Study of Dividend Payout Analysis of Asian And European Markets: Relationship with Dow Jones Asia Select Dividend 30 Index (DJASD) and Dow Jones Europe Select Dividend 30 Index: A Pre-Study Paper

1,2Research Scholar, Chitkara Business School,Chitkara University, Punjab, India

3University Institute of Applied Management Sciences,Panjab University, Chandigarh, India

Volume 2019,

Article ID 301968,

Journal of Financial Studies and Research,

11 pages,

DOI: 10.5171/2019.301968

Received date: 5 February 2019; Accepted date: 29 July 2019; Published date: 9 October 2019

Cite this Article as:

Saurabh GANDHI, Sandhir SHARMA and Manu SHARMA (2019)," Study of Dividend Payout Analysis of Asian And European Markets: Relationship with Dow Jones Asia Select Dividend 30 Index (DJASD) and Dow Jones Europe Select Dividend 30 Index: A Pre-Study Paper", Journal of Financial Studies & Research, Vol. 2019 (2019), Article ID 301968, DOI: 10.5171/2019.301968

The study below aims at determining the existence of correlation and the degree of the correlation of the dividend payout of different stock markets across Asia and Europe with the Dow Jones Dividend Select 30 indices, respectively. Most of the current studies around dividend payouts are anchored around its viability for companies and to tackle issue of optimum reserves and surplus as well as agency problems to some extent. In some other cases, it is related to the existent Tax structure of that country and how the variance in dividends is attributed to the same and how it helps the companies with managing their financial resources. However, from a global investor point of view, as a factor of choice among various stock markets to invest, all these studies become limited in scope as they may at best be indicators of a particular sector of the economy at a certain point in time. Through this study, the authors shall endeavor to enlarge the scope of this understanding from the global investor perspective by identifying the existing gaps from the investors’ perspective and aim to bridge the same to provide a more structured result-oriented model for the investors. This shall benefit the investors at two important levels:

A more structured indicative approach to study shareholder/investor wealth vis-à-vis a stock market group, thus, leading to a more informed choice from an investor perspective

The ability to set realistic expectations on the return of investment and to be able to account for the same in a more appropriate way with the least available variance.

Keywords: Keywords: Dividend, Payout, Asian Market, European Market

Background to The Study

Starting from 2015, there were $294 Trillion invested in financial assets across the world. These investments include:

Non-securitised loan

Securitised loans

Non-Financial Corporate bonds

Financial Institutional Bonds

Public debt securities

Stock market capitalisation

Out of these financial assets, Stock Market Capitalisation, which is also our area of interest for this research, has $69 trillion in investments or 89% of the world GDP. Overall, all the financial assets combined of 378% of the world GDP.

The economies of the various countries have an intrinsic linkage to each other and world trade, interest rates, currency rates, demand-supply and tariffs play an important role in the same. The interdependency of the economies provides the necessary checks and balances model for the world order to move smoothly. The increase in the size of the world economy has been a boon for the developing world as the surplus cash and low interest rates in the developed markets make them logical investors to the rest of the world as scalability within their own markets become saturated or optimised. This gives rise to the global investors, companies, financial institutions and individuals who have the knowledge and the resources to add value as well as derive benefits from the different economies of the world. In some selected cases, the type of economy makes it relatable to the investor to be a part of their financial story. As an example, Australia is a financial service driven economy wherein banks, financial institutions and superannuation funds form the largest part of the economy. For investors with a greater understanding of the financial sector, the Australian economy makes it a viable global investor option. Another example of the same is the Indian economy, an emerging economy with strong fundamentals, having a strong industrial and services sector with ample room for growth. An investor looking for inorganic shareholder value increase over a decade may find investing in the Indian economy suitable. From the point of view of shareholder wealth and before studying the various parameters of the study, it’s important to understand a few definitions and terminologies to take the study further.

Definition of Terms

Dow Jones Europe Select Dividend: The Dow Jones Europe Select Dividend 30 aims to represent the leading stocks by dividend yield traded in the developed markets of Europe, currently defined by S&P Dow Jones Indices as Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the U.K

Dow Jones Asia Select Dividend 30: The Dow Jones Asia Select Dividend 30 Index aims to represent the leading stocks by dividend yield traded in major Asian markets.

