1Maria-Mădălina BOGEANU-POPA, 1Mariana MAN and 2Carmen-Florentina PAUNESCU

1Faculty of Sciences, Department of Economic Sciences, University of Petroșani, Petrosani, Romania

2Doctoral School of Economics, University of Craiova, Craiova, Romania

Volume 2024,

Article ID 675311,

Journal of Accounting and Auditing: Research & Practice,

16 pages,

DOI: https://doi.org/10.5171/2024.675311

Received date: 8 March 2024; Accepted date: 5 June 2024; Published date: 10 July 2024

Academic Editor: Dean Učkar

Cite this Article as:

Maria-Mădălina BOGEANU-POPA, Mariana MAN and Carmen-Florentina PAUNESCU (2024), " Examining the Interplay of Social and Financial Metrics: Case Study of the Retail Sector", Journal of Accounting and Auditing: Research & Practice, Vol. 2024 (2024), Article ID 675311, https://doi.org/10.5171/2024.675311

In this paper, the way in which social performance, which is increasingly present in the evaluation of the activity of organizations, has an impact on their financial performance was studied. Social performance and financial performance are seen as a necessity when we assess the economic performance of an organization. For this, notions such as growth, profitability, productivity, yield and social and environmental competitiveness are used. The case study focused on the retail sector, which has experienced accelerated development in recent years. Social information and financial information were collected from the annual reports of retail organizations to be able to use social and environmental performance indicators (Ips) and financial performance indicators (Ips). In the research to establish the link between Ips and Ipf, descriptive statistics analysis and the Hausman test regression model were used. The results of the research revealed that social performance positively influences financial performance in organizations operating in the retail sector.

Keywords: social performance, financial performance, retail, sustainable development, CSR.

Introduction

Ever-so present today, the concept of sustainable development refers to taking into consideration protecting, supporting, and improving the human, natural, and financial capital of the organizations. Adopting this organizational behavior involves a long-term approach and perspective. In other words, sustainable development implies a convergence between three fundamental pylons which define its content: economic development, social equity and environment protection (Eccles and Serafeim, 2017). The policy of sustainable development includes actions of social responsibility of an organization (CSR). Thus, the conduct of the organizations which have adopted CSR principles are in consensus with the exigencies of sustainable development (Fourati and Dammak, 2020). Therefore, an enterprise is considered responsible if it reports its social, economic, and environmental performances in a systematic manner to interested parties concerning relevant information regarding the impact of its activities on these three spheres (Bogeanu-Popa and Man, 2023). Given the wide spread of adopting sustainable development through CSR, there is the matter of justifying these aspects on a financial level. Do CSR-aware organizations perform better socially or financially? (Busco and Sofra, 2021).

The appearance and evolution of the performance concept in general has been met with remarkable development. The definitions of performance referred to financial type measures being analyzed through the difference between expenses and income generated by the economic activity (Busco and Sofra, 2021). After the ‘50s and up until the beginning of the ‘90s, other analyses have been used such as the quality and benefits offered to every interested party (Eccles and Serafeim, 2017). These days the concept of performance has been developed even more by evolving towards a global approach. Now, this concept includes financial aspects (expenses and income from the economic activity) as well as aspects of non-financial nature (expenses and income from the social and environmental activity). The majority of aspects of non-financial nature refer to elements of social responsibility (CSR).

The relationship between performance and social responsibility is underlined by the identification of a balancing scheme of the financial and operational indicators in order to evaluate the organization’s performance. Some authors consider that the organization that is able to become socially responsible determines a positive perception on stakeholders (Rupley, Brown, Marshall, 2017 and Argento, Culasso, Truant, 2019). Seen in the opposite direction, a financially strong organization will have the possibility to spend more for socially responsible activities. Inevitably, this fact determines profit growth during its development. One can say that the relationship between the two performances of the organization can be framed on a circular ascending line. A line can be identified as being part of the maturity of the organizations which achieve multinational status, and which develop more and more social and ecological projects (Djellal, Gallouj, 2020 and Latif and Sajjad, 2018).

Finding a general explanation of the relationship of the two represents a hard to achieve objective and the random factors which influence this interaction are numerous. New variables, worthy of taking into account, include: the organization’s size, the risks the organization is exposed to, the industry it is a part of, as well as the investments in research and development that it makes (Eccles and Serafeim, 2017). Reconsidering what it is understood though the term of social performance depends on finding some indications through the help of which the development of the organizations’ activity can faithfully be mirrored (Buendía-Martínez and Carrasco Monteagudo, 2020).

The competitiveness – performance – social responsibility triptych of the organization allows managers to improve upon their knowledge regarding the real effects of the CSR practices on the organization’s performance, especially on the medium and long-term competitiveness (Buendía-Martínez and Carrasco Monteagudo, 2020). This must be seen as a reflective construction composed of two main dimensions, one which includes economic and financial aspects and one which gathers some measures of competitive differentiation. Therefore, one may highlight the need to double evaluate the organization’s performance from a financial point of view as well as from a CSR perspective. Regarding the internal model of relational improvements, having an adequate approach to multi-participant usage has been confirmed (Singh, Misra and Yadav, 2021). The direct involvement within the value chain, the relationship with the internal interested parties (shareholders, employees, managers etc.) and external interested parties (clients, investors, suppliers, community etc.) must be managed carefully as it will have a higher significant impact on the corporate performance for other interested parties (Gokten, Ozerhan and Gokten, 2020). If one reviews the causal effects, the development of CSR practices has a positive influence on the competitive performance. It is necessary for the real value CSR generates for the organization to be understood. This value can innovate products or markets, offering improvements within the value chain, value which is always generated considering the interaction between the organization and the interested parties (Hörisch, Schaltegger and Freeman, 2020).

