1Egypt Japan University of Science and Technology, Alexandria, Egypt

2Ritsumeikan Asia Pacific University, Oita, Japan

Volume 2024,

Article ID 145355,

Journal of Accounting and Auditing: Research & Practice,

15 pages,

DOI: https://doi.org/10.5171/2024.145355

Received date: 5 February 2024; Accepted date: 12 June 2024; Published date: 12 July 2024

Academic Editor: Kamal Abou El Jaouad

Cite this Article as:

Rola Samy Shawat, Ahmed Zamel, Toshitsugu Otake, Sara Sabry and Hebatallah Badawy (2024), " How Firm Size Shapes the ESG and Financial Performance Nexus: Insights from The MENA Region", Journal of Accounting and Auditing: Research & Practice, Vol. 2024 (2024), Article ID 145355, https://doi.org/10.5171/2024.145355

In an era of increasing environmental and social awareness, sustainability reporting is becoming a global trend that is regarded as an essential tool for organizations to demonstrate their commitment to sustainability, manage risks, and respond to stakeholder expectations. This study aims to examine the relationship between a firm’s environmental, social, and governance (ESG) performance, and its financial performance in the Middle East and North Africa (MENA) Region. In addition, the study investigates the moderating role of firm size in the ESG performance – firm performance relationship. The paper relied on data panel drawn from Thomson Reuters Eikon database to analyze the abovementioned relationships on the countries in the MENA region during the period from 2013 to 2022. Based on a sample of 522 firm-year observations of non-financial firms in the MENA Region, the regression results showed that ESG performance contributes significantly towards better financial performance supporting the stakeholder’s theory. Additionally, firm size is a relevant moderator for the association between sustainability performance and financial performance nexus. Overall, the research results are of great interest as understanding how ESG practices affect financial performance could provide valuable insights for firms, investors, and policymakers seeking to optimize both sustainability efforts and financial outcomes.

Keywords: ESG Performance, Firm Size, Financial Performance, MENA

Introduction

Sustainability reporting practices have emerged as a strategic tool that is gradually being implemented by firms all across the world (Singh et al., 2023). It is considered a way of communicating an organization’s performance in terms of various stakeholders’ interests. One of the major aims of the guiding conceptual accounting framework depicted in Statement of Financial Accounting Concepts No. 8 (SFAC #8) (FASB, 2018) is to help improve users’ judgments and decisions when confronted with a variety of information sources. Consequently, more information would reduce the information asymmetry between the firm and its external stakeholders. In the last few decades, stakeholders have become increasingly aware of the importance of sustainability, especially after global warming, the economic crisis and market crashes (Setiani, 2023). Financial performance measures are the traditional way of measuring any business’s success. However, nowadays firm stakeholders’ information expectations have been shifted beyond financial information, and they began seeking non-financial information beyond the traditional metrics to evaluate a business. According to Pu (2023), the overall direction towards sustainable investing and sustainability practices seeks to ensure that all stakeholders are taken care of while making investment decisions. This strategic action signifies a purposeful shift towards a widely recognized concept known as the ‘Triple Bottom Line’ or 3 Ps (People, Planet and Profit). The underlying notion is to progress and expand beyond the only goal of shareholders’ wealth maximization to the optimization of the advantages associated with the 3 Ps (Pu, 2023). As a result, the importance of non-financial information has grown rapidly. In order to meet the information needs of their stakeholders, firms now report both financial and non-financial information.

In this regard, firms implemented the disclosure of environmental, social, and governance (ESG) factors, as the main pillars of sustainability, to disclose their non-financial information. ESG is an extension of corporate social responsibility (CSR) and socially responsible investment (SRI). ESG refers to a wide range of environmental, social, and corporate governance factors that may have an impact on a company’s ability to generate value. It refers to the incorporation of non-financial elements into corporate business strategy and decision-making (Koundouri et al., 2022). ESG performance is a measurable indicator of the firm’s sustainability and societal efforts, which uses metrics meaningful to stakeholders to identify responsible firms (Serafeim, 2020). Concerned investors and stakeholders intend to know where the firm invests its money and how it conducts business, particularly in the context of environmental, social, and governance (ESG) activities. For instance, to investors, the advantages of a firm’s ESG performance can reduce information asymmetry between the corporations and their investors. Therefore, investors will react positively if the corporations serve their demands by providing enough information in ESG disclosures to them for decision-making (Suttipun, 2022).

The impact of ESG performance on companies’ financial performance is debatable and controversial (Chen & Xie, 2022). There are two conflicting points of view regarding the ESG – firm performance relationship (Lunawat & Lunawat, 2022). The first point of view argues that ESG activities are a burden which imposes additional costs on firms, and that firms struggle to balance these costs with their financial performance. The second point of view proposes that firms benefit from the costs related to ESG activities, where stakeholders, such as investors, advocate greater understanding of ESG and its significance to businesses to enable them to make more informed investment decisions and react positively if the firms serve their demands by providing enough information in ESG (Suttipun, 2022). Accordingly, the study of the correlation between ESG performance and firm financial performance has yielded contradictory results. There are positive, negative, mixed, and conflicting research results in the prior literature. Nonetheless, there is no conclusive evidence that ESG has an impact on a company’s cash flow, financial position, reputation, or value (Lunawat, 2022). These differences in the existing literature could be attributed to a variety of factors as ESG examination may vary by country, region, and industry or sector. For instance, the dynamics of developing and developed markets differ significantly. In which, stakeholders in developed markets are better informed and more aware of ESG issues and thus demand and value ESG disclosures and activities (Ali et al., 2017).

The value of this paper arises from the unavailability of conclusive research findings for the hypothesized relationship which creates an opportunity for this research to make potential contribution and reduce this research gap in particular regarding the developing countries in the MENA Region. Furthermore, most research relies on oversimplified models that focus primarily on the direct association between ESG performance and financial performance ignoring alternative moderating factors, which is a driving force to add to the existing literature by testing alternative moderating variables affecting the relationship such as firm size on the hypothesized relationship. Since ESG practices are gaining prominence in the MENA region, in this paper, the debate on the performance impact of ESG is revisited using data pertaining to MENA region countries. Accordingly, the major aim of this research is to contribute to the existing literature and to examine whether ESG performance contributes to the firm’s financial performance in the MENA region. In addition, this research will test the moderating role of firm size in the ESG- Firm financial performance nexus.

