Bucharest University of Economic Studies, Bucharest, Romania

Volume 2023,

Article ID 106863,

Journal of Eastern Europe Research in Business and Economics,

13 pages,

DOI: 10.5171/2023.106863

Received date: 16 September 2022; Accepted date: 3 January 2023; Published date: 9 February 2023

Academic Editor: Florin Cornel Dumiter

Cite this Article as:

Cristina ANGHELESCU (2023)," Is there a Neo-Fisher Effect in the case of Selected Central and Eastern European Countries?", Journal of Eastern Europe Research in Business and Economics Vol. 2023 (2023), Article ID 106863, DOI: 10.5171/2023.106863

At the current juncture, the global economy is facing adverse supply side shocks amid the ongoing war in Ukraine. The persistent energy crisis and a potential flare-up in bottlenecks in global value chains are expected to further fuel inflationary pressures. Against the background of escalating prices, central banks have already started increasing the key interest rates. At the same time, given the worsening economic outlook, fears of a global recession have intensified. However, recent empirical evidence shows that a tightening monetary policy is not necessarily contractionary. In this regard, the aim of this paper is to investigate the existence of a Neo-Fisher effect in Hungary, Poland and Romania. Results show that a permanent tightening of the monetary policy, identified through long run restrictions within a vector autoregressive model, is expansionary and inflationary, contrary to the common knowledge regarding the effects of a temporary increase in interest rates. Under these circumstances, the ongoing process of normalizing monetary policy is not automatically leading to a recession in selected Central and Eastern European countries. The importance of anchoring inflation expectations is also highlighted.

The COVID-19 pandemic has struck a hard blow on economies all around the globe. Despite the emergence of several vaccines and the progress made in terms of vaccination campaigns, in tandem with less aggressive COVID variants, the sanitary crisis still represents a threat to economic activity. In this regard, the main risks are related to the strict policies in China. The social distancing measures in this country can prolong and even worsen the disruptions in global value chains, amid the high integration of China in international trade. However, at the current juncture, probably the most important source of uncertainties relates to the ongoing war in Ukraine and the introduction of international sanctions. These have already exacerbated the energy crisis, with significant adverse effects on economic activity. At the same time, bottlenecks in global production and supply chains persist.

Overall, 2022 has brought in its first half generalized increases of prices on the back of various overlapping factors such as the above-mentioned energy crisis, persistent disruptions in global value chains to which adds the severe drought affecting most part of Europe. These also caused a deterioration in inflation expectations. Their worsening played an important role in the recent hikes in wages. Against this background, the upward pressures on all categories of inputs used by companies have favoured the pass-through of higher production costs into the final prices of consumer goods.

Apart from the impact on prices, the war in Ukraine is also eroding confidence, which in turn is reflected in higher volatility on international markets and increased risk premium. Future investments are uncertain, as the tightening of financial conditions could put a break on them. The exacerbation in risk aversion is mostly seen as affecting countries that are in the geographical proximity of Ukraine.

The significant hikes in the inflation rate have triggered responses from central banks. As a consequence of high inflationary pressures in tandem with worsening inflation expectations, monetary authorities have started increasing the policy rate. The current juncture could represent the ending of the zero lower bound era, as even the European Central Bank has decided to increase its policy rates. Central and Eastern Europe countries such as Romania, Poland and Hungary make no exception, as significant increases in the key interest rate have also occurred.

While fighting high inflation and trying to anchor inflation expectations, a tight monetary policy is also assumed to exert restrictive effects on the aggregate output. Investment could be hindered by increased financing costs, while consumption could also be affected by a higher propensity to save. However, recent evidence in related literature shows that a permanent monetary policy shock is inflationary and expansionary.

Against this background, the analysis of the effects of monetary policy shocks becomes more relevant. Given that central banks all around the world have started increasing key interest rates, it is questionable whether the normalization of the monetary policy is likely to trigger a recession, already favored by the existing negative supply shocks. In this regard, the aim of this paper is to investigate whether Neo-Fisher effects are present in the case of selected Central and Eastern European (CEE) countries, namely Hungary, Poland and Romania. Therefore, the main objective of the analysis is to evaluate the response of the main macroeconomic indicators to a permanent monetary policy shock and assess whether the risk of a recession is high under these circumstances.

The paper is envisaged to contribute to the existing literature by extending it in the case of the above-mentioned economies. By tackling the most recent economic problems, the results could also provide insightful information for both policymakers and people outside public administration. In the case of policymakers, results could help deciding the nature of the monetary policy shock, whether the ongoing tightening is temporary or permanent. At the same time, it might help solving economic puzzles which might occur by better understanding the evolution of macroeconomic indicators. Nevertheless, such empirical evidence could also prove useful in the case of macroeconomic forecasts. In the case of people outside public administration, empirical evidence within this manuscript could help when forming expectations regarding the effects of the ongoing policies.

The manuscript firstly provides a brief overview for the related literature in the case of effects of monetary policy shocks, especially as regards the permanent ones. Moreover, we focus on evidence regarding the presence and characteristics of the Neo-Fisher effect. We continue by describing the latest evolutions in the case of selected CEE countries. We highlight the main evolutions regarding inflationary pressures and show the main decisions taken until the second semester of 2022 by central banks. Furthermore, we describe data and methodology, while in the following section we highlight the main results. We analyze the response of the main macroeconomic indicators such as the gross domestic product, the inflation rate and the exchange rate to a permanent monetary policy shock. Lastly, we conclude by summarizing the main results and implications for policymakers. The concluding remarks section also provides incentives for future research and potential drawbacks of the current estimations.

