1doctor of economic sciences, associate professor,

University of European Political and Economic Studies “Constantin Stere”,

Faculty of Economics, Institute of Mother and Child, Chisinau, Republic of Moldova

2doctor of medical sciences, associate professor,

Institute of Mother and Child, Chisinau, Republic of Moldova

Volume 2022,

Article ID 676661,

Journal of e-health Management,

9 pages,

DOI: 10.5171/2022.676661

Received date: 21 October 2021; Accepted date: 3 February 2022; Published date: 22 April 2022

Academic Editor: Sanja Franc

Cite this Article as:

Cristina COPACEANU and Sergiu GLADUN (2022)," Internal Public Financial Control in the Republican Medical Institutions from the Republic of Moldova", Journal of e-health Management, Vol. 2022 (2022), Article ID 676661, DOI:10.5171/2022.676661

In the conditions of the COVID-19 pandemic, the health system in the Republic of Moldova requires increased attention and involvement, because the pressure of the pandemic, economic and political crisis directly affect its proper functioning. The sustainability of the health system is a major challenge for the government, in the context of the pandemic crisis, as well as the emergence of emerging risks specific to the field. Thus, the research of this aspect is gaining momentum, and the internal public financial control in the health system in general and in the republican medical institutions in particular requires a new approach. In this regard, the results of the paper are appreciated by strengthening the audit and internal control components in the health system, especially in the republican medical institutions, as optimal tools for the management and development of the institution in crisis and pandemic shocks. Thus, the authorss concluded that in the current conditions, the effective governance of the medical institution can be improved by the effective and actual implementation of the internal managerial control system and the internal audit function.

Keywords: internal audit, medical audit, internal managerial control, pandemic and economic crisis

Introduction

The health system has been and will always be the most sensitive system in a state, because without a healthy population, without a well-organized health system, the development and existance of the country will not be possible. In conditions of crisis, pandemic shocks, the good governance of medical institutions and of the system as a whole is becoming more and more evident, so in this article the authors will address the current situation but also the evolution of internal managerial control and internal audit at the level of the health system but also at the level of public medical institutions in the Republic of Moldova.

The good governance of medical institutions depends on the level of implementation and development of internal managerial control but also of internal audit. The present interest of the study derives from the fact that the governance of the health system, but also of the medical institutions, requires new efficient and prompt governance tools. Thus, we are motivated to research both methodologically and applicatively how the health system survives in general and especially in crisis situations and how to manage the existing internal managerial control and internal audit in crisis situations or pandemic shocks.

Therefore, we will further review the evolution of internal audit and internal managerial control in the health system of the Republic of Moldova, based on the case of the Institute of Mother and Child.

Literature Review

In the Consolidated Annual Report, prepared by the Ministry of Finance on Public Internal Financial Control for 2020 [Consolidated annual report, 2020], the information on internal managerial control (hereinafter IMC) and internal audit was analyzed and consolidated, thus, the COVID-19 pandemic left its mark on both the internal audit function, as well as on the internal managerial control, both being exposed to the emerging risks imposed by the pandemic.

The research provides a detailed analysis of the situation regarding the internal management control system and the function of the internal audit in the health system, with the exemplification of the practical aspects based on the Institute of Mother and Child, a republican institution. Being a tertiary level institution, with a scientific-curative profile, the mission of the Institute of Mother and Child is to contribute to improving and maintaining the health of mothers and children throughout the Republic, providing quality healthcare in a pleasant and safe environment, the best professionals in the field, application of international practices and modern technologies, patients’ trust representing an indicator of the quality of medical service. In 2020, the Institution has a potential of 2 294 workers, including 30 scientific collaborators, 465 doctors, 172 resident doctors, 648 nurses, 122 midwives, 545 lower staff, 266 auxiliary staff [Mother and Child Institute, 2021].

Therefore, based on concrete data, we will highlight the problematic aspects, as well as the progress made by the largest medical institution in the Republic of Moldova on the implementation and development of the internal management control system and the function of the internal audit.

