1Kingsley A. ADEYEMO, 1Festus ODHIGU, 2David ISIAVWE, 3Cordelia Onyinyechi OMODERO and 4Gbenga EKUNDAYO

1Middle East College, Muscat, Oman

2General Manager, Ecobank Plc., Nigeria

3Covenant University, Ogun State, Ota, Nigeria

4Oman College of Management and Technology, Muscat, Oman

Volume 2024,

Article ID 808297,

Journal of Financial Studies and Research,

18 pages,

DOI: https://doi.org/10.5171/2024.808297

Received date: 16 May 2023; Accepted date: 28 June 2024; Published date: 23 July 2024

Academic Editor: Ajayi Emmanuel Olusuyi

Cite this Article as:

Kingsley A. ADEYEMO, Festus ODHIGU, David ISIAVWE, Cordelia Onyinyechi OMODERO and Gbenga EKUNDAYO (2024)," Mandatory Adoption of Taxpayers’ Identification Number (Tin) and Economic Growth in Nigeria: Any Connectedness?", Journal of Financial Studies & Research, Vol. 2024 (2024), Article ID 808297,

https://doi.org/10.5171/2024.808297

This study evaluates the impact of the mandatory adoption of Taxpayers Identification Number (TIN) on tax revenues and the growth of the economy of Nigeria over 1995 – 2020 period. The type of research design adopted for the study was the ex-facto research design. This was because the facts/raw data used for the inquiry have already occurred, without the researcher’s intervention. The Secondary source of data employed in addressing the research objectives, was sourced from the Federal Inland Revenue Service (FIRS) annual reports and the relevant World Bank reports. In analyzing the data gathered, the ordinary least square was adopted and Co-integration test was also conducted to see the possibility of a long run relationship between the variables though there may be variation in the short run. The error correction model (ECM), and the ARDL Long Run and Form test, used in the research correct the discrepancies between long run and short run impact of the explanatory variables. The study revealed inter alia, that the Adoption of TIN has positively influenced Tax revenue in Nigeria; there is a significant relationship between the adoption of TIN and Economic growth in Nigeria during the period studied; and there is a significant relationship between tax revenue and Economic growth in Nigeria.

Keywords: TIN, Economic growth, GNP, Revenue

Introduction

Tax has variously been defined as a mandatory levy required from the residents by the ruling authority, for the objective of providing social amenities for economic growth and advancement. The electoral, financial, and communal growth and expansion of any nation are functions of the sum of money that is available for the provision of infrastructure in that given nation (Gylych, Samira & Abdurrah 2016). According to Okpe (2000), “Tax payment is the transfer of resources and income from the private sector to the public sector in order to achieve some of the nation’s economic and social goals.”

Taxation serves as an integral component of government revenue in virtually every country in the world. The International Centre for Tax and Development’s figures supports this aforementioned fact, by stating that tax revenues are anticipated to account for eighty percent of world countries income accruable to the government (Adeyemi & Adeduro, 2020). The Federal Government of Nigeria, like any other nation, needs revenue to finance a variety of social services such as good transportation, accommodation, education, healthcare facilities, stable electricity, reliable water supply, and quality infrastructure to her people, (Olagunju, Laguda & Megbon, 2020). In Nigeria, the needed revenues are sourced through two basic ways namely, oil revenue and non-oil revenue. While the oil revenue comprises the sale of crude oil, the non-oil revenue is gotten from the collection of taxes from individuals and business entities chargeable under different conditions as prescribed by the government.

It has been established in literature that if taxation was not made compulsory, there would have been no motive or inclination for the populace to voluntarily pay. This is sequel to the perceived notion that the revenue generated has never been judiciously used by successive governments as a result of the inefficiency in tax administration by the government (Herbert, Nwarogu, & Nwabueze,2018). Undoubtedly, there is a clear positive association between the economic impact of taxes and the degree of compliance among taxpayers. Thus, a high degree of tax evasion and tax avoidance, leads to low revenue generation which in turn leads to poor economic growth of any nation. Besides, poor tax compliance and lack of ability to drag people especially those in the informal sector into the tax net, has led to a reduced amount of revenues made by government. Additionally, Oshiobugie and Akporere (2019), opined that embezzlement of funds, corruption, and lack of statistical data are the chief causes of the insufficient revenue generation in the case of Nigeria. Other drawbacks to the collection of taxes in Nigeria are characterized by the difficulties faced while paying taxes and the incidence of multiple taxation encountered by taxpayers. According to Kesavan and Srinivasan (2023), currently global payment systems are going through a period of change, during which the most creative and cost-effective technologies are being developed to enhance payment operations.

A praiseworthy tax system is rooted in three considerations, namely: tax policy, tax regulations, and tax administration. Whereas Tax policy establishes rules, regulations, and objectives to be met by taxation, tax regulations address the issues of tax forms, tax rates, enforcement of penalties for noncompliance, and the system’s overall legal and regulatory framework. Tax administration on the other hand is involved in the process of enforcing tax laws through the actions of authorities charged with the collection and collation of tax revenue (Okauru, 2012). In order to strengthen the foregoing three-dimensional structure of tax, certain reforms have been undertaken by Nigerian government over the years with the major purpose of boosting tax revenue. Tax reforms are steps or measures embarked upon by the authority(ies) designated by the government to ensure that tax system is enhanced to function better than before (Ahuru & Oriakhi (2014), and Nwokoye & Rolle (2015)).

One of the major tax reforms in Nigeria that this paper seeks to X-ray is the initiation of taxpayer identification number (TIN) in the enhancement of accountability of tax revenue. In the words of Iheduru and Ajaero (2018), “Taxpayer Identification Number is a dynamic consecutive set of numbers generated electronically to all form of taxpayers made up of individuals and corporate bodies”. TIN came into effect from 1st February 2008, sequel to the Federal Inland Revenue Service (FIRS) Establishment Act as contained in Section 8(9) for the main purpose of efficient tax administration. The cardinal objective of this paper, therefore, is to examine any relationship between the adoption of taxpayer identification number and economic growth in Nigeria. Other objectives are to ascertain the effect of the adoption of taxpayer identification number on tax revenue in Nigeria and to assess any possible relationship between tax revenue and economic growth in Nigeria.