The remainder of the paper is organized as follows: Section 2 provides a background on the theoretical perspective behind ESG, a brief literature review, and develops the research hypotheses. Section 3 illustrates the research methodology used in this study. Section 4 presents the empirical results and the research findings. Section 5 concludes the paper and presents the recommendations and implications for future research.

Literature Review and Hypotheses Development

Environmental, Social, and Governance (ESG)

Environmental, Social, and Governance (ESG) is a term widely used in a company’s Corporate Social Responsibility (CSR). However, ESG has wider implications than CSR as it also covers environmental and governance aspects with social factors (Gillan et al., 2021). ESG information has lately become everyone’s concern due to the potential long-term impact given to stakeholder investments rather than just shareholders (Almeyda & Darmansyah,2019). ESG is considered a sustainability metric of firms that measures and reports their sustainable performance towards the goal of sustainable development as well as indicating the accountability to all the stakeholders both inside and outside of the companies. ESG is regarded as useful additional information to supplement traditional financial and investment analysis, as well as influence the long-term value of a company (Wong ,2017). Firms that report ESG information address the firm’s use of sources, natural resources, human rights, and their level of corruption, as well as how they invest in community relations, among other things. For instance, under the environmental performance, a company’s initiatives towards environmental and climatic impacts from the business operations are measured. Governance performance reflects board member independence, minority shareholder policies, transparency in corporate disclosures, and ownership structure. Lastly, human rights, workplace equality and diversity, and societal contribution are all social factors that influence social performance (Lunawat & Lunawat, 2022).

Theoretical Perspective

There are several theories that explain the influences of non-financial information disclosures on firm financial performance. Two contradictory theoretical approaches explain the ESG performance and financial performance nexus; the stakeholder theory and the trade-off hypothesis show a positive and negative relationship between ESG performance and financial performance respectively. According to the stakeholder theory, companies must not only operate for their own benefit, but also for the benefit of other stakeholders (Freeman, 1984). Stakeholder theory can help companies understand how ESG issues affect their relationships with various stakeholders such as employees, customers, suppliers, creditors, and the wider community. According to this theory, acting in a way that meets the demands of stakeholders contributes in gaining support from both internal and external parties. Stakeholders are at the center of business organizations, and it is necessary to satisfy the demands of the various stakeholders in order to improve long-term performance (Kalia & Aggarwal, 2022). Following Chouaibi et al. (2022) and Huang (2022), this study will use the stakeholder theory to explain empirical reasons for the impacts of ESG performance on firm financial performance.

On the opposite hand, according to the trade-off hypothesis or traditionalist view (Friedman, 2007), there is a negative relationship between ESG performance and financial performance. Where, spending resources to achieve social and environmental goals (such as initiatives towards pollution reduction, higher employee wages and benefits, donations, and community sponsorships) raises costs, reduces profitability, and reduces competitive advantage (Galant & Cadez, 2017). This can be explained as socially responsible firms encounter more financial expenses, resulting in worse operational and financial performance.

ESG and Financial Performance

Through ESG disclosure, companies can effectively boost transparency, reduce the degree of information asymmetry, and enhance investors’ long-term investment interests in companies (Cui et al. 2018). Non-financial disclosures such as ESG are expected to evolve into a societal investment to satisfy stakeholder interests, which will in turn improve firm performance. Previous research on the impact of ESG on firm performance has shown inconsistent results. However, as explained by the stakeholder theory, most studies found evidence that companies with higher ESG performance tend to have better financial performance and better market value (Aboud & Diab, 2018; Sharma et al., 2020; Ahmad et al., 2021; Chouaibi et al., 2022; Sandberg et al., 2022; Setiani, 2023).

Setiani (2023) examined the impact of ESG scores on firm financial performance on companies listed on the Indonesian stock exchange; the results of this research showed that there is a positive relationship between ESG scores and firm financial performance. Chouaibi et al., (2022) explored the direct links between ESG practices and financial performance and indirect through the mediate role of green innovation. The findings show that better ESG practices increase firm value while ESG weaknesses decrease it. Moreover, Sandberg et al. (2022) investigated how ESG ratings impact financial performance in the European food industry. The results showed that higher ESG ratings are associated with better financial performance. Kalia et al., (2022) investigated the effect of total and each individual component of environmental, social, and governance score (ESG) on the financial performance of 468 healthcare companies across developing and developed countries. The results revealed that higher ESG scores have a positive and significant impact on firm financial performance measured in ROA & ROE. Additionally, the results of the sub-sample analysis suggested that the relationship between ESG performance and financial performance cannot be generalized as the results showed that performing ESG activities impacts firm financial performance of healthcare companies in developed economies positively; suggesting that this relationship would be negative or insignificant in the case of developing economies. Also, in their study on the determinants of ESG disclosures, Sharma et al. (2020) carried out the content analysis and found that ESG disclosure and financial performance have a significantly positive relationship. Aboud & Diab (2018) examined the impact of ESG practices disclosure on firm value in the Egyptian context. They found that firms listed in the ESG index have higher firm value, and that there is a positive relationship between firms’ higher rankings in the index and firm value. Velte (2017) evaluated the impact of ESG performance on financial performance on a sample of 412 firm-year observations of companies listed on the German Prime Standard. The results showed that ESG performance has a positive impact on ROA but has no impact on Tobin’s Q.

On the other hand, in a recent study, Zahid et al. (2022) explored the moderating role of audit quality in the relationship between ESG factors and financial performance in Western European countries. The results showed that ESG has a significantly negative effect on a firm’s financial performance, supporting the trade-off hypothesis that investing in ESG activities increases the cost of business. Moreover, the research results of Duque Grisales & Aguilera-Caracuel (2021) applied on 104 multinationals in Latin America showed that the relationship between ESG scores and financial performance is statistically negative. Other studies showed a U-shaped link between ESG performance and financial performance implying that this relationship is influenced to an extent. The research results of Barnett and Salomon (2012) showed a U-shaped link where, at the beginning, ESG activity harms financial performance because costs outweigh the benefits but, later on, the connection is reversed and becomes positive.

