Hassan II University of Casablanca, ENCG Casablanca, Casablanca, Morocco

Volume 2025,

Article ID 320461,

Journal of Accounting and Auditing: Research & Practice,

15 pages,

DOI: 10.5171/2025.320461

Received date: 31 October 2024; Accepted date: 25 January 2025; Published date: 25 March 2025

Academic Editor: Kamal Abou El Jaouad

Cite this Article as:

Aymane Chemmaa and Mohammed Ibrahimi (2025), " Two Decades of Research on Earnings Management and Corporate Governance: Insights from a Bibliometric Review ", Journal of Accounting and Auditing: Research & Practice, Vol. 2025 (2025), Article ID 320461, https://doi.org/10.5171/2025.320461

Earnings management has garnered considerable attention from scholars, regulators, and stakeholders concerned with the integrity of financial reporting. This study conducts a bibliometric analysis of research articles indexed in the Scopus database from 2002 to 2024, offering a comprehensive overview of the link between corporate governance and earnings management. The field has witnessed substantial growth, with 56% of publications over the past 22 years appearing in the last six years (2018–2024), reaching a peak of 42 articles in 2022. Notably, Chandren, S. stands out with five publications, while Al-Haddad, L. holds the highest citation count, accumulating 146 citations across four articles. The primary contributions in this area originate from countries such as the United States, the United Kingdom, China, and Malaysia. This study explores four key dimensions of earnings management: transparency and financial reporting quality, the relationship between corporate governance mechanisms and earnings management, earnings management practices in commercial banks, and the influence of executive behavior on earnings management. Furthermore, the paper outlines promising avenues for future research, particularly examining the influence of audit committee characteristics—such as financial expertise, independence, and gender diversity—in emerging economies. Additionally, it highlights the need to deepen the understanding of real earnings management by considering aspects such as family ownership, religiosity, institutional ownership, and corporate social responsibility. corporate social responsibility is increasingly recognized as a critical factor that influences financial reporting practices, encouraging greater transparency and ethical behavior within firms.

In the early 2000s, the world witnessed the collapse of major companies due to their collusion in earnings management practices, leading to a deterioration of investor trust and transparency in the financial market (Goncharov, 2005; Nguyen et al., 2020). Goncharov (2005) shows that the majority of financial scandals that the world has experienced were due to executives resorting to manipulative techniques. Similarly, Kardan et al. (2016) demonstrate that the disregard for ethics and the principle of true and fair view is the root cause of fraud in the financial market.

The emergence of financial scandals is perceived as a sign of the failure of governance mechanisms to preserve the quality of financial information (Bajra and Cadez, 2018). Bao and Lewellyn (2017) show that the failure of governance codes is often due to their failure to consider the institutional environment specific to each country. Additionally, Almarayeh (2021) indicates that the failure of governance mechanisms in the MENA region is related to weak law enforcement, ownership concentration, and inadequate investor protection. Likewise, Bajra and Cadez (2018) demonstrate that the period can affect the effectiveness of governance mechanisms in reducing earnings management practices. The best example of this is the financial crisis of 2008, during which executives adopted strategies to aggressively inflate current-period earnings to present a favorable picture of their financial situation. Furthermore, Kumar and Vij (2017) suggest a decrease in earnings management during the 2008 financial crisis and an increase during periods marked by economic expansion.

To address these financial scandals, regulatory bodies have proposed certain measures to strengthen governance mechanisms and reduce earnings management, thereby improving the trust relationship with stakeholders (Sáenz González and García-Meca, 2014). Similarly, Leuz et al. (2003) show that strengthening governance mechanisms is beneficial for companies in terms of improving the quality of financial information, increasing company value and performance, fostering a trust relationship in the financial market, and mitigating agency problems. On the other hand, Mersni and Ben Othman (2016) emphasize the importance of the board of directors and Big Four audit firms in certifying accounts and enhancing the reliability of financial reporting.

Q1: What is the total volume and growth trajectory of research on earnings management and corporate governance?

Q2: Who are the most cited authors in the literature on earnings management and corporate governance?

Q3: What are the most influential articles, as well as the leading countries and institutions in the field of earnings management and corporate governance?

Q4: What approaches to earnings management have received most attention in the literature?

Q5: What are the themes that have received most attention in the literature on corporate governance and earnings management?

The structure of the article is organized as follows: Section 1 presents the research methodology. Section 2, titled “Results and Discussions,” presents the findings of the bibliometric study and the analysis of keywords. Finally, the “Conclusions” section presents the empirical conclusions, the topics that attract most attention in the scientific community, and recommendations for future researchers.

Bibliometric Research on Earnings Management and Corporate Governance

Previous literature provides little insight into bibliometric studies addressing the relationship between earnings management and corporate governance. Nyabakora (2023) examined 1,615 publications on earnings management collected from the Scopus database. The article showed that the term “earnings management” has gained particular significance at publicly traded companies since 1997. Similarly, several terms have been strongly associated with earnings management, such as “corporate governance,” “board characteristics,” “accounting fraud,” and “auditor performance.” It then suggested that future research should focus on the following terms: “earnings characteristics,” “institutional characteristics,” and “corporate social responsibility.”

Teixeira and Rodrigues (2022) conducted a bibliometric analysis using data from Web of Science, including 4,342 articles published between 1900 and 2020. Their results also revealed a growing trend in research from emerging countries, particularly on topics related to earnings management in connection with corporate governance, performance, and financial information quality.

Additionally, Zheng and Kouwenberg (2019) utilized 6,302 publications available in the Scopus and Web of Science databases between 1996 and 2018. These studies primarily focus on board attributes and their impact on company performance and earnings management. They then suggested that future research should concentrate on gender diversity, corporate social responsibility, and earnings management.

Finally, we propose a systematic review of the literature on earnings management and corporate governance, providing a clearer overview of research trends in emerging and developed countries, the most influential authors in terms of publications and citations, the countries and journals that focus on this research area, as well as existing gaps that will serve as a foundation for future research.

