Florin PUCHEANU, Ruxandra DINULESCU and Alexandru-Mihai BUGHEANU

Bucharest University of Economic Studies, Bucharest, Romania

Volume 2022,

Article ID 551530,

Journal of Financial Studies and Research,

pages,

DOI: 10.5171/2022.551530

Received date: 16 September 2021; Accepted date: 19 January 2022; Published date: 4 March 2022

Academic Editor: Oana Vlăduţ

Cite this Article as:

Florin PUCHEANU, Ruxandra DINULESCU and Alexandru-Mihai BUGHEANU (2022)," ”The evolution of Financial Wealth and Net-Worth during Covid-19 Pandemic Case Study: Romania", Journal of Financial Studies & Research, Vol. 2022 (2022), Article ID 551530, DOI: 10.5171/2022.551530

The current study’s goal is to examine the influence of the corona-virus outbreak on economic goals and personal finances for Romanian consumers. This article also compares Romanians’ reaction capabilities in the present health crisis to the economic collapse of 2007-2008. The primary findings of this study include the notion that Romanians’ ability to cope with severe financial shocks has improved significantly since the previous financial crisis. Furthermore, this study conducts research on the net worth of the Romanian people, as well as consumer preferences for various types of assets and financial instruments. The current paper gives an insight into the Romanian consumer’s approach to dealing with financial prosperity and stability following pandemics.

In the current economic climate, which is strongly influenced by the COVID-19 pandemic, the global financial wealth undergoes extensive adjustments all over the world.

The worldwide economy, as well as the Romanian one, starts to reopen and recover after months of lock-down and extensive restrictions. Under these conditions, the consumers are starting to face new opportunities and challenges in terms of money management.

This issue is highly relevant for consumers due to the long-term financial consequences of their decisions.

Specifically, the level of systemic risks to financial stability in our country remains significant, comparable to international dynamics. In addition, the outlook for future economic activity continues to be marked by uncertainty, fueled mainly by the multitude of effects associated with the COVID-19 pandemic. Fortunately, the measures to support the economy, as well as the relaxation of restrictions on social distancing, have positively reduced the negative effects caused by the health and sanitary situation.

The evolution of the Romanian economy in 2020 was marked by the emergence of the COVID-19 pandemic outbreak and the adoption of various measures to restrict the individuals’ mobility. All the measures were considered necessary by the public authorities to prevent the spread of the disease.

From May 2020, these restrictions began to be gradually lifted, some of which were reinstated during the second and third waves of pandemic, but the measures were no longer as severe as those applied during the initial period.

One of the most significant current discussions in the field of financial wealth refers to what happened during the pandemic period with the financial stability of the Romanian consumers.

Moreover, the start of the Romanian vaccination campaign in December 2020 created the premises for an accelerated recovery of economic activities. According to a study conducted by the National Bank of Romania (2021), Romania’s economy contracted by 3.9 percent in 2020, the most significant decrease in annual terms, respectively 10 percent compared to the same quarter of 2019. Nevertheless, the European Commission estimates that the Romanian economy is expected to grow by 7.4% in 2021, followed by an advance of 4.9% in 2022.

For the year 2021, Romania estimates one of the highest values of the GDP growth compared to other European countries (Bulgaria – 4.6%, Denmark – 3%, Croatia – 5.4%, Hungary – 6.3%, Poland – 4.8%, Sweden – 4.6%, Germany – 3.6%, France – 6%, Italy – 5%, etc).

On the other hand, several segments of the working population in Romania were affected harder than others, and the negative effects continue even after most of the restrictions were removed.

The novelty of this study can be summed up as follows:

Presenting the overall financial situation of Romanian consumers during the COVID-19 outbreak;

Analyzing the users’ perspective regarding the financial wealth after the pandemic.

Literature Review

The worldwide markets encountered a series of harmful effects due to the occurrence of COVID-19 pandemic (Naeem et al., 2021), which is thought to be one of the most significant economic shocks in history (Insaidoo et al., 2021). Generally, Xu (2021) noticed an adverse reaction of a rise in the COVID-19 cases on the financial market. Furthermore, the European financial markets were considered to be a victim of the pandemics, in comparison to other countries (Youssef et al., 2021). Also, almost all territories felt the pandemic insecurity through small returns and intense market volatility (Szczygielski et al., 2021b). What is more, the lack of security caused by the COVID-19 outbreak and the rapidity with which the novel coronavirus diffused worldwide produced a panic reaction for the international financial markets (Lo et. al., 2021).

In other words, according to Zhang and Hamori (2021), the effects of the pandemics on the volatility of the oil and stock markets surpassed that of the 2008 global financial crisis.

A considerable amount of literature has been published on the topic of financial wealth and net-worth. In general, financial well-being is defined as total wealth, excluding real estate assets such as real estate, consumer durables, liabilities, non-monetary gold, and other metals, held by adult individuals.