In the background of this subject, one can refer to the problems and gap research as well as to the novelties and tendencies in CSR within the retail sector. The environmental sustainability represents the manner in which multiple organizations within the retail sector focus more and more on reducing their carbon footprint and on promoting sustainable practices. This can include the transition towards environmentally friendly packaging, efficient resource management and carbon footprint reduction (Gokten, Ozerhan and Gokten, 2020). The diversity and inclusion represent another chapter retail organizations are more and more preoccupied with (Busco and Sofra, 2021). Promoting diversity and inclusion happens within the organization as well as within the relationship with the clients and suppliers. This can involve using policies of diverse employment and promoting products which reflect cultural diversity. Another important aspect is represented by the transparency in the supply chain. The retailers assume responsibility for ensuring transparency within their supply chain, so that they can identify and approach problems related to human rights, work conditions or the impact on the environment in the production areas (Gokten, Ozerhan and Gokten, 2020).

A series of other problematic aspects has also been identified such as equitable and ethical commerce which would respect human rights, reduce food waste by donating unsold food to charities, adopting some strategies to minimize waste in their supply chain and last but not least local responsibility which can include supporting local schools, non-profit organizations and community events. With a growing emphasis on sustainability and social responsibility, it is to be expected that these elements continue to be important for the retail companies in the future (Hörisch, Schaltegger and Freeman, 2020).

The objective of the paper is that of researching the relationship between the social performance and the financial one through a case study on an organization from the retail sector, active on the Romanian market.

The structure of our paper is organized as follows. Section 2 drafts a short literature review, first on the general CSR topic and then more specifically on the financial and social performance. Section 3 showcases a short presentation on the Lidl Group and its activity on the Romanian market. Section 4 and 5 present the research methodology, respectively the results of researching the relationship between the indicators of social performance and those of financial performance. Section 6 contains a short discussion on the obtained results by presenting an action plan for the management. Finally, Section 7 presents the main conclusions derived from this research and suggests potential directions for further research.

Literature review

In order for sustainable development to occur, the organization must consider a new dimension of the performance and the organization’s social performance which together with the financial performance make up the global corporate performance (Argento, Culasso, 2019). The importance the performance of the organizations has gained through its use in every field of the economic and social has determined the definition of a new concept, a new dimension of the corporate performance, that of the organization’s social performance (Rupley, Brown, and Marshall, 2017).

The fact that the CSR elements intersect with those related to global performance is also proven by the amplest study of Gallup Organization, conducted for 25 years, having as purpose the sociological approach of the economic activities of over 400 organizations worldwide (Friedman and Kass, 2018). The study proves the fact that not only the productivity and profitability, but also the elements of social responsibility, such as maintaining the personnel and client satisfaction, constitute a competitive advantage which can support a superior performance of the organization (Friedman and Kass, 2018). Promoting this system of values determines an active and responsible participation from the organization in accomplishing objectives, and, implicitly, obtaining performance (Tilt, 2016). Equally important are also factors such as market measurements, the quality of offered goods and the quality of the offered services, focusing on satisfying the consumer. All these elements showcase in a much clearer manner the economic condition of an organization together with its growth targets than its reported earnings do (Swain and Yang-Wallentin, 2020).

In numerous case studies the authors state that implementing CSR improves performance through the impact that these practices have on the relationships between the organization and the interested parties (Voiculescu and Neagu, 2016). The capacity of the organizations to manage relationships with the interested parties, together with the development of a proactive strategy and the knowledge for obtaining a common vision, are positively associated with a proactive CSR (Ting, et. al., 2020). Thus, it is shown how a proactive social responsibility determines an improvement of the organization’s financial performance (Margolis, Elfenbein and Walsh, 2007).

A performing organization, able to better value the CSR opportunities, satisfies at a superior level a certain segment of the social need in a qualitative as well as quantitative manner, resulting in a competitive advantage on the specific market it activates in (Singh, Misra and Yadav, 2021). In such conditions, poorer performances from the CSR domain are equal to losing profits (Roblek, et. al., 2020). In other words, it is considered that a high social performance is based on the even stronger financial performance (Caraiani, et. al., 2018).

The empirical studies drafted regarding the interaction between the social and environmental performance of the organization and the financial performance cannot conclude the existence of a stable relation between the two types of performances. As some authors state, there is no proof that a socially responsible organization can obtain constantly better results on the long-term (Dumitru and Dragomir, 2021). The papers of other authors state that the social performance – financial performance relationship would be positive (in 71 of 122 studies, one identifies a strictly positive relation), but that there also would exist certain inconsistencies within samples, tested variables analyses and causal relations (Orlitzky, Schmidt and Rynes, 2003).

The social performance from the perspectives of some authors refers to the way a company manages the social impact on the communities, employees and the environment (Arvidsson and Dumay, 2022). The social performance can have a significant impact on a company’s reputation and can attract loyal customers and investors interested in sustainable businesses (Lee, 2021). The motivation of some authors to research this subject was given by government regulations and the pressure held on the third parties for more social responsibility, leading towards a bigger and bigger preoccupation of this subject towards the retail sector (Vo and Arato, 2020).

Judging by the studies on this subject, there are authors claiming that the retail sector can adopt practices of sustainable sourcing for their products, ensuring that they come from responsible sources from a social and environmental point of view. This can imply, for instance, ensuring that the products have not been produced through forced work or that the latter did not lead to tropical woods deforestation (Dang, Nguyen, and Pervan, 2020). The authors are of opinion that if the organization correlates the actions for obtaining economic performance with CSR actions, it will obtain an even stronger impact within society (Ramos and Santos, 2020). Because these kinds of measures are based on the analysis of inputs and outputs, in certain conditions given by the market, one may wonder whether the estimations made regarding the productivity and the performance of the organization have considered the social and environmental activity (Carroll and Jamali, 2017).

By analyzing recent papers focused on the conditions in which the social and environmental performances of the organization may have a positive impact on the financial performance, these two performances show that their relationship is more positive than negative (Demir and Maung, 2021). Some authors consider this impact of social and financial performance as being a positive one, their studies being based on the concept of social strategy (Dumitru and Dragomir, 2021). This mentality allows them to differentiate between different integration levels of the social responsibility within the organization’s strategy. Other authors propose a model in which the social and financial performances are based on four essential elements: the industry structure the organization is a part of, the resources the organization has, the values it has created and how it manages interested parties (Heimann and Lobre-Lebraty, 2018). The CSR practices applied in under-development countries can increase the living standard of the community, contribute to the economic development, and can solve social and environmental specific problems (Pandey, et. al. 2020). Thus, more and more organizations in Romania try to determine the importance of appreciating the elements which make up the concept of CSR. Some of them appreciate the importance of CSR for the ethical value it brings while others appreciate it for its commercial valences. Considering these misunderstandings, multiple organizations are still more than skeptical regarding the relationship between these two performances, even though the relationships between them are more and more evident (Nechita, 2019).

