Department of Accounting, Reporting, and Financial Analysis, Wrocław University of Economics and Business, Poland

Volume 2025,

Article ID 794776,

Journal of Accounting and Auditing: Research & Practice,

14 pages,

DOI: https://doi.org/10.5171/2025.794776

Received date: 18 March 2025; Accepted date: 30 June 2025; Published date: 29 July 2025

Academic Editor: Beata Sofrankova

Cite this Article as:

Bartłomiej NITA and Piotr OLEKSYK (2025), " Designing Intelligent Analytical Systems for Financial Risk Management in SMEs: Evidence from Interviews with Polish Managers ", Journal of Accounting and Auditing: Research & Practice, Vol. 2025 (2025), Article ID 794776, https://doi.org/10.5171/2025.794776

This study explores the financial safety challenges faced by small and medium-sized enterprises (SMEs) and investigates the information needs of their managers in mitigating financial risk. Based on structured interviews with 23 SME managers across various industries in Poland, the research identifies key internal and external data requirements as well as market threats contributing to financial instability. Particular emphasis is placed on the use of intelligent analytical tools to support decision-making under uncertainty. The study reveals that SME managers are aware of the necessity for prospective financial data and contextual forecasting, despite having limited resources. The findings highlight a strong demand for affordable, automated systems that can provide early warnings, simulate business scenarios, and filter relevant external signals. The paper concludes with a set of practical implications for the development of intelligent financial management systems tailored to SME needs.

Survival of small and medium-sized enterprises in a market dominated by big players is difficult. Corporations very often receive large orders associated with significant margins. On the other hand, large companies while doing contracts share risk with their subcontractors, but there is no profit sharing. Small entrepreneurs very often can only provide subcontracting services. Unfortunately, they also have to finance many of their tasks with their own means. Market-driven mechanisms enforce long payment terms which often exceed six months. Ultimately, SMEs finance the activities conducted by large corporations (Migliero, 2012) and do not receive any fee in the form of interest payments. Moreover, small entities must seek additional sources of funding on their own. This is also obvious that SME loans are more expensive than those dedicated to corporations. All these factors mean that small entities are forced to operate under risk that cannot be easily mitigated.

Risk is an inseparable part of doing business in case of any company. The concept of risk can be used in different meanings, but the most measurable concept of risk is the threat of failure to achieve the intended goals. Small businesses are most likely to be exposed to standard types of risk such as: risk of money collection, which leads to the problems with maintaining liquidity, risk of payment of short-term liabilities on time, risk of products aging, risk of excessive dependence of a company on one customer or supplier (see: Świerk, Banach, 2013, pp. 443-446). However, they are much less prepared to limit and mitigate risk. This is due to the negligible resources allocated for the purposes of risk management. SMEs do not generate such surplus, which allows for the implementation of effective hedging instruments (OECD 2014, p.48).

Risk estimation is not a straightforward activity, because it is very important to identify potential threats on an ongoing basis. This is also a difficult task due to the fact that managers spend most of their time on technical and operational issues (Mankins, 2014). Thus, it is necessary to design and implement an efficient information system that is aimed to point out the most important financial risks for SMEs system in a simple and understandable way. It should be mentioned that there are at least two problems associated with information support in SMEs. The first problem refers to excess data, and the other issue is the high cost of implementing tailor-made solutions.

The main objective of the paper is to identify the information needs of managers with respect to the financial safety in small and medium-sized enterprises as well as the root causes of financial problems in practice, and to propose the foundations for intelligent analytical approach that could be useful for managers in SMEs.

Methodology adopted in the paper includes the logical reasoning based on the experiment performed in the group of small entrepreneurs. As a result of this study, we present the essential elements used to support the development of intelligent financial safety management system along with the suggestions of decision-making pathways.

Research Background

Each company assesses various aspects of its business on an ongoing basis. The need for such evaluation results from the necessity to assess a company’s financial safety. Although this evaluation aspect should be perceived as a dominant factor in overall company assessment, the most important issue refers to the assessment of future prospects of a company. This is necessary to estimate the company’s ability to continue its operation in the future. Corporate financial safety is a problem directly related to company survival in the market. There are no perfect solutions that have been worked out to completely avoid the future threat. Small businesses often represent a relatively low level of equity that is a key item in the balance sheet to absorb unexpected losses. These losses are most often the result of the influence of the external environment on SME. Low capitals require the need to address financial safety in a different way taking into account that the key aspect is avoiding risk at lower cost. It is also very important to provide stable development financed by means of its own sources of financing. Significant increase in liabilities allows for rapid growth, but is also a frequent cause of rapid bankruptcy. An important issue to be taken into account in small business management is oriented towards risk management. Any managerial decision is subject to uncertainty and risk, which may result from the limited ability of a company to continue its operations. The most common causes of financial problems in small companies are bad debts and excessive levels of liabilities.

