University of Zagreb, Faculty of Economics and Business, Zagreb, Croatia

Volume 2026,

Article ID 317082,

Journal of Eastern Europe Research in Business and Economics,

9 pages,

DOI: https://doi.org/10.5171/2026.317082

Received date: 12 December 2025; Accepted date: 24 February 2026; Published date: 25 March 2026

Cite this Article as:

Ivana BARIŠIĆ (2026)," Contextual Determinants of Internal Audi Engagement in Sustainability Practices: Insights from a Semi-Systematic Literature Review", Journal of Eastern Europe Research in Business and Economics Vol. 2026 (2026), Article ID 317082, https://doi.org/10.5171/2026.317082

This paper aims to analyse recent research regarding the factors related to internal audit engagement in sustainability reporting. Internal audit is becoming an indispensable partner in ensuring the reliability of sustainability information. However, its actual involvement varies considerably across organisations, prompting a need to understand better the contextual factors that influence its role. Research on the involvement of internal audit in sustainability, both in assurance engagements and in an advisory capacity has been increasing, but it remains diverse in terms of methods and research focus. For the purposes of further examining the topic within this study, a semi-systematic literature review was conducted, covering publications indexed in Scopus in the period from 2017 to 2025 and combined with a thematic analysis. The analysis findings indicate the existence of various factors related to the involvement of internal audits in sustainability processes and sustainability reporting. They are related to relationships with key stakeholders, as well as those related to the internal audit function itself, such as a risk-based approach to internal audit, characteristics like size and effectiveness, and the use of information technology in internal audit. The identified themes indicate that the involvement of internal audit in sustainability processes must be viewed multidimensionally to consider factors from different perspectives that influence the role of internal audit in sustainability processes while also enhancing the impact of its work in this context.

Modern business is entering a new phase of development: after decades of focusing on digitalisation and technological efficiency within the framework of Industry 4.0, the need to redefine the purpose of business through the lens of sustainability and social responsibility is becoming increasingly apparent, representing the fundamental idea of Industry 5.0. Due to the specific responsibilities of internal audit, which include providing engagements that express assurance on the effectiveness of internal controls and risk management, as well as advisory activities, internal audit has insight into all aspects of a company’s business. Therefore, involvement in the area of achieving business sustainability is logical. Environmental, social, and corporate governance (ESG) encompasses criteria that determine the sustainability, responsibility, and ethics of business. Increasingly pronounced regulatory and social pressures require effective management of related risks. To ensure the accuracy of reporting and compliance with regulations, it is essential to establish effective internal controls, with internal audits playing a crucial role in assessing their adequacy (IIA, 2021). Users of sustainability information value their quality, and it is the internal audit function that can influence the increase in credibility of such information and increase its usefulness for business decision-making.

Internal audit, as a relatively young branch of the audit profession (Parker & Johnson, 2017), has evolved from a relatively passive role focused on internal controls to a requirement to take on an “active role as a builder” (Lenz & Hoos, 2023), by contributing to management and supervisory structures in the context of implementing a company’s sustainable business strategy. Internal audit, thanks to its independence and broad perspective, plays an important role in connecting other internal and external assurance providers, especially in the context of more effective contributions to achieving sustainable business (ECIIA, 2023). In academic discussions, the emphasis is on redefining the role of internal audit so that it is not limited only to monitoring, but also acts as an active participant in the development and strengthening of the corporate governance system. The internal audit function is expected to be more involved in the areas of sustainability, create value for stakeholders, clearly define its professional role, contribute to business objectives, and focus on the application of technology (Lenz & Jeppesen, 2022). Recent changes in the legislative framework, particularly at the European Union level, with the adoption of Directive 2022/2464 on corporate sustainability reporting, extend the obligation to report on sustainability to a larger number of companies than previously required by law. According to estimates by the European Commission, around 49,000 companies will be covered by Directive EU 2022/2464 (CSRD), representing approximately 75% of the total revenue of all companies in the European Union (ECIIA, 2023). In such a context, there is a growing need for effective internal control and a strengthening of the role of internal audit in assessing the compliance and reliability of published information. Although sustainability was among the less relevant risks in 2020, according to the global IIA report (2021), recent research indicates an apparent shift in focus. According to ECIIA (2025), the various dimensions of sustainability encompassed in the ESG acronym are increasingly classified among the five key risks for internal audit, with significantly greater involvement of the audit function in this area expected in the coming years.