Based on the documentation regarding financial and sustainability reports made during the first research stage, the following hypotheses have been issued:

Hypothesis 1: The retail sector organizations are interested in their social performance.

Hypothesis 2: The social performance influences the financial performance of the retail sector organizations.

The – Lidl Group – retail sector activity on the Romanian market

Within this research the retail sector has been chosen as a case study. This choice is due to the accelerated dynamic of transformation and development the retail sector has met these last few years. The retail sector has the highest investor request, mainly due to the offered stability. The attractiveness of the retail sector is given by its adaptation to the actual business context. The traditional retail model has become competitive-free because the organizations that were based on the conventional business model were overwhelmed by the innovative and agile competitors. The retail organizations must surpass the less flexible operational model for two reasons. Firstly, the retail sector must generate a superior quality business experience on the competitive market. Secondly, the retail sector’s activity must answer to the requirements of the actual period of fast growth of consumer needs, investors, suppliers, local community, authorities etc. As a follow up, within the retail sector a rethinking of the business strategy is overdue. The continuous improvement of operations, product and service diversification, as well as offering new experiences to the consumers are no longer enough these days. In order to differentiate from the retail sectors’ competitors, it is imposed that the organizations direct their attention towards objectives which can be achieved through technology and the receptivity presented from a social point of view. One must give a great deal of attention to CSR objectives, becoming decisive factors for consumers or investors within the buying process.

Within this paper, in order for the social performance – financial performance relationship to be analyzed, the attention was directed towards Lidl International Group, originally from Germany, a family multinational retail group operating under the Lidl and Kaufland trademarks, being the biggest retailer in Europe and the fourth biggest retailer in the world judging by the revenue.

Starting with 2011, the first Lidl stores were opened on the Romanian market, currently having over 300 shops with over 9500 employees with an indefinite period contract. Lidl Romania Group is made up of five organizations: Lidl Discount SRL, Lidl Imobiliare Romania Management SCS, Lidl România SCS, Lidl România SRL, and Lidl România Digital, having WE INTERNATIONAL GMBH as a majority shareholder with over 97%.

Starting with 2018, the Lidl Group publishes its first sustainability report according to the GRI standard. Operating as a responsible retailer, the Lidl Group, through its CSR policies, looks towards solid investments towards the development of the local community and environmental protection. The 2019-2022 timeframe has been analyzed where one noticed that the growing turnover assured the Group the achievement of social and environmental objectives through allocations of consistent funds to reduce the direct and indirect negative impact on the environment and the local community. During the 2019-2022 timeframe, the Lidl Group has commenced a series of CSR campaigns („Școala în culori vesele” where for each article of stationery bought, Lidl donated 1 RON, „Pâine şi Mâine” of World Vision by offering warm meals for children in disadvantaged areas, the „Edu Networks” program through which the Lidl Group has facilitated the access to education for over 64.000 children from the rural environment). All these CSR campaigns have summed up more than 1.3 million RON for the local community. Starting with 2021, the Lidl Group has commenced the „100 de Români” CSR program, an initiative for researching the differences between the Romanian citizens’ lives which live in the rural environment as opposed to those living in urban environments. The project called „România cu un singur chip” has allocated a sum of up to 3% of 2021’s turnover. Currently, the Group carries out projects such as „Punct de prim ajutor. Fii salvator!” with the purpose of facilitating the possibility of giving first aid by equipping the Group’s specific shops and some heavily transited public spaces with advanced equipment of urgency medical assistance.

Research Methodology

In order for this research to be drafted, one started from the following research premise: Can we talk about the social performance of retail sector organizations? One referred to qualitative and quantitative research methods to answer the research question.

Within this research one analyzed, with the help of a set of ten indicators of appreciating the social performance, how the dimension of an organization’s financial performance is influenced. In this sense, data from the Lidl Group have been used, data which reflected the development of activity within the Romanian retail sector during the 2018-2022 timeframe. Considering that starting with January 2017, the organizations with over 500 employees at the date of submitting the balance sheet have the obligation to describe the CSR actions, for the analysis of the social and financial appreciation indicators the 2018-2022 timeframe has been used (European Parliament, & Council of the European Union, 2023.).

To analyze the indicators of measuring the social performance, one was able to collect sufficient CSR data, available within the sustainability reports of the studied organization.

During the first part of the research, data collection was done by studying and processing the published financial situations while collecting and processing non-financial data from the sustainability reports available by accessing the Group’s webpage (Lidl Group, 2023).

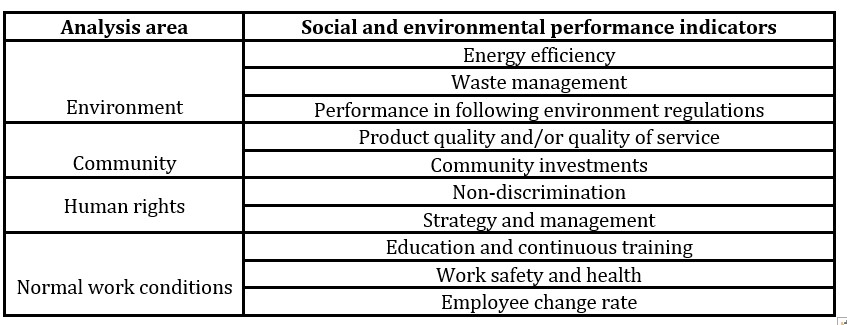

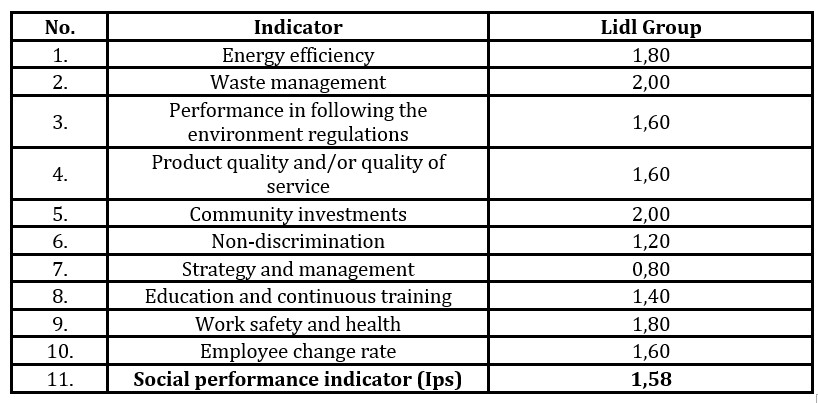

Regarding the analysis of the social and environmental analysis (part of CSR), a number of ten indicators considered relevant by the authors were chosen, which are found within Table no. 1.

