University of Zagreb, Faculty of Economics and Business, Zagreb, Croatia

Volume 2026,

Article ID 925305,

Journal of Accounting and Auditing: Research & Practice,

14 pages,

DOI: doi.org/10.5171/2026.925305

Received date: 27 November 2025; Accepted date: 26 February 2026; Published date: 24 March 2026

Academic Editor: lukasz Brzezinski

Cite this Article as:

Ivana BARIŠIĆ (2026), " Data Analytics and AI-Enabled Technologies in Internal Audit: A Review of Recent Research through the Lens of Theory of Technology Dominance ", Journal of Accounting and Auditing: Research & Practice, Vol. 2026 (2026), Article ID 925305, https://doi.org/10.5171/2026.925305

The research focus of this paper is based on the analysis of the application of Data Analytics and Artificial Intelligence in internal auditing. Although the current use of DA and AI in internal audit is still limited, especially the use of AI,this early adoption phase is crucial for studying their professional implications and ensuring their responsible and safe future integration into the audit process. The paper examines the reasons for the adoption of these technologies, their impact on the audit process, and the implications of long-term use through the lens of the Theory of Technology Dominance. A semi-structured literature review is employed to systematically identify, analyse, and synthesise recent empirical findings to address research questions, analysing recent research in the period from 2021-2025, focusing on academic papers indexed in WOS. Results point out that the maturity level of acceptance of these technologies in internal audit is still quite low, but evidence has been found confirming the use of generative AI in the audit process. Also, reliance on these technologies faces various challenges, such as the need for adequate skills and the costs of implementation. Also, these modern technologies have an influence on the change in the paradigm of internal audit towards continuous audit, as well as significant implications for greater effectiveness of the risk-based approach. The analysed research was least oriented towards the long-term implications of using the researched technologies, which provides a basis for conducting further research in the area, especially in the context of ethical implications for internal auditors’ decision-making.

Keywords: internal auditing, Data Analytics, Artificial Intelligence, Theory of Technology Dominance

Introduction

Contemporary academic debate increasingly highlights the need for internal audit to strengthen its strategic identity and contribute not only to oversight, but also to organisational development and corporate governance enhancement. Once a function centred primarily on testing internal controls, it has gradually developed into a role with expectations to provide proactive, forward-looking support to governance structures and to become “ an active builder” within the organisation (Lenz & Hoos, 2023). Looking ahead, the internal audit function is expected to deliver broader value to stakeholders, articulate its professional mandate more clearly and embrace technologically driven practices (Lenz & Jeppesen, 2022). The digital transformation of organisations provides internal audit with a unique opportunity to redefine its contribution by leveraging new analytical and intelligent technologies. In today’s digital environment, the use of technology in audit processes is becoming part of the professional requirements defined by the new Global Standards for Internal Auditing (IIA, 2024). In this environment, technological adaptability is becoming a prerequisite for the continued relevance of the profession.

Despite high expectations, internal audit functions still show a low level of digital maturity. According to global surveys of internal audit practice, most internal audit functions are in the early stages of digital transformation, despite the recognised importance of digital tools, primarily due to the lack of necessary knowledge and skills (IAF and Deloitte, 2021). This finding is consistent with research in the accounting profession, according to which the accounting profession is often slow to adopt new technologies, especially in the areas of big data analysis (Big Data) and Data Analytics (DA) (Tang et al., 2017). According to a global study by Protiviti (2018), data analytics in internal audit has limited utility, most commonly in traditional financial processes and transaction-intensive areas. Despite the proven benefits: greater efficiency, broader coverage, and better risk detection, adoption remains. This highlights the gap between the potential of advanced analytics and actual practice, and underscores the need for further research into the conditions and barriers to its adoption. According to the results of a research review (Ramadhan et al., 2023) from a recent period, the implementation of audit analytics (AA), which is defined as: “the process of identifying, gathering, validating, analyzing, and interpreting digital data using information and communication technology to further the purpose and mission of internal auditing” in internal auditing, mainly encourages the growth of the amount of digital data, the limitations of traditional auditing approaches, and the increased expectations of stakeholders for faster and better security, with the support of increasingly strong technological possibilities (p.6). At the same time, the application of AA is mostly hindered by insufficient competence of auditors, high investment costs, challenges in cooperation between internal auditors and users and other assurance providers, within the audit process, and limited access to quality data (p.12).

The impetus for faster development came during the pandemic, which accelerated the application of technologies such as Data Analytics and Artificial Intelligence, opening up new opportunities to strengthen audit capabilities. Artificial intelligence (AI) is considered one of the most important technologies for the future of internal audit, as confirmed by 74% of respondents in the global Vision 2035 survey (IIAF &Audit Board, 2024). Despite this, the current use of AI in audit functions is very low, with 77% of respondents reporting that they use it almost never. Only 18% of internal auditors currently apply AI in audit activities, indicating a large gap between expectations and reality (IIAF &Audit Board, 2024). However, some early adopters are already developing first uses of AI, indicating the direction of future development of the profession. Although it is expected that Artificial Intelligence will be more involved in the audit process in the immediate future, according to existing research, its inclusion and impact in the internal audit context are insufficiently explored (Wassie & Lakatos, 2024).

