UNIAG, Instituto Politécnico de Bragança (IPB), Bragança, Portugal

Volume 2025,

Article ID 630933,

Journal of Accounting and Auditing: Research & Practice,

8 pages,

DOI: 10.5171/2025.630933

Received date: 23 June 2025; Accepted date: 18 July 2025; Published date: 19 September 2025

Academic Editor: Jose Lopes

Cite this Article as:

Joaquim LEITE, Joana FERNANDES and Ana FERNANDES (2025), " Navigating Profitability: A Cost Volume Profit Analysis in the Portuguese Inflatable Products Industry", Journal of Accounting and Auditing: Research & Practice, Vol. 2025 (2025), Article ID 630933, https://doi.org/10.5171/2025.630933

Companies in the industrial sector continue to face significant challenges in identifying specific solutions that support the formulation of strategies for the continuous improvement of cost management practices. This study focuses on the year 2020, marked by the onset of the COVID-19 pandemic, and aims to explore how Cost-Volume-Profit (CVP) analysis can be effectively applied to support managerial decision-making within a company specializing in the production of inflatables. The theoretical foundation of the research is grounded in management accounting, with an emphasis on CVP analysis as a tool for strategic planning and control. The methodological approach adopted is a qualitative case study, applied to a real-world manufacturing company. Financial and operational data – including costs, pricing structures, and production volumes – were obtained from internal records and documents. Quantitative data were processed and analyzed using Microsoft Excel, while qualitative insights were interpreted in alignment with the central research question. The results reveal how the company under study conducts expense planning and cost control and demonstrate the practical usefulness of CVP analysis in guiding strategic decisions, particularly during a period of economic instability and uncertainty. In practical terms, the CVP analysis enabled managers to identify easily correctable mistakes and discover new opportunities for operational improvement. The study also contributes to theoretical discussions by affirming the continued relevance and applicability of CVP analysis, even during an atypical and turbulent economic period.

This work is structured in five essential sections. The first section is the introduction, which provides a theoretical framework for Cost-Volume-Profit (CVP) analysis, contextualizing its relevance to the objectives of the study. The second section describes the methodology used. The third section is dedicated to presenting and analyzing the results. The last two sections include, respectively, a discussion of the results in the light of the theoretical framework and the formulation of the main conclusions of the research.

Management accounting and control practices play a fundamental role in companies in order to support decision-making and strategic cost management. These practices have been consolidated as an essential tool in the strategic orientation of contemporary organizations, both national and international, taking on a dynamic role in responding to the growing demands of complex business contexts. The concept of management control incorporates predictive information and performance indicators that support tactical and strategic decisions (Drury, 2018; Ferreira et al., 2019). In contexts of high competitiveness and pressure from consumers, all organizations face the challenge of adopting more efficient production structures, which requires highly qualified professionals and flexible and adaptable management tools (Drury, 2018).

In this context, management control is crucial for defining pricing policies, controlling costs and analyzing operational profitability, providing relevant information that is timely and tailored to the needs of decision-makers. This information covers both financial and operational variables and is essential for all stages of the management cycle, promoting continuous monitoring of organizational performance (Major & Vieira, 2017).

The classification of costs into fixed and variable, based on their relationship with the volume of production, is crucial for analyzing profitability and adopting appropriate costing methods (Ferreira et al., 2019). In-depth knowledge of costs is vital for effective financial management. Obtaining detailed information on the various cost components – such as raw materials, direct labor and overheads costs – allows for an accurate assessment of the company’s financial health and supports informed strategic decisions. Costing systems for measuring, recording and analyzing costs are mainly distinguished by their treatment of fixed industrial costs (Datar & Rajan, 2021).

The correct allocation of indirect costs is particularly relevant in diversified production environments. The use of allocation bases ensures an equitable distribution of expenses, in line with the principles of variable costing (Horngren et al., 2020). This procedure is in line with the recommendation in the literature, which advocates the adoption of objective and measurable criteria in the allocation of costs, as a way of ensuring the reliability of information to support management (Kaplan & Atkinson, 2015; Drury, 2018).