Accordingly, the first research hypothesis (H1) is formulated as follows:

H1: Firm ESG performance has a positive significant impact on its financial performance in the MENA region.

Moderating Role of Firm Size

Many studies used firm size simply as a control variable. However, the role of firm size is more than a control variable in investigating the relationship between firm ESG performance and financial performance. There are various reasons as to why firm size relates to the relationship between ESG and financial performance. According to Barney (1991), the resource-based view assumes that a firm’s resources are invaluable, unique, imitable, and non-substitutable. In this case, large sized firms are considered to have more competitive advantages when compared to the small sized firms. In which, large firms are financially solvent, have more available financial resources to devote to ESG activities when compared to small firms (Shakil, 2020). Therefore, large sized firms are able to invest more in sustainability initiatives and practices than small sized firms. To conclude, the resource-based view assumes that large firms have higher sustainability performance and financial performance. On the contrary, small sized firms having limited resources engaging in ESG activities implies that those resources cannot be used for more productive purposes.

Moreover, large firms are perceived to have a well-defined strategy and goals for monitoring their business and, as a result, are better suited to handle sustainability projects. Furthermore, a firm’s visibility could be taken into account in this context, as more visible firms appear to be more willing to engage in better sustainability practices as a result of their public image among shareholders (D’Amato & Falivena, 2020). In their research, Ahmad et al. (2021) examined the impact of ESG on the financial performance of UK firms and investigated the moderating role of firm size on the relationship; the results support the role of firm size as a moderator in this relationship. Moreover, the results of the research conducted by D’Amato & Falivena (2020) showed that the relationship between CSR and firm value is moderated by firm size on a sample of nonfinancial companies listed in Western European countries. Theoretically exploring the role of firm size in the relationship between ESG and firm financial performance; it is assumed to be a positive relationship as larger firms have a greater ability to participate in more and better sustainability practices than smaller firms.

Accordingly, the second research hypothesis (H2) is formulated as follows:

H2: Firm size significantly moderates the relationship between ESG and firm financial performance in the MENA region.

Research Design and Methodology

Population and Sample Selection

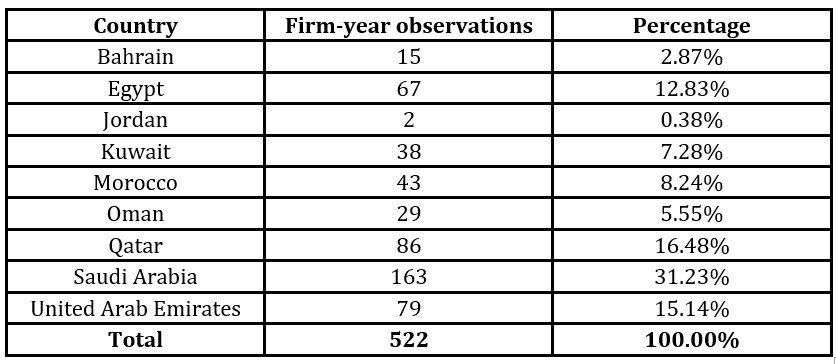

The research population includes all non-financial firms in the Middle East and North Africa (MENA) region. As financial firms differ greatly from non-financial firms, all financial firms including banks, insurance companies, and investment companies were excluded as they have special regulations and accounting standards. The research relied on financial data and ESG scores collected from Thomson Reuters database over a period of 10 years from 2013 to 2022, which assigns ESG scores and tracks the financial performance of firms from the MENA region. This final sample relied on 162 non-financial firms in the MENA Region with 522 firm-years observations over the 10-year period after excluding missing data and outliers. Table (1) presents the distribution of firm-year observations across countries. Three countries (Saudi Arabia, Qatar, and United Arab Emirates) represent a large portion of the total sample (62.85%)

Table 1: Firm-Year Observations by Country

Measurement of Variables and Models Development

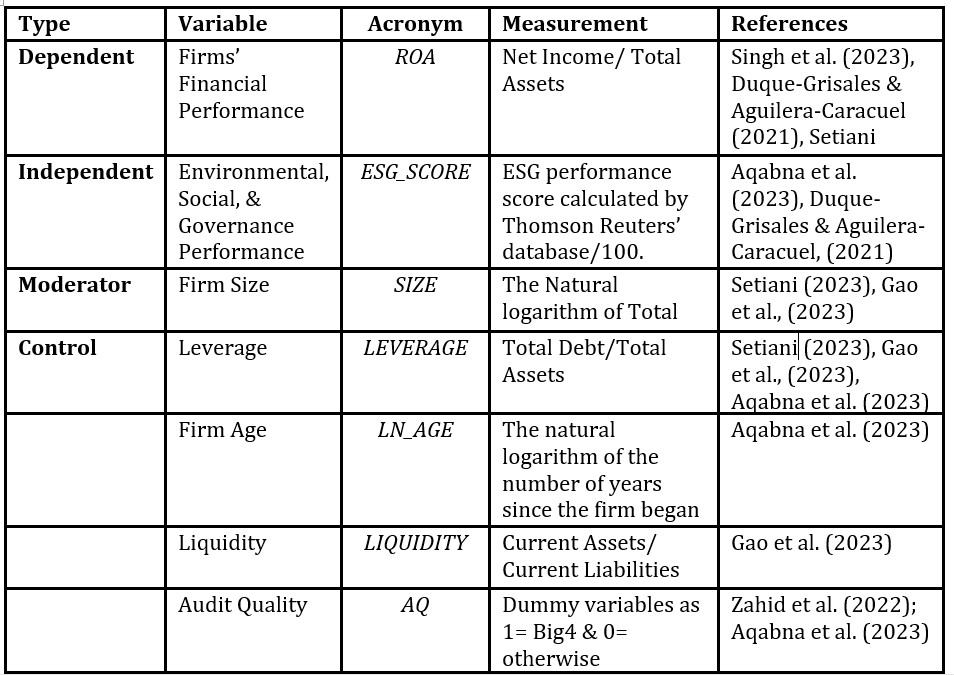

This paper involves one dependent variable which is firm financial performance measured in an accounting-based measure which is Return on Assets (ROA), and it has been calculated as net income divided by total assets. (Duque-Grisales & Aguilera-Caracuel, 2021; Singh et al., 2023; Setiani, 2023).