The remaining part of this paper comprises five subsections as follows: Sections 2 and 3 are centered on the review of relevant literature/hypotheses and method of data analysis, respectively. Section 4 focuses on the results of the test of hypotheses, while sections 5 and 6 focus on the discussion of findings and conclusion, and recommendations, respectively.

Review of Literature

The Federal Inland Revenue Services (FIRS) of Nigeria, determined to boost revenue from tax and prevent tax leakage through noncompliance, introduced the Taxpayer Identification Number (TIN). The adoption of TIN basis moved taxpayer enrolment in the nation from a mechanically disorganized procedure to an automated order that is far more organized and synchronized using a computerized system. The previous method was ineffective, monotonous, and inconvenient, and it provided a significant challenge to both tax officials and taxpayers. As a result, the authorities were compelled to replace the manual system with a new and more contemporary one that is in line with international standards (Gurama, Mansor & Pantamee, 2015).

Ebifuro, Mienye, and Odubo (2016) opined that TIN expedites the handling of taxpayer’s key information across the country, as well as the enhancement of compliance, the resultant effect being an enhancement of government earnings. It also fosters the harmonization and synchronization of the authentication of all persons or institutions remitting taxes which is grounded on a computerized set-up (Jocet, 2014).

According to Ezugwu and Agbaji (2014), the underlisted are some of the benefits of TIN “(i) Filling of existing loopholes in the Country’s tax system. (ii). Enhancement of taxpayer identification and registration thereby bringing more taxpayers into the tax net. (iii). Minimization of errors and mistakes associated with manual registration. (iv). Reduction in the issues of multiple taxations which have been major challenges for taxpayers and administrators. (V). Enhancement of information sharing among relevant agencies in the country. (vi). Minimizing or eliminating cost of tax compliance as a result of greater accuracy in capturing data of taxpayers; with the electronic system, tax authorities will be able to effectively access, collate, analyze, and retrieve data with ease. (Vii). The TIN will facilitate a more efficient system of tax assessment and collection as well as tax audit and investigation. (Viii). Enhancement of voluntary compliance thereby allowing tax authorities to focus on review and verification of claims by taxpayers. (Ix). The system blocks all leakages in tax collection, eliminate corruption in tax system and enables tax authorities ascertain the actual income and taxes of all registered taxpayers. (X). Enhancement of ICT literacy and capacity building among the State Board of Internal Revenue (SBIR) staff. (Xi). Provision of basis for planning and budgeting purposes. (xii). Widening and deepening of taxpayer database”.

Types of Tax Revenue in Nigeria

Petroleum Profit Tax

This is one of the most important taxes collected by the Nigerian government as the economy is mostly driven by the oil sector. This is because Nigeria is one of the biggest manufacturers of crude oil in the world. Because of the prominence of petroleum to the revenue of oil and gas companies in Nigeria, a new law governing the taxes of profits from petroleum operations was enacted (Ogodo & Nweze, 2021). According to Attamah (2004), the Petroleum Profit Tax is Nigeria’s most major tax in terms of revenue share, accounting for 95 and 70 percent of foreign exchange earnings and revenue for the government, respectively.

The Petroleum Profit Tax Act is the regulation that governs the taxation of petroleum profits (PPTA). The Federal Military Government revised it for the first time in January 1967 with Decree No. 1 of 1967. Since the last amendment in 1967, there have been more amendments. The Petroleum Profits Tax Act of 2007 is the main law governing the taxation of petroleum profits in Nigeria. The Act took effect from January 1, 1959, sequel to the beginning of oil export to the worldwide market in 1958.

Petroleum operations are defined in Section 2 of the PPTA as “the act of obtaining petroleum chargeable oil for a company’s own account in Nigeria through any methods involving oil drilling and extraction but excluding refining activities carried in the course of a business carried on by the company engaged in such operations, and all operations incidental thereto, as well as any sale or disposal of chargeable oil”.

The petroleum profit tax was charged at a rate of 67.5 percent for the first five years of taxable operation and 85 percent till date.

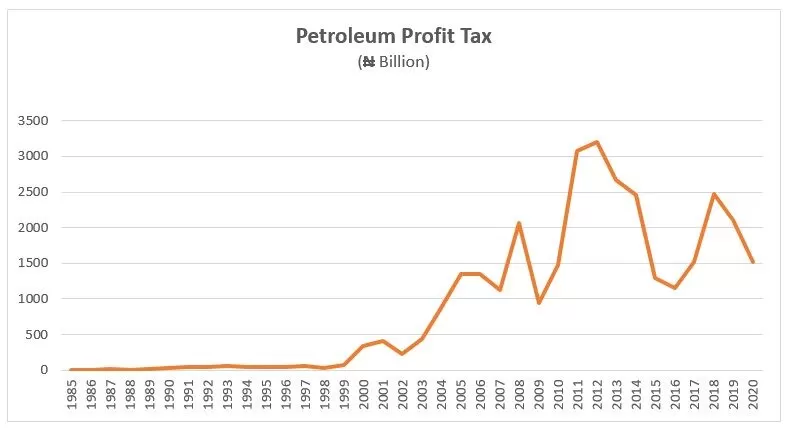

Source: Researchers with Data Sourced from Various FIRS Tax Reports

The graph of the Petroleum Profit Tax above depicts a steady growth in revenue over the years, with periodic vacillations in some years. However, revenue from Petroleum Profit Tax reached its peak in 2012 with the sum of 3.2 trillion Naira as revenue.

Company Income Tax

The Companies Income Tax Act (CITA) of 1961 is a statutory law that allows the federal government to collect income tax from registered corporations through the Federal Inland Revenue Service with the exception of those companies involved in petroleum activities as this is covered under the Petroleum Profits Tax Act. It also includes international companies that carry on business and generate profits in Nigeria.

All public companies in Nigeria are required to pay income tax and education tax. The rate is 30 percent of total profit for income tax and 2 percent of assessable profit for education tax. Profit after deducting losses carried forward from the previous year and capital allowances is referred to as total profit. Prior to subtracting capital allowances, assessable profit is derived (Ogodo & Nweze, 2021).