CVP analysis is a useful tool for decision-making, as it allows us to understand the interaction between fixed costs, variable costs, sales prices and production volume in determining profitability (Blocher et al., 2021). This analysis can identify loss-making products, support the definition of pricing policies and guide the composition of the production mix (Carvalho et al., 2020; Silva et al., 2021). The contribution margin, calculated as the difference between the sales price and variable costs, is a critical indicator for covering fixed costs and generating profit. However, this indicator tends to disregard the impact of fixed costs on pricing, which can lead to inappropriate decisions (Wernke et al., 2008).

Unit contribution margin analysis is particularly relevant for identifying situations in which the sales price is not sufficient to cover total variable costs, thus compromising the economic viability of certain products (Colpo et al., 2015). CVP analysis thus proves to be an indispensable tool in management accounting, especially in contexts marked by high uncertainty, allowing for more informed strategic decisions adjusted to market dynamics (Silva et al., 2021).

Through a CVP analysis, using quantities, expenses and income over a 4-year period, the financial break-even point in public hospital inpatient services was identified to support decision-making (Fadzil et al., 2023). CVP analysis applied to higher education explains how the break-even point can exceed the number of students enrolled during a given analysis period, indicating profit or loss (Oliveira et al., 2023). The outputs of this analysis provided the institution’s managers with valuable information to make a course economically viable. The critical break-even point defines the volume of sales needed to cover total costs without generating a profit or loss (Martins, 2003; Dutra, 2010). This indicator makes it possible to identify safety and operational risk zones. The safety margin, in turn, expresses the difference between the current sales volume and the critical point, functioning as an indicator of the organization’s resilience in the face of market fluctuations.

During periods of uncertainty or economic crisis, the rigidity of fixed costs can compromise the financial sustainability of companies, particularly when they have oversized structures in relation to the volume of activity (Fernandes, 2021; Oliveira & Martins, 2022). A corporate structure with high fixed costs limits the ability to adapt to drops in demand, amplifying the negative impacts on operating results (Santos & Santos, 2014; Costa et al., 2021). In these contexts, sensitivity analysis and systematic control of fixed and variable costs become essential for effective and resilient management (Cardoso, 2020).

Maintaining operational activity, even in the absence of an immediate financial return, can be a strategic decision geared towards organizational sustainability in the medium term (Fernandes, 2021; Oliveira & Martins, 2022). Recent experience reinforces the importance of organizational flexibility and the use of management control tools to support decision-making in highly volatile environments. CVP analysis, combined with a costing model suited to the organization’s operational complexity, proves to be a useful tool for optimizing decisions related to production, pricing and resource efficiency, contributing to the organization’s sustained viability and competitiveness (Carvalho et al., 2020; Silva et al., 2021; Blocher et al., 2021).

Based on the theoretical framework presented, a research question was established: how can Cost Volume Profit (CVP) analysis be used to support strategic decisions in a company in the inflatables production sector? This question arises from the need to use a tool to generate structured and relevant information for strategic cost management.

Methodology

The aim of this study is to understand how CVP analysis can be applied to support decision-making in an inflatables manufacturing company. The theoretical framework is CVP analysis (Blocher et al., 2021; Horngren et al., 2020; Silva et al., 2021). It is intended to help the manager of the company under study to understand how damaging the pandemic has been for the company and how it should readjust its strategic plans for the future, in terms of spending, quantities and sales prices. The research method used was the single case study (Yin, 2017). This methodological option of a holistic nature is often adopted in the field of business, including management control systems, especially in very particular contexts (Yin, 2017). It is a qualitative approach that is particularly appropriate for exploring “how” questions. Indeed, specific contexts justify the use of certain management control practices, which makes this method appropriate in qualitative research (Spanò et al., 2020).

Data were only collected from the company’s internal documents. The data collected were financial and non-financial, namely costs, prices and quantities. Through internal accounting documents, simplified business information, production reports and information in the company’s computer systems, it was possible to obtain the data needed to draw up the CVP analysis for 2020. The data were processed using the Excel tool.

