significantly influenced by the quality of the audit performed, as it is necessary to fulfill the principles of professional competence and due care. Within this frame of reference, the auditor’s competence must be maintained throughout the audit mission to be able to issue a pertinent audit opinion based on the audit evidence collected (Purnama, 2021), while also maintaining independence and objectivity (Hidayat, 2022).

Hategan et al. (2018) analyzed the companies listed on the Bucharest Stock Exchange regarding the subsequent events that take place before or after the date of the audit report, since these can have negative effects on the audit opinion and, thus, lead to an unfavorable audit opinion, taking into account the fact that these events lead to the adjustment of the annual financial statements.

On the same note, Barnes et al. (2018) considered the fact that in recent years Non-Big 4 auditors have placed a great emphasis on performing audits with superior quality in order to attract new clients and retain the loyalty of existing clients in exchange for what the big Big4 auditors have lost quite a lot of reputation.

In this vein, Fulop (2018) considers the fact that when a different opinion is issued compared to the unmodified one, the independent auditor is obliged to present a paragraph in the audit report based on which to provide additional explanations regarding the issued audit opinion.

Consequently, there are several factors that can influence the audit opinion issued by an auditor from one year to another. Some of the factors that may cause the audit opinion to change include (Hosseinniakani, 2014):

Changes in the financial position or performance of the organization being audited: If the organization experiences significant changes in its financial position or performance, this could affect the audit opinion.

Changes in the accounting policies or practices of the organization: If the organization changes its accounting policies or practices, this could also affect the audit opinion.

Changes in the relevant financial reporting framework: If there are changes to the financial reporting framework that the organization is required to follow, this could affect the audit opinion.

Changes in the auditing firm: If the organization changes auditing firms, this could also affect the audit opinion.

It’s important to note that audit opinions are based on the information and documentation available to the auditors at the time the audit is performed. As a result, the audit opinion may change from one year to another if there are significant changes in the organization or in the audit process.

Stakeholders, such as shareholders, creditors, and regulatory bodies, may view changes in the audit opinion from one year to another as a potential indication of changes in the financial position or performance of the organization being audited.

There are several types of audit opinions that an auditor may issue, including an unmodified opinion, a qualified opinion, an adverse opinion, and a disclaimer of opinion (ISA 700). A change in the audit opinion from one year to another may be viewed as a red flag by stakeholders if it indicates a decline in the financial health or reliability of the organization (Kuruppu et al., 2012; Tian, 2017; Hategan et al. 2018; Adhikari et al, 2019; Bunget et al., 2022; Lu, 2020; MohammadRezaei et al., 2021; Hu et al., 2022).

On the one hand, if the audit opinion changes from an unmodified opinion to a qualified opinion or an adverse opinion, this may be viewed as a negative development by stakeholders, as it indicates that the financial statements may not present a true and fair view of the organization’s financial position.

On the other hand, if the audit opinion changes from a qualified opinion or an adverse opinion to an unmodified opinion, this may be viewed as a positive development by stakeholders, as it indicates that the financial statements are considered to present a true and fair view of the organization’s financial position.

It’s important to note that changes in the audit opinion do not necessarily reflect negatively on the organization being audited. In some cases, changes in the audit opinion may simply reflect changes in the audit process or in the relevant financial reporting framework.

Renewing interest in the auditor’s assessment and reporting on a business’s capacity to continue as a going concern has been sparked by company failures, financial crises, and the coronavirus epidemic.

In response to the COVID-19 crisis, auditors have had to adapt their operations and procedures to maintain the integrity of the auditing process while also ensuring the health and safety of all involved parties. This has resulted in a shift towards remote working and digitalization of many aspects of the audit process. For example, auditors are conducting more virtual meetings with clients and other stakeholders, and relying on technology to review and analyze financial information. Some auditors are also using data analytics tools to identify potential areas of risk and fraud.

In addition, auditors have had to consider the impact of COVID-19 on their clients’ financial statements. This may involve assessing the reasonableness of estimates and assumptions used in financial reporting, and evaluating the potential impact of pandemic-related disruptions on future financial performance.

Overall, auditors are adapting to the challenges posed by COVID-19 by leveraging technology and innovative approaches to ensure the integrity of the auditing process while also protecting the health and safety of all involved parties.

In the context of the COVID-19 pandemic, auditors should pay close attention to the issue of going concern when evaluating their clients’ financial statements. The going concern principle is the assumption that a business will continue to operate into the future, and the ability of a company to continue as a going concern is a key factor in the preparation of financial statements.

The COVID-19 pandemic has caused significant disruptions to the global economy, leading to financial difficulties for many businesses. As a result, auditors should assess the impact of the pandemic on their clients’ ability to continue as a going concern and evaluate the management’s plans for addressing any related risks.

This may involve reviewing the company’s financial projections and considering factors such as its liquidity, the availability of financing, the level of government support, and the general economic outlook. Auditors may also need to consider the impact of the pandemic on the company’s industry and the potential for long-term changes to the business environment.

If auditors have concerns about the company’s ability to continue as a going concern, they may need to issue a qualified opinion or a disclaimer of opinion in the financial statements. In some cases, auditors may also need to make recommendations for steps that the company should take to improve its prospects for survival.

Overall, in the context of the COVID-19 pandemic, auditors must remain vigilant and proactive in assessing the going concern of their clients and ensuring that financial statements accurately reflect the risks and uncertainties associated with the pandemic.