Market capitalisation: It is the market traded value of a company’s share multiplied by the number of publicly traded shares. For instance, the market capitalisation of reliance Industries is INR 699904 Crores or Approx USD 1 Billion

Capital Gain/Loss: A Capital gain that occurs on any security or stock is sold at a price higher than it was paid for at the time of purchase. A reverse trend shall entail a capital loss. The capital gain/Loss triggers a tax event only when the gain or loss is realised.

Income Gain: While Capital gain occurs when the overall value of the investment rises, the income gain in the case of security/stock occurs when dividend is paid out from the quarterly/half yearly or annual earnings of the company.

Capital gain as a strategy of shareholder wealth has a larger time horizon as the stock prices across companies vary from time to time. There is no timeframe for an optimum return and the same is at best a structured and calculated judgement call by the investor in terms of both entry and exit from the stock market. Capital Gain/Loss over a financial year may neutralise itself due to the variation in stock prices over the full year or investment horizon.

Income gain is a more organic way of growing shareholder wealth as it provides a recurring stream of income to the investor on a quarterly, half yearly or annual basis. More often than not, income gain through dividend receipt is a regular feature for the investor. Income gain may or may not happen, however it doesn’t lead to an exponential surge or exponential loss in value to the investor. As a strategy and also as definition, income gain through dividend payout is one of the key indicators of the financial health of the companies and the stock market they form a part of and, thus, is a key indicator of its overall ability to scale in capital size and volume. As this study moves further, there is an analysis of the importance to study this aspect of shareholder wealth creation from the perspective of an investor to help evaluate a particular stock market behaviour and its correlation towards income gain through dividend payout.

Problem Statement

Nearly 84% of the companies in the S&P 500 index (Large cap) segment pay dividends on a regular annual basis. 70.4% of companies in the S& P mid-cap segment pay dividends and 54% of the companies in the small cap segment pay regular dividend to its investors. The three important points to note here are:

As the companies grow in market capitalisation, dividend payout becomes an important feature of stakeholder engagement

Investment in large cap companies indicated that the viability of an income gain from large cap companies is one of the reasons for investors to make that a strategy for increasing their shareholder wealth.

As a global investor looking at income gain, with the ability and the likelihood to choose among different markets to invest, the study of different companies, industries and the vagaries of their dividend payouts and capital gains can be quite cumbersome. Even if the same is successfully achieved, different markets can bring out similar results across industries thus leaving the investor with the same dilemma as to where to invest. The likelihood to invest in multiple sectors amplifies this dilemma.

There is no present evidence of the existence of and a degree of relationship between dividend payouts in the Asian and European markets. As mentioned above as well, with the propensity of the large cap companies to share more dividends, it would be prudent to understand the relationship of the various stock markets against well-defined benchmarks for dividend payouts and assessing the degree of correlation. The benchmarks are normally market verified indices like the Dow Jones Asia and Dow Jones Europe. This study aims to provide some definitive results on the amount of correlation between the markets and these indices.

Objectives of The Study

To understand the relationship between dividend rewards in Asian market and performance of the Asian financial markets.

To understand the relationship between dividend rewards in European and performance of the European financial markets.

Comparative analysis of robust regression using WLS and Robust regression using M-Estimators in identifying relationship between dividend rewards and performance of financial markets and to identify leading indicators of correlation between the same.

Review of Literature

For the purpose of literature review and as part of the exploratory and secondary research for the project, the finding of the existing available literature in the form of research papers shall be discussed. The endeavour is using this research to identify the areas where no/low research has happened and arrived at a unique problem statement and carry on research on the same.

Giuli, Karmazeine and Sekerci (2018), in their study “Common Ownership and Firm dividend policies”, discuss the dividend policy of the newly inducted firms in the investor’s portfolio. They reason that after new companies are added to an investor’s portfolio, the dividend policy of the newly inducted firms follow the investor’s dividend “taste”. This is more prominent in the case of companies with low concentrated institutional ownership. While the study provides the progression of dividend policy as per ownership, it doesn’t provide a definitive indicator for investors to have parameters basis stock exchange indicators to choose companies from.