Research Methodology

As sources of information, the authors used the statistical data of the Ministry of Finance, the Ministry of Health, the Institute of Mother and Child, etc. In the paper, the authors used the classical methods of analysis and synthesis, induction and deduction, history and logic, comparative and systemic analysis, as well as a contemporary approach to COVID-19 pandemic trends.

Thus, through a theoretical and practical approach, reviewing the literature, identifying, analyzing and systematizing news, the authors alert the society about the shortcomings of the internal management control system and the function of the internal audit and plans recommendations to eliminate divergences.

Analysis and Interpretation of Results

In order to improve the rational administration and control of public finances in the Republic of Moldova, in 2005, the EU Moldova Action Plan was approved [EU-Moldova Action Plan, 2005]. The need to implement public internal financial control (hereinafter CFPI) in the Republic of Moldova derives from point 42 of the Action Plan, through which the Republic of Moldova has commited itself to implementing the public internal financial control system at national level in accordance with internationally recognized methodologies and standards, as well as with EU best practices. The Ministry of Finance is responsible for the implementation of the CFPI.

In 2006, the Concept of the internal control and internal audit system in the public sector was approved [GD no.1143/2006]. In 2008, the Strategy for the development of public internal financial control was approved, which aims at the sustainable development of the CFPI system [GD no.74, 2008]. We draw attention to the fact that the development of public internal financial control was regulated by the development programs approved by GD (Government Decree) no.1041 of 10 December 2013 and GD no.124 of 02 February 2018 [OMH no.519/2008; OMF no.4/2019].

In 2010, the Law on public internal financial control was approved with the aim of strengthening managerial responsibility for the optimal management of resources according to the objectives of the public entity, based on the principles of good governance, by implementing the system of financial management and control and internal audit activity in the public sector [GD no.1041/2013]. According to the provisions of Law 229, the internal public financial control comprises three basic pillars:

internal managerial control (hereinafter IMC);

internal audit;

centralized coordination and harmonization (responsible being Ministry of Finance).

Currently, the implementation of the CFPI at the level of the health system is at a very low level, especially the pillar regarding the internal public financial control but also the internal audit. At the level of the central public authority, the Ministry of Health is responsible for the implementation and development of the IMC, the Institutional Management Department. Regarding the internal audit pillar, we mention that within the Ministry is established the internal audit service, which helps the public entity in achieving its objectives through a systematic and methodical approach, assessing and improving the effectiveness of risk management, control and governance processes [GD no.1041/2013].

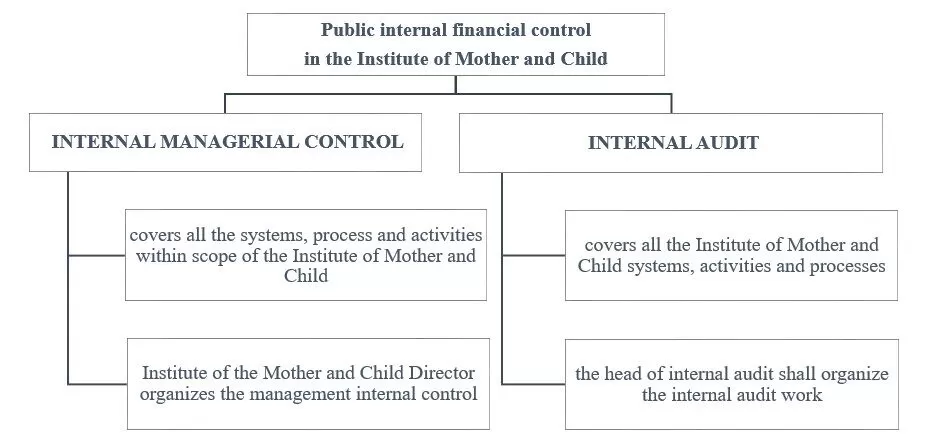

Next, we will address the level of implementation of internal managerial control and internal audit in public medical institutions, based on data from the Institute of Mother and Child. Thus, the system of internal public financial control within the Institute of Mother and Child is organized in two components, reflected in Figure 1.

