Bucharest University of Economic Studies, Bucharest, Romania

Volume 2024,

Article ID 735542,

Journal of Eastern Europe Research in Business and Economics,

11 pages,

DOI: https://doi.org/10.5171/2024.735542

Received date: 23 March 2022; Accepted date: 28 October 2024; Published date: 19 November 2024

Academic Editor: Simona Andreea Apostu

Cite this Article as:

Robert-Adrian Grecu and Cheptis Alexandra (2024)," Synchronization of Financial Cycles in Selected Central and Eastern European Countries", Journal of Eastern Europe Research in Business and Economics Vol. 2024 (2024), Article ID 735542, https://doi.org/10.5171/2024.735542

The COVID-19 pandemic had a strong economic impact, but its effects were felt also in the financial area. As a result of the economic recovery in 2021, there has been registered a significant growth of the lending activity in Central and Eastern European countries. This study illustrates that these increases have generated, for countries such as Hungary, the re-entry of the financial cycle in the expansion phase, having recorded positive deviations of credit from its long-term trend, situation which was not seen since the period before the last financial crisis. The results of the analysis also show that the financial cycle has a longer duration compared to the business cycle, as well as a higher amplitude. Thus, the turning points of the financial cycle are rarer, but they generate stronger effects than those of the business cycle. Regarding the synchronization of financial cycles at the level of the analyzed CEE countries, the results of this paper illustrate a strong correlation between the financial cycles of Romania, Bulgaria, and Hungary.

The crisis from 2007-2008 has shown that, in addition to the study of the business cycle, a very high importance should be given to the analysis of the financial cycle, whose turning points can have strong effects on the macroeconomic framework. According to the analyzes in the literature, the financial cycle is defined in its simplest form as the dynamics of credit in the economy, presented by several types of proxy variables. The duration of a financial cycle differs significantly from that of a business cycle, the results of the literature confirmed by this study at the level of the CEE countries illustrate that a financial cycle tends to be longer than a business one. The turning points of the financial cycle being rarer, but with a higher amplitude than those of the business cycle.

In addition to the characteristics of the financial cycle, another important aspect is the type of the links between the financial cycles of different states. In this study, 4 countries from Central and Eastern Europe were analyzed, namely: Romania, Hungary, Poland, and Bulgaria. The results show relatively close links between financial cycles in Romania, Bulgaria, and Hungary bilaterally. The financial cycle in Poland has a relatively different dynamics from that of the above-mentioned group of states. Thus, although Poland is part of the peer group of CEE countries, the characteristics of the financial cycle bring it closer to other EU Member States.

Another result of the analysis is that in the second half of 2021, the deviation of credit-to-GDP from its long-term trend, considering the standard approach, was positive only for Hungary. The only country, out of the 4 analyzed, which is currently in an expansion phase of the financial cycle, registering a very strong increase in lending activity. However, by conducting an analysis based on additional indicators specific to developing countries, it is observed that Hungary, Bulgaria, and Romania have positive deviations of credit-to-GDP from the long-term, a sign of a sharp increase in lending during the recent period.

Literature Review

The analysis of the financial cycle has become more important after the last financial crisis, at which point it was observed that the banking system through its activity has a very important role in the macroeconomic dynamics. One of the econometric instruments applied to determine the financial cycle is the Hodrick-Prescott filter, used in analyzes such as Drehmann et al. (2010), Gachter et al. (2013) or Drehmann and Yetman (2018). An important aspect of determining the financial cycle is related to the variables through which it is defined, namely, starting from the dynamics of lending activity, the dynamics of real estate prices or the dynamics of financial asset prices. Claessens, Kose and Terrones (2011) have shown that equity and house cycles are longer than the credit cycle. At the same time, Stremmel (2015) identified that the best measures for determining the financial cycle are the variables: credit-to-GDP, credit growth and the house prices to income indicator.