Although the role of internal audit in the field of sustainability and ESG is increasingly emphasized in professional guidelines and positions of relevant professional associations (IIA, 2021.; ECIIA, 2023), scientific literature on this topic is still in development. Empirical insights into the actual practice and impact of the internal audit function are limited (Hazaea et al., 2022). One of the first papers to link sustainability, assurance, and the role of internal audit is a 2011 paper by Ridley et al. (2011), which warns of the need to include internal audit in this context. Additionally, a recent review of the literature highlights that the function of internal audit is increasingly recognized as a key factor in achieving sustainability. This increased interest among researchers is attributed to new regulatory requirements and policies introduced in recent years (Hazaea et al., 2023). Research on internal audit engagement in sustainability, whether through assurance engagements or advisory activities, is growing (DeSimone et al., 2020); however, it remains methodologically and thematically diverse. There is a need for further research into the role of internal audit, as well as the various factors that significantly influence its role in sustainability. This research responds to calls for future research (Hazaea et al., 2022; Al-Qadasi et al., 2024; Hazaea et al., 2025) with the following research question: What are the relevant factors or drivers related to internal audit involvement in sustainability practices, and what is the nature of their influence?

The remainder of this paper is structured as follows. Section 2 outlines the methodology employed to analyse recent research, intending to address the research question. Section 3 presents the findings of a thematic analysis conducted to identify themes or factors associated with the involvement of the internal audit function in sustainability practices. The final section provides a discussion and conclusion of the paper.

Methodology

Given the evolving nature of internal audit’s role in sustainability and ESG reporting, this study adopts a semi-systematic literature review approach, as proposed by Snyder (2019), combined with thematic analysis, as proposed by Braun and Clarke (2006). A semi-systematic literature review approach is suitable for research topics that have been addressed from multiple perspectives within a broad discipline, where consistent conceptual frameworks and standardised methodologies are still developing and help detect themes. The scope of the research focused on the publication period from 2017 to 2025, utilising data sources (open-access articles, book chapters, and conference proceedings) indexed in Scopus. The year 2017 was chosen as the starting point, following the conclusions of the literature review conducted by Hazaea et al. (2022) on the period from 1993 to 2021, which found only seven papers related to the internal audit role in sustainability and only seven papers from the period of 2006 to 2015. However, those papers explored internal auditors’ perceptions regarding their role in sustainability. To further investigate the scope of the research, search terms included the following terms: ‘internal audit’ and ‘sustainabl*, similar to previous reviews (e.g. Hazaea et al., 2022) but with a different objective and screening focus. The search resulted in 142 documents (filtered by subject area that included social sciences, business, management and accounting, economics and related subject areas), which were then reduced to only those that related to the subject matter topic. Data sources were inspected to include only those sources that satisfied the following inclusion criteria: literature reviews and empirical research about the contextual factors related to internal audit involvement in sustainability practices. Two additional relevant articles were identified using snowballing techniques, one through Scopus’ related article suggestions and one through backward reference tracking and in total 24 papers were analysed.

Once the subject papers for the final data analysis were defined, a thematic analysis was conducted following the six-step approach defined by Braun & Clarke (2006):

1) Familiarisation with the data, which involved repeated reading and active engagement with the selected literature, allowing for the identification of initial ideas and patterns relevant to internal audit’s engagement in sustainability practices.

2) Initial codes were generated by identifying the specific contextual factors examined in the selected studies that influenced internal audit’s involvement in sustainability practices, which served as a basis for developing broader themes in the following phase.

3) In the third phase (searching for themes), all the coded factors were grouped into thematic categories in order to create a meaningful structure for the literature review and to draw conclusions about the key contextual factors that shape the role of internal audit function in sustainability practices.

4) In the fourth phase, the initial themes were reviewed and refined.