Figure 1. Organization of the CFPI system within the the Institute of Mother and Child

Source: Compiled by the authors

Next, we will address how the two components of internal public financial control are organized and developed within the Institute of Mother and Child.

The first component of the public internal financial control system within the Institute of Mother and Child is the internal audit. As in all other public institutions in the Republic of Moldova, initially within the Institute of Mother and Child, the emphasis was on the implementation of internal audit and then on internal managerial control, which we consider to be a mistake because the internal audit aims to provide consulting and providing objective assurance on the effectiveness of the internal management control system, providing recommendations for its improvement and contributing to improving the activity of the public entity [GD no.1041/2013].

The first trends in the implementation of internal audit in the public sector belong to the National Bank of Moldova and the National Social Insurance House, which through projects, with the support of foreign experts, created internal audit units, whose specialists received training and assistance in organizing internal audit activity, according to international standards [Ministry of Finance, Internal Audit Manual, 2009, p.11].

It should be mentioned that according to Article 2 of Law 229/2010, the provisions of the law apply to the central and local public administration authorsities, public institutions, as well as to the autonomous authorsities / institutions which manage the means of the national public budget.

Respectively, the medical institutions fall within the scope of this article, and are therefore obliged to organize the internal audit activity.

In the hospitals of the Republic of Moldova, the internal audit activity started on the basis of the provisions of Decision no.27 of April 30, 2010, on “Regularity audit reports at public medical institutions: the Republican Clinical Hospital, Institute of Cardiology and Republican Clinical Hospital for Children” Emilian Cotaga“ for 2009 ”, Decision of the College of the Ministry of Health no.3/6 of May 20, 2010, as well as based on the order of the Ministry of Health no. 375 of June 03, 2010 regarding the Decision of the Court of Accounts no. 27 of April 30, 2010. Thus, it was decided to implement the public internal audit function in the hospitals of the Republic of Moldova, in order to advise the manager (director) to find solutions to problems, in a different way, through the provisions taken to ensure better control of activities, programs and actions [Copaceanu Cr., 2015]. As a result, the Internal Audit Service was established within the Institute of Mother and Child.

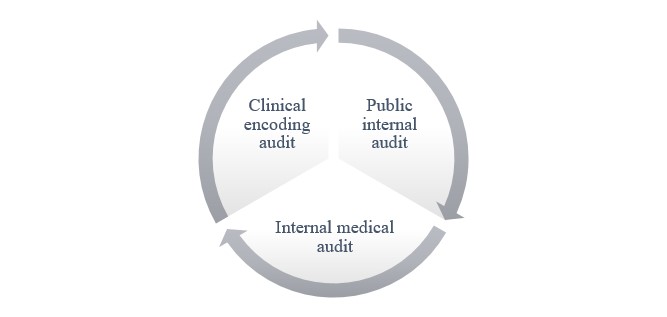

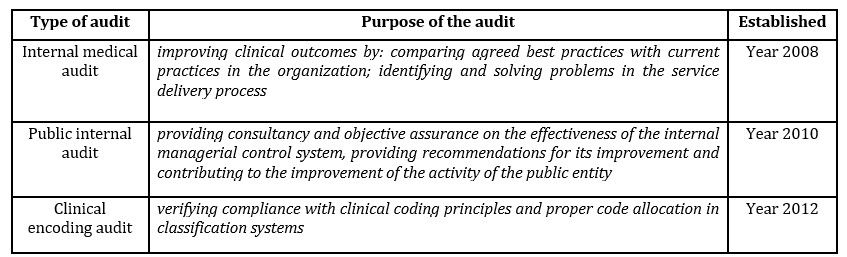

It is necessary to note that the internal medical audit is also implemented in medical institutions, in accordance with the order of the Ministry of Health no.519 of December 29, 2008. According to Annex no.2 to the mentioned order, which approves the Guide to practice on internal medical audit, the medical audit can be defined as the assessment, estimation and contribution to ensuring the continuous improvement of the quality of healthcare provided to patients. The medical audit aims to improve clinical outcomes, by: comparing agreed best practices with the current practices in the organization; identifying and solving problems in the services delivery process. The medical audit measures the performance and takes corrective action when the performance is poor, encourages the health care institutions to provide quality services, without danger [OMH no.519/2008]. In this respect, within the Institute of Mother and Child, the quality management and medical audit service was established.

