The Bucharest University of Economic Studies Bucharest, Romania

Volume 2025,

Article ID 230203,

Journal of Eastern Europe Research in Business and Economics,

8 pages,

DOI: https://doi.org/10.5171/2025.230203

Received date: 30 September 2024; Accepted date: 31 December 2024; Published date: 24 February 2025

Cite this Article as:

Cristina – Elena BEJENARU (2025)," Early Detection of Sovereign Market Instability in Romania: The Role of SovCISS", Journal of Eastern Europe Research in Business and Economics Vol. 2025 (2025), Article ID 230203, https://doi.org/10.5171/2025.230203

Drawing on the methodology proposed by Garcia-de-Andoain and Kremer (2018), SovCISS incorporates key factors – credit risk, volatility, and liquidity – to provide a comprehensive overview of potential market pressures in the Romanian bond market. The indicator’s empirical applications reveal a notable alignment between Romania’s market and those of the Euro Area and three major Central European economies (Poland, Hungary, and the Czech Republic), underscoring shared susceptibilities to external shocks. The analysis highlights a balanced contribution of credit risk, volatility, and bid-ask spreads to overall stress levels, although credit spreads have taken on a more substantial role since 2021 in tandem with Romania’s comparatively restrictive monetary stance. By providing early warnings and detailed signals across different maturities, SovCISS helps policymakers respond to looming challenges and reinforce financial stability. This research expands existing literature by introducing a real-time surveillance instrument that strengthens sovereign risk management strategies within Europe’s increasingly interconnected financial environment.

JEL Classifications: G10, G12, G15, G20, E44

Keywords: financial system, financial stability, financial stress index, sovereign bonds.

Introduction

Measuring sovereign bond market stress is crucial for identifying and mitigating systemic risks in the financial system. Stress in sovereign bond markets can spread through several channels, most notably through the sovereign-bank nexus, where tensions in sovereign markets spill over into the banking sector, increasing overall systemic risks (Romo & Tejada, 2020). Furthermore, stress in these markets can disrupt interbank lending, leading to liquidity shortages and a breakdown in credit flows, as demonstrated by Frutos et al. (2016) during the European Financial and Sovereign Debt Crisis.

Rising sovereign yields can exacerbate these issues by increasing public sector borrowing costs, which may necessitate austerity measures. These measures can aggravate economic downturns and further strain fiscal stability, particularly in countries with weaker fiscal fundamentals, as Bongaerts, De Jong, and Driessen (2011) have shown in their analysis of euro area sovereign bond spreads. In highly interconnected regions like the Eurozone, the potential for cross-border contagion underscores the need for continuous monitoring (Skouralis, 2023). The risk of systemic stress transmission through cross-country spillovers has been further emphasized in studies on systemic risk and euro area monetary policy (Skouralis, 2023).

Traditionally, sovereign stress is typically evaluated using metrics such as the yield spread between a government’s bond and a safer benchmark bond, or through the credit default swap (CDS) spread for government debt. These metrics serve as indicators of the excess default risk premium, reflecting the market’s perception of heightened risk associated with a particular government’s bonds (Longstaff, Pan, Pedersen, & Singleton, 2011). However, such metrics alone do not capture the full range of market stress, which can also manifest in yield volatility and reduced liquidity (Fleming & Remolona, 2002). Recent studies by Gómez-Puig, Pieterse-Bloem, and Sosvilla-Rivero (2023) highlight how the dynamic interconnection between credit and liquidity risks can shift during times of financial tension, further complicating the measurement of market stress.

This paper applies the Composite Indicator of Systemic Sovereign Stress (SovCISS) methodology, originally developed by Garcia-de-Andoain and Kremer (2018), to quantify sovereign bond market stress in Romania. Unlike the existing SovCISS indicators available in the European Central Bank’s Statistical Data Warehouse (SDW) for the Eurozone and select EU member states, Romania has not previously been included in such assessments. To the best of our knowledge, this study is the first to apply SovCISS to Romania, addressing a critical gap in both the literature and data regarding Romania’s financial stability.

The customized SovCISS for Romania integrates a broader set of stress factors, including yield volatility and bid-ask spreads alongside credit spreads, offering a more comprehensive and dynamic measure of market stress. This approach follows the methodology suggested by Bongaerts, De Jong, and Driessen (2011), where multiple risk factors, such as country-specific credit risk and spillover effects, were crucial in understanding sovereign spreads during the euro area crisis.

The paper is structured as follows: the first section introduces the topic, followed by a detailed description of the methodology and data used in the second section. The third section presents the results, and the final section discusses the conclusions drawn from the analysis.