5) The fifth phase involved defining and naming themes. Clear definitions were developed for each theme, forming the basis for structured interpretation in the discussion section.

6) In the sixth phase, themes were used to construct an analytical narrative that connects the findings to the research aim and highlights how contextual factors shape internal audit engagement in sustainability.

While the author’s awareness informed the analysis of theoretical debates in the field, the coding and theme development were grounded in the actual content of the literature reviewed.

Analysis of recent literature regarding factors related to internal audit involvement in sustainability practices

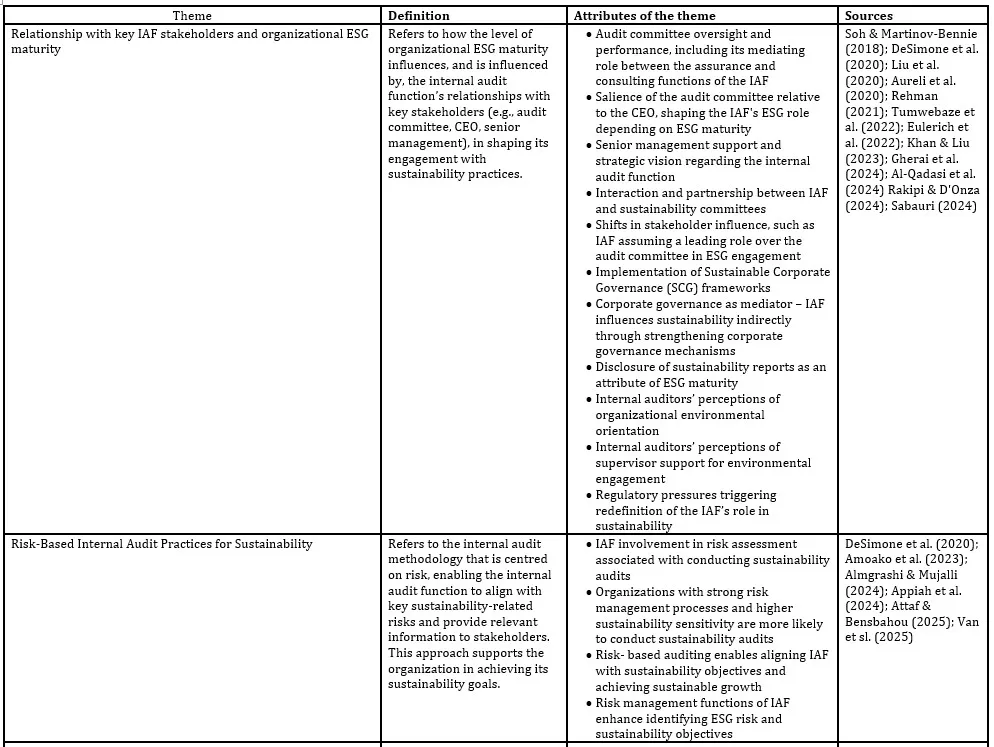

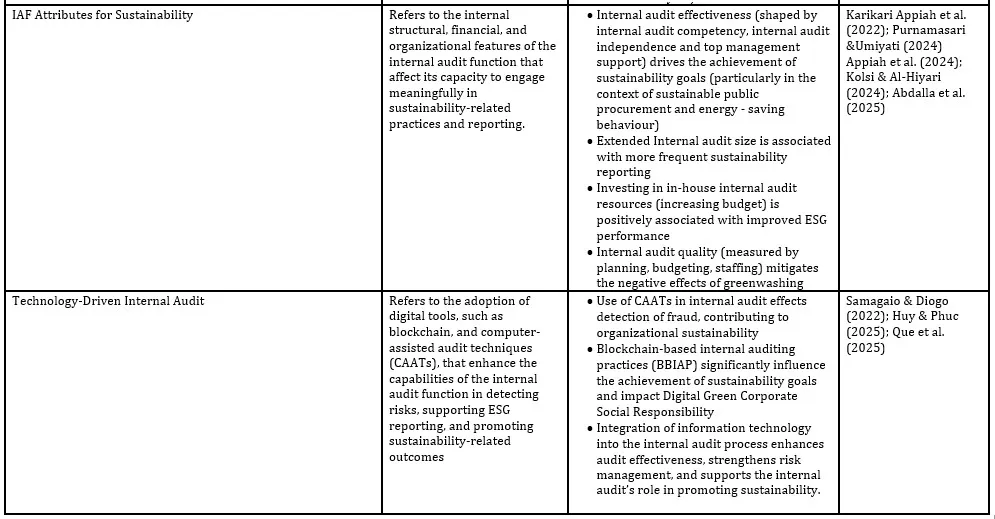

The thematic analysis conducted in this study followed an inductive, data-driven approach, as described by Braun and Clarke (2006), with an interpretative focus on how internal audit engagement in sustainability is framed across different studies. Themes were not based on a pre-existing coding framework or predefined theoretical categories but rather emerged through systematic reading and interpretation of the selected literature. As described in table 1., four themes were identified as a result of a prescribed process; Relationship with key IAF (internal audit function) stakeholders and organizational ESG maturity, Risk-Based Internal Audit Practices for Sustainability, IAF Attributes for Sustainability and Technology-Driven Internal Audit.

The research reviewed encompasses public sector organisations (seven papers), listed companies, financial services companies, manufacturing companies, and other sectors. The studies were conducted in diverse geographical contexts, including countries such as Australia, China, Italy, Uganda, Pakistan, Vietnam, Portugal, Indonesia, Romania, Saudi Arabia, Yemen, and Germany.

This diversity further enhances the value of the findings, as it provides insight into different perspectives on the role of internal audit in sustainability practice while also considering specific institutional contexts. In some European countries, for example, research has focused on the factors driving internal audit engagement in sustainability reporting driven by regulatory changes. In other contexts, the emphasis is on the characteristics of internal audit that contribute to its greater usefulness in sustainable management and the achievement of ESG objectives.

Table 1. Identified Themes and Attributes Related to Factors Associated with Internal Audit Involvement in Sustainability Practices