Given these findings, it is important to examine in detail the benefits and risks of applying digital technologies in internal audit, which is the central focus of this paper. Previous research shows that the application of advanced DA and AI in auditing is an increasingly common topic in the academic community, but the focus of most studies is in the area of external audit (Kokina et al., 2025; Wagener et al., 2025). Wassie & Lakatos (2024) conducted the first systematic review of the literature on AI in the function of internal audit and identified only 15 papers published between 2019 and 2023. Their analysis showed that the application of AI in internal audit is still in its early stages, geographically limited and theoretically underdeveloped. Although their work represents an important starting point, it encompasses broad concepts of AI and includes studies that also apply to external audit.

This paper builds on their findings, but differs in that it narrowly focuses exclusively on internal auditing use of DA and AI through the analytical framework of Theory of Technology Dominance (TTD). This gives a more specific and detailed insight into how modern technologies affect the internal audit process. Although the current implementation of DA and AI in internal audit is still low, it is the early adoption phase that represents a key moment for researching the professional implications of technologies, to ensure a responsible and safe integration of technologies into the audit process in the future.

The research questions of the paper are loosely based on the Theory of Technology Dominance (TTD) (Arnold & Sutton, 1998), as the analysis interprets the findings of recent empirical work through the prism of its three fundamental parts: (1) reliance or non-reliance on technology, (2) short-term effects of technology on decision-making, and (3) long-term risks of technology implementation, where the risks related to internal auditors, as stated in the analyzed papers, will be investigated. It is important to emphasise that the aim of the paper is not to test the theory, but rather to use the conceptual parts as a kind of interpretive lens for the analysis of recent research in the field of internal auditing. Given the above, the research questions of the paper are as follows:

RQ1: What does recent empirical research reveal about internal auditors’ adoption and reliance on Data Analytics and AI at different stages of the audit process?

RQ2: What short-term benefits and challenges of applying Data Analytics and AI does the existing literature identify in the context of internal audit effectiveness, quality, and performance?

RQ3: What potential long-term implications and ethical risks do the authors identify regarding the use of Data Analytics and AI in internal audit, including possible changes in competencies and professional responsibility?

An analysis of recent research that considers the short-term and long-term dimensions of the application of Data Analytics and Artificial Intelligence in internal audit will complement existing knowledge in the field of internal audit research, which is still underdeveloped at the level of academic research, but also as a function (Chammaa et al., 2025), especially in the area of the application of Artificial Intelligence. Considering both the advantages and disadvantages of using these technologies, the paper provides a comprehensive overview of the research topic in papers published in the Web of Science database, in the period 2021–2025.

The remainder of this paper is structured as follows. Section 2 outlines the methodology employed to analyse recent research, intending to address the research questions. Section 3 presents the results of the theory-driven thematic synthesis, organised according to the dimensions of the Theory of Technology Dominance, covering analysis of adoption and use, short-term effects, and long-term implications. The final section discusses the key insights, contributions, limitations and avenues for future research, and concludes the paper.

Methodology

This paper adopts a semi-systematic literature review approach, as proposed by Snyder (2019), which combines elements of systematic search procedures with a narrative, often theory-driven synthesis. The methodology is broadly based on steps outlined in Amani and Fadlalla (2017), based on Khlif and Chalmers (2015) (involves: scoping of the study; identification of search terms; data sources identification and article collection; article filtering; content evaluation; synthesis and framework development).

This paper focuses on the recent application of Artificial Intelligence and Data Analytics techniques in internal auditing through the analytical framework of Theory of Technology Dominance.

Search terms included: internal audit*, “internal auditor* and broader search terms regarding Data Analytics and Artificial intelligence: search terms artificial intelligence, machine learning, deep learning, intelligent system, expert system, neural network, algorithmic decision, predictive analytics, Data Analytics, continuous audit*, automated audit”, “CAAT*.

A paper was included if: it primarily deals with internal audit, contains the application of DA or AI, describes benefits, risks, process phases or implementation, was published in 2021-2025, or published in a peer-reviewed journal or conference (open access). Papers were excluded if they were not related to internal audit or described technology, but not in the context of internal audit.

Search resulted from 102 documents (open access articles and proceeding papers, English language), reduced to only those that related to the internal auditing context, resulting in 26 papers. In the last step, records were manually inspected to only include papers that satisfy the described inclusion criteria and one article (also indexed in WOS) was also identified with the snowballing method and taken into consideration for the analyses. A total of 16 academic papers were included in the further analyses.

In the content evaluation stage, analysis was focused on bibliographic data, the type of technology examined (DA/AI), the internal audit tasks and phases addressed, the reported benefits and risks, short-term benefits, and long-term professional implications. The framework for analysis is loosely based on TTD, and organised into three dimensions: reliance/use in the audit process, short-term effects and long-term implications, and divided according to the analysed technologies (Data Analytics and AI) as described in the next section of the paper.

