Volume 2024,

Article ID 246695,

Journal of Economics Studies and Research,

11 pages,

DOI: https://doi.org/10.5171/2024.246695

Received date: 26 September 2023; Accepted date: 17 January 2024; Published date: 7 October 2024

Academic Editor: Agnieszka Komor

Cite this Article as:

Norman SCHERER (2024), “Transformative Dynamics in Private Equity: Exploring Co-investment, ESG Integration and Digitalization Strategies ", Journal of Economics Studies and Research, Vol. 2024 (2024), Article ID 246695, https://doi.org/10.5171/2024.246695

This paper delves into the evolving landscape of private equity (PE) financing, particularly in the context of the real estate and project development sectors amidst global economic fluctuations and geopolitical uncertainties. With traditional debt financing losing its sheen, the study focuses on the burgeoning role of PE, especially co-investment funds, as a viable financial alternative. Utilizing a rich dataset from reputable sources such as Morningstar, Pitchbook, and the European Central Bank, along with other pertinent studies, the paper presents a nuanced analysis of the declining PE transaction activity in 2023. It highlights how this downturn has catalyzed the adoption of innovative strategies, including the rise of “continuation vehicles” and the increasing significance of co-investments. Moreover, the research offers an insightful examination of the German SME sector, showcasing how PE can be a transformative force. It particularly emphasizes the incorporation of ESG (environmental, social, and governance) considerations and the advancement of digitalization within these enterprises. The study employs a mixed-methods approach, blending qualitative insights with a robust collection of both primary and secondary data. It argues that PE is not merely a financial instrument but a catalyst for meaningful business evolution, enabling German SMEs to effectively respond to current market challenges and undergo essential transformations. This paper aims to contribute to the broader understanding of PE’s role in contemporary business environments, offering valuable perspectives for academics, industry practitioners, and policymakers.

In the midst of economic uncertainties, exacerbated by geopolitical tensions such as the Ukraine war and economic fluctuations, the real estate industry and project development face significant challenges, particularly in terms of liquidity supply. While traditional debt financing instruments are losing traction due to these uncertainties, private equity (PE) appears to be an increasingly attractive financing alternative. A key advantage of private equity in this context is its inherent flexibility. In contrast to traditional financing methods, which often have rigid structures and conditions, PE investors can offer tailor-made financing solutions that meet the specific requirements of real estate projects. This allows both project developers and owners greater adaptability in a market characterised by fast-moving and constant change. In addition, PE offers deeper risk diversification. Investors are often willing to invest in different property sub-segments, be they residential, commercial or industrial, which helps to protect the portfolio against certain market shocks. This type of diversification can be invaluable in volatile times when certain market segments may be hit harder than others. Another significant advantage of private equity is the possibility of a long-term commitment. Many PE investors enter the market not only with the intention of a short-term profit, but with a strategic perspective that prioritizes sustainable development and values enhancement over time. This can be particularly attractive for real estate developers and investors looking for stable and long-term partnerships. Furthermore, it should be noted that in times when traditional financing methods seem inadequate due to external shocks and uncertainties, the characteristics of private equity – flexibility, diversification and long-term commitment – make it a particularly attractive financing alternative for the real estate industry and project development. Not only does it provide the supply of capital needed, but it can also help make the industry more resilient to future economic turmoil.

In the past, crisis years were good investment opportunities for private equity. However, investors have historically been able to participate little in these good vintages, as transaction activity has declined sharply during these periods. Private equity co-investment funds offer the opportunity to invest broadly diversified in resilient companies in the current market environment. The market is difficult for private equity funds. According to recent market data, private equity transaction activity fell by almost 50 percent in the first half of 2023. Fund managers were able to invest much less capital through company acquisitions or generate liquidity and returns for their investors through sales or refinancings (Pitchbook, 2023a, p. 3).