Table 1: Social and environmental performance indicators

In analyzing social performance for the selected research organization, one considered for each of the 10 indicators a scoring of 0 through 3, depending on the grade of completion of existent data within the organization’s sustainability reports.

A score of 0 points was given in case there was no mention of that indicator within the report, 1 point in case the indicator is taken into account without any further details, 2 points if the group provides a detailed description of the indicator. A maximum score of 3 points was given when the description of the indicator is made in a satisfying manner regarding the integration of CSR aspects within the published sustainability reports. The maximum number of points that could be obtained is of 30. By adding the score given to each component that was considered, the social performance indicator (Ips) was defined, indicator which approximates the way in which the Lidl Group complies with their sustainable objectives.

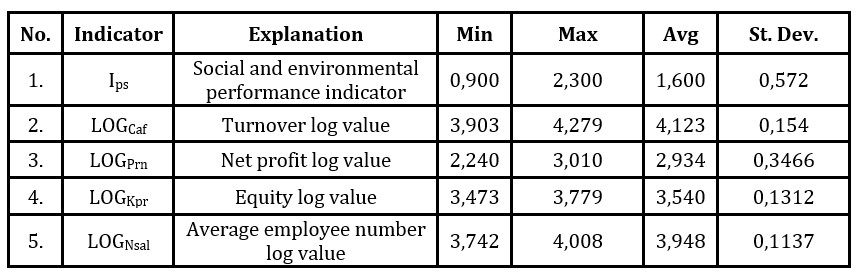

In order to analyze financial performance, the following financial indicators were taken into consideration: equity, turnover, net profit and the average number of employees. The logarithmical values for these financial indicators have been calculated: turnover (LOGCaf), achieved net profit (LOGPrn), equity (LOGKpr), and the average number of employees (LOGNsal).

Putting the values of the financial indicators under a logarithm was done taking into account that they are, in terms of magnitude, significantly higher than the values of the social and environmental indicators, thus obtaining distributions that are closer to the normal ones. This way, the significant impact of the selected organization’s specific values was diminished, fact which is highlighted by the existence of some significant gaps between the minimum and maximum values, as it can be seen in Table no. 2.

Table 2: Descriptive statistics

Describing the statistical analysis data

In drafting the hypotheses, one took into consideration elements derived from the collected empirical observations, according to which the organizations with a solid financial performance (fact shown by the existence of financial profits and positive and growing equities) manifest an increased attention to social performance, being involved in different projects in this sense. Regarding the establishing of the relation between the two performances, one referred to the Hausman test regression model according to which the null hypothesis considers that the model with variable effects is adequate, and the alternative hypothesis indicates the fact that the model with fixed effects is not adequate, having the form:

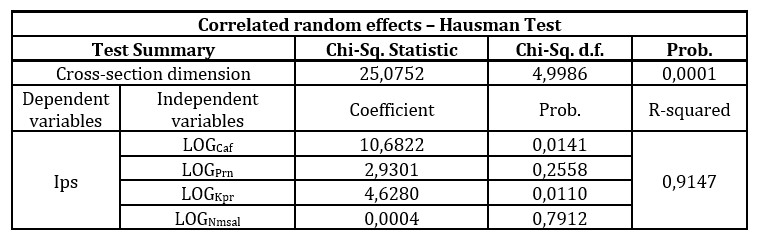

In order to establish the type of relationship between the order of the financial performance and the order of the organization’s social performance, regression models which apply to panel-type data have been used. As a follow up, a model has been built in which the Ips (indicator of social performance) dependent variable was considered, together with the indicators of the financial performance (LOGCaf, LOGPrn, LOGKpr, LOGNmsal) independent variables, the results being presented under Table 3. The underlined results in the first part of Table 3 showcase the relation between the endogenous variable (Ips) and the exogenous variables (LOGCaf, LOGPrn, LOGKpr, LOGNmsal).

Results

The research on the Lidl Group proposes to determine whether the increase or decrease of the financial performance is determined in the same measure or not by the increase or decrease of their social and environmental performance.

Table 3: Proposed model for the Ips variable based on four independent variables

It can be observed, based on the data presented in Table 3, the fact that a significant growth of the financial indicators has a positive impact on the social and environmental performance growth, pointing to CSR improvement. The probability that it is under the level of 5% (4,998679%) indicates a positive relation between the social performance and the financial performance of the organization. It is therefore explained why, as the organizations develop their production abilities and/or services, their interest for attenuating the impact of their activity on the community and the environment increases.

In order to see whether the retail sector influences the social performance, the indicators of the social performance have been determined for the 2018-2022 timeframe for the Lidl Group (service provider domain), the results being presented in Table 4.

Table 4: Indicators of social performance

After scoring the CSR elements specific to each social and environmental indicator within the organization, the social performance indicator has been determined by dividing the number of elements which are reported by the organizations to the total number of elements which should be reported.

The interval of values of the social performance indicators is within 0 and 3. The value of 0 signifies the fact that the indicator is not achieved and the maximum value of 3 signifies the fact that the indicator is met in a satisfying manner. As a result of the social and environmental performance measurement indicator analysis, one can observe that they vary between a minimum of 0,80 for the strategy and management indicator, and a maximum of 2,00 for indicators such as waste management and community investments.