There is also the third type of audit within the Institute of Mother and Child, namely the clinical coding audit, which is established within the framework of the operations and auditors DRG service, based on the order of the Ministry of Health no. 546 of June 06, 2012 [OMH no.546/2012].

Based on the above, we can present the types of internal audit within the Institute of Mother and Child, shown in Figure 2.

Figure 2. Types of internal audit existing within the Insitute of Mother and Child

Source: Elaborated by the authors

Next, we will address the basic aims of each existing internal audit structure within the Institute of Mother and Child in order to clarify.

Table 1: Reflection on the purposes of the audits within the Institute of Mother and Child

Source: Elaborated by the authors

In our opinion, all these existing subdivisions within the Institute of Mother and Child must be strengthened, by:

replenishment with individuals;

training auditors in vulnerable processes;

valuing the activity of auditors;

highlighting the importance of auditors within the institution.

Strengthening this area is essential to ensure the achievement of objectives and the achievement of the mission of the Institute of Mother and Child; maintenance costs will also be made more efficient. The existence of small structures that are orphan can lead to failure to fulfill the purpose for which they were set up and can generate inefficient activity. In the light of the above, we believe that the work of internal audit in medical institutions, especially in exceptional situations (pandemics, crises, etc.), would visibly increase their contribution and added value. That is why, in our view, crises offer new opportunities to fortify managerial tools such as internal audit.

The second component of the public internal financial control system within the Institute of Mother and Child is the managerial internal control.

The process of implementing internal managerial control (then financial management and control) within the Insitute of Mother and Child started in 2014. The first step in this regard was the creation of the working group on coordination of the implementation of financial management and control system (IMC), by the coordinator’s order no.01-19/261a of November 14, 2014. It should be mentioned that until 2016, no activities were undertaken in this chapter, which is why in 2016, the coordinator’s order No.01 -19 / 261a was updated, dated November 14, 2014 and approved the action plan on the implementation of the MFC system within the Institute of Mother and Child.

The Institute of Mother and Child carried out for the first time the process of self-assessment of the MFC system (IMC), starting with 2016, completing the report on the organization and functioning of the MFC system within the Institute of Mother and Child and the declaration on good governance, based on the provisions ot MF No.49 of April 26, 2012 [OMF no.49/2012].

As a result, by MF order No.4 of January 09, 2019, the MF order No.49 of April 26, 2012, was abrogated, so starting with 2019, the self-assessment, reporting of the internal managerial control system and issuing of the declaration of managerial responsibility within the Institute of Mother and Child took place on the basis of the provisions of that order [OMF no.4/2019].

Therefore, as a result of the annual exercise carried out by public institutions on the self-assessment of the IMC system for the purpose of determining its degree of compliance with the relevamt regulatory framework in the field, the Institute of Mother and Child has self-assessed its IMC system. The results of the self-assessment show that, during the years 2016-2020, the system under assessment is largely in line with the provisions of the National Internal Control Standards in the public sector, and the shortcomings found are to be removed, in order to comply with the rules in force.

Next, we will present the seven compartments of the annual self-assessment report of internal managerial control within the Insitute of Mother and Child [Annual self-assessment report, 2021], prepared for 2020.

The IMC self-assessment process starts with general information, which includes general information on the IMC within the Institute of Mother and Child, such as: budget, number of employees, level of implementation of the action plan, level of achievement of the annual public procurement plan, the number of core processes identified and described, specific training in the field of IMC.