According to the research on Global Wealth from Boston Consulting Group (2021), the financial well-being of Romanians increased in 2020 by 9% compared to 2019. Comparatively, it is 4% faster than Western Europe, but 12% slower than Eastern Europe, which also includes the Baltic States and Russia.

The data in the report show that the allocation of Romanian assets is characterized by a strong increase in life insurance and pensions. In contrast, the proportion of stocks is much lower than the global level or in other parts of Eastern Europe. Correspondingly, the percentage of cash and low-risk deposits is well below the Eastern European average.

Furthermore, the report shows that, in 2020, many clients using wealth management services have chosen alternative investments in the pursuit of better returns, to the detriment of low-yield bonds.

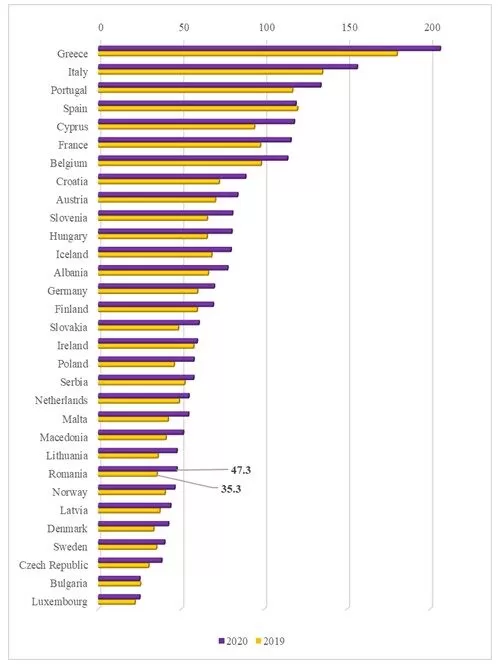

The measures taken during the global pandemic to support the economy were significant. The International Monetary Fund estimated a total amount of global measures in June 2020 worth approximately $ 10.7 trillion (about 13 percent of global GDP) (European Commission, 2021). The graphic representation of the situation is presented in Figure 1.

Figure 1: Public debt for countries of the European Union (% of GDP).

Comparison between 2019 and 2020

Source: Authors’ adaptation from European Commission, 2021

As the National Bank of Romania (2021) pointed out, Romanian’s savings in banks and deposits are growing in the pandemic time, while overall loans are declining. The increase in the value of deposits was due to the introduction of restrictive measures on the circulation of individuals and store closing.

By the same token, The Romanian Institute for Evaluation and Strategy (IRES) (2021) confirms based on their research that almost half of the Romanians were concerned in the first year of the pandemic about their own financial situation or that of their family.

While almost a third (31%) of the study participants said that they spent more during this period, a quarter say they spent less. With this in mind, 23% of the respondents managed to make higher savings than before the pandemic, while 33% saved less or not at all. Furthermore, the survey data also show that if the respondents would dispose of a large amount of money:

28% of the Romanians would invest in their own education or that of family members;

23% of the respondents would deposit money in the bank in a form of deposit;

16% of the respondents would have entrepreneurial initiatives;

10% of the respondents would buy foreign currency;

9% of the respondents would keep the money cash;

14% of the respondents were undecided.

The increasing interest in the topic of financial wealth has heightened the need for research on the area of population resistance to economic shocks. For this reason, this paper is important in the context of the COVID-19 pandemic both from a macroeconomic point of view and from the perspective of financial stability. In addition, households’ ability to cope with the shock affects the extent to which consumption will decrease and the likelihood of borrowers falling behind.

To clarify the issue, consumers’ resistance is defined as the amount of disposable income remaining available to the population after covering all family debts and covering the subsistence expenses.

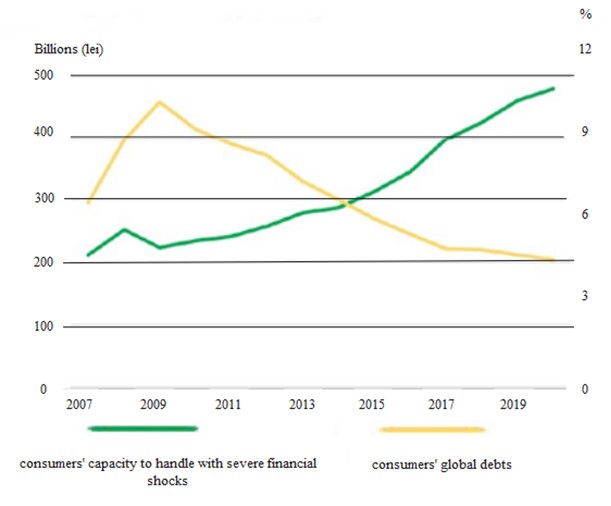

With this in mind, Figure 2 presents a graphical representation of the consumers’ ability to cope with the new sanitary crisis.