Research Methodology

Data Selection

We used the Scopus database in our research for several reasons. First, it provides a comprehensive coverage of high-quality journals in a multidisciplinary research field (Nyabakora, 2023; Vagner et al., 2021). Second, it offers the necessary tools to conduct a bibliometric analysis, such as tracking the evolution of research trends on a given topic (Vatis et al., 2023). Finally, it allows researchers to work on subjects that have a significant impact in the scientific community and to monitor the evolution of research trends in real time.

Based on the data collected from Scopus, we opted for a systematic review methodology, in accordance with the principles of the PRISMA protocol, using the keywords “Earnings management” and “Corporate governance.” My search string is as follows:

( KEY ( “Earnings management” ) AND KEY ( “Corporate governance” ) ) AND ( LIMIT-TO ( SUBJAREA , “BUSI” ) ) AND ( LIMIT-TO ( DOCTYPE , “ar” ) ) AND ( LIMIT-TO ( LANGUAGE , “English”)).

PRISMA Process

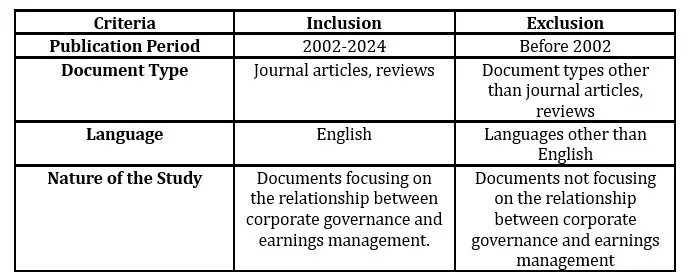

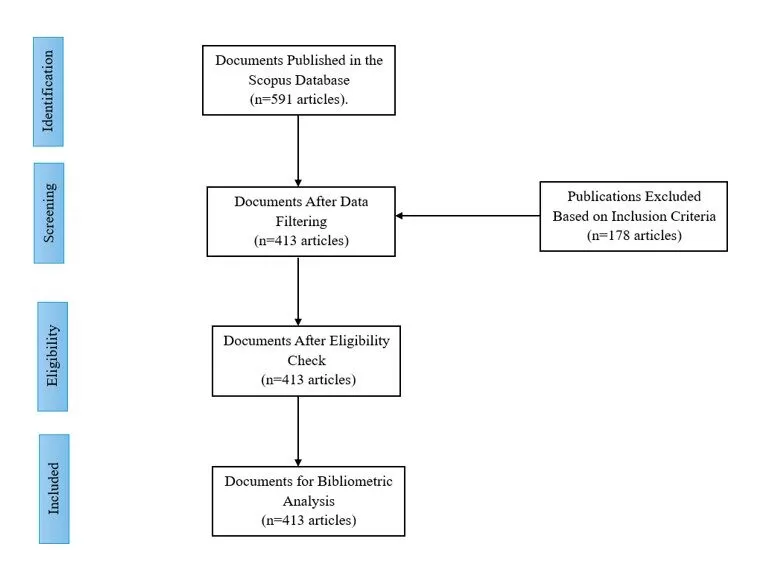

Referring to the principles of the PRISMA protocol, we defined the inclusion and exclusion criteria as illustrated in Table 1. First, we collected nearly 591 articles published in the Scopus database based on the keywords “Earnings management” and “Corporate governance.” Among these, we excluded 142 articles because they did not belong to the study field “Business, Management and Accounting.” Next, we applied the criteria of “Document type” and “Language,” which allowed us to retain only the articles written in English, resulting in a total of 413 articles.

Table 1. Inclusion and Exclusion Criteria

Bibliometric Method and Data Analysis

The bibliometric method was first defined by Pritchard (1969) as “the application of statistical and mathematical methods to articles and other types of communications.” The purpose of this method is to identify articles that have addressed the link between earnings management and corporate governance. This method is frequently used by researchers across various fields, utilizing databases such as Scopus and Web of Science (Krymskaya, 2023; Patra et al., 2022). Similarly, we employed VOSviewer software, developed by van Eck and Waltman (2010), to generate network maps based on bibliometric data, including citations, co-citations, authors, institutions, and countries. Additionally, descriptive analysis and citation analysis are used in this article to extract bibliometric information related to the number of articles published each year, the most cited articles, the main authors addressing the relationship between corporate governance and earnings management, the ranking of countries and institutions by the number of publications, as well as the co-occurrence analysis of keywords.

Fig 1. Publication Selection Process (PRISMA).

Research Results and Discussions

RQ1. The Total Volume and Growth Trajectory of Research on Corporate Governance and Earnings

Management

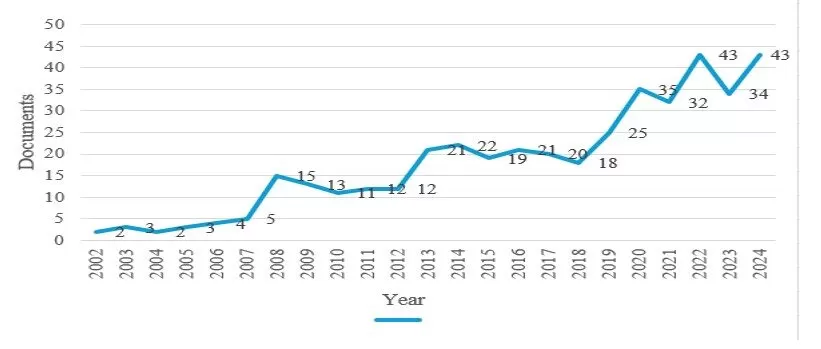

The 414 articles available in the Scopus database, covering the last 22 years (2002–2024), reveal a growing trend in research related to corporate governance and earnings management, particularly between 2018 and 2024. During the period 2002–2008, researchers focused significant attention on these topics, especially with the emergence of major financial scandals in large global corporations, such as Enron (2001), WorldCom (2002), and Parmalat (2003). This period saw a stagnant document count, ranging from 2 to 15 articles. Starting in 2008, the number of publications on corporate governance and earnings management began to rise, reaching 15 documents in 2008 and increasing to 35 publications by 2020. In 2021, however, the number of publications slightly declined to 32 articles (compared to 35 articles in 2020). Between 2002 and 2008, 34 articles were published on the relationship between corporate governance and earnings management. From 2009 to 2015, 110 articles were published, while from 2016 to 2024, the publication count reached 270 articles. The topic of corporate governance and earnings management has gained particular prominence within the scientific community over the last decade, with 56% of the literature produced over the past six years, from 2018 to 2024 (see Error! Reference source not found.).

