Silesian University in Opava, School of Business Administration in Karvina, Czechia

Volume 2022,

Article ID 856279,

Journal of Eastern Europe Research in Business and Economics,

11 pages,

DOI: 10.5171/2022.856279

Received date: 24 September 2020; Accepted date: 16 August 2022; Published date: 11 October 2022

Academic Editor: Fran Galetic

Cite this Article as:

Irena Szarowská (2022)," Does Fiscal Decentralization Matter for Economic Development? Case of the Czechia", Journal of Eastern Europe Research in Business and Economics Vol. 2022 (2022), Article ID 856279, DOI: 10.5171/2022.856279

Economic growth and performance is influenced by a number of internal and external factors. The goal of the article is to explore the relationship between fiscal decentralization and economic development in the Czechia in the years 2000-2020. The article deals with territorial arrangement as the Czechia belongs to countries with the highest territorial fragmentation of municipalities and applies a combined model of fiscal federalism with relatively low fiscal decentralization. The study uses the following indicators: expenditure decentralization, revenue decentralization, intergovernmental transfer decentralization and tax revenue decentralization. Empirical tests are based on cross correlation and Granger causality methodology. The found results imply that economic growth does not relate exclusively to the degree of fiscal decentralization of a country as coefficients of correlation are very low, and decentralization revealed to be positively associated with GDP per capita but negatively associated with real GDP growth, except expenditure decentralization positively correlated in both cases. The relationship is stronger for economic maturity than for economic growth and economic performance comes first followed by decentralization.

Theory of fiscal federalism has started to highlight fiscal decentralization since the 1970´s of the 20th century. Fiscal decentralization is usually characterized by a division of decision – making powers combined with a limited shift of the resources to sub-central governments (SCGs). Aristovnik (2012) notes that many post-communist countries started the public sector reforming process later, with some derogation from the optimal fiscal decentralization implementation. In the Czechia, state decentralization and local autonomy were understood in a way that gave the right to become a separate local government, to almost each settlement unit, even if that unit was a tiny village. The number of municipalities rose by almost 50%, from 4,120 in 1993 to 6,250 in 2001. Nowadays, the Czechia uses a combined model of fiscal federalism and belongs to countries with the most territorial fragmentation (Szarowská 2020, OECD 2019).

In this context, the relationship between economic performance and the size of municipality is often discussed. Economic growth is affected by many factors among other fiscal decentralizations (Mose 2021; Oates 1972). Studies highlight the theoretical prediction that fiscal decentralization enhances the efficiency of government and promotes economic development (e. g. Oates, 2005 or Baskaran et al., 2016), but some report present contradictory direction of influence.

The aim of the article is to examine the relationship between fiscal decentralization and economic development in the Czechia in the years 2000-2020. The article is organized as follows. The opening chapter introduces a theoretical background and literature review. The next chapter provides a description of methodology and data. The empirical part focuses on fiscal decentralization and economic growth and performance in the Czechia and the intention is to identify the direction of influence as well. The conclusion summarises the main findings.

Literature Review

Traditional theory of fiscal federalism is mostly based on Oates’s (1972) theorem, which predicts a greater allocative efficiency and production efficiency. An important extension of literature brings “second-generation” of fiscal federalism which takes into account political and fiscal institutions, imperfect information and political agents. Generally, fiscal decentralization is linked to sharing fiscal responsibilities and power among central, state and local governments, but the term is not sufficiently clear even in the fields of political science or public administration (Bird and Wallich, 1993 or Rodríguez-Pose and Krøijer, 2009). Bahl (2008) introduces the pillars and twelve implementation rules for fiscal decentralization.

Thiessen (2003) as well as Martinez-Vazquez and McNab (2003) mention the absence of a formalized theory on the relationship between fiscal decentralization and economic growth. Thiessen (2003) describes a positive relation between decentralization and growth when decentralization is increasing from low levels, but as decentralization increased, the relation eventually turned negative in a cross section of high-income OECD economies using annual data for the period 1973–1998.