With regard to the first component of the control environment, we mention that it is intended to assess personal and professional integrity, management and employees ethics, leadership style, organizational structure, delegation of powers, human resources policies and practices, as well as employee competence. In the opinion of the internal auditor, the control environment component is partially in line with the requirements of the National Internal Control Standards (hereafter NICS), and therefore improvements are needed, namely: the lack of disciplinary board, regulation on fraud and corruption prevention, the regulation on the continuous professional development of all employees, the Human Resources Management Policy, and the management staff does not have a job description.

The second component of performance and risk management aims to assess whether the Institute of Mother and Child has correctly established its mission, its strategic and operational objectives; whether the action plans include measurable actions and performance indicators for the institution’s activity and organizational subdivisions; whether the institution establishes the risk management strategy, on the basis of which it systematically identifies, records, evaluates, controls, monitors and reports the risks, including the risks of corruption that may affect the achievement of the objectives; whether the identified risks are associated with the objectives. In the opinion of the internal auditor, the performance and risk management component is partially in line with NICS requirements, so improvements are needed because the operational objectives set out in the Annual Action Plans are not set according to the SMART method, and therefore institutional performance cannot be monitored and assessed.

The annual action plans of the Institute of Mother and Child do not include risks associated with the objectives and financial costs. The heads of subdivisions do not fullly realize the obligation and need to implement risk management, as well as the IMC system; respectively the Register of risks per subdivision and the Register of consolidated risks are missing.

Through component three, control activities, policies and procedures are assessed that help to ensure that management directives are enforced and that objectives are met in an economical, effective and efficient manner. In the opinion of the internal auditor, the component of control activities is partially in line with NICS requirements, so improvements are needed because: the control- access system on the territory of the institution is not functional (installed turnstiles do not work, the access of foreigners on the territory of the institution without supporting documents); no internal rules on reporting fraud, irregularities and other infringements are approved; no core processes are identified, cataloged and documented, and those described are not up-to-date; sensitive functions are not identified (list of sensitive functions is missing), and there are no policies for managing sensitive functions.

In the outcome of the evaluation of component four, information and communication, the internal and external information and communication systems, as well as the quantity, quality, periodicity and sources of information within the Institute of Mother and Child were assessed. In the opinion of the internal auditor, the information and communication component is partially in line with the NICS requirements, therefore improvements are needed because: within the Institute of Mother and Child Institute, there is no transparency of information regarding quantity, quality and periodicity, as well as the sources and recipients of information. Thus, there is no reasonable assurance of the correctness, clarity, usefulness and completeness of the submitted information. Although within the Institute of Mother and Child there are different means of communication (e-mail, telephone, fax, paper, etc.), there is still no instruction / procedure on how to communicate internally and externally to ensure the rapid circulation of information, the provision of a response to the request, etc..

Component five, monitoring, evaluated the own tools of supervision of the IMC system of the Institute of Mother and Child. In the opinion of the internal auditor, the monitoring component is in line with the requirements of NICS, which is why improvements are needed because: the continuous monitoring process within the Institute of Mother and Child is ensured through various actions undertaken by the staff of the institution in the performance of their duties. It is also established the task force responsible for coordinating the development activities of the IMC and the internal audit assessing efectiveness of risk management, control and governance processes is implemented. In addition, the institution is continually subject to several internal and external evaluations.

The last part of the IMC self-assessment report is patrimony, finance and information technologies, which aims to evaluate its own control activities for the main patrimonial, economic and financial processes and information technologies of the Institute of Mother and Child. In the opinion of the internal auditor, the patrimony, finance and information technology component is partially in line with NICS requirements, therefore improvements are needed because: information technologies within the Institute of Mother and Child are constantly evolving. However, IT-specific risks (data intergity, non-disclosure of information, record of changes, etc.) need to be properly and timely managed.

According to the provisions of the MF Order No. 4/2019, the opinion of the internal audit is exposed for each component of the report. The internal audit opinion shall contain precise, clear, objective and concise information on the situation found as a result of the internal audit work carried out during the reporting period within the public entity and, where applicable, within the subordinated entities [OMF no.4/2019].

