The General Framework of the Corporate Governance Codes for the G20 & 25 European Countries: An Overview on Corporate Governance of Bucharest Stock Exchange

Doctoral School of Finance, Bucharest University of Economic Studies, Bucharest, Romania

Volume 2023,

Article ID 488942,

Journal of Financial Studies and Research,

19 pages,

DOI: 10.5171/2023.488942

Received date: 9 September 2022; Accepted date: 9 March 2023; Published date: 25 April 2023

Academic Editor: Raluca Florentina Crețu

Cite this Article as:

Ileana BOTEZ (2023)," The General Framework of the Corporate Governance Codes for the G20 & 25 European Countries: An Overview on Corporate Governance of Bucharest Stock Exchange", Journal of Financial Studies & Research, Vol. 2023 (2023), Article ID 488942,

DOI: 10.5171/2023.488942

This paper analyses the general corporate governance framework at the international level focusing on the G20 countries and 25 countries from Europe, and its evolution from the beginnings, respectively 1992. It also studies the implementation of the Corporate Governance Code of Bucharest Stock Exchange during the period 2016-2021. To have a better understanding of the historical development main stages and specific concepts for corporate governance, this paper presents the worldwide evolution of the corporate governance beginnings until today and important aspects related to the content of the most relevant economies’ and capital markets’ corporate governance codes. In this context, the present paper contributes to the relevant literature by examining recent data for most developed countries worldwide and Romania for the mentioned six years, respectively the companies listed on the Premium tier on the Bucharest Stock Exchange since the implementation of the new Corporate Governance Code in 2016. A significative element will be emphasized within the study regarding the key role of the Board of Directors as the essence of the corporate governance for creating and protecting the value of a company.

Keywords: corporate governance code, board of directors, Bucharest Stock Exchange.

Introduction

Short history about the origins of the central concept of corporate governance, Board of Directors

According to the King IV Report on Corporate Governance for South Africa, “Corporate governance is defined as the exercise of ethical and effective leadership by the governing body towards the achievement of the following governance outcomes: ethical culture, good performance, effective control and legitimacy” (2016). The origins of the corporate Board of Directors as the central business governance structures are in Europe beginning with the fourteenth century from where the concept was spread around the world (Gevurtz, 2004). Different approaches were developed by countries in terms of Board type models from two-tier to single-tier (Andre, Jr 1996) or to other ones related to elections by shareholders (Hopt, 1984), involvement of stakeholders versus shareholders (Bradley et al. 1999) or minority versus dominant shareholders (Cheffins, 2000). The first beginnings (Gevurtz, 2004) were identified in 1313 and 1363 with the setting-up of the Company of the Merchants of the Staple of England, and in 1505 and in 1654 with the Company of Merchant Adventurers of London. They were followed in the sixteenth and seventeenth centuries by the foreign trade English companies’ set-up by the Queen Elisabeth I, like Russia Company as the first joint stock company (1555), Eastland Company (1579), Levant Company (1581, 1592 and 1605), East India Company (1599), Hudson’s Bay Company (1670), Massachusetts Bay Company (1628) and South Sea Company (1711). Having the purpose of trade and colonization in North America, London Company (later called Virginia Company), which was set-up in 1606 by King James I, was given the right to plant a colony between 34th and 41st parallels and Plymouth Company between the 38th and 45th parallels. Both companies had a local resident council in England for “superior management and direction” (Davis, 1904). According to Franklin A. Gevurtz, “…the essence of the corporate board of directors comes from three underlying concepts which involve the relationship of the directors to the shareholders, the relationship of the directors to each other, and the relationships of the directors to the corporation’s executives” (2004). All the charters of the above-mentioned companies provided different types of councils and structures. The first time when the institution of board member is used as a new concept relates to the by-laws of Bank of England in 1694 (Formoy, 1912) where the board was composed of 24 members out of which a third could had been reelected, and the chairman was elected by the shareholders (O’Donnell, 1952). Another representative example is the charter of the First Bank of the United States from 1791 which provided the annual election of 25 board members out of which a quarter could had been reelected and the Chairman was elected by Board members. This governance structure was considered to reflect the tendencies of former colonies to copy them from European institutions (Gevurtz, 2004). Nowadays most of the leading structures of a company continue to follow the same main benchmark as in the past.

Highlights of the corporate governance regulations evolution worldwide

Toba Beta, an Indonesian reputed writer and an economist, affirmed that “Good corporate governance, it’s about being proper and prosper”, a statement which most probably represents the core of the corporate governance. From Cadbury Report issued in December 1992 which addressed the financial aspects of corporate governance and was a model for the development of different codes in the United States, the European Union, and other countries, focusing on voluntary adoption and “comply or explain” principle to Sarbanes-Oxley Act in 2002, legal act approved by the American Congress to protect the shareholders and the public in general, the legal framework improved considerably in the last decades. The main triggers were different situations that determined the authorities to improve the regulations. Since then, a multitude of codes and guidelines were published and became a popular means to increase the accountability of the corporations (Mallin, 2013). In addition to these, the Organization for Economic Co-operation, and Development (OECD) published a series of principles in 1999 and 2004 which have become an international benchmark for all the involved actors in corporate governance. In November 2015, the third edition was endorsed as the G20/OECD Principles of Corporate Governance. The six main directions of actions regard ensuring the basis for an effective corporate governance framework, rights and equitable treatment of the shareholders, and key ownership functions, institutional investors, stock markets and other intermediaries, the role of stakeholders, disclosure and transparency, and the responsibilities of the board. (G20/OECD, 2015).