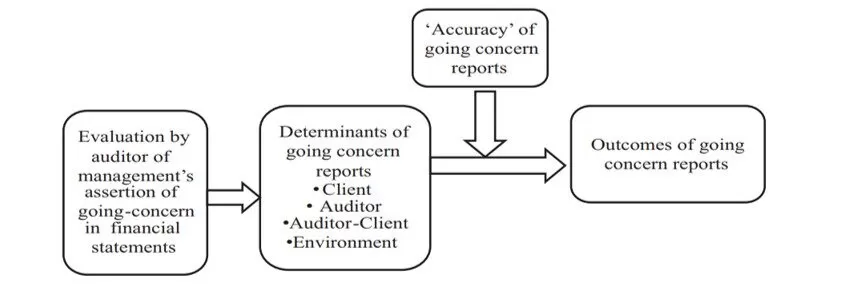

Researchers in accounting have long analyzed auditors’ reports. The analysis of reports adjusted for going-concern risks has received a lot of attention. As illustrated in Figure 1, I structure the analysis of the research around the conceptual framework put forth by Carson et al. (2013).

This framework organizes research into the auditors’ assessment of management’s going-concern assertion, factors influencing going-concern reports, the accuracy of going-concern reports, and the outcomes. Romanian evidence is somewhat scant compared to the larger body of largely US evidence (Carson et al., 2013), as will be explored below.

Figure 1. Audit reporting of going-concern uncertainty research framework

Source: Carson et al., 2013

Evaluation of management’s assertion regarding the going concern

1.1. Models for predicting failure

Even if a report from an auditor that includes commentary on going-concern issues is not a forecast of a company’s failure, knowledge of the likelihood of a company’s failure is important for people making decisions about going-concern uncertainties. Both the importance of fundamental concepts and the development of extremely sophisticated approaches for modeling default risk have been highlighted by research on failure prediction models. The factors used to predict company failure include: cash position, operating cash flow (both reported and estimated), working capital, profitability and earnings performance, turnover, financial structure, debt servicing capacity, industry determinants, and the valuation of intangibles (Wu et al., 2006; Jones, 2011). According to Kuruppu et al., 2012, auditors believe these models are helpful for gathering pertinent evidence, reducing some of the subjectivity involved in determining whether a business is still in operation, and fostering agreement on the auditor’s judgment. However, more practitioner-academic collaboration is required to do research that enhances the criteria currently utilized in practice to evaluate the possibility of firm collapse in the context of going concern.

1.2. Auditor decision process

Experimental research methodologies are applicable to the decision-making process utilized by auditors to issue going-concern opinions. Sometimes the choice of information made by auditors limits their ability to make sound judgments (Simnett & Trotman, 1989). Concurrently, in comparison to less experienced auditors, more experienced auditors may retain more unusual information, are more likely to reach valid findings, and make prognosticatory assessments. (Choo & Trotman, 1991).

However, most studies looking at auditor judgments have not given the going concern setting enough consideration. Experimental and survey methodologies, in addition to archival studies on going concern issuance, can offer valuable understanding, particularly on the information processing and decision-making processes of auditors. In circumstances where the “black box” of the auditor’s decision-making process cannot be seen through archival observation, experimental and survey procedures can be very helpful. In light of recent study findings in adjacent fields including auditor skepticism, client advocacy, and presumptive doubt, there are prospects for taking auditor judgment as regards going-concern uncertainties into consideration.

Determinants of going concern reports

2.1. Defining uncertainty modified reports

Using a sample from the years 1984 to 1988, Simnett and Trotman (1989), Choo and Trotman (1991) present a model to forecast “subject to” attitudes based on financial statement and market data in a widely recognized work. More recent models concentrate on forecasting changes for uncertainty in going concerns. Explanatory factors are taken into account by Carey & Simnett (2006) and Hossain (2013). These factors include prior year non-standard reports, profitability as measured by ROA, incidence of losses, cash from operations, financial risk as measured by leverage, and default risk as captured by summary measures like Altman’s Z-score or Zmijewski’s bankruptcy score. There are still opportunities to analyze issues surrounding going-concern reports in the Romanian context, such as their initial issuance and removal, as well as industry-specific uncertainties.

2.2. Auditors’ response to crises

Investors, regulators, standard-setters, and others are becoming more interested in the auditor’s evaluation and reporting on a firm’s capacity to continue as a going concern as a result of company failures and financial crises. Following firm failures, auditors are expected to respond to increased regulatory inspection, more public scrutiny, increased litigation against auditors, and higher insurance costs (Fargher & Jiang 2008; Deliu, 2013). Auditors were more likely to give going concern amendments right after the high-profile company failures that occurred between 2000 and 2002 (Carey et al., 2012) and after the Great Financial Crisis around 2007 (Xu et al., 2013; Deliu, 2013; Dionisijev, 2021). There will be business failures and financial crises, which will spark interest in the reporting decisions made by the auditors before to the collapse or crisis. The difficulty in this area of research is to more clearly distinguish between how events affect clients’ underlying risk and how events affect auditors’ reporting judgments.

2.3. Independence issues

The problem of auditor independence is significant to standard-setters and regulators and has frequently come up in studies. The likelihood of receiving a going-concern report may be associated with non-audit services or even audit fees, which may at least suggest a perception of a problem with auditor independence. The degree of other services and the type of auditor’s report were not significantly correlated, according to earlier studies by Craswell (1999), and Craswell et al. (2002). Aitken & Simnett (1991) and Wines (1994) discovered that, in contrast to corporations that received some sort of audit certification, auditors of companies that didn’t receive one received a considerably higher proportion of their compensation from non-audit activities.

According to some studies performed on samples of bankrupt companies, a lower likelihood of giving a going concern opinion is connected with a higher proportion of non-audit services fees to total fees (Fargher and Jiang 2008). Concurrently, Berinde & Groúanu, 2013, discovered some evidence sustaining that non-audit services are related to audit reporting. By looking at a more holistic perspective of auditor-client relations, other research revisits the topic of auditor independence and the likelihood to offer a going concern opinion.