Literature Review

Shortly before the negative effects of both the pandemic and the military conflict and its related sanctions leading to exacerbated negative supply side shocks, the global environment was generally dominated by low inflation. Against this background, in economic literature, the analysis of the relationship between the inflation rate and the stance of the monetary policy has gained momentum. One particular research objective relates to the potential ineffectiveness of conventional monetary policy, especially in a zero lower bound environment. Gobbi et al. (2019) find that instead of pursuing an aggressive monetary policy which empirical evidence shows is inefficient both at the zero lower bound and above, monetary authorities should switch to a reflationary policy package that prevents the entrenchment of deflationary expectations. Erceg et al. (2021) also support unconventional tools in order to boost output and inflation. However, Egea and Hierro (2019) bring criticism to unconventional monetary policy tools, while supporting the conventional ones. The authors highlight differences in terms of channels of transmission. While in the United States the risk channel is found to be more effective; in the Eurozone the credit channel was representative before the financial crisis and the risk one has recently become more relevant.

It is common knowledge that the transmission of monetary policy shocks depends on a series of factors and country-specific characteristics. In related economic literature, there are plenty of papers investigating such factors, also with a view on monetary policy rules. For instance, according to Svensson (2003), the commitment to a simple instrument rule is inadequate in the case of inflation targeting regimes. Rules should also depend on marginal rates of transformations between the target variables, such as the output gap or the inflation rate. Bilbiie and Ragot (2021) take into consideration liquidity for insurance purposes when accounting for the optimal monetary policy in an environment dominated by heterogeneous agents. Another factor influencing the transmission channels in the case of monetary policy shocks refers to price stickiness, as shown by Weber et al. (2020). By contrast, high volatility can reduce price stickiness and firms have greater desire to change prices. This in turn translates in monetary policy becoming less effective at influencing output (Vavra, 2014).

The transmission of the monetary policy shocks is also influenced by the nature of the shock. In this regard, one research direction refers to the analysis of the Neo-Fisher effect. It describes a positive relation between the interest rates and the inflation rate amid a permanent monetary policy shock. This comes in contradiction with the conventional wisdom regarding the transmission channels of monetary policy shocks. However, empirical evidence suggests differences between a temporary and a permanent shock. For instance, Uribe (2022) implies that temporary increases in the nominal interest rate lead to a decrease in inflation and output, whereas a permanent increase in the interest rate is rather inflationary and, at the same time, expansionary. Such results are also confirmed by Uribe (2017) in the case of the United States of America and Japan and by Wolden-Bache (2008) in the case of simulated data. Furthermore, Olgun (2022) finds bidirectional causality between interest rates and CPI variables in the case of Turkey. Moreover, Beckworth (2017) associates the failure of quantitative easing programs to create a robust recovery to Fed not credibly committing to a permanent expansion of the monetary base.

In related literature, there is plenty of empirical evidence arguing in favor of Neo-Fisher effects stemming from a permanent monetary policy shock. Schmitt-Grohe and Uribe (2022) highlight that Neo-Fisher effects hold in a New-Keynesian model. Cochrane (2016) describes a series of failed attempts to escape the positive relation between interest rates and inflation. The author cannot infirm the Neo-Fisher effect by introducing sticky prices in empirical models, backward-looking Phillips curves and active Taylor rules, as inflation continues to respond positively to nominal increases in the interest rates. While Chattopadhyay (2021) finds a short-run co-movement of the interest rates and inflation rate, Williamson (2019) and Lukmanova and Rabitsch-Schilcher (2022) suggest inflationary pressures triggered by an increase in interest rates in both short and medium term. The same author highlights that central banks can escape the low inflation trap only by becoming Neo-Fisherians (Williamson, 2016).

At a first glance, the Neo-Fisher effect might seem counter-intuitive, as one might expect a tightening monetary policy to lead to a decrease in both the inflation rate and the output. However, there are some explanations regarding the impact of a permanent monetary policy shock as compared to a temporary one. Firstly, Garin et al. (2018) explain that Neo-Fisherianism is a consequence of the forward-looking nature of empirical models. Therefore, the authors highlight the importance of expectations. Secondly, Alvarez and Lippi (2020) imply that temporary price changes are an imperfect tool to respond to permanent monetary policy shocks. Given the fact that those sticky prices are an important fraction of total prices in the United States, Argentina and Chile, they lead to an overall slow propagation of monetary shocks. Thirdly, according to Gobbi et al. (2022), Neo-Fisherian policy becomes feasible under certain circumstances, such as the economy settling in a deep zero lower bound depression and the confidence in the normal regime falling. Lastly, Airaudo and Hajdini (2021) consider that the Neo-Fisher effect is more pronounced in environments with weaker effects on labor supply and smaller price to wage markups.

The analysis of inflation expectations and their role is a central part in economic literature. According to Hazell et al. (2022), the greater stability of prices is related to inflation expectations becoming more firmly anchored. This result was previously provided by Blanchard (2016). The author finds that inflation expectations becoming more steadily anchored lead to a decline in the slope of the Phillips curve. More recently, Abhoff et al. (2021) explain that inflation expectations are currently the main channel for the transmission of the monetary policy. While not directly accounting for Neo-Fisher effects, the authors highlight that conventional monetary policy tools are ineffective and a positive shock increases inflation expectations in the short term and has no sustained impact on the gross domestic product.