Directions for global corporate governance future

The increasing role of a good corporate governance continues to spread around the world and to guide the implementation of best practices with a scope to create and protect the value based on its fundamental tool, the board of directors. It is important that the previous corporate scandals in the last three decades do not occur again and to produce the question “Where were the directors?”. In the current 21st-century digital environment, the Board is called to cope with volatility, uncertainty, complexity, and ambiguity (VUCA concept). The “four Ds” as diversity, disclosure, data, and development of financial institutions will represent the main changes and challenges for the whole society until 2030 (Nestor, 2019). Diversity is going to generate structural impact and most probably will accelerate the phenomenon to bring different voices around the board tables to face decisions’ challenges due to the increase of the complexity of the business. Disclosure is included especially within the corporate governance codes which contribute to the increase of the quality of transparency for the companies as a best practice requirement for boards’ activity. The third D, data are considered the driving force for the other Ds and their availability will intervene on the Board’s way of work. The fourth D, development of financial institutions will be used as factor of changing for the frontier and emerging markets. (Nestor, 2018)

The purpose of the present paper is to conduct an international review of the key countries around the world for the Corporate Governance Codes with a closer look at the Bucharest Stock Exchange New Corporate Governance Code and its implementation. The author contributes to the growing literature by analyzing the current codes of the 44 countries to provide a map for future research on their implementation.

Literature Review

The changes of the European Union legislation determine the need to frequently align the corporate governance codes. Besides this reason, the constant development of best practices can be another explanation (ecoDa & Mazars, 2018). Corporate governance codes can be drawn up at three levels: international, national, and individual firm level (Cuomo et al, 2015). Currently, 110 countries issued Codes, Guidelines or Principles which apply to listed or non-listed companies, where the government is a shareholder, institutional investors, investment companies, business families, asset managers or other types of legal entities (ICGI, 2021). Between 2016-2021, 51 countries modified their Codes which shows a lot of interest for the corporate governance best practices to be enforced locally. Some of them amended more than once their Codes like the USA and Slovenia 3 times and other 12 countries 2 times (Japan, United Kingdom, New Zealand, Malaysia, Portugal, Italy, France, Germany, Philippines, Norway, Austria, China). Combining hard law and soft law is more seen as a complementary way instead of an alternative one to solve corporate governance (Cuomo et al, 2015). The changes of the Codes reflected the increasing pressure from the largest investors, institutional or supra-national, the new legislation related to ESG, the interest of the public and the stakeholders. But this new approach represents a step forward to the entire eco-system dedicated to corporate governance.

An appropriate governance is considered a sustainable development factor which should follow an adequate management business practice, sustained financial performance, company increase value, responsibility to the shareholders, prevention of illegal or nonethical behavior, positive work environment, retention of employees using incentives and ESG. Sustainability and corporate governance issues are in close relationship which determine increasing market value and improving organization are the effects of the implementation of sustainability by using corporate governance practices (Jaimez-Valdez and Jacobo-Hernandez, 2016).

Corporate governance is emerging as a topic related to the implementation of sustainability because businesses are beginning to consider sustainability as a means to increase market value (Warren-Myers, 2013) and improve the organization in general (Klettner, Clarke, & Boersma, 2014) in addition to reducing operating costs and increasing profits (Lacy & Hayward, 2011).

To have an overview of the perspective of the most prominent countries of the world regarding the corporate governance principles, the author analyzed G20 countries and 25 countries of Europe in terms of codes published and implemented with a focus on the current codes. It is important to mention that in 2021, G20 countries represent 77.3% of the world GDP (96.1 trillion USD), 75% of the global foreign trade (21.38 trillion USD) and 60% of the world population (G20, 2021).

Methodological approach and findings

The analysis will target 6 main aspects for the Corporate Governance Codes (CGC) of G20 and 25 European countries which cover title, content, topics approach, preparation, application, and principles as shows figure 1 below (ECGI, 2021). This will permit a detailed look at these documents to understand better the whole environment of the Codes. The data were collected from the 44 current Codes of the countries analyzed and structured per each category of information.

