1Abanoub Wassef, 2Ahmed Zamel, 1Ola I.S. El Dardery,

3Hosam Moubarak and 3Hebatallah Badawy

1Egypt-Japan University of Science and Technology (E-JUST), Alexandria, Egypt

2Egypt-Japan University of Science and Technology (E-JUST)/Faculty of Commerce,

Zagazig University, Cairo, Egypt

3Egypt-Japan University of Science and Technology (E-JUST)/Faculty of Business,

Alexandria University. Alexandria, Egypt

Volume 2024,

Article ID 196114,

Journal of Accounting and Auditing: Research & Practice,

14 pages,

DOI: https://doi.org/10.5171/2024.196114

Received date: 29 January 2024; Accepted date: 12 June 2024; Published date: 16 July 2024

Academic Editor: Hassan Younies

Cite this Article as:

Abanoub Wassef, Ahmed Zamel, Ola I.S. El Dardery, Hosam Moubarak and Hebatallah Badawy (2024), " Unraveling Determinants of Sustainable Growth in Egyptian Firms across the Firm Life Cycle", Journal of Accounting and Auditing: Research & Practice, Vol. 2024 (2024), Article ID 196114, https://doi.org/10.5171/2024.196114

This research investigates the determinants that shape the Sustainable Growth Rate (SGR) of non-financial firms listed on the Egyptian Stock Exchange (EGX) over a decade from 2012 to 2022. The study’s main determinants are profitability, asset efficiency, dividend policy, liquidity, and leverage. It further explores how these determinants evolve throughout the different stages of a firm’s life cycle. Findings from multiple regression models indicate that SGR is positively influenced by profitability and leverage, while dividend policy employs a negative effect. Interestingly, asset efficiency and liquidity do not have a significant impact on SGR. Upon examining these factors across the life cycle of a firm, profitability, and dividend policy consistently affect SGR. Asset efficiency becomes significant during the growth stage, and leverage during the maturity stage. However, liquidity does not significantly influence SGR at any stage of the life cycle. This study offers a unique insight into the determinants of SGR in the Egyptian context, highlighting their variability across different stages of a firm’s life cycle.

Keywords: Sustainable Growth Rate, Non-Financial Firms, Firm Life Cycle, Egypt.

Introduction

For decades, profit generation has traditionally been the primary goal of firms; the focus has shifted towards sustainable growth, a measure of a company’s ability to manage resources, make informed decisions, and plan financially (Madbouly, 2022). The concept of Sustainable Growth Rate (SGR), introduced by Robert Higgins in 1977, is defined as the maximum growth rate a company can achieve without depleting its financial resources. It aligns with the company’s financial strategies and serves as a crucial metric for evaluating profitability performance (Ramli et al., 2022).

This research tries to fill out the gap in firm sustainability literature where there is little research that focuses on the firm’s sustainability, especially over their life cycle different stages. This research is in alignment with the United Nations’ 2030 Agenda, more specifically, Goal 8, which advocates for the promotion of inclusive and sustainable economic growth. Madbouly’s (2022) research, focusing on Egypt, investigates the relationship between the SGR and several accounting aspects of firm performance, including profitability, size, leverage, liquidity, and operational efficiency. This research serves as a motivation for our study to further examine other determinants like dividend policy on SGR and to investigate whether these determinants fluctuate from one stage to another. Moreover, it aims to broaden the scope by analyzing a larger sample of Egyptian firms over an extended period.

The purpose of this paper is to analyze the determinants (profitability, asset efficiency, dividend policy, liquidity, and leverage) of the SGR of non-financial firms listed on the Egyptian Stock Exchange (EGX) between 2012 and 2022. In addition, this study aims to investigate how these determinants differ across the different stages of a firm’s life cycle.

The importance of this research lies in its comprehensive examination of the determinants of a company’s SGR. It further assesses how these determinants will differ according to the firm life cycle stages. The study offers valuable insights by focusing on the determinants of a firm’s sustainable growth in a developing country, Egypt, over eleven years from 2012 to 2022.

The study was carried out with 923 observations of firm-years from non-financial companies listed on the EGX, spanning the years 2012 to 2022. The study found a positive correlation between SGR and both profitability and leverage, but a negative correlation with dividend policy. The study also concluded that asset efficiency and liquidity have no significant influence on SGR. The study discovered that the influence of these determinants varies depending on the stage of the firm’s life cycle. Profitability and dividend policy are crucial for SGR throughout all stages of the firm’s life cycle, while asset efficiency is significant during the growth stage, and leverage during the maturity stage. Liquidity does not significantly impact SGR at any life cycle stage. These conclusions will have potential interests for policymakers, company managers, investors, and researchers working in sustainability and the determinants of firm sustainable growth.

To achieve the research objective, the paper will be structured as follows. In Section 2, we will examine previous literature about the determinants of sustainable growth and how they differ across different stages of a firm’s life cycle and develop the research hypotheses. In Section 3, we will present the research methodology, variables, and their measurements. Section 4 will discuss the empirical findings. Finally, in Section 5, we will conclude and provide recommendations and implications for future research.

Literature Review And Hypotheses Development

Sustainable Growth Rate (SGR)

Sustainable Growth Rate (SGR), as defined by Higgins (1977), is the maximum growth rate a company can achieve without depleting its financial resources. The SGR model is a valuable tool for aligning financial, operational, and growth strategies. Lockwood and Prombutr (2010) describe SGR as a complex measure integrating operational elements like profit margin and asset efficiency with financial factors such as capital structure and retention ratio. Altahtamouni et al. (2022) emphasize the importance of SGR in decision-making, with factors like profitability, asset efficiency, and liquidity shaping a company’s ability to sustain growth.