Analysis of Research Results

Analysis of research results on the acceptance of DA in internal audit, short-term effects and challenges of application and long-term effects of application

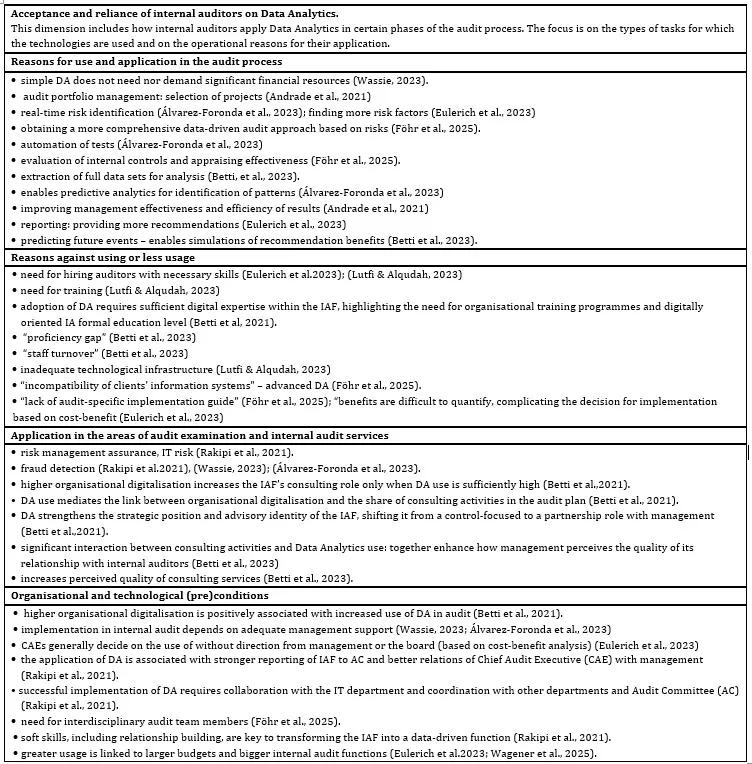

According to the analysed papers (Table 1) related to the use of DA in the IAF, the reasons related to its acceptance and application in the audit process are diverse. Regarding the application of simple DAs, the reason that their implementation does not require significant financial resources is emphasised (Wassie, 2023). Related to the higher levels of development of DA and their application in the internal audit process, it is applied throughout the entire audit process, from the selection of audit projects (Andrade et al., 2021), to its use in the planning phase where risks are assessed on which audit activities and resources will be directed, which in most cases are limited either due to the number of personnel or financial constraints. The use of DA in the procedures that characterise internal audit planning enables the identification of risks in real time (Álvarez-Foronda et al., 2023), as well as the identification of multiple risk factors (Eulerich et al., 2023). Ultimately, this means that the entire audit approach is more strongly oriented to the risk-based approach, which is at the centre of all requirements related to the approach to internal audit, in addition to the fact that this procedure is data-driven (Föhr et al., 2025).

In the phase of critical examination, better known as audit fieldwork, the use of DA enables the automation of testing (Álvarez-Foronda et al., 2023), the evaluation of the effectiveness of internal controls (Föhr et al., 2025) based on the analysis of the entire data set (Betti et al., 2023), and also enables a more precise and comprehensive observation of anomalies and unusual patterns related to the test subjects, as well as predictive analysis (Álvarez-Foronda et al., 2023). Ultimately, this should lead to greater efficiency and effectiveness of audit results (Andrade et al., 2021), which is also an identified reason for relying on DA in internal audit. In addition to the above, the possibility of providing more recommendations is emphasised (Eulerich et al. 2023), and DA allows foresight of future events (Betti et al., 2023), which enables internal auditors to see more clearly the consequences of the recommendations they provide to users and their expected impact.

Although the previously mentioned reasons are a good basis for adopting DA in internal audit, the results of the analyzed research show that the degree of DA application in the analyzed period is still very weak (Eulerich et al., 2023; Lutfi & Alqudah, 2023). Positive developments towards the use of advanced DA have been identified (Wagener et al., 2025), but the results vary in different geographical areas and are more consistent with more developed countries (such as Germany, Austria, and Switzerland). The most common reason against the use or lower level of acceptance of DA in internal audit is the need to hire new internal auditors with the necessary skills (Eulerich et al.2023; Lutfi & Alqudah, 2023), which is a real limitation in conditions of limited financial resources, as well as the need to train existing staff (Lutfi & Alqudah, 2023) given the identified “proficiency gap” (Betti et al. 2023) related to the use of DA, and limitations in this regard are also due to “staff turnover” (Betti et al. 2023). There are also proposals to include technology education at the level of internal auditors’ initial professional development and to make it part of formal education at a higher level of education (Betti et al, 2021), which could also have a long-term impact on reducing the costs of training and additional education of audit staff.