Long-term audit partner tenure tends to undermine auditor independence, according to other studies. Carey & Simnett (2006), using data from a 1995 sample, discovered a marginally positive association between partner tenure of less than two years and the propensity to issue a going concern opinion, but a significant negative association between audit partner tenure over seven years and the propensity to issue a going-concern opinion. Similar findings were made by Ye et al. (2011) who discovered that alumni affiliation, long audit engagement partner tenure, and the combined effect of auditor-provided nonaudit services have a negative impact on the auditor’s tendency to offer a going-concern opinion.

In contrast, Monroe & Hossain (2013) discover a substantial positive correlation between the likelihood of granting a going-concern opinion to a financially troubled company and the tenure of audit partners of five years or more. Overall, the findings point to a possible reduction in auditor independence, at least on the surface, due to a decreased likelihood of issuing a going-concern opinion when auditors do non-audit services or have a long tenure.

Additionally, there is no proof that it affects mental independence (Berinde & Groúanu, 2013). Standard-setters and regulators are constantly interested in the topic of auditor independence and how it affects audit quality. The majority of the recent research has been on the effects of fee dependency and audit tenure on the likelihood of issuing a going-concern opinion. For a deeper understanding of the linkages between the auditor-client relationship and the choice to issue or refrain from issuing a going-concern opinion, more research is required. Other dangers to the independence of the auditor in the context of going concern may be taken into account in future studies.

“Accuracy” of going-concern reports

3.1.

The auditor’s report is an important document that provides assurance to stakeholders about the reliability of a company’s financial statements. While an auditor’s report is not meant to predict the failure of a company, the public and regulators become concerned when a company fails shortly after receiving an unmodified audit opinion for going-concern uncertainty. In Australasia, studies of auditors’ reports have focused primarily on Type 1 misclassifications, where a company continues to operate despite an auditor’s report modified for going concern. The survival rate following a modified auditor’s report for going-concern uncertainty is high in Australia, suggesting a high level of Type 1 misclassification (Xu et al., 2011; Berinde & Groúanu, 2013; Xu et al., 2013; Hosseinniakani, 2014, Tian, 2017, Velury et al., 2020). This may be due to the nature of many entities, such as mining exploration companies that require future financing to continue as a going concern. Few studies have examined this issue, but research suggests that the accuracy of auditor reporting has remained similar over time.

3.2.

To help with standard creation and regulation in these areas, more thorough case studies and industry analysis are essential. By doing so, stakeholders and regulators can gain insights into the factors that contribute to corporate failures and how auditors’ reports can provide more accurate information to help prevent such failures. Ultimately, improving the accuracy and reliability of auditors’ reports is vital to maintain the trust and confidence of stakeholders in the financial reporting process (Chen et al, 2020; Kim et al., 2021; Hu et al., 2022).

Materials and Methods

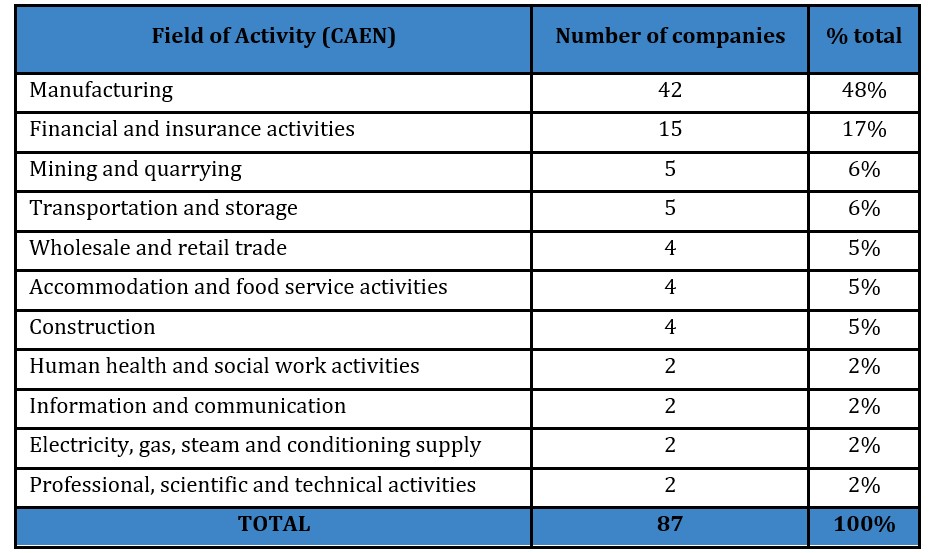

First, I identified the statistical population of the sample represented by the companies listed on the stock market of the Bucharest Stock Exchange, in the period 2018-2021. Thus, the structure by fields of activity of the sample of companies is presented in Table no. 1 and Figure no.

Table 1. Companies’ structures by fields of activity

Source: Author’s own projection

Figure 2. Companies’ structures by fields of activity

Source: Author’s own projection

Following the analysis of the structures of the companies by fields of activity, the significant share of the companies in the manufacturing industry and of the financial and insurance companies can be observed, representing a percentage of 65% of the total analyzed sample.