Profitability and Sustainable Growth Rate

A company’s ability to sustain itself over time is closely linked to its profitability. To improve their profitability, companies need to continuously expand their operations. Efficient management of assets is demonstrated by a high return on assets, but an excessively high return may indicate underutilization of assets. If the return on assets does not match the SGR, it can create challenges for the business.

Studies indicate a correlation between a company’s profitability and its SGR. Sahin and Ergun (2018) found a negative correlation between SGR and profitability indicators. Nastiti et al. (2019) revealed that efficient working capital management indirectly influences sustainable growth through profitability. Manullang and Hutabarat (2020) and Vuković et al. (2022) both found that an increase in SGR enhances a firm’s earnings and sustainable growth.

Based on the previous discussion, the first research hypothesis (H1) will be developed as follows:

H1: Firm profitability has a positive significant impact on firm sustainable growth.

Asset Efficiency and Sustainable Growth Rate

Efficient asset management is crucial for achieving strategic objectives, maintaining funding streams, and supporting sustained growth. Operational efficiency measures well the company’s ability to achieve sustainable growth, as it measures how effectively a company utilizes its resources. It acts as a key determinant of a company’s revenue-generating ability (Vuković et al., 2022). In general, a higher asset turnover ratio indicates an enhanced financial standing for the firm. Essentially, a robust asset turnover ratio indicates the company’s expertise in generating income from each dollar invested in its assets.

The study by Rahim (2017) found that higher net asset turnover positively influences SGR by improving sales’ efficiency. In contrast, Vasiu & Ilie (2018) found that higher asset utilization, leading to increased revenue, negatively impacts SGR in Romanian firms. Mamilla et al. (2019) found an inverse correlation between asset efficiency and SGR in Indian oil refinery companies. These studies highlight the complex relationship between asset management and SGR.

Based on the previous discussion, the third research hypothesis (H2) will be developed as follows:

H2: Asset efficiency has a positive significant impact on firm sustainable growth.

Dividend Policy and Sustainable Growth Rate

The dividend policy refers to how a company distributes its earnings between dividends and investments. This decision significantly influences a firm’s growth potential. When a corporation generates profits, it can distribute a portion as dividends to its shareholders, while the remaining funds, known as retained earnings, are earmarked for future reinvestment (Nguyen et al., 2021). Reinvesting a smaller proportion of profits in operations leads to high dividend payments, which can limit a company’s growth and expansion initiatives.

To my knowledge, there is a shortage of studies that investigate the relation between dividend policy and SGR. Hartono and Utami (2016) investigated the impact of a company’s SGR on financial indicators within the Indonesia Stock Exchange, revealing an insignificant negative effect on the price-to-earnings ratio. Ramli et al. (2022) explored the role of SGR as a mediator in the correlation between firm-specific factors and share price performance in Sharia-compliant companies in Malaysia. The study found a significant connection between SGR and share price, with a negative correlation between dividend policy and SGR.

Based on the previous discussion, the fourth research hypothesis (H3) will be developed as follows:

H3: Dividend policy has a negative significant impact on firm sustainable growth.

Liquidity And Sustainable Growth Rate

Ensuring ideal liquidity is fundamental for enabling a company to meet short-term obligations efficiently. The extent of liquidity assessed by current assets with short-term liabilities directly shapes sustainable growth, where sufficient available assets required to meet immediate financial obligations play a pivotal role in ensuring a company’s continued prosperity (Vuković et al., 2018). Essentially, having the right amount of liquidity, where current assets exceed short-term liabilities, plays a critical role in a company’s ability to manage its long-run debt and facilitates its sustainable growth in a significant way.

Research on the relationship between a firm’s liquidity and SGR has yielded mixed results. Amouzesh et al. (2011) and Madbouly (2022) found no significant relationship between Iranian and Egyptian firms, respectively. However, Hartono and Utami (2016) found a positive but insignificant effect of SGR on the current ratio in Indonesian firms. Lim and Rokhim (2021) found a strong positive correlation between liquidity and SGR in Indonesian pharmaceutical companies, suggesting that more liquid assets can support sustainable growth and improved financial performance.

Based on the previous discussion, the second research hypothesis (H4) will be developed as follows:

H4: The firm Liquidity has a positive significant impact on the firm sustainable growth.

Financial Leverage And Sustainable Growth Rate

Financial leverage is a measure of how much a company’s investments rely on borrowed funds. It can serve as a rough measure of a firm’s ability to obtain funding from outside sources (Vuković et al., 2020). In the context of a firm’s financial structure, investments can be funded through various means, including debt, equity, and preference shares.

Nevertheless, it’s important to highlight that given the inherent risk and unpredictability linked with businesses, their capacity to fulfill obligations significantly influences their financial health and survival. In the relationship between financial leverage and SGR, it’s seen that financial leverage can act as a stimulant for growth if it’s managed effectively to maintain the firm’s sustainability. This is particularly relevant for firms’ functioning in risky scenarios.

Investigations into the link between financial leverage and SGR have produced diverse outcomes. Alayemi and Akintoye (2014) observed a negative yet insignificant influence of capital structure on SGR in firms in Sub-Saharan Africa. Vuković et al. (2022) determined that financial leverage adversely impacts the SGR of companies that pay dividends in Eastern Europe. Conversely, Rahim (2017) identified a positive association between financial leverage and SGR, while Mumu et al. (2019) reported a negative effect in Indonesian firms. Madbouly (2022) found a positive relationship between financial leverage and SGR in Egyptian firms. These findings underscore the multifaceted and inconsistent relationship between financial leverage and SGR.