In addition to the problem related to the skills of internal auditors, the problem of inadequate technological infrastructure was also identified (Lutfi & Alqudah, 2023), i.e. the incompatibility of company information systems (Föhr et al., 2025), which prevents the full usefulness of DA, as well as the lack of guidelines for the implementation of DA (Föhr et al., 2025). In addition, it is emphasised that the benefits of applying technology are difficult to measure, i.e. they are difficult to quantify, which makes the decision to apply DA in internal audit difficult, given that it has been established that this decision is based on a cost-benefit analysis (Eulerich et al.2023).

In the context of the analysis of the application of DA in audit areas and types of services, s, it is possible to conclude that, in addition to being used in assurance engagements related to risk management engagements, it is also used in fraud detection and IT audits (Rakipi et al. 2021; Wassie, 2023; Álvarez-Foronda et al., 2023). Namely, according to some findings (Betti et al., 2021), internal audit consulting engagements increase when internal audit makes greater use of data analytics, particularly in conditions of a higher level of organisational digitalisation. Data Analytics acts as a mediator between the digitalisation of the organisation and the advisory services provided by internal auditors, enabling the role of internal audit in such organisations to shift “from a control-focused to a partnership role with management” (Betti et al., 2021). Ultimately, this contributes to an increased perception of the quality of the internal audit function by management.

Regarding the organizational and technological conditions related to the application of DA in internal audit, according to the above mentioned, it was determined that a higher level of organizations’ digitalisation is positively related to the increased use of DA in internal audit (Betti et al., 2021), and implementation of DA depends on management support (Wassie, 2023; Álvarez-Foronda et al., 2023). There have also been cases when CAEs independently decided on the application of DA in internal audit, based on a cost-benefit analysis, which, as previously stated, is difficult due to the difficulty in quantifying benefits (Eulerich et al., 2023). The application of DA in internal audit is associated with stronger reporting to the Audit Committee, as well as a better relationship with management (Rakipi et al., 2021) because it provides greater informative value to the information and conclusions that internal audit communicates to its users.

The successful implementation of DA in internal audit requires cooperation with the IT department and the audit committee (Rakipi et al., 2021), the interdisciplinary nature of the audit team (Föhr et al., 2025), as well as soft skills that are essential for the transformation of the internal audit function into a “data-driven” function” (Rakipi et al., 2021). It was also established that greater use of DA in internal audit is related to larger internal audit departments and higher budget levels (Eulerich et al., 2023; Wagener et al., 2025), which is expected considering the necessary investments related to the implementation and education of audit staff.

Table 1: Research results on the acceptance of DA in internal auditing

(analyses of recent WOS indexed research from 2021-2025)