Another important aspect regarding the financial cycle is related to its duration. Drehmann, Borio and Tsatsaronis (2012) found that the financial cycle is longer and has a higher amplitude than the business cycle. More recent results in this area have been obtained by Schuler, Hiebert and Peltonen (2017) who showed that at the G7 level the financial cycle has a size of about 15 years, well above that of about 6,7 years of the business cycle. Runstler and Vlekke (2018) also found that for developed countries such as France, Germany, UK or USA, the financial cycle is longer than the business cycle, ranging from 13 to 18 years.

The degree of financial cycle synchronization in different states is another discussed topic in the literature. An important study conducted for the Euro Zone countries by Oman (2019) illustrates that financial cycles are less correlated with each other compared to business cycles. At the same time, in terms of intertemporal evolution, the synchronization between financial cycles has decreased over time, compared to the synchronization between business cycles which seems to have followed an upward trend. Another study on the synchronization of financial cycles at the level of a group of states from the Euro Zone is that of the Deutsche Bundesbank (2019) which illustrated that the financial cycle of Germany is less synchronized with those of the rest of the analyzed states (Belgium, France, Italy, The Netherlands, and Spain). A similar result regarding the low level of synchronization of the German financial cycle, this time compared to those in the G7 states, was obtained by Schuler, Hiebert, and Peltonen (2017). For European countries, Stremmel (2015) illustrated that financial cycles are more correlated during periods of financial stress compared to boom periods, a result also obtained by Oman (2019), but also by Stremmel and Zsamboki (2015). However, there are studies that have analyzed the synchronization of financial cycles in other groups of states; Gammadigbe (2021) conducted an analysis for West African Economic and Monetary Union countries, the results illustrating a low level of correlation between the financial cycles of these states. Thus, it is recommended to implement different macroprudential policies and tools adapted to the context of each country. Although there are groups of states with a relatively low level of financial cycle synchronization, Rey (2015) illustrates that, overall, there is a strong international co-movement among financial variables. The analysis regarding the correlation of the financial cycles in different states has a very important role since a synchronization of the turning points of the financial cycle in several states can generate long periods of strong economic decline.

Although financial and business cycles are not always synchronized, they can influence each other. Cagliarini and Price (2017) have shown that the business cycle is the one that drives the variation of the financial cycle in most cases. Given these links, macro-prudential policy must be synchronized with monetary policy so that both the economic and financial objectives of a country can be met. A similar recommendation is made by Deutsche Bundesbank (2019) because of obtaining a high level of synchronization of financial cycles with business ones, which implies a congruence between monetary policy and macro-prudential policy. However, the financial cycle also influences the business cycle. Dees and Zorell (2011) illustrate that financial integration generates a decrease in the level of business cycles synchronization, but this result may differ from an emerging economy to an advanced one. Ozcan, Papaioannou and Perri (2013) also show that financial integration influences the synchronization of business cycles. The link between the financial cycle and the business cycle has important effects on determining the recession risk. Borio, Drehmann and Xia (2018) show that a boom period of the financial cycle makes the business cycle more fragile and brings it closer to a turning point. Thus, the financial cycle can be another important proxy for the analysis of the business cycle dynamics.

Methodology

Data

The article analyzes 4 countries from the Central and Eastern Europe region, namely: Romania, Poland, Hungary, and Bulgaria. The first indicator used to identify the financial cycle is credit-to-GDP, which was calculated by reporting the nominal value of the private sector credit stock to the annualized gross domestic product. Data on the nominal value of the private sector credit stock were taken from the ECB database while data on quarterly gross domestic product were taken from the Eurostat database.

The second indicator used as a proxy for the financial cycle is the one used by Mendoza and Terrones (2008). In this context, data processing started from the value of the private sector credit stock, which through the GDP deflator was transformed from nominal to real values. The next step was to turn real credit data series into per capita values and, as a last step, the real per capita credit series was passed through the logarithmic operator. Credit data were taken from the ECB database while data on the GDP deflator and population were taken from the Eurostat database.