Fig 1. 6 main aspects for CGC

Evolution of the Corporate Governance Codes by G20 countries without the European Union

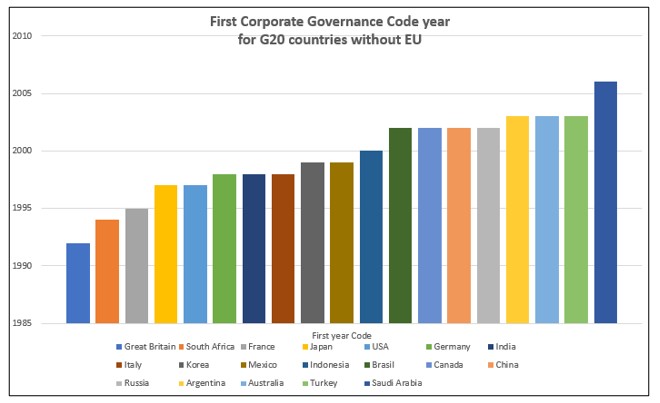

The author analyzed detailed information about the corporate governance codes issued by the countries from G20 without the EU. The details were included in a large database comprised of country, stock exchange, title of the code, year of the first and last codes issued, number of total issued codes, number of last code pages and the issuer of the code. In addition, the database includes details about the structure and content of the Codes analyzed. The relevant results obtained are illustrated below in the graphics and show that the topic on corporate governance mainly began in the United Kingdom in 1992 when it was issued the Cadbury Report and is the oldest Code for all the countries analyzed, not only for G20, but also for the rest of the 25 European countries analyzed in the next section. It is followed by South Africa in 1994, France in 1995, Japan and the USA in 1997.

Fig 2. First CGC year for G20 countries without the EU

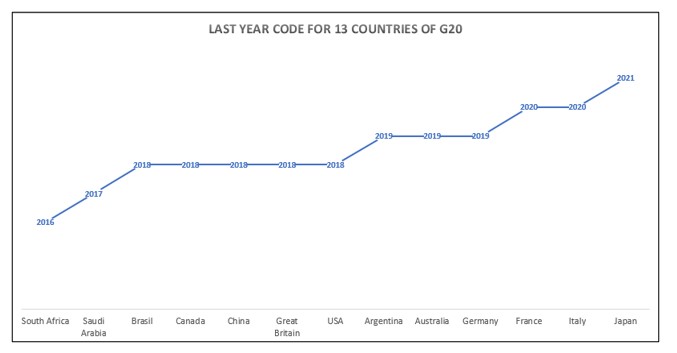

Significative elements that could be underlined based on the analysis are related to the fact that 13 countries out of 19 amended the Codes during 2016 and 2021 which indicate the importance of this topic as presented in the below graphic.

Fig 3. Last year CGC for 13 countries of G20

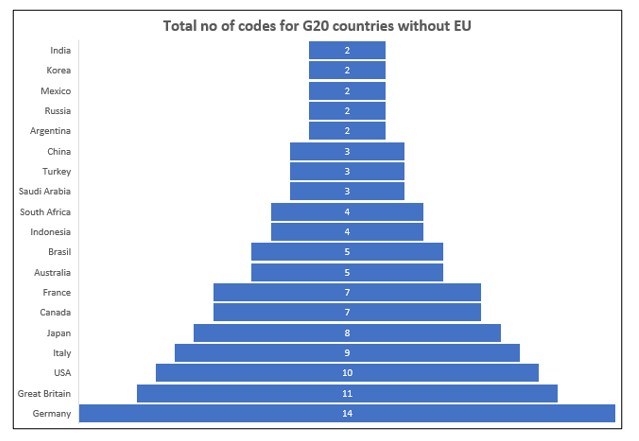

In fact, looking at the number of codes issued by these countries the author found that top 5 is formed by Germany with 14 codes, the United Kingdom with 11, followed by the USA with 10, Italy with 9 and Japan with 8 as indicated by the graphic presented below and an average of 5 codes per country.

Fig. 4. Total number of CGC for G20 countries without the EU

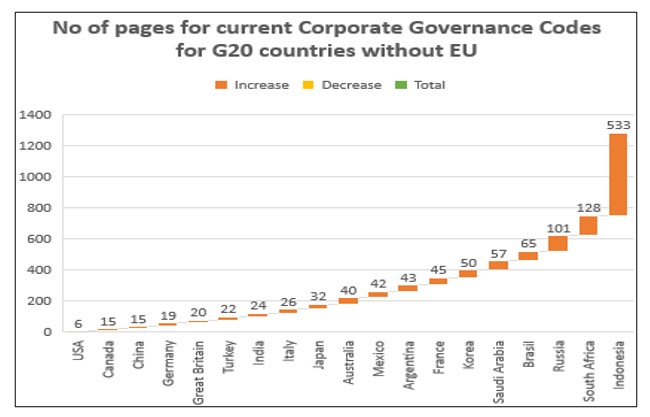

About the volume of provisions included in the codes, the author remarked 3 codes which are extended versions and are coming from Indonesia with 533 pages (2014), followed by South Africa with 128 pages (2016) and Russia with 101 pages (2014) and an average of 67 pages per country analyzed.