Fig 2. Number of Publications Related to Earnings Management and Corporate Governance Between 2002 and 2024.

RQ2. The main authors in the literature on earnings management and corporate governance

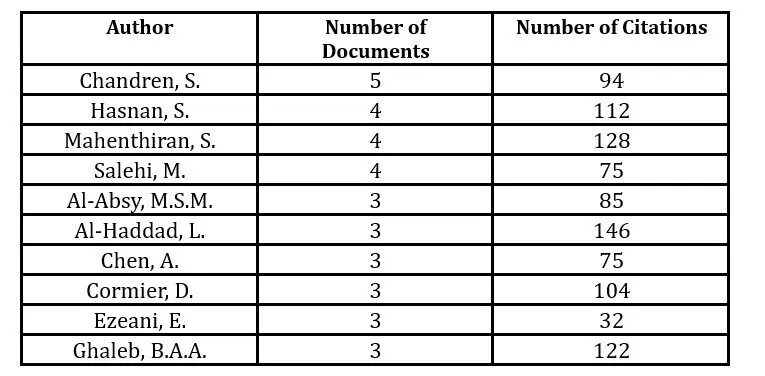

Table 2.Top authors by citations and number of publications.

Source: Extract from VOSViewer.

The list of authors who have contributed to the literature related to governance and results management is presented in Table 2, with a minimum threshold of 3 papers per author and a minimum of 10.66 citations per author. Referring to the number of papers, the most published authors are Chandren, S. (5 publications, 94 citations), Hasnan, S. (4 publications, 112 citations), Mahenthiran, S. (4 publications, 128 citations), and Salehi, M. (4 publications, 75 citations). In terms of the number of citations per author, Al-Haddad, L. is the most cited author with 146 citations for 3 publications. Similarly, Mahenthiran, S., Hasnan, S. and Salehi, M., with 4 publications each, received 128, 112 and 75 citations respectively. In addition, Ghaleb, B.A.A., Cormier, D., Al-Absy, M.S.M., Chen, A., and Ezeani, E., each with 3 publications, received 122, 104, 85, 75 and 32 citations respectively. Although Chandren, S. is the author with the highest number of publications (5 papers), he received only 94 citations.

RQ3. Most influential papers, leading countries and institutions

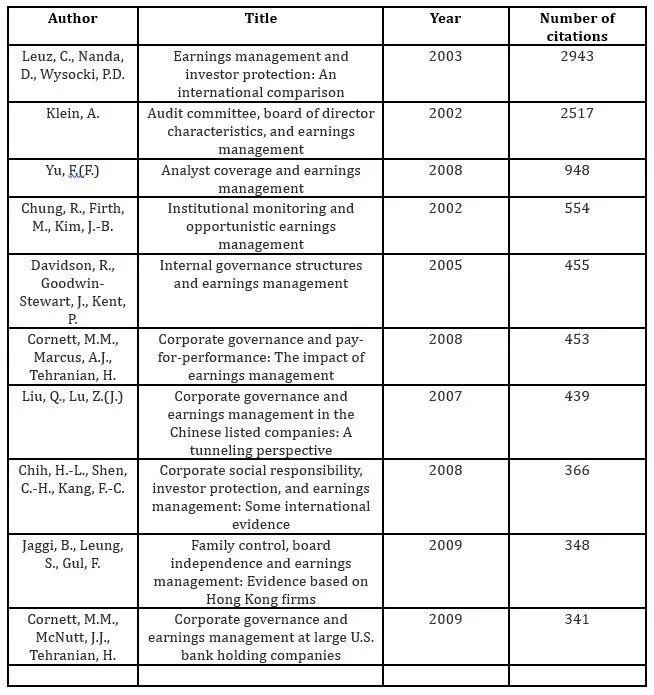

Referring to the highest number of citations, the following articles are considered among the most influential in the field of scientific research, particularly in emerging countries: “Earnings management and investor protection: An international comparison” (Leuz et al., 2003), “Audit committee, board of director characteristics, and earnings management” (Klein, 2002), and “Analyst coverage and earnings management”(Yu, 2008). Leuz et al. (2003) studied the relationship between corporate governance and earnings management for a sample of 8,616 non-financial companies from 31 countries between 1990 and 1999. Klein (2002) examined the relationship between board characteristics and earnings management for a sample of 687 US listed companies (S&P 500). The study revealed a negative relationship between board independence, audit committee independence and earnings management. Yu (2008) analyzed the influence of financial analysts on limiting earnings management practices for large listed US companies between 1988 and 2002. He found that the presence of a large number of financial analysts is likely to curb managers’ opportunistic behavior (see Error! Reference source not found.).