Based on the previous discussion, the fifth research hypothesis (H5) will be developed as follows:

H5: Financial leverage has a positive significant impact on firm sustainable growth.

Firm Life Cycle Stages

The Corporate Life Cycle theory, proposed by Chandler (1962) and expanded by Mueller (1972), likens organizations to living organisms progressing through life cycle stages. These stages of growth, maturity, and decline involve significant changes in resources, structure, and capital needs. Each stage presents unique opportunities and challenges, illustrating the dynamic evolution of firms over time.

Moreover, Dickinson (2011) proposes a cyclical approach to assess a firm’s life cycle stages using cash flow patterns. This method offers a holistic view of the company’s financial status, considering factors like firm age, sales growth, and flexibility. It also reflects the company’s position within the business cycle accurately. The Corporate Life Cycle theory suggests that companies progress through distinct stages: introduction, growth, maturity, shake-out, and decline. Each with unique financial characteristics and challenges.

The Introduction stage is marked by high risk and limited assets, often leading to lower profit margins (Jovanic, 1982; Dickinson, 2011). The Growth phase sees increased profitability, sales volume, and a reduction in debt ratio (Bulan & Yan, 2009; Habib, 2010). The Maturity stage is characterized by stable profits, cash flow, and higher dividends, indicating improved financial stability (DeAngelo et al., 2010; Habib & Hasan, 2019). The Shake-out stage involves identifying new growth avenues as growth rates decelerate (Dickinson, 2011). Finally, the Decline phase may involve decreased profit margins, revenue volume, and dividends due to unexpected circumstances.

Based on the previous discussion, the sixth research hypothesis (H6) will be developed as follows:

H6: Determinants of firm sustainable growth will differ according to the firm life cycle stage.

Research Methodology and Design

The author will outline the methodology of the research, the procedures for selecting the sample, the measurement of independent and dependent variables utilized in the study, and the development of the research models.

Sample And Data Collection

The research methodology for this study depends on a sample of non-financial firms listed on the Egyptian Exchange (EGX). The study excludes financial firms due to their unique nature and specific regulatory requirements. The focus of the study is to explore the impact of various determinants on the sustainable growth of firms, with a special emphasis on identifying the most influential determinant. Additionally, the study seeks to investigate whether the determinants of

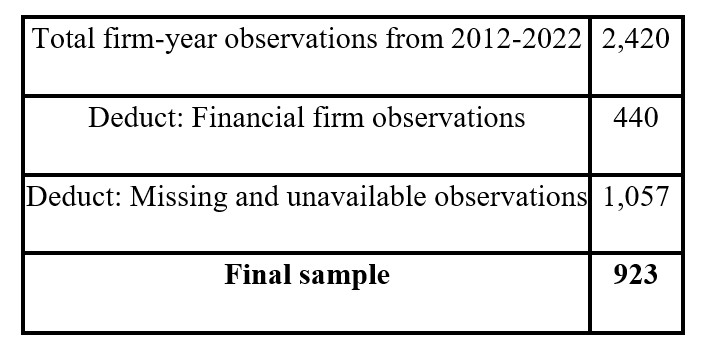

SGR differ across various stages of a firm’s life cycle. For this purpose, we divided the entire sample into five subsamples based on the firm life cycle stages, following Dickinson’s (2011) classification of life cycles using their cash flow matrix. This empirical study relies on secondary data obtained from the Bloomberg Database for the period between 2012 and 2022. To prove our research hypotheses, we will employ multiple regression analysis. This statistical method will be executed using the most recent versions of the SPSS software package. After eliminating observations with missing data, the concluding sample size reached 923 firm-year observations (as shown in Table 1).

Table (1): Sample selection procedure

Empirical Model

To investigate the determinants of firm sustainable growth and to examine if these determinants of SGR vary at different stages of a firm’s life cycle, the following multiple regression model is developed:

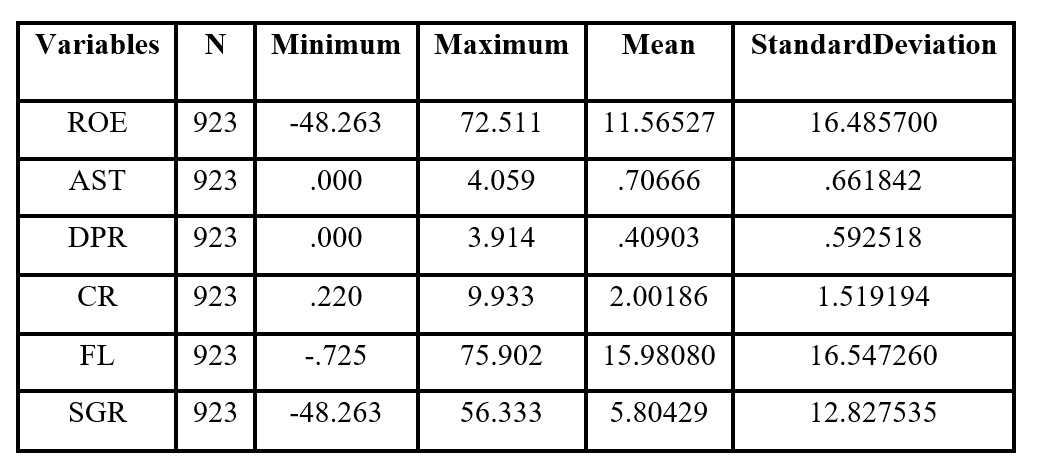

In Table 3, the descriptive statistics of the study variables are presented. The SGR reveals a mean value of 5.80429 and a standard deviation of 12.827535. Meanwhile, the profitability level mean is 11.56527, with a standard deviation of 16.485700. Asset efficiency in Egyptian firms averages approximately 70.666%, with a standard deviation of 0.661842. Moreover, Egyptian firms allocate around 40.903% of their earnings as dividends, with a standard deviation of 0.592518. The mean liquidity level of Egyptian firms stands at 2.00186 with a standard deviation of 1.519194, while the average leverage level is 15.98080 with a standard deviation of 16.547260.

Table (3): Descriptive statistics

Correlation Analysis

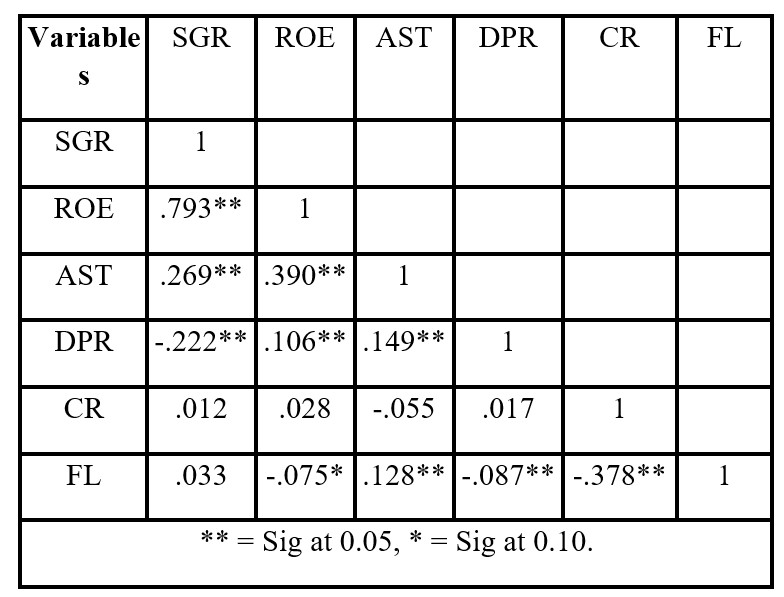

From the data presented in Table 4, it can be initially concluded that there is a significant and positive correlation between SGR and profitability. Similarly, asset efficiency also shows a positive and significant association with SGR. In contrast, the dividend policy appears to have a negative correlation with SGR. Liquidity and financial leverage, while positively correlated with SGR, do not show significant associations. Furthermore, the maximum correlation observed is 39%, and considering the Variance Inflation Factor (VIF) values in the following section, it can be deduced that multicollinearity is not likely to influence the regression results.

Table (4): Pearson correlations between dependent and independent variable

Hypotheses Testing

Testing H1

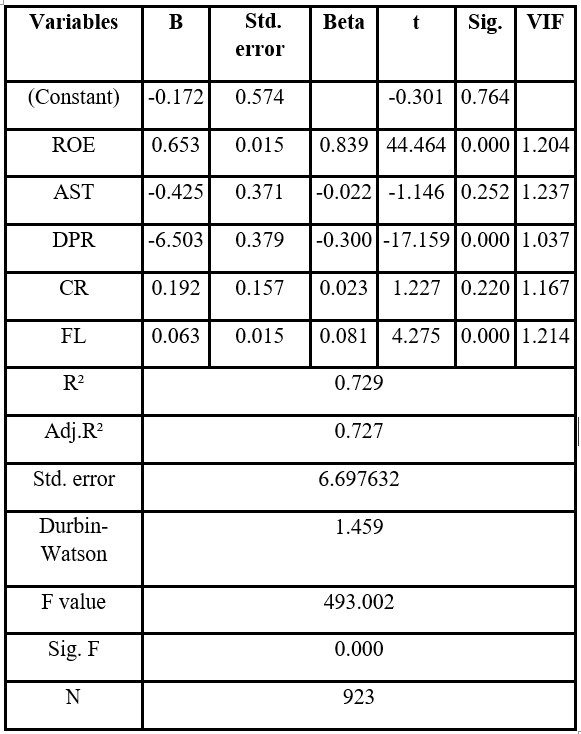

The outcomes of the multiple regression model, which examines SGR and the determinants of sustainable growth in firms (profitability, asset efficiency, dividends policy, liquidity, and leverage) using SPSS, are presented in Table (5). The Model Summary reveals the model’s significance (Sig.=.000), thereby validating the overall model, with an R² value of .729 and an adjusted R² value of .727.