Within the service department, the Lidl Group, through the waste management indicator, has reached the highest level. This signifies that no matter the domain of activity, this indicator occupies a significant place within the sustainable development strategy. On par with the waste management indicator, there is also the community investments indicators. The performance in following environmental regulations and employee change rate indicators shows that the studied organization must make efforts in respecting the environmental regulations applied by law and other initiatives and in showing a greater deal of interest regarding the absenteeism and the personnel variations in the workplace. A superior quality of the produced goods is obtained by assuring a favorable climate in the workplace and increasing their trust. Generally, the Group registers a percentage of satisfaction of over 50%, even though the minimum level is represented by the strategy and management indicator with just 0,80.

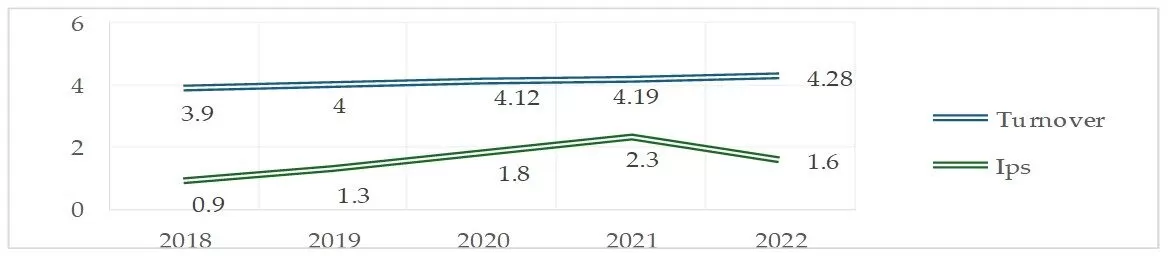

To better understand the organization’s social performance indicator based on each financial indicator, the evolution was graphed in Figure 1.

Fig 1. Evolution of Ips versus turnover

According to Figure 1, the evolution of the Lidl Group’s turnover has a permanent growing tendency during the analyzed period. This feat can be one of the reasons for which the organization has been motivated to adopt and promote policies of social and environmental responsibility. It can be observed that the indicator of social performance in 2020 has doubled as opposed to 2018 (from 0,9 to 1,8), maintaining its growth within the analyzed time frame, reaching a level of 2,3 in 2021. This signifies that during the analyzed period the organization has continued its active involvement in CSR actions and activities. The fact that in 2022 the Group has registered an Ips decrease of 0,5 as opposed to the previous year does not represent a motive of concern for the social performance, with no negative values being registered.

Regarding the Lidl Group, its premise is „sustainability is not just caring about the communities we conduct our activities in today, but caring about the legacy we leave to future generations”. During the analyzed period, 2018 – 2022, the Group has continued to be responsible (the indicator of social performance measurement has increased from 0,9 in 2018 to 1,6 in 2022) and to act for a better future, focusing mainly on reducing the impact of its own operations.

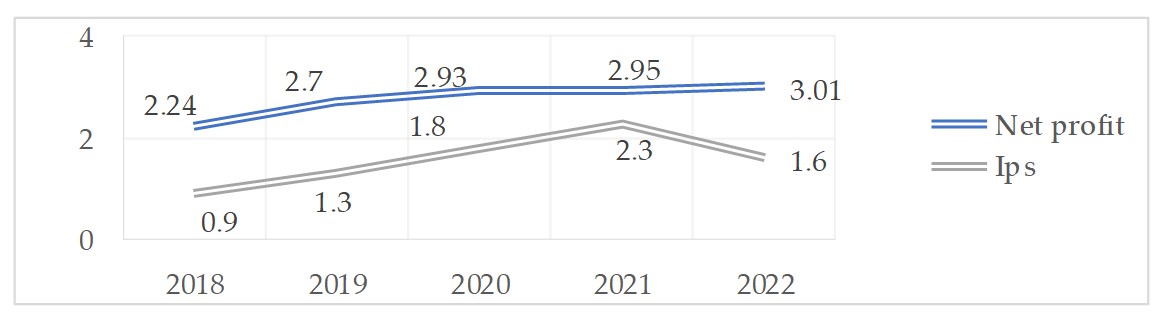

Regarding the net profit, during the analyzed timeframe, the organization has registered growth each year, but this is not truly in compliance with Isp, according to the graphical representation from Figure 2.

Fig 2. Ips versus net profit evolution

According to Figure 2, one can notice that the net profit indicator (which has grown from 2,24 in 2018 to 2,95 in 2021) as well as the CSR indicator – social performance (which has grown from 0,90 in 2018 to 2,30 in 2021) have had an ascending trend. Thus, one can say that the increase of the net profit of the Lidl Group has determined a growth of the social and environmental performance up until 2021. Even though the net profit of the organization has registered a growth in 2022 as opposed to the previous year, Ips has decreased. This can be explained through the fact that the organization’s profit was not headed towards actions of social performance.

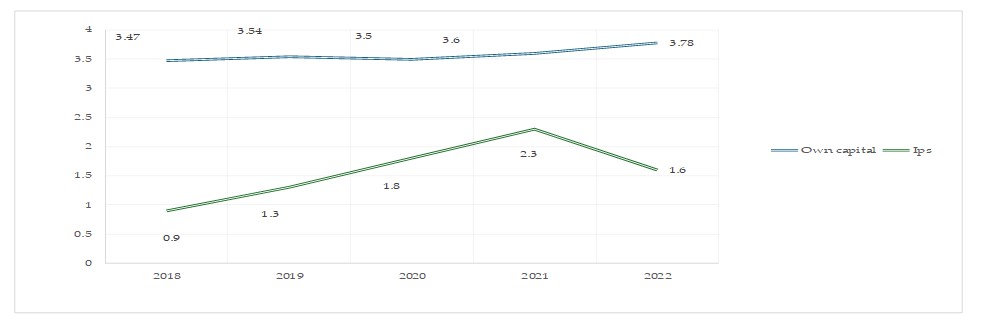

Judging by the drafted analysis, it results that the rhythm of the social indicator’s growth is not followed by the same rhythm of the financial indicator’s growth. Although, the registering of positive values of the organization’s own capital shows a favorable tendency of growth and development of the CSR activity according to Figure 3.