The above financial risks are closely related to problems with financial liquidity, and are not the only ones that cause SME bankruptcy. Two additional types of operational risk should be mentioned. The first one is an organizational risk that refers to the experience and qualifications of the staff employed, the rules of each department management, as well as the rules of interaction among organizational units. The second type of operational risk identified by some risk researchers is the legal risk. Legal risk can be defined as the probability of tangible and intangible loss arising from inappropriate preparation of legal acts. Due to the limited volume of the paper, we limit the scope of research to the financial aspects of risk.

Liquidity analysis is heavily based on estimating the ability of a company to pay its debt on time. It is also very important not to exceed the basic safety thresholds. Any analyses require examining current financial obligations, and may be based on different sources of information. While conducting liquidity analysis, the proper cash management should be taken into consideration with regard to the phases of the key repayment obligations. Improving financial liquidity also refers to accounts receivable, which are converted into cash in a normal business cycle. Insight into practice reveals that the most frequent cause of financial problems faced by many small business entities is the collection of receivables. Credit risk, which is understood in a special way as a potential loss due to the high level of the days sales outstanding ratio, is the most serious problem of SMEs in Poland. The threat of liquidity loss due to the problems with money collection is even more serious in corporations.

Liquidity management also requires detailed information in cash position, including information on cash surplus or cash deficit. It is concise information including cash in-flows and cash out-flows. Cash flow statement is very useful for estimating future cash flows, but the key aspect is to prepare such a report on a monthly basis. The information contained in the report allows to estimate the ability to generate excess cash in the various phases of the loan repayment.

The cash flow statement also reflects the entity’s activities performed in the field of liquidity management (Sneezer, Wiatr 2011, p. 39). Detailed information on money collection as well as increases or decreases in receivables and liabilities evaluates the quality of liquidity management and provides aggregate information on customer behavior. Detailed decomposition of cash flows is due to the need for comprehensive information on the impact of the company environment on its ability to acquire the current assets, and pay out liabilities. These operations cannot be implemented by means of increasing liabilities without making payments. Applying of additional external sources of financing cannot be perceived as an unfavorable situation and is not restricted by any legal regulation, but market practice has developed mechanisms to prevent a company from the liquidity problems arising from suppliers who drop further deliveries without obtaining a minimum payment for operations performed earlier. Detailed information on the various types of operations that significantly influence financial performance but do not generate cash is an important factor in assessing financial safety (Sniezek 2008, p. 21).

Financial liabilities are an indispensable source of financing business, but they are also a source of risk that is often the cause of the insolvency of a company. The main risk factor for liabilities is the lack of cash to pay debt on time. Exceeding the payment deadlines is related to legal actions against the company or other problems that disrupt business operations. Delay in paying short-term liabilities causes many problems. In particular, short-term liabilities significantly absorb cash and decrease operational capacity by reducing operational efficiency. Information on contracted liabilities in business entities is crucial for estimating the level of liquidity. Liquidity estimation is the basis for determining the short- and medium-term strategy of a company. Labilities are also important for the purposes of solvency estimation, i.e. long-term ability to conduct undisturbed business in the future and avoid bankruptcy.

LiteratureReview

Methods of bankruptcy prediction are broadly described in the literature and used by large corporations (Jones, Hensher, 2008, p. 3). In SMEs, there is a problem of excessive amount of information which leads to information noise that cannot be analyzed by their managers (Liew 2007, p. 4). In this situation, multi-dimensional analyzes interfere with proper decision making.

According to Altman (Altman et al., 2010, p. 9), using non-financial variables as predictors of company failure significantly improves the accuracy of prediction model. This is even more important for SMEs considering the lack of financial information available for some of them. Moreover, non-accounting information can be updated frequently, allowing financial institutions to correct their credit decisions in a timely manner.

The problem of managing financial safety in SMEs is also related to the lack of funds for financing both internal and external experts. (Brown, Lee, 2014 p. 15). SMEs often cannot employ professional analysts and managerial accounting specialists. The controllership function is shared by the accountant and the owner or manager. This situation results in a blur of responsibility and a lack of effective control. Hiring external consultants is very rare and the main support of the manager in SMEs is intuition (Wang, Walker, Redmond, 2007, p. 9).