The period analyzed in the article is Q4 2004 – Q3 2021, and the program used for the application of the econometric procedures was Matlab 2020b.

Model

In order to identify the financial cycle, the Hodrick-Prescott filter was used as an econometric procedure. It was applied on two categories of indicators, the construction of the data series for them being previously presented. By means of this econometric procedure, a data series is decomposed into the trend component and cyclical component :

To determine the trend of the data series, a loss function presented in formula (2) was minimized:

Where is representing the smoothing parameter. In the study performed by Hodrick and Prescott (1980), to determine the business cycle, it was used a smoothing parameter . However, when it comes to financial cycle analysis, the Basel Committee on Banking Supervision recommends the use of a smoothing parameter , included even in the standard methodology for determining the financial cycle in order to apply and recalibrate the countercyclical capital buffer. The use of a high smoothing parameter, such as the one recommended by BCBS, is considered suitable for long-term cycles, such as the one of credit.

By using the smoothing parameter recommended by BCBS, the financial cycle is considered to be four times longer than the business cycle, as noted by Drehmann et al. (2010). However, this long duration is specific to countries with a developed financial sector; for those with an emerging economy, it is more appropriate to use a lower smoothing parameter.

In this regard, Ravn and Uhlig (2002) proposed a standard formula for determining the optimal value of the smoothing parameter, depending on the ratio between the duration of the financial cycle and the one of the business cycle, ratio denoted by ().

Thus, in addition to the standard results based on the smoothing parameter proposed by BCBS, in the article it was also performed an analysis according to an additional approach in which, for the 4 emerging economies from CEE, a significantly lower smoothing parameter was applied, similar to the one applied in the business cycle analysis, as in the paper by Alupoaiei et al. (2020).

Results and discussions

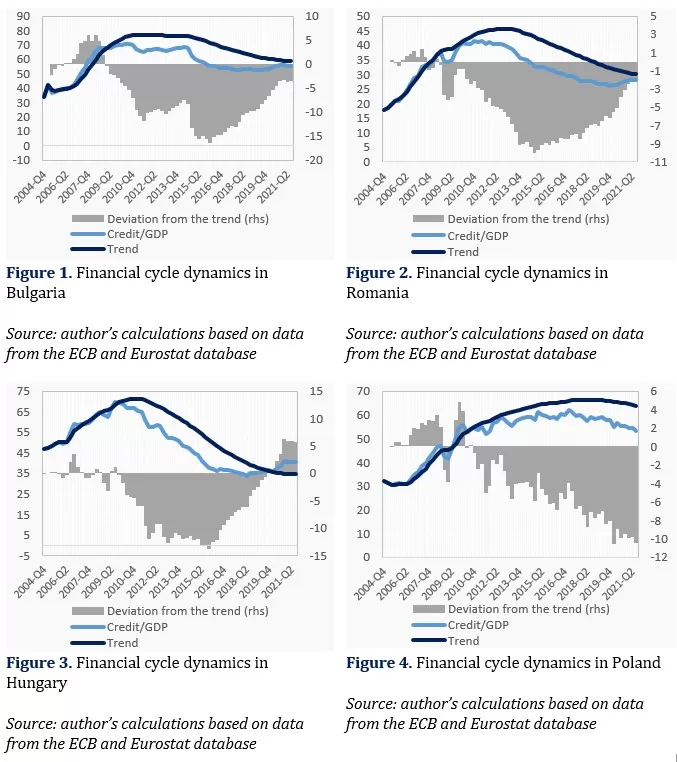

The analysis of the financial cycle was performed through the variables related to the evolution of the lending activity. Starting from the methodologies used in the literature, the financial cycle was determined in a first phase based on the credit-to-GDP indicator (recommended by BCBC), then based on the indicator applied by Mendoza and Terrones (2008). The results regarding the dynamics of the financial cycle based on the credit-to-GDP methodology are presented in figures 1-4.