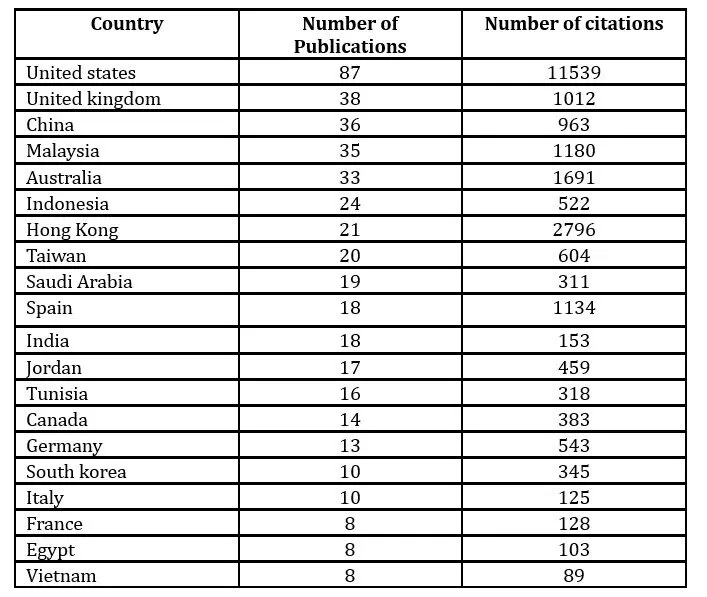

The USA (87 publications), the UK (38 publications), China (36 publications), Malaysia (35 publications), Australia (33 publications), Indonesia (24 publications), Hong Kong (21 publications), Taiwan (20 publications), Saudi Arabia (19 publications) and Spain (18 publications) are among the top ten nations, as shown in Table 4. In terms of publications and citations, the USA and the UK have the highest number of citations, 11,539 and 1,012 respectively, with 87 and 38 publications. Results management was also of particular importance in other countries, such as China, Malaysia, Australia, Indonesia, Hong Kong, Taiwan, Saudi Arabia, Spain, India, Jordan, Tunisia, Canada and Germany, each with at least 13 publications and 543 citations.

Table 3. Analysis of the most influential articles by citations

Source: Extracted from VOSViewer.

Although China and Indonesia have a high number of publications, they received only a low number of citations, 963 and 522 respectively. However, Hong Kong, with 21 publications, has the highest number of citations after the USA, with 2,796.

Table 4. Influential countries in terms of documents and citations.

Source: Extracted from VOSViewer.

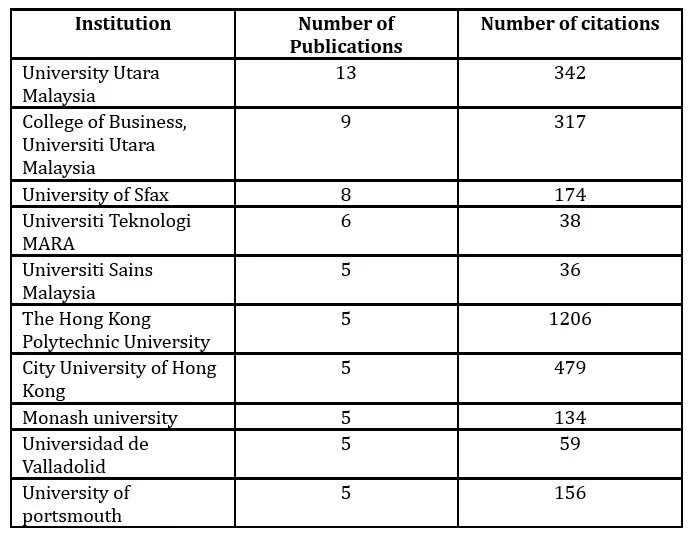

In terms of citations, the main institutions publishing articles dealing with the relationship between corporate governance and results management come from Malaysia (32 publications), Hong Kong (10 publications), Australia (5 publications), Spain (5 publications) and the UK (5 publications), as shown in Table 5. In terms of the number of publications, Utara University and Utara University College of Business have 13 and 9 publications respectively. However, Hong Kong Polytechnic University has a high citation count of 1,206, with only 5 publications.

Table 5. Top 10 contributing institutions by citations.

Source: Extracted from VOSViewer.

RQ4. Approaches to Earnings Management

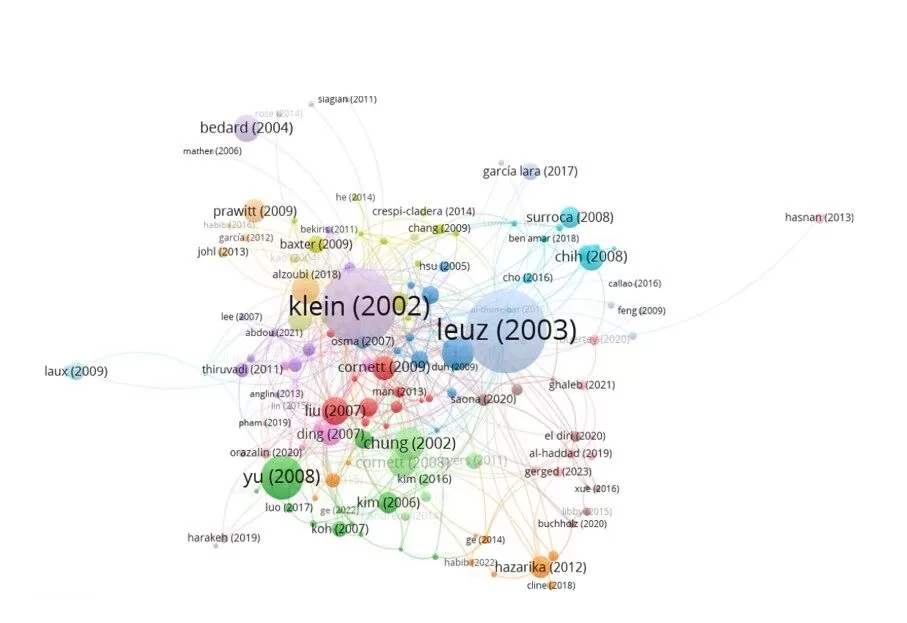

With a minimum threshold of 20 citations per document, the results of the bibliometric analysis yielded 145 documents grouped into 18 clusters: Cluster 1 (12 documents), Cluster 2 (12 documents), Cluster 3 (12 documents), Cluster 4 (11 documents), Cluster 5 (10 documents), Cluster 6 (10 documents), Cluster 7 (10 documents), Cluster 8 (8 documents), Cluster 9 (8 documents), Cluster 10 (8 documents), Cluster 11 (7 documents), Cluster 12 (7 documents), Cluster 13 (7 documents), Cluster 14 (6 documents), Cluster 15 (5 documents), Cluster 16 (11 documents), Cluster 17 (5 documents), and Cluster 18 (2 documents). Therefore, it can be inferred that the literature on earnings management focuses on five main approaches ().