Fig 3. Evolution of Ips versus own capital

The 2019 – 2020 pandemic timeframe will remain in the history of the business environment as being an unusual period which has brought a lot of uncertainty globally, putting to test the capacity to adapt and the organizations’ reaction time. However, the Lidl Group managed to grow with over 2,5 times its contribution towards environmental protection and local community wellbeing (the indicator for measuring social performance has grown during the analyzed period from 0,9 to 2,3). The year 2022 registers a growth of their own capital of 0,28 as opposed to 2021, but at the same time it also registers a decrease of Ips with 0,5 in 2022 as opposed to 2021. Therefore, one can say that in 2022 the Group has not invested its own capital in social actions.

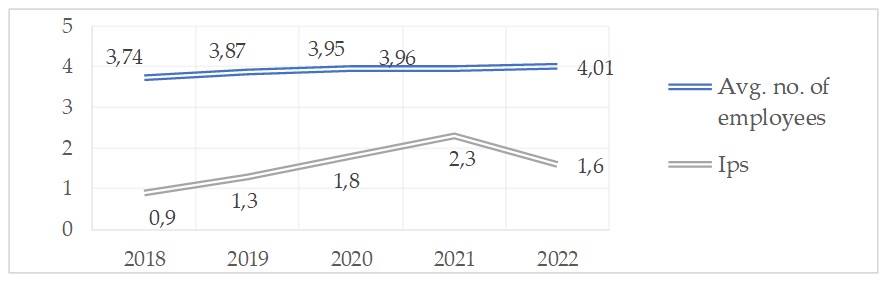

As a responsible employer, to attenuate absenteeism and/or workforce migration, the Lidl Group tries to ensure a safe workplace for every employee by respecting their rights and contributing to their professional development. The graphical representation is shown in Figure 4.

Fig 4. Evolution of Ips versus average number of employees

Workplace discrimination is forbidden with the respective regulations being stipulated within the „Lidl code of conduct”, available on the organization’s website. Even though during 2018-2022, at the level of the Lidl Group, there is no specific policy regarding employee diversity, it is on the organization’s work agenda, and it is about to be drafted in the future. Even though the average number of employees has not significantly grown during 2018-2022 (from 3,74 to 4,01), one can notice a significant growth of the social performance measurement indicator from 0,9 to 2,3 during 2018-2021. This signifies the fact that, at group level, the personnel policies occupy a significant spot. By decreasing Ips with respect to growing the average number of employees in 2022, it would result that the Group has focused more on growing the number of employees detrimental to personnel training, work quality promotion and their motivation at the workplace.

Having that in mind, Table 5 presents the evolution of Ips versus Ipf during the analyzed period. This was made to see whether the retail sector involved in CSR actions influences the organization’s financial aspect.

Table 5: Social and financial performance indicators

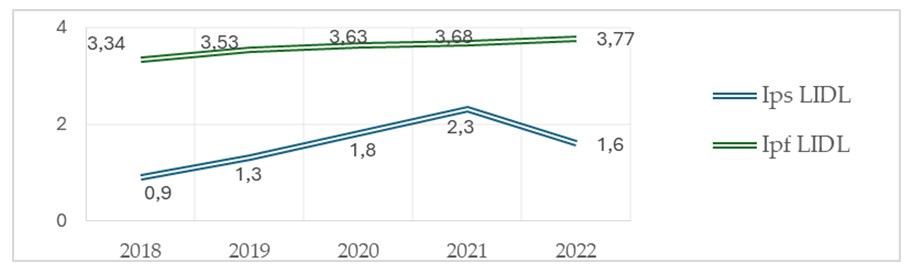

The evolution of the social and financial performance indicators made by the Lidl group during 2018-2022 is graphed in figure 5.

Fig 5. Ips and Ipf evolution

Judging by Figure 5, it can be noticed that their trend is growing up until 2022 which signifies the fact that, within the retail sector, the involvement in CSR actions and the organization’s financial status are directly proportional. Although, this cannot be truly said because in 2022 the organization’s financial performance is in continuous growth, but it does not influence the evolution of the involvement in the actions of social and environmental responsibility which is decreasing (from 2,3 to 1,6). Even though the financial indicators during 2018-2021 do not have a significant growth, increasing from 3,34 to 3,68, for the Lidl Group the social performance indicators have seen a growth of at least 50% (from 0,9 to 2,3). This showcases the awareness as well as the growth of the involvement in actions and activities of social and environmental responsibility. Even though during 2020-2021 the retail sector suffered from the COVID-19 pandemic, the analyzed organization did not restrict nor cancel its CSR actions. In this context, the explanation for the Ips decrease in relation with Ipf in 2022 can be the result of legislative policy modifications or inflation, leading to a rethinking of the organization’s short-term objectives.

Discussions

Using data specific to the Lidl Group, for the 2018-2022 timeframe, the existence of some relationships between the social and financial performance has been analyzed, in case of some representative organizations which develop their activity in the Romanian economy. In this sense, a social performance index has been built, using a number of 10 measurement indicators of the social performance which were analyzed in relation with 4 indicators of measuring financial performance. As a result of the drafted research, the following issued hypotheses can either be validated or invalidated:

Hypothesis 1: The organizations from the retail sector are interested in their social performance- it is valid. Validating this hypothesis results from the fact that, at the level of the organization this research is based upon, interest was manifested for social aspects. The presence of the environmental elements, involvement in the community, respect for human rights or aspects such as conditions at workplace conditions elements has were represented the starting point for studying and appreciating Ips. For the analyzed period, Ips has been present within the activity of the organization and has registered only positive values, reaching its peak in 2021, with a value of 2,3. Moreover, the positive relationship between Ips and Ipf induces the necessity of drafting a based strategy for the transition towards a sustainable development, so that the temporary shocks are absorbed by using new technologies.

The obtained results are of interest for a large variety of organizations: investors, supervision authorities, nongovernmental organizations etc. Thus, for the organizations which develop their activity in Romania, this research brings an image on the actual state of the compliance with the CSR principles, as well as the challenges associated to this concept.