Intuition in small entity management is obviously important, but cannot serve as a basis to solve all the managerial problems. While making decisions, there are not always ways to apply analogies to situations occurred in the past. Economic reality creates new problems that need to be solved on a regular basis. Then, intuition without a proper information support turns into gambling. Thus, a smart contextual information system may be helpful. Such a system should contain the rapid creation of simple simulations. It is also important that this solution is affordable for small entities.

In the area of small and medium-sized enterprises (SMEs), understanding the financial security and challenges they face is crucial to their longevity and success. Managers need specific information to identify financial risks, which is essential to mitigate potential problems such as insolvency and bankruptcy. Various studies have emphasized the importance of sound financial management and the creation of early warning systems to help SMEs recognize and effectively address these financial risks.

One of the significant approaches discussed in the literature is the implementation of IT systems designed to provide early warning of financial problems. Such systems rely on high-quality financial information from financial statements, enabling managers to make informed decisions. According to Chłodnicka and Zimon, early identification of bankruptcy risk can be achieved through dedicated assessment measures tailored to Polish SMEs, emphasizing the need for constant vigilance in financial reporting and analysis to avoid the risk of bankruptcy (Chłodnicka and Zimon, 2020, p. 7). Similarly, Kubičková et al. emphasize the importance of recognizing financial risk with the help of available information resources, which helps managers make appropriate decisions based on the company’s financial situation (Kubičková et al., 2025, p. 4).

In terms of understanding the root causes of financial distress, many factors contribute to the financial vulnerability of SMEs. Jindřichovská highlights critical issues in SME financial management, focusing on liquidity management and cash flow as essential elements that can lead to financial distress if not properly addressed. Their research indicates that effective cash management is crucial for preventing insolvency (Jindřichovská, 2013, p. 141). This viewpoint is complemented by the findings of Brijlal et al., who point to the need for better education of SMEs in financial management in order to reduce the likelihood of cash flow problems leading to business failure (Brijlal et al., 2014, p. 227). Furthermore, the identification of cash flow risks and the resulting risk management strategies can be systematically evaluated using methodologies such as the Analytic Hierarchy Process (AHP), as demonstrated by Alrawad et al. who presented a structured model for analyzing financial risk and cash flow risk as perceived by SME managers (Alrawad et al., 2023, p. 3).

Recent advances in predictive analytics also offer intelligent analytical approaches to help SME managers. Research by Kiseleva and Efimov suggests that the use of predictive analytics can significantly mitigate the risk of bankruptcy by providing insights into future financial challenges before they turn into crises (Kiseleva and Efimov, 2019). This predictive capability can complement traditional financial practices, guiding managers towards more proactive financial strategies. Furthermore, the growing adoption of Business Intelligence (BI) and Business Analytics (BA) in SMEs, as analyzed by Ericsson and Persson, emphasizes the importance of data-driven decision-making to increase financial security through better insights into business operations and market conditions (Ericsson and Persson, 2022, p. 5).

Furthermore, the use of the intellectual capital concept in bankruptcy prediction provides another layer of analysis for SMEs. Papíková and Papík argue that understanding and utilizing intellectual capital can provide SMEs with a competitive advantage that will increase their financial resilience (Papíková and Papík, 2023, p. 7). Thus, integrating these approaches – early warning systems, improved financial management education, predictive analytics, and the utilization of intellectual capital – creates a multi-faceted strategy for SMEs to cope with financial challenges and ensure sustainable operations.

It is necessary to conduct a research study on a smart financial safety management system that can be applied in small and medium-sized enterprises. This research should focus on: identifying the most serious threats, the management reporting system, the contextual use of decision pathways, and the simplified way of forecasting. The purpose of the study is to identify the information needs of managers with respect to the financial safety in small and medium-sized enterprises as well as the root causes of financial problems in practice, and intelligent analytical approach that could be useful for managers in SMEs. Methodology adopted includes structured interview in the focus group of managers responsible for SMEs.

Empirical Study

Design of the Study

The study began with introducing mangers with the fundamental problems of the financial safety in small enterprises. Participants were presented the results of research (Wiatr 2013 pp. 415-417) on bankruptcy causes of Polish small- and medium-sized enterprises in recent years. The most important economic measures related to financial safety have also been defined. This was necessary because many managers use internal reports and metrics created in many different ways.