Source: Author based on literature review

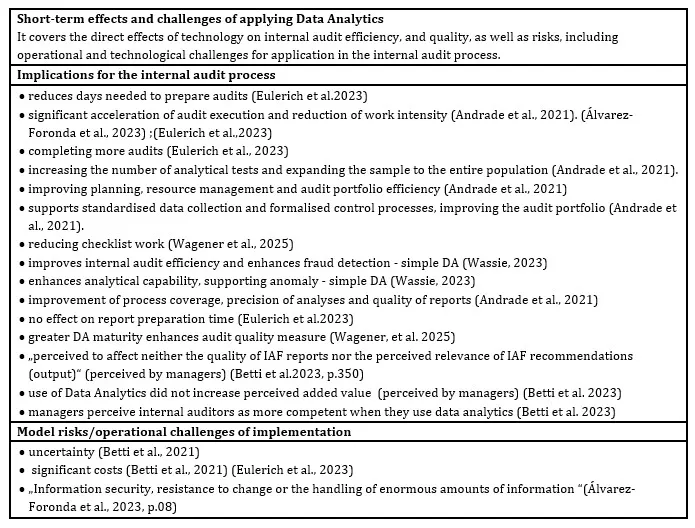

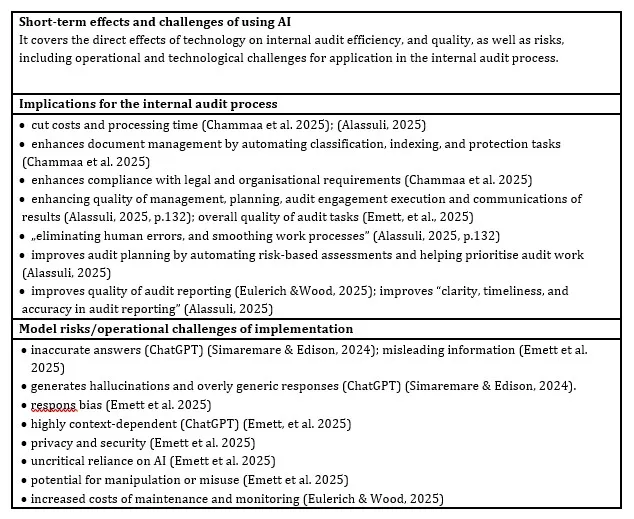

Regarding the short-term effects and challenges of implementing DA in internal audit, the analysis (Table 2) focuses on the immediate effects of these technologies on efficiency, quality, and risks, including operational and technological challenges (risks) related to their implementation in the internal audit process. According to the analysis, data analytics is used at all stages of the internal audit process, and its effects include: a significant reduction in the time required for audit preparation (Eulerich et al., 2023); a substantial acceleration of audit task execution with reduced work intensity for audit staff (Andrade et al., 2021), which ultimately enables the performance of a greater number of audit engagements (Eulerich et al., 2023). The following conclusions were established: improved planning, data collection, resource management, and audit portfolio efficiency (Andrade et al., 2021); an increased number of analytical tests and expansion of the sample to the entire population (Andrade et al., 2021); reduced checklist work (Wagener et al., 2025); enhanced analytical capability through simple DA (Wassie, 2023); and improved process coverage, analytical precision, and report quality (Andrade et al., 2021).

The use of DA, even simpler models, also enhances fraud detection through increasing analytical possibilities and research of detected anomalies (Wassie, 2023), but no effects on shortening the time for preparing the audit report were observed (Eulerich et al. 2023). However, some contradictory results were also observed, that is, while in some studies it was found that a higher level of DA maturity increases the measure of audit quality (Wagener, et al. 2025), in others it was found that the use of DA does not affect the usefulness of recommendations perceived by management, nor does it increase the perceived added value of internal auditors, although management perceives internal auditors as more competent in the case of using DA (Betti et al. 2023). Also, uncertainty (Betti et al., 2021) and information security (Álvarez-Foronda et al., 2023), as well as significant costs in implementing more advanced DA (Betti et al., 2021), and resistance to change (Álvarez-Foronda et al., 2023) were detected as risks, or operational challenges of implementation.

Table 2: Research results on short-term effects and challenges of Data Analytics use in internal auditing

(analyses of recent WOS indexed research from 2021-2025)

Source: Author based on literature review

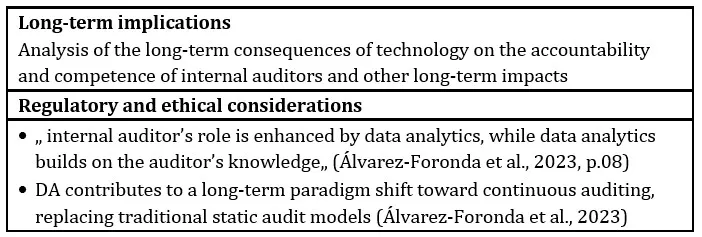

In the context of the analysis of long-term implications (Table 3), not many findings were found, except for individual ones according to which “internal auditor’s role is enhanced by data analytics, while data analytics builds on the auditor’s knowledge” (Álvarez-Foronda et al., 2023, p.08) with an indication of a change in the internal audit paradigm static model towards continuous auditing (Álvarez-Foronda et al., 2023).

Table 3: Research results on long-term implications of Data Analytics use in internal auditing

(analyses of recent WOS indexed research from 2021-2025)

Source: Author based on literature review

Analysis of research results on the acceptance of AI in internal audit, short-term effects and challenges of application, and long-term effects of application

An analysis of available research on the use of artificial intelligence in internal audit shows that very few papers address this technology, analyse it, or provide proposals for implementing (mostly) GenAI. Moreover, almost all of these papers were published only in 2024 and 2025, which clearly indicates a lack of academic research on this topic.