Later, Oates (2005) gives a review of the fiscal decentralization characteristics and their economic implications. This and other relevant studies (e.g., OECD, 2021) claim to demonstrate the direct impact of fiscal decentralization on economic growth. However, a causality is not clear and absolute, and decentralization may affect growth indirectly through its impact on other socio-economic variables, such as macro stability and government quality (Martinez-Vazquez and McNab, 2003), or through its interaction with the institutional framework (Feld and Schnellenbach, 2011). Martinez-Vazquez et al. (2017) offer a complex review of the impact of fiscal decentralization on the economy and society. Dougherty and Phillips (2019) in their research present new measures of spending power and performance across five key sectors of sub-national government service delivery – education, long-term care, transport services, social housing and health care. The new indicators reveal unique insights about how responsibilities are assigned across levels of government, which enable the analysis of different arrangements on outcomes. Recently, Slavinskaite et al. (2020) introduce a theoretical model for evaluating the fiscal decentralization.

Empirical studies that focused on the relationship between fiscal decentralization and economic growth provide mixed ambiguous results, sensitive to the choice of the data sample and the investigated period. Slavinskaitė (2017) summarizes the empirical findings of the research on the impact of fiscal decentralization on economic growth in cross–countries terms. Blöchliger and Égert (2013) present an overview of literature review, which is divided into two groups – cross-country studies and national studies. Many empirical studies are focused on the share of SCG revenue or expenditure in consolidated government revenue or expenditure as the measure of fiscal decentralization. Studies that have reported a positive and statistically significant impact using these measures include, among others, Iimi (2005), who reports significant and positive impact of expenditure decentralization on per capita GDP growth in a panel of 51 developed and developing countries covering 1997-2001.

Akai et al. (2007) stress the complementarity relationship between fiscal decentralization and economic growth in the USA and promote further revenue decentralization by computing the optimal degree of fiscal decentralization measured by expenditure decentralization and revenue decentralization. Thornton (2007) highlights the relationship between fiscal decentralization and long-run economic growth is ambiguous as is apparent from the results of empirical studies.

Contrary to a majority view, it is possible to find many empirical studies with a proven negative impact of fiscal decentralization on economic growth (e. g. Zhang and Zou, 1998, Rodríguez-Pose and Ezcurra, 2011 or Baskaran and Feld, 2013). Some studies even consider decentralization harmful, especially in the case of developing and transition economies (Rodden, 2002). This scepticism is fuelled by problems often associated with decentralization, such as increasing deficits, lower quality of government decisions, corruption, increased influence of interest groups, and greater interregional inequalities, which result in lower overall economic growth.

Rodríguez-Pose and Krøijer (2009) examine, using a panel data approach with dynamic effects, the relationship between the level of fiscal decentralization and economic growth rates across 16 Central and Eastern European countries over the 1990-2004 period. While expenditure at and transfers to subnational tiers of government are negatively correlated with economic growth, tax as assigned at the subnational level evolves from having a significantly negative to a significantly positive correlation with the national growth rate.

Gemmell et al. (2013) investigate whether the efficiency gains accompanying fiscal decentralization generate higher growth in 23 OECD countries, 1972–2005. They find that spending decentralization tends to be associated with lower economic growth while revenue decentralization is associated with higher growth. Wang (2018) offers diverse results for revenue and expenditure decentralization as well. He states revenue decentralization does not affect economic performance. But, expenditure decentralization dividend in terms of an enhanced economic growth rate can be achieved only when the initial share of local government expenditure is smaller than the growth-maximizing degree through along with tax collection and trade openness.

Also, Radoniqi (2018) points out that empirical studies about the impact of fiscal decentralization in economic growth all the time have provided mix results. Her paper reviews, analyses and compares the findings of these studies and highlights and explains differences on the dimensions studied from the authors about this phenomenon. Later, Carniti et al. (2019) tested the effects of fiscal decentralization on economic growth empirically on a panel of 25 European countries (1995-2015) and focuses on expenditure composition. Their econometric results show that relationship between investment decentralization and growth is an inverted bell-shaped curve: there is a critical mass of decentralized investments beyond which it is possible to enhance growth.