The study was aimed to identify the most important factors in supporting the assessment of financial safety. For the purpose of the study, we developed a set of questions on the most important factors supporting comprehensive analysis of financial safety.

The study was conducted on a sample of 23 managers from micro and small companies. The surveyed participants were senior managers and owners. 15 of them are men and 8 are women. The majority (20) came from small enterprises, and 3 from micro enterprises. 14 of the respondents were CEOs and 9 were CFOs. 7 managers came from the agriculture sector, 5 from Construction, 4 from Manufacturing, 3 each from the Wholesale and Retail Trade and Transportation and Logistics sectors, and 1 from Information and Communication. Participants demonstrated different levels of knowledge and experience. The interview was conducted in two parts:

First part has a structured approach and respondents were asked a set of closed questions with suggested answers to be chosen,

Second part included two closed questions, and managers were encouraged to propose their own original answers.

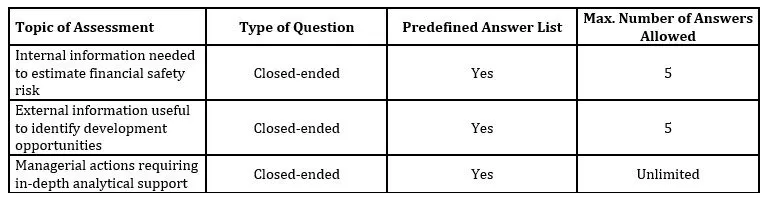

The ultimate aim of the first part of the research was to examine the information needs of SME managers important from the perspective of assuring the financial safety. The objective of the second part is to figure out the root causes influencing financial distress of the surveyed companies as well as to indicate the analytical approach to support how to overcome such issues. The structure of the research interview and groups of questions asked were briefly described in tables 1 and 2. In the first part of the interview, participants answered three structured questions: (1) regarding internal information used to assess financial safety (with a limit of 5 choices), (2) external information supporting enterprise development (5 choices), and (3) managerial actions requiring in-depth analysis (unlimited choices). The second part of the study consisted of two open-ended questions: (1) about specific market situations that caused financial difficulties in their companies (unlimited responses), and (2) about analytical tools managers believe should be implemented (up to 5 responses).

Table 1. Scope of Part I – Structured (Closed-Ended) Interview Questions

Source: Authors’ own.

Table 2. Scope of Part II – Open-Ended Interview Questions

Source: Authors’ own.

Participants disclosed their experiences about their own problems and suggested how to solve them. Asked questions focused on the inventory of financial safety risks. Important questions referred to the usefulness of the information system. The research was completed with a question about managers’ expectations of the proposed intelligent financial support system.

Research Findings

During the interview, various responses were offered to characterize the impact of individual decisions on the entity’s future financial position. Participants in the focus group indicated a lot of original answers to the key elements of the company’s financial safety management system. In the first section, participants were given the opportunity to indicate more than one answer. Summary of the answers obtained during the first part are presented in table 3, 4, and 5.

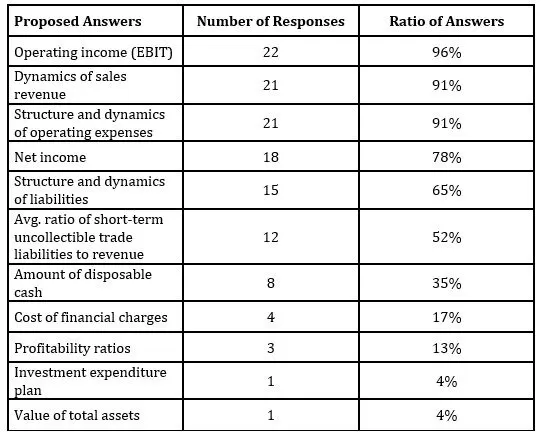

Table 3. Internal Information Used to Estimate Financial Safety Risk

Source: Authors’ own.