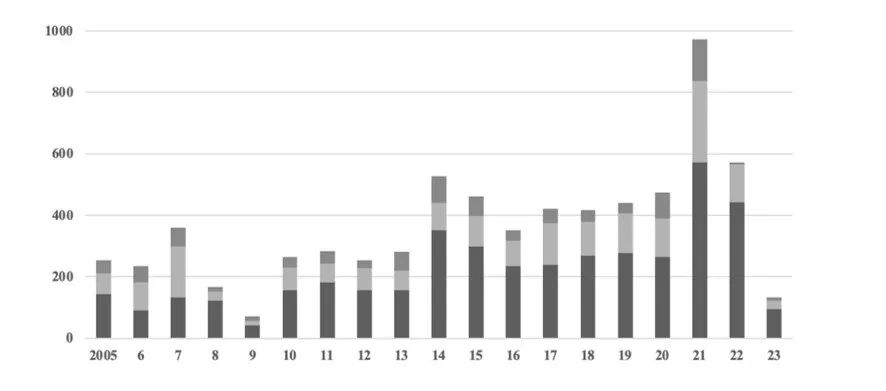

Tab. 1: Significant decline in realisations in the buyout segment. Own illustration modified by the author based on Dealogic (2023)

There are two reasons for the sharp decline in transactions. On the one hand, the evaluation of company prospects is extremely complex against the backdrop of the very uncertain macroeconomic situation. Investors shy away from risk and focus exclusively on companies with very resilient business models in new transactions. These include, for example, software companies that have a very high proportion of recurring revenues and a broadly diversified customer base. Companies with less stable prospects are almost impossible to sell (Pitchbook, 2023c, p. 11). The second reason for the decline in new transactions is the new interest rate environment. The use of debt to finance corporate acquisitions has become more expensive, and the volume of credit available for individual transactions is declining. Accordingly, private equity funds can only offer lower valuations in new transactions in order to be able to calculate adequate returns for their investment. Sellers are, therefore, currently only entering the market with their top assets because attractive valuations can still be achieved for these companies (European Central Bank, 2023, p. 42).

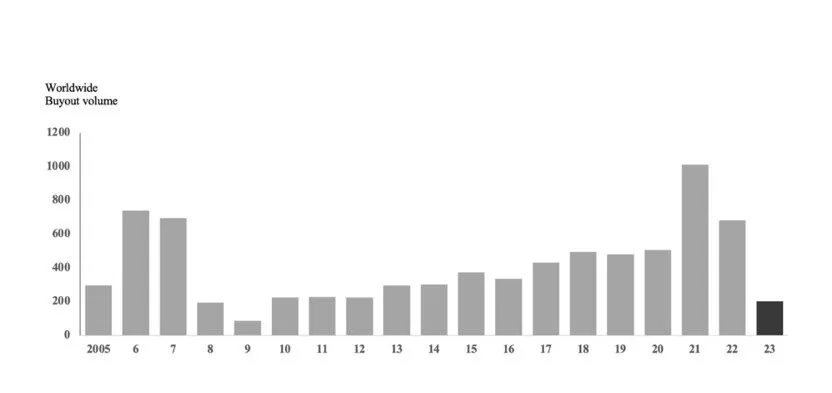

Tab. 2: Significant slump in global transaction volume in the buyout segment. Own illustration modified by the author based on Dealogic (2023)

But it is not only the transaction business that is complex for private equity funds in 2023. After many years with ever new records, investor demand for private equity is declining again for the first time. This is illustrated by surveys by S&P Global Market Intelligence: according to these, only 481 new funds were launched in 2022 – not even a third of the number in the previous year. Many funds are currently finding it difficult to raise sufficient funds for new deals (Pitchbook, 2023b). The reasons for this are complex. One of them is the denominator effect: precisely because private equity investments have been exposed to less severe devaluations than other asset classes such as bonds in particular in recent months, the value share of private equity in the portfolios of many investors has risen above the target allocation, which is why they are hardly taking on any new commitments in the asset class at present. Furthermore, due to the low transaction activity, the returns from the portfolio are not sufficient to finance new exposures. Furthermore, the changed interest rate environment offers investors the opportunity to achieve return targets outside of private equity again (Morgan Stanley, 2023, p. 3). The situation is exacerbated for many fund managers by the concentration of investors with their commitments to the big names in the market. CVC has in recent weeks announced the successful fundraising for its latest private equity fund, which at €25 billion is the largest private equity fund ever, absorbing a large share of the investor capital available this year. Accordingly, many smaller funds are suffering from investor attrition – even those that have already proven their capabilities with many years of good performance (Bloomberg, 2023).