Source: Author, Abbreviations: AC – audit committee; CEO – chief executive officer; IAF – internal audit function

The following section of the paper discusses the themes identified through the analysis of the studies presented in Table 1.

Discussion and Conclusion

As presented in Table 1 of the previous section, the results of the analysed papers within the theme Relationship with Key IAF Stakeholders and Organizational ESG Maturity indicate that the level of involvement and type of engagement of the internal audit function in the area of sustainability depends on the expectations of its key stakeholders, as well as on the level of ESG maturity of the organisation in which it operates. Key prerequisites for effective engagement of the IAF include support from senior management and a recognised need to ensure the credibility and accuracy of information related to sustainability practices. Additionally, relationships with relevant committees, such as the audit committee or the sustainability committee, also influence the role of the IAF. The literature has already recognised that support from key stakeholders is a crucial factor in the performance of internal audits (Eulerich et al. 2017), and the findings indicate that this connection remains equally important in the context of sustainability.

Regarding the second theme, Risk-Based Internal Audit Practices for Sustainability, the research analysis found that the application of this internal audit paradigm is considered important for investigating the contribution of the internal audit function to achieving sustainability goals. An internal audit using a risk-based approach, focusing on the risk management process, can help companies better manage ESG risks by assuring the effectiveness of internal controls and overall sustainability risk management. Although some analysed papers have not established a direct connection between RBIA and sustainability, this paradigm is linked to achieving sustainable growth. Various factors influence the achievement of sustainability goals, and internal audit plays a key role in improving these opportunities. The risk-based approach is a paradigm of modern internal audit, which focuses on activities important to the company. First, it concentrates on goals and threats to their achievement, i.e., risks, and only then on controls designed to mitigate these threats. Information derived from the risk-based internal audit process has greater value for management in the decision-making process.