Jílek (2009) deals with the issue of fiscal decentralization in the Czechia. His analysis shows that though the expenditure decentralization in the Czechia is quite high, the degree of revenue and tax decentralization is low. This result is supported also by the comparison with OECD-Europe unitary countries average. Bryson et al. (2004) survey fiscal decentralization in the Czechia too. They conclude that the Czechia made more substantial transfers to local governments, but the development of fiscal autonomy was stifled as transfers reduced the need for own-source local revenues. The Czech real estate tax has remained nominal as it was under central planning, and its administration is fraught with moral hazard problems. The property tax never became a tool for generating independent funds which is also confirmed by Sobotovičová and Janoušková (2020) and present specifics of real estate taxation in the Czechia.

Methodology and Data

The intention of the article is to examine the relationship between fiscal decentralization and economic growth and performance and also identify the direction of influence in the Czechia in the years 2000-2020 (the latest available data). The empirical evidence relies on the secondary statistical data of the Czech Statistical Office, Ministry of Finance (monitor.statnipokladna.cz) and the OECD Fiscal Decentralization Database; data were tested and are consistent in time.

Fiscal decentralization has many dimensions (e.g., Harguindéguy et al. (2021) review and compare 25 decentralization indexes), therefore, it is necessary to point out that variables are used in accordance with the OECD definition. The Czechia is a unitary state; SCG is formed by municipalities and regions, hence values of SCG (expenditure, revenues, tax, transfer) are equal to a sum of financial flows for these basic and higher self-governing units. Variables are specified as follows (Szarowská, 2020):

Expenditure decentralization (EXPD) is the ratio of subcentral to total general government expenditure as defined in (1).

EXPSCG means total expenditures of SCG, TrSCG transfers provided by SCG, EXP total government expenditures, Tr transfers between levels of government.

Revenue decentralization (REVD) means the ratio of subcentral own revenue to total general government revenue.

In (2), REVSCG means total revenues of SCG, TrSCG transfers (grants) received by SCG, REV total government revenues, Tr transfers between levels of government.

Tax revenue decentralization (TAXD) expressing the ratio of subcentral tax revenue (TAXSCG) to total general government tax revenue (TAX):

Intergovernmental transfer decentralization (TRFD) means transfers between the central government level and social security which are considered to be internal and have not been considered when calculating either the inter-governmental transfer revenue or the total revenue.

Economic development is assessed using the real GDP growth rate (RGDP) and nominal GDP per capita (GDP) expressed in Purchasing Power Parity (PPP). GDP per capita values were transformed into natural logarithms. It is necessary to test the stationary time series before starting analysis. Unit root tests identified that all-time series are stationary at the first differences (RGDP and EXP also at level data). The empirical tests relating decentralization and economic development are based on cross correlation methodology.

Cross correlation assesses how one reference time series correlates with another time series, or several other series, as a function of time shift (lag). Cross correlation does not yield a single correlation coefficient but rather a whole series of correlation values. Like all correlations, cross correlation only shows statistical associations not causation. Consider two financial series and, then, the cross-correlation at lag (lead) k is defined as follows:

where is the correlation coefficient and mx and myare the means of corresponding series. The series can be related in three possible ways: (i)can lead (), (ii) can lag (). (iii) series can be contemporaneously related ().

Granger causality methodology (Granger, 1980) is also applied. The Granger causality refers to a specific notion of causality in time-series analysis. A time series X is said to Granger-cause Y if it can be shown, usually through a series of t-tests and F-tests on lagged values of X (and with lagged values of Y also included), that those X values provide statistically significant information about future values of Y.

Results and discussion

Fiscal decentralization in the Czechia

The 1993 Constitution established the Czechia as a sovereign unitary state and guaranteed two levels of SCG system, with no hierarchical link: the higher self-governing units (the regions), and the basic self-governing units (the municipalities which are regulated through the Municipal Act 128/2000). Regions were established in 2000 (Regions Act 129/2000). There were instead 77 district offices, which were deconcentrated units of the state territorial administration and which, to a certain extent, worked as surrogate regional governments. The system of intergovernmental fiscal relations in the Czechia remains quite centralized. A fair assessment of the current system is that the Czechia may be considered as having a significantly deconcentrated state administration structure. This is because all of the activities of district offices and the bulk of the activities of municipalities have been aimed at implementing the central government’s policies at the local level. Most of the fiscal decision-making power emanates from the center and local level governments have only a marginal influence on local fiscal matters.