Data and Methodology

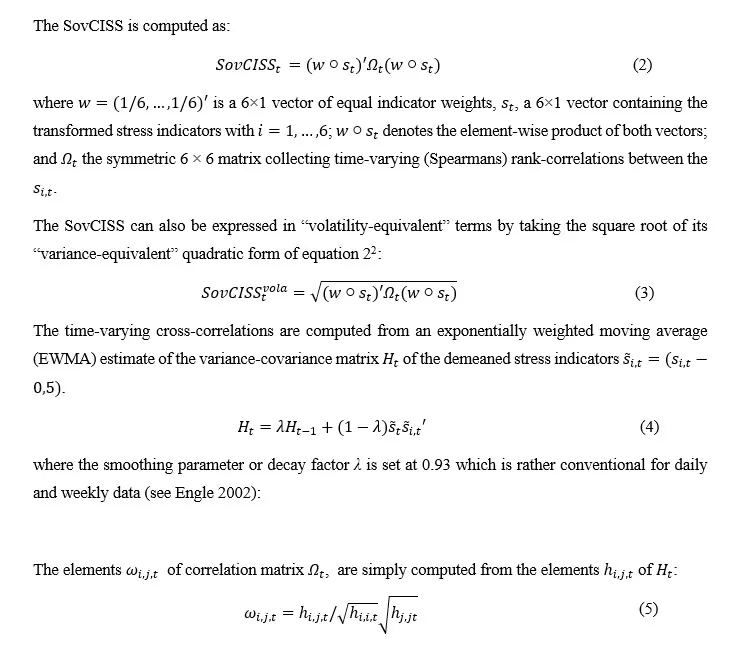

The methodology followed is that developed by Garcia-de-Andoain & Kremer (2018). According to this, constructing the SovCISS indicator involves three stages: data selection, their transformation, and aggregation[1].

Data Selection

SovCISS consists of three main groups of indicators aimed at capturing the specific symptoms of a distressed market:

the spread between the yield on Romanian government bonds and the EUR interest rate swap reflects credit risk;

volatility in government bond yields, indicating the market’s fragility and uncertainty, is measured by the daily variation in yields;

the bid-ask spread represents the liquidity conditions in the government bond market.

Indicators are calculated for the yields of Romanian government bonds with maturities of 3 and 10 years and the euro interest rate swap rate for 3-year and 10-year contracts, data being expressed as weekly averages and sourced from NBR’s database (National Bank of Romania) and investing.

Transformation

Aggregation

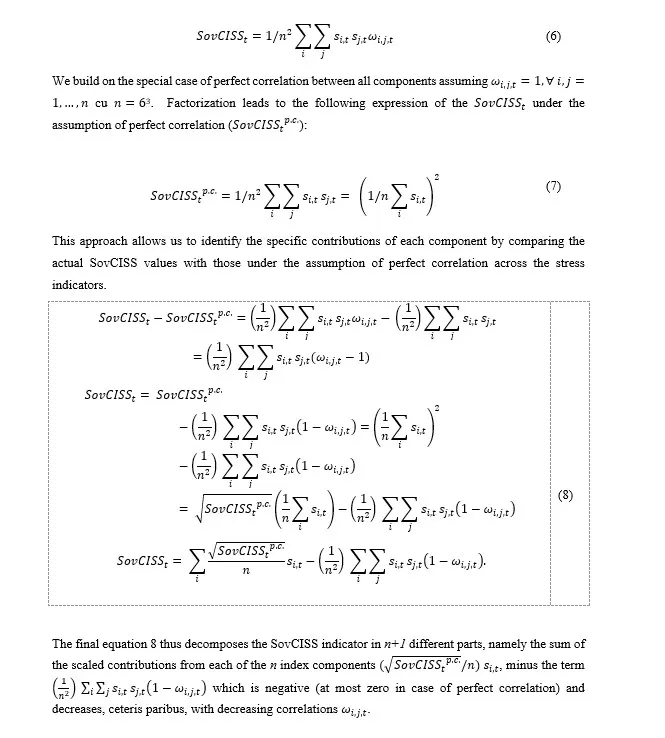

Index Decomposition

As highlighted by Andoain and Kremer (2018), it is often valuable to determine the contribution of each component to specific developments in the SovCISS. However, decomposing the SovCISS into the individual contributions of credit spreads, yield volatility, or bid-ask spreads presents significant challenges. This complexity arises from the nonlinear aggregation scheme used and the lack of identified causality in the contemporaneous correlations between index components. To address the issue of identifying these contributions, we separate the overall effect of rank correlations as a distinct factor. Consequently, we reformulate equation 2 as a double summation, allowing for a clearer breakdown of the components’ influence.