Hunjra, Faisal and Khan (2017) in their study “Application of Linter’s Dividend Model in Pakistan: Sector-Wise Analysis” reflects on the stability of dividend payouts in the manufacturing sector in Pakistan. They highlight that regulators and policy makers need to ensure the growth and profitability of the sector in the long run so that it ensures a regular dividend payout. The study reinforces the company side analysis that profitability drives the dividend payouts for the companies. From a global investor point of view, looking at a dividend earning strategy, the study doesn’t provide any conclusive leads to follow.

Hamza and Hassan (2017), in their study “Impact of dividend policy on shareholders wealth: a comparative study among dividend paying and non-paying technology based firms in USA”, concludes that in the technology sector in the USA, the existence of dividend payout or the absence of it does not have any significant bearing on the shareholder wealth. The technology sector is always in the growth mode and, thus, there is a more chance of capital gains in the long term as technology companies invest the retained earnings back in the company. Though our study does not cover the USA markets, we can always try to understand the holding of the technology sector within a stock market and see the variation in the correlation of the different markets with the dividend payout indices

Dreeper and Turki (2016), in their study “Dividend policy following mergers and acquisitions: US evidence”, endeavour to understand the impact on dividend following Mergers and Acquisitions of dividend paying companies. The study tries to understand the impact of the strategy of a target company after its merging or acquisition by another company, and the degree to which it impacts the overall dividend payout of the new entity. The study concludes that the new entity alters its strategy to meet the pre-merger/acquisition expectation of the target’s shareholders and, thus, re-aligns its dividend payout strategy, accordingly. For the purpose of this study, it adds value as M&A could be one of the factors for stock markets having higher dividend payouts as compared to others.

Demirgüneş (2015), in the study “Determinants of Target Dividend Payout Ratio: A Panel Autoregressive Distributed Lag Analysis”, takes into account the Target Dividend Payout ratio (TDPR) as the dependent variable. The study looks into the effect of profitability, liquidity, growth, risk, market expectations and taxation over the short and long run on the TDPR. The study concludes that profitability has a positive impact on TDPR but in the longer run and as growth patterns change, market risks vary and taxation policies take effect, there is a negative impact on TDPR. The study reinforces that dividend payouts are studied from a company/industry perspective, in this case; the cement industry. The perspective of the global investor and how it correlates with the overall dividend correlation with stock markets still remains to be studied.

Ali Ahmed (2008), in his study “The Impact of Financing Decision, Dividend Policy, and corporate ownership on Firm Performance at Presence or absence of growth Opportunity: A Panel Data Approach Evidence from Kuala Lumpur Stock Exchange”, studies the impact of dividend policy and debt policy on firm value, both in presence and absence of growth opportunities. The study highlights the following key points:

Dividend payment as a policy remains constant in both growth and no growth times in a company’s history as the same is valued by investors

Growth opportunities may lead to a reduction in dividend value as the profits are likely to be reinvested in growth opportunities. However, an increase in form value by capital/market expansion would lead to an increase in shareholder wealth

The absence of growth opportunities may lead to an increase in dividend payout as the firm would like the investors to stay invested and also to indicate a strong future expected performance.

Ghauri (2008), in his paper “A Comparison of Dividend Policy of UK and US Banks over the Period 2003 – 2007 From Shareholder’s Point Of View”, makes a niche investor side study to understand the dividend payouts for banks in UK and USA for a specific timeframe. The study concludes that UK banks have a greater relationship between shareholder wealth and dividend payout. However, the study does not analyse and compare the relationship with the overall stock market and highlights the particular sector of banking. Through this study, we aim to explore and explain the larger correlation of dividend payout of the Asia and Europe level indices and their relationship with the stock market

Bulan and Subramanian (2008), in their study “A Closer Look at Dividend Omissions: Payout Policy, Investment and Financial Flexibility”, study dividend omission and find out that a complete dividend omission is directly related to the financial stability of a firm and companies with lower financial performance which tend to omit dividends to take care of short term stability. 25% of these firms, however, start paying dividend within 3 years of dividend omission. The study highlights that while dividend reduction may not trigger any concern from an investor perspective, however, a complete omission of a dividend may lead to negative stock fallout which may make it harder for the company to recover in the long term.