Figure 2: Consumers’ ability to cope with the new sanitary crisis.

Comparison with the financial crisis from 2007.

Source: Authors’ adaptation from The Romanian Institute for Evaluation and Strategy (IRES), 2021, and the National Bank of Romania, 2021.

As can be seen from Figure 2, the resilience of the Romanian population has improved considerably compared to the situation before the financial crisis of 2007-2008. Equally important, the percentage of consumer debt has decreased. These dynamics suggest a robust evolution of the individuals’ financial wealth.

When discussing the real estate assets, the analysis included only the estate assets. Secondly, the total net-worth represents the difference between financial assets and financial debts/liabilities.

Gold Vs Bitcoin as Store of Value/ Haven

Gold has been for thousands of years not only a traditional store of value or medium of exchange in the economy, but also, historically, one of the most reliable safe havens in times of economic distress, no matter what the reason of the crises presented to humanity, or the overall social climate. Regardless of the way in which it has been presented and analyzed in the scientific literature, either as a safe haven (Baur & McDermott, 2010) or as a hedge for the US dollar (Joy, 2011), stocks (Beckmann, Berger.T., & Czudaj, 2015), oil (Reboredo, 2013) or inflation (VanHoang, Lahiani, & Heller, 2016), the role played by gold in protecting peoples’ wealth from geopolitical risks is undoubtedly a major one.

A considerable number of studies have analyzed from different perspectives gold’s behavior during the 2007-2008 recession and the period after, to extract insights about its reactions and influence on people’s wealth during turbulent economic times. Related to the above-mentioned period, the most intriguing inverse correlation was between gold and real estate valuations, which was one of the most affected metrics regarding portfolios across the developed world. While the prices of real estate across the world were plummeting, cutting deep into people’s wealth, the gold’s price registered a boom, acting as a counterbalance for ravaged portfolios (Yunus, 2020).

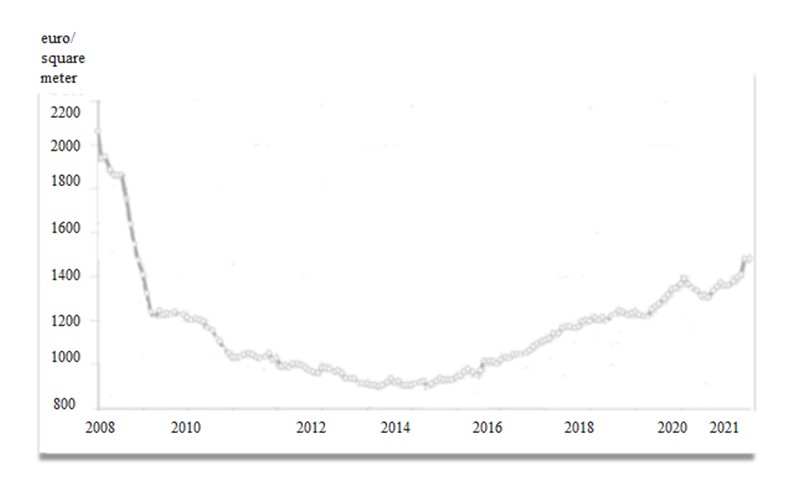

Figure 3. Real estate index (euro/square meter) for Romania

Source: Authors’ adaptation from Realmedia Network, 2021.

Figure 3 suggestively depicts the sharp decline in real estate valuations in Romania, between the arrival of the financial crisis wave in Europe, in the spring of 2008 and the end of 2013, which is considered the start of the recovery. During this interval, the price fell from a maximum of 2058 euro/square meter in March 2008 to a minimum of 903 euro/square meter in October 2013, equivalent to a reduction of 56% in the average price of real estate properties owned by Romanians.

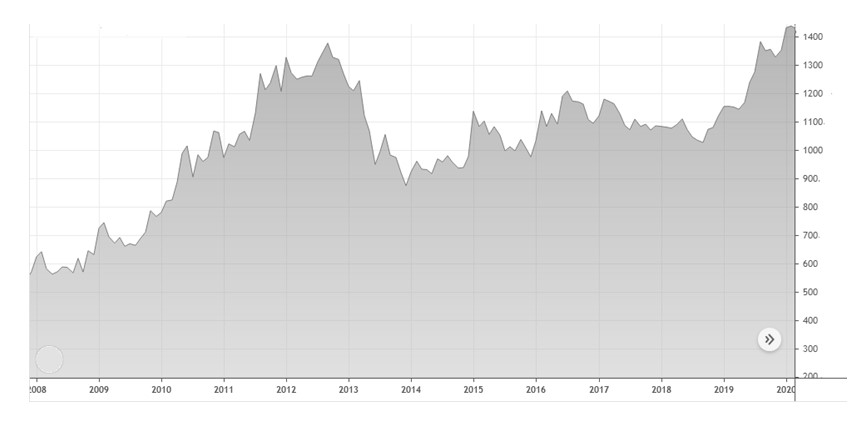

Figure 4. Gold price (euro/ounce) during the 2008 financial crisis and after

Source: Authors’ adaptation from TradingView, 2021.