In the CEE countries, the duration of the financial cycle was relatively high during the analyzed period (Q4 2004 – Q3 2021). These results illustrate that the size of the financial cycle is on average higher than the one of the business cycle, which for the analyzed states is about 4 years, according to the results of Grecu (2022). Important differences are registered also in terms of amplitude, financial cycle being characterized by higher dynamics than the business cycle.

The strong effects of the shocks during the last two decades have been felt significantly in all four analyzed countries. Following the last financial crisis (2007-2008), the deviation from the long-term trend of credit-to-GDP became negative, and remained negative for Bulgaria, Romania, and Poland until the end of the analysis period (Q3 2021). However, for Hungary the credit-to-GDP gap has become positive since the beginning of 2020, both as a result of the increase in credit (especially for the household sector, where Hungary was on the first position at EU level[1]) and due to the strong contraction of gross domestic product. An increase of the credit-to-GDP gap was registered during the COVID-19 pandemic also in Romania and Bulgaria, but, for these two countries, the deviation remained negative. In Romania, the evolution of the financial cycle during the health crisis came as a result of a strong increase in lending to non-financial companies, while in Bulgaria the increase came mainly from the increase in the stock of loans to households.

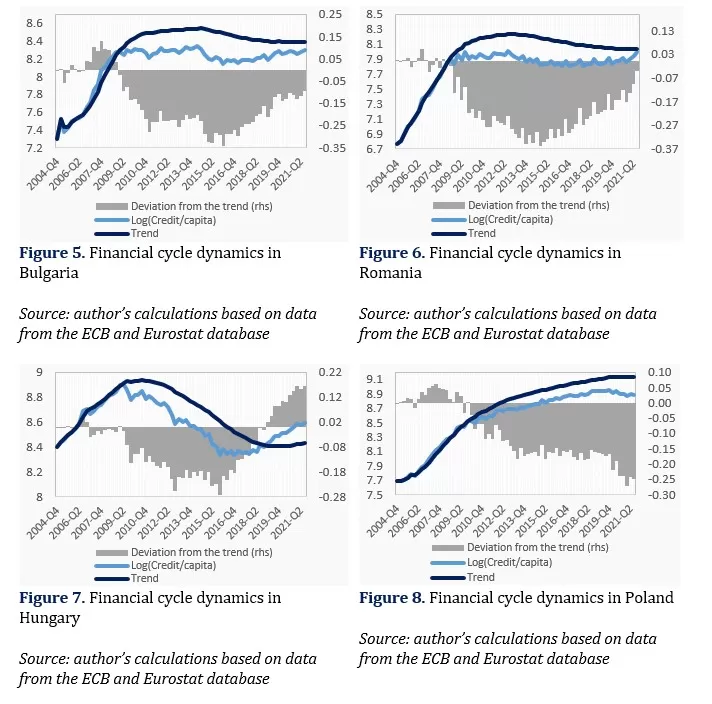

The second representation of the financial cycle is the one in which the credit dynamics is used as in the methodology applied by Mendoza and Terrones (2008), the results being presented in figures 5-8.

Similar to the analysis performed having as reference indicator credit-to-GDP, also in this case, to determine the financial cycle, a proxy of the lending activity, materialized in the log (real credit/capita), was used. The results regarding the size of the financial cycle are in line with the ones obtained through the previous analysis, the duration of the cycle being relatively large exceeding that of the business cycle. At the same time, in this case too the most important turning points were generated as a result of the last financial crisis. However, unlike the analysis based on the credit-to-GDP indicator, because of the last financial crisis, the deviation from the long-term trend became negative faster. Thus, an analysis of the financial cycle based on the indicator used by Mendoza and Terrones (2008) captures the turning points in advance compared to the analysis based on the standard Basel indicator.

Regarding the dynamics during the COVID-19 pandemic period, it can be noticed that a strong increase of the deviation from the long-term trend was registered in Romania, Bulgaria, and Hungary. In the case of the last-mentioned country, the deviation became even positive starting from 2020.