Dynamics and Nuances of Co-investment in the context of Private Equity

The Yield Clock is ticking

Meanwhile, pressure is growing on fund managers to revive the transaction business. On the one hand, the yield clock is ticking louder and louder: in order to achieve their investment goals, well-developed companies must be successfully sold to realize returns for investors. At the same time, investors expect the capital provided to fund managers in recent years to be invested in attractive transactions. Only when the transaction merry-go-round has regained momentum, will there be sufficient liquidity and demand to rekindle the demand for private equity funds (Hudson, 2014, p. 20).

To solve this dilemma, private equity fund managers have developed a new tool: “continuation vehicles”. These are investment vehicles or investment funds set up by fund managers to acquire one or more companies from their existing portfolio. This allows the fund manager to retain control of these companies, invest new investor money in attractive companies, and, at the same time, offer liquidity options to their investors. The valuation and other material terms of the transfer are negotiated by independent investors, who then finance the vehicle together with the fund manager. These liquidity options are highly attractive to the majority of legacy investors (Pitchbook, 2021). Over the last twelve months, it has been observed that around 90 percent of investors have opted for liquidity rather than remaining committed to the companies on unchanged terms. “Continuation vehicles” are a very recent development in the private equity market and have quickly taken a significant share of transaction business. Market participants believe that this is not a short-term phenomenon but will remain an important liquidity option for private equity managers in the future. It allows fund managers to stay engaged in their best companies for longer and, together with management teams, to tap future opportunities. For investors in the private equity asset class, continuation vehicles offer new investment opportunities that cannot be addressed through the traditional fundraising market (Barings, 2023).

Co-investors as a Way Out of the Liquidity Squeeze

The successful initiation of a private equity transaction often extends over several years. Building relationships with decision-makers and developing concrete post-acquisition development plans for a company takes time. Based on the work done in recent years, acquisition opportunities for private equity funds present themselves, which are difficult to finance due to the complex fundraising market. Many fund managers are not in a position to cover the entire equity requirement for a transaction from their funds’ own resources, as the fund volume is still far from the target size (Hellmann et al., 2020, p. 85). Other fund managers stretch the available equity over more transactions to delay the time when they have to approach their investors again for new capital. This gives them time to further develop the portfolio and launch their fundraising campaign in a later, hopefully friendlier, market environment. In addition, fund managers use co-investment transactions as an opportunity to build relationships with new investors. Working closely on an investment gives new investors very deep insights into how a private equity fund works and increases the likelihood that this investor will also subscribe to the manager’s fund (Barings, 2023). The trend towards “continuation vehicles” and the liquidity squeeze among many fund managers, especially in the lower and mid-market segments, have caused the supply of co-investment opportunities to grow considerably in recent months. Although private equity transaction activity has declined sharply in absolute terms, the penetration of co-investment opportunities in these transactions has increased massively. While well-connected investors in private equity funds were approached with three to four deals per month in the past, this number is now often reached within a week. Since in this market environment, as explained above, almost only top assets are acquired, the quality of the companies on offer is above average for co-investors (Institutional Investor, 2023). The implementation of co-investments in private equity is complex. Access to co-investment opportunities requires an extensive private equity portfolio, deep market knowledge and broad networks to even become aware of individual transactions. Fund managers are then very careful in selecting their co-investors. Here, it is not only the capital strength that matters, but very much the transaction security that a co-investor can offer. This means that the co-investor has the necessary expertise, capacities, and processes to examine and implement a transaction in an often very tight timeframe. In addition, fund managers prefer co-investors who could also be considered as investors in the next fund or whose reputation can be helpful to the fund manager in future capital measures (Ernst & Young, 2023).

Co-investment Funds Provide Fast and Diversified Access

Investors who do not have the access, expertise, or processes to engage directly as co-investors, have the option of participating in a co-investment fund. Such a fund pools capital from different investors and, as an established and experienced investor, creates a diversified portfolio of co-investments alongside experienced private equity funds. Experienced investors have been using co-investment funds as a building block in their sophisticated private equity portfolios for some time, as they represent an efficient access to the asset class by passing on cost savings (Blackrock, 2021). In addition, all individual investments in the portfolio undergo a double check by the fund manager and the co-investor, and the diversification in co-investment funds is also broader than in most classic private equity funds. The result is a highly attractive risk-return profile for the investor (Blackrock, 2021).