It is very imperative to note that firms that merely advertise petroleum goods, such as petrol, do not fall into the category of companies/firms participating in petroleum operations, and are therefore taxed under the Companies Income Tax Act (CITA). When a firm engages in both petroleum operations and petroleum product marketing, the transaction results from the petroleum operations are taxed under the Petroleum Profits Tax, while the transaction results from the marketing activities are taxed separately under the Companies Income Tax Act (Aminu, Ibrahim & Sulu-Gambari, 2019).

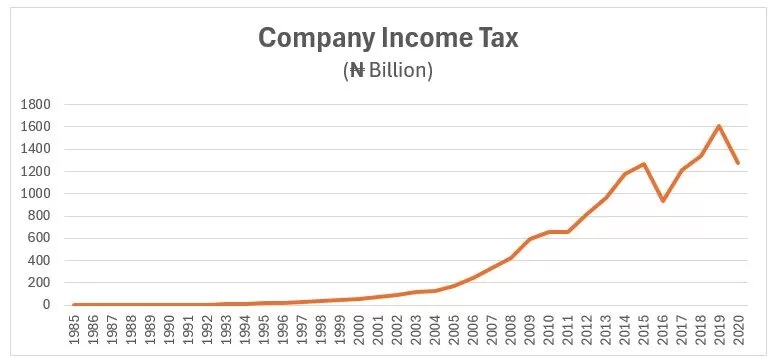

Source: Researchers with Data Sourced from Various FIRS Tax Reports

The graph of Company Income Tax above shows the growth trajectories for the 36 years under consideration. Like the Petroleum Profit Tax graph, there was a slight fall in revenue in 2020, very likely due to the unsavory impact of Covid’19.

Tertiary Education Tax

The Tertiary Education Tax was set up by the Nigerian government under the Tertiary Education Trust Fund Act 2011. It was enacted to rescind the Education Tax Act No 7 1993. Its crucial aim is to levy, monitor, & disperse education tax to public universities in Nigeria (Federal Republic of Nigeria Official Gazette, 2011). All established companies are subject to a 2% tax on their assessable profits under the Act. The totality of the firms incorporated in Nigeria is subject to the tax. How a company’s assessable profits are determined as stated under key provisions in either the CITA or the PPTA depending on the nature of the private enterprise.

The widely acknowledged fall in Nigerian educational standards, as well as the profound degradation in social and physical facilities and other utilities at all stages of the educational sector in Nigeria, coupled with the inability of the government to fund education budget without the intervention of the private sector, prompted the passage of this Act (Ugwanyi (2014), Oraka, Ogbodo & Ezejiofor, (2017)). The Tertiary Education Fund, as specified under the Act, is shared among higher institutions, secondary institutions, and primary institutions across the Federation at the rates of 50%, 30%, and 10% respectively.

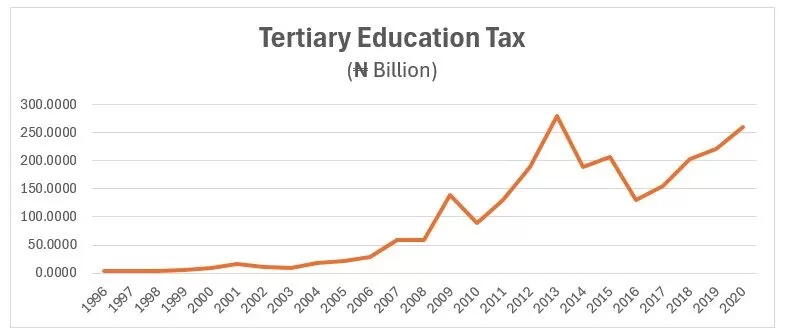

The graph of Tertiary Education Tax below, shows a consistent growth in Tertiary Education Tax over the period of 25 years, under consideration. The highest revenue from Tertiary Education Tax was realized in 2013, the sum of 279.35 Billion Naira.

Source: Researchers with Data Sourced from Various FIRS Tax Reports

Concept of Economic Growth

The increase in the quality and quantity of goods and services produced in an Economy is referred to as Economic Growth. According to Haller (2012), “Economic Growth is attained through the optimal utilization of accessible resources and the expansion of a nation’s production capacity”. It also can be defined as an increase in the expansion in the collective output in the economy. These collective outputs are mainly expressed as natural resources, human/physical capital, labor, infrastructure, and technology. It is imperative to mention that such an increase in the collective output should be maintained as it serves as a major determinant of a country’s financial health (Nwadiolor & Agbo, 2020).

Economic growth can be measured using Gross Domestic Product (GDP), Gross National Product (GNP), National income, and per capita income. However, out of all these indexes, GDP is deemed to be the most effective way to estimate economic growth over an extended period of time. This is because it gives the indicator of the size of the Economy and how well the Economy is performing.

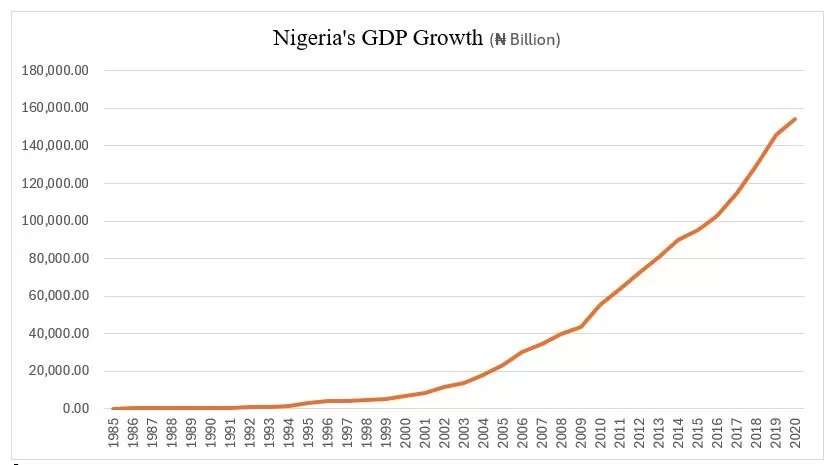

Below, is the curve of Nigerian GDP over the 36 years under consideration in this analysis.

The graph below shows the Nigerian Economic Growth trajectory within the period under study.