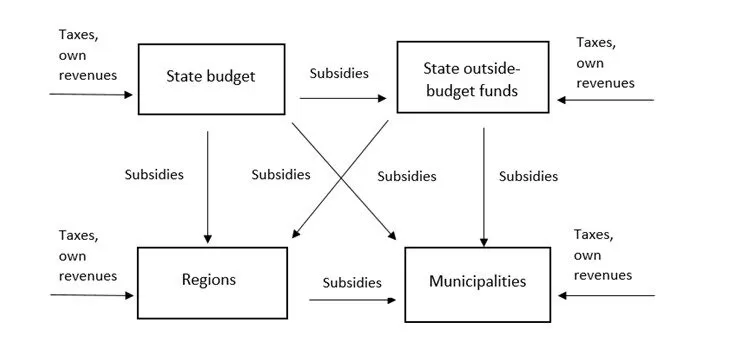

The contemporary government in the Czechia is organized in a three-tier structure: the central government, 14 regions and 6258 municipalities (Czech Statistical Office, 2021). The capital Prague has a special statute and is considered both a region and a municipality. Most of the municipality’s revenues come from shared taxes, where the largest part consists of the collection of VAT. However, municipalities also have the possibility to set their own fees and have in their delegated powers the collection of property tax. Municipality also may freely dispose of its properties and can also have rental income, sales, or conduct business. The distribution of revenue from shared taxes between the various levels of government, and consequently between the municipalities, is precisely defined in the Act 243/2000, Act on budgetary allocation of taxes. Municipalities and regions also receive state subsidies for the performance of state administration under delegated powers as Figure 1 shows.

Fig. 1: Combined model of fiscal federalism in the Czechia

A degree of decentralization has evolved during the transition. Regions and municipalities are entitled by state law to both autonomous responsibilities, over which they have considerable freedom with regards to financial and legal aspects, and delegated responsibilities, which need to be executed according to central government guidelines. Municipalities are autonomously responsible mainly for pre-elementary and primary education, local social welfare, environment, public housing, public transports and local roads. Regions are autonomously responsible for secondary education, regional road networks, regional economic development and healthcare. SCGs get their revenues from taxation (own-source), grants and other sources, mainly fees resulting from the provision of services. In 2020, sub-national expenditure represents 13% of GDP and 27.6% of total public expenditure. The revenue of municipalities can be broken down as follows: 14.5% from autonomous taxation, 47.3% from shared taxation, 26.3% from grants and 11.9% from other sources. The revenue of regions can be broken down as follows: 0.2% from autonomous taxation, 26.8% from shared taxation, 70.5% from grants and 2.5% from other sources (Czech Statistical Office, 2021).

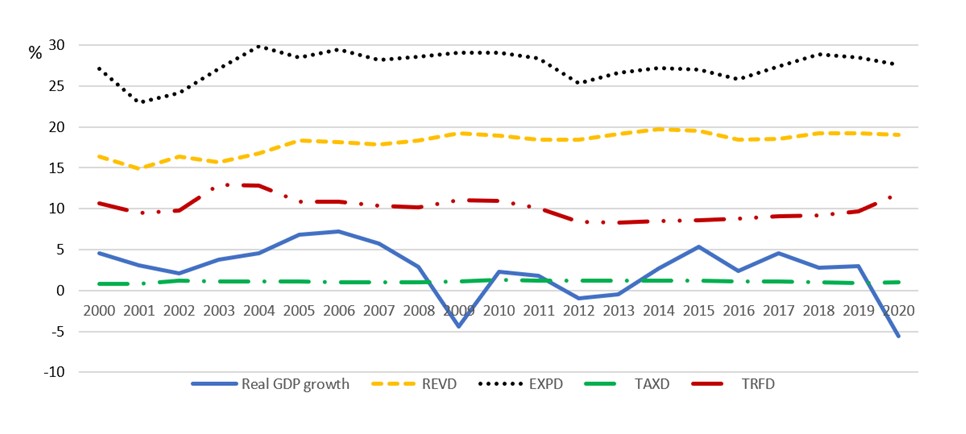

Fig 2. GDP growth and decentralization in the Czechia (2000-2020 in percentage)