The independent variable is ESG Performance (ESG_SCORE). Following prior literature (Duque-Grisales & Aguilera-Caracuel, 2021; Neitzert & Petras, 2022; Aqabna et al., 2023), this variable is measured using ESG scores calculated by Thomson Reuters’ database. Thomson Reuters Refinitiv Eikon derives its ESG scores from a comprehensive analysis of publicly available data, including regulatory filings, news articles, and company reported information and websites (Thomson Reuters 2017, p. 4). The underlying measures are grouped into 10 categories. A combination of the 10 categories formulates the final ESG score, which is a reflection of the company’s ESG performance. According to Neitzert & Petras (2022), table (2) summarizes all the three pillars of ESG, and the weights assigned to the subcomponents of each pillar. The aforementioned scores are constantly revised and updated in order to provide the most up-to-date data and trends, with the objective of providing stakeholders with the needed information to make well-informed decisions (Thomson Reuters, 2017).

Table 2: Breakdown of Thomson Reuters Eikon’s ESG Score

The moderating variable in this paper is firm size (SIZE) which is measured by the natural logarithm of total assets (Setiani 2023; Gao et al. 2023). There are several factors that can be considered in determining firms’ financial performance. Based on prior literature, the following four control variables were considered which are: firm leverage (LEVERAGE), which is measured by the ratio of total debt to total assets; firm age (LN_AGE), which is measured by the natural logarithm of the number of years since the firm is established (reference); firm liquidity (LIQUIDITY), which is measured using current ratio; and finally, audit quality (AQ), which is measured as a dummy variable that takes the value (1) in case the auditor is a Big 4 audit firm, and (0) otherwise. Table (3) summarizes the variables’ measurement.

Table 3: Variables’ Description

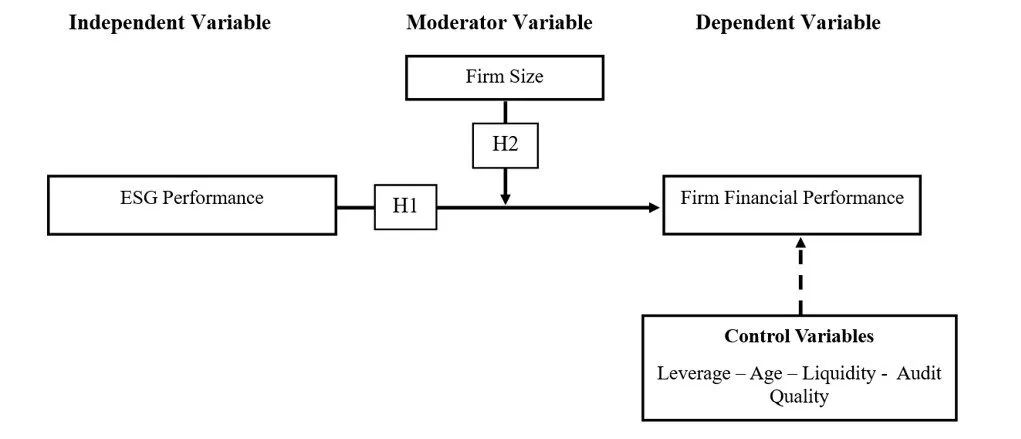

Conceptual Design & Research Model

Based on the above literature and hypothesis, the following conceptual design illustrates the relationship between the variables.

Figure 1: Research Model

(Source: Authors)

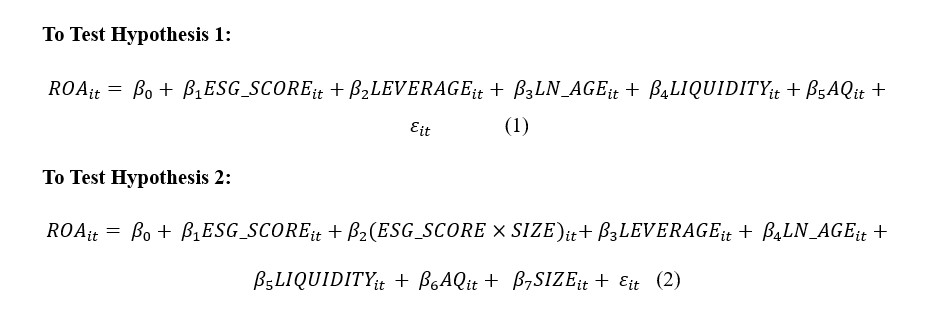

Empirical Model

The following multivariate regression models are estimated to test the hypothesized relationships:

Empirical Results

Descriptive Statistics

In this section, the descriptive statistics of the independent, dependent, and control variables that were used in the research are illustrated. These statistics include the mean, the standard deviation, the minimum, and the maximum. Table (4) shows the descriptive statistics of the research sample, which involves 522 firm-year observations. Table (4) shows that ESG_SCORE ranges from 0.72 to 86.29, with a mean of 29.1272222 and a standard deviation of 18.65833261, indicating variations between the firms’ ESG performance in the research sample. The dependent variable ROA represents a firm’s financial performance; table (4) shows that the mean of this variable is 0.0600448 and the standard deviation is 0.08980036 with a range from -0.57965 to 0.70301. Regarding the moderating variable SIZE, which is measured by the natural logarithm of total assets, table (4) indicates that the mean of size is 21.7704 and the standard deviation is 1.74712, with a minimum of 16.39 and a maximum of 27.22.

As for the control variables, it is shown that LEVERAGE ranges from 0.00 to 1.02 with an average of 0.2481801; for the variable Firm age (LN_AGE), the natural logarithm value of firm age was taken to eliminate the effect of outliers with a range from 1.79 to 5.12 years and a mean of 3.3114; for the variable LIQUIDITY, the table shows a mean of 1.8040038 and a standard deviation of 1.88877223; lastly, the variable Audit Quality (AQ) which is measured as a dummy variable that takes the value (1) in case the auditor is Big 4 firms, (0) otherwise, 81% of the firms in the sample are Big 4 audit clients.