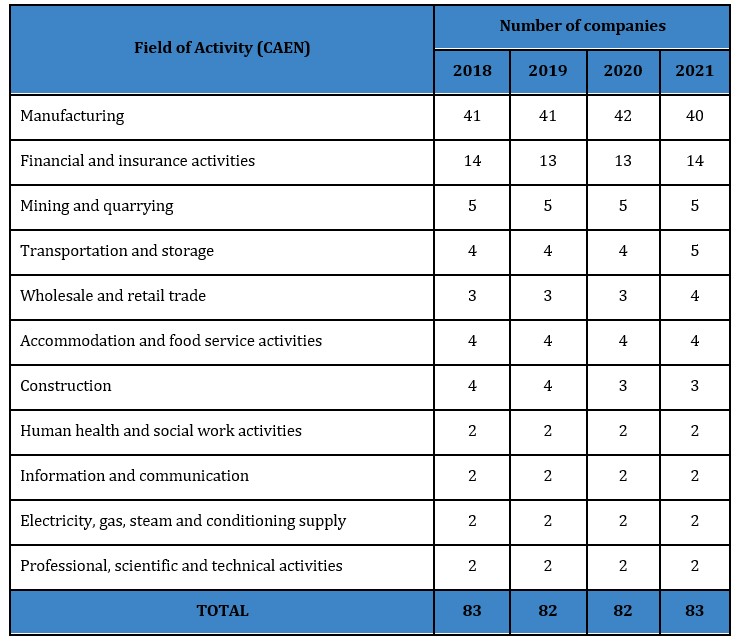

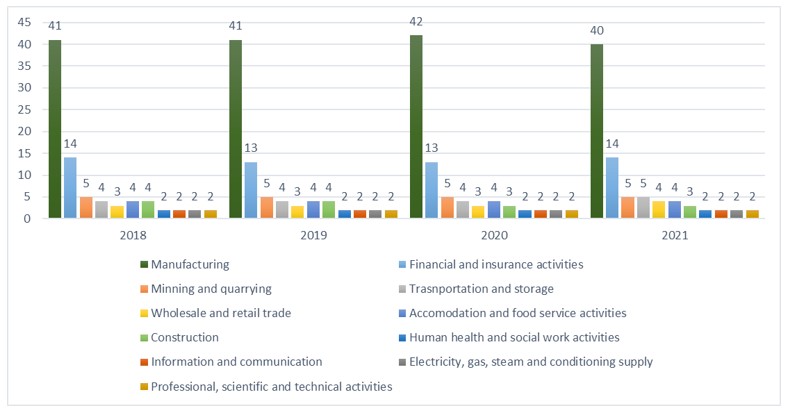

For a more detailed analysis of the companies by fields of activity, their structuring was performed for each verified year, as presented in Table no. 2 and Figure no. 3.

Table 2. Annual structure of companies by fields of activity

Source: Author’s own projection

Figure 3. Annual structure of companies by fields of activity

Source: Author’s own projection

Over the whole period analyzed, the companies in the manufacturing industry represented the largest share of the sample, the annual structure being relatively constant. Thus, I considered this field of activity as the most relevant to analyze in order to formulate a conclusion of the study.

Even if there were certain fluctuations of the companies listed on the stock market of the Bucharest Stock Exchange, I can say that they are minor, being made mainly based on the opening of the insolvency procedure.

Results

The independent, impartial, and expert opinion provided by a financial auditor ensures that financial information complies with the required accounting reporting structure (Carey et al., 2008). According to ISA – International Standards on Auditing, the audit opinion is the most significant element of the audit report. By including some elements related to the reporting quality, the assumption of ongoing concern, the presence of the fraud risk, and even sustainable development, the report issued by an auditor helps to improve the transparency and relevance of the information from financial statements (Turner & Grey, 2010).

One of the main objectives established was to identify the types of audit opinions issued to the companies listed on the stock market of the Bucharest Stock Exchange, in the period 2018-2021. The aim was to identify the number of audit opinions (unqualified opinion, qualified opinion, adverse opinion, disclaimer of opinion) issued for each company, for the period 2018-2021, then analysed specifically for each field of activity.

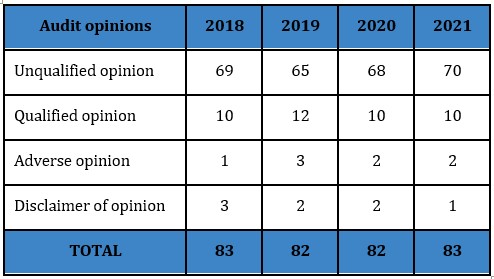

Thus, the situation of the annual audit opinions is presented in Table no. 3 and Figure no. 4.

Table 3. Annual structure of audit opinions

Source: Author’s own projection

Figure 4. Annual structure of audit opinions

Source: Author’s own projection

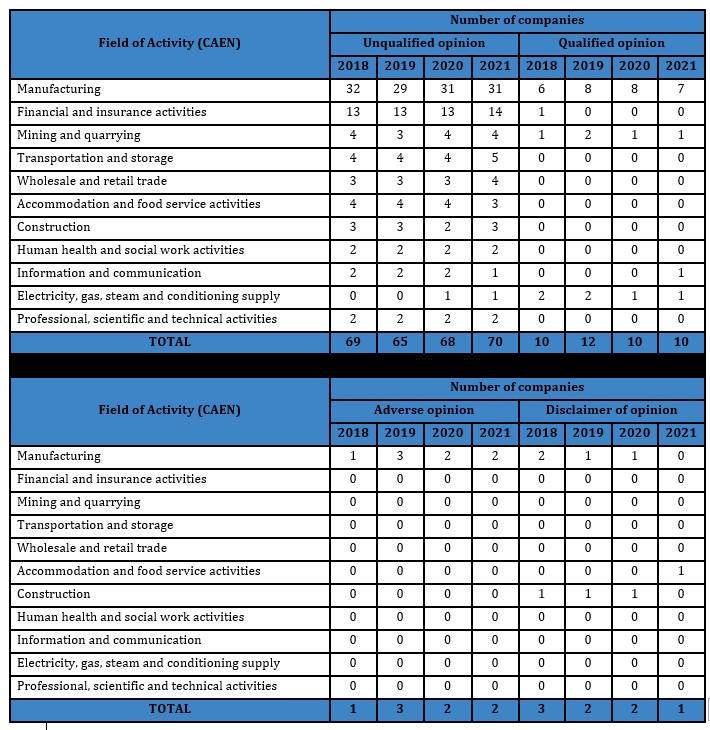

However, I considered it appropriate to analyze the audit opinions for each field of activity, in order to ascertain whether the significance would remain the same as the initial one, the results being presented in Table no. 4.