Fig 5. Number of pages for current CGC for G20 countries without the EU

Below is presented the current year of the Codes for G20 countries without EU countries from 2003 to 2021.

Fig 6. Year of the current CGC for G20 countries without the EU

Evolution of the Corporate Governance Codes in 25 European Countries

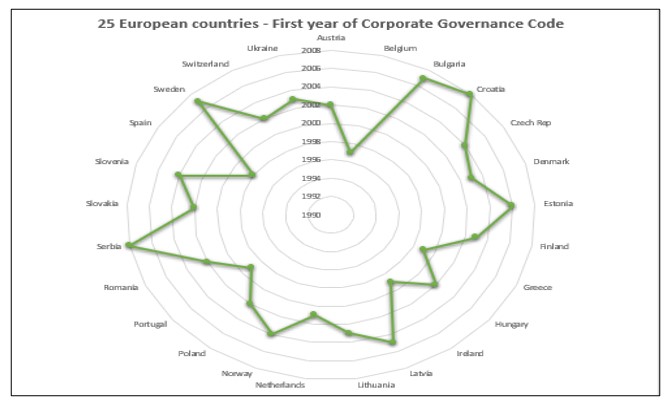

The second analysis continued with the most important European countries in terms of corporate governance topic. Looking again from the same perspective as the previous analysis, the author observed that most of the largest capital markets are represented in the results obtained. Top 5 countries include Belgium which issued the first code in 1997, followed by Spain in 1998, Portugal and Ireland in 1999 and the Netherlands in 2001. Significative aspects that could be underlined are related to the fact that 16 countries out of 25 issued their amended Codes during 2016 and 2021 showing a high appreciation for this topic.

Fig 7. 25 European countries – First year of CGC

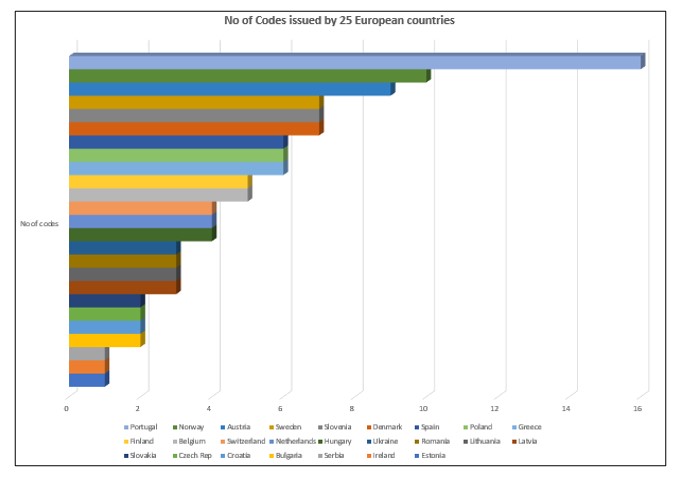

The author determined that the number of codes issued by these countries is dominated by Portugal with 16 codes, followed by Norway with 10, Austria 9 closing with Denmark, Slovenia, and Sweden 7 and an average of 4.76 codes per country.

Fig 8. Number of CGC issued by 25 European countries

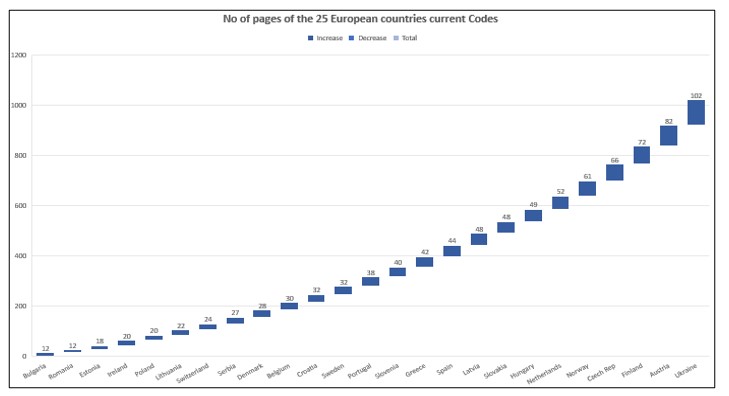

Another interesting element to be mentioned covers the volume of the provisions of the codes, where is remarked Ukraine with 102 pages, Austria with 82 pages, Finland with 72 pages, Czech Republic with 66 pages and Norway with 61 pages and an average of 40.84 pages.

Fig 9. Number of pages of the 25 European countries current CGC

Analyzing the content of the Corporate Governance Codes issued by G20 countries without the European Union and other 25 European countries

To understand better the general framework for which apply the codes issued by all these 44 countries, the author continued to analyze in a synthetic manner the main content of these codes. From the perspective of the title used for this document, 30 countries out of 44 (68%) have Codes of Corporate Governance, out of which 17 are issued at the level of the country and 5 by the stock exchanges. Looking in detail at the title of the document, 6 countries have recommendations, 5 principles, 4 best practices, 2 Guides, 1 Manual, 1 Regulation, 1 Report and 1 Administration, which shows a diverse use of terminology and different approach. The author observed that the content included 42% recommendations, 36% principles, 13% practices and the rest of the documents are comprised of rules, regulations, suggestions, instructions, clarifications, and explanations.