Results

The industry dedicated to the production of inflatables and tarpaulins is part of a specialized segment of industrial activity whose importance is growing, especially in the fields of entertainment, advertising, event organization and logistics. It is a sector that combines typical manufacturing processes with technical design skills, distinguished by highly customized products, constant innovation in the materials used and the seasonal nature of demand.

The company that is the subject of this study has a diversified production structure, categorized into two major product groups: type I, corresponding to tarpaulins for fruit trimming machines, and type II, referring to inflatables. The diversity of internal references required a process of aggregation and simplification in order to allow a viable analysis of costs and income through CVP analysis. Type I products were grouped into five representative subgroups: “tarpaulin for machine 100” (P1), “add-on for machine 100” (P2), “tarpaulin for machine 75” (P3), “add-on for machine 75” (P4) and “tarpaulin for machine 65” (P5). Type II products were organized into seven categories according to their functional nature: “economy line” (P6), “bounce houses” (P7), “slides” (P8), “sports” (P9), “aquatic” (P10), ‘advertising’ (P11) and “decoration (P12)”.

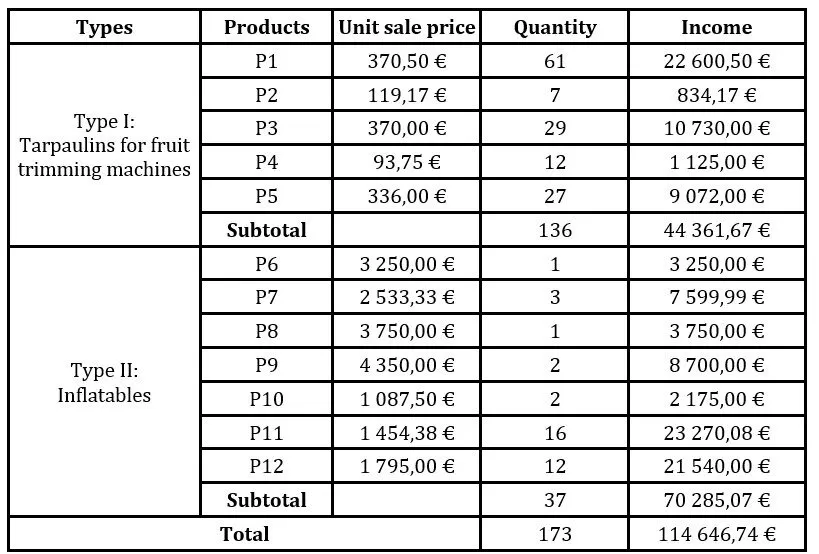

The quantities of products sold (Type I and Type II), as well as the unit prices and income generated in the year 2020 to which this study refers, are shown in Table 1.

Table 1. Sales prices, quantity sold and income for the Year 2020

Source: Authors’ own elaboration

The last income column was calculated on the basis of unit sales prices and quantities sold, showing a greater number of Type I units sold. Type II products, due to their higher added value and greater manufacturing complexity, have significantly higher sales prices.

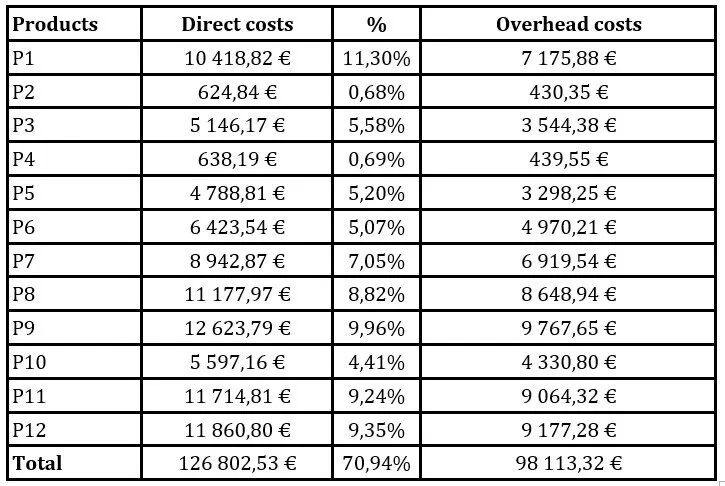

The breakdown of direct production costs (consumption of raw materials and direct labor) and indirect production costs (overhead costs) by the various end products is shown in Table 2.