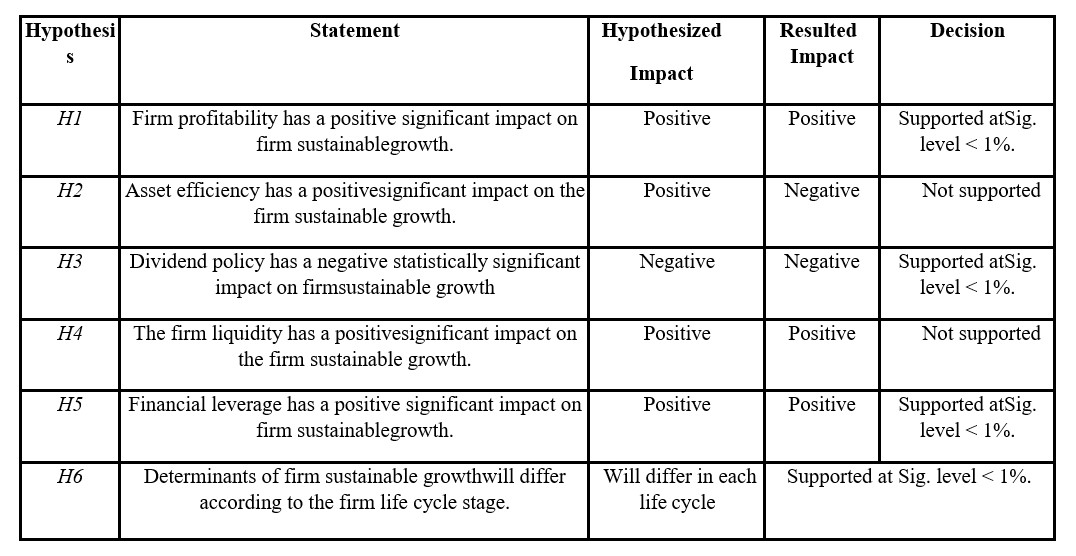

Based on the below table results, the empirical evidence of our first hypothesis suggests that profitability has a positive significant effect on SGR (t =44.464, Sig.= .000). This observation aligns with previous research findings conducted by Amouzesh et al. (2011), Alayemi and Akintoye (2014), Ramli et al. (2022), Madbouly (2022), and Vuković et al. (2022) that confirm that a rise in profitability leads to an increase in sustainable growth. This finding highlights that Egyptian companies aiming for high sustainable growth should focus on earning high profits. Consequently, the first hypothesis (H1) which stated that “Firm profitability has a positive significant impact on firm sustainable growth” is supported.

Testing H2

Asset efficiency suggests a negative and statistically insignificant impact on SGR (t =-1.146, Sig. = .252). This result is similar to Ramli et al. (2022), and Vuković et al. (2022). Conversely, the findings of Madbouly (2022) contradict our results. Even though Madbouly’s research was carried out in Egypt from 2015 to 2019, the inconsistency with our findings could be justified by the difference in the number of observations made, the duration of the study, and the method of measuring asset efficiency. Furthermore, our results contrast with those of Mamilla et al. (2019), who found a significant negative impact on asset efficiency, and Rahim (2017), who reported a significant positive influence of asset efficiency on SGR. In the context of the Egyptian business environment, our research suggests that asset management does not significantly influence the sustainability of firm growth. We propose that asset efficiency is not essential for maintaining sustainable growth. Furthermore, it appears that Egyptian corporations do not prioritize asset management efficiency as a key strategy for ensuring sustainable growth. Accordingly, the second hypothesis (H2) which stated that “Asset efficiency has a positive significant impact on firm sustainable growth” is not supported.

Testing H3

Our study indicates that the dividend policy, as represented by the payout ratio, has a negative and statistically significant influence on SGR (t = -17.159, Sig. =.000). This finding is consistent with previous research findings conducted by Ramli et al. (2022). Companies that are experiencing or expecting high growth rates often aim to decrease dividend payments to avoid the need for external financing (Gill et al.,2010). We propose that Egyptian firms that distribute higher dividends subsequently reduce the proportion of earnings allocated for reinvestment in their assets, which is crucial for maintaining their operational cycle. This strategy could potentially limit the firm’s future growth opportunities and operational efficiency, as reinvestment plays a critical role in business expansion and sustainability. Therefore, achieving a balance between dividend payouts and reinvestment is key for firms to ensure sustainable growth. Thus, the third hypothesis (H3) which stated that “Dividend Policy has a negative significant impact on firm sustainable growth” is supported.

Testing H4

Moving on, our fourth hypothesis discovered that liquidity has a positive but statistically insignificant effect on SGR (t=1.227, Sig. = .220). This finding aligns with the results of Amouzesh et al. (2011), Mamilla et al. (2019), and Madbouly (2022). However, it contradicts the findings of Rahim (2017) who found that liquidity has an insignificant negative impact on SGR, and Vuković et al. (2022) who observed a significant negative effect of liquidity on SGR. Therefore, the fourth hypothesis (H4) which stated that “The firm Liquidity has a positive significant impact on the firm sustainable growth” is not supported.

Testing H5

Our fifth hypothesis uncovered that leverage has a positive and statistically significant effect on SGR (t=4.275, Sig. = .000). This result is consistent with the findings of Fonseka et al. (2012), Rahim (2017), and Madbouly (2022). Conversely, studies by Mumu et al. (2019) and Vuković et al. (2022) reported a significant negative effect of financial leverage on SGR. Meanwhile, Alayemi and Akintoye (2014) observed a negative statistically insignificant impact of capital structure on SGR. Hence, the fifth hypothesis (H5) which stated that “Financial leverage has a positive significant impact on firm sustainable growth.” is supported.