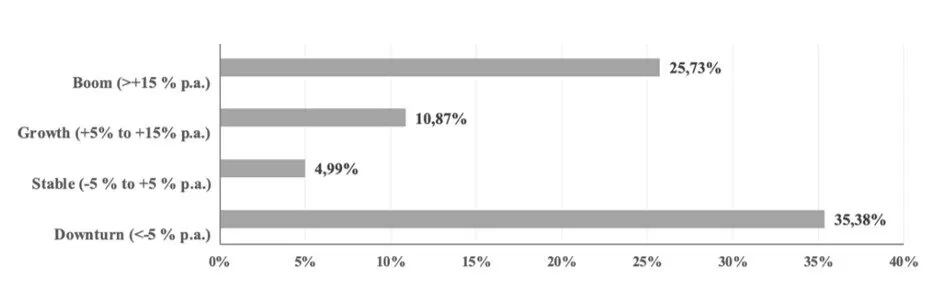

Tab. 3: Alpha in different market phases (boom, growth, stable, downturn). Own illustration modified by the author based on Dealogic (2023)

Private equity is also an important portfolio component in the current environment. In the past, the asset class has been able to generate excess returns compared to comparable transactions on the stock market, especially in times of increased volatility and uncertainty, as Golding recently explained in his “Alpha Study” with Professor Oliver Gottschalg from the HEC School of Management Paris. Investors who want to specifically take advantage of the current opportunities in the private equity market should consider co-investments as an addition to their private equity portfolio. The opportunity to build an attractive co-investment portfolio with the right partners has never been better (Gottschalg, 2022, p. 2).

Current Challenges – How Private Equity Can Generate Sustainable Value

Against the backdrop of dynamically changing business conditions, a large number of medium-sized companies are facing various challenges. These include, among others, technological change, globalization issues, growing competitive pressure, as well as tightening regulatory requirements with regard to sustainability issues (such as the Supply Chain Act, which has been in force since 2023, or the SFDR and CSRD directives). To meet these challenges and be competitive in the long term, SMEs need to adapt to the dynamic market environment and implement sustainable business processes that ensure not only their competitiveness but also their future viability. Sustainable business models help to reduce risks, improve resource efficiency and strengthen stakeholder trust. Meanwhile, digital transformation is opening up new opportunities for companies to increase efficiency, enter new markets and develop innovative strategies (Hellmann et al., 2020, p. 548). In this context, private equity investors are becoming increasingly important. While sustainability aspects now play a leading role in investments, financial investors are also increasingly bringing a high level of expertise and experience in the area of digitalisation. Based on strong internal resources and expert networks, private equity investors can support the development and implementation of sustainable business processes, the implementation of digital solutions and the optimization of corporate strategy, helping SMEs to successfully overcome current challenges and transform business models in a sustainable way (Hellmann et al., 2020, p. 548).

Private Equity Investments in Germany

There are approximately 2.5 million small and medium-sized enterprises (“SMEs”) in Germany, of which ~62,000 companies generate sales of between 10 and 50 million euros and ~16,000 companies exceed the sales threshold of 50 million euros (as of 2020). Thus, based on the number of companies in the German SME sector alone, there are many interesting investment opportunities for private equity investors. Furthermore, there are currently many SMEs seeking a succession solution for their company: By the end of 2023, around 190,000 owners will be looking for a successor for their own company. While 120,000 entrepreneurs have already successfully found a successor, there are still almost 70,000 unresolved succession issues in the current year. According to KfW, the number of unresolved succession issues will even increase to 560,000 by the end of 2026. By far the biggest problem here is the lack of finding a suitable successor – 79% of all entrepreneurs surveyed cited this as the main problem. Experienced private equity investors can provide support here and solve unresolved succession issues (Neue Züricher Zeitung, 2022).