The analysis also identified specific organisational, structural, and financial characteristics of the internal audit function that affect its capacity to engage meaningfully in sustainability-related practices and reporting, which describes the third identified theme, IAF Attributes for Sustainability. Various factors influence the involvement of internal audits in sustainability processes and their greater contribution in this sense. Recent regulatory changes related to the obligation to report on sustainability, particularly in the EU, will impact the increasing demands of internal audit stakeholders for conducting assurance engagements and advisory activities. In this sense, according to the research findings within this theme, the size of the department and investments, in the form of an increase in the internal audit budget, are associated with better ESG performance among companies in which internal audit is involved in sustainability-related processes. Also important are the effectiveness and quality of internal audit, which significantly affect the degree of achievement of internal audit objectives, particularly in the context of achieving sustainable business objectives, given the involvement of internal audit in these processes. A particular challenge for internal audit teams involved in sustainability-related processes is the knowledge and skills required to understand this issue, which is quite heterogeneous due to the different areas covered by the concept of sustainability. In this sense, the teams will likely need to include specialists from different fields who have expert knowledge and the necessary skills related to environmental and other issues. It is interesting to note that, in the analysed studies, outsourcing of internal audit did not prove to be a significant factor (Soh & Martinov-Bennie, 2018; Kolsi & Al-Hiyari, 2024; Abdalla et al., 2025) regarding ESG performance or sustainability reporting. In other words, the involvement of internal audits in sustainability processes or the improvement in ESG performance did not depend on the extent of outsourcing but rather on the size of internal audit departments and investments in departments operating within companies.

Recent research on the contribution of the internal audit function to achieving sustainable business operations includes research on the impact of using digital technologies in internal audit in this context, identified within the Technology-Driven Internal Audit theme. The assumption of expanded internal audit roles has been significantly influenced by the impact of digital technologies, which enable greater efficiency and effectiveness in all aspects of the function’s operations. The internal audit function has a unique opportunity to expand its role, leveraging technological capabilities developed in the digital era, and can actively contribute to the company’s strategic direction towards long-term, sustainable business operations. In this sense, adapting to new stakeholder demands is a necessary condition for the internal audit function to remain relevant in the context of key internal corporate governance mechanisms. Internal audit plays a key role in ensuring compliance with ESG standards and improving sustainability risk management. The use of advanced technologies enables precise data analysis, risk identification and anomaly detection, which improves the efficiency of audit activities and supports better decision-making. Additionally, according to practice, internal audit is increasingly utilising data analytics to more effectively collect and analyse ESG information, thereby contributing to the accuracy of assessing ESG risks and their impacts (KPMG, 2023).

According to the global Institute of Internal Auditors (IIA, 2021), internal audit plays a crucial role in the field of ESG reporting, not only by providing objective assurance related to internal controls over sustainability reporting, but also through advisory activities aimed at strengthening ESG governance. Such an approach confirms the need for internal audit to be systematically involved in the processes of achieving sustainable business goals, thereby contributing to the improvement of the overall corporate governance system in line with its purpose and public interest. This research is subject to certain limitations, as the literature review was based solely on studies sourced from a single academic database. Nevertheless, it offers an interesting overview of the factors that influence the inclusion of the internal audit function in sustainability-related practices, as well as those that influence the increase of its contribution in this context. According to the analysed research, it is evident that the number of studies on this topic has increased over the last two years. This fact makes the results of this research particularly relevant and significant in the context of the research topic, providing a comprehensive overview of current topics and factors that serve as drivers of the internal audit function’s activities in the context of sustainability.

References

Abdalla, A.A.A., Alodat, A.Y., Salleh, Z. and Al Ahdal, W.M. (2025) ‘The effect of audit committee effectiveness, internal audit size and outsourcing on greenhouse gas emissions disclosure’. International Journal of Disclosure and Governance https://doi.org/10.1057/s41310-025-00297-0

Almgrashi, A. and Mujalli, A. (2024) ‘The Influence of Sustainable Risk Management on the Implementation of Risk-Based Internal Auditing’. Sustainability, 16(19), 8455

Al-Qadasi, A. A., Ghaleb, B. A. and Qaderi, S. A. (2024) ‘Unlocking the power of internal audit function (IAF) and corporate social responsibility (CSR): enhancing integrated reporting quality in Malaysian companies’. Managerial Auditing Journal, 40(1), 1–29

Amoako, G. K., Bawuah, J., Asafo-Adjei, E. and Ayimbire, C. (2023) ‘Internal audit functions and sustainability audits: Insights from manufacturing firms’. Cogent Business; Management, 10(1), 2192313-219