A closer look to the themes developed within the Codes emphasizes the core and most important aspects treated by them. The roles and responsibilities of the Boards of Directors are addressed mostly by all the codes analyzed reaching 70% as importance in the whole eco-system of a company. From the type of Boards and mandates, structure, composition, size, diversity, meetings’ frequency, committees, assessment characteristics, the Boards are the regulators in terms of effectiveness and accountability (Grant Thornton, 2017). A significant element is seen to be the rules of the Board which are necessary for a better internal organization and for the protection of investors (The Sarbanes-Oxley Act, 2002). In addition, the institution of independent directors brings quality (Pichet, 2017) and value to the Boards (Reguera-Alvarado and Bravo Urquiza, 2016) which determine an increase in the corporate reputation. Almost all countries require or recommend about a minimum number or ratio of these directors from 30% to 50% from the Board members (OECD Corporate Governance Factbook, 2019). An effective Board should follow five core principles: leadership, capability, accountability, sustainability, and integrity which will encourage an appropriate corporate culture (ecoDa and AIG, 2016).

The second topic is regarding the shareholders and the general assembly of the shareholders which is found in at least 60% of the codes’ content. This institution is the supreme one in a company where the strategy is approved, and the main directions of actions are settled. The general assembly is the link between the company’s shareholders and its Board (EBRD, 2019).

Information dissemination and transparency are seen as a key for a good corporate governance and are listed on top 3 topics approached within the codes. More than 43% of the codes are addressing it. The most important tool to achieve transparency is the current and periodic reporting which is provided by the Transparency Directive implemented by each country. This will generate appropriate behavior of the companies on the capital markets towards investors to achieve attractiveness and liquidity (EY European Commission, 2020).

Closed to the third topic in terms of importance is remuneration which reached 42% in the analyzed Codes’ provisions. Much more attention was given to the remuneration governance for board members and executives after 2008 financial crisis. An important crisis effect was the change in the financial systems to the remuneration system for directors which modified the high weight of annual bonuses targeting the short-term performance for a higher weight of those for medium- and long-term effects with a scope to widen their horizon of interest for company’s performance. Adequate measures and for many jurisdictions were taken to improve the corporate governance at the level of the board by setting up committees like the ones for nomination and remuneration (OECD Corporate Governance Factbook, 2021).

In comparison with the previous topic, the audit function works through the committee which is imposed in most countries as being independent. Higher degrees of risks impose the necessity of more independent members within the audit committee and even most of them (Bucharest Stock Exchange Corporate Governance Code, 2016). The audit role is related to all the types of audits referring to the internal, financial and informatic. The last two are outsourcing, but the reports are submitted to the Boards. In addition, the boards should take into consideration developing auditing practices which are applied by the company (The Cadbury Report, 1992).

The company’s environment reaching 24% includes, besides the shareholders, also relevant stakeholders whose role varies considerably across countries and sectors. The author identified that the rights of stakeholders in some European countries are provided by the company law. Closely related to this topic is the corporate responsibility of the company and benefit from dedicated policies (ecoDa and IFC, 2015).

The codes develop other aspects related to risk management, evaluation, committees other than the ones mentioned above depending on the extended areas of activity, reporting, ethics, conflict of interests and supervision which are treated by Codes under 22%. The Board should establish culture, values, and ethics for the company, and it must set the correct tone (Shah and Napier, 2015). Leading by example and ensuring good standards of behavior will represent models for the organization (UK Corporate Governance Code, 2018).

Analyzing in a synthetic manner from the perspective of another three relevant aspects

Regarding the preparation of the Codes analyzed, the stock exchanges are the entities the most involved in this process with 25%, being directly interested to issue and monitor the implementation of the provisions, principles, and recommendations of the Codes on their capital markets for the listed companies. They are followed by local financial authorities with 20% and the last group of entities are represented by different committees, councils, and directors’ institutes with 15%. 39 out of 44 countries (89%) apply in a voluntary way the Codes and 75% of the countries (33 out of 44) follow the “comply or explain” principle. The author remarked that the corporate governance framework is entitled to promote transparent and fair markets. From what it has been noticed at the national level of each country analyzed, there is a mix of legislation, regulation, self-regulation, and voluntary standards. That means flexibility combining them from hard to soft provisions (G20/OECD Principles of Corporate Governance, 2015).

Romania’s case – General legal framework and Bucharest Stock Exchange Corporate Governance Code

The Romanian general legal framework for corporate governance is structured on four levels: the company law, legislation specific to the financial-banking, pensions and insurance areas, legislation for the listed companies and for the government companies. This framework is comprised of a code applied to listed companies on the regulated market, principles of corporate governance for the listed companies on the Multilateral Trading System, both for Bucharest Stock Exchange, a government ordinance (2011) complemented by an ordinary law (2016), and other different regulations issued by government or by the Financial Supervisory Authority.