Figure 2 reports the development of the analyzed variables and it is evident that expenditures are more decentralized than revenues. While both revenue and expenditure became more decentralized over the past 21 years, expenditure decentralization outpaced revenue decentralization, resulting in a higher vertical fiscal imbalance and growing intergovernmental grants (for details look at Halásková and Halásková, 2018; Szarowská, 2014 and 2015). Martinez-Vazquez et al. (2017) draw attention to the fact that shared taxes usually appear in official statistics as sub-national revenue, although the SCG has no autonomy in determining the revenue base or rate. When the degree of taxing power of SCGs is considered, the decline of revenue decentralization and stagnation of tax autonomy is seen. The increase of decentralization is visible from 2013 and is connected with a positive economic growth. This positive economic development was disrupted by the COVID pandemic, and a sharp economic decline followed by an increase in transfers was recorded in 2020. Overall, expenditure decentralization (EXPD) has varied from 23% to nearly 30% with average value 27.47%. SCGs have a very low share in total tax government revenues, and increase of revenue decentralization (REVD) is less 5 percentage points (from 15% to 19.7%) in the analyzed period. A degree of revenue fiscal decentralization is similar to the EU average (18%) as is reported by Czech Statistical Office (2021) and OECD (2021). Very low value (about 1%) of tax revenue decentralization (TAXD) results from the fact that the Czechia is the country without tax legislative powers at the sub-national level. SCGs are highly dependent on financial redistribution by the government. The system of shared taxation, according to which approximately 9% of state taxes are transferred to regional authorities and about 22% of state taxes are transferred to local and regional authorities, leaves the latter considerable freedom in deciding how these resources should be used within the field of their proper responsibilities. Municipalities have a limited discretion by adjusting (local and size) coefficients over the property tax (representing about 3% of municipal revenues) and full discretion over local fees (representing 2.3% of municipal revenues in 2020). From 2013, intergovernmental transfer decentralization (TRFD) stagnated after the initial decline but increased again during the pandemic. Economic growth (real value) reports cyclical development. Maximum value is reported in 2006 (+7.25%), minimum in 2020 (-5.60%), mean value is 2.59%.

Granger Causality

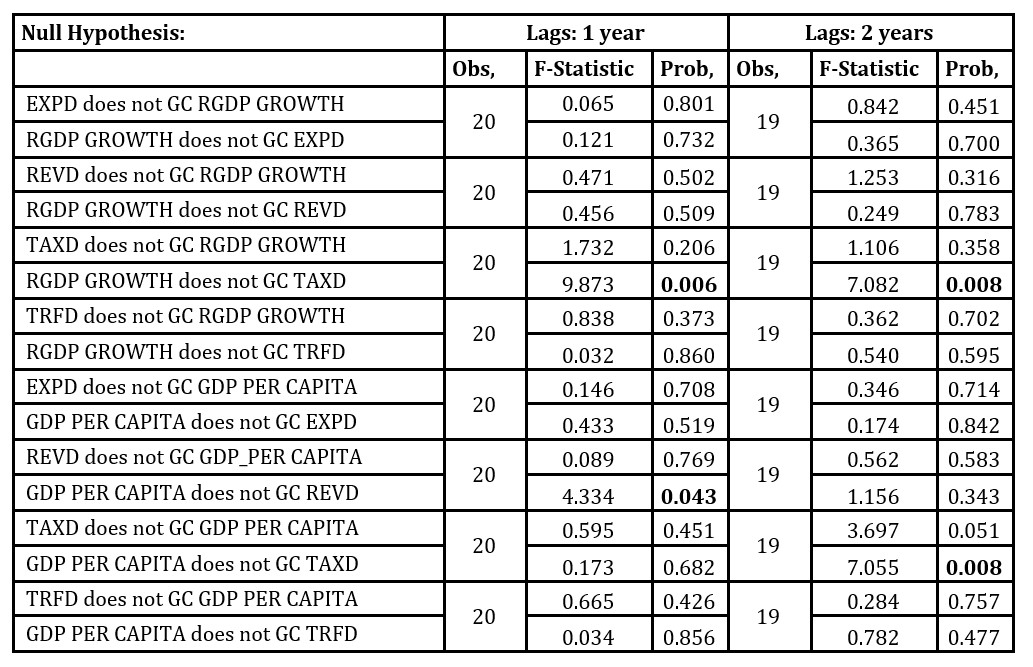

Pairwise Granger causality tests are applied for examining relations between GDP growth and EXPD ratio as well as other selected variables in a short-term. It is important to mention that the statement for example “Expenditure Granger causes GDP” does not imply that GDP is the effect or the result of EXPD. Granger causality measures precedence and information content but does not by itself indicate causality in the more common use of the term. The null hypothesis should be rejecting if probability is less than 0.05. Table 1 summarizes results for lags one and two years. Bold values indicate hypothesis, which should be rejected.