Table (5): Multiple regression results Model between SGR and its determinants

Testing H6

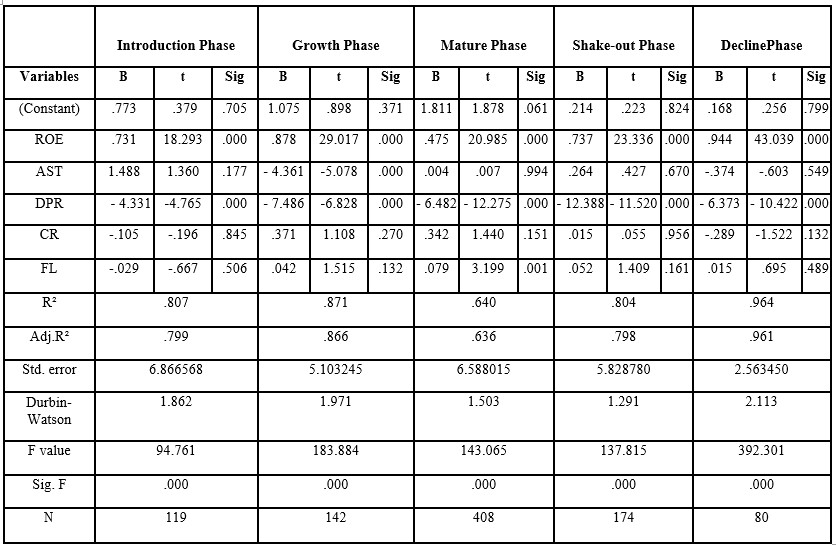

In this section, we examine the findings of our regression model that studies SGR and the factors contributing to sustainable growth in Egyptian firms (profitability, asset efficiency, dividends policy, liquidity, and leverage) throughout the 5 phases of a firm’s life cycle. The analysis is based on the primary regression model, which categorizes the examined Egyptian firms according to their life cycle stage. This categorization is achieved using Dickinson’s 2011 cash flow formula, which employs three types of cash flows: cash from operations, cash from investments, and cash from financing to classify a firm’s life cycle into five stages: introduction, growth, maturity, shake-out, and decline. These cash flows can be either positive or negative, resulting in eight potential combinations. Each combination signifies a unique status of the company.

During the introduction stage, the model’s significance is fulfilled (Sig.=.000), thus confirming the model’s overall validity, with an R² value of .807 and an adjusted R² value of .799. The data reveal a positive and statistically significant influence of profitability on SGR (t =18.293, Sig. = .000). t). This finding is along with our previous research findings of a statistically negative substantial effect of dividend policy on the sustainable growth of Egyptian firms in the introduction phase (t =- 4.765, Sig. = .000).

In the Growth stage, the findings validate the model’s significance (Sig.=.000), thereby verifying the model’s overall reliability, with an R² value of .871 and an adjusted R² value of .866. The findings show a positive statistically significant effect of profitability on SGR (t =29.017, Sig. = .000). Conversely, both dividend policy (t=-6.828, Sig. = .000) and asset efficiency (t =-5.078, Sig. = .000) have a negative and statistically significant influence on the SGR of Egyptian firms during the growth phase.

Moving through the mature stage, the regression outputs validate the model’s significance (Sig.=.000), thereby verifying the model’s overall reliability, with an R² value of .640 and an adjusted R² value of .636. The findings show a positive statistically significant impact of profitability on SGR (t =20.985, Sig. = .000). Conversely, both dividend policy (t =-12.275, Sig. = .000) and financial leverage (t =- 3.199, Sig. = .000) have a negative significant influence on the SGR of Egyptian firms during the third phase.

In the fourth stage, the model’s significance, indicated by Sig.=.000, confirms its reliability with an R² value of .804 and an adjusted R² value of .798. Particularly, profitability displays a robust and positive impact on SGR (t = 23.336, Sig. = .000). Conversely, dividend policy significantly affects SGR negatively (t = -11.520, Sig. =.000).

In the final stage, the model summary confirms the model’s significance (Sig.=.000), thereby supporting the model’s overall reliability, with an R² value of .964 and an adjusted R² value of .961. Similar to the previous stage, profitability continues to exhibit a strong and positive influence on SGR (t = 43.039, Sig. = .000) and a significant negative impact of dividend policy on SGR (t = -10.422, Sig. =.000).

Table (6): Multiple regression results model between SGR and its determinants over FLC stages

Based on the above findings, the determinants influencing SGR in Egyptian firms shift at each stage of the firm’s life cycle. Profitability and the dividend policy consistently have a significant influence across all stages of the firm’s life cycle. Meanwhile, asset efficiency is significant during the growth stage, and leverage is significant during the mature stage. However, liquidity does not seem to influence the SGR at any stage of the firm’s life cycle. Therefore, the sixth hypothesis (H6) which stated that “Determinants of firm sustainable growth will differ according to the firm life cycle stage” is supported.

In Table 7, we provide a summary of our research hypotheses, their results, and our decisions concerning whether these hypotheses are supported or not.

Table (7): Research hypotheses summary

Additional Analysis

For further analysis in our research, we categorized the firms into two subsets: profitable (assigned a dummy variable value of 1) and non-profitable (assigned a dummy variable value of 0). This categorization was based on their net income from 2012 to 2022. Our findings indicate that the factors contributing to sustainable growth remain relatively consistent, irrespective of the profitability status of the firms.

Profitable firms mirrored the results of the original regression model. Where, Profitability (t= 30.121, Sig. = 000), Dividend policy (t= 6.914, Sig. =.000), and leverage (t= 1.613, Sig. =.109) have a statistically positive, negative, and positive impact respectively. These findings underscore the consistency of these determinants in influencing sustainable growth across different firm profiles.