Thirumalvalavan and Sunitha (2006), in their paper “Share price behaviour around buy back and dividend announcements in India”, discuss the most effective way of impacting shareholder wealth. Their analysis is based on the signaling price theory which states that the announcement of dividends signals positive financial prospects and outcomes for the companies in the future and, thus, evince a greater interest from existing and new investors. In addition to the same, they also check the viability of a share repurchase option as a signal price theory apart from dividend announcements. They understood that abnormal return post share repurchase is higher than abnormal returns post dividend announcements.

Savov (2006), in his paper “Dividend Changes, Signaling, and Stock Price Performance”, studied the post signaling performance of German Companies. The study only covered the dividend announcement as a parameter of signaling and came to the conclusion that the post announcement performance of companies does not increase significantly as compared to companies with reduced or similar dividends. Thus, an announcement in increased dividend may signal positive future performance but actually does not follow the desired pattern in comparison to companies with flat dividend growth. Thus, there is no relatable correlation of the signaling theory with actual post announcement company performance.

Banerjee, Gatchev and Spindt (2005), through their study “Stock Market Liquidity and Firm Dividend Policy”, emphasize that dividend payout policy for a firm is depending on the level of liquidity of the stock. Illiquid or low liquid stocks tend to pay out more dividends as compared to liquid stocks. From the perspective of our research, it emphasizes that dividend payout needs a more focused study and its correlation to overall market dividend payouts.

Amromin, Harrison, Liang and Sharpe (2005), in their paper “How Did the 2003 Dividend Tax Cut Affect Stock Prices and Corporate Payout Policy”, discuss the implication of tax cuts on dividend payouts. As per their study on the US markets, the tax cuts impact the increase in dividend payouts and, thus, emphasize once again the importance of studying the different markets across continents to have a more definitive correlation of dividend payouts with markets.

Goergen, Renneboog and Da Silva (2004), in their study “Dividend policy of German firms: A dynamic panel data analysis of partial adjustment models”, make 2 important observations:

German firms pay out low dividends as compared to UK firms within Europe.

The dividend returns from a market could be related to the accounting policies of a particular country

This provides impetus to our study for the need to study different European markets as there is no standardised method across the world to add to shareholder wealth and the factors which impact it.

Y Subba Reddy (2003), through his study “Dividend Policy of Indian Corporate Firms: An Analysis of Trends and Determinants”, takes this a step further and argues that the agency problem may not be the only reason in the variability of dividend payouts. He highlights other factors such as:

Dividend tax on the propensity to pay dividends.

Firm characteristics such as profitability, growth and size of the dividend payment pattern.

Influence of loss on dividend reductions.

While the study again highlights the importance of studying dividends, it provides factors from a firm perspective and not from an investor or overall stock market perspective.

Farinha (2002), through his paper “Dividend policy, corporate governance and the managerial entrenchment hypothesis: an empirical analysis”, discusses the dividend policy of 600 large UK firms and ideates how the existence of dividends helps to transform the managerial entrenchment levels. The study focuses on the importance of dividends and maintenance of an optimum level so that it reaches a critical level and, thus, insider ownership becomes positive from negative. While this paper highlights the importance of ongoing dividends, the correlation of their payout is defined in terms of the firm requirement and not the shareholder or investor perspective.

Penman and Sougiannis (1995 and revised in 1996), through their research on “A comparison of dividend, cash flow, and earnings approaches to equity valuation”, highlight the linkage between the shareholder price and dividends. They highlight that by stating that the calculation of equity value is typically characterized as a projection of future payoffs and a transformation of those payoffs into a present value (price). In more general terms, it means that the share price value is the financial capacity of the stock to pay future dividends. Shares use a dividend discount model to arrive at a present price for the stocks. However, they also point out that a much-improved way of doing the same is through a discounted cash flow method. While this provides credence to our area of research that dividend payout is a variable to be studied, the study does not provide any degree of correlation.