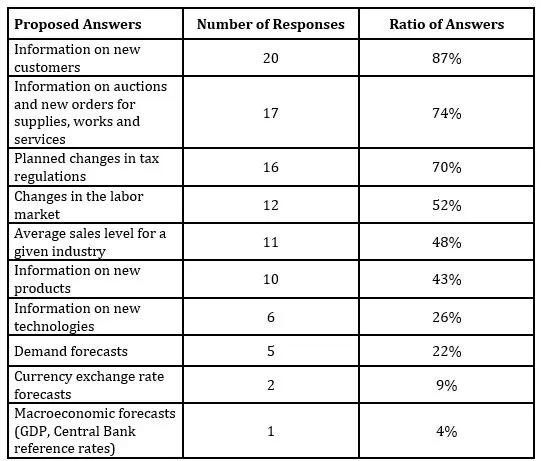

Table 4. External Information Used to Identify Development Opportunities

In addition to selecting predefined answers, several participants provided their own original insights in open comment fields. With regard to internal information needed to estimate the risk of financial safety, some managers emphasized the importance of monitoring the utilization rate of machines and equipment, expressed as average monthly usage time, in order to assess the level of operational waste. Others pointed to the need for identifying the most important risk factors that may threaten the company in the near future, which goes beyond purely financial indicators. In the context of external information supporting enterprise development, participants highlighted the relevance of performance and financial results achieved by market competitors, as well as access to information about external European Union aid funds, which they viewed as crucial to planning and growth. Finally, in response to the question on managerial actions requiring in-depth decision-making analysis, one participant noted the strategic importance of applying for public support instruments for business development, particularly under conditions of financial constraint or market transition. The results of the survey presented in Table 3, 4, and 5 show the use of standard financial information. While answering the first question, participants indicated typical balance sheet items and profit and loss accounts for current financial risk management of the company. More than half of the participants consider it important to report bad receivables and their relation to sales revenue. This is not a standard report generated by customer relationship management systems. Other non-standard managerial information is the level of use of fixed assets. This kind of information is very helpful in estimating waste, but it was indicated only by one participant.

Managers appreciate the need for using tools to track external market symptoms. Additionally, they point out that there is a need for information support in SME management. Among the most important information coming from the business environment is information related to the potential for increased sales such as information on new customers and new orders. Managers need to keep track of changes in the employment structure on the labor market trends. This is related to the growing problem of attracting new employees. Also, the activities performed by direct competitors are important for estimating the level of financial safety. In this part of the interview, managers rarely added their own answers outside the open list. It was possible during the second part of the research. The questions that were included in the second part of the study are detailed in Tables 6 and 7.

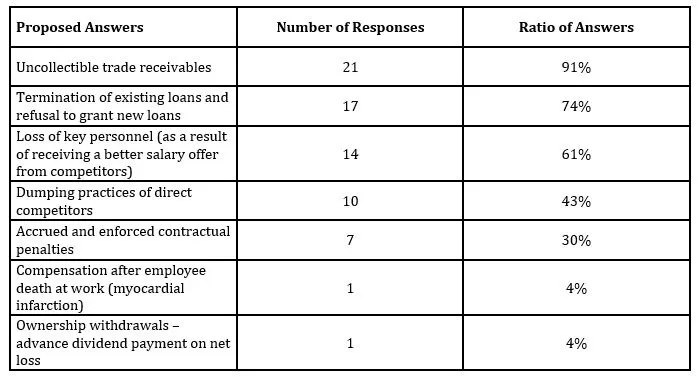

Table 6. Market Situations That Have Caused Financial Problems

Source: Authors’ own.

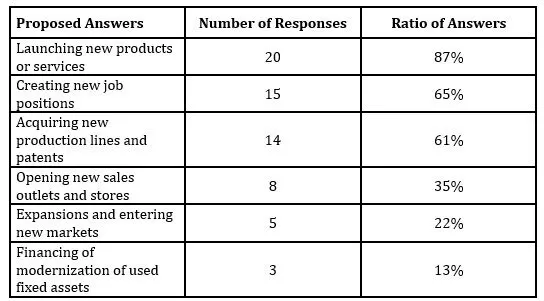

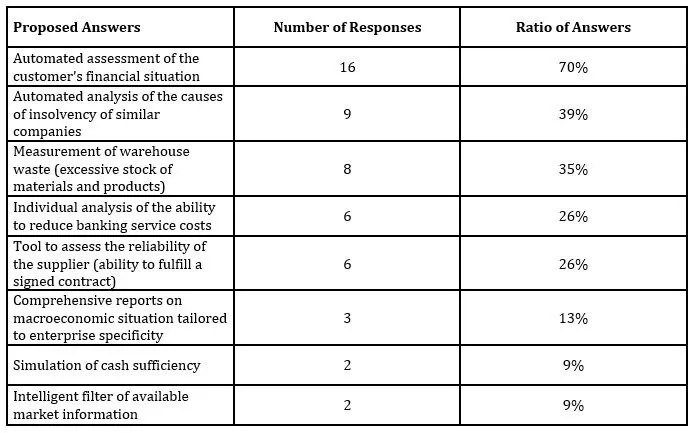

Table 7. Analytical Tools Considered Necessary by Managers

Source: Authors’ own.