As regards the impact of a permanent monetary policy shock in the case of other macroeconomic variables, Uribe (2022) finds a positive response of the output. Uhlig (2005) suggests ambiguous effects of a contractionary monetary policy shock on real gross domestic product. At the same time, Plescau (2017) points to a negative relation between policy rates and economic growth in the case of Central and Eastern European countries. As regards the exchange rate, a permanent tightening is assumed to depreciate the currency. This finding is confirmed by both Schmitt-Grohe and Uribe (2022) and Carvalho et al. (2021). Similar results in the case of a depreciating exchange rate are found by Gurkaynak et al. (2021) in the case of unexpected tightening of the monetary stance.

There are also some views in related literature against the existence of Neo-Fisher effects. Spahn (2018) explains that the Neo-Fisherian perspective is less convincing as one may doubt that individuals think in terms of analytical equilibrium conditions. Furthermore, Crowder (2020) does not find evidence for a bidirectional causality between interest rates and the inflation rate. However, the author still considers that under certain circumstances, the basic policy recommendation of Neo-Fisherianism is valid. Empirical evidence also shows possibilities to blur the Neo-Fisher effect by including habit persistence in consumption and real wage rigidities (Zahid, 2019).

Methodology and data

Methodology

The aim of this paper is to investigate the response of the main macroeconomic indicators to a permanent monetary policy shock. For this purpose, we consider a vector autoregressive (VAR) model and we estimate impulse response functions. In order to obtain a permanent shock, we impose long-run restrictions following the Blanchard-Quah method (Blanchard-Quah, 1989).

In general, a VAR model can be described by the following equation:

where is a vector of endogenous data, B and C are matrices of coefficients and is a vector of identically and individually distributed disturbances with mean equal to zero and covariance matrix equal to matrix . The covariance matrix can be written as follows:

The impulse responses for the VAR described in equation (1) are C in impact period, after one period and after i periods.

Long-run effects are given by equation (3) below:

Equation (4) holds if eigenvalues of are inside the unit circle. The Blanchard-Quah method implies imposing restrictions regarding the long-run effects described in matrix . For instance, assuming that is lower triangular, only the first shock has a long-run effect on the first variable, only the first and second shocks have long-run effects on the second variable and so on. This is obtained by finding the elements of containing non-zero effects. As for the two-variable case, the above-mentioned restrictions translate into:

After defining , matrix can be computed as shown in equation (8) and impulse response functions can be estimated.

Turning to the aim of the paper, the vector autoregressive model contains data in the following order: nominal interest rate, proxy for output, real interest rates, exchange rates and the difference between the domestic interest rate and the foreign one. In order to obtain a permanent monetary policy shock, we impose that the innovation corresponding to nominal interest rates is the only shock that has a non-zero effect on the level of the nominal interest rate in the long-run.

Data

The methodology presented in the previous section is applied in the case of Hungary, Poland and Romania. Besides being part of CEE, these countries share similar characteristics, such as comparable economic scales and similar monetary policy regimes. At the same time, given stylized facts, all these countries have recently witnessed various increases in the monetary policy interest rates.

We focus on the impact of such a shock on economic activity, prices and bilateral exchange rates. As a proxy for the monetary policy shock, the nominal three months money market interest rate is considered. In the case of economic activity, the model includes the gross domestic product per capita. Furthermore, we analyse the impact on the harmonized index of consumer prices. As for the bilateral exchange rates, given that the main trading partners of all selected CEE economies are Euro Area countries, we have chosen the EUR exchange rate. The estimations also embody foreign influences, namely an external monetary policy shock in the case of the Euro Area. Similar to the domestic one, the three months money market interest rate was considered.

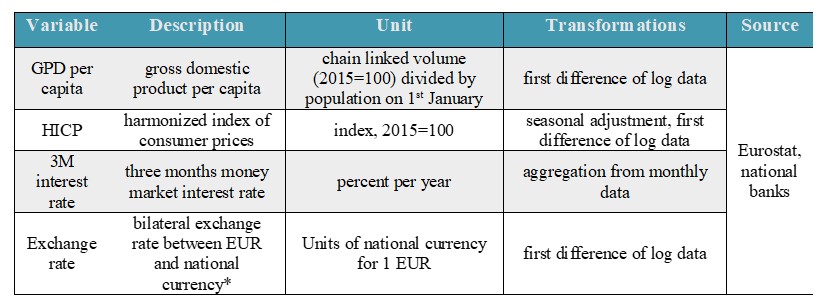

Table 1. Data introduced in estimations

*Hungarian forint in the case of Hungary, Polish zloty for Poland and Romanian leu in the case of Romania

Source: author’s formatting

Data have a quarterly frequency and span from the second quarter of 2000 to the first quarter of 2022. As regards transformations, we seasonally adjusted data using the X-13 ARIMA method. Furthermore, we compute annualized growth rates as first difference of logarithmic data. Data source is Eurostat, as well as the database of national banks from Romania, Hungary and Poland. Table 1 summarizes the main information regarding data.

Stylized facts

At the current juncture, high inflationary pressures are stemming from the ongoing war in Ukraine. The unprecedented military conflict in Europe since the World War II has fueled strains in global value chains leading to an upward spiral in commodity prices. The economic environment had already been severely affected by the pandemic and the war is currently jeopardizing economic recovery.