On the other hand, as shown in Figure 4, during roughly the same interval, gold registered an increase from 580 euro/ounce in March 2008 to 1375 euro/ounce in September 2012, gaining more than 136 % in value. This explosive increase confirms gold as a reliable safe haven for the given interval, efficiently protecting from losses the investors who diversified their portfolios in the direction of owning enough precious metal to offset the substantial losses on the housing market.

For the purpose of this study and discussion, when looking at the economic recession that started in 2008 and the ways different portfolio structures might have reacted to the volatility in the markets and protected people’s wealth, Bitcoin is not a relevant topic of analysis, as it was still in its infancy. Both its valuation and adoption were negligible at the start, and for the most part of the downturn caused by the housing market bubble in the United States, so its weight on people’s portfolios was too limited to count for any kind of analysis. Nevertheless, the financial crunch mentioned before is viewed by most of the financial analysts as the turning point that originated and legitimated Bitcoin in particular and cryptocurrencies in general. This new financial and investment paradigm is presented as a new instrument for diversifying portfolios to make them more crisis-proof, generating more long-term resilience through its decentralized architecture and facilitating a higher degree of fairness in the redistribution of wealth. Bitcoin is, at the moment of its inception, featured as a valuable new tool to fight uncertainty and generate wealth, effectively diversifying portfolios, thus being labeled as “digital gold”.

The Covid 19 sanitary crisis that started in spring 2020 in Europe brought a very different set of challenges for governments and society as a whole, but the extreme uncertainty and volatility characteristic of any other major shock in human history were just as prevalent. On top of major health issues, societies had to manage a whole range of financial and economic adverse effects, generated by an induced and sharp shutdown of the world economies, at a scale never experienced before.

In the real estate market, the initial shock of lockdown weighted significantly on the valuations of properties, with a drop in prices of around 7% over an interval of six months since the start of the pandemic. After this drop, due to structural changes in demand towards bigger properties and especially individual houses with gardens, prompted by the quarantine pressure, the prices started climbing again, so overall, at the scale of the Romanian market, the real estate portfolios were not significantly affected by the pandemic. Nevertheless, a different story was unfolding in the rents market, which is an important revenue segment for investors’ portfolios mix, being a key metric, which investors use to evaluate the rentability of real estate.

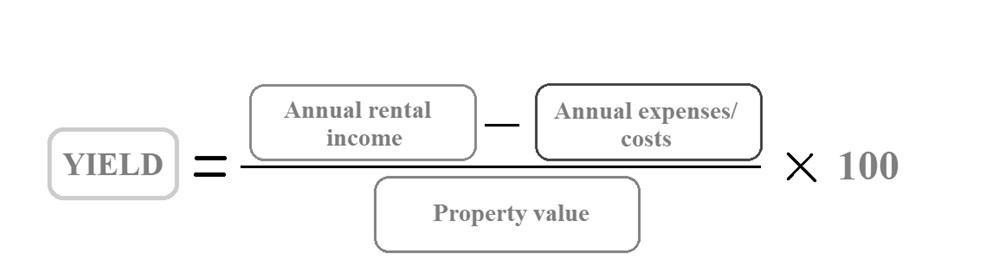

Figure 5. Real estate yield formula

Source: The Authors

In Romania, more specifically in Bucharest, before the pandemics, the range prices of houses and apartments was from around 950 euros per square meter, to 1950 euros.

This pointed out good rental yields, between 6% and 8% (the mentioned values are applied for well-maintained apartments).

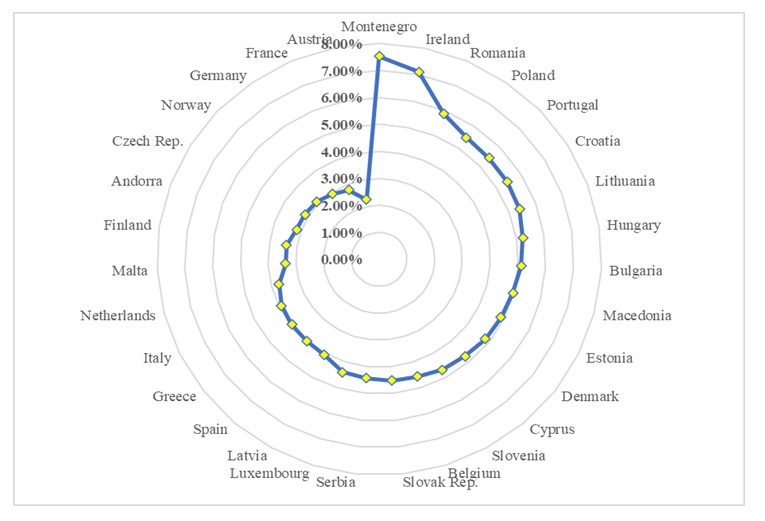

Figure 6 presents a situation of European countries (for its capitals), regarding the gross rental yield (expressed in percentage per year):

Figure 6. European countries compared after the gross rental yield

Source: Authors’ adaptation from Global Property Guide, 2021.