Table 2. Allocation of production costs

Source: Authors’ own elaboration

In Table 2, the second column (consumption of raw materials and variable direct labor costs) is used to determine the variable unit production costs needed to apply the CVP analysis. The amount relating to direct labor was determined by allocating percentages of each employee’s working time to the respective products, based on the activities carried out during the production process. These percentages were then applied to the total labor costs, resulting in the estimated cost of variable direct labor per product.

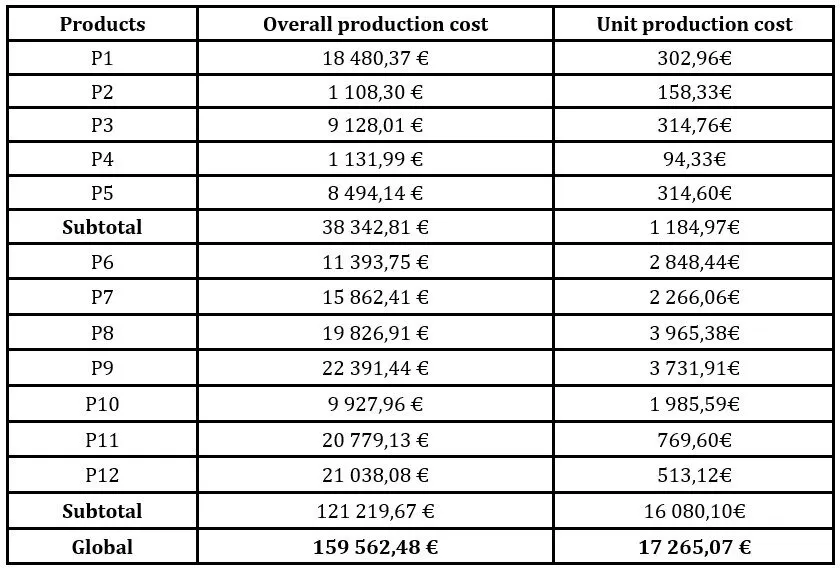

The third column shows the relative weight of each product in the company’s total variable costs. This ratio was used to allocate overhead costs proportionally, ensuring a balanced and reliable distribution of indirect costs. Thus, the unit costs of finished products, using the variable costing system, are shown in Table 3.

Table 3. Unit costs of manufactured products (variable costing system)

Source: Authors’ own elaboration

Table 3 shows the industrial cost of the finished product and its unit cost, using the variable costing methodology, which only considers variable costs directly related to production volume. The results show that the products classified as Type II, given their greater production complexity, recorded higher values for the industrial cost of the finished product and the respective unit cost, reflecting a greater intensity of direct resources applied per unit produced.

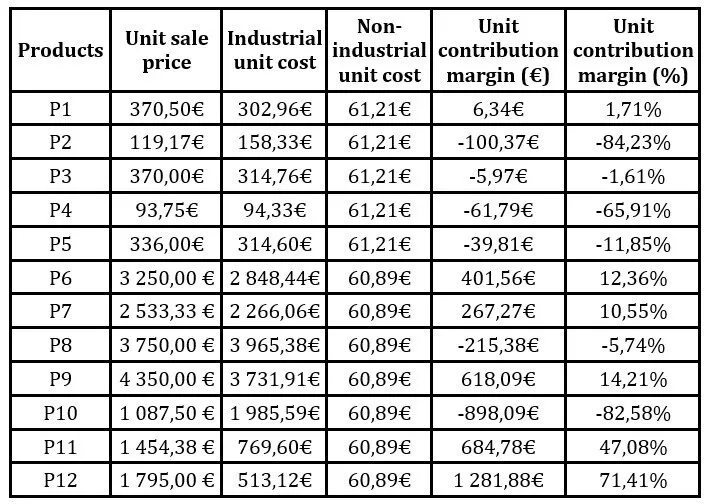

The absolute unit and percentage contribution margin is shown in Table 4.