Inflation all around the globe has embarked on a sharp upward trend, reflecting the superposition of various factors. A relevant contribution to such evolution is related to the energy crisis. In the first part of 2021, the increase in energy prices was mostly associated with the reopening of the economies. In the second part of the year, electricity and natural gas prices started increasing against a series of supply factors, such as the long winter in 2020 or the limited gas storage levels. However, in 2022, the war in Ukraine with its related sanctions has worsened the energy crisis. Significant uncertainties are also stemming from their future evolution. In this regard, in the event of Russia cutting off energy supplies, there would most probable be a renewed increase in commodity prices.

Inflationary pressures are also related to non-energy components. The persistent disruptions in global production and supply chains, in tandem with high transport costs amid the energy crisis, have led to generalized increases of prices. To these adds the drought affecting most European countries. The higher companies’ production costs have witnessed a fast pass-through into final prices.

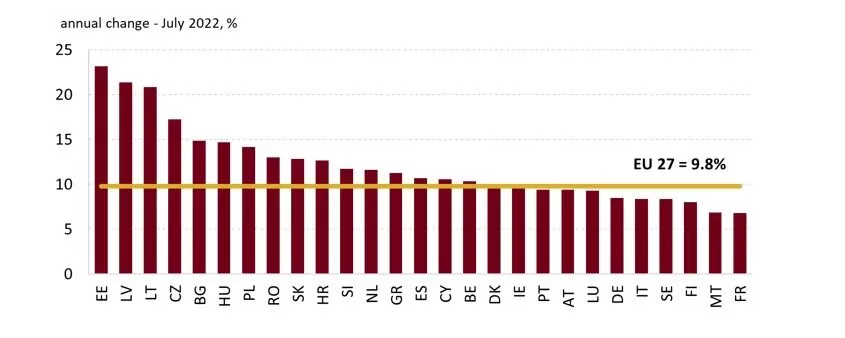

Central and Eastern European (CEE) countries make no exception in what concerns high inflation. In fact, in July 2022 all European countries ran inflations above 5 percent, as shown in Figure 1. According to Eurostat data, the average inflation rate in the European Union according to the harmonized index of consumer prices (HICP) reached 9.8 percent in July, 0.2 percentage points higher as compared to the June readings (9.6 percent).

Figure 1. Generalized inflationary pressures in the EU – HICP in July, 2022

Source: Eurostat, author’s calculations

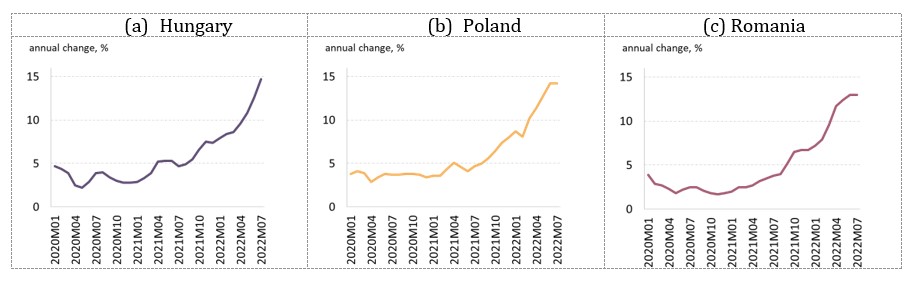

Even though most countries have already adopted several measures in order to partially alleviate the impact of the adverse supply shocks, prices have still embarked on an upward trajectory. Figure 2 shows the evolution of the harmonized index of consumer prices in Hungary, Poland and Romania. Inflation started to increase during 2021, but in 2022 it witnessed sharp step-ups.

Figure 2. Evolution of HICP in selected CEE Countries

Source: Eurostat, author’s calculations

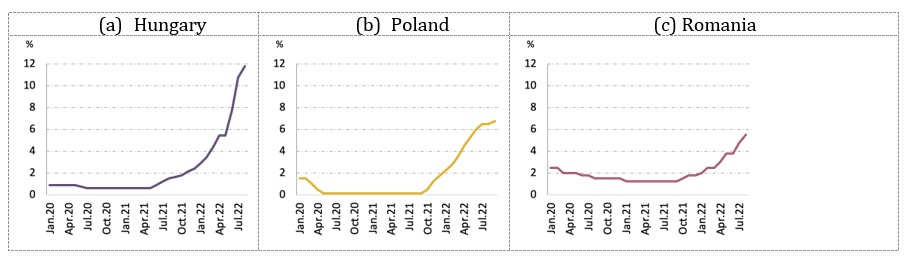

Central banks have started the normalization of the monetary policy. The successive increases in the key interest rate have aimed at fighting inflationary pressures and anchoring inflation expectations. In the case of selected CEE countries, Hungary has the highest key rate. The Central bank started the normalization of the monetary policy in June 2021, with a 0.3 percentage points increase. Instead, Poland and Romania started this process with a slight delay. These countries increased their policy rate in October 2021, by 0.4 percentage points and, respectively, 0.25 percentage points. Figure 3 shows the evolution of the monetary policy interest rate between January 2020 and July 2022. In the case of Romania, the normalization process is slower as compared to the other two selected countries. However, this evolution is also related to both the starting point (as the key interest rate was close to 2 percent per annum in 2020-2021, whereas in Hungary and Poland it was below 1 percent per annum) and the slightly lower inflationary pressures.

To sum up, at the current juncture, high inflationary pressures are stemming. Despite the ongoing normalization of the monetary policy, the annual inflation rate is still embarked on an upward trend. The key interest rate has suffered multiple changes and it is unclear for how long it will remain at a higher level. At the same time, the future steps of the normalization process are marked by high uncertainty. Given the adverse effects of the ongoing war, increased concerns are stemming from a probable slowdown in economic activity. The following sections investigate the impact of a permanent monetary policy shock on the main macroeconomic variables.