The first and largest cluster (in blue) primarily focuses on topics related to transparency, financial information quality, and accounting manipulations. The main authors associated with this research stream are Leuz et al. (2003) – 2,943 citations, Chih et al. (2008) – 366 citations, Gastón and Jarne (2010) – 278 citations, Surroca and Tribó (2008) – 269 citations and García Lara et al. (2017) – 193 citations. This research has revealed various factors that can either encourage or limit executives use of earnings management, such as weak law enforcement, low investor protection, and a less developed stock market (Leuz et al., 2003), macroeconomic and institutional factors (Chih et al., 2008), as well as corporate social responsibility (Surroca and Tribó, 2008), which are considered motivating factors for earnings management. However, strong law enforcement, along with the presence of high-quality auditors (García Lara et al., 2017) and the implementation of IFRS standards (Gastón and Jarne, 2010), can improve the quality of financial information.

Fig 3. Scientific mapping of documents related to earnings management and corporate governance based on a

bibliographic coupling analysis from 2002 to 2024.

The second cluster (in green) primarily focuses on the relationship between corporate governance mechanisms and earnings management (Cho and Chung, 2022; Harakeh et al., 2019; Koh, 2007; Luo et al., 2017; Pham et al., 2019; Yu, 2008). The findings of Yu (2008) and Koh (2007) demonstrate the importance of independent boards of directors and external audit committees in enhancing the transparency and quality of financial information. Similarly, Luo et al. (2017) emphasize the significance of independent directors within the board of directors and audit committees in limiting earnings management practices.

The third cluster (in red) presents the relationship between corporate governance and earnings management in commercial banks (Chung et al., 2002; Cornett et al., 2009; Ding et al., 2007; Liu and Lu, 2007). Cornett et al. (2009) revealed that commercial banks, during a crisis, engage in earnings management through the adjustment of loan loss provisions to meet stakeholder expectations and cope with the financial crisis. Similarly, Ding et al. (2007) show that governance mechanisms are ineffective in restricting earnings management, thereby allowing commercial banks more freedom to engage in provisions for doubtful debts.

The fourth cluster (in orange) focuses on the relationship between managerial behavior and earnings management (Buchholz et al., 2020; Cline et al., 2018; Hazarika et al., 2012). Buchholz et al. (2020) demonstrate that companies that develop a management culture based on ethics are less likely to resort to earnings management practices, as managers adopt conservative strategies that align with stakeholder expectations. Similarly, Cline et al. (2018) emphasize that strengthening governance mechanisms, through the presence of an independent board of directors, is likely to control managerial behavior and, consequently, improve the quality of financial reporting. Hazarika et al. (2012) show that managers engage in earnings management practices upon their departure to maximize their compensation, asserting that the board of directors is effective in limiting opportunistic behavior among managers.

Finally, the fifth cluster (in purple) focuses on the relationship between audit quality and the quality of financial information (Bedard et al., 2004; Mather and Ramsay, 2006; Thiruvadi and Huang, 2011). Thiruvadi and Huang (2011) revealed that companies audited by the Big Four tend to publish high-quality financial reports. Mather and Ramsay (2006) and Bedard et al. (2004) demonstrate that external auditors are effective in detecting earnings management and preserving the quality of financial information.

RQ5. Thematic trends in the literature on earnings management and corporate governance.

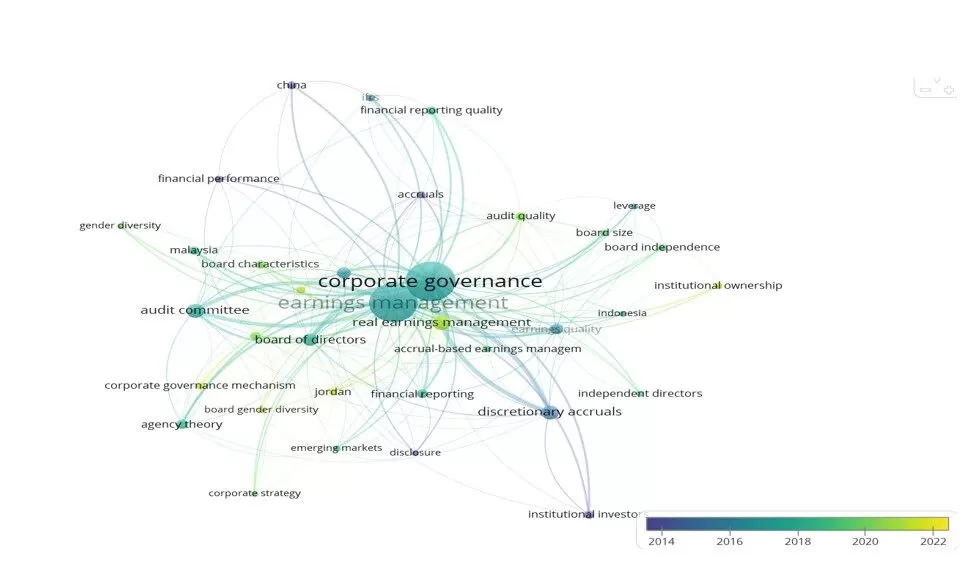

Figure 4 presents the visualization map of the keyword co-occurrence network. The most frequent keywords are “Corporate Governance” (380 occurrences) and “Earnings Management” (362 occurrences). These two current topics (large nodes) were primarily published between 2018 and 2022 and coincide with the second cluster, which mainly focuses on governance mechanisms and earnings management. The lighter nodes represent topics that garner the most importance in the field of scientific research, highlighting the frequency of occurrence of the terms “Audit Committee,” “Discretionary Adjustments,” “Board of Directors,” “Real Earnings Management,” “Ownership Structure,” “Earnings Quality,” “Malaysia,” “Jordan,” and “China.”