In addition to predefined answers, one participant also proposed the development of an automated system for forecasting revenues, costs, and financial flows based on individual assumptions, emphasizing the need for personalized analytical solutions in financial decision-making processes.

The results indicate two major threats that significantly impact the functioning of SMEs. The first is the risk of unreliable customers, as bad debts lead to substantial financial losses. The second threat arises from the actions of competitors. In an effort to increase their market share, competitors often engage in predatory pricing by offering more attractive conditions, which may result in the loss of key customers. Another harmful practice is the poaching of key employees. Hiring experienced staff from rival companies is often considerably more cost-effective than investing in the internal training and development of new employees. In addition, many respondents identified the loss of stable external financing as a major risk. Some managers also suggested the need to develop forecasting systems for revenues, costs, and cash flows based on individual business assumptions.

Results presented in tables 6 and 7 confirm that the most important problem in SMEs is the lack of implementation of contextual solutions. The key conclusion of the study is that there is a need to simulate future business results in an automated way. These simulations are intended to be analytical support for decision-making process oriented towards company development. Another conclusion from the research refers to the expectations for the complexity of the solutions needed. Managers need simple and understandable solutions and applications. They strongly point to the need to implement new solutions. They are not interested in the simplification of solutions used in large corporations. Attention is drawn to the need for external information filtering. This is related to the limited perception of managers. It is not a matter of their competence but a matter of limited time. Solving current operational problems does not allow for in-depth insight in the future.

Research Limitations

The main limitations of the study include: (1) the size and nature of the research sample, (2) the subjectivity of respondents’ answers, (3) the lack of comparison with larger companies, (4) limitations in access to financial data, (5) the dynamics of changes in the economic environment, and (6) the lack of a full analysis of the behavioural aspects of decision-making.

The study was conducted on a relatively small group of 23 SME managers, which may limit the possibility of generalising the results to the entire population of small and medium-sized enterprises. The companies included in the study operated in different industries, which may lead to differences in the approach to financial risk management. Furthermore, the opinions of the participants are subjective and based on their individual experience, which can lead to simplifications in the perception of financial risk and information needs.

Another limitation is the lack of comparison with larger companies. The study focused exclusively on SMEs, not taking into account the differences in financial security management in large organisations, which could have provided a broader context for the analysis. In addition, many SMEs do not conduct detailed financial analyses or use simplified reporting methods, which could have affected the quality of the information provided. In particular, the lack of complete data on cash flows and liability structures could have made it difficult to accurately assess financial risks.

The results of the study reflect the market situation at the time of the study, which means that they may change depending on macroeconomic conditions, new legal regulations or unpredictable external factors such as economic crises. It is also worth emphasising that the study did not fully consider the behavioural aspects of financial decision-making by SME managers, which can have a significant impact on the way financial risk is managed.

Managerial Implications

The results of the study show that internal reporting must necessarily be supplemented with information coming from the entity’s business environment. Market signals, the basis of managerial decisions, provide external sources of information describing the activities of other companies, customers and the public administration. An entrepreneur who is in financial difficulty, if it is not possible to avoid unacceptable risk, must seek other solutions. In such a situation, it is necessary to seek information on the availability of credit, aid funds or potential new strategic investors and changes in the macroeconomic situation.

The information on cash flow and liabilities is very important and helpful in estimating the entity’s ability to continue its operations (Samonas, 2015, p. 39). Reliable information on total financial obligations and cash surplus of the entity is very important especially while deciding on strategic objectives, which affect both strategic plans and operational budgets. This past information is not enough, thus it is necessary to develop forecasted data. The process of forecasting financial results is essential in the effective management of any company. This allows managers to look into the future and analyze various scenarios. First of all, preparing forecasted report allows recognizing conditions and constraints in which a company is likely to operate. Financial forecast is obviously uncertain, but it is an acceptable version of the future position of the company. All financial projections should be adjusted taking into account the industry in which the company operates as well as macroeconomic and strategic factors, and managerial experience. The financial forecast is complementary to the financial analysis conducted based on historical data, and this is the next step informing about possible future threats to the enterprise.

It is necessary to carry out detailed research on the determination of external symptoms taking into account the size of the company and the industry in which it operates. Symptoms may be understood as a conjunction of the results of particular indicators derived from compulsory financial reporting along with the measurable trends and changes in its environment.