Figure 3. Evolution of the key interest rate in selected CEE countries

Source: Eurostat, author’s calculations

Results

It is common knowledge that a temporary increase in the interest rate leads to a decline in both the inflation rate and economic activity. However, empirical evidence in the case of a permanent monetary policy shock shows different responses of the main macroeconomic indicators.

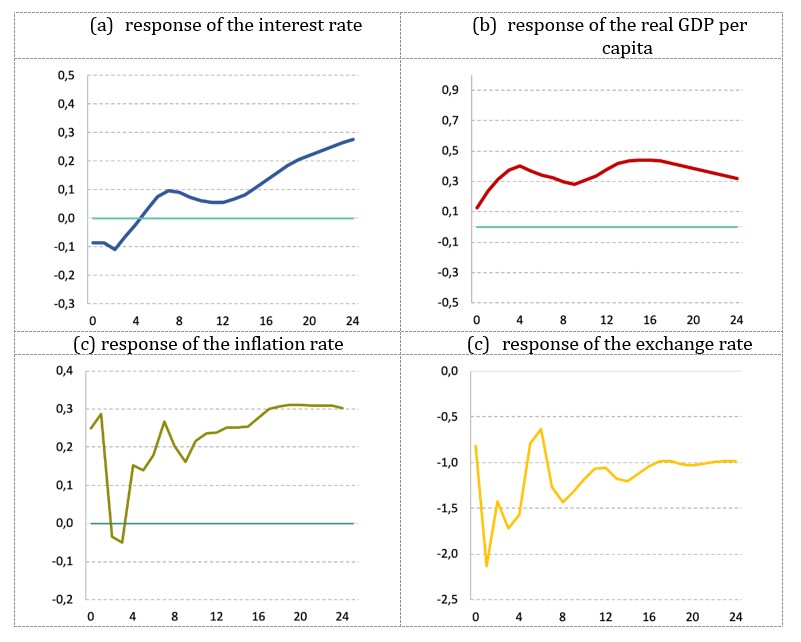

Figure 4a. Impulse response functions in the case of Hungary

Source: author’s calculations

Firstly, in the case of Hungary, as shown in Figure 4a, the permanent monetary policy shock starts with an easing for the first three quarters. Yet, after the fourth quarter, the interest rate gradually increases and it approaches its higher level. The shock is an expansionary one, as economic activity responds positively and empirical evidence points to a slight increase of the output, leading to a higher GPD per capita. The expansionary effects on the output translate into increased inflationary pressures. As a result, the inflation rate is evaluated to respond positively as well. In the first year, the initial inflationary response fades out fast until the fourth quarter. Over the medium term, it embarks on an upward trajectory and stabilizes at a higher level after sixteen quarters. As regards the exchange rate, the permanent monetary policy shock leads to an initial appreciation of the domestic currency, followed by a short-lived depreciation. However, exchange rate is anticipated to stabilize at a lower level.

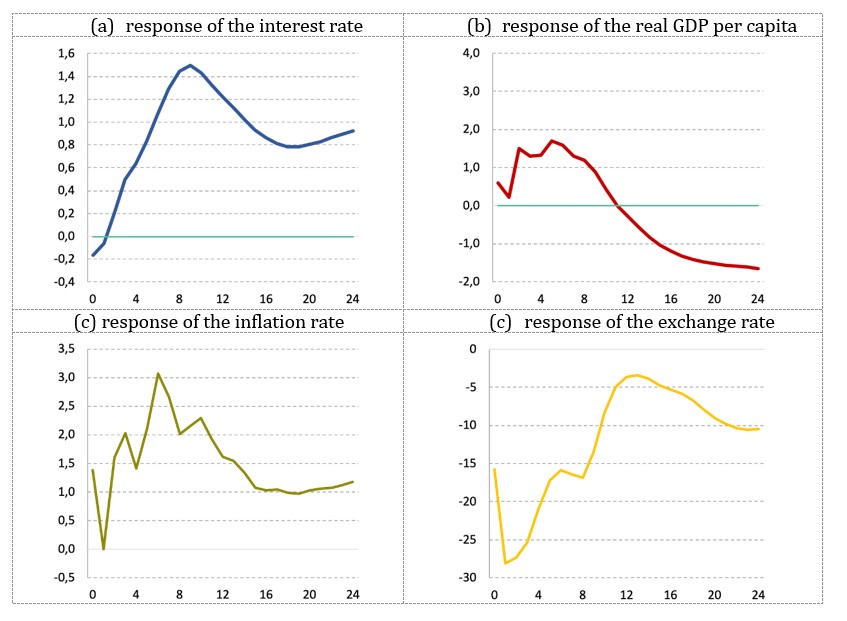

Secondly, in the case of the Polish economy, empirical evidence also shows an initial decrease of interest rates (Figure 4b). However, it embarks fast on an upward trajectory and reaches a peak after eight quarters, pointing to a possible overshooting. After this quarter, it slowly decreases. The permanent monetary policy shock is expansionary as well. The response of economic activity is a positive one for the first twelve quarters. However, some restrictive effects are envisaged over the longer term, as GDP per capita seems to stabilize below its pre-shock level. Furthermore, inflationary pressures are exerted. After an initial positive response followed by a short-lived decrease, the inflation rate follows an upward path and reaches a peak after six quarters. Afterwards, empirical evidence points to a decrease, yet the inflation rate is envisaged to stabilize at a higher level as compared to its initial state. In the case of the exchange rate, the relatively strong appreciation in the first two quarters is followed by a gradual return to values close to its initial state. However, the exchange rate is expected to remain at lower values, thus pointing to an overall appreciation of the domestic currency.