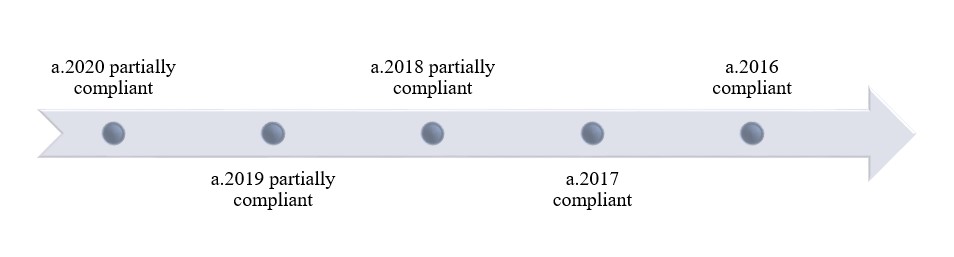

In conclusion, by analyzing the reports on the implementation of the IMC system within the Institute of Mother and Child and the declaration of managerial responsibility for the period 2016-2020, we find that the degree of compliance of the institution with NICS is – partially compliant, figure 3.

Figure 3. Degree of compliance of the IMC system within the Institute of Mother and Child

Source: Compiled by the authors

The assessment of the degree of compliance in the managerial accountability statement is made in relation to the number of NICS/fully implemented compartments, as follows [OMF no.4/2019]:

the IMC system is compliant if all 20 NICS/compartments are fully implemented;

the IMC system is partially compliant if between 9 and 19 NICS/compartments are fully implemented;

the IMC system is non-compliant if between 1 and 8 NICS/compartments are fully implemented.

The management declarations of responsibility signed by the head of the medical institution are placed annually on the official website of the institution, until March 1, in accordance with legal provisions.

Conclusions

In conclusion, we mention that the rehabilitation of the internal public financial control in the health system is a necessity and not a fad, and the COVID-19 pandemic highlighted this.

In the context of the above, the authors propose:

Strengthening managerial responsibility regarding the need and benefits of implementating and developing internal public financial control within the republican medical institutions from the Republic of Moldova;

Media coverage and in-depth information of managers, IMC coordinators, internal auditors and other stakeholders on the benefits of public internal financial control;

Harmonization of the internal audit function in the republican medical institutions, taking into account the factors influencing the efficiency of the function;

De facto implementation of the managerial internal control system in the republican medical institutions, for good governance of institutions;

Identification and management of emerging risks associated to public internal financial control in republican medical institutions.

Bibliography

Copaceanu C., Ensuring the efficiency of the financing mechanism of the health care system in the Republic of Moldova. Monograph. Iasi: Vasiliana 98, 2015. ISBN: 978-973-116-416-8

Government Decision no.124 of 02.02.2018. On the approval of the Program for the development of internal public financial control for the years 2018-2020 and of the Action Plan for its implementation.Available: https://www.legis.md/cautare/getResults?doc_id=119173&lang=ro

The Ministry of Finance. Internal audit manual, Edition I: Normative Framework. ISBN 978-9975-78-707-9. Chisinau, 2009. Î.S.F.E.P “Tipografia Centrala”, 276 p.

Order of the Ministry of Health no.519 of 29.12.2008 regarding the internal medical audit system.

Order of the Minister of Finance no. 4 of 09.01.2019 on the approval of the Regulation on self-assessment, reporting of the internal managerial control system and issuance of the Declaration of managerial responsibility.Available: https://www.legis.md/cautare/getResults?doc_id=112116&lang=ro

Order of the Minister of Finance no.49 of 26.04.2012 on the approval of the Regulation on evaluation, reporting of the financial management and control system and issuance of the declaration on good governance.Available: https://www.legis.md/cautare/getResults?doc_id=113590&lang=ro#

Order of the Ministry of Health no. 546 of 06.06.2012 on the approval of the rules for coding diagnoses and medical procedures.