Table 4: Descriptive Statistics

Pearson Correlations

A Pearson Correlation test was conducted as a means of performing an initial analysis into the relationship between the research variables as a correlation coefficient measures the strength and direction of a linear relationship between two variables. Table (5) presents the Pearson correlations matrix confirming the expectations, where ROA is positively and significantly associated with the ESG_SCORE at 5% significance level (Pearson correlation = 0.074). This indicates that the higher the ESG performance of firms measured in (ESG_SCORE) the higher its financial performance measured in (ROA).

As for the control variables, table (5) provides initial evidence that LEVERAGE is negatively associated and significant with ROA at 1% significance level (Pearson correlation = -0.365), which means the higher the leverage of firms the lower its financial performance and vice versa. On the other hand, LN_AGE is positively and significantly associated with the ROA. Moreover, LIQUIDITY as well as AQ are both positively and significantly associated with ROA. The values of the Pearson correlation coefficients of variables are lower than 0.90. The results presented in table (5) show that multicollinearity issue is not present among variables (Hair et al. 2006).

Table 5: Pearson Correlations

* Correlation is significant at the 0.05 level (2-tailed).

** Correlation is significant at the 0.01 level (2-tailed).

Hypotheses Testing

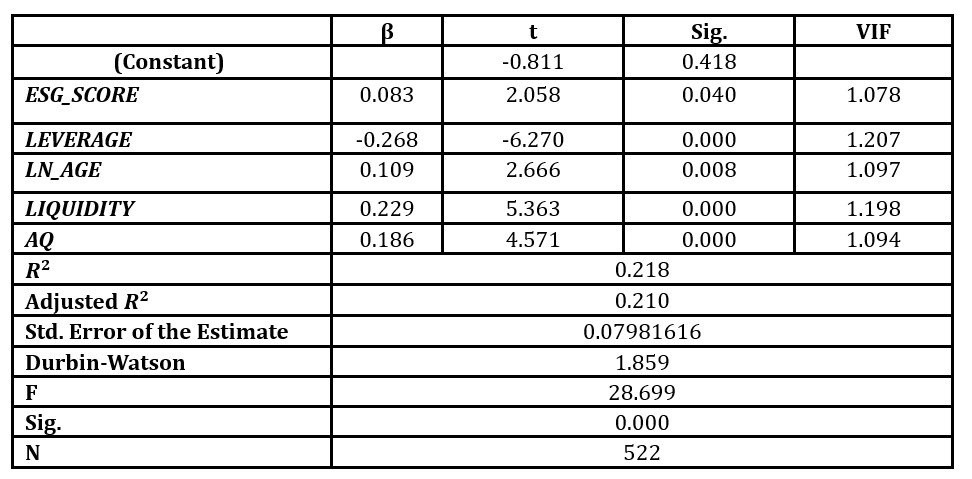

To test the first research hypothesis (H1) which assumes that firm ESG performance has a positive significant impact on its financial performance in the MENA region, we ran the first regression model. In the regression test result of the first research hypothesis (H1), table (6) indicates that F-test model is significant (F = 28.699, Sig.= 0.000), showing that the results of the model can be relied on to analyze the effect of ESG performance (ESG_SCORE) on firm financial performance (ROA), table (6) shows the regression results.

The R-squared value of 0.218 indicates that 21.8% of the changes in the dependent variable can be explained by the independent variables. The adjusted R-squared value of 0.210 shows that 21% of the changes in the dependent variable can be explained by the independent variables, providing a slightly more conservative estimate of the model’s explanatory power. The Durbin-Watson statistic of (1.859) is used to test for autocorrelation in the residuals suggesting that there is no significant autocorrelation as the accepted threshold is 2 (Nerlove & Wallis, 1966).

Based on the multicollinearity test which indicates a threat to the model, it can be concluded that the regression model is free from the multicollinearity problem as the Variance

Inflation Factor (VIF) values are lower than 10 for each of the models presented, indicating that the results are not biased due to issues of multicollinearity (Alin,2010).

As for the t-statistics of ESG_SCORE, (t = 2.058, Sig. = 0.040) showing that ESG is positively and significantly associated with ROA. Based on the obtained results, the first research hypothesis (H1) is supported (β= 0.083, p-value < 0.05), showing that there is a significant positive relationship between ESG performance (ESG_SCORE) and financial performance (ROA). This result indicates that firms with higher ESG performance are more likely to perform financially better. The results are inconsistent with that of Duque Grisales & Aguilera-Caracuel (2021) and Zahid et al. (2022), which showed that ESG has a significantly negative effect on a firm’s financial performance supporting the trade-off hypothesis in which investing in ESG activities increases the cost of business. However, the results shown in table (6) are in line and consistent with prior research (Aboud & Diab, 2018; Sharma et al., 2020; Ahmad et al., 2021; Chouaibi et al., 2022; Setiani, 2023; Sandberg et al., 2022) which showed that there is a positive relationship between ESG scores and firm financial performance. The results of testing H1 support the stakeholder theory, which explains that ESG performance can help companies to create long-term value for all stakeholders.

Table 6: Impact of ESG Scores on ROA

Table (6) shows that Leverage (LEVERAGE) is having a negative significant effect on ROA (t = -6.207, Sig. = 0.000), implying that the high leverage firms are more likely to have low financial performance. As for the firm age, table (6) shows that Age (LN_AGE) is having a positive and significant effect on ROA (t = 2.666, Sig. = 0.008). As for the firm liquidity, table (6) provides evidence that highly liquid firms are more likely to have higher ROA (t = 5.363, Sig. = 0.000). Finally, Audit Quality (AQ) is having a positive significant effect on financial performance (ROA) implying that large audit firms always have higher audit quality, which infers that high audit quality can help corporations perform better financially (Zahid et al., 2022).