Source: Researchers with Data Sourced from Central Bank of Nigerian Statistical Bulletin

Tax Revenue Vs Nigerian Economic Growth

It is important to note that key macroeconomic metrics such as market prices, inflation rate, interest rates, statistics of the workforce, currency strength index, and rate of GDP growth are heavily influenced by a nation’s tax structure. To put it in proper context, there is a nexus between a government’s tax structure and the amount of advancement in the economy in many industrialized nations of the world (Ogwuche, Abdullahi & Oyedokun, 2019). This can be established using the tax-to-GDP ratio. A tax-to-GDP ratio is a measure of a country’s tax revenue in relation to its economic magnitude. Because it displays prospective taxes compared to the GDP, the ratio is a valuable tool for analysing a country’s tax revenue. It also allows for universal rankings and a sense of a country’s overall tax policy orientation. According to Nwadialor, & Agbo (2020) , “despite the fact that the tax-to-GDP ratio is just an expression of the percentage of a country’s colletive output due to tax income, it is a recurring tool for assessing a country’s tax system’s performance”.

When tax revenue rises at a lesser speed than the GDP, the tax-to-GDP ratio falls; and vice versa. In many cases, this ratio remains generally steady because tax revenue is directly associated with the level of economic undertaking. As a result, the prevailing supposition is that GDP will expand in synchronization with tax income (Kolade & Ajogbor, 2019). In other words, government revenue must expand faster than GDP in order to enhance the tax revenue to GDP ratio.

Despite reporting the highest-ranking GDP value and being Africa’s richest country, Nigeria was rated worst in terms of tax-to-GDP ratio among the leading African economies. Nigeria’s tax-to-GDP ratio stands at about 6.3% in 2018. In comparison to other countries, this is on the low side. According to the International Monetary Fund (2018), the West African Geographic average is 15%, the Asian average is 22%, and the OECD average is 27%. An average advanced country’s tax to GDP ratio is roughly 40%, according to the World Bank (2018). Many developing countries, on the other hand, also have low figures, with about sixty of them falling just under 15%. This could explain the reason why Nigerian ratio is low as Nigeria falls under the developing country category. According to the IMF, a more thorough tax reform in Nigeria might boost the tax-to-GDP ratio to about 8%.

Empirical Review

Abdul, Zubairu and Abubakar (2021) carried out a study on the efficiency of the adoption of Taxpayer Identification Number (TIN) in reducing tax evasion in Niger State. A qualitative research design was used by carrying out an interview using a sample size of ten tax governmental officers out of thirty-six staffs in Niger State Internal Revenue Service. The findings revealed that before the introduction of TIN the probability of evading tax was higher than the post adoption of TIN proving its effectiveness.

Ngodoo (2019) looked at the impact of tax revenue (as measured by petroleum profit tax, customs and excise duty, corporate income tax & value added tax) on Nigeria’s economic growth (proxy by real GDP). Data covered the period between 2002 till 2017. The data were examined using regression analysis technique. All the taxes measured, contributed insignificantly to the real GDP based on the study’s findings.

Olatunji and Oludayo (2018) assessed the impact of TIN on boosting revenue in Ekiti State. The years of coverage were from 2006 to 2015. A linear equation model was derived where revenue spawned from the state was made a function of when TIN was implemented. The state’s capital spending served as a constant variable. The analysis was carried out using ordinary least square regression. The findings indicated that the complete implementation of TIN has a considerable favourable effect on the state’s revenue. That means TIN is a good means to drive revenue generation. As a result, suggestions were geared towards government working out mechanisms vital to ensure that all taxable persons and/or business entities acquire a TIN, in order to optimize the TIN’s beneficial reform.

Saleh and Daluma (2017) inquired into the impact of tax reform on federal revenue generation in Nigeria. The research work used spanned the years 1991 throughout 2011. Augmented Dicker Fuller was used for unit root analysis. The Johansen co-integration method and error correction modelling were employed in testing the variables. A Partial Stock Adjustment Model was designed to aid the analysis. The various income taxes (such as taxes VAT, CED, PPT and CIT) were adopted to represent tax reform and they served as the independent variable. Federal Revenue figures served as the dependent variable. Findings revealed that the income taxes have a positive relationship with federal collected revenue.

Ezugwu and Agbaji (2014) undertook a research study on the implementation of TIN on state revenue in Kogi. The timeframe was from 2003 – 2012. The study used tables and regression to look at how domestically produced state income added to overall revenue accruing to the state prior to and following the introduction of TIN. Findings show that prior to the implementation of TIN, the domestically accrued revenue was not significant but showed phenomenal increase after TIN implementation.

Akinleye, Ogunmakin and Olaoye (2019) explored the impact of TIN on raising revenue in Southwestern Nigeria. The states used in the scope of the study are Ekiti, Osun, and Ondo states which were determined randomly. It covered the period between 2008 and 2017. Data collected from the internal revenue generating bodies of the states were analysed using paired sampled t-test. The findings suggested that TIN had a substantial effect on the revenue generated in the aforementioned states when it was implemented compared to when it was not.

Salman, Akintayo, Kasum and Bamigbade (2019) undertook a study on the effect of TIN on increasing revenue in Lagos State. The aim was to find out the impact of TIN on tax compliance and to see whether TIN has improved the revenue figures of the state. They collected data for the duration of December 2010 and September 2015 which was split into December 2010-April 2013 before the introduction of TIN and May 2013- September 2015 after the introduction of TIN. A qualitative research method was used in the form of questionnaires. Secondary data were also used for the revenue figures for Lagos State. The Population of the study was 11600 officials working in the Lagos State Internal Revenue Service (LIRS). The sample size which was randomly selected was 300. 221 out of the 300 respondents filled in the questionnaire completely. Least square regression technique was used in its methodology. Results showed that TIN positively influences revenue, and it has enhanced the level of tax compliance in Lagos.

Efanga, Umoh and Jonah (2019) and Abdul, Zubairu and Abubakar (2021) enquired into the Examination of The Effectiveness of TIN in eliminating tax evasion in Akwa Ibom and Niger States respectively. The statistical tool utilized for the analysis was the Auto Regressive Distributed Lag (ARDL) Model. Internally generated revenue (IGR) was not considerable prior to the adoption of TIN (1997-2007), according to the model. It was also reported that, with the implementation of TIN (2008-2018), there has been a significant increase in revenue. Thus, the null hypothesis that TIN did not militate against tax evasion in Akwa Ibom State was rejected, resulting in a massive increase in internally generated income in the state.