Gap Analysis

Equity and its related investments come with their share of risk. While investment as a strategy can be structured from time to time basis frameworks developed with the existing important variables at that point in time, as well as, the extraneous factors that may be prevalent at the time of the development of the investment framework, and as markets and knowledge evolve, there always remains a scope of improvement.

Equity risk is a structured risk wherein as an investor you evaluate:

Historical performance of the company.

The financial data of the company.

Its performance vis a vis its local and global industry.

Projections for the future.

An empirical analysis and empirical leveraging/haircut of the projections.

As an investor in the same domestic space and the companies, the study of individual stocks and industries may lead to a well-informed decision because the scope of investment has also been limited by choice or by provision as being domestic.

From a global investor perspective, this leaves many data points to analyse. This can also be cited as a problem of plenty but reaching that point becomes an exhaustive and sometimes financially obtrusive effort for the global investor. While capital gain as a parameter of shareholder wealth is a long-term strategy, dividend payout year on year provides the right context to an investor to help modify their long-term strategy and, thus, enhance the overall capital gain as well. Thus, dividend payout becomes an important aspect for a global investor as a medium of study and selecting a stock market/exchange to be a part of.

Despite, as it stands, available literature which highlights the existence of the dividend payout criteria as part of shareholder wealth creation mechanism, a large majority of the payout perspective is from the firms’ point of view. There is no definite correlation available of a dividend payout trend from the overall market/stock exchange perspective for a global investor.

This inherent gap needs more comprehensive research from a global investor point of view. A more informed approach for a global investor becomes important as the world markets become globally interdependent and, thus, provide more opportunities to both markets and investors to explore and gain from each other. A thorough gap analysis from the point of view of the global investor shall help us understand the following variables/gaps to build on and develop this progressive investor journey forward:

The presence of correlation between dividend payout with a stock market.

The degree/level of correlation between them.

The impact of both the above on the other variables studied by the investor to invest in any global market.

Provide Justification for The Study

The presence of a gap or a newly identified variable may or may not have any direct bearing on the pattern of investment for an investor. There has to be relevant literature and past indicators which trigger the necessity of a thorough study for the same.

If dividend payout had been a linear study with finite variables, all markets would follow the leaders and, thus, it would be easy to predict the patterns of dividend payout and make an investment. However, a study by Henderson Global for dividend payouts shows that the US companies leads the way in global dividend payout with 37% of the global dividend payouts.

Emerging markets account for 14% of the global dividend payout. An interesting trend here is the comparison between companies in the UK and the Rest of Europe: – markets which are more alike than different. While UK accounts for 11% of the global dividend payouts, the rest of Europe (Ex-UK) is double that quantum at 22% of the global dividend payouts. It re-emphasizes the fact that the degree of dividend payout is not a market and from the perspective of a global investor, it became imperative to have a more structured market analysis around dividend payouts and their correlation with the individual markets to make informed choices for the short, medium as well as long term perspective.

Another important aspect which is important for this study is the quantum of market capitalization held by Institutional investors. Some important aspects through a study by Charles McGrath in Pensions and Investments highlight the following:

Institutions own about 78% of the market value of the U.S. broad-market Russell 3000 index, and 80% of the large-cap S&P 500 index. In dollars, that is about $21.7 trillion and $18 trillion, respectively.

Of the 10 largest U.S. companies, institutions own between 70% and 85.8%.

Apple, the largest company by market cap, is the most widely held company by institutions, with Vanguard, Blackrock (BLK) and State Street the largest holders.

Institutional investors have the scale, geographic ability and the management capability to be present in more than 1 market, concurrently. Thus, it becomes imperative to study and structure the investor side mechanism for dividend payouts for more effective decision making.

Through this study/research, it’s aimed to provide an indicative trend and a degree of correlation of the dividend payout from a market perspective and, thus, its study is important before investments in various global markets across Europe and Asia.