Before the pandemics, the gross rental yield varied between 2,25 % – the lowest value being in Austria, with a very poor gross rental rating – and 7,09% – the highest value being in Ireland, with a good yield rating.

In 2019, Romania had one of the best gross rental yields, compared to other European countries, with 5,88% per year.

Romania’s house prices continue to rise, even though at a slower pace, among a struggling economy due to the pandemic. During 2020, the average selling price of apartments in Romania rose modestly by 2.44% y-o-y (0.95% inflation-adjusted) to €1,371 (US$ 1,662) per square meter, a sharp slowdown from an annual growth of 8.23% in 2019.

In the first quarter of 2020, prior to lockdown, selling prices for residential properties in Romania registered an 8.1% increase, compared to the same period of 2019. This growth margin was above the European Union recorded average (+ 5.5%), but also above the Euro zone (+5%).

Another negative influence on people’s wealth is represented by inflation, which picked up quite significantly during the Covid pandemic, and continues to have an accelerated ascending tendency. During one year of official pandemic, the inflation doubled in Romania, from 1,1 % in T1 2020 to 2,0 % in T1 2021, on a background of global scale inflationary environment, having as probable main cause a shortage of raw materials and other essential products due to disruptions in the global supply chains. Another reason for the sustained increase in inflation is the big amount of money spent by the state to support affected segments of the economy, which increased the overall supply of money in the economy.

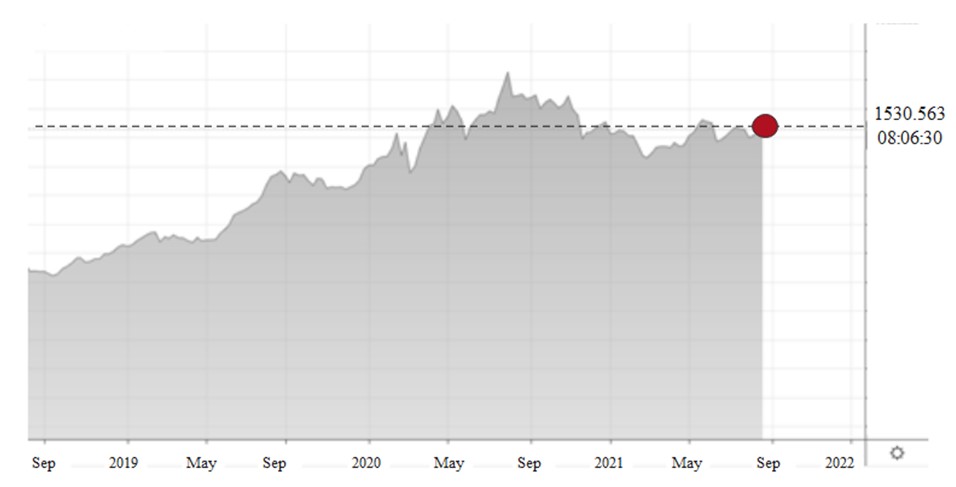

Compared to the evolution in the 2007-2008 crisis, this time gold had an obviously less meaningful appreciation in value, thus failing for the moment to shield portfolios from the economical adverse effects of the pandemic. The precious metal went from 1375 euro/ounce in spring 2020, when the adverse effects of the sanitary crisis started to be visible in the economy and society, to a maximum of 1730 euro/ounce in August 2020, an increase in value a little above 25%. After reaching this temporary peak, gold started going down to a level of 1429 euro/ounce in March 2021, losing around 18% of its value, although the incertitude and negative influence of lockdowns on the economy was still in full swing.

Figure 7. Gold price (euro/ounce) during the Covid 19 pandemic

Source: Authors’ adaptation from TradingView, 2021.