Iheduru and Ajaero (2018) investigated the effect of TIN on non- oil tax revenue by comparing the pre and post introduction of TIN spanning the years 2000- 2015. Secondary data were sourced from the annual CBN statistical bulletin. Descriptive and pair wise t-test statistical techniques were employed to peruse the data gathered. The results show that the cumulative non-oil revenue increased during post TIN periods when compared with the pre-TIN periods. The same was also applicable with the revenue accruing from CIT and TET. On the other hand, revenue accruing from VAT drastically reduced following the adoption of TIN. It was recommended that the tax base of VAT should be broadened via digital means.

Olatunji and Oludayo (2018) and Ezugwu and Agbaji (2014) assessed the impact of TIN on boosting revenue in Ekiti and Kogi states respectively. The years of coverage were from 2006 to 2015, and 2003 – 2012 accordingly. A linear equation model was derived where the revenue that spawned from the state was made a function of when TIN was implemented. The state’s capital spending served as a constant variable. The analysis was carried out using ordinary least square regression. The findings indicated that the complete implementation of TIN has a considerable favourable effect on the state’s revenue. That means TIN is a good means to drive revenue generation. As a result, suggestions were geared towards government working out mechanisms vital to ensure that all taxable persons and/or business entities acquire a TIN, in order to optimize the TIN’s beneficial reform.

Charles, Ekwe and Azubuike (2018) looked at the research topic Federal collected tax revenue and economic growth in Nigeria. The data was analyzed using the Johansen Co-Integration test, which revealed that there is a significant long-run link between Federally Collected Tax Revenue (FTCR) and Nigeria’s Gross Domestic Product (GDP). CED, VAT, and PPT all contributed to the increase in GDP. It means that the proper and effective execution of these tax regulations will result in the desired tax reform, as well as a substantial rise in governmental earnings to implement its policies and programs.

Asaolu, Olabisi, Akinbode and Alebiosu (2018) inquired into the association between tax revenue and economic growth in Nigeria. The research utilized secondary data for twenty-two years (1994 -2015). Tax revenue was measured with Value Added Tax (VAT); Petroleum Profit Tax (PPT); Company Income Tax (CIT) and Custom and Excise Duties (CED), while Economic Growth (EG) was proxy by GDP. Auto Regressive Distributed Lag (ARDL) and other post estimations tests were utilized to assess whether or not there is an association between the variables. Findings generated from the research postulated that VAT and CED had statistical meaningful association with economic growth; CIT has a negative link with economic growth while PPT had no considerable connection with economic growth.

Furthermore, flowing from the research problem and objectives, the following hypotheses stated in their null (H0) forms, are useful to this study:

Hypothesis 1:

H0: The adoption of TIN has no significant impact on tax revenue in Nigeria.

Hypothesis 2:

H0: The adoption of TIN does not have significant association with economic growth in Nigeria.

Hypothesis 3:

H0: There is no significant relationship between tax revenue and economic growth in Nigeria.

Method of Data Analysis

The type of research design adopted for the study is the ex-facto research design. This is because the facts/raw data used for the inquiry have already occurred, without the researcher’s intervention. The Secondary source of data employed in resolving the research objectives, was sourced from the FIRS annual reports and the World Bank.

In analyzing the data gathered, the ordinary least square was adopted. Co-integration test was also conducted to see the possibility of a long run relationship between the variables even though there may have been variation in the short run. This served as the error correction model (ECM) used in the research. It corrects the discrepancies between long run and short run impact of the explanatory variables. The ARDL Long Run and Form test served as the ECM model in the research. The study also made use of the E-view 11.0 and Stata 16.0 in the analysis of data collection from the annual reports of the governmental agencies involved.

Model Specification

To test the stated hypotheses, achieve the study’s objectives, and examine the link between tax revenue and economic growth, our model is firstly expressed in its implicit form:

Yt=β1+Xt β2+εt

Where Yt is the dependent variable, Xt is the explanatory variable and εt is the error term. Furthermore, the model is expressed in explicit form as follow:

Model 1: Adoption of taxpayers’ identification number on Tax Revenue

Taxt = β1+TINt β2+εt

Where:

Tax is proxy by petroleum profit tax; corporation income tax and tertiary education tax

TIN is a dummy variable where 1 represents when taxpayers’ identification number is adopted while 0 is otherwise.; ε = error term; β = coefficient of parameter; = Time Coefficient

Model 2: Adoption of taxpayers’ identification number on Economic Growth

GDPt = β1+TINt β2+εt

Where:

GDP is gross domestic product; TIN is a dummy variable where 1 represents when taxpayers’ identification number is adopted while 0 is otherwise.; ε = error term; β = coefficient of parameter; = Time Coefficient

Model 3: Tax Revenue and Economic Growth

GDPt = β1+PPTt β2+CITt β3+TETt β4+εt

Where:

GDP = Gross Domestic Product; PPT = Petroleum Profit Tax ; CIT = Corporation Income Tax; TET Tertiary Education Tax; ε = error term; β = coefficient of parameter; = Time Coefficient