Theoretical Framework

The theoretical framework of this study has been developed in 3 stages:

Existing dividend payout models

A brief framework for further research

Selection of Stock markets for study

A) Existing dividend payout models: The existing dividend payout models and their important features are mentioned below:

Gordon’s Model: The Gordon’s dividend discount model is used to determine the valuation of equity of company based on dividend payout on future basis. The future dividend payouts are discounted to calculate the value of equity of a given company. The Walter model also discounts the future dividends assuming that retained earnings are the only source for company, the investment risk remains irrespective of selection of future projects and the company continues to grow till infinity.

BIRD in hand theory: The bird in hand theory on dividends state that out of capital gains and income gains, the investors prefer income gains in the form of dividends as they consider the capital gains as a higher risk investment.

M-M Hypothesis: According to Miller and Modigliani Hypothesis or MM Approach, dividend policy has no effect on the price of the shares of the firm and believes that it is the investment policy that increases the firm’s share value. The investors are satisfied with the firm’s retained earnings as long as the returns are more than the equity capitalization rate “Ke”. What is an equity capitalization rate? The rate at which the earnings, dividends or cash flows are converted into equity or value of the firm. If the returns are less than “Ke” then, the shareholders would like to receive the earnings in the form of dividends.

B) A brief framework for further research: Development and deliberation of further research is based on the following steps:

Analysis of the existing models and their sufficiency w.r.t. decision making ability for the global investor.

Identification of relevant gaps vis-à-vis the scope for the investors to identify defined patterns for investment.

A thorough analysis of the identified gaps in related frameworks to lay the basis and justify the further course of the research.

In light of the above, it is important to highlight how the existing models and theories do not provide the required sufficiency of choices to the investors for making informed choices to select the markets to invest. For instance, the Gordon model takes dividend as a parameter to value future equity prices of the stock. It does not provide details on investment patterns basis of the dividend payouts. The M-M hypothesis moves away from the equity price theory, however, the assumptions on which it is based such as perfect capital markets, uniformity in taxation in income and capital gains, certainty of future profits and no additional risk in future make it unviable to be used by investors to calculate and develop models for income gains.

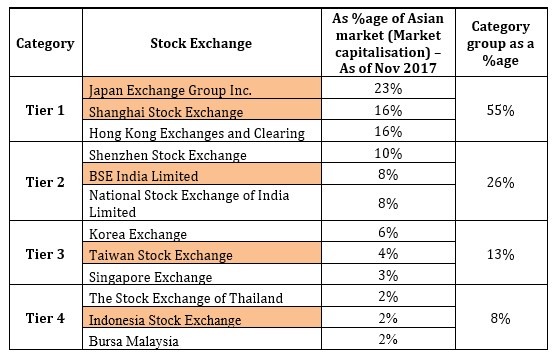

C) Selection of Stock markets for study: The study shall examine the relationship of the Dow Jones Asia Select Dividend 30 Index (DJASD) with six Asian market indices namely Bombay Stock Exchange (BSE), Jakarta Stock Exchange (JKSE) Index, Korea Composite Stock Price Index (KOSPI), Nikkei (Japan), Shanghai Stock Exchange (SSE) and Taiwan Stock Exchange Corporation (TSEC) and five European market indices namely Austria (ATX), Belgium (BEL20), France (CAC40), Germany (GDAXI) and Switzerland (SSMI). It involves the calculation of coefficient of correlation and coefficient of determination to explain the pattern of variance of the DJASD Index with the aforesaid independent indices.

The selection of the Asian stock markets is based on choosing a representative sample of the overall Asian market. The markets have been tabulated in order of decreasing market capitalisation, and have been subdivided into different tiers/categories and the following selection is to ensure a representation across market sizes as well as geographies.

The selection of the European markets has been done on the basis of the following:

The dividend payout in European markets Ex-UK is double that of UK at 22% of the global markets.

The selected markets in Europe have the highest growth rates i.e. Austria, France, Germany, Belgium and Switzerland.

Identification of The Problem

Stock markets do not follow a linear pattern in terms of investments and, thus, they cannot be understood from one or a few selective frameworks. From a global investor perspective, there could be a number of scenarios and variables to study. We take the example of the Indian stock market for the sake of understanding.

The stocks which have given the highest capital gain between 2003 and 2013 haven’t necessarily given the best dividend yield

The same is vice versa true for the best dividend yield companies.