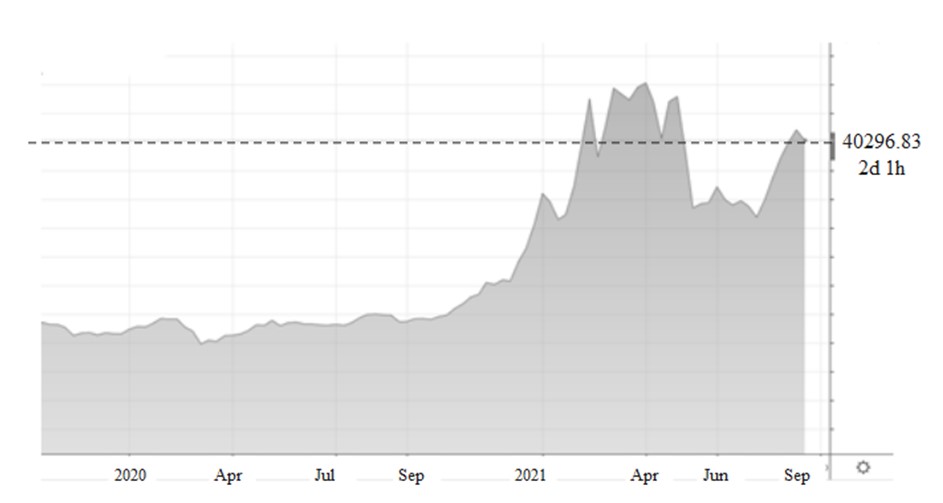

During this time, Bitcoin had a much more different behavior compared to Gold. Between March 2020, when it was quoted at 5000 euro, and August 2020, it doubled in price, reaching around 10.000 euro. At this moment, when gold started going down, Bitcoin took another quantum leap, straight to 50.000 euro by March 2021, for a staggering 1000% increase compared to the moment the sanitary crisis and lockdowns started in Europe.

Figure 8. Bitcoin price during the Covid 19 pandemic

Source: Authors’ adaptation from TradingView, 2021.

Even taking into consideration the extreme volatility in cryptocurrencies market, and certain risks that the investors might be exposed to, Bitcoin registered a much more significant adoption rate in investing portfolios compared to the 2007-2008 crisis. This, coupled with the extraordinary evolution in price during this turbulent economic environment, lead to a much better protection for the investors who diversified their portfolios into Bitcoin, confirming once again that the so called “digital gold” is not an unrealistic label, at least for the moment.

Methodology Research

In support of this research, we have gathered a sample of 1137 respondents which were asked to answer 4 questions from a survey. Thus, the research was based on a quantitative study, rather than a qualitative one.

The data gathered for this study were made through an online survey, sent on Facebook groups which had as a main theme the financial wealth. The survey was accessible for 2 months, from June to August.

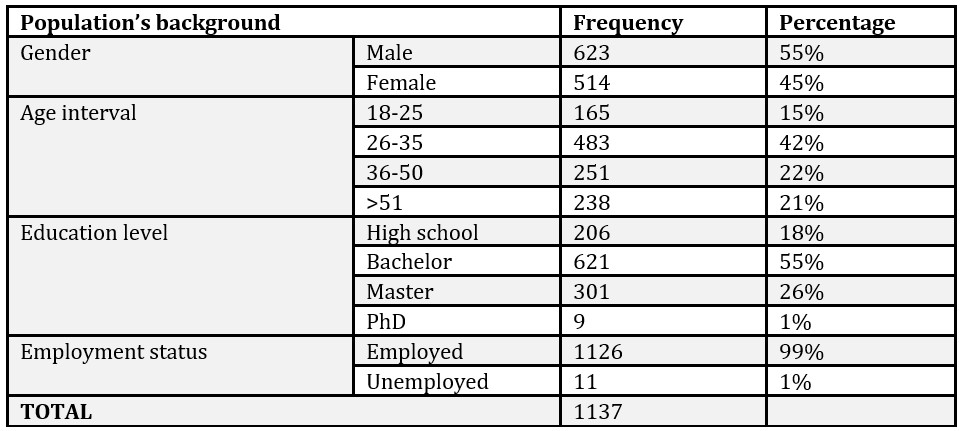

The descriptive statistics of the population’s background was the following:

Table 1. Population of the study

Source: The Authors

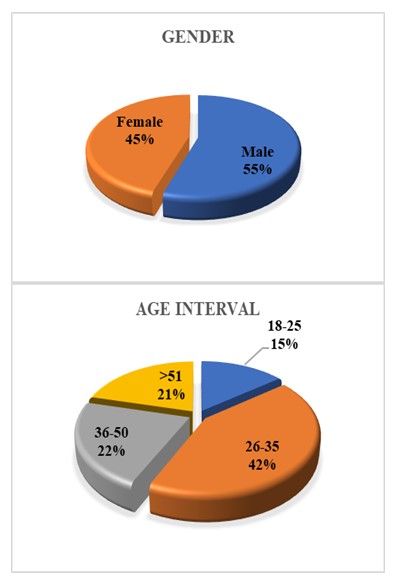

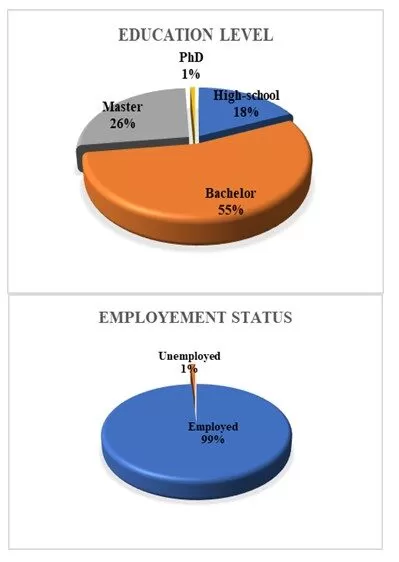

From the table above, we can observe that most of our participants were males (55%), the main age interval was between 26 years old and 35 years old (42%), most of them had their bachelor’s degree (55%) and the majority was currently employed (99%).

Figure 9. Gender and age interval of the respondents

Source: The Authors

Figure 10. Education level and employment status of the respondents

Source: The Authors

The survey consisted of the following 4 questions (besides the demographic questions related to age, gender, etc):

Q1: Do you think your financial wealth has been affected because of the pandemic?

Q2: Do you currently invest in cryptocurrencies?

Q3: Do you invest more in different markets once the pandemic started?

Q4: Do you have another source of incoming (e.g., stocks, mutual funds, cryptocurrencies, etc) besides the current job?

Based on the answers received from the participants to our study, we were able to interpret, in a certain manner, the Romanian investors’ behavior.

Results

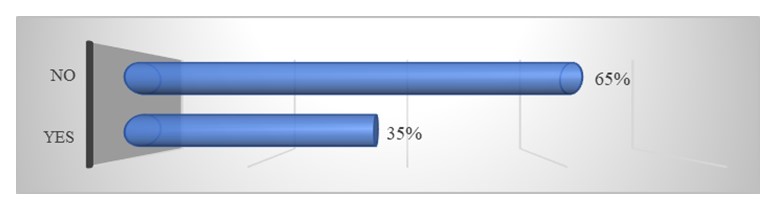

The results from the survey indicated that most of the Romanian users were not very affected by the effects of the pandemic, at least not from a financial point of view.

Figure 11 presents the results from Question no.1. Regarding how the pandemic affected the level of financial health for individuals, 65% answered that the financial health wasn’t affected by the COVID-19 financial effects, while 35% affirmed that the pandemic affected their financial health.

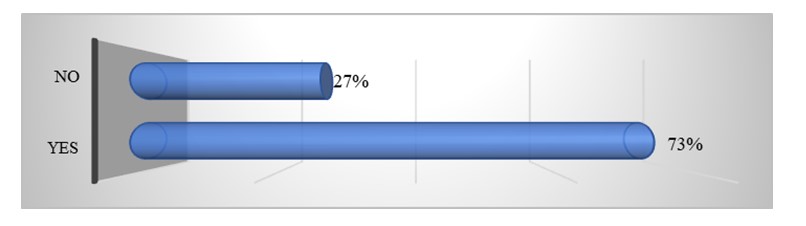

During the lock-down many people turned their thoughts to the cryptocurrency market. Therefore, we wanted to know how many were involved in this market during the COVID-19 pandemic. As a result, we have 73% of the participants who invest in cryptocurrency, while 27% prefer to avoid this market.

We consider that the pandemic has changed the individuals’ vision regarding the financial wealth. When the initial jobs, the traditional ones, could have been shaken by the pandemic’s effects, people tried to find different financial alternatives to survive the pandemic. As a result, for most of them, the cryptocurrency market represented a viable option.

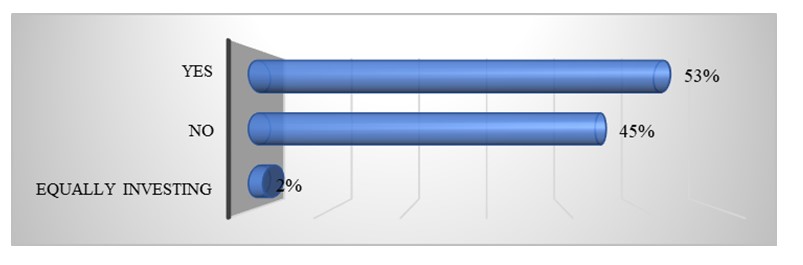

Question no. 3 also presents the fact that people turned their attention to various financial markets. In this case, 53% stated that they invest in different financial markets once the pandemic started, 45% affirmed that they didn’t invest in other financial markets, while 2% affirmed that the investing manner did not change once the pandemic started.