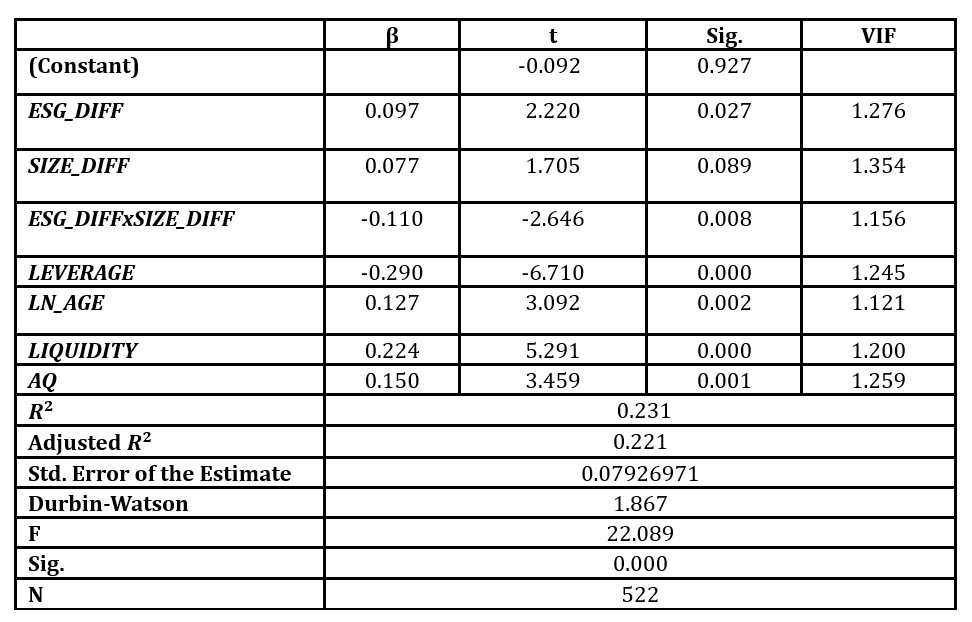

To test the second research hypothesis (H2) which assumes that firm size significantly moderates the relationship between ESG performance and firm financial performance in the MENA region, we ran the second regression model. In the regression test result of the second research hypothesis (H2), the F-test model is significant (F = 21.279, Sig.= 0.000). Table (7) shows the regression results.

Table 7: Impact of ESG Scores & Firm Size on ROA

Based on the results shown in table (7), the model cannot be relied on as there is a multicollinearity problem faced in testing the above hypothesis where the variance inflation factor (VIF) for some variables is above 10. To solve this threat, we use centering variables technique to reduce multicollinearity. This is known as standardizing the variables by subtracting the mean. According to Ross & Willson (2017), centering the data eliminates the correlation between predictors. Otherwise, the interaction will highly correlate with the predictors and make estimation unstable or even not possible. This is done by subtracting the mean of the variable from each score, and then the centered variables are multiplied together to get the interaction term according to the following formula (Ross & Willson, 2017):

So, first the mean of the variable which measures the firm size which is (SIZE) for all the sample was calculated. Then a newly created variable called (SIZE_DIFF) was calculated which is the difference between the variable SIZE and the mean. Second, the mean of the variable which measures ESG performance which is (ESG_SCORE) was calculated and a newly created variable called (ESG_DIFF) was calculated in the same manner. Lastly, the centered variables are multiplied together to get the interaction referred to as (ESG_DIFFxSIZE_DIFF).

After using this technique, the multicollinearity threat was eliminated. The results of table (8) show that multicollinearity is not a problem anymore as the variance inflation factors (VIFs) are all under 10. In the regression test result of the second research hypothesis (H2) after centering the variables, table (8) indicates that F-test model is significant (F = 22.089, Sig.= 0.000).

Table 8: Regression Results after Centering the Variables to Test H2

Table (8) indicates that ESG_DIFF has a positive and significant impact on ROA (t-value = 2.220, Sig.= 0.027). The results are consistent with the results of testing the first research hypothesis. The results also show that SIZE_DIFF has a positive and significant impact on ROA (t-value = 1.705, Sig.= 0.089). The interaction term (ESG_DIFFxSIZE_DIFF) shows a negative significant impact on ROA (t-value = -2.646, Sig.= 0.008). This result indicates firm size moderates the relationship between ESG performance and ROA. It implies that when the ESG_DIFF interacts with the SIZE_DIFF, the final effect on ROA is negative and significant.

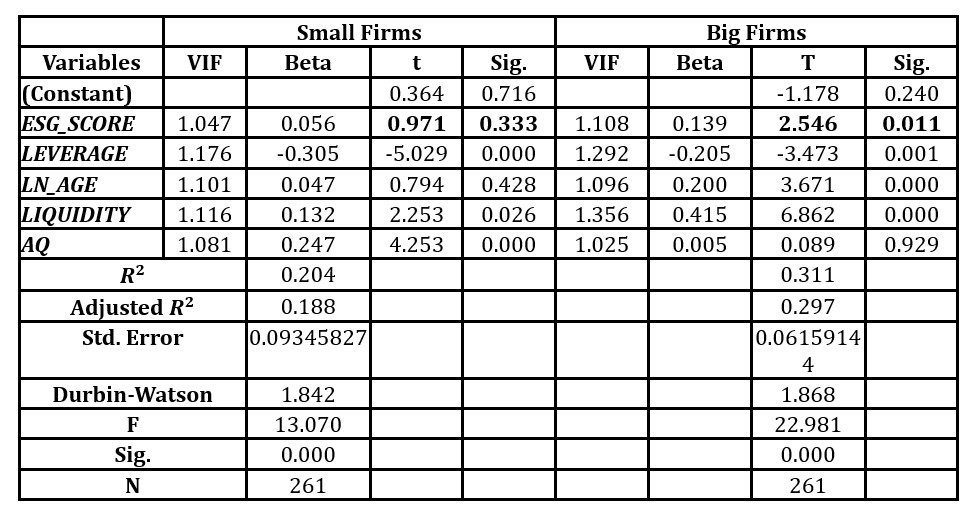

Because we are relying on the differences from the mean to measure our main variables, it is important to make further analysis to understand whether the ESG performance of big firms is significantly different than that of small firms. We divide the sample into 2 subsamples, small firms vs big firms based on firm size which is measured using the natural logarithm of total assets. The 1st sample is the firms whose size is smaller than the mean (Small Firms) and the other sample is the firms whose size is greater than the mean (Big Firms).