Based on the keyword co-occurrence network, this article has gathered gaps that have not yet been addressed in the existing literature on earnings management. First, the keyword “Audit Committee” has attracted particular attention from researchers. Nikulin et al. (2022) suggest that future research should focus on the effect of audit committee characteristics on earnings management, such as financial expertise, audit committee independence, and gender diversity. They also propose conducting comparative studies addressing the relationship between audit committees and earnings management, particularly in emerging countries. Second, future research should place greater emphasis on real earnings management rather than accounting earnings management (Ali, 2024; Chouaibi et al., 2018). Lyu and Zhang (2017) show that executives tend to engage in both accounting and real earnings management simultaneously when their salaries increase. Moreover, Zang (2012) demonstrate that the two forms of earnings management are substitutable and depend on the preferences of executives. Third, some researchers suggest that future studies should focus on the factors that may moderate the relationship between gender diversity and earnings management, such as the legal and cultural environment (Halaoua and Boukattaya, 2023; Triki Damak, 2018) and audit quality (Ghaleb et al., 2020). Fourth, Mohammad (2022) recommends that future research explore how family-owned businesses affect the relationship between governance mechanisms and earnings management, particularly in emerging countries. Similarly, Ghaleb et al. (2021) emphasize the need to examine the relationship between corporate social responsibility and real earnings management. Furthermore, Elnahass et al. (2022) recommend studying how religiosity affects the relationship between corporate governance mechanisms and earnings management. Finally, Eissa et al. (2023) suggest that future research should investigate the relationship between institutional ownership (e.g., national or foreign), investor effectiveness, and earnings management.

Fig 4. Keyword co-occurrence network map of various keywords.

Conclusions and Limitations

This study presents a literature review on earnings management and corporate governance by examining the past, present, and future. Our bibliometric analysis focuses on 414 publications indexed in Scopus from 2002 to 2024. My database reveals rapid growth in the field of earnings management and corporate governance, with 56% of the literature produced over the last 22 years generated during the last 6 years, from 2018 to 2024, peaking at 43 articles in 2024. Leuz, Klein, and Yu are the three main contributors to the existing literature related to earnings management and corporate governance. The most cited author is Al-Haddad, with 146 citations and 3 publications. Researchers from the United States, the United Kingdom, China, Malaysia, and Australia significantly contribute to this research area. The most influential institution in terms of citations is the Hong Kong Polytechnic University, with 1,685 citations from 10 publications.

With a broader Scopus database (2002-2024), my article highlights the five main themes in earnings management. The largest cluster (blue) focuses on transparency, financial reporting quality, and accounting manipulations. The key authors associated with this research stream are Leuz et al. (2003), Chih et al. (2008), Surroca and Tribó (2008) and García Lara et al. (2017). Their research has uncovered various factors that may encourage or limit managers’ use of earnings management, such as weak law enforcement, low investor protection, macroeconomic and institutional factors, as well as corporate social responsibility. The second cluster (green) primarily examines the relationship between governance mechanisms and earnings management. This group emphasizes the importance of independent boards of directors and audit committees in enhancing transparency and financial reporting quality. The third cluster (red) focuses on the relationship between corporate governance and earnings management in commercial banks. This group suggests that commercial banks engage in earnings management through loan loss provisions and allowances for doubtful accounts, despite strengthened governance mechanisms. The fourth cluster (orange) centers on the relationship between managerial behavior and earnings management. This group reveals the importance of governance mechanisms in limiting opportunistic behavior and preserving financial reporting quality. Finally, the fifth cluster (purple) primarily explores audit quality and financial reporting quality. This group highlights the role of “Big Four” audit firms in improving financial reporting quality. Our study contributes to the existing literature on earnings management and corporate governance while addressing gaps in research for the coming years. It demonstrates the importance of focusing on the effect of audit committee characteristics on earnings management, such as financial expertise, audit committee independence, and gender diversity. It also suggests conducting comparative studies that examine the relationship between audit committees and earnings management, particularly in emerging countries. Furthermore, future research should place greater emphasis on real earnings management rather than accounting earnings management and consider other factors that may affect earnings management, such as family ownership, religiosity, and institutional ownership.

Although this study provides valuable insights into earnings management and corporate governance, it has certain limitations. First, relying on a single database, Scopus, may mean that some relevant articles were not included because they exist in other databases, such as Web of Science. Second, our study primarily focuses on articles, which could be a limitation as it does not account for other types of publications. Finally, this study used only “Earnings Management” and “Corporate Governance” as keywords for conducting this bibliometric analysis, which could allow for the inclusion of additional keywords to broaden our research scope.

Funding: This work was supported by the National Center for Scientific and Technical Research (CNRST) as part of the “PhD-Associate Fellowship – PASS” program, awarded to Aymane Chemmaa.

References

Ali, A. (2024), “Audit committee characteristics and earning management of insurance companies in Ethiopia”, Cogent Business and Management, Vol. 11 No. 1, doi: 10.1080/23311975.2023.2301136.

Almarayeh, T.S. (2021), “Do board characteristics mitigate real and accrualbased earnings management activities? Evidence from MENA countries”.

Bajra, U. and Cadez, S. (2018), “The Impact of Corporate Governance Quality on Earnings Management: Evidence from European Companies Cross-listed in the US”, AUSTRALIAN ACCOUNTING REVIEW, Wiley, Hoboken, Vol. 28 No. 2, pp. 152–166, doi: 10.1111/auar.12176.

Bao, S.R. and Lewellyn, K.B. (2017), “Ownership structure and earnings management in emerging markets—An institutionalized agency perspective”, International Business Review, Vol. 26 No. 5, pp. 828–838, doi: 10.1016/j.ibusrev.2017.02.002.

Bedard, J., Chtourou, S.M. and Courteau, L. (2004), “The effect of audit committee expertise, independence, and activity on aggressive earnings management – USA”, AUDITING-A JOURNAL OF PRACTICE & THEORY, Amer Accounting Assoc, Sarasota, Vol. 23 No. 2, pp. 13–35, doi: 10.2308/aud.2004.23.2.13.

Buchholz, F., Lopatta, K. and Maas, K. (2020), “The Deliberate Engagement of Narcissistic CEOs in Earnings Management”, Journal of Business Ethics, Vol. 167, doi: 10.1007/s10551-019-04176-x.

Chih, H.-L., Shen, C.-H. and Kang, F.-C. (2008), “Corporate Social Responsibility, Investor Protection, and Earnings Management: Some International Evidence”, Journal of Business Ethics, Vol. 79 No. 1, pp. 179–198, doi: 10.1007/s10551-007-9383-7.