The next stage of the analysis is based on determining the synchronization degree of the financial cycles in the analyzed countries.

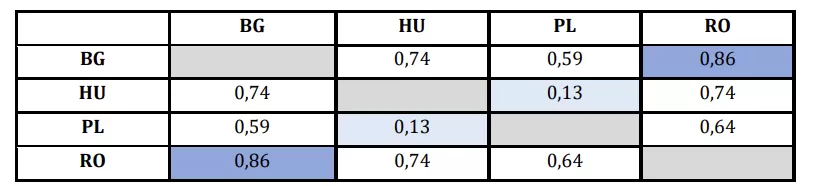

Table 1. Correlation matrix of financial cycles in the CEE states, for reference indicator credit-to-GDP

Source: author’s calculations based on data from the ECB and Eurostat database

According to the results in Table 1, the strongest correlation of financial cycles was registered between Romania and Bulgaria. The correlation coefficient of the financial cycles from the two countries is 0,86. There is also a strong correlation of financial cycles from Hungary and Romania but also between Bulgaria and Hungary. In both cases, the correlation coefficient is 0,74. On the other hand, the least correlated financial cycles are those of Hungary and Poland, for which the correlation coefficient is about 0,13.

The second representation of the financial cycle is the one based on the methodology applied by Mendoza and Terrones (2008), for which the correlation matrix at the level of the analyzed countries is presented in Table 2.

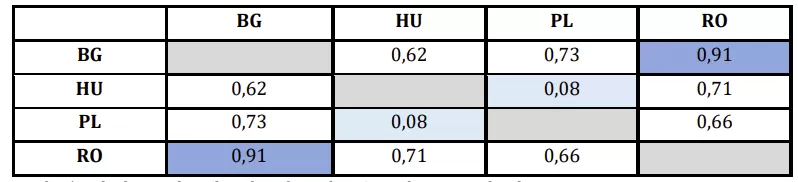

Table 2. Correlation matrix of financial cycles in the CEE states, for reference indicator log (credit/capita)

Source: author’s calculations based on data from the ECB and Eurostat database

Similar to the previous situation, in this case too the highest level of the correlation coefficient of the financial cycles is registered for the pair of countries composed of Romania and Bulgaria. However, in this case, the degree of correlation is even higher than in the previous case, standing at 0,91. The second higher correlation coefficient is that recorded between Bulgaria and Poland, standing at 0,73. However, as in the previous case, the lowest level of the correlation coefficient is recorded between Poland and Hungary, its value being even lower than in the case of the credit-to-GDP gap analysis, standing at 0,08. Another important aspect regarding this issue is the synchronization of the financial cycles identified based on the two methodologies (Table 3).

Table 3. Correlation between the financial cycles from the two methodologies

Source: author’s calculations based on data from the ECB and Eurostat database

Table 3 shows that the determination of the financial cycle using the Basel indicator generates results relatively similar to those obtained from the analysis based on the methodology of Mendoza and Terrones (2008). The highest degree of synchronization of the financial cycles obtained by the two methods is identified for Bulgaria, where the correlation coefficient is about 0,96. In the opposite corner, the lowest correlation coefficient between the financial cycles obtained through the two methodologies is identified in Romania, being close to the level of 0,85.