Results

To calculate the SovCISS indicator for Romania, I used weekly data covering the period from April 2015 to August 2024. For comparison, I retrieved pre-calculated SovCISS indicators for the Euro area and the Central European countries (CE3: Czech Republic, Hungary, and Poland) from the ECB’s database, spanning the period from January 2007 to March 2024 (this being the last available observation).

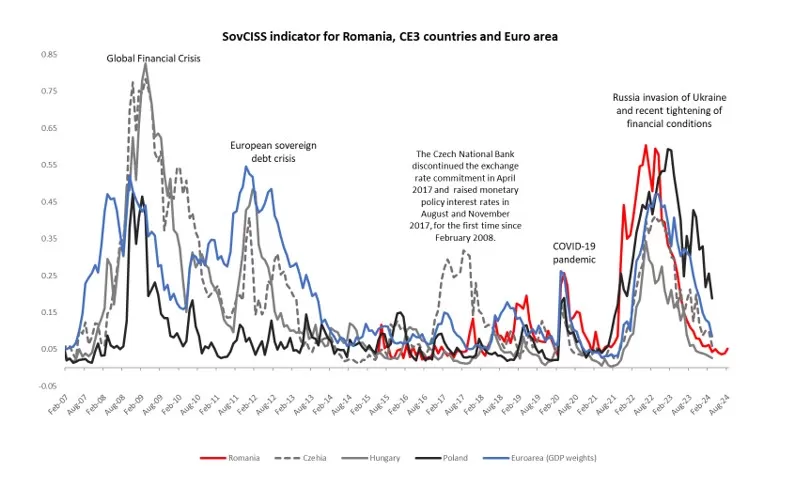

Figure 1 presents the SovCISS indicator for Romania’s government bond market, alongside SovCISS indices for the Euro area and CE3 countries, illustrating a strong correlation between Romania’s bond market and these regions. Additionally, the indicator effectively captures periods of financial stress in these markets. For instance, in the Euro area and CE3, the SovCISS highlights the global financial crisis (2007-2009), the sovereign debt crisis (2011-2012), the COVID-19 pandemic crisis (2020), and the recent tightening of financial conditions, indirectly amplified by Russia’s invasion of Ukraine in February 2022. Moreover, the SovCISS indicator for the Czech Republic effectively captures the increased tensions in the sovereign bond market in 2017, likely due to the Czech National Bank’s decision in April 2017 to discontinue the exchange rate commitment, which had been in place from 2013 to 2017 after monetary policy rates were lowered to “technical zero” in November 2012. This decision was followed by monetary policy rate hikes in August and November 2017, marking the first changes in interest rates since 2012 and the first increases since February 2008.

Figure 1: The SovCISS for Romania, the Euro area, and CE3 countries

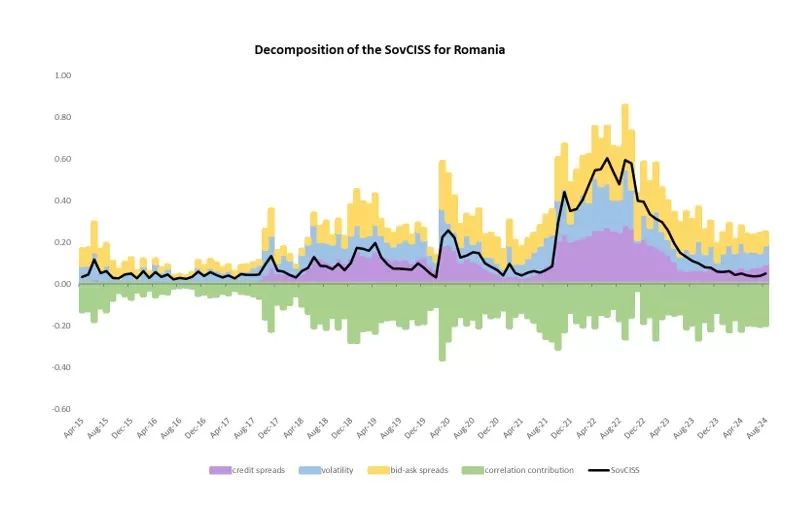

Figure 2 shows the decomposition of the SovCISS for Romania. The contributions from bid-ask spreads, credit spreads, and volatility are computed as averages from both short- and long-maturity bonds. Typically, the aggregate contribution from imperfect correlations between these components is significant, indicating relatively weak correlations between credit spreads, bid-ask spreads, and bond volatility under normal circumstances. However, during the period between 2015 and 2017, reduced volatility was observed, during which the SovCISS and its perfect-correlation counterpart aligned closely, essentially coinciding. Figure 2 also reveals that the factors contributed relatively uniformly to the SovCISS value, with an increased contribution from the credit spread, followed by the bid-ask spread, particularly in the more recent period of 2021-2023, most probably against the backdrop of global monetary policy tightening cycles led by central banks, aimed at curbing inflation that reached historic highs in many developed economies during the post-pandemic period, and the comparatively sharper cumulative increase in representative interest rates by the National Bank of Romania (NBR) relative to the ECB within this inflationary context.