Tab. 1: Granger causality tests

Note: GC means Granger cause

One can find only one example of one-way Granger causality from GDP growth to tax revenue ratio TAXD and one example of one-way Granger causality from economic maturity expressed by GDP per capita to revenue ratio REVD for the 1-year lag. With the lag of 2 years, there are two reported cases of one-way Granger causality – one from GDP growth and one from economic maturity – both for tax revenue ratio TAXD. A two-way Granger causality is not revealed in any case. From this point of view, it can be concluded that there is just one-way causality, which was reported from GDP growth as well as economic maturity to TAXD and from economic maturity to REVD. That means that economic performance comes first followed by decentralization. Deeper analysis focused on the direct impact of variables will follow in a next paper.

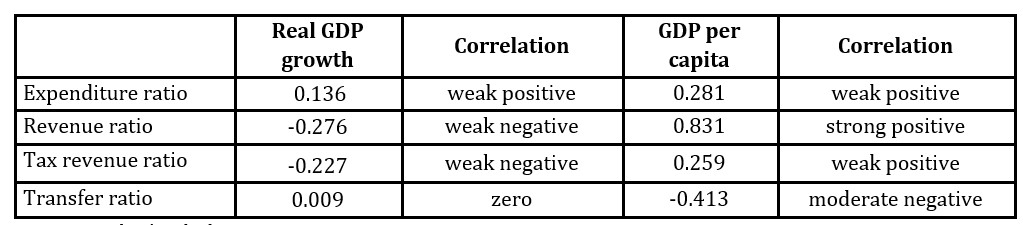

Results of correlation analysis

Correlation is a statistical technique that can show whether and how strongly pairs of variables are related. The correlation coefficient can vary from –1 to +1. The correlation coefficient –1 indicates perfect negative correlation, and +1 indicates perfect positive correlation. Its value smaller than 0.1 means zero correlation, from 0.1 to 0.35 weak correlation, from 0.35 to 0.7 moderate correlation and higher than 0.7 expresses strong correlation. The results in Table 1 report cross-correlations for all possible combinations of growth and decentralization variables.

Tab. 2: Correlation coefficients

Source: Author´s calculations in Eviews12

Findings suggest that revenue and tax decentralizations appear to be positively associated with GDP per capita but negatively associated with GDP growth, while expenditure decentralization is positively correlated in both cases. Transfer decentralization was found to be significant only in the case of economic maturity, when its relation is negative. Coefficients also express that correlation is stronger for economic maturity expressed by GDP per capita (a strong positive relation was reported especially for revenue decentralization) than for economic growth. The information about GDP growth provided by Table 2 can be interpreted as economic growth does not relate exclusively to the degree of fiscal decentralization of a country (as coefficients of correlation are very low).

The results are similar to the conclusion about the relationship between GDP per capita growth and decentralization observed in the research of Martinez -Vazquez (2016). Aristovnik (2012) also finds a positive correlation between fiscal decentralization and economic growth in Eastern European countries; so the case of the Czechia confirms this trend. Coefficients suggest that fiscal decentralization might accelerate economic performance. The similar conclusion is possible to find in Iimi (2005), Akai et al. (2007) or Thornton (2007).

The found correlation coefficients and the positive influence of the degree of fiscal decentralization on economic performance may be affected by country differences in political and administrative decentralization as Rodríguez-Pose and Ezcurra (2011) also assumed. In terms of subnational expenditure and revenues, the results of empirical evidence are in line with the findings of other empirical studies on fiscal decentralization and economic growth, such as Thiessen (2003), Iimi (2005), Akai et al. (2007), or Rodríguez-Pose and Krøijer (2009), Kim and Dougherty (2019), but opposite as in Zhang and Zou (1998), Rodden (2002) or Rodríguez-Pose and Ezcurra (2011). The variety is generated due to differences in the used econometric models, country samples, observation periods and considered variables.