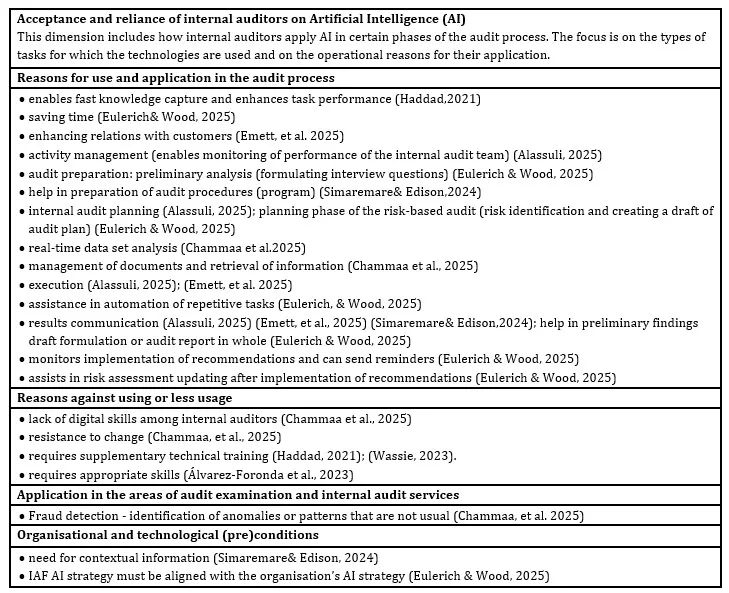

Regarding the reasons for accepting AI and its application in the audit process (Table 4), similar conclusions were found as for the reasons for accepting DA. They relate to cost savings, improved execution (Haddad, 2021), time savings (Eulerich & Wood, 2025), and improved relations with audit clients (Emmett et al., 2025). The possibility of using AI to supervise the performance of the audit team was also identified (Alassuli, 2025). Regarding the internal audit process, AI can be used in the preparation of audit assignments and preliminary analyses, especially in preparing questions for employee interviews (Eulerich & Wood, 2025), in developing the audit program (Simaremare & Edison, 2024), and in risk analysis during the planning phase and the creation of an audit plan (Alassuli, 2025; Eulerich & Wood, 2025). This is further supported by the capability for real-time data analysis (Chammaa et al., 2025). In conducting fieldwork, AI is used in the management of documents as well as in information recovery (Chammaa et al., 2025), it also automates repetitive tasks (Eulerich & Wood, 2025) during execution. Communicating the results is a phase in which AI has significant application possibilities (Simaremare & Edison, 2024; Alassuli, 2025; Emett et al., 2025), with the possibility of using it when preparing a draft report or a complete report (Eulerich & Wood, 2025). In addition to the mentioned phases, it is also possible to use it in the phase of monitoring the implementation of recommendations (Eulerich & Wood, 2025) and in risk assessment after the implementation of recommended activities, i.e. corrections or corrective actions (Eulerich & Wood, 2025).

As with the results related to the application of DA, the following reasons stand out for the limited or reduced use of AI in internal auditing: the lack of digital skills among internal auditors, resistance to change (Chammaa et al., 2025), the need for appropriate auditor competencies (Álvarez-Foronda et al., 2023), and the need for additional technical training (Haddad, 2021; Wassie, 2023). As in the earlier analysis, the application of AI in fraud detection is highlighted due to its ability to identify unusual patterns (Chammaa et al., 2025). Concerning organisational and technological conditions, emphasis is placed on AI’s need for contextual information (Simaremare & Edison, 2024) and on the recommendation that the IAF’s AI strategy must be aligned with the organisation’s AI strategy (Eulerich & Wood, 2025), which improves follow-up efficiency.

Table 4: Research results on the acceptance of AI in internal auditing (analyses of recent WOS indexed research from 2021-2025)

Source: Author based on literature review

In the context of the analysis of the short-term effects and challenges of the application of artificial intelligence in internal audit (Table 5), it is determined that costs and processing time are reduced (Chammaa et al. 2025); (Alassuli, 2025), and that they enable better management of the documentation collected through the audit process (Chammaa et al. 2025). It has also been found that the use of AI increases compliance with regulatory requirements (Chammaa et al.2025), as well as the overall quality of audit tasks (Emett, et al. 2025) and reduces the possibility of human error (Alassuli, 2025). Regarding the reporting phase, AI improves the quality of audit reporting (Eulerich &Wood, 2025), especially in terms of “clarity, timeliness, and accuracy in audit reporting” (Alassuli, 2025).

As risks of applying AI in internal audit, the analysed papers mention the problem of incorrect answers (e.g., ChatGPT) (Simaremare & Edison, 2024), misleading information (Emett et al., 2025), and the issues of hallucination and response bias (Emett et al., 2025), which are highly context-dependent (Emett et al., 2025). Concerns have also been expressed regarding privacy and security (Emett et al., 2025), uncritical reliance on AI and the potential for manipulation or misuse (Emett et al., 2025), as well as higher maintenance and monitoring costs (Eulerich & Wood, 2025).

Table 5: Research results on short-term effects and challenges of AI use in internal auditing

(analyses of recent WOS-indexed research from 2021-2025)

Source: Author based on literature review

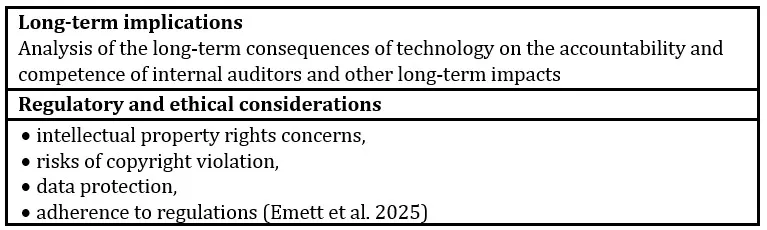

As in the case of the analysis of the long-term implications of the use of DA in internal audit, there are no discussions or conclusions on this topic in the field of artificial intelligence applications either. The terms mentioned in this context include issues related to intellectual property rights, the potential for copyright breaches, data privacy requirements, and the need to comply with regulatory standards (Emmett et al., 2025).

Table 6: Research results on long-term implications of Data Analytics use in internal audit

(analyses of recent WOS-indexed research from 2021-2025)

Source: Author based on literature review

Conclusion

An analysis of recent research publications published in the WOS (CC) database during the period from 2021 to 2025 found that there is significant room for development of the application of Data analytics and Artificial Intelligence (AI) in internal audit. The results obtained are consistent with the results of previous research (Ramadhan et al., 2023; Wassie & Lakatos, 2024) and reports of professional associations and organisations (IAF and Deloitte, 2021; IIAF & Audit Board, 2024). Although a limitation of the research is the fact that the analysed works were indexed only in the WOS database, these findings complement existing conclusions about the level of digital maturity of internal audit in the recent period.