Figure 2: Decomposition of the SovCISS for Romania

Concluding Remarks

The analysis reveals that the SovCISS indicator serves as an effective tool for capturing periods of heightened tensions in the government bond market, positioning it as a valuable instrument for the early identification of risks that may have spillover potential.

In developing this index for Romania and assessing its dynamics, it became evident that there is a significant correlation between Romania’s government bond market and those of the Euro area and Central European countries (CE3: Czech Republic, Hungary, and Poland). This correlation can offer both advantages and challenges. On the one hand, it suggests Romania’s ongoing economic and financial convergence with the Euro area, while, on the other hand, it highlights Romania’s heightened exposure to external financial shocks, particularly those affecting Euro area markets.

The decomposition of SovCISS further demonstrates a tendency for increased correlation between the index’s components during periods of heightened bond market stress, whereas lower correlations are observed during more stable periods. Moreover, the decomposition reveals that credit risk, volatility, and bid-ask spreads contributed relatively uniformly to the SovCISS evolution, with a marked increase in the contribution of the credit spread, followed by the bid-ask spread, particularly in the more recent period of 2021-2023. This development aligns with the more pronounced increases in benchmark interest rates enacted by the National Bank of Romania (NBR) relative to the European Central Bank (ECB), in response to the recent inflationary environment.

In conclusion, the SovCISS is an important indicator for assessing the conditions in the government bond market, focusing on three key factors: credit risk, volatility, and liquidity across short- and long-maturity instruments (3-year and 10-year bonds). The indicator offers a comprehensive perspective on the state of the market, making it essential for monitoring financial stability and early risk detection.

References

Baldwin, R., & Giavazzi, F. (2015). The Eurozone Crisis: A Consensus View of the Causes and a Few Possible Solutions. AEA Papers and Proceedings.

Bongaerts, D., De Jong, F., & Driessen, J. (2011). Sovereign Bond Spreads: A New Approach to the Euro Area Sovereign Debt Crisis. Journal of Financial Economics, 102(3), 491-513.

Finance Research Letters. (2023). Measuring sovereign bond fragmentation in the Eurozone. Finance Research Letters, 51, 103354. https://doi.org/10.1016/j.frl.2023.103354

Fleming, M. J., & Remolona, E. (2002). Price Formation and Liquidity in the U.S. Treasury Market: The Response to Public Information. The Journal of Finance, 54(5), 1901-1915.

Garcia-de-Andoain, C., & Kremer, M. (2018). Beyond spreads: measuring sovereign market stress in the euro area. Working Paper Series 2185, European Central Bank.

Gómez-Puig, M., Pieterse-Bloem, M., & Sosvilla-Rivero, S. (2023). Dynamic connectedness between credit and liquidity risks in euro area sovereign debt markets. Journal of Multinational Financial Management, 68, 100800. https://doi.org/10.1016/j.mulfin.2023.100800

Greenwood-Nimmo, M., Nguyen, V. H., & Shin, Y. (2023). What is mine is yours: Sovereign risk transmission during the European debt crisis. Journal of Financial Stability, 65, 101103. https://doi.org/10.1016/j.jfs.2023.101103

Hollo, D., Kremer, M., & Lo Duca, M. (2012). CISS – a composite indicator of systemic stress in the financial system. ECB Working Paper No. 1426, March.

Laeven, L., & Valencia, F. (2018). Systemic Banking Crises Revisited. International Monetary Fund.

Longstaff, F. A., Pan, J., Pedersen, L. H., & Singleton, K. J. (2011). How Sovereign Is Sovereign Credit Risk? The American Economic Journal: Macroeconomics, 3(2), 75-103.

Romo, J., & Tejada, J. (2020). The Sovereign-Bank Nexus: A Review of the Evidence. Journal of Financial Stability.

Skouralis, A. (2023). The Role of Systemic Risk Spillovers in the Transmission of Euro Area Monetary Policy. Open Economies Review, 34(4), 1079-1106.

[2] The difference between both variants of the SovCISS is analogous to the difference between a variance and a standard deviation (or volatility) as a statistical measure of dispersion.

[3]This assumption implies that the matrix becomes an all-ones matrix (with all elements being equal to one) for all t.