Table 4: Unit contribution margin

Source: Authors’ own elaboration

Analysis of the unit contribution margin shows that, in 2020, most Type I products had negative margins. This means that the respective sales prices were insufficient to cover the total variable costs, both industrial and non-industrial, compromising the operating profitability of these products for a company that is in losses. For this reason of the lack of profits in an atypical period (the start of the Covid-19 pandemic), the breakeven point was not calculated for all the products, nor the contribution of each product to that breakeven point, either in quantity or value. It was possible to simulate increases or decreases in quantities for each of the 12 products studied, as well as changes in prices and costs with an impact on results. However, in management terms, the speculative interest of this exercise would be purely academic. This was followed by the preparation of the profit and loss account (see Table 5).

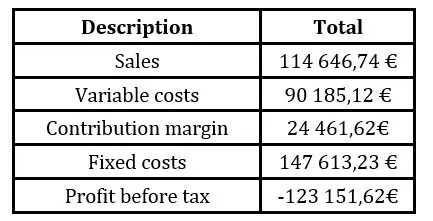

Table 5: Results for the year 2020

Source: Authors’ own elaboration

According to Table 5, in 2020 the company posted a negative net result, a direct consequence of the adverse impact of the COVID-19 pandemic, with a reduction in production activity, the adoption of lay-off measures and the partial discontinuation of operations. Production was partially maintained in order to ensure employment and the operational minimum, although at a loss as a result of maintaining a large part of the fixed costs.

Discussions

The use of variable costing made it possible to determine unit costs, allowing us to understand profitability by product (Horngren et al., 2020). In 2020, the majority of Type I products had negative contribution margins, indicating sales prices that were insufficient to cover total variable costs. This result compromised operating profitability and reinforced the relevance of CVP analysis as a strategic decision support tool, particularly when defining the production mix and pricing policy (Drury, 2018; Kaplan & Atkinson, 2015).

The adverse situation caused by the COVID-19 pandemic had a direct impact on the company’s financial performance, which recorded a negative net result. The partial maintenance of the activity, although loss-making, had a strategic purpose: to preserve operational continuity and protect human resources (Fernandes, 2021; Oliveira & Martins, 2022). However, the rigidity of the fixed cost structure, resulting from previous investments, made it difficult to adapt to the new economic context, amplifying the negative effects on profitability (Santos & Santos, 2014; Costa et al., 2021).

In addition, the results show the importance of integrated and technologically supported costing and control systems, especially in complex production environments. The adoption of tools such as CVP analysis is crucial to improving the quality of management information and supporting informed decisions in contexts of high uncertainty (Blocher et al., 2021; Fadzil et al., 2023). The experience analysed thus demonstrates the decisive role of management accounting in promoting efficiency, financial sustainability and strengthening the strategic capacity of organizations.

Conclusions

This research used the case study method in an inflatables production company to assess how the use of a management control tool can support management decisions. Among the management tools suggested at the company, CVP analysis stood out, which allowed a detailed analysis of production costs, sales volume and results for the pandemic year 2020. The study made it possible to understand how the company’s planning and cost control is carried out and how the CVP management tool can help with strategic decision-making. Through this analysis, carried out in the year in question, a negative result was observed, as a result of Covid-19, which affected the company’s activity on a large scale.

The fact that this study is a qualitative investigation applied to a single company, in a specific period associated with a pandemic context, very much focused on production costs, can be pointed out as the main limitation of this work. Another limitation was the fact that only one company manager was interviewed. Some ideas are suggested for future scientific research on the subject covered in this study. One recommendation would be to re-run the CVP analysis over a different period to see if there have been any improvements, which ones and in what respects. Finally, a more comprehensive study is recommended, comparing the company’s situation with other industries in the same sector of activity, specifically in the same area, inflatables.

References

Blocher, J., Juras, E. and Smith, S. (2021), ‘Cost management: A strategic emphasis,’ 9th, McGraw-Hill Education.

Carvalho, F. M., Fernandes, C. H. and Bandeira-de-Mello, R. (2020), ‘Gerenciamento de custos em ambientes de incerteza: uma abordagem baseada na análise CVR,’ Revista de Administração da UFSM, 13(4), 885–902. https://doi.org/10.5902/1983465934231

Cardoso, R. (2020), ‘Gestão estratégica de custos em tempos de crise: uma abordagem centrada na contabilidade de gestão,’ Revista Portuguesa de Contabilidade, 34(135), 45–60.