Conclusion

The aim of the paper was to examine the relationship between fiscal decentralization and economic development in the Czechia in the years 2000-2020. The empirical tests relating to decentralization and economic performance are based on cross correlation and Granger causality methodology.

Decentralization process in the Czechia is driven by both economic and political forces. Currently, the Czechia uses a combined model of fiscal federalism with a three-tier structure: the central government, 14 regions and 6258 municipalities (Czech Statistical Office, 2021). Municipalities and regions form the SCG level and are entitled by state law to both autonomous and delegated responsibilities, which need to be executed according to central government guidelines. SCGs are highly dependent on financial redistribution by the central government. Shared taxes usually appear in official statistics as sub-national revenue, although the SCG has no autonomy in determining the revenue base or rate. Municipalities have a limited discretion by adjusting (local and size) coefficients over the property tax and full discretion over local fees. Very low value of tax revenue decentralization results from the fact the Czechia is the country without tax legislative powers at the sub-national level. Expenditures are more decentralized than revenues.

The Granger causality identified just one-way causalities, which were reported from GDP growth as well as economic maturity to tax revenue decentralization TAXD and from economic maturity to revenue decentralization REVD. That indicates that economic performance comes first followed by decentralization. But this result is very limited to draw general conclusions. Deeper analysis focused on a direct impact of variables will follow in next paper. Correlation analysis implies revenue and tax decentralizations appear to be positively associated with GDP per capita but negatively associated with GDP growth; but expenditure decentralization positively correlated in both cases. On the other hand, increase of transfers has negative relation. Coefficients express that correlation is stronger for economic maturity than for economic growth. The results also can be interpreted as economic growth does not relate exclusively to the degree of fiscal decentralization of a country as coefficients of correlation are very low.

As economic maturity has significantly increased during the analyzed period, it allows formulating implications for the government/economic policy. Fiscal decentralization simplifies the system of public sector and local SCGs, because responsibility for generating and managing public resources is assigned to the lower level of governments. As mentioned above, the Czechia belongs to countries with the most territorial fragmentation of municipalities. Hence, specific decision-making actions and changes should include institutional intergovernmental cooperation. The high territorial fragmentation at the lowest tier of the government is the most remarkable attribute of the administrative structure and can be seen as a reason for a low level of revenue decentralization, although expenditure decentralization is relatively high.

Revenue autonomy should be enhanced by increasing predictability of local budgets and e.g., resuming tax-effort incentives. The Act on budgetary allocation of taxes should be modified to decrease differences between local governments. A system of transfers should concentrate on reducing the number of specific subsidies, and boosting transfers and programs stabilizing SCG budgets in a medium-term framework.

Acknowledgment

This contribution was supported by the Ministry of Education, Youth and Sports Czech Republic within the Institutional Support for Long-term Development of a Research Organization in 2022.

References

Akai, N., Nishimura, Y. and Sakata, M. (2007) ‘Complementarity, fiscal decentralization and economic growth,’ Economics of Governance, 8 (4), 339–362.

Aristovnik, A. (2012) ‘Fiscal decentralization in Eastern Europe: Trends and selected issues,’ Transylvanian Review of Administrative Sciences, 37, 5–22.

Baskaran, T., Feld, L.P. and Schnellenbach, J. (2016) ‘Fiscal federalism, decentralization, and economic growth: A meta-analysis,’ Economic Inquiry, 54 (3), 1445–1463.

Baskaran, T. and Feld, L.P. (2013) ‘Fiscal decentralization and economic growth in OECD countries. Is there a relationship?,’ Public Finance Review, 41 (4), 421–445.

Bird, R.M. and Wallich, C.I. (1993) ‘Fiscal decentralization and intergovernmental relations in transition economies,’ Research Working Paper No. 1122, World Bank, Washington, DC.

Blöchliger, H. and Égert, B. (2013) Decentralization and economic growth – Part 2: The impact on economic activity, productivity and investment,’ Working Papers on Fiscal Federalism No. 15, OECD, Paris.

Bryson, P.J., Cornia, C. and Wheeler, G.E. (2004) ‘Fiscal decentralization in the Czech and Slovak Republics: A comparative study of moral hazard,’ Environment and Planning C: Government and Policy, 22 (1), 13–113.