Related to Bucharest Stock Exchange, there were issued two regulations in 2001 and 2008, and the last one is a Code dedicated and separated from the legal framework of the exchange. The Code was prepared with the support of EBRD, and other international and local consultants and it was issued late 2015 to be implemented beginning with January 2016 for the regulated market managed by Bucharest Stock Exchange. The code is structured in four main sections from A to D dedicated to responsibilities of the board of directors, risk management and internal control system, fair rewards and motivations and building value through investors’ relations. The document is a set of 34 provisions to be complied with and 15 general principles as recommendations, and its scope was to create in Romania a capital market at the international level based on the best practices, transparency, and trust (Bucharest Stock Exchange Corporate Governance Code, 2016). Like most of the countries analyzed in the sections above of this paper, the principle applied by the local code is “comply or explain”. When implemented in 2016, the listed companies sent based on a current report the status related to complying or not to the principles provided by the code. In addition, every time when changes occur, the companies should send a new current report. Also, annually, they had to prepare a declaration of corporate governance as a separate section within the annual report of the company comprising of a self-evaluation, and to detail the measures to take to comply with the provisions of the code.

The author contemplated to the implementation of the code between 2016-2021 for the companies listed on the top of the quote of the exchange, respectively Premium tier. These companies represented more than 33% of the companies from the regulated market, 65% of the market capitalization, 85% of the total trading values and 14 areas of activities. There were analyzed the declarations of the companies related to the 34 provisions of the code, which means a total of 5,168 individual observations.

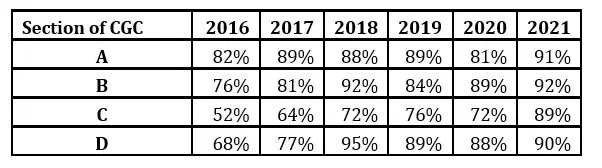

In the table below, the author presents the results obtained in the period 2016-2021, 6 years, from the implementation of the new Code and the compliance with each section of the Code.

Fig 10. Compliance percentage for each section of CGC

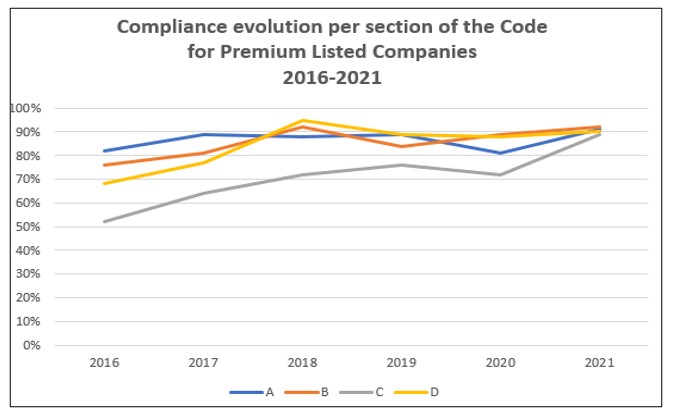

An overview of the synthetic results and the evolution in the period 2016-2021 are shown below in the graph.

Fig 11. Compliance evolution per section of CGC for Premium listed companies

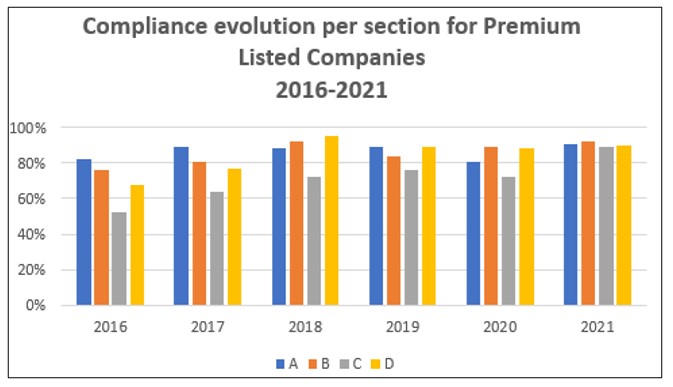

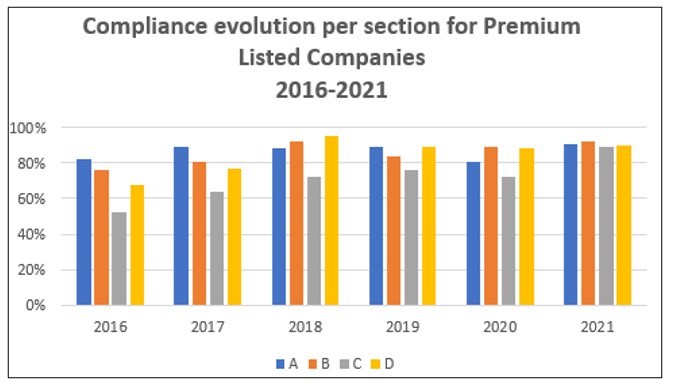

Fig. 12 Compliance evolution per years for each section for Premium Listed companies