Managers in SMEs usually base their decisions on intuition. They are often aware of the work to be done and the processes to be carried out. However, they cannot fully assess the financial implications of managerial actions. It is even more difficult to assess the overall financial impact of a planned project to be taken into consideration. To clarify the need to implement a contextual-based decision support system, we will use the following example.

The example refers to a development project scenario for automotive company. The assumptions are as follows:

Based on publicly available macroeconomic information, the manager acquires knowledge on the increased demand for car parts and components. This information is related to the national strategy for the development of electro-mobility.

Additional signal coming from the company’s environment is the intensified recruitment of competitors.

There is a significant risk of losing key personnel, because competitors are aware of the potential for increased production and actively looking for experienced employees. Some employees in the analyzed company choose to accept the competitive offers.

If a manager is predominantly engaged in technological problems, they may be able to recognize the described signals too late for an ad hoc decision.

The above situation is not favorable and should not happen in practice. By using an intelligent analytical system, the manager does not need to track market symptoms on his own. The warning signal will be generated by the system. An effective system should propose various solutions tailored to managerial problem. Examples of potential scenarios include:

Proposal to change the salary conditions offered to current employees.

Implementing technological innovations to reduce the labor hours needed.

The assessment of both above scenarios should be carried out using all available internal and external information.

Scenario no. 1 (changing the salary conditions offered to current employees) requires the following information:

Liquidity, Debt and Sales profitability ratios;

Forecast of operating income;

Break-Even-Point forecasts including increased wage costs;

Availability of aid funds to increase the innovation level.

Developed scenarios should be implemented on the basis of concrete performance achieved by the company. It is therefore necessary to establish the minimum and maximum targets for selected internal measures that should trigger off the decisions associated with specified scenarios. Appropriate automation and visualization of the discussed process will allow developing a model of system supporting financial safety management in small and medium enterprises.

Conclusions and Future Research Directions

Financial safety management in small and medium-sized enterprises is an extremely difficult process. The most important problems of the functioning of SMEs refer to ensuring the operational continuity, ongoing customer service, and technological aspects. Building an internal information system based on managerial needs is a complex and expensive process. There are many limitations identified:

SMEs do not have the sufficient internal resources (both human resources and monetary resources) in small and medium-sized enterprises available for such implementations. Thus, it is crucial to develop an intelligent system that is affordable to SMEs. In case of mass implementation for thousands of small entrepreneurs, the solution could be profitable for the software provider.

Access to the appropriate information is also problematic, because information required by surveyed managers may be hardly obtainable. It is difficult to analyze and evaluate the reasons behind SME bankruptcy based only on external information. Financial failure analysis very often requires internal information that is not publicly available.

It is also needed to take into account behavioral aspects. Very difficult task refers to the problem of maintaining key personnel. Once employees announce their intention to accept a competitive offer, this is not always sufficient to announce additional motivational packages.

The research conducted allows drawing up the following conclusions:

Although SMEs are not required to prepare cash flow statement, managers are aware that there is a need to create reports that contain cash flow information. This is a key element in SME financial safety management.

Business unit managers are aware of the need to use prospective information to reduce financial risks. However, they are more interested in strategic plans, which absorb free cash, and forecasting based on factors coming from the business environment.

The study clearly shows that there is a need for the development of intelligent systems supporting financial security management. The warning system should include an intelligent external information filter.

It is very difficult to use tailor-made solutions in small and medium-sized enterprises. The primary limitation is the cost of adapting the smart system to the needs of a particular business. There are unique situations in every company that cannot be predicted. This is another limitation that hinders the automation of analytical process. The solution could be the use of the so-called knowledge network to gather information about new threats and risks. Participants of this network would jointly develop appropriate risk management methods. Network knowledge can be the basis for preparing improved decision-making patterns.

Future works should focus on the feasibility analysis of implementing solutions such as decision-making pathways and quick visualization of decisions including forecasts of cash flows and financial liquidity. Such forecasts should be adjusted to market conditions and company performance. These activities are too difficult for SME managers to handle, because they do not have enough expertise and internal resources to design such intelligent solutions. It is also important to figure out ways of searching for external information. Taking into account both internal and external information, it would be possible to develop leading and lagging indicators useful for managers. Additionally, these systems should offer interactive simulation trees along with advanced visualization techniques. The software vendor may use big data approach which makes such intelligent systems affordable for SMEs, because IT companies may earn based on a large number of small customers.