According to table (9), the results for small firms’ sample indicate that F-test model is significant (F = 13.070, Sig.= 0.000), showing that the results of the model can be relied on to analyze the moderating effect of firm size on ESG and firm financial performance nexus. The R-squared value of 0.204 indicates that 20.4% of the changes in the dependent variable can be explained by the independent variables. The t-statistics of ESG_SCORE (t = 0.971, Sig. = 0.333) show that ESG performance is positively but insignificantly associated with ROA for small sized firms. The results for big firms’ sample show that F-test model is significant (F = 22.981, Sig.= 0.000). Moreover, the results show that t-statistics of ESG_SCORE (t = 2.546, Sig. = 0.011) indicate that ESG performance is positively and significantly associated with ROA for big sized firms. The regression results in table (9) indicate that big size firms investing in ESG activities tend to have higher ROA (Adj. R2 = 29.7%). According to the above-mentioned results, H2 is supported as the results indicate that the relationship between ESG performance and financial performance behaves differently for small‐ and large‐sized companies. In other words, firm size moderates the relationship between ESG and firm’s financial performance in the MENA region. The results are consistent with the results of (Ahmad et al., 2021; Abdi et al., 2022) that support the role of firm size as a moderator in this relationship between ESG and the financial performance.

Table 9: Regression Results: Small Firms vs. Big Firms

Conclusion and Discussion

To date, research on the relationship between the ESG performance and financial performance of firms in the MENA region has been limited. This study addresses this gap in the research by examining the effect of ESG performance on financial performance and the moderating role of firm size in this relationship on non-financial firms in the MENA region. The results of this study show results that are consistent with previous research, as the regression models show that ESG scores have a positive and significant relationship to firm’s financial performance, measured in ROA, corroborating the stakeholder theory. ESG scores can demonstrate that companies that properly manage environmental, social, and governance aspects will be able to improve their financial performance. In addition, by investigating the moderating influence of firm size on the relationship between ESG performance and firm financial performance, it was found that Firm size can strengthen the relationship between ESG scores and firm financial performance. This study contributes to the research domain of ESG and firm financial performance by presenting the significant influence of ESG on ROA in the MENA region. This study also contributes to the stakeholder theory by empirically depicting that firms’ ESG performance increases the financial performance.

This research possesses both theoretical and managerial implications. From a theoretical perspective, the findings signify a progression of the existing body of knowledge regarding the correlation between ESG performance and firm financial performance by adding firm size as variables that influence the direction of this correlation. Consequently, these findings facilitate a more precise interpretation of this correlation. Furthermore, the findings propose that researchers should explore additional moderating or mediating variables that may offer a more realistic portrayal of this relationship. This research goes beyond investing only the impact of ESG initiatives on firm financial performance, whether positive or negative, but also the context and conditions under which ESG positively or negatively affects firm outcomes. The findings of this study have significant implications for managers and policy makers in MENA region countries and other developing economies. The findings indicate that ESG provides long-term benefits to shareholders, therefore it is imperative to allocate considerable resources to this field. For investors when making investment decisions, they must not only consider financial aspects but also non-financial aspects in terms of considering ESG performance of firms. Further, it is claimed that regulatory bodies such as central banks, auditors, and stock market administrators take into account ESG factors in order to provide trustworthy financial data.

This study has several limitations. The study uses the ESG scores combined only to test the impact of ESG performance on financial performance. Future research may analyze the individual effects of the E, S and G dimensions. Moreover, firm financial performance variable is only measured by an accounting-based measure using return on assets, further research can add other measurements such as market-based measurements. The study’s results are restricted only to countries in the MENA region, so they cannot be generalized. Moreover, due to the lack of ESG scores information, some MENA countries were excluded from the sample. Future researchers should consider increasing the scope of their research sample and could use other data sources.

References

Abdi, Y., Li, X. and Càmara-Turull, X. (2022). ‘Exploring the impact of sustainability (ESG) disclosure on firm value and financial performance (FP) in airline industry: the moderating role of size and age,’ Environment, Development and Sustainability, 24(4), 5052-5079.

Aboud, A. and Diab, A. (2018).‘The impact of social, environmental and corporate governance disclosures on firm value: Evidence from Egypt,’Journal of Accounting in Emerging Economies, 8(4), 442-458.

Ahmad, N., Mobarek, A. and Roni, N. (2021). ‘Revisiting the impact of ESG on financial performance of FTSE350 UK firms: Static and dynamic panel data analysis,’ Cogent Business & Management,8(1), 1-18. Available at: https://doi.org/10.1080/23311975.2021.1900500

Ali, W., Frynas, J. G. and Mahmood, Z. (2017). ‘Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: A literature review,’ Corporate Social Responsibility and Environmental Management, 24(4), 273–294. https://doi.org/10. 1002/csr.1410

Almeyda, R. and Darmansya, A. (2019). ‘The influence of environmental, social, and governance (ESG) disclosure on firm financial performance,’ IPTEK Journal of Proceedings Series, (5), 278-290.

Aqabna, S., Aga, M. and Jabari, H. (2023). ‘Firm Performance, Corporate Social Responsibility and the Impact of Earnings Management during COVID-19: Evidence from MENA Region,’ Sustainability, 15(2), 1-20. Available at: https://doi.org/10.3390/su15021485.

Barnett, M. L. and Salomon, R. M. (2012). ‘Does it pay to be really good? Addressing the shape of the relationship between social and financial performance,’ Strategic management journal, 33(11), 1304-1320.

Barney, J. (1991). ‘Firm resources and sustained competitive advantage,’ Journal of Management, 17(1), 99–120. Available at: https://doi.org/10.1177/014920639101700108.

Chen, Z. and Xie, G. (2022). ‘ESG disclosure and financial performance: Moderating role of ESG investors,’ International Review of Financial Analysis, 83, 1-20. Available at: https://doi.org/10.1016/j.irfa.2022.102291.

Chouaibi, S., Chouaibi, J. and Rossi, M. (2022). ‘ESG and corporate financial performance: the mediating role of green innovation: UK common law versus Germany civil law,’ EuroMed Journal of Business, 17(1), 46–71. Available at: https://doi.org/10.1108/EMJB-09-2020-0101.