Through the prism of TTD, the reasons for internal auditors’ adoption and reliance on Data Analytics and AI at different stages of the audit process, as well as short-term benefits and challenges of applying Data Analytics and AI, were investigated. The reasons for adopting Data Analytics are most often associated with improved risk identification, better planning, the ability to analyse a complete set of data and the recognition of unusual patterns. In the end, better effectiveness and efficiency of the results, as well as recommendations resulting from audit engagements, are made possible, but the strengthening of internal audit advisory activities is also made possible. These advantages could ultimately overcome the barriers that prevent the increase of the maturity level of the application of data analytics in internal audit, where the lack of appropriate skills of internal auditors is most often highlighted, which requires additional investments by organisations, and can have a long-term effect on changes within the formal education of internal auditors.

Also, the application of DA in internal audit is influenced by the degree of digitalization of the organization, as well as management support, while, on the other hand, greater use of DA affects a better relationship with internal audit users, although, as stated in the previous part of the paper, certain findings show that management sometimes does not perceive the benefits of DA-driven internal audit.

The use of AI in internal audit also brings numerous benefits in the context of the efficiency and effectiveness of the audit process, as well as in the field of fraud detection, as is the case with the application of Data Analytics. Large language model chatbots, despite risks such as response bias and provision of incorrect information, find their place in the practice of internal auditing and are also identified within the analysis of this paper (Simaremare & Edison, 2024; Emmett et al., 2025; Eulerich et al., 2025; Chammaa et al., 2025). Their capabilities in terms of risk identification, analysis of procedures, creation of audit plans and reports provide significant opportunities for improving the usefulness of internal audit results.

Although one of the aims of the paper was to analyse the long-term implications mentioned in the context of the application of the mentioned technologies, few publications directly address this issue. The findings mostly relate to the paradigm shift towards continuous auditing, without detailed analyses of the impact on the competencies and professional responsibility of internal auditors. This confirms the need for further research, especially in the area of ethical implications of the application of cognitive technologies. In the context of the work of internal auditors in the conditions of the digital economy, it is important to note that technology brings new challenges that can affect the judgment of the internal auditor. In the digital economy, technology brings numerous advantages, but also new challenges that can affect the judgment of the internal auditor. What represents a challenge in modern audit practice, but will certainly be a challenge in the future, is the use of technology in a way that does not take precedence in drawing conclusions arising from audit engagements.

Notes

Acceptance and reliance of internal auditors on Data Analytics

The dimension maintains a conceptual link with the “reliance” phase from the theory of technology dominance, but is adapted to empirical research that primarily refers to patterns of use and functional benefits in specific audit tasks, rather than motivational factors of acceptance.

Acceptance and reliance of internal auditors on Artificial Intelligence (AI)

The dimension maintains a conceptual link with the “reliance” phase from the theory of technology dominance, but is adapted to empirical research that primarily refers to patterns of use and functional benefits in specific audit tasks, rather than motivational factors of acceptance.

References

Alassuli, A. (2025), ‘Impact of artificial intelligence using the robotic process automation system on the efficiency of internal audit operations at Jordanian commercial banks, ‘ Banks and Bank Systems, 20(1), 122–135.

Álvarez-Foronda, R., De-Pablos-Heredero, C. and Rodríguez-Sánchez, J.-L. (2023), ‘Implementation model of data analytics as a tool for improving internal audit processes,’ Frontiers in Psychology, 14.

Amani, F., and Fadlalla, A. (2017), ‘Data mining applications in accounting: A review of the literature and organizing framework’, International Journal of Accounting Information Systems, (24), 32-58.

Andrade, A., Penha, R.,and Ferreira da Silva, L. (2021), ‘Use Of Data Analytics Tools For Increased Efficiency In The Internal Audit Project Portfolio’, Journal on Innovation and Sustainability RISUS, 12(03), 138–149.

Arnold, V. and Sutton, S.G. (1998), ‘The theory of technology dominance: understanding the impact of intelligent decision aids on decision makers’ judgments’, Advances in Accounting Behavioral Research, 1, 175-194.

Betti, N., DeSimone, S., Gray, J. and Poncin, I. (2023), ‘The impacts of the use of data analytics and the performance of consulting activities on perceived internal audit quality’, Journal of Accounting & Organizational Change, 20(2), 334–361.

Betti, N., Sarens, G. and Poncin, I. (2021), ‘Effects of digitalisation of organisations on internal audit activities and practices’, Managerial Auditing Journal, 36(6), 872–888.

Chammaa, H., Ed-Daoudi, R. and Benazzi, K. (2025), ‘Large Language Models for Academic Internal Auditing’, InternationalJournal of Advanced Computer Science and Applications, 16(1).