Table 4. Annual structure of audit opinions by fields of activity

Source: Author’s own projection

It can be identified that the most significant share of qualified opinions is also allocated to the manufacturing industry, holding a minimum percentage of 44.61% of the total opinions of this type, during 2019, respectively a maximum percentage of 46.37% during 2018.

As for the unqualified opinions, it is predominantly found in the manufacturing industry, reaching 80% of the total of this type of opinion during the 2020.

The number of adverse opinions and the disclaimer of opinions is very low, being encountered almost entirely in the manufacturing industry.

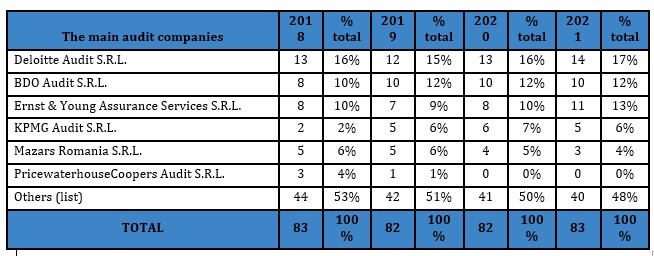

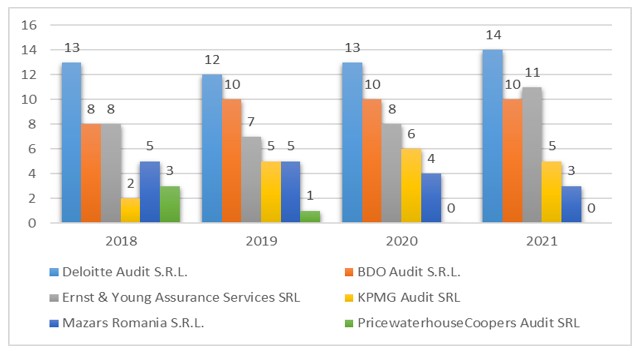

Regarding the main companies that performed the audit mission for the verified sample, I found mostly the companies from the Big Four group (Deloitte Audit S.R.L., Ernst & Young Assurance Services S.R.L., KPMG Audit S.R.L. and PricewaterhouseCoopers Audit S.R.L.) but I also identify other Non Big Four companies that have a large portfolio of customers in the sample analyzed. The situation regarding the main audit companies is presented in Table no.5 and Firure no. 5.

Table 5 – Main audit companies related to the analyzed sample

Source: Author’s own projection

Figure 5 – Main audit companies related to the analyzed sample

Source: Author’s own projection

Discussion

The purpose of the research was to analyze the audit opinions of companies listed on the Bucharest Stock Exchange from 2018 to 2021. By examining these data, I aimed to gain insights into how often auditors switch the audit opinions, which can have significant implications for the quality of financial reporting and overall business performance.

To ensure that the findings are relevant and up-to-date, I chose to study the period between 2018 and 2021. This time frame is notable because it includes the COVID-19 pandemic, which had a profound impact on the global economy and business operations across many industries.

As a result, I believe that the pandemic may have affected the financial statements and audit engagements of the studied companies, and this analysis will provide valuable insights into the potential impact of this unprecedented event on audit practices and procedures. Overall, this study will contribute to the ongoing conversation around audit quality and best practices for financial reporting in today’s rapidly changing business landscape.

In addition to investigating the trend of audit opinions, this study also aimed to identify any trends or patterns that may emerge from my analysis of the audit opinions. Furthermore, I explored whether certain industries or sectors are more likely to experience changes of audit opinions than others, and whether there are any correlations between audit opinion and financial performance or other business metrics. By taking a comprehensive and data-driven approach to this research, I hope to shed light on the complex and evolving landscape of audit practices and their impact on corporate governance and financial reporting.

Looking at the trend of audit opinions in Romania can provide us with valuable insights into the state of accounting and auditing practices in the country. Romania is considered to be an emergent market, which means that the country’s economy is in the process of rapid development and growth. As such, it was important to understand the financial health of Romanian companies and the quality of their financial reporting. By analyzing the trend of audit opinions, I can gain a better understanding of the level of scrutiny and oversight applied to financial reporting practices in Romania. This can help identify areas where improvements can be made in order to increase transparency, accountability, and overall confidence in the financial markets.

The issuance of audit opinions is not a one-time event, and it is common for opinions to change from one year to another. This may happen due to various reasons, including changes in the financial performance of the audited entity, new accounting standards or regulations, or changes in the auditor’s assessment of the risks and materiality of certain transactions or events.

For example, if an audited company experiences a significant increase in revenue or changes its accounting policies, this may affect the auditor’s assessment of the financial statements and lead to a different opinion than the previous year. Similarly, if there are changes in the legal or regulatory landscape that impact the company’s financial reporting obligations, this may result in a change in the auditor’s opinion (Hirst et al., 2018; Adhikari et al., 2019; Chen et al., 2020).

It is also important to note that audit opinions are not static and can be updated or revised in response to new information or events (Deliu, 2013). For instance, if an auditor becomes aware of new evidence or information that materially affects the financial statements, they may need to update their opinion to reflect this (Felix et al., 1982; Turner & Gray, 2010; Jones, 2011; Ye et al. 2011; Berinde & Groúanu, 2013; Velury et al., 2020; Kim et al., 2021; MohammadRezaei et al., 2021).