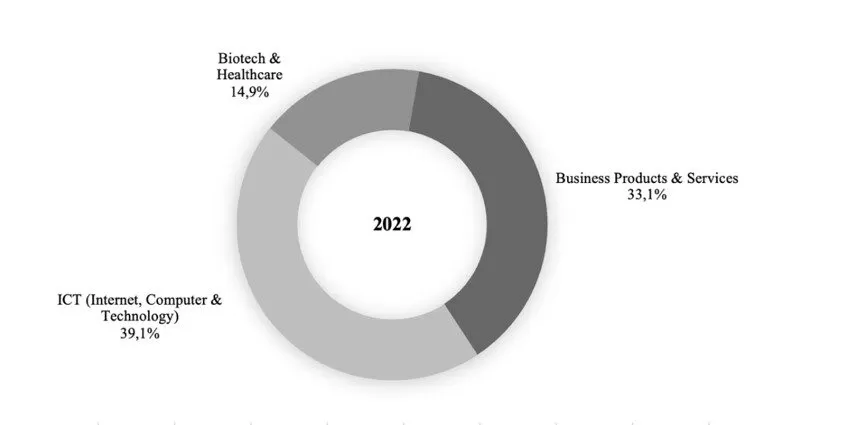

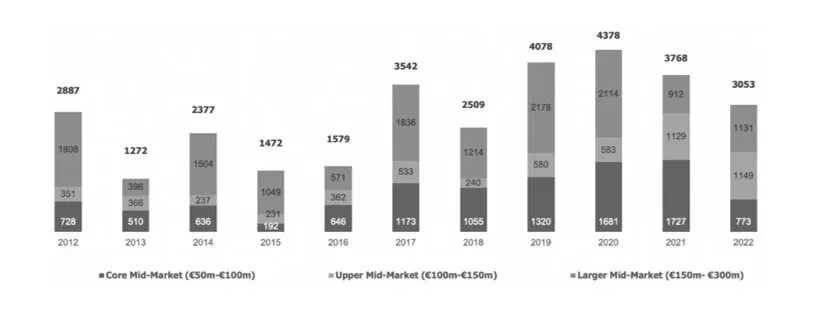

A closer look reveals that private equity has played an increasingly significant role in financing and succession solutions for companies in the German mid-market in recent years. Between 2012 and 2022, around €30.9 billion was invested in the German “mid-market” sector, which includes equity investments of €50 million to €300 million. The most attractive sectors for private equity in 2022 were ICT (Communications, Computers & Electronics), which accounted for 39.1% of the total investment amount, followed by Business Products & Services with 33.1%, and Biotech & Healthcare with 14.9% (Pitchbook, 2023a, p. 3).

Tab. 4: Private equity investments in Germany by sector. Own illustration modified by the author based on Dealogic (2023)

ESG is Now a “Must-Have”

In addition to the increasing popularity of private equity investments, the sustainability aspect has also become much more important in recent years. Both growing investor awareness and the regulatory environment have meant that ESG is now much more of a “must-have” than a “nice-to-have” for private equity funds and institutional investors. According to surveys, particularly important aspects for limited partners (“LPs”) are an existing ESG reporting system or an ESG policy and consideration of the social and environmental aspects of investments. Especially in Europe, an ESG anchoring is of great importance and for 56% of LPs it is definitely a reason for refusal to invest in a private equity fund. Furthermore, the introduction of the SFDR increases the transparency requirements for private equity investors with regard to ESG metrics which LPs have to disclose, e.g. certain environmental emissions, water consumption as well as occupational safety and diversity. In addition, the CSRD imposes comprehensive sustainability reporting obligations on many SMEs in Germany, regardless of their ownership structure. Thus, portfolio companies have further incentives to optimize their ESG performance (J.P. Morgan, 2023).

Tab. 5: Private equity investments in German SMEs. Own illustration modified by the author based on Dealogic (2023)