Emett, S., Eulerich, M., Lipinski, E., Prien, N. and Wood, D. A. (2025), ‘Leveraging ChatGPT for Enhancing the Internal Audit Process -A Real-World Example from Uniper, a Large Multinational Company’, Accounting Horizons, 39(2), 125–135.

Eulerich, M. and Wood, D. A. (2025), ‘A Demonstration of How ChatGPT and Generative AI Can be Used in the Internal Auditing Process’, Journal of Emerging Technologies in Accounting, 22(2), 47–77.

Eulerich, M., Masli, A., Pickerd, J. and Wood, D. A. (2023), ‘The Impact of Audit Technology on Audit Task Outcomes: Evidence for Technology‐Based Audit Techniques’, Contemporary Accounting Research, 40(2), 981–1012.

Föhr, T. L., Reichelt, V., Marten, K.-U. and Eulerich, M. (2025), ‘A Framework for the Structured Implementation of Process Mining for Audit Tasks’, International Journal of Accounting Information Systems, 56.

Haddad, H. (2021), ‘The Effect of Artificial Intelligence on the AIS Excellence in Jordanian Banks’, Montenegrin Journal of Economics, 17(4), 155–166

Internal Audit Foundation and Delloitte (2021), ‘Internal Audit Foundation Premier Global research study (2021) Assessing Internal Audit Competency: Minding the gap to maximize insights [Online], [Retrieved November 2, 2025], https://www.theiia.org/en/content/research/foundation/2021/assessing-internal-audit-competency-minding-the-gaps-to-maximize-insights/

Internal Audit Foundation and Audit Board (2024), ‘Demystifying AI: Internal Audit Use Cases for Applying New Technology. [Online], [Retrieved November 1, 2025] https://www.theiia.org/en/content/research/foundation/2024/demystifying-ai-internal-audit-use-cases-for-applying-new-technology/

Khlif, H., and Chalmers, K. (2015), ‘A review of meta analytic research in accounting’, Journal of Accounting Literature, 35, 1-27.

Kokina, J., Blanchette, S., Davenport, T. H. and Pachamanova, D. (2025), ‘Challenges and opportunities for artificial intelligence in auditing: Evidence from the field’, International Journal of Accounting Information Systems, 56, 100734.

Lenz, R. and Hoos, F. (2023), ‘The Future Role Of The Internal Audit Function: Assure. Build. Consult’, EDPACS, 67(3), 39–52.

Lenz, R. and Jeppesen, K. K. (2022), ‘The Future Of Internal Auditing: Gardener Of Governance’, EDPACS, 66(5), 1–21.

Lutfi, A. and Alqudah, H. (2023), ‘The Influence of Technological Factors on the Computer-Assisted Audit Tools and Techniques Usage during COVID-19′. Sustainability, 15(9), 7704.

Protiviti (2018), ‘Analytics in Auditing is a game changer. [Online], [Retrieved October 15, 2025] https://www.protiviti.com/sites/default/files/2022-06/2018-internal-audit-capabilities-and-needs-survey-protiviti.pdf

Rakipi, R., De Santis, F. and D’Onza, G. (2021), ‘Correlates of the internal audit function’s use of data analytics in the big data era: Global evidence’, Journal of International Accounting, Auditing and Taxation, 42, 100357.

Ramadhan, M. G., Janssen, M.,and Van der Voort, H. (2023), ‘Driving and Inhibiting Factors for Implementing Audit Analytics in an Internal Audit Function’, Journal of Emerging Technologies in Accounting, 20(2), 135–163.

Simaremare, M. and Edison, H. (2024), ‘The State of Generative AI Adoption from Software Practitioners’ Perspective: An Empirical Study’, 2024 50th Euromicro Conference on Software Engineering and Advanced Applications (SEAA), 106–113.

Snyder, H. (2019), ‘Literature review as a research methodology: An overview and guidelines’, Journal of Business Research (104), 333–339

Tang, F., Norman, C. S. and Vendrzyk, V. P. (2017), ‘Exploring perceptions of data analytics in the internal audit function’, Behaviour & Information Technology, 36(11), 1125-1136.

The Institute of Internal Auditors (2024), ‘The Global Internal Audit Standards. [Online], [Retrieved October 15, 2025] https://www.theiia.org/en/standards/2024-standards/global-internal-audit-standards/free-documents/complete-global-internal-audit-standards/

Wagener, M., Eulerich, M. and Bonrath, A. (2025), ‘From Pen-and-Paper to Technology-Driven Analytics: Technology Usage in Internal Auditing’, Journal of Information Systems, 39(3), 39–66.

Wassie, F. and Lakatos, L. (2024), ‘Artificial intelligence and the future of the internal audit function’, Humanities and Social Sciences Communications,11(386).

Wassie, F. A. (2023), ‘Leveraging computer-assisted audit tools for corporate sustainability: Evidence from Ethiopia. Journal of Infrastructure’, Policy and Development, 8(1).2690.