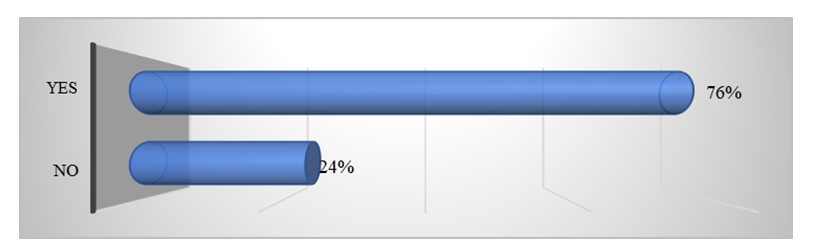

Question no. 4 presents how the investment behavior changed once the pandemic arrived. People feared losing their jobs, so, consequently, they ensure another source of income, just in case they would have to give up their current employee. Thus, 76% of our respondents affirmed that they have another source of income, while only 24% affirmed that they kept their current job as a unique employee.

The current crisis has shown, more than before, the need for a change in the structure of personal savings and investments.

In conclusion, it is necessary to monitor the evolution of the macro-financial framework and the implementation by the authorities of the necessary measures. Thus, the objective involves achieving an adequate and balanced mix of economic policies, able to reduce both structural vulnerabilities and the negative effects generated by the current pandemic.

In conclusion, the consumers’ ability to cope with severe financial shocks has improved considerably compared to the situation before the previous crisis, both in terms of holding real estate assets, but especially on the one of financial assets, the latter category conferring a higher degree of liquidity in the context of unforeseen situations.

The present study represents ongoing research, because, unfortunately, the pandemic is still not over. The economy had a chance to reborn during the summer period, but the autumn of 2021 brings with it the so-called “4th wave” of the COVID-19 pandemic, which will destabilize once again the worldwide economy.

Acknowledgment

“This paper was co-financed by The Bucharest University of Economic Studies during the PhD program”.

Baur, D. & McDermott, T. (2010), Is gold a safe haven? International evidence. Journal of Banking & Finance, 34(8), 1886-1898.

Beckmann, J., Berger.T., & Czudaj, R. (2015), Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling, 48, 16-24.

Boston Consulting Group, 2021. Global Wealth 2021, l.: s.n.

Dayong, Z., Min Hu, Q. J. (2020), Financial markets under the global pandemic of COVID-19. Finance Research Letters, vol. 36. https://doi.org/10.1016/j.frl.2020.101528.

European Commission, 2021. General government gross debt – quarterly data. [Online] Available at: https://ec.europa.eu/eurostat/databrowser/view/teina230/default/table?lang=en [Accessed 28 07 2021].

Global Property Guide. (2021). Global Property Guide. Retrieved 07 28, 2021, from https://www.globalpropertyguide.com/rental-yields

Lo, G.D., Basséne, T., Séne, B. (2021), COVID-19 And the african financial markets: Less infection, less economic

impact, Finance Research Letters. https://doi.org/10.1016/j.frl.2021.102148

Insaidoo, M., Lilian A., Samuel A., and Francis K.A. (2021), Stock market performance and COVID-19 pandemic: Evidence from a developing economy. Journal of Chinese Economic and Foreign Trade Studies14(1), 60–73.

Naeem, M.A., Sehrish, S., Costa, M.D. (2021). COVID-19 pandemic and connectedness across financial markets. Pacific Accounting Review, 33(2), 165-178.

National Bank of Romania, 2021. Financial Stability Report June 2021, Bucharest: National Bank of Romania.

Reboredo, J. (2013), Is gold a hedge or safe haven against oil price movements? Resources Policy, 38 (2), 130-137.

Szczygielski, J.J., Bwanya, P.R., Charteris, A.,Brzeszczyński, J. (2021), The only certainty is uncertainty: An analysis of the impact of COVID-19 uncertainty on regional stock markets. Finance Research Letters. https://doi.org/10.1016/j.frl.2021.101945.

The Romanian Institute for Evaluation and Strategy (IRES). (2021), The impact of Covid-19 on the quality of life of romanians, Bucharest: S.C. INSTITUTUL ROMÂN PENTRU EVALUARE ŞI STRATEGIE (I.R.E.S.) S.R.L.

VanHoang, T., Lahiani, A., & Heller, D. (2016), Is gold a hedge against inflation? New evidence from a nonlinear ARDL approach. Economic Modelling, 54, 54-66.

Xu, L. (2021), Stock Return and the COVID-19 pandemic: Evidence from Canada and the US, Finance Research Letters, Volume 38. https://doi.org/10.1016/j.frl.2020.101872

Youssef, M., Mokni, K. &Ajmi, A.N. (2021), Dynamic connectedness between stock markets in the presence of the COVID-19 pandemic: does economic policy uncertainty matter? Financial Innovation7(13) https://doi.org/10.1186/s40854-021-00227-3

Yunus, N. (2020), Time-varying linkages among gold, stocks, bonds and real estate. The Quarterly Review of Economics and Finance, 77, 165-185.