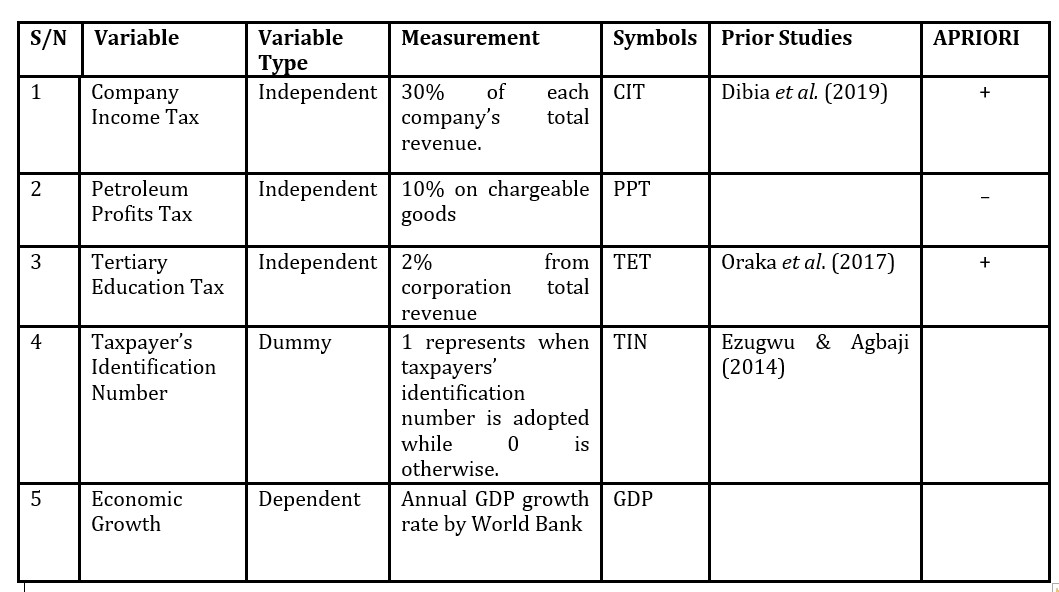

Table 1. Variable description and measurement

Source: Adapted by the authors

The table represents the range, minimum, maximum, mid values, spread, normality and the observation number for each variable.

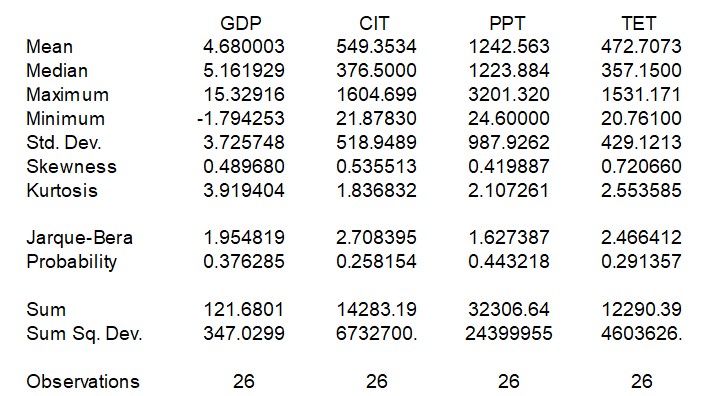

Descriptive Statistics

Table 2 below shows that the results obtained from the dependent variable GDP is leptokurtic having a kurtosis of 3.914 which makes it peaked relative to the normal distribution while the independent variables are platykurtic with CIT having a kurtosis of 1.836, PPT having 2.107 and TET has a kurtosis of 2.553 which makes their distribution flat relative to the normal distribution.

Table 2. Descriptive Statistics

Source: Authors’ Computation with the aid of EViews 11

Furthermore, the Jarque-bera statistics test result reveals the normality of the series distribution and the decision criteria are positioned at 0.05 which represents a 5% level of significance. The result presented in the table above indicates that all the variables are normally distributed as the probability of their Jarque-bera is higher than 0.05.

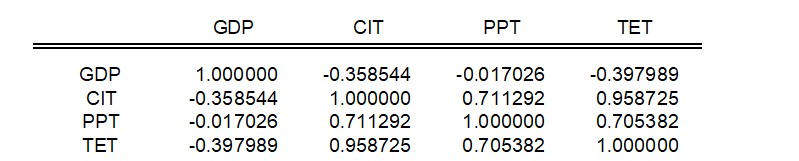

Correlation Matrix for Variables

The general rule of statistics suggests that correlation coefficients between 0 and 0.30 signify a weak correlation, 0.30 and 0.60 shows a moderate correlation, and 0.60-1.00 indicates a strong correlation.

Table 3. Correlation Matrix for Variables

Source: Authors’ Computation with the aid of EViews 11

The correlation matrix shows that there is a negative relationship between Company Income Tax (CIT), Petroleum Profit Tax, Tertiary Education tax and Economic Growth (GDP). These negative correlations were supported by a p-value of -0.358544, 0.017026 and -0.397989, respectively.

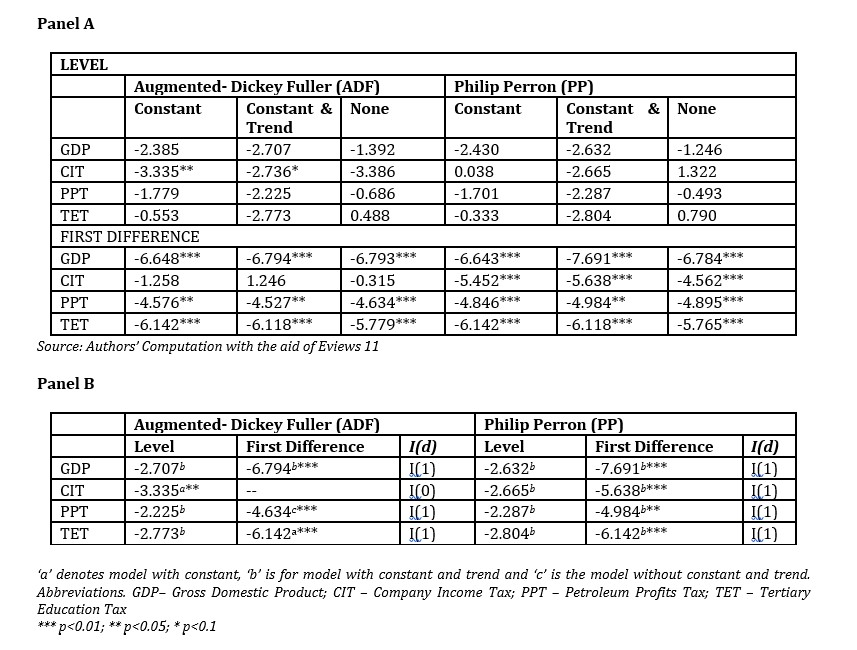

Unit Root Test

In this study, we made use of the Augmented Dickey-Fuller (ADF) and Philip Perron (PP) root unit test. Table 4 below reports the unit roots results, and it is evident that none of the variables are stationary at level I (0) but are stationary at first difference.