For non-profitable firms, the model’s significance (Sig.=.000) validates the overall model, with an R² value of .889 and an adjusted R² value of .885. Profitability (t= 30.121, Sig. = 000) and Dividend policy (t= 6.914, Sig. =.000) were found to be statistically significant, exerting a positive and negative impact respectively. Additionally, leverage showed a slight statistically significant positive effect (t= 1.613, Sig. =.109). These findings align with the initial results of our research.

Conclusion And Research Implications

This study examined the determinants influencing the SGR of non-financial firms in Egypt from 2012 to 2022. It found that SGR is positively correlated with profitability and leverage, negatively correlated with the dividend policy, and unaffected by asset efficiency and liquidity. These effects vary across the firm’s life cycle. Additional analysis revealed that for both profitable and non-profitable firms, SGR is positively correlated with profitability and negatively correlated with dividend policy. The study underscores the importance of understanding these determinants in the context of a firm’s profitability status and life cycle stage.

The researchers recommend that regulators, corporate managers, and investors focus on the determinants that ensure sustainability in Egyptian companies. They emphasize the importance of understanding these factors across different life cycle stages to optimize sustainable growth, particularly in terms of profitability and dividend distribution. By incorporating these determinants into strategic planning and decision-making, firms can enhance sustainable growth, improve financial performance, and ensure long-term sustainability. This research is a valuable resource for those aiming to achieve sustainable growth in their organizations.

This research does have some limitations. Firstly, the study focuses only on non-financial firms in Egypt, a developing country, from 2012 to 2022. Therefore, the findings may not be applicable to developed countries or even other developing countries due to variations in market conditions. Secondly, our research selected specific determinants for measuring their impact on SGR. Future research could consider additional determinants related to corporate governance or macro-level factors such as national GDP, tax rate, or inflation rate and change the measurements used to evaluate those determinants. Lastly, the lack of financial data for Egyptian firms, even in large datasets like Bloomberg, stands as a challenge. The study was conducted on 161 firms and only 923 firm-year observations out of a potential 2420, indicating that more than half of the data is either unavailable or missing.

The authors propose that further research could investigate additional determinants of SGR, such as ESG, investment efficiency, share price performance, various types of ownerships, and various aspects of corporate governance such as the board of audit committee, directors’ characteristics, and CSR committee, within the context of Egyptian firms. It would be insightful to conduct future studies focusing on a comparative analysis of SGR determinants in developing countries, specifically comparing Egypt and Saudi Arabia due to their similar market conditions. Moreover, a comparative study of SGR determinants between developed and developing countries could reveal whether these determinants vary in different economic contexts. Understanding these determinants could assist in devising effective growth strategies and making informed investment decisions. The authors suggest that future studies could explore alternative measurements of SGR, such as the Van Horne model. Additionally, for measuring the firm’s life cycle, researchers could consider retained earnings scaled by total assets or total equity to determine the stages of a firm’s life cycle as proposed by DeAngelo et al. (2006).

References

Ahmed, B., Akbar, M., Sabahat, T., Ali, S., Hussain, A., Akbar, A., & Hongming, X. (2021) ‘Does firm life cycle impact corporate investment efficiency?’, Sustainability, 13 (1), 197.

Alayemi, S.A., & Akintoye, R.I. (2014) ‘Strategic Management of Growth in Manufacturing Companies in Sub-Saharan Africa: A Case Study of Nigeria’, Journal of Economics, Management and Trade, 6(2), 151–160. [Online]. Available: https://doi.org/10.9734/BJEMT/2015/13796

Altahtamouni, F., Alfayhani, A., Qazaq, A., Alkhalifah, A., Masfer, H., Almutawa, R., & Alyousef, S. (2022) ‘Sustainable Growth Rate and ROE Analysis: An Applied Study on Saudi Banks Using the PRAT Mzodel’, Economies, 10(3), 70-91. [Online]. Available: https://doi.org/10.3390/economies10030070

Amouzesh, N., Zahra, M., & Zahra, M. (2011) ‘Sustainable Growth Rate and Firm Performance: Evidence from Iran Stock Exchange’, International Journal of Business and Social Science, 2(23), 249–255.

Arora, L., Kumar, S., & Verma, P. (2018) ‘The Anatomy of Sustainable Growth Rate of Indian Manufacturing Firms’, Global Business Review, 19, 1050–1071.

Badawy, H. (2020) ‘Audit Committee Effectiveness and Corporate Sustainable Growth: The Case of Egypt’, Alexandria Journal of Accounting Research, 4(2). [Online]. Available: https://ssrn.com/abstract=3780978

Bulan, L.T., & Yan, Z. (2009) ‘The pecking order theory and the firm’s life cycle’, Banking and Finance Letters, 1(3), 1-16.

Chandler, A.D. (1962) ‘Strategy and Structure: Chapters in the History of American Enterprise’, MIT Press, Boston.

DeAngelo, H., DeAngelo, L. & Stulz, R.M. (2010) ‘Seasoned equity offerings, market timing, and the corporate lifecycle’, Journal of Financial Economics, 95(2), 275-295.

DeAngelo, H., DeAngelo, L. and Stulz, R.M. (2006) ‘Dividend policy and the earned/contributed capital mix: a test of the life-cycle theory’, Journal of Financial Economics, 81(2), 227-254.

Detthamrong, U., Chancharat, N. & Vithessonthi, C. (2017) ‘Corporate Governance, Capital Structure and Firm Performance: Evidence from Thailand’, Research in International Business and Finance, 42, 689-709.

Dickinson, V. (2011) ‘Cash flow patterns as a proxy for firm life cycle’, The Accounting Review, 86(6), 1969-1994.