Carniti, E., Cerniglia, F., Longaretti, R. and Michelangeli, A. (2019) ‘Decentralization and economic growth in Europe: for whom the bell tolls,’Regional Studies, 53 (6), 775–789.

Czech Statistical Office (2021). Small lexicon of municipalities of the Czech Republic – 2021, CZSO, Prague.

Dougherty, S. and L. Phillips (2019) The spending power of sub-national decision makers across five policy sectors, OECD Working Papers on Fiscal Federalism 25, OECD Publishing, Paris.

Feld, L.P. and Schnellenbach, J. (2011) ‘Fiscal federalism and long-run macroeconomic,’ Environment and Planning C: Government and Policy, 29 (2), 224–243.

Gemmell, N., Kneller, R. and Sanz, I. (2013) ‘Fiscal decentralization and economic growth: Spending versus revenue decentralization,’ Economic Inquiry, 51 (4), 1915–1931.

Granger, C. W. J. (1980) ‘Testing for causality: A personal viewpoint,’ Journal of Economic Dynamics and Control, 2, 329-352.

Halásková, M., Halásková, R. (2018) ‘Evaluation Structure of Local Public Expenditures in the European Union Countries,’ Acta Univ. Agric. Silvic. Mendelianae Brun., 66, 755–766.

Harguindéguy, J.-B. P., Cole, A. and Pasquier, R. (2021) ‘The variety of decentralization indexes: A review of the literature,’ Regional & Federal Studies, 31 (2), 185–

Iimi, A. (2005) ‘Decentralization and economic growth revisited: An empirical note,’ Journal of Urban Economics, 57, 449–461.

Radoniqi, D. Q. (2018) ‘Does fiscal decentralization contribute in economic growth?,’ Journal of Academic Research in Economics, 10 (3), 389-411.

Rodden, J. (2002) ‘The dilemma of fiscal federalism: grants and fiscal performances around the world,’ American Journal of Political Science, 46 (3), 670–687.

Rodríguez-Pose, A. and Ezcurra, R. (2011) ‘Is fiscal decentralization harmful for economic growth? Evidence from the OECD countries,’ Journal of Economic Geography, 11 (4), 619–643.

Rodríguez-Pose, A. and Krøijer, A. (2009) ‘Fiscal decentralization and economic growth in Central and Eastern Europe,’ Growth and Change, 40 (3), 387–563.

Slavinskaite, N., Novotny, M. and Gedvilaite, D. (2020) ‘Evaluation of the fiscal decentralization: Case studies of European Union,’ Inzinerine Ekonomika-Engineering Economics, 31 (1), 84–92.

Slavinskaite, N. (2017) ‘Fiscal decentralization and economic growth in selected European countries,’ Journal of Business Economics and Management, 18 (4), 745–757.

Sobotovičová, Š., Janoušková, J. (2020) ‘Specifics of real estate taxation in the Czech and Slovak Republics,’International Advances in Economic Research, 26, 273–287.

Szarowská, I. (2020) ‘Fiscal decentralization and economic growth in the Czechia’ Proceedings of the 36th International Business information Management Association Conference (IBIMA), ISBN: 978-0-9998551-5-7, 4-5 November 2020, Granada, Spain, 6793-6799.

Szarowská, I. (2015) ‘Impact of fiscal decentralization on economic development in the European Union,’ Acta academica karviniensia, 15 (2), 136–147.

Szarowská, I. (2014) ‘Fiscal decentralization and economic development in selected unitary European countries,’ European Financial and Accounting Journal, 9 (1), 22–

Thiessen, U. (2003) ‘Fiscal decentralization and economic growth in high income OECD countries,’ Fiscal studies, 61 (1), 64–70.

Thornton, J. (2007) ‘Fiscal decentralization and economic growth reconsidered,’ Journal of Urban Economics, 61 (1), 64–70.

Wang, F. (2018) ‘The influences of fiscal decentralization on economic performance: Empirical Evidence from OECD countries,’Prague Economic Papers, 27 (5), 606-618.

Zhang, T. and Zou, H. (1998) ‘Fiscal decentralization, public spending, and economic growth in China. Journal of Public Economics,’ 67 (2), 221–240.