Overall, changes in audit opinions from one year to another are a natural part of the audit process and can reflect the dynamic nature of financial reporting and auditing. While changes in opinions may cause concern among stakeholders, they can also be an indication of the thoroughness and diligence of the auditing process and the auditor’s commitment to ensuring the accuracy and transparency of financial reporting.

The data presented regarding the annual audit opinions indicate that most companies receive unqualified opinions, which means their financial statements are presented fairly and in compliance with the relevant accounting standards. The number of unqualified opinions remained relatively stable over the years, with a slight increase in 2021 compared to the previous years.

The number of qualified opinions also remained consistent over the years, indicating that only a few companies had material misstatements or limitations of scope in their financial statements. The number of adverse opinions and disclaimers of opinions remained low, indicating that only a few companies had significant material misstatements or limitations that affected the auditor’s ability to form an opinion.

Overall, these data suggest that the majority of companies are presenting their financial statements fairly and complying with accounting standards, but there are a few exceptions where material misstatements or limitations of scope have been identified.

Based on the analysis of the audit opinions for each field of activity, it is evident that the manufacturing and financial and insurance activities’ sectors have consistently received the most unqualified opinions. This suggests that companies operating in these fields have maintained a consistent level of financial reporting quality over the years, which is a positive indicator of the strength of their financial systems and internal controls.

However, it is also concerning that the manufacturing industry has consistently received the highest number of qualified opinions, indicating a need for improvement in their financial reporting practices for some companies. The electricity, gas, steam and conditioning supply sector also received qualified opinions, which could suggest a need for better internal controls and financial systems.

The fact that adverse opinions and disclaimers of opinion are mostly found in the production activity field is justifiable based on the fact that approximately 83% of the analyzed sample can be found in this field of activity. This indicates that there can be issues with the financial reporting practices of some companies in this field, which could lead to a lack of transparency and a higher risk of financial misstatement.

The majority audit companies of these companies belong to the Big Four group, which includes: Deloitte Audit S.R.L., Ernst & Young Assurance Services S.R.L., KPMG Audit S.R.L., and PricewaterhouseCoopers Audit S.R.L. These companies are known for their global reach and expertise in the field of auditing. However, it is worth noting that other non-Big Four companies were also identified, indicating that they have a significant presence in the market and a large portfolio of customers in the sample analyzed. This suggests that while the Big Four may dominate the market, other companies are also competitive and capable of providing quality audit services. Overall, the presence of both Big Four and non-Big Four companies in the sample highlights the diversity of the audit industry and the various options available to companies seeking audit services.

Conclusions and Future Research Directions

In general, audit opinions are issued on an annual basis for financial audits of companies and other organizations. The frequency of audit opinions may vary depending on the specific circumstances and the requirements of the relevant regulatory or legal framework.

Changes in the audit opinion from one year to another can be significant for companies and their stakeholders, as they may indicate changes in the financial position or performance of the organization. It’s important for companies to carefully review the audit report and the underlying financial statements to understand the reasons for any changes in the audit opinion.

It’s also important for companies to maintain transparent and accurate financial reporting practices, as this can help to ensure the reliability and integrity of the financial statements and enhance the credibility of the audit opinion. This can help to build trust among stakeholders and support the company’s long-term financial stability and success.

The audit activity is a complex one and the opinion expressed by the auditor significantly influences the decisions made by investors because they consider the opinion of the auditors absolutely necessary, especially based on previous financial scandals and the pandemic context of recent years.

Based on research and analysis, the conclusions about changes in audit opinions from one year to another:

Changes in audit opinions are relatively common: It is not uncommon for companies to receive a different audit opinion from one year to another, especially if there have been significant changes in the company’s operations or financial performance.Reasons for changes in audit opinions can vary: There are many factors that can contribute to changes in audit opinions, such as changes in accounting policies or estimates, new regulatory requirements, or changes in the company’s risk profile.

Changes in audit opinions can have significant implications: A change in audit opinion can have significant implications for a company, including changes in investor perceptions, increased regulatory scrutiny, and potential legal or financial consequences.

Auditors have a responsibility to carefully consider and communicate changes in audit opinions: Auditors have a responsibility to carefully evaluate changes in audit opinions and to communicate their findings clearly and accurately to stakeholders.

Improvements in transparency and communication can help mitigate the impact of changes in audit opinions: Companies can help mitigate the impact of changes in audit opinions by improving transparency and communication with stakeholders, including providing clear explanations of the reasons for the change and outlining plans to address any issues identified by the auditor.

Overall, changes in audit opinions can be a normal part of the audit process, but they should be carefully evaluated and communicated in order to minimize their impact on stakeholders and ensure the integrity of financial reporting.

The study of the trend of audit opinions for companies listed on the Bucharest Stock Exchange from 2018 to 2021 revealed that a significant majority of audit opinions issued were unqualified opinions. An unqualified opinion is considered the best outcome for a company because it indicates that the financial statements are free from material misstatements and can be relied upon by stakeholders. The maximum percentage of unqualified opinions was found to be 84.33% in 2021, which suggests that a large number of companies listed on the Bucharest Stock Exchange are presenting accurate financial statements.

However, it is important to note that the presence of unqualified opinions does not necessarily mean that a company is financially healthy or performing well. An unqualified opinion only reflects that the financial statements are fairly presented and does not take into account other factors such as a company’s strategic direction, operational efficiency, or future prospects. Therefore, it is important for investors and other stakeholders to conduct a holistic analysis of a company’s performance before making any investment or strategic decisions.

This does not guarantee that all companies listed on the stock exchange are financially healthy or performing well. It is important for stakeholders to conduct further analysis and due diligence before making any investment or strategic decisions.