Appiah, M. K., Dordaah, J. N., Sam, A., Yeboah, S. A. and Amaning, N. (2024) ‘Modeling the Influence of Internal Audit Efficacy on Energy Saving Behavior: The Role of Sustainability Audit’. Sage Open, 14(2) https://doi.org/10.1177/21582440241257784

Attaf, W. F. and Bensbahou, A. (2025) ‘The Effect of Improving Risk Management as a Mediator Variable in the Relationship between the Modern Approach to Internal Auditing and Competitive Advantage: A Study in Yemeni Islamic Banks’. International Journal of Economics and Financial Issues, 15(2), 163–172

Aureli, S., Del Baldo, M., Lombardi, R. and Nappo, F. (2020) ‘Nonfinancial reporting regulation and challenges in sustainability disclosure and corporate governance practices’. Business Strategy and the Environment, 29(6), 2392–2403

Braun, V. and Clarke, V. (2006) ‘Using thematic analysis in psychology’. Qualitative Research in Psychology, 3(2), 77–101

DeSimone, S., D’Onza, G. and Sarens, G. (2020). ‘ Correlates of internal audit function involvement in sustainability audits’. Journal of Management and Governance, 25(2), 561–591

ECIIA (2023) Position paper: The role of Internal Audit in ESG in industrial and commercial companies. [Online], [Retrieved April 15 2025] https://www.eciia.eu/wp-content/uploads/2023/10/IA-in-ESG-v3.pdf

ECIIA (2025) RISK IN FOCUS:Hot topics for internal auditors. [Online], [Retrieved April 15 2025] https://www.eciia.eu/2024/09/risk-in-focus-2025-hot-topics-for-internal-auditors/

Eulerich, M., Bonrath, A. and Lopez Kasper, V. I. (2022) ‘Internal auditor’s role in ESG disclosure and assurance: An analysis of practical insights’. Corporate Ownership and Control, 20(1), 78–86.

Eulerich, M., Henseler, J. and Köhler, A. G. (2017) ‘The internal audit dilemma – the impact of executive directors versus audit committees on internal auditing work’. Managerial Auditing Journal, 32(9), 854–878.

Gherai, D. S., Sabău Popa, D. C., Rus, L., Matica, D. E. and Mare, C. (2024) ‘The Impact of Romanian Internal Auditors in ESG Reporting and Sustainable Development Goals’. Sustainability, 16(19), 8680. https://doi.org/10.3390/su16198680

Hazaea, S., Al-Matari, E., Khatib, S., Albitar, K.and Zhu, J. (2023) ‘Internal Auditing in the Arab World: A Systematic Literature Review and Directions for Future Research’. SAGE Open. 13 (4). https://doi.org/10.1177/21582440231202332

Hazaea, S. A., Cai, C., Al-Matari, E. M., Al-Bukhrani, M. A. and Chong, H. G. (2025) ‘Mapping the Literature Trends of Internal Auditing in the United States: A Systematic Review and Directions for Future Research’. Sage Open, 15(1). https://doi.org/10.1177/21582440251318071

Hazaea, S. A., Zhu, J., Khatib, S. F. A., Bazhair, A. H. and Elamer, A. A. (2022) ‘Sustainability assurance practices: a systematic review and future research agenda. Environmental Science and Pollution Research, 29(4), 4843–4864.

Huy, P. Q., & Phuc, V. K. (2025) Unveiling how blockchain-based internal auditing practices impact SDG 8 achievement? Mediating role of digital green corporate social responsibility’. Research in Economics, 79(3), 101057. https://doi.org/10.1016/j.rie.2025.101057

IIA (2021) White paper – Internal Audit’s Role in ESG Reporting. [Online], [Retrieved April 20 2025], https://www.theiia.org/globalassets/documents/communications/2021/june/white-paper-internal-audits-role-in-esg-reporting.pdf

Karikari, A. M., Tettevi, P. K., Amaning, N., Opoku Ware, E. and Kwarteng, C. (2022) ‘Modeling the implications of internal audit effectiveness on value for money and sustainable procurement performance: An application of structural equation modeling’. Cogent Business; Management, 9(1). https://doi.org/10.1080/23311975.2022.2102127

Khan, U. and Liu, W. (2023) ‘The role of internal auditing on corporate governance: its effects of economic and environmental performance’. Environmental Science and Pollution Research, 30(52), 112877–112891.