El Madbouly, D. (2022) ‘Factors affecting the Sustainable Growth Rate and its impact on Firm Value: Empirical Evidence from the Egyptian Stock Exchange’, Journal of Accounting and Auditing of the Association of Arab Universities, 11(1), 1-40.

Gill, A., Biger, N. & Tibrewala, R. (2010) ‘Determinants of dividend payout ratios: evidence from the United States’, Open Business Journal, 3, 8–14.

Habib, A. (2010) ‘Value relevance of alternative accounting performance measures: Australian evidence’, Accounting Research Journal, 23(2), 190-212.

Hartono, G.C. & Utami, S.R. (2016) ‘The comparison of sustainable growth rate, firm’s performance, and value among the firms in Sri Kehati index and IDX30 index in Indonesia stock exchange’, International Journal of Advanced Research in Management Growth Rate, 284284(5), 68–81.

Higgins, R.C. (1977) ‘How much growth can a firm afford?’, Financial Management, 6(3), 7-16.

Jovanic, B. (1982) ‘Selection and the Evolution of Industry’, Econometrica, 50(3), 649–670.

Lim, H. & Rokhim, R. (2020) ‘Factors affecting profitability of pharmaceutical company: Indonesian evidence’, Journal of Economic Studies, 48(5), 981-995. [Online]. Available: https://doi.org/10.1108/JES-01-2020-0021.

Lockwood, L. & Prombutr, W. (2010) ‘Sustainable growth and stock returns’, Journal of Financial Research, 33(4), 519–538.

Lyroudi, K. (2018) ‘Do financial ratios affect stock returns in the Athens stock exchange?’, Economic Alternatives, 1(4), 497–516.

Mamilla, R. (2019) ‘A study on sustainable growth rate for firm survival’, Strategic Change, 28(4), 273–277. [Online]. Available: https://doi.org/10.1002/jsc.2269.

Manullang, S.V. & Hutabarat, F. (2020) ‘The Effect of Sustainable Growth and Liquidity on the Profitability of Mining Sector Companies in Indonesia Stock Exchange In 2018’, Akuntansi Dan Sistem Informasi, 5(1), 24–29.

Mueller, D.C. (1972) ‘A life cycle theory of the firm’, The Journal of Industrial Economics, 20(3), 199-219.

Mumu, S., Susanto, S. & Gainau, P. (2019) ‘The Sustainable Growth Rate and The Firm Performance: Case Study of Issuer at Indonesia Stock Exchange’, International journal of Management, IT and Engineering, 9(12).

Nastiti, P., Atahau, A. & Supramono, 2019. ‘Working capital management and its influence on profitability and sustainable growth’, Business: Theory and Practice, 20(4), 61–68.

Nguyen, A. H., Pham, C. D., Doan, N. T., Ta, T. T., Nguyen, H. T., & Truong, T. V. (2021) ‘The Effect of Dividend Payment on Firm’s Financial Performance: An Empirical Study of Vietnam’, Journal of Risk and Financial Management, 14(8), 353. [Online]. Available: https://doi.org/10.3390/jrfm14080353.

Obradovich, J. & Gill, A. (2013) ‘The impact of corporate governance and financial leverage on the value of American firms’, International Research Journal of Finance and Economics, 91, 1–14.

Pratama, A.A.P. (2019) ‘Liquidity and Asset Quality on Sustainable Growth Rate of Banking Sector’, International Journal of Scientific Research, 8, 125–128.

Rahim, N. (2017) ‘Sustainable growth rate and firm performance: A Case study in Malaysia’, International Journal of Management, Innovation & Entrepreneurial Research, 3(2), 48-60.

Ramli, N. A., Rahim, N., Nor, F. M., & Marzuki, A. (2022) ‘The mediating effects of sustainable growth rate: evidence from the perspective of Shariah-compliant companies’, Cogent Business & Management, 9(1). [Online]. Available: https://doi.org/10.1080/23311975.2022.2078131.

Sahin, A. and Ergun, B. (2018) ‘Financial sustainable growth rate and financial ratios: a research on Borsa Istanbul manufacturing firms’, Journal of Business Research Türk, 10, 172-197.

Singh, R., Gupta, C.P. and Chaudhary, P. (2023) ‘Dividend policy and corporate life cycle: a study of Indian companies’, Managerial Finance, 49(11), 1722-1749.

Vasiu, D.E. and Ilie, L. (2018) ‘Sustainable growth rate: an analysis regarding the most traded companies on the Bucharest Stock Exchange’, In: S. Marginean, C. Ogrean and R. Orastean, eds., Emerging Issues in the Global Economy. Cham: Springer, pp.447-457.

Vuković, B., Milutinovic, S., Milicevic, N. and Jaksic, D. (2020) ‘Corporate bankruptcy prediction: evidence from wholesale companies in the Western European countries’, Ekonomska Casopis, 68, 477-498.

Vuković, B., Pestovic, K., Mirovic, V., Jaksic, D. and Milutinovic, S. (2022) ‘The analysis of company growth determinants based on financial statements of the European companies’, Sustainability, 14, 770.

Vuković, B., Tica, T. & Jaksic, D. (2022) ‘Sustainable growth rate analysis in Eastern European companies’, Sustainability, 14(17), 10731.

Wahjudi, E. (2020) ‘Factors affecting dividend policy in manufacturing companies in Indonesia Stock Exchange’, Journal of Management Development, 39(1), 4-17.