The manufacturing industry was found to have the highest percentage of qualified opinions, accounting for 46.37% of all qualified opinions issued in 2018. This industry also represented the field of activity with the most companies in the analyzed sample, suggesting that the manufacturing industry in Romania is generally characterized by higher levels of financial scrutiny and stricter regulatory requirements.

The prevalence of qualified opinions in the manufacturing industry may reflect the industry’s reliance on fixed assets, inventory, and production processes. These factors can be more complex to evaluate than other types of assets or operations, and may require a higher degree of financial expertise to accurately assess. Additionally, manufacturing companies may be subject to stricter environmental and safety regulations, which can increase the complexity of their financial reporting and auditing requirements.

While the study of audit opinions for Romanian companies listed on the Bucharest Stock Exchange from 2018 to 2021 provides valuable insights into the quality of financial reporting in this market, it is important to note that the study has some limitations.

The COVID-19 pandemic has had a significant impact on auditor opinions, as businesses have faced unprecedented challenges in terms of financial reporting and disclosure. The pandemic has disrupted supply chains, caused a decline in economic activity, and forced businesses to adapt to new ways of working. As a result, auditors have had to adjust their audit procedures and make judgments about the impact of the pandemic on their clients’ financial statements.

One of the primary effects of the pandemic on auditor opinions has been an increase in the number of companies receiving going-concern opinions. With the economic uncertainty brought on by the pandemic, many companies have faced financial difficulties that have raised doubts about their ability to continue as a going concern. Auditors have had to carefully consider the potential impact of these issues on their clients’ financial statements and provide appropriate disclosures in their audit reports.

Another impact of the pandemic on auditor opinions has been a greater emphasis on the need for transparency and disclosure. As businesses face new risks and uncertainties, auditors have had to ensure that their clients provide adequate disclosure about the potential impact of the pandemic on their financial statements. This has required auditors to use their professional judgment to assess the materiality of COVID-19-related risks and disclosures and provide appropriate opinions.

The increase in going-concern opinions and the greater emphasis on transparency and disclosure are just two examples of how the pandemic has changed the way that auditors approach their work. As businesses continue to navigate the challenges brought on by the pandemic, auditors will need to remain vigilant and flexible in order to provide the high-quality independent opinions that stakeholders rely on.

One of the main limitations of the study is the small volume of the analyzed sample. The analysis only included Romanian companies listed on the Bucharest Stock Exchange during the period 2018-2021, which may not be representative of the broader Romanian economy or the global market. Therefore, it is important to be cautious when generalizing the findings of this study to other markets or industries.

In future studies, it may be beneficial to expand the sample size to include a larger number of companies, both nationally and internationally. This would allow for a more comprehensive analysis of audit opinions and financial reporting trends, and could help to identify any patterns or trends that are specific to certain regions or industries.

References

Adhikari, A. and Tondkar, RH. (2019), ‘The impact of audit opinions on financial reporting quality: Evidence from the USA’, Journal of Applied Accounting Research 20(3), 367-389.

Aitken, M. and Simnett, R. (1991), ‘The Association between Auditor Changes and Changes in Ownership Structure’, Accounting & Finance 31(2), 1-16.

Barnes, BG., Cussatt, M. and Harp, N. (2018), ‘Audit Firm Reputation and Perceived Audit Quality: Evidence from Envelopegate’, SSRN Electronic Journal.

Berinde, S. and Groúanu, A. (2013), ‘Particularities concerning the beneficiaries of audit services provided by Big 4 companies: evidence from Romania’, Annales Universitatis Apulensis Series Oeconomica 15(2), 2013, 483-492.

Berinde, SR. (2013), ‘Forecasting the structure of the Romanian audit market’, Studia Universitatis Babes Bolyai-Negotia 3, 95-108.

Bunget OC., Lungu C. and Olariu AM. (2022), ‘The Interdependence Between The Type Of Audit Opinion And The Variation Of The Stock Price’, Annals of University of Craiova – Economic Sciences Series, University of Craiova, Faculty of Economics and Business Administration 1 (50), 89-97.

Carey, P. and Simnett, R. (2006), ‘Audit Partner Tenure and Audit Quality’, The Accounting Review 81, no. 3, 653 – 676.

Carey, ML., and Jennings, MM. (2008), ‘The importance of auditing small businesses: Evidence from a survey of small business owners’. Journal of Small Business Management 46(3), 348-365.

Carey, J. (2012), ‘Effective audit committee oversight of cybersecurity risk’, The CPA Journal 82(10), 32-37.

Carson, E., Fargher, N. and Zhang, Y. (2006), ‘Trends in auditor reporting in Australia: A synthesis and opportunities for research’, Australian Accounting Review 26(3), 226-242.

Carson, E., Fargher, N., Geiger, MA. and Lennox, CS. (2012), ‘International differences in the timeliness, conservatism, and classification of earnings’, Journal of Accounting Research 50(5), 1245-1272.

Carson, E., Fargher, N., Geiger, MA. and Lennox, CS. (2013), ‘Audit reporting of going concern uncertainty: Research framework and review of prior studies’, Auditing: A Journal of Practice & Theory 32(1), 1-32.

Chen, X. and Wu, Y. (2020), ‘Do auditors issue conservative audit opinions to avoid litigation? Evidence from China’. Pacific-Basin Finance Journal 62, 101359.

Choo, F. and Trotman, KT. (1991), ‘An investigation of the effect of information accessibility on the credibility of auditors’ judgments’. Accounting, Organizations and Society 16(6), 547-560.

Craswell, AT. (1999), ‘Audit quality attributes: the perceptions of audit partners, preparers of financial statements and audit committee members’, Journal of International Accounting, Auditing and Taxation 8(2), 201-219.