Figure 4b. Impulse response functions in the case of Poland

Source: author’s calculations

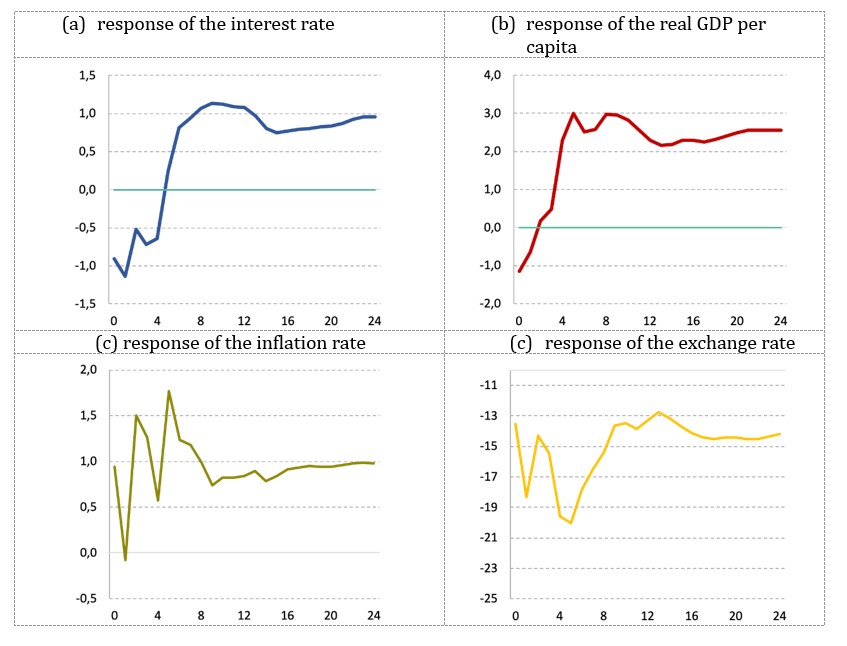

Lastly, a permanent shock of monetary policy in Romania also starts with an easing over the first four quarters (Figure 4c). Over the medium term, the interest rate slowly approaches its higher level. In the case of economic activity, the initial response is a negative one. However, it fades off fast. Expansionary effects dominate over the medium term as empirical evidence suggests a positive response of GDP peaking after twelve quarters and stabilizing at a higher level as compared to its initial state. As regards the inflation rate, after an overshooting in the first period, it starts decreasing. Moreover, it is envisaged to even hit a negative response, also reflecting the short-lived restrictive effects stemming from economic activity. Yet, over the medium term, it embarks on an upward trajectory and stabilizes after sixteen quarters at a higher level. Empirical evidence also points to a higher volatility in terms of the response in the inflation rate. The exchange rate is evaluated to decrease and to remain at a lower value over the medium term. The peak in this regard is reached after six quarters. Afterwards, the negative response starts fading out. Yet, it still stabilizes at a negative value, pointing to an overall appreciation of the domestic currency.

The three selected CEE countries respond quite similar to a permanent monetary policy shock. In this regard, the shock seems to be expansionary and inflationary, contrary to what one expects from the tightening of monetary policy. This evolution relates to the nature of the shock. While the temporary one is envisaged to lead to a decrease in both the inflation rate and GDP, the permanent one leads to opposite effects. One potential explanation is the impact on inflation expectations. Given the permanent nature of the normalization of the monetary policy, agents might anticipate a highly persistent inflation. This contributes to the inflationary pressures seen in the case of all CEE countries. In the first quarter, the inflation rate in the selected countries overshoots and afterwards it starts to decrease gradually, just to quickly embark on an upward trajectory and to stabilize at a higher level. An increased volatility in terms of the response of the inflation rate is seen in the case of Romania. However, it also confirms the path followed by Hungary and Poland.

Figure 4c. Impulse response functions in the case of Romania

Source: author’s calculations

In the case of economic activity, all three countries are expected to witness expansionary effects. While in the case of Hungary and Romania, empirical evidence points to a persistent positive response, the one in Poland is evaluated to fade out over the medium term. At the same time, the initial response of the Romanian GDP is not in line with that of Poland and Hungary. Empirical evidence suggests a short-lived restrictive impact during the first quarters, with a potential effect also on the inflation rate, leading to its decrease.

As regards the exchange rate, all countries experience an appreciation of the domestic currency. Despite a moderation in the negative response over several quarters, the exchange rate is expected to stabilize at a lower level as compared to its initial state.

Overall, the results point to the existence of Neo-Fisher effects in Hungary, Poland and Romania. A permanent monetary policy shock is envisaged to be inflationary and expansionary. These results are in line with the existing literature. However, in the case of the exchange rate, evidence points to an appreciation of the domestic currency, whereas Schmitt-Grohe (2020) finds evidence for a depreciation.

Concluding Remarks

At the current juncture, high inflationary pressures are stemming also on the back of the ongoing war in Ukraine. The persistent bottlenecks in global value chains and a potential flare-up in the energy crisis are likely to continue to fuel new hikes in the inflation rate. As a result, central banks have started the normalization of the monetary policy through successive increases of the key interest rate. This, however, has raised concerns regarding the impact of this process on economic activity, already hindered by the stagflation risk.