Cui, J., Jo, H. and Na, H. (2018). ‘Does corporate social responsibility affect information asymmetry?,’ Journal of Business Ethics, 148(3), 549–572. Available at: https://doi.org/10.1007/s10551-015-3003-8.

D’Amato, A. and Falivena, C. (2020). ‘Corporate social responsibility and firm value: Do firm size and age matter? Empirical evidence from European listed companies,’ Corporate Social Responsibility and Environmental Management, 27(2), 909–924.

Duque-Grisales, E. and Aguilera-Caracuel, J. (2021). ‘Environmental, Social and Governance (ESG) Scores and Financial Performance of Multilatinas: Moderating Effects of Geographic International Diversification and Financial Slack,’ Journal of Business Ethics, 168(2), 315–334. Available at: https://doi.org/10.1007/s10551-019-04177-w.

FASB (2018). Statement of Financial Accounting Concepts No. 8, Qualitative Characteristics of Useful Financial Information. Financial Accounting Standard Board.

Freeman, R. (1984). Strategic Management: A Stakeholder Approach. New York: Cambridge University Press.

Friedman, M. (2007). The Social Responsibility of Business Is to Increase Its Profits. In Corporate Ethics and Corporate Governance, edited by W. C. Zimmerli, M. Holzinger, and K. Richter, 173– 178. New York, Springer.

Galant, A. and Cadez, S. (2017). ‘Corporate Social Responsibility and Financial Performance Relationship: A Review of Measurement Approaches,’ Economic Research-Ekonomska Istraživanja, 30(1), 676–693. Available at: https://doi.org/10.1080/1331677X.2017.1313122

Gao, S., Meng, F., Wang, W. and Chen, W. (2023). ‘Does ESG always improve corporate performance? Evidence from firm life cycle perspective,’ Frontiers in Environmental Science, 11, 1-14. Available at: https://doi.org/10.3389/fenvs.2023.1105077

Gillan, S. L., Koch, A. and Starks, L. T. (2021). ‘Firms and social responsibility: A review of ESG and CSR research in corporate finance,’ Journal of Corporate Finance, 66, https://doi.org/10.1016/j.jcorpfin.2021.101889

Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E. and Tatham, R. (2006). Multivariate data analysis . Uppersaddle River.

Huang, D. (2022). ‘Environmental, social and governance factors and assessing firm value: valuation, signalling and stakeholder perspectives,’ Accounting and Finance, 62(1), 1983–2010. Available at: https://doi.org/10.1111/acfi.12849.

Kalia, D. and Aggarwal, D. (2022). ‘Examining impact of ESG score on financial performance of healthcare companies,’ Journal of Global Responsibility, 14(1), 155-176.

Koundouri, P., Pittis, N. and Plataniotis, A. (2022). ‘The impact of ESG performance on the financial performance of European area companies: An empirical examination,’ Environmental Sciences Proceedings, 15(1), 1-11.

Lunawat, A. and Lunawat, D. (2022). ‘Do Environmental, Social, and Governance Performance Impact Firm Performance? Evidence from Indian Firms,’ Indonesian Journal of Sustainability Accounting and Management, 6(1), 133–146. Available at: https://doi.org/10.28992/ijsam.v6i1.519.

Neitzert, F. and Petras, M. (2022). ‘Corporate social responsibility and bank risk,’ Journal of Business Economics, 92(3), 397–428. Available at: https://doi.org/10.1007/s11573-021-01069-2.

Nerlove, M. and Wallis, K. (1966). Use of the Durbin-Watson statistic in inappropriate situations. Econometrica: Journal of the Econometric Society, 235–238.

Pu, G.(2023). ‘A non-linear assessment of ESG and firm performance relationship: evidence from China,’ Economic Research-Ekonomska Istraživanja, 36(1), 1-17. Available at: https://doi.org/10.1080/1331677X.2022.2113336

Ross, A. and Willson, V. (2017). Basic and Advanced Statistical Tests: Writing results sections and creating tables and figures. Springer. Available at: http://dx.doi.org/10.1007/978-94-6351-086-8

Sandberg, H., Alnoor, A. and Tiberius, V. (2022). ‘Environmental, social, and governance ratings and financial performance: Evidence from the European food industry,’ Business Strategy and the Environment, 32(4), 2471-2489. Available at: https://doi.org/10.1002/bse.3259.

Setiani, E. (2023). ‘The Impact of ESG Scores on Corporate Financial Performance: Moderating Role of Gender Diversity,’ Nominal Barometer Riset Akuntansi dan Manjemen, 12(1), 128-139.

Shakil, M. (2020). ‘Environmental, social and governance performance and stock price volatility: A moderating role of firm size,’ Journal of Public Affairs, 22(3), 1-11. Available at: https://doi.org/10.1002/pa.2574.

Sharma, P., Panday, P. and Dangwal, R. (2020). ‘Determinants of environmental, social and corporate governance (ESG) disclosure: a study of Indian companies,’ International Journal of Disclosure and Governance, 17(4), 208–217. Available at: https://doi.org/10.1057/s41310-020-00085-y.

Singh, A., Verma, S. and Shome, S. (2023). ‘ESG-CFP relationship: exploring the moderating role of financial slack,’ International Journal of Emerging Markets. Available at: https://doi.org/10.1108/IJOEM-03-2022-0536

Suttipun, M. and Yordudom, T. (2022). ‘Impact of environmental, social and governance disclosures on market reaction: an evidence of Top50 companies listed from Thailand,’ Journal of Financial Reporting and Accounting, 20(3/4), 753–767. Available at: https://doi.org/10.1108/JFRA-12-2020-0377.

Velte, P. (2017). ‘Does ESG performance have an impact on financial performance? Evidence from Germany,’ Journal of Global Responsibility, 8(2), 169-178.

Wong, K. (2017). ‘A literature review on environmental, social and governance reporting and it’s impact on financial performance,’ Austin J. Bus. Adm. Manag, 1(4), 1-4.

Zahid, R., Khan, M., Anwar, W. and Maqsood, U. (2022). ‘The role of audit quality in the ESG-corporate financial performance nexus: Empirical evidence from Western European companies,’ Borsa Istanbul Review, 22(2), 200-212.