Thus, while selecting the stocks within a stock market, there cannot be one common strategy, similarly, the choice of a particular stock market from a global investor perspective becomes even more complex.

While dividend yields are the more stable source of identifiable revenue for a global investor, the lack of an identifiable and verifiable benchmark analysis requires more research to ascertain the existence of correlation and the degree of the same for a particular stock market, thus, providing a more concrete analysis for the global investors to make an informed investment choice.

Through our research, we shall be providing one of the solutions to the identified problem. With the choice of the Select 30 Asia and Europe indices respectively as benchmarks, the existence of correlation with dividend payouts with the markets shall be determined as well as the degree to which the correlation exists.

Ali Ahmed, F. M. (2008). The Impact of Financing Decision, Dividend Policy, and corporate ownership on Firm Performance at Presence or absence of growth Opportunity: A Panel Data Approach Evidence from Kuala Lumpur Stock Exchange. 21st Australasian Finance and Banking Conference 2008 Paper, Pages From 1 To 22.

Amromin,Harrison,Liang and Sharpe F. M. (2005), How Did the 2003 Dividend Tax Cut Affect Stock Pricesand Corporate Payout Policy. Federal Reserve Board Academic Consultants Pages From 1 To 28.

Banerjee,Gatchev and Spindt F. M. (2003), Stock Market Liquidity and Firm Dividend Policy. EFMA 2003 Helsinki Meetings, Pages From 1 To 47.

Bulan and Subramanian F. M. (2009). A Closer Look at Dividend Omissions:Payout Policy, Investment and Financial Flexibility, Cornerstone Research and Cornerstone Research – Boston Office Pages From 1 To 55.

Demirgüneş F. M. (2015). Determinants of Target Dividend Payout Ratio: A PanelAutoregressive Distributed Lag Analysis, International Journal of Economics and FinancialIssues Pages From 1 To 9

Farinha, F. M. (2002). Dividend Policy, Corporate Governance and the Managerial Entrenchment Hypothesis: An Empirical Analysis , Pages 1 to 43

Ghauri, F. M. (2008). A Comparison of Dividend Policy of UK and US Banks over the Period 2003 – 2007 From Shareholder’s Point Of View. SSRN Papers, Pages From 1 To 82.

Giuli,Karmaziene and Serkeci, F. M. (2018). Common Ownership and Firm Dividend Policies. SSRN Papers, Pages From 1 To 32.

Goergen, Renneboogand and da Silva F. M. (2004). Dividend policy of German firms. A dynamic panel data analysis of partial adjustment models. ECGI – Finance Working Paper No. 45/2004, Pages From 1 To 38.

Hamza and Hassan F. M. (2017). Impact of dividend policy on shareholders wealth: acomparative study among dividend paying andnon-paying technology based firm’s in usa, International Journal of Information, Business and Management, Vol. 9, No.3, 2017, Pages From 1 To 27

Hunjra, Faisal and Khan F. M. (2017). Application of Lintner’s Dividend Model in Pakistan: Sector-Wise Analysis, NUML International Journal of Business & ManagementPages From 1 To 12

Penman and Sougiannis, F. M. (1997). A Comparison of Dividend, Cash Flow, And Earnings Approaches To Equity Valuation. Columbia Business School Research Paper Series, Pages From 1 To 68.

Savov, F. M. (2006). Dividend Changes, Signaling, and Stock Price Performance studied the post signaling performance of German Companies. Mannheim Finance Working Paper, Pages From 1 To 45.

Thirumalvalavan and Sunitha F. M. (2006), Share price behaviour around buy back and dividendannouncements in india,Indian Institute of Capital Markets 9th Capital Markets Conference Paper, Pages From 1 To 15.

Yarram, F. M. (2003). Dividend Policy of Indian Corporate Firms: An Analysis of Trends and Determinants. National Stock Exchange (NSE) Research Initiative Paper No. 19, Pages From 1 To 47.

investopedia.com, February 2019

http://www.finra.org/investors/how-companies-use-their-cash-dividends, February 2019

https://money.usnews.com/investing/dividends/articles/2018-01-22/why-foreign-stocks-may-not-be-best-for-dividends, February 2019