The conclusions of the analysis for these 6 years show that from the very beginning of implementation, it was considered difficult to comply with the provisions of the code related to: evaluation of the board and issuing a policy in this regard (section A, provision A8 – an evolution of compliance from 58% to 68%), setting-up a nomination committee formed by nonexecutives and the majority to be independent (section A, provision A11 – an evolution of compliance from 62% to 71%), setting-up an audit committee comprised of 3 members where the majority has independent members and the chairman of the audit committee to be an independent nonexecutive (section B, provision B1 – an evolution of compliance from 75% to 86%), the approval of a policy for company’s transactions with closed related companies with an equal value or more than 5% from the net assets (section B, provision B10 – an evolution of compliance from 58% to 86%), publishing and implementing a remuneration policy (section C, provision C1 – an evolution of compliance from 54% to 89%), the approval and publishing of a forecast policy (section D, provision D3 – an evolution of compliance from 54% to 71%), organizing of calls for analysts and investors (section D, provision D9 – an evolution of compliance from 67% to 86%), and publishing, if it is adopted, a CSR policy (section D, provision D10 – an evolution of compliance from 67% to 82%).

An important aspect that is important to be emphasized regards the adoption by 12 out of the 25 Premium companies of their own Codes (5), regulations (6) or Statute (1) for corporate governance. These decisions reflect the attention paid by the listed companies on the Premium Tier to corporate governance.

Fig 13. The lowest level of compliance for 8 provisions of CGC for Premium companies

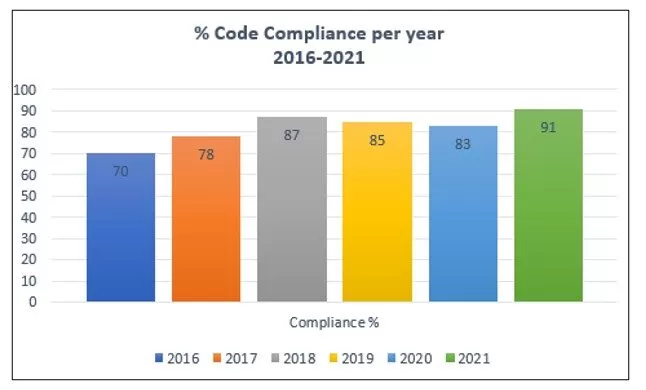

The author remarked that the implementation of the code considerably improved between 2016-2021, from 70% in 2016 to 91% in 2021.

Fig 14. Percentage CGC compliance per years 2016-2021

Short analysis of some variables of corporate governance of the 25 Premium listed companies at the end of 2021

The analysis focuses on the main variables regarding the characteristics of the 28 boards and the results showed that 25 boards are one-tier and 3 two-tier; 12% of the members are foreigners; the average age of the board members is 53; the average size is 6; 13% of board members are women; 77% are nonexecutives; 45% are independent; 3 out of 28 CEOs are women; 29% of the executives are women; different committees were organized by the boards as audit, remuneration, nominalization, risk management, policies, development, investments, evaluation, strategy, security or regulations dedicated. All this information provides an overall image of the listed companies at a moment in time and correlated with the above data. The author can draw the conclusion that the implementation of the code had a positive effect on the companies and conducted to improvement.

Conclusions

In the last decades, corporate governance codes were developed based on fundamental norms pursuing justice, fairness, and equality (Zattoni and Cuomo, 2008), having as main target the increase of the accountability for the shareholders’ companies (Hermes et al, 2007). Nowadays, these documents gained their place as an important element for the business environment and are the systemic response to governance inefficiency. The corporate governance essential tool for company communication to investors is today the declaration of conformity based on “comply or explain” principle. (Aluchna and Kuszewski, 2021). This rule offers flexibility in adopting as a soft law voluntary decisions in implementing best practices and preparing the companies on a gradual basis for the future. The investors monitor the evolution of the companies regarding the compliance with the codes and decide suitably (Easterbrook and Fischel, 1996). It is an ongoing process, where the explanation for the non-compliance is very important especially for the companies which show their interest to comply in the future with the codes.

The key role within the companies is played by the boards of directors and their role is continuing to increase taking into consideration the main trends affecting them in the recent years. Greater degree of responsibility for greater range of issues and new types of stakeholders, technological developments and innovations impact the boards’ activity (ICSA The Governance Institute, 2019). An important step forward to implement in an adequate manner the corporate governance is to build a model of the board effectiveness based on board characteristics, process, and role, to successfully carry out the control and service roles (Jansen, 2021). In accordance with Horwath Corporate Governance Report, “An effective board will contain ethical, skilled and critically thinking individuals who contribute special expertise to the company.” (Horwath, 2002).