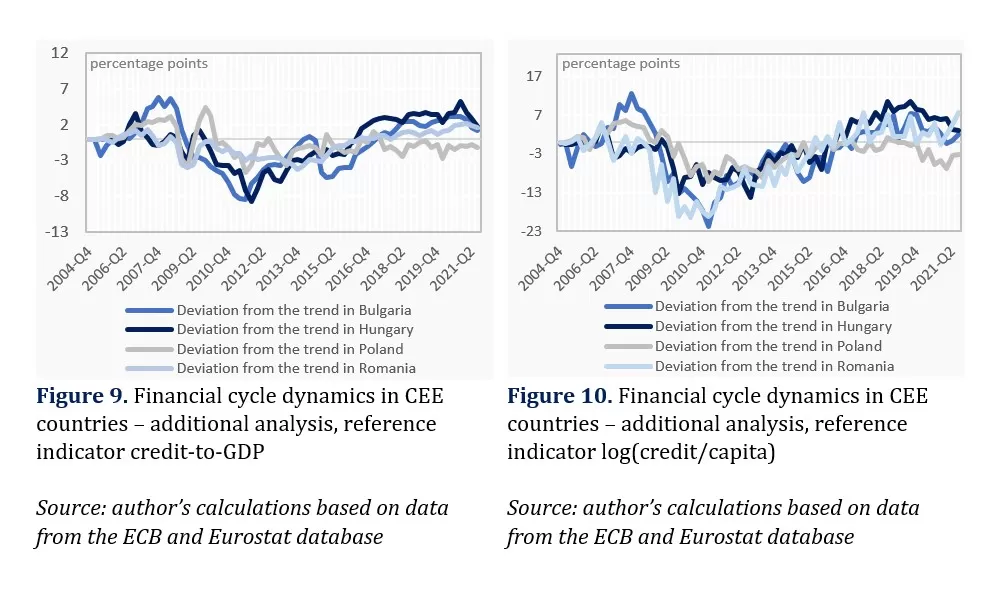

Up to this point, a Hodrick-Prescott filter with a smoothing parameter of 400.000 was used to determine the financial cycles. This smoothing parameter was proposed by the BCBS to calculate the Basel standard indicator used to identify the phases of the financial cycle in order to calibrate the countercyclical capital buffer. However, this relatively high value of the parameter has a higher practical applicability for advanced economies, at the level of which a financial cycle extends over a very long period. For emerging economies, it is suitable to use a lower smoothing parameter, with a value closer to the one used in determining the business cycle. In this regard, for the robustness of the results, the analyzes carried out previously will be presented below using a smoothing parameter of 1.600, representative for a significantly shorter financial cycle, characteristic for the emerging economies from CEE. In the following, this approach will be called additional analysis, while the classical approach previously performed will be called standard analysis.

The analysis based on the additional approach illustrates that the financial cycle measured both through the credit-to-GDP gap and through the indicator log(credit/capita) is shorter and much more volatile than in the case of the standard approach. However, even in this situation the financial cycle has a longer duration than the business cycle in all analyzed countries. According to the results based on the credit-to-GDP indicator, at the end of the analysis interval, the deviation from the long-term trend is positive for Bulgaria, Hungary, and Romania. This result illustrates that the financial cycle is in an expansion phase for these countries, largely determined by the significant lending growth registered. The most pronounced minimum point of the financial cycle during the period studied is that generated in the last financial crisis, the impact of which, as can be seen graphically, was felt even after a period of several years since its inception.

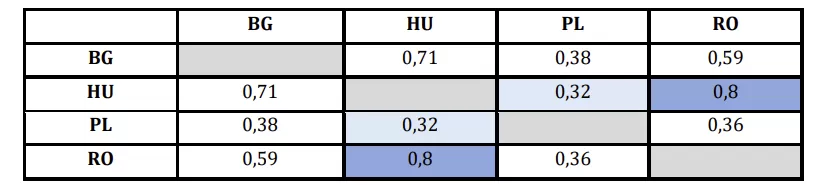

Starting from the previous analysis on the standard approach also in the case of the additional one, the correlation matrix of the financial cycles from the CEE states was calculated (Table 4).

Table 4. Correlation matrix of financial cycles in the CEE member states, for reference indicator credit-to-GDP, additional analysis

Source: author’s calculations based on data from the ECB and Eurostat database

According to the results in Table 4, the strongest correlation of financial cycles, determined based on the additional approach, is between Romania and Hungary, different from the standard approach where the strongest link was identified between Romania and Bulgaria. Thus, the correlation coefficient of the financial cycles in the two states, Romania and Hungary, is 0,8. There is also a strong correlation of financial cycles between Bulgaria and Hungary, in this case the coefficient is 0,71. On the other hand, the least correlated financial cycles are those in Bulgaria and Poland, for which the correlation coefficient is about 0,32. The result is different from the one of the analysis based on the standard approach where the lowest correlation coefficient was identified between the financial cycles in Poland and Hungary. It should also be noted that the analysis based on the standard approach illustrates more extreme values of the correlation coefficients compared to the additional approach.