Table 4. Unit root result – Augmented Dickey-Fuller (ADF) & Philip Perron (PP)

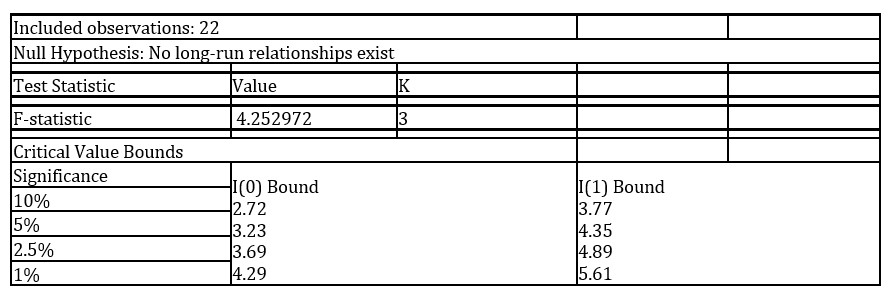

Cointegration Test

As seen from table 4 above, it is observed that the variables in the time series are not stationary: hence, cointegration test in this analysis is used to establish if correlation exists between the several time series data.

Table 5. ARDL Bounds Test

Source: Authors Computation with the aid of Eviews 11

If the series in question are cointegrated, this indicates they are linked and hence may be merged linearly. Three criteria alternatives are utilized in the Cointegration Test, including: (i) there is cointegration, if the computed F-statistic is larger than the Critical Value Bounds for the upper bound I(1); (ii) If the calculated F-statistic falls below the theoretical critical value for the lower bound I(0) bound, then we conclude that there is no cointegration; (iii) If the F-statistic falls between the lower and upper bounds, the test is considered inconclusive.

The F-statistic produced (4.252) which is greater than the upper bound I(1) at 10% level of significance in this empirical evidence, as indicated in the result in the Table above (0). This indicates that there is a long run relationship between the variables. Hence there is a cointegration of the non-stationary variables which leads to an error correction modelling process to analyse the variables.

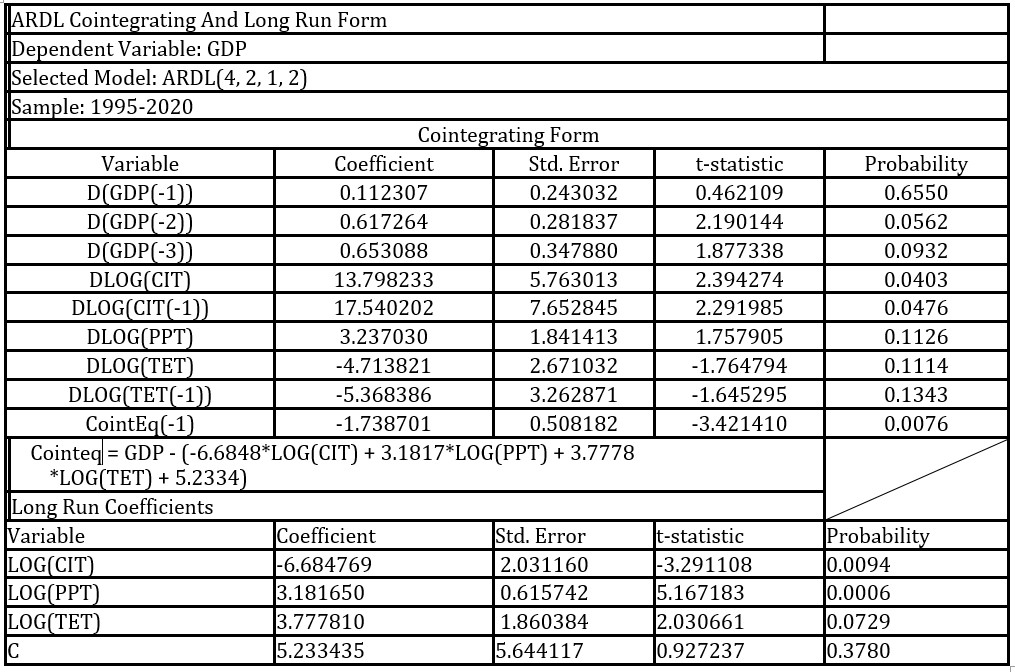

Table 6. ARDL Cointegrating and Long Run Form Test

Source: Authors’ Computation with the aid of Eviews 11

Empirical Results

Having estimated the cointegration test, it is necessary to analyse the long-run and short-run relationships using the Error Correction Model. The coefficient on the lagged EC term (-1.73) is statistically significant at the 1 per cent level and suggests that convergence to equilibrium is rapid.

The estimated coefficients of the long-run relationship are significant for Company Income Tax (-6.684769), Petroleum Profits Tax (3.181650), and Tertiary Education Tax (3.777810) because the p-value is less than 0.10. This implies that those variables are strong predictors of economic growth, thus, suggesting that a 1 percent increase in CIT is associated with 6.684 per cent decrease in economic growth, on average, ceteris paribus; while a 1 per cent increase in PPT is associated with a 3.181 percent increase in economic growth, on average, ceteris paribus and lastly a 1 per cent increase in TET leads to a 3.777 percent increase in economic growth, on average, ceteris paribus. This result is consistent with other studies, evidencing that growth in the economy will significantly be attributable to a positive change in tax revenue in Nigeria (Yahaya & Bakare 2018; Ebi & Ayodele, 2017; Edewusi & Ajayi 2019). These outcomes are in line with a priori expectations because, in the long run, it is expected that TET and PPT will boost economic growth. However, the outcome is not in line with the a priori expectation for CIT since in the long run it doesn’t contribute to economic growth.

For the short-run analysis, the findings show that the first and second lags of Company Income Tax are positive and statistically significant at the 5 per cent level respectively. This scenario implies that, a percentage change in the past realisations of Company Income Tax is associated with a 13.798 and 17.540 percentage increase in current level of economic growth, on average, ceteris paribus. The findings for Petroleum Profits Tax postulated that at first lag it is positive but not statistically significant at 1 per cent level which implies that a percentage change in the past realisations of Petroleum Profit Tax is associated with a 3.237 percentage increase in current level of economic growth.

Conversely, the coefficients of Tertiary Education Tax are negatively signed and not significant at the 1 per cent level in the first and second lag. Relative interpretations show that a percentage point increase in the past realisations of Tertiary Education Tax leads to a 4.713 and 5.368 percentage decline in economic growth in the short run, on average, ceteris paribus.