Launching in 2015 with implementation from 2016 of the new Corporate Governance Code by Bucharest Stock Exchange indicated that it was the appropriate time for a new framework applied to the local capital market. The author found that the last five years analyzed correspond to the strong economic growth that Romania had up to 2020 (OECD, 2021). During this period, the local capital market was upgraded officially to emerging market in September 2020 by FTSE Russell, one of the leading stock indexes’ providers in the world. That was a historic moment for Romania and its capital market, which permitted to enter the radar of a wider category of investors. This promotion represents an important step forward for all the listed companies and encourages them to improve their mechanisms and practices on corporate governance to increase efficiency on the company’s management (Vintila and Gherghina, 2013).

Bucharest Stock Exchange made a lot of visible progress in relation to its investors and issuers in the last years and the results were obtained step by step. The company developed significant projects for education towards high-schools and universities, listed and non-listed companies and all the individuals interested in investing on the capital markets. Its flagship project dedicated to new potential issuers in the market called Made in Romania where more than 600 companies were enrolled to be closer to the capital market has reached its fourth edition in 2021. Another new project is for promoting companies to the investors through its Research Hub comprising of analysts’ reports.

The author considers that Romania should improve the legal framework dedicated to the companies by updating provisions of the Company Law after more than 15 years form its fundamental change since 1991. The corporate eco-system is more prepared now to face new challenges and to reduce the discrepancies between the ordinary companies and the listed ones. It should be appreciated as a normal step towards a better business environment. Also, after 6 years from the implementation of the new Code of Corporate Governance of Bucharest Stock Exchange, taking into consideration the higher experience of the market participants and the investors whose number increased significantly in the last years, the Code should be revisited and adapted to the new trends including here diversity and ESG.

References

Aluchna Maris and Tomasz Kuszewski (2021). Responses to corporate governance code: evidence from a longitudinal study. Review of managerial science. https://doi.org/10.1007/s11846-021-00496-3

Bradley Michael, Cindy Schipanni, Anant K. Sundaram & James P. Walsh (1999), Challenges to Corporate Governance: The purposes and accountability of the corporation in contemporary society: Corporate Governance at a crossroads. 62 Law and Contemporary Problems 9-86 (Summer 1999) https://scholarship.law.duke.edu/lcp/vol62/iss3/2/

Davis John P. (1904). Corporation: A Study of the Origin and Development of Great Business Combinations and of Their Relation to the Authority of the State, Volume 2. https://lawcat.berkeley.edu/record/322241

EY for European Commission. Directorate-General for Justice and Consumers, Study on directors’ duties and sustainable corporate governance: final report, Publications Office, https://data.europa.eu/doi/10.2838/472901

Hopt Klaus J. (1984), New Ways in Corporate Governance: European Experiments with Labor Representation on Corporate Boards, vol. 82, Is.5, MICH. L. REV. 1338. https://repository.law.umich.edu/mlr/vol82/iss5/15/

Jaimez-Valdez and Jacobo-Hernandez (2016). Journal of Management and Sustainability. Vol. 6, No. 3. 5539/jms.v6n3p44

Klettner, A., Clarke, T., & Boersma, M. (2014). The Governance of Corporate Sustainability: Empirical Insights into the Development, Leadership and Implementation of Responsible Business Strategy. J Bus Ethics. http://dx.doi.org/10.1007/s10551-013-1750-y

Lacy, P., & Hayward, R. (2011). A new era of sustainability in emerging markets? Insights from a global CEO study by the United Nations Global Compact and Accenture. Corporate Governance: The International Journal of Business in Society http://dx.doi.org/10.1108/14720701111159208

Mallin Christine (2013). Corporate Governance. 4th Edition, Oxford University Press, Oxford.

O’Donnell Cyril (1952). Origins of the corporate executive. Business History Review , Volume 26 , Issue 2 , June 1952. ttps://www.cambridge.org/core/product/identifier/S0007680500024806/type/journal_article

Pichet Eric (2017). Defining and selecting independent directors. Journal of Governance and Regulation, volume 6, Is. 3. http://dx.doi.org/10.2139/ssrn.2302467

Reguera-Alvarado N. and Bravo-Urquiza F. (2016). Multiple directorship and corporate regulation. Corporate Board: Role, Duties, & Composition, https://doi.org/10.22495/cbv12i1art3

Vintila Georgeta and Stefan Cristian Gherghina (2013). Board of directors’ independence and firm value: Empirical evidence based on the Bucharest Stock Exchange listed companies. International Journal of Economics and Financial Issues 3. 885

Warren-Myers, G. (2013). Is the valuer the barrier to identifying the value of sustainability? Journal of Property Investment & Finance, 31(4). http://dx.doi.org/10.1108/JPIF-01-2013-0004

Websites of the analyzed 25 listed companies, April 2021

Zattoni, A. and Cuomo, F. (2008) Why Adopt Codes of Good Governance? A Comparison of Institutional and Efficiency Perspectives. Corporate Governance: An International Review. https://doi.org/10.1111/j.1467-8683.2008.00661.x