Empirical evidence points to the importance of the nature of the monetary policy shocks. In related literature, there is consensus regarding the impact of a temporary shock. It is assumed to decrease the inflation rate and to have a restrictive effect in the case of aggregate output. Instead, the paper investigates the macroeconomic impact of a permanent monetary policy shock. By introducing long run restrictions, we show that such a shock is inflationary and expansionary in the case of Hungary, Poland and Romania. In this regard, inflation is expected to stabilize at a higher level. This result might be explained by the role of anticipations. Given the permanent nature of the shock, agents expect the inflation rate to stand at persistent high values, leading to upward adjustments in inflation expectations. As a consequence, prices are anticipated to stabilize at a higher level. Yet, the model shows moderate inflationary pressures in the case of all selected CEE countries.

As for the economic activity, empirical evidence points to overall expansionary effects, to a lesser extent in the case of Poland. While in the case of the Romanian economy the initial response is a restrictive one, the permanent monetary policy shock gradually leads to an increase in GDP. However, in the case of the Polish economy, over the medium term, the response of economic activity turns slightly negative.

Empirical evidence suggests the presence of a Neo-Fisher effect in the case of selected CEE countries. A permanent monetary policy shock is expected to be inflationary and expansionary. Such results are in line with those found in related literature (Uribe, 2022, Cochrane, 2016). As for CEE countries, similar evidence in the case of the inflation rate is also confirmed by Plescau (2017), yet we obtain a slightly positive response in the case of the aggregate output. However, as regards the exchange rate, empirical evidence highlights an appreciation of the domestic currency in the case of selected CEE countries, contrary to the depreciation found by Schmitt-Grohe and Uribe (2022).

Overall, the research outcomes show that a permanent monetary policy is expansionary and inflationary, as opposed to a temporary shock which is likely to lead to output losses and disinflationary effects. These results have several implications for policymakers. At the current juncture, it is clear that the exacerbated inflationary pressures have to be fought. Given the envisaged positive impact on GDP, monetary authorities should not fear that a permanent shock might favour a recession. However, prices could be further fuelled. As a result, more focus should be on anchoring inflation expectations. In this regard, monetary authorities should strengthen their commitment to price stability and, if possible, increase the credibility of central banks. By contrary, if agents perceive the intervention of the monetary policy as a temporary shock, prices are expected to lower in tandem with adverse effects on economic activity, already jeopardized by the ongoing energy crisis and the negative shocks stemming from the war in Ukraine. Being aware of these outcomes, authorities should decide which trade-off is more convenient.

The model has its limitations. Despite being a useful tool for assessing the impact of a permanent monetary policy shock, its main weakness relies on its simplicity. It provides only a brief overview of the impact of the monetary policy tightening on the main macroeconomic indicators. Future research could imply the extension of the model. For instance, a Neo-Keynesian model embodying a whole set of equations and interactions between macroeconomic sectors could be built. At the same time, it could also include a clear specification for inflation expectations. In the case of those, another future direction for research could imply the analysis between inflation expectations and a permanent monetary policy shock. This way, it might help explaining better the positive relation between the tightening of the monetary policy and inflationary pressures, which might be counterintuitive, especially compared to the standard response of a temporary monetary policy shock.

References

Abhoff, S., Belke, A., Osowski, T. (2021), ‘Unconventional monetary policy and inflation expectations in the Euro area’, Economic Modelling, vol. 102(9), DOI: 10.1016/j.econmod.2021.105564

Airaudo, M., Hajdini, I. (2021), ‘Wealth effects, price markups and the Neo-Fisherian hypothesis’, Working Papers 21-27, Federal Reserve Bank of Cleveland, DOI: 10.26509/frbc-wp-202127

Alvarez, F., Lippi, F. (2020), ‘Temporary price changes, inflation regimes and the propagation of monetary shocks’, American Economic Journal: Macroeconomics, vol. 12(1), pages 104-152, DOI: 10.1257/mac.20180383

Bilbiie, F., Ragot, X. (2021), ‘Optimal monetary policy and liquidity with heterogeneous households’, Review of Economic Dynamics, vol. 41, pp. 71-95, DOI: 10.1016/j.red.2020.10.003

Beckworth, D. (2017), ‘Permanent versus temporary monetary base injections: implications for past and future Fed policy’, Journal of Macroeconomics, vol. 54(A), pp. 110-126, DOI: 10.1016/j.jmacro.2017.07.006

Blanchard, O., Quah, D. (1989),’The Dynamic Effects of Aggregate Demand and Supply Disturbances’, The American Economic Review, vol. 79(4), pages 655-673

Blanchard, O. (2016), ‘The Phillips curve: back to the ‘60s?’, The American Economic Review, vol. 106(5), pp. 31-34, DOI: 10.1257/aer.p20161003

Carvalho, A., Azevedo, J., Ribeiro, P. (2021), ‘Permanent and temporary monetary policy shocks and the dynamics of exchange rates’, Working Paper, Banco de Portugal

Chattopadhyay, S. (2021), ‘The Neo-Fisherianism to escape zero lower bound’, Environmental, Social, and Governance Perspectives on Economic Development in Asia, Vol. 29A, Emerald Publishing Limited, Bingley, pp. 1-19, DOI: 10.1108/S1571-03862021000029A016