Kolsi, M. C., & Al-Hiyari, A. (2024) ‘Does internal audit function outsourcing policy matter for environmental, social and governance performance score? Evidence from Bursa Malaysia’. Sustainability Accounting, Management and Policy Journal, 15(6), 1442–1459

KPMG (2023) ESG and Internal Audit: Insights and guidance to make impact as Internal Audit. [Online], [Retrieved April 22 2025], https://assets.kpmg.com/content/dam/kpmg/nl/pdf/2023/services/esg-and-internal-audit.pdf

Lenz, R. and Hoos, F. (2023) ‘The Future Role of The Internal Audit Function: Assure. Build. Consult’. EDPACS, 67(3), 39–52

Lenz, R. and Jeppesen, K. K. (2022). ‘The Future of Internal Auditing: Gardener of Governance’. EDPACS, 66(5) 1-21.

Liu, X., Li, W. and Parsons, K. (2020) ‘Exploring the antecedents of internal auditors’ voice in environmental issues: Implications from China. International Journal of Auditing, 24(3), 396–411.

Parker, S. and Johnson, L. A. (2017) The Development of Internal Auditing as a Profession in the U.S. During the Twentieth Century’. Accounting Historians Journal, 44(2), 47–67

Purnamasari, P. and Umiyati, I. (2024) ‘Greenwashing and financial performance of firms: the moderating role of internal audit quality and digital technologies’. Cogent Business; Management, 11(1). https://doi.org/10.1080/23311975.2024.2404236

Que, N. T., Duyen, N. T. H., Thuy, T. T. T. and Bac, D. T. (2025) ‘The relationship between organizational culture, information technology, and the effectiveness of internal auditing: A study in Vietnam’. Edelweiss Applied Science and Technology, 9(3), 2891–2901

Rakipi, R. and D’Onza, G. (2023) ‘The involvement of internal audit in environmental, social, and governance practices and risks: Stakeholders’ salience and insights from audit committees and chief executive officers’. International Journal of Auditing, 28(3), 522–535

Rehman, A. (2021) ‘Can Sustainable Corporate Governance Enhance Internal Audit Function? Evidence from Omani Public Listed Companies’. Journal of Risk and Financial Management, 14(11), 537. https://doi.org/10.3390/jrfm14110537

Ridley, J., D’Silva, K., & Szombathelyi, M. (2011) ‘Sustainability assurance and internal auditing in emerging markets’. Corporate Governance: The International Journal of Business in Society, 11(4), 475–488.

Sabauri, L. (2024) ‘Internal Audit’s Role in Supporting Sustainability Reporting’. International Journal of Sustainable Development and Planning, 19(5), 1981–1988

Samagaio, A. and Diogo, T. A. (2022) ‘Effect of Computer Assisted Audit Tools on Corporate Sustainability’. Sustainability, 14(2), 705. https://doi.org/10.3390/su14020705

Snyder, H. (2019) ‘Literature review as a research methodology: An overview and guidelines’. Journal of Business Research (104), 333–339

Soh, D. S. B. and Martinov‐Bennie, N. (2018) ‘Factors associated with internal audit’s involvement in environmental and social assurance and consulting’. International Journal of Auditing, 22(3), 404–421.

Tumwebaze, Z., Bananuka, J., Kaawaase, T. K., Bonareri, C. T. and Mutesasira, F. (2021) ‘Audit committee effectiveness, internal audit function and sustainability reporting practices’. Asian Journal of Accounting Research, 7(2), 163–181

Van, H. V., Abu Afifa, M. and Bui, D. V. (2025) ‘How risk management functions of internal audits enhance green process innovation toward sustainability: the role of green transformational leadership and green knowledge sharing’. Meditari Accountancy Research. ahead-of-print No. ahead-of-print. https://doi.org/10.1108/medar-11-2024-2710