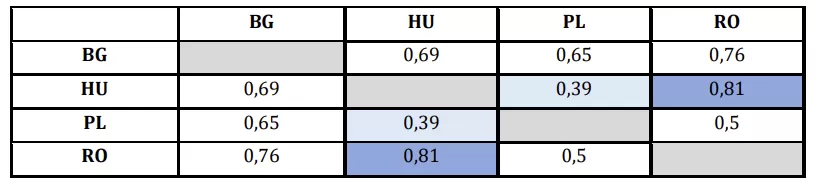

The second representation of the financial cycles is the one through which the financial cycle is based on the methodology used by Mendoza and Terrones (2008); for the additional approach, the correlation matrix at the level of the four analyzed countries is presented in Table 5.

Table 5. Correlation matrix of financial cycles in the CEE member states, for reference indicator log (credit/capita), additional analysis

Source: author’s calculations based on data from the ECB and Eurostat database

Similar to the previous situation, in this case too the highest correlation coefficient of the financial cycles is registered for the pair of states composed of Romania and Hungary. The correlation coefficient is even higher than in the previous case, standing at 0,81, but lower than the maximum level recorded through the standard approach for this methodology. The second highest correlation coefficient is the one recorded between Bulgaria and Romania, approximately 0,76. The level being higher than the one obtained through the analysis based on the credit-to-GDP gap but lower than the result based on the standard approach for this indicator. As in the previous case, the lowest level of the correlation coefficient is recorded between Poland and Hungary, its value being higher than in the initial case, standing at 0,39.

Another important aspect is the synchronization of the financial cycles given by the two methodologies, based on the additional approach (Table 6).

Table 6. Correlation between the financial cycles from the two methodologies for the additional analysis

Source: author’s calculations based on data from the ECB and Eurostat database

The results in Table 6 illustrate that determining the financial cycle using the Basel indicator with the additional approach generates results relatively similar to those obtained from the analysis based on the methodology of Mendoza and Terrones (2008). The highest degree of financial cycles synchronization between the two methods is identified for Bulgaria, where the correlation coefficient is about 0,93. In the opposite corner, the lowest correlation coefficient between the financial cycles obtained through the two methodologies is identified in Poland, close to the level of 0,56. Taking into account these results, it could be concluded that the additional approach shows a lower level of correlation between the financial cycles obtained based on the two methodologies.

Conclusions

The purpose of this article was to determine the characteristics of the financial cycles in four of the Central and Eastern European countries. In addition to analyzing the case for each of the states, the level of financial cycles synchronization between them was determined.

A first result obtained is that the duration of financial cycles in the CEE countries is longer than the duration of the business cycles, both through the BCBS methodology and through the methodology of Mendoza and Terrones (2008). Currently, the only country that, based on the standard analysis, has a positive credit-to-GDP gap is Hungary, because of a strong increase in lending activity. However, the results of the additional approach illustrate that in addition to Hungary, in the scenario of a smaller financial cycle, also Romania and Bulgaria, have a positive credit-to-GDP gap. In view of this, during 2021 both the Romanian[2] and Bulgarian[3] macro-prudential authorities took decisions to increase the countercyclical capital buffer (CCyB), to limit the amplitude of the financial cycle.

Regarding the link of the financial cycles in the CEE countries, the results show that, through the standard approach, Romania and Bulgaria register the highest level of the correlation coefficient, approximately 0,86 for the BCBS indicator and 0,91 based on the methodology of Mendoza and Terrones (2008). However, the least correlated financial cycles, according to the same approach, are those in Hungary and Poland, for which the correlation coefficient is below 0,15 considering both methodologies.