Cochrane, J. (2016), ‘Do higher interest rates raise or lower inflation?’, Working Paper, Becker Friedman Institute

Crowder, W. (2020), ‘The Neo-Fisherian hypothesis: empirical implications and evidence?’, Empirical Economics, Springer, vol. 58(6), pages 2867-2888, DOI: 10.1007/s00181-018-1591-8

Egea, F., Hierro, L. (2019), ‘Transmission of monetary policy in the US and EU in times of expansion and crisis’, Journal of Policy Modeling, vol. 41(4), pp. 763-783, DOI: 10.1016/j.jpolmod.2019.02.012

Erceg, C., Jakab, Z., Linde, J. (2021), ‘Monetary policy strategies for the European Central Bank’, Journal of Economic Dynamics and Control, vol 132(9), DOI: 10.1016/j.jedc.2021.104211

Garin, J., Lester, R., Sims, E. (2018), ‘Raise Rates to Raise Inflation? Neo-Fisherianism in the New Keynesian Model’, Journal of Money Credit and Banking, 50(1), pages 243-259, DOI: 10.1111/jmcb.12459

Gobbi, L., Mazzocchi, R, Tamborini, R. (2022), ‘Monetary policy, rational confidence and Neo-Fisherian depressions’, Metroeconomica, DOI: 10.1111/meca.12398

Gobbi, L., Mazzocchi, R., Tamborini, R. (2019), ‘Monetary policy, de-anchoring of inflation expectations, and the “new normal’, Journal of Macroeconomics, vol. 61(1), DOI: 10.1016/j.jmacro.2018.10.006

Gurkaynak, R., Kara, A. Kisacikoglu, B., Lee, S. (2021), ‘Monetary policy surprises and exchange rate behaviour’, Journal of International Economics, vol. 130(C), DOI: 10.1016/j.jinteco.2021.103443

‘Hazell, J., Herreno, J., Nakamura, E., Steinsson, J. (2022), ‘The slope of the Phillips curve: evidence from US States’, The Quarterly Journal of Economics, vol. 137(3), pp. 1299-1344, DOI: 10.1093/qje/qjac010

Lukmanova, E., Rabitsch-Schilcher, K. (2022), ‘New VAR evidence on monetary transmission channels: temporary interest rate versus inflation target shocks’, SSRN Electronic Journal, DOI: 10.2139/ssrn.4164365

Olgun, E. (2022), ‘Interest rate and inflation: is there a Fisher or Neo-Fisher effect? Evidence from Turkey’, Journal of Administrative Sciences, vol. 20(45), pages 759-775, DOI: 10.35408/comuybd.1071560

Plescau, I. (2017), ‘Monetary Policy and inflation: Is there a Neo-Fisher Effect? Evidence from Inflation Targeting Countries in Central and Eastern Europe’, Ovidius University Annals, Economic Sciences Series, vol. XVII, issue 1, pages 578-583

Schmitt-Grohe, S., Uribe, M. (2022), ‘The effects of permanent monetary shocks on exchange rates and uncovered interest rate differentials’, Journal of International Economics, 135:103560, DOI: 10.1016/j.jinteco.2021.103560

Spahn, P. (2018), ‘Unconventional views on inflation control: Forward guidance, the Neo-Fisherian approach, and the fiscal theory of the price level’, Hohenheim Discussion Papers in Business, Economics and Social Sciences 02-2018, University of Hohenheim, Faculty of Business, Economics and Social Sciences

Svensson, L. (2003), ‘What is wrong with Taylor rules? Using Judgment in monetary policy through targeting rules’, Journal of Economic Literature, vol. 41 (2), pp. 426-477, DOI: 10.1257/002205103765762734

Uhlig, H. (2005), ‘What are the effects of monetary policy on output? Results from an agnostic identification procedure’, Journal of Monetary Economics, vol. 52(2), pages 381-419, DOI: 10.1016/j.jmoneco.2004.05.007

Uribe, M. (2017), ‘The Neo-Fisher effect in the United States and Japan’, NBER Working Paper series no. 23977, National Bureau of Economic Research, DOI: 10.3386/w23977

Uribe, M. (2022), ‘The Neo-Fisher Effect: Econometric Evidence from Empirical and Optimizing Models’, American Economic Journal, Macroeconomics, 14(3), pages 133-162, DOI: 10.1257/mac.20200060

Vavra, J. (2014), ‘Inflation dynamics and time-varying volatility: new evidence and an SS interpretation’, The Quarterly Journal of Economics, vol. 129(1), pp. 215-258, DOI: 10.1093/qje/qjt027

Weber, M., Pasten, E., Schoenle, R. (2020), ‘The propagation of monetary policy shocks in a heterogeneous production economy’, Journal of Monetary Economics, vol. 116, pp. 1-22, DOI: 10.1016/j.jmoneco.2019.10.001

Williamson, S. (2016), ‘Neo-Fisherism: A radical idea or the most obvious solution to the low-inflation problem?’, The Regional Economist, Federal Reserve Bank of St. Louis

Wolden-Bache, I., Leitemo, K. (2008), ‘The price puzzle: mixing the temporary and permanent monetary policy shocks’, Working Paper 2008/18, Norges Bank

Williamson, S. (2019), ‘Neo-Fisherism and inflation control’, Canadian Journal of Economics, vol 52(3), pages 882-913, DOI: 10.1111/caje.12403

Zahid, S. (2019), ‘From price puzzle to Neo-Fisherianism’, SSRN Electonic Journal, DOI: 10.2139/ssrn.3349096