Colpo, G. S., Santos, L. M. and Lima, M. M. (2015), ‘Custeio variável como ferramenta para análise de rentabilidade em uma empresa industrial de pequeno porte,’ Revista de Contabilidade e Organizações, 9(24), 3–15. https://doi.org/10.11606/rco.v9i24.103143

Costa, P., Azevedo, G. and Ferreira, M. (2021), ‘Impacto da rigidez dos custos fixos na performance de PME industriais durante a pandemia,’ Revista de Contabilidade e Finanças, 32(85), 12–27. https://doi.org/10.1590/1808-057×20211234

Datar, S. and Rajan, M. (2021), ‘Horngren’s cost accounting: A managerial emphasis,’ (17 th). Pearson.

Drury, C. (2018), ‘Management and cost accounting,’ 10th, Cengage Learning EMEA.

Dutra, R. (2010), ‘Custos: Uma abordagem prática,’ 7 th, Atlas.

Fadzil, M. M., Puteh, S. E., Aizuddin, A. N., Ahmed, Z., Muhamad, N. A. and Harith, A. A. (2023), ‘Cost volume profit analysis for full paying patient services in Malaysia: A study protocol,’ PLoS ONE, 18(11), e0294623. https://doi.org/10.1371/journal.pone.0294623

Fernandes, M. (2021), ‘A resposta das empresas à pandemia: estratégias de resiliência e continuidade do negócio,’ Revista de Administração e Inovação, 18(3), 250–267. https://doi.org/10.1016/j.rai.2021.03.002

Ferreira, D., Caldeira, C., Asseiceiro, J., Vieira, J. and Vicente, C. (2019), ‘Contabilidade de gestão estratégica de custos e de resultados,’ 2nd, Rei dos Livros.

Kaplan, R. S. and Atkinson, A. A. (2015), ‘Advanced management accounting,’ 3rd, Pearson Education.

Major, M. J. and Vieira, R. (2017), ‘Contabilidade e controlo de gestão,’ 2nd, Escolar Editora.

Martins, E. (2003), ‘Contabilidade de custos,’ 9th, Atlas.

Oliveira, J. and Martins, A. (2022), ‘Gestão financeira em tempos de incerteza: lições da crise pandémica para as PME,’ Revista Contemporânea de Contabilidade, 29(1), 1–19. https://doi.org/10.5007/2175-8069.2022.e86213

Oliveira, J. N., Cintra, G. A. and Oliveira, M. A. (2023), ‘Sensitive analysis based on cost-volume-profit ratio,’ Revista FOCO – Interdisciplinary Studies, 16(6), e2152. https://doi.org/ 54751/revistafoco.v16n6-026

Santos, J. F. and Santos, M. (2014), ‘Os efeitos da rigidez dos custos fixos no desempenho financeiro das empresas: evidências do setor industrial português,’ Revista de Contabilidade e Finanças, 25(64), 62–76. https://doi.org/10.1590/rcf.v25i64.204

Silva, R. A., Ferreira, D. R. and Andrade, L. H. (2021), ‘A análise custo-volume-lucro como instrumento de apoio à tomada de decisão,’ Revista de Educação e Pesquisa em Contabilidade, 15(1), 1–20. https://doi.org/10.17524/repec.v15i1.2631

Spanò, R., Caldarelli, A., Ferri, L. and Maffei, M. (2020), ‘Context, culture and control: A case study on accounting change in an Italian regional health service,’ Journal of Management and Governance, 24(1), 229-272. https://doi.org/10.1007/s10997-019-09458-0

Yin, R. (2017), ‘Case study research and applications: Design and methods,’ 6th, Sage Publications.

Wernke, R., Lembeck, M. and Prudêncio, C. (2008), ‘Aplicação da análise custo/volume/lucro em pequena indústria de laticínios,’ Revista Catarinense da Ciência Contábil, 7(21), 53-70. http://doi.org/10.16930/2237-7662/rccc.v7n21p53-70.