Cho, S. and Chung, C. (2022), “Board Characteristics and Earnings Management: Evidence from the Vietnamese Market”, Journal of Risk and Financial Management, Multidisciplinary Digital Publishing Institute, Vol. 15 No. 9, p. 395, doi: 10.3390/jrfm15090395.

Chouaibi, J., Harres, M. and Ben Brahim, N. (2018), “The Effect of Board Director’s Characteristics on Real Earnings Management: Tunisian-Listed Firms”, JOURNAL OF THE KNOWLEDGE ECONOMY, Springer, New York, Vol. 9 No. 3, pp. 999–1013, doi: 10.1007/s13132-016-0387-3.

Chung, R., Firth, M. and Kim, J.-B. (2002), “Institutional monitoring and opportunistic earnings management”, Journal of Corporate Finance, Vol. 8 No. 1, pp. 29–48, doi: 10.1016/S0929-1199(01)00039-6.

Cline, B.N., Walkling, R.A. and Yore, A.S. (2018), “The Market Price of Managerial Indiscretions”, Journal of Applied Corporate Finance, Vol. 30 No. 4, pp. 78–88, doi: 10.1111/jacf.12319.

Cornett, M.M., McNutt, J.J. and Tehranian, H. (2009), “Corporate governance and earnings management at large U.S. bank holding companies”, Journal of Corporate Finance, Vol. 15 No. 4, pp. 412–430, doi: 10.1016/j.jcorpfin.2009.04.003.

Ding, Y., Zhang, H. and Zhang, J. (2007), “Private vs State Ownership and Earnings Management: evidence from Chinese listed companies”, Corporate Governance: An International Review, Vol. 15 No. 2, pp. 223–238, doi: 10.1111/j.1467-8683.2007.00556.x.

van Eck, N.J. and Waltman, L. (2010), “Software survey: VOSviewer, a computer program for bibliometric mapping”, Scientometrics, Vol. 84, pp. 523–538, doi: 10.1007/s11192-009-0146-3.

Eissa, A., Elgendy, T. and Diab, A. (2023), “Earnings management, institutional ownership and investment efficiency: evidence from a developing country”, Journal of Financial Reporting and Accounting, doi: 10.1108/JFRA-10-2022-0392.

Elnahass, M., Salama, A. and Yusuf, N. (2022), “Earnings management and internal governance mechanisms: The role of religiosity”, Research in International Business and Finance, Vol. 59, p. 101565, doi: 10.1016/j.ribaf.2021.101565.

García Lara, J.M., García Osma, B., Mora, A. and Scapin, M. (2017), “The monitoring role of female directors over accounting quality”, Journal of Corporate Finance, Vol. 45, pp. 651–668, doi: 10.1016/j.jcorpfin.2017.05.016.

Gastón, S. and Jarne, J. (2010), “Have IFRS Affected Earnings Management in the European Union?”, Accounting in Europe, Vol. 7, pp. 159–189, doi: 10.1080/17449480.2010.511896.

Ghaleb, B.A.A., Kamardin, H. and Al-Qadasi, A.A. (2020), “Internal audit function and real earnings management practices in an emerging market”, Meditari Accountancy Research, Emerald Publishing Limited, Vol. 28 No. 6, pp. 1209–1230, doi: 10.1108/MEDAR-02-2020-0713.

Ghaleb, B.A.A., Qaderi, S.A., Almashaqbeh, A. and Qasem, A. (2021), “Corporate social responsibility, board gender diversity and real earnings management: The case of Jordan”, edited by Ntim, C.G.Cogent Business & Management, Cogent OA, Vol. 8 No. 1, p. 1883222, doi: 10.1080/23311975.2021.1883222.

Goncharov, I. (2005), Earnings Management and Its Determinants : Closing Gaps in Empirical Accounting Research, Frankfurt am Main [u.a.] : Lang.

Halaoua, S. and Boukattaya, S. (2023), “Board gender diversity and real earnings management: the moderating role of auditor reputation”, International Journal of Accounting, Auditing and Performance Evaluation, Inderscience Publishers, Vol. 19 No. 1, pp. 101–127, doi: 10.1504/IJAAPE.2023.130529.

Harakeh, M., El-Gammal, W. and Matar, G. (2019), “Female directors, earnings management, and CEO incentive compensation: UK evidence”, Research in International Business and Finance, Vol. 50, pp. 153–170, doi: 10.1016/j.ribaf.2019.05.001.

Hazarika, S., Karpoff, J.M. and Nahata, R. (2012), “Internal corporate governance, CEO turnover, and earnings management”, Journal of Financial Economics, Vol. 104 No. 1, pp. 44–69, doi: 10.1016/j.jfineco.2011.10.011.

Kardan, B., Salehi, M. and Abdollahi, R. (2016), “The relationship between the outside financing and the quality of financial reporting: evidence from Iran”, Journal of Asia Business Studies, Emerald Group Publishing Limited, Vol. 10 No. 1, pp. 20–40, doi: 10.1108/JABS-04-2014-0027.

Klein, A. (2002), “Audit committee, board of director characteristics, and earnings management”, Journal of Accounting and Economics, Vol. 33 No. 3, pp. 375–400, doi: 10.1016/S0165-4101(02)00059-9.

Koh, P.-S. (2007), “Institutional investor type, earnings management and benchmark beaters”, Journal of Accounting and Public Policy, Vol. 26 No. 3, pp. 267–299, doi: 10.1016/j.jaccpubpol.2006.10.001.

Krymskaya, A.S. (2023), “The Bibliometrics of Bibliometrics as a New Area of Research”, Scientific and Technical Information Processing, Vol. 50 No. 4, pp. 286–291, doi: 10.3103/S0147688223040147.

Kumar, M. and Vij, M. (2017), “Earnings Management and Financial Crisis: Evidence From India”, Journal of International Business and Economy, Vol. 18, pp. 84–101, doi: 10.51240/jibe.2017.2.4.