Hypothesis 2.: The social performance influences the financial performance of the organizations from the retail sector- it is valid, as one may highlight the existence of a fluctuating positive relation between Ips and Ipf with a growth from 0,9 in 2018 to 1,6 in 2022 and a peak of 2,3 in 2021. Thus, the social aspects the organization has been involved in and its financial aspects (turnover, own capital, net profit, and average number of employees) had an ascending trend during the whole analyzed period. The performance indicators offer the organizations useful information for changing the policies existent at group level (investments, increasing the turnover, acquisitions etc.) heading them towards a development of the actions of social and environmental responsibility, as an activity based on knowledge, using financial, human, and social resources in a sustainable manner.

Creating a relationship between the social performance and the financial one leads towards a sustainable economy and can be made by using innovation, knowledge, ecological technology for providing services, products, or goods. Under the circumstances of a competition already manifested globally, the success of a business is obtained through efficient resource management, especially CSR actions, so that the organization’s activity is registered under applying priorities in sustainable development established at a European Union level which would lead towards creating long-term value.

Considering the obtained results, as a follow-up of our research one can compare to other studies developed with this subject in mind. Thus, there are authors which affirm that, even though there is no direct nor linear relationship between the social performance and the financial one, there is a great deal of proof that a positive social performance can bring financial benefits on the long-term for companies (Demir and Maung, 2021). Other studies have appreciated that a positive social performance can grow customer loyalty, making them choose the products and the services of a company as opposed to another (Lee, 2021). Similar studies in the domain appreciate that CSR can contribute to improving operational efficiency by reducing waste, saving energy and resources which can lead to significant cost savings on the long-term (Vo and Arato, 2020).

According to specialty literature, it has been demonstrated that the organizations which are perceived as being socially responsible and which invest in communities and the environment can attract clients and investors interested in such practices. The studies’ results have shown that a positive reputation can consolidate the brand and can attract more business (Nyame-Asiamah, and Ghulam, 2020).

CSR represents an important component of the retail sector management. A well drafted action plan for the managers in this sector can help promote ethical values while contributing to the wellbeing of the communities and the environment. A general plan which a retail manager can follow to develop and implement CSR within the organization could have the following structure: initial evaluation by analyzing the actual impact of the business on the community and the environment; establishing objectives by defining clear objectives for the CSR initiatives; creating and implementing the CSR policy by drafting a CSR policy which would reflect the commitment of the organization regarding social responsibility; employee involvement in CSR projects and offering training and resources for active participation; collaborating with suppliers to promote ethical and sustainable practices in the supply chain; communicating and reporting CSR efforts by the costumers and interested parties and publishing periodic reports tracking the organization’s CSR progresses; measuring, monitoring and evaluating the impact of the CSR initiatives as well as adjusting the strategy according to the results; continuous development and updates regarding best practices in CSR (Busco and Sofra, 2021) (Lee, 2021).

Implementing an efficient action plan requires long-term commitment and continuous effort from the management and the team. It is important that realistic objectives are set which would support innovation and constant improvement to ensure the positive impact within the community and the environment.

Conclusions

This paper presents the connections between the social and financial performances of the organization with the empirical results regarding the nature of the relation being unambiguous. A usually identified reason for these results refers to the way the social and financial performances are operationalized and measured. The financial performance is usually measured with the rentability rates extracted from the relatively standardized and easily accessible financial situations. However, due to a number of reasons, measuring the social performance is much more problematic. The first challenge is the lack of consensus regarding operationalization. The second challenge involves measurement issues mainly due to the fact that information regarding this concept is mostly non-financial whereas not a lot of report standardization methods exist. The third issue lies within unveiling. Reporting social performance in multiple jurisdictions is not mandatory because social responsibility is a voluntary action. Thus, one must track the revision, operationalization, and alternative measurement of the approach for the construction of the financial performance and the social performance developed within the concerning empirical literature. By making use of the qualitative research, the results of the research were obtained for them to be analyzed.

Through the drafted research, one can affirmatively answer the research premise: Can we talk about the social performance of retail sector organizations? Motivating the answer is supported by the following arguments: at the level of retail organizations there is non-financial information found, represented as CSR actions, resulting in an active involvement of the retail sector in the social sphere. The interest manifested towards non-financial actions can lead towards establishing a level of social performance of the organizations. Moreover, the research results regarding the determination of the relationship between Ips and Ipf demonstrate how the social performance influences the financial one. A retail organization which is involved in social actions has a better visibility, an increased level of trust and a greater impact on the third-parties, clients, employees, and investors, contributing to a long-term growth in revenue.

Within the paper, the limits of the research have been drawn out, mainly referring to the relatively low timeframe to reflect an overall tendency on the impact of social performance measures, a non-uniform application of principles or the reduced number of available data. Another limitation could be the sample extension of analyzed organizations as well as the observation period, or the lack of a control variable. We intend to use, for future studies, potential control variables such as: the market condition, the organizational dimension or factors specific to the industry which could influence the social performance, as well as the financial one. Future research directions can head towards a comparable study of the retail sector having as sample the whole chain of stores from within the Lidl Group from every country it is active in.

Considering that, the transition towards a sustainable development of businesses leads to major structural modifications within the technological processes used by the organizations, involving significant costs. Also, the investors could be interested in the results of this research, for substantiating their own investment decisions, especially regarding the ones with reduced impact on the environment and the community, with the non-governmental organizations having a clear image on the compliance grade of Romanian organizations with the social performance, aspect also sought by the European Union.

References

Argento, D.; Culasso, F.; Truant, E. (2019). From sustainability to integrated reporting: The legitimizing role of the RSC manager, Organization & Environment, 32(4), 484-507.

Arvidsson, S.; Dumay, J. (2022). Corporate ESG Reporting Quantity, Quality and Performance: Where to Now for Environmental Policy and Practice? Business Strategy and the Environment, 31(3), 1091–1110.

Bogeanu-Popa, M.M, Man, M, (2023). Does the Integrated Reporting Influence the Financial Performance Within the Banking System? Case Study on Romanian Banks, International conference KNOWLEDGE-BASED ORGANIZATION, 29 (2).