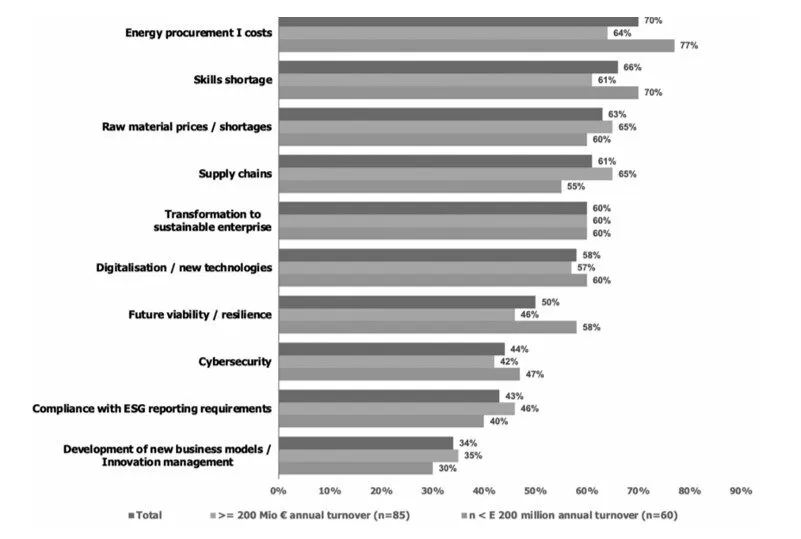

The consulting firm PWC conducted a survey among German SMEs on the ten biggest challenges in the coming years. With energy procurement/costs, shortage of skilled labour, raw material prices/scarcity, supply chains, transformation to sustainable companies, future viability as well as compliance with ESG reporting requirements, seven ESG-related challenges are in the most frequently mentioned responses. At the same time, the companies surveyed worry about overburdening their organization by aligning their business with ESG requirements. Private equity investors can offer comprehensive support here – not only financially, but also through expertise and specialised networks, as many private equity investors now have in-house ESG teams. They can help develop and implement a comprehensive ESG strategy that meets the needs of investors, lenders and other stakeholders (PWC, 2023). By implementing environmentally friendly technologies, sustainable supply chains and processes, companies can increase their resource efficiency and reduce costs. This leads to improved operational performance and long-term value creation. Companies that are also committed to social responsibility and promote a positive corporate culture can attract and retain talented employees over the long term (Matos, 2020, p. 27).

A study published in 2023 by Bain & Company together has shown that the area of sustainable supply chains and employee satisfaction in particular has a direct positive influence on the operational performance of companies. The evaluation shows that companies with sustainable supply chains generate on average a 3% higher EBITDA margin than companies that do not consider ethical and environmental aspects when selecting suppliers. In addition, companies with a high level of employee satisfaction even achieve a 6% higher EBITDA margin compared to companies with a low level of employee satisfaction, as well as an average annual sales’ growth that is 5 percentage points higher (Bain & Company, 2023).

Tab. 6: The ten most important challenges in the coming years. Own illustration modified by the author based Bain & Company (2023)

Other positive aspects of implementing an ESG strategy can be better financing conditions. Financing partners have an increased interest in companies with strong ESG performance, as they are seen as more stable and sustainable in the long term and have lower environmental and operational risks. In addition, the so-called “sustainability-linked” financing is becoming increasingly popular, also in the private equity context. In this context, financing partners link loan conditions to sustainability targets, whereby the loan interest rates are reduced or increased during the term depending on whether the targets are achieved or not. This also creates incentives for companies to align their corporate strategy with ESG (Landesbank Baden-Württemberg, 2023, p. 6).