In the additional approach, the countries for which the highest level of financial cycles correlation was obtained are Romania and Hungary, while, as in the case of the standard approach, the lowest level of cycle correlation was recorded between Hungary and Poland.

As future research directions, this study can be extended with an analysis of the financial cycle’s synchronization at the level of all EU Member States. Moreover, extensions could be made also in terms of methodology, using other types of filters or other indicators to identify financial cycles.

Bibliography

Alupoaiei, A., Kubinschi, M., Tatarici, L., & Zaharia, A. (2020). The implementation of the countercyclical capital buffer (CCyB) in Romania. National Bank of Romania Occasional Papers, No. 50.

Borio, C., Drehmann, M., & Xia, D. (2018). The financial cycle and recession risk. BIS Quarterly Review, December 2018, pp. 59 – 71.

Cagliarini, A., & Price, F. (2017). Exploring the Link between the Macroeconomic and Financial Cycles. Reserve Bank of Australia Conference Volume, pp. 7 – 50.

Claessens, S., Kose, M. A., & Terrones, M. E. (2011). Financial Cycles: What? How? When? IMF Working Paper, No. WP/11/76.

Dees, S., & Zorell, N. (2011). Business cycle synchronization disentangling trade and financial linkages. ECB Working Paper, No. 1322.

Deutsche Bundesbank (2021). Financial cycles in the euro area. Monthly Report, January 2021, pp. 51–74.

Drehmann, M., Borio, C. E., Gambacorta, L., Jimenez, G., & Trucharte, C. (2010). Countercyclical Capital Buffers: Exploring Options. BIS Working Papers, No. 317.

Drehmann, M., Borio, C., & Tsatsaronis, K. (2012). Characterising the Financial Cycle: Don’t Lose Sight of the Medium Term! BIS Working Paper, No. 380.

Drehmann, M., & Yetman, J. (2018). Why you should use the Hodrick-Prescott filter at least to generate credit gaps. BIS Working Paper, No. 744.

Gachter, S., Riedl, A., & Ritzberger-Grünwald, D. (2013). Business cycle convergence or decoupling? Economic adjustment in CESEE during the crisis. BOFIT Discussion Papers, No. 3/2013.

Gammadigbe, V. (2021). Financial Cycles Synchronization in WAEMU Countries: Implications for Macroprudential Policy. Finance Research Letters, 41.

Grecu, R. (2022). Synchronization of Business Cycles in European Union Countries. Proceedings of the International Conference on Business Excellence, No. 16.

Kalemli-Ozcan, S., Papaioannou, E., & Perri, F. (2013). Global Banks and Crisis Transmission. Journal of International Economics, No. 89.

Mendosa, E. T., & Terrones, M. E. (2008). An anatomy of credit booms: evidence from macro aggregates and micro data. NBER Working Paper Series, No. 14049.

Oman, W. (2019). The Synchronization of Business Cycles and Financial Cycles in the Euro Area. International Journal of Central Banking, No. 57.

Ravn, M., & Uhlig, H. (2002). On Adjusting the HP-Filter for the Frequency of Observations. Review of Economics and Statistics, No. 84.

Rey, H. (2015). Dilemma Not Trilemma: The Global Financial Cycle and Monetary Policy Independence. NBER Working Paper, No. 21162.

Runstler, G., & Vlekke, M. (2018). Business, Housing, and Credit Cycles. Journal of Applied Econometrics, No. 33.

Schuler, Y. S., Hiebert, P., & Peltonen, T. A. (2017). Coherent Financial Cycles for G-7 Countries: Why Extending Credit Can Be an Asset. ESRB Working Paper, 43.

Stremmel, H. (2015). Capturing the financial cycle in Europe. ECB Working Paper, No. 1811.

Stremmel, H., & Zsamboki, B. (2015). The Relationship between Structural and Cyclical Features of the EU Financial Sector. ECB Working Paper, No. 1812.