Busco, C.; Sofra, E. (2021). The Evolution of Sustainability Reporting: Integrated Reporting and Sustainable Development Challenges, In Corporate Sustainability in Practice, Cham: Springer.

Buendía-Martínez, I.; Carrasco Monteagudo, I. (2020). The Role of CSR on Social Entrepreneurship: An International Analysis. Sustainability, 12, 6976.

Caraiani, C.; Lungu, C. I.; Dascălu, C.; Colceag, F. (2018). The Triple Bottom Line (TBL) Approach from the Accounting and Performance Measurement Perspective. In Operations and Service Management: Concepts, Methodologies, Tools, and ApplicationsIGI Global, 785-808.

Carroll, AB.; Jamali, D. (2017). Capturing advances in RSC: Developed versus developing country perspectives, Business Ethics: A European Review,26(4), 321-325.

Dang, V. T.; Nguyen, N.; Pervan, S. (2020). Retailer corporate social responsibility and consumer citizenship behavior: The mediating roles of perceived consumer effectiveness and consumer trust. Journal of Retailing and Consumer Services, 55, 102082.

Demir, A.; Maung K.M. (2021). A Comparative Analysis of Sustainability Reports Published by Global Enterprises: Standalone RSC Versus Integrated Reporting, The BRC Academy Journal of Business, 11(1), 23–51.

Djellal, F.; Gallouj F. (2020). Services, innovation and performance: General presentation, Journal of Innovation Economics & Management, 1(5), 5-15.

Dumitru, M., Dragomir, V.D. (2021). The Factors of Integrated Reporting Quality: A Meta-Analysis, SSRN Journals, 1-78.

Eccles, R. G.; Serafeim, G. (2017). Corporate and integrated reporting: A functional perspectiv; Routledge, London

European Parliament, & Council of the European Union. 2023. Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32014L0095.

Fourati, Y.M.; Dammak, M. (2021). Corporate Social Responsibility and Financial Performance: International Evidence of the Mediating Role of Reputation; Wiley: Hoboken, NJ, USA.

Friedman, H.H.; Kass, F. (2018). Substance Over Form: Meaningful Ways to Measure Organizational Performance, Journal of the CPA Practitioner, 25-50.

Gokten, S,; Ozerhan, Y.; Gokten, P.O. (2020). The historical development of sustainability reporting: a periodic approach, Theoretical Journal of Accounting, 107(163), 99-118.

Heimann, M., Lobre-Lebraty, K. (2018). When does CSR motivate investors? A simulation study, Recherches en sciences de gestion, 6, 93-124.

Hörisch, J.; Schaltegger, S.; Freeman, R.E. (2020). Integrating stakeholder theory and sustainability accounting: A conceptual synthesis, Journal of Cleaner Production, 275, 124097-124155.

Latif, K.F.; Sajjad, A. (2018). Measuring Corporate Social Responsibility: A Critical Review of Survey Instruments. Soc. Responsib. Environ. Manag. 25, 1174–1197.

Lee, S. H. (2021). Effects of retailers’ corporate social responsibility on retailer equity and consumer usage intention. Sustainability, 13, 3080. https://doi.org/10.3390/su13063080.

Margolis, J.; Elfenbein, H.A.; Walsh, J.P. (2007). Does it pay to be good? A meta- analysis and redirection of research on the relationship between Corporate Social and Financial Performance, Scientific Research, 7-8.

Nechita, E. (2019). Analysis of the Relationship between Accounting and Sustainable Development. The Role of Accounting and Accounting Profession on Sustainable Development. Audit Financiar, 17(155), 520-536.

Nyame-Asiamah, F.; Ghulam, S. (2020). The relationship between CSR activity and sales growth in the UK retailing sector. Social ResponsibilityJournal, 16(3), 387–401. https://doi.org/10.1108/SRJ-09-2018-0245.

Orlitzky, M., Schmidt, F.L., Rynes, S.L. (2003). Corporate social and financial performance: a meta analysis. Organ Stud,24(3), 403-441.

Pandey, S.C.; Panda, S.; Widmier, S.; Harvey, E. (2020). CSR and Social Entrepreneurship: Combining Efforts towards Sustainability. Glob. Sch. Mark. Sci.30, 335–343.

Pizzi, S.; Rosati, F.; Venturelli, A. (2021). The determinants of business contribution to the 2030 Agenda: Introducing the SDG Reporting Score, Strategy Environ, 30, 404–421.

Ramos, T.M.; Santos, T.R. (2020). The Social Balance as an influence for a sustainable business society: A bibliometric analysis. ConTexto Porto Alegre, 20, 13–28.

Roblek, V.; Thorpe, O.; Bach, M.P.; Jerman, A.; Meško, M. (2020). The Fourth Industrial Revolution and the Sustainability Practices: A Comparative Automated Content Analysis Approach of Theory and Practice, Sustainability,12(20), 8497.

Rupley, K. H.; Brown, D.; Marshall, S. (2017). Evolution of corporate reporting: From stand-alone corporate social responsibility reporting to integrated reporting,Research in Accounting Regulation, 29(2), 172-176.

Singh, K.; Misra, M.; Yadav, J. (2021). Corporate Social Responsibility and Financial Inclusion: Evaluating the Moderating Effect of Income. Decis. Econ.42, 1263–1274.

Swain B.R.; Yang-Wallentin, F. (2020). Achieving sustainable development goals: predicaments and strategies, International Journal of Sustainable Development & World Ecology, 27(2), 96-106.

Tilt, C.A. (2016). Corporate social responsibility research: the importance of context, International journal of corporate social responsibility, 1(1), 1-9.

Vo, H. T. M.; Arato, M. (2020). Corporate social responsibility in a developing country context: a multi-dimensional analysis of modern food retail sector in Vietnam. Agroecology and Sustainable Food Systems, 44(3), 284–309.

Voiculescu, N.; Neagu M.I. (2016). Responsabilitatea socială a întreprinderii – de la concept la normatizare; Editura Universitară, București, 195-197.

Ting, I.W.K.; Azizan, N.A.; Bhaskaran, R.K.; Sukumaran, S.K. (2020). Corporate social performance and firm performance: Comparative study among developed and emerging market firms, Sustainability, 12(1), 26.