Leuz, C., Nanda, D. and Wysocki, P.D. (2003), “Earnings management and investor protection: an international comparison”, JOURNAL OF FINANCIAL ECONOMICS, presented at the Meeting of the European-Accounting-Association, Elsevier Science Sa, Lausanne, Vol. 69 No. 3, pp. 505–527, doi: 10.1016/S0304-405X(03)00121-1.

Liu, Q. and Lu, Z. (Joe). (2007), “Corporate governance and earnings management in the Chinese listed companies: A tunneling perspective”, Journal of Corporate Finance, Vol. 13 No. 5, pp. 881–906, doi: 10.1016/j.jcorpfin.2007.07.003.

Luo, J., Xiang, Y. and Huang, Z. (2017), “Female directors and real activities manipulation: Evidence from China”, China Journal of Accounting Research, Amsterdam: Elsevier, Vol. 10 No. 2, pp. 141–166, doi: 10.1016/j.cjar.2016.12.004.

Lyu, C. and Zhang, C. (2017), Executive Compensation and Earnings Management -An Empirical Study of Manufacturing Industry, doi: 10.2991/icedem-17.2017.2.

Mather, P. and Ramsay, A. (2006), “The Effects of Board Characteristics on Earnings Management around Australian CEO Changes”, Accounting Research Journal, Emerald Group Publishing Limited, Vol. 19 No. 2, pp. 78–93, doi: 10.1108/10309610680000680.

Mersni, H. and Ben Othman, H. (2016), “The impact of corporate governance mechanisms on earnings management in Islamic banks in the Middle East region”, Journal of Islamic Accounting and Business Research, Emerald Group Publishing Limited, Vol. 7 No. 4, pp. 318–348, doi: 10.1108/JIABR-11-2014-0039.

Mohammad, W.M.W. (2022), “Does internal and external governance reduce earnings management in family owned firms in Malaysia?”, International Journal of Business Governance and Ethics, Inderscience Publishers, Vol. 16 No. 2, pp. 129–157, doi: 10.1504/IJBGE.2022.121828.

Nguyen, A.H., Nguyen, L.H. and Doan, D.T. (2020), “Ownership Structure and Earnings Management: Empirical Evidence from Vietnam Real Estate Sector”, Real Estate Management and Valuation, Vol. 28 No. 2, pp. 37–51, doi: 10.1515/remav-2020-0014.

Nikulin, E.D., Smirnov, M.V., Sviridov, A.A. and Bandalyuk, O.V. (2022), “Audit committee composition and earnings management in a specific institutional environment: the case of Russia”, Corporate Governance: The International Journal of Business in Society, Emerald Publishing Limited, Vol. 22 No. 7, pp. 1491–1522, doi: 10.1108/CG-01-2021-0011.

Nyabakora, W.I. (2023), “Earnings management in public companies: a bibliometric review”, SN Business & Economics, Vol. 3 No. 9, p. 166, doi: 10.1007/s43546-023-00546-w.

Patra, R.K., Pandey, N. and Sudarsan, D. (2022), “Bibliometric analysis of fake news indexed in Web of Science and Scopus (2001-2020)”, Global Knowledge, Memory and Communication, Emerald Publishing Limited, Vol. 72 No. 6/7, pp. 628–647, doi: 10.1108/GKMC-11-2021-0177.

Pham, H.Y., Chung, R.Y.-M., Roca, E. and Bao, B.-H. (2019), “Discretionary accruals: signalling or earnings management in Australia?”, Accounting & Finance, Vol. 59 No. 2, pp. 1383–1413, doi: 10.1111/acfi.12275.

Pritchard, A. (1969), “Statistical Bibliography or Bibliometrics?”, Journal of Documentation, Vol. 25, pp. 348–349.

Sáenz González, J. and García-Meca, E. (2014), “Does Corporate Governance Influence Earnings Management in Latin American Markets?”, Journal of Business Ethics, Vol. 121 No. 3, pp. 419–440, doi: 10.1007/s10551-013-1700-8.

Surroca, J. and Tribó, J.A. (2008), “Managerial Entrenchment and Corporate Social Performance”, Journal of Business Finance & Accounting, Vol. 35 No. 5–6, pp. 748–789, doi: 10.1111/j.1468-5957.2008.02090.x.

Teixeira, J.F. and Rodrigues, L.L. (2022), “Earnings management: a bibliometric analysis”, International Journal of Accounting & Information Management, Emerald Publishing Limited, Vol. 30 No. 5, pp. 664–683, doi: 10.1108/IJAIM-12-2021-0259.

Thiruvadi, S. and Huang, H.-W. (2011), “Audit committee gender differences and earnings management”, Gender in Management: An International Journal, Vol. 26, pp. 483–498, doi: 10.1108/17542411111175469.

Triki Damak, S. (2018), “Gender diverse board and earnings management: evidence from French listed companies”, Sustainability Accounting, Management and Policy Journal, Emerald Publishing Limited, Vol. 9 No. 3, pp. 289–312, doi: 10.1108/SAMPJ-08-2017-0088.

Vagner, L., Valaskova, K., Durana, P. and George, I. (2021), “Earnings management: A bibliometric analysis”.

Vatis, S.E., Nerantzidis, M., Drogalas, G. and Chytis, E. (2023), “Connecting IFRS and earnings management: a bibliometric analysis”, Journal of Accounting Literature, Vol. ahead-of-print No. ahead-of-print, doi: 10.1108/JAL-02-2023-0036.

Yu, F. (Frank). (2008), “Analyst coverage and earnings management”, Journal of Financial Economics, Vol. 88 No. 2, pp. 245–271, doi: 10.1016/j.jfineco.2007.05.008.

Zang, A.Y. (2012), “Evidence on the Trade-Off between Real Activities Manipulation and Accrual-Based Earnings Management”, The Accounting Review, Vol. 87 No. 2, pp. 675–703, doi: 10.2308/accr-10196.

Zheng, C. and Kouwenberg, R. (2019), “A Bibliometric Review of Global Research on Corporate Governance and Board Attributes”, Sustainability, Multidisciplinary Digital Publishing Institute, Vol. 11 No. 12, p. 3428, doi: 10.3390/su11123428.