References

Alrawad, A., Tensil, J., & Zouravliov, A. (2023). Managers’ perception and attitude toward financial risks associated with SMEs: Analytic hierarchy process approach. Journal of Risk and Financial Management, 16(2). https://doi.org/10.3390/jrfm16020086

Altman E.I., Sabato G., and Wilson N. (2010), The value of non-financial information in small and medium-sized enterprise risk management, „The Journal of Credit Risk”, 6, no. 2.

Brijlal, P., Tengeh, R., & Ibuowo, A. (2014). The use of financial management practices by small, medium and micro enterprises: A perspective from South Africa. Industry and Higher Education, 28(4), 223-232. https://doi.org/10.5367/ihe.2014.0223

Brown, R., Lee N. (2014) Funding issues confronting high growth SMEs in the UK ICAS, Edinburgh

Chłodnicka, A., & Zimon, G. (2020). Bankruptcy risk assessment measures of Polish SMEs. WSEAS Transactions on Business and Economics, 17, 1-10. https://doi.org/10.37394/23207.2020.17.3

Dudycz H. (2013), Map of Concepts as a Visual Representation of the Knowledge in Economy, Wydawnictwo Uniwersytetu Ekonomicznego we Wrocławiu, Wrocław (in Polish)

Ericsson, A., & Persson, M. (2022). A review of business intelligence and analytics in small and mediumsized enterprises. Journal of Enterprise and Business Intelligence. https://doi.org/10.53759/5181/jebi202202009

Gordini, N. (2014). A genetic algorithm approach for SMEs bankruptcy prediction: Empirical evidence from Italy. Expert Systems with Applications, 41(4), 1229-1245. https://doi.org/10.1016/j.eswa.2014.04.026

Jindřichovská, A. (2013). Financial management in SMEs. European Research Studies Journal, 16(4), 132-146. https://doi.org/10.35808/ersj/405

Jones S. (Ed.) & D. A. Hensher (Ed) (2008), Advances in Credit Risk Modelling and Corporate Bankruptcy Prediction, Cambridge, Cambridge University Press.

Kiseleva, N., & Efimov, A. (2019). Predictive analytics as an instrument to prevent bankruptcy. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3677898

Kubičková, J., Šebestová, J., & Novák, P. (2025). Innovative approach to business education in SMEs in the knowledge economy of the 21st century. International Journal of Instruction. https://doi.org/10.29333/iji.2025.1818a

Liew A. (2007) Understanding Data, Information, Knowledge And Their Inter-Relationships Journal of Knowledge Management Practice, Vol. 8, No. 2, June 2007

Mankins M. (2014) Stop Wasting Valuable Time, Harvard Business Review, September 2004

Migliero S. (2012), “Getting to yes when banks say no. Bifurcated collateral loans provide incremental liquidity”, Abf Journal, September 2012

OECD (2014), Public SME Equity Financing – Exchanges, Platforms, Players, OECD Financial Roundtable meeting, 23 October 2014, OECD, Paris, DAF/CMF(2014)19

Papíková, A., & Papík, J. (2023). Application of intellectual capital in SME bankruptcy. Applied Economics. https://doi.org/10.1080/00036846.2023.2281291

Samonas M., (2015) Financial Forecasting, Analysis and Modelling: A Framework for Long-Term Forecasting John Wiley & Sons.

Širá, T., Szarowská, M., & Adamec, F. (2016). Using of risk management at small and medium-sized companies in the Slovak Republic. Economic Annals-XXI, 156(3-4), 33-40. https://doi.org/10.21003/ea.v156-0016

Śnieżek E. (2008), How to use cash flow statement?, “Rachunkowość” 2008vol. 1

Śnieżek E., Wiatr M. (2011), Interpretation and analysis of cash flows: reporting and managerial approach, Wolters Kluwer Business, Warszawa

Świerk J., Banach A. (2013) Bankruptcy of Polish enterprises in 2009-2012, “Zarządzanie i Finanse” 2013 vol. 2

Wang C., Walker E., Redmond J. (2007) Explaining the Lack of Strategic Planning in SMEs: The Importance of Owner Motivation International Journal of Organisational Behaviour, Volume 12(1), Edith Cowan University Research Online

Wolmarans, H., & Meintjes, A. (2015). Financial management practices in successful small and medium enterprises (SMEs). The Southern African Journal of Entrepreneurship and Small Business Management, 7(1), 8-19. https://doi.org/10.4102/sajesbm.v7i1.8