Digitization

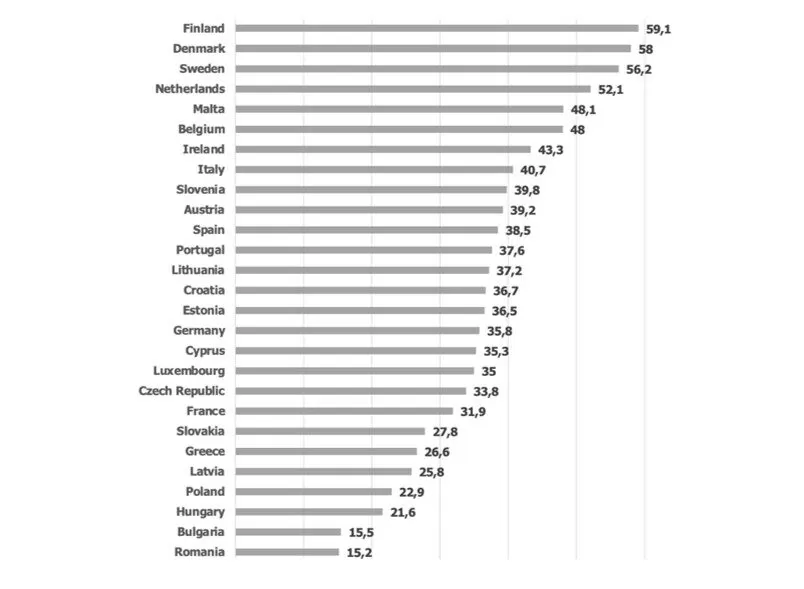

The trend towards automation, digitalisation, and networking has been established in many large national and international corporations for some time. In contrast, however, numerous medium-sized companies in Germany have some catching up to do in these areas and sometimes have considerable difficulties integrating new technologies into their business processes. This is also shown by the Digital Economy and Society Index (DESI) 2022, in which Germany ranks in the lower half of all 27 EU countries, in 16th place, with 35.8 index points. Finland takes the top position with 59.1 points. Germany also lags far behind countries such as the USA, France or the UK, in terms of IT investments (European Commission, 2023, p. 10). According to a study by KfW, the corresponding investments in relation to gross domestic product (GDP) would have to more than double to reach the level of the countries mentioned above (KFW, 2021, p. 4).

This reluctance to make urgently needed investments in digitization can be attributed to various obstacles, e.g. (i) cyber security concerns, especially the fear of cybercrime, but also the handling of data protection issues due to the DSGVO changeover in 2018; (ii) lack of internal IT competences, additionally reinforced by the existing shortage of skilled workers; (iii) lack of infrastructure (especially speed and quality of the Internet connection) or (iv) limited financial resources. On average, a medium-sized company spends 12 times as much on investments in fixed assets than on digitalisation.

Tab. 7: Ranking of the German economy with regard to the integration of digital technologies. Own illustration based on European Commission (2023)

In this context, private equity investors can provide support to the companies concerned. They not only provide financial resources for digitization projects, but also bring in their extensive network of technology providers and experts (e.g. in the form of a dedicated advisory board member) to facilitate access to expertise and resources. In addition to ESG teams, most established investors now also have internal digitalisation teams that can specifically support the management of portfolio companies in the implementation of digitalisation projects. An important value driver can be, for example, the introduction of a uniform ERP and financial reporting system in order to standardize data processes and increase transparency in business processes. Furthermore, the topic of cyber security is now high on the agenda for many investors (PWC, 2016, p. 7).

Conclusions

In a rapidly changing market environment, private equity co-investment funds have proven to be valuable tools that offer investors the opportunity to invest in resilient companies. Despite a significant decline in private equity transaction activity in 2023, mainly due to macroeconomic uncertainties and changing interest rate environments, newly developed continuation vehicles and co-investment strategies offer solutions to liquidity challenges. A key theme running throughout the paper is the growing importance of ESG (environmental, social and governance) in the private equity industry. This is reflected in the need for SMEs to develop sustainable business models and undertake digital transformations. Germany, although economically strong, has some catching up to do in terms of digitalisation compared to other EU countries. Private equity can serve as a valuable partner for companies that need to adapt to current market requirements. This is highlighted in particular by the introduction of “continuation vehicles” and co-investment strategies developed in response to current market conditions. These instruments offer both liquidity options and new investment opportunities. The complexities and nuances of co-investment in the private equity context are also discussed in detail. Implementing co-investments requires deep market understanding and broad networks. Despite the current challenges, co-investment funds offer a fast and diversified way for investors to access the market. With regard to Germany, the paper shows that the country has a rich landscape of SMEs that present both challenges and opportunities for private equity investors. ESG and digitization are two main areas where private equity can provide significant value to these companies. Introducing ESG strategies and supporting digitization projects are just two examples of how private equity can transform German SMEs and adapt them to current market demands.

In conclusion, the author underlines the crucial role that private equity plays in the current business environment, especially in terms of helping companies overcome challenges and transformations. Whether through ESG integration, digitalisation or innovative investment strategies, private equity remains a key player in shaping the future of entrepreneurship.

Matos, P. (2020) ‘ESG and Responsible Institutional Investing around the world: A Critical review’ (August 7, 2020). CFA Institute Research Foundation Literature Reviews, Charlottesville.