Craswell, AT., Francis, JR. and Taylor, SL. (2002), ‘Auditor brand name reputations and industry specializations’, Journal of Accounting and Economics 33(3), 375-400.

Deliu, D. (2013), ‘The Responsibilities and Limited Liability of the Financial Auditor in a Sensitive Socio-Economic Context’, PhD thesis, West University of Timişoara, Timişoara, Romania.

Deliu, D. (2019), ‘Brief Critical Analysis of the Main Corporate Governance Traits within Romanian Banks Listed on Bucharest Stock Exchange’, Proceedings of the 34th International Business Information Management Association (IBIMA) Conference.

Deliu, D. (2020a), ‘Key Corporate Governance Features within Romanian Banks Listed on Bucharest Stock Exchange: A Thorough Scrutiny and Assessment’, Journal of Eastern Europe Research in Business and Economics 271202(10).

Deliu, D. (2020b), ‘The Intertwining between Corporate Governance and Knowledge Management in the Time of Covid-19–A Framework’, Journal of Emerging Trends in Marketing and Management 1(1), 93-110.

Dionisijev, I. (2021), ‘The Audit Opinion In The Role Of Stock Prices Fluctuations On The Macedonian Stock Exchange’, Financial Studies, Centre of Financial and Monetary Research “Victor Slavescu” 25 (3), 29-43.

Fargher, NL. and Jiang, L. (2008), ‘The association between audit reports for going concern uncertainty and financial distress subsequent to audit reporting periods’, Accounting & Finance 48(2), 181-198.

Felix Jr, WL. and Kinney Jr, WR. (1982), ‘Research in the auditor’s opinion formulation process: State of the art’. Accounting Review 245-271.

Fulop, MT. (2018), ‘New tendencies in audit reporting, examples of good practices BVB’, Audit Financiar Journal 2 (150), 249-260.

Hategan, CD. and Crucean, AC. (2018), ‘Reporting of subsequent events in financial statements – between obligation and necessity’, Audit Financiar Journal 4 (152), 571–583.

Hidayat, AH. (2022), ‘Impact of Pandemic Financial Crisis to the Going Concern Audit Opinion Factors’, Advances in Social Sciences Research Journal 9 (5), 147-158.

Hirst, DE., Koonce, L. and Venkataraman, S. (2018), ‘The changing nature of auditor reporting: A review and research agenda’, Journal of Accounting Research, 56(1), 5-47.

Hosseinniakani, SM., Inacio, H. and Mota, R. (2014), ‘A review on audit quality factors. International Journal of Academic Research in Accounting’. Finance and Management Sciences 4(2), 243-254.

Hu, M., Muhammad, A. and Yang, J. (2022), ‘Ownership concentration, modified audit opinion, and auditor switch: New evidence and method’, The North American Journal of Economics and Finance 61, 101692.

International Auditing and Assurance Standards Board (IAASB). 2016. ISA 700 (Revised), Forming an Opinion and Reporting on Financial Statements.

Jones, MJ. (2011), ‘A review of the empirical disclosure literature: Discussion’, Journal of Accounting and Economics 51(1-2), 204-218.

Kim, HJ., Lim, S. and Shin, H. (2021), ‘The effect of auditor‐provided key audit matters on the reliability of auditor opinions’, Journal of Business Finance & Accounting 48(7-8), 981-1014.

Kuruppu, N., Shackleton, R. and Tanewski, G. (2012), ‘Auditor selection and audit committee characteristics: Evidence from Australian companies’, Accounting & Finance 52(1), 177-200.

Lu, B. (2020), ‘Literature Review of Audit Opinion’, Modern Economy 11(01), 28.

MohammadRezaei, F., Faraji, O. and Heidary, Z. (2021), ‘Audit partner quality, audit opinions and restatements: evidence from Iran’, International Journal of Disclosure and Governance 18, 106-119.

Monroe, GS. and Hossain, M. (2013), ‘Expertise, auditor independence, and fraud detection: An experimental’, Accounting, Organizations and Society 38(4), 253-267.

Purnama, A. (2021), ‘Previous Years Audit Opinions, Profitability, Audit Tenure and Quality Control System on Going Concern Audit Opinion’, European Journal of Business Management and Research 6 (2), 140-145.

Simnett, R., and Trotman, KT. (1989), ‘The impact of audit structure on auditors’ judgments’, Journal of Accounting Research 27(1), 1-20.

Tian, J. and Xin, M. (2017), ‘Literature review on audit opinion’, Journal of Modern Accounting and auditing 13(6), 266-271.

Turner, JL. and Gray, GL. (2010), ‘A case for teaching ethics in the auditor-client relationship’, Journal of Business Ethics 94(2), 151-160.

Velury, UK. and Rebele, JE. (2020), ‘The impact of negative financial statement disclosures on auditor judgments’. Auditing: A Journal of Practice & Theory 39(2), 183-200.

Wines, G. (1994), ‘Auditors’ use of analytical review procedures: a cognitive fit perspective’, Journal of Accounting Research 32(2), 263-281.

Wu, X., Zhang, G. and Zhang, J. (2006), ‘The pricing of audit services: Evidence from the market for audit services in China’. Journal of International Accounting, Auditing and Taxation 15(1), 60-84.

Xu, Y., Lai, KS. and Krishnan, J. (2011), ‘The impact of going concern reporting on auditor reputation’, Australian Accounting Review 21(1), 20-29.

Xu, Y., Krishnan, J. and Lai, KS. (2013), ‘The impact of going concern modification on audit fees and auditor changes: Evidence from Australia’, Journal of Contemporary Accounting & Economics 9(1), 1-17.

Ye, P., Simnett, R. and Tilling, M. (2011), ‘Client importance, non-audit services and auditor independence: An analysis of auditor perceptions’, Accounting and Finance 51(3), 747-770.