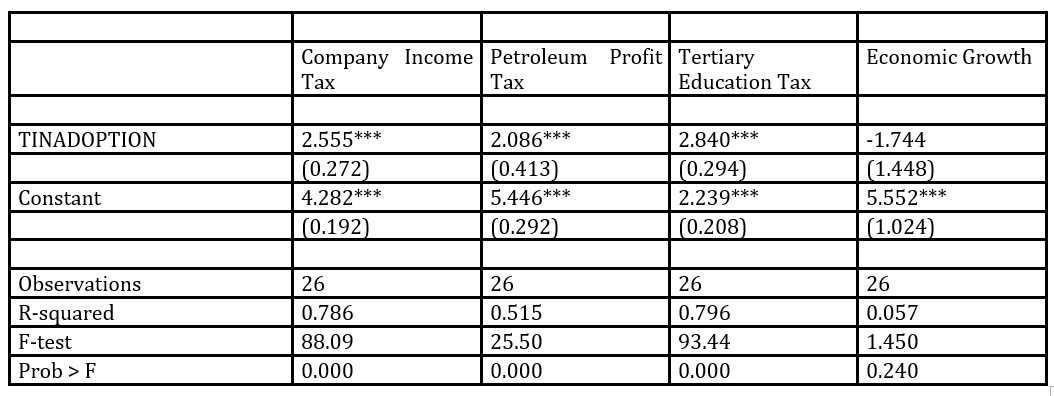

Ordinary Least Square Results

Table 7: The effect TIN Adoption on Tax revenue and Economic Growth

Standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Source: Authors’ Computation with the aid of Stata 16

Table 7 above reports the impact of TIN Adoption on the various tax revenues used in the study and economic growth. As shown, the coefficient of TIN Adoption has statistical significance on company income tax, petroleum profit tax and tertiary education tax with a value of 2.555, 2.086 and 2.840 respectively at 1 per cent level. These results suggest that the adoption of TIN influences the tax revenue mobilization. These values are positive but albeit small when compared with the expectations of the percentage that the adoption of TIN is supposed to generate on these taxes. It also points at the fact that tertiary education tax recorded the highest percentage with 2.840% and petroleum profits tax with a percentage of 2.086%.

The R-squared value identifies the percentage of dependent variability explained by the independent variables. The R-squared value for company income tax, petroleum profit tax and tertiary education tax is 0.786, 0.515, and 0.796 respectively. Thus, this implies that 78.6% of the variability is explained by CIT. 51.5% of the variability is explained by PPT and 79.6% of the variability is explained by TET.

However, the effect of TIN adoption has no significance on economic growth with a value of -1.744.

Test of Hypotheses

For the hypotheses testing, ARDL Cointegrating and Long Run Form Test was used to calculate the overall relationship existing between each independent variable and the dependent variable. The implementation of TIN on tax revenue and economic growth was analysed using Ordinary Least Square. For the purpose of this study, the accepted level of significance is 5%. The null hypothesis will be rejected in favour of the alternate if the level of significance is less than 0.05. When the P-value is greater than 0.05, the null hypothesis will be accepted. Therefore, the result of the hypotheses is tested below:

Hypothesis 1

H0: The adoption of TIN has no significant difference on Tax Revenue in Nigeria.

The results of the ordinary least square model shows that there is a positive and significant difference of 2.5% that the adoption of TIN has on company income tax in Nigeria at 5% level of significance.

The results of the ordinary least square model shows that there is a positive and significant difference of 2% that the adoption of TIN has on petroleum profits tax in Nigeria at 5% level of significance.

The results of the ordinary least square model shows that there is a positive and significant difference of 2.8% that the adoption of TIN has on tertiary education tax in Nigeria at 5% level of significance.

Overall, the null hypothesis of no significant difference that the adoption of TIN has on Tax Revenue in Nigeria is rejected. Therefore, the adoption of TIN has positive influence on Tax Revenue in Nigeria.

Hypothesis 2

H0: The adoption of TIN has no significant difference on Economic Growth in Nigeria.

The results of the ordinary least square model shows that there is a negative and insignificant difference of 1.7% that the adoption of TIN has on economic growth in Nigeria at 5% level of significance. Therefore, the null hypothesis of no significant difference that the adoption of TIN has on economic growth in Nigeria is accepted.

Hypothesis 3

H0: There is no significant relationship between tax revenue and economic growth in Nigeria.

The results from the error correction model showed that Company Income Tax had a significant but negative relationship with economic growth in Nigeria at 5% level of significance. While that of Petroleum Profits Tax had a significant and positive relationship with economic growth in Nigeria at 5% level of significance. Moreso, the error correction model showed that Tertiary Education Tax had a significant and positive relationship with economic growth in Nigeria at 5% level of significance. Overall, the null hypothesis of no significant relationship between tax revenue and economic growth in Nigeria is rejected.

Recommendation

Based on the literature reviewed in this study, one of the reasons for the mandatory use of TIN is the reduction of the incidence of tax evasion which in turn would increase revenue generation and subsequently affect positively the economic growth. The Deterrent Theory states that an individual would want to weigh the cost/benefits of paying taxes and pick the one that appeals to his utmost advantage. It is hereby recommended that governments at all levels should implement stringent sanctions to dissuade any act of avoidance and evasion of tax.

The Popular Psychological Theory of tax reveals that the willingness to pay taxes is mostly determined by behavioral attitudes or disposition towards the government. That is, whether their taxes would be used for what they ought to be used for in the society. The solution is for the government to be much more accountable and efficient so that citizens would be encouraged to pay taxes if they are seeing their monies being used for the right purposes and lastly.

The Ability to Pay theory postulated that people should pay taxes in accordance with their financial capacity. This reduces the tax burden on the poor who cannot afford to pay and also would not discourage them from paying. All these foster revenue mobilizations which in turn should encourage economic growth.

Currently, Nigeria’s tax-to-GDP ratio is abysmally low at 6.3%. The onus is on the government to ensure that it should be improved to the minimum threshold set by the Organization for Economic Co-operation and Development (OECD) which is 15%. It is also recommended that the TIN reform should be revised to ensure that it covers every single taxpayer in the nation because it is evident that a wide tax gap is still prevalent in Nigeria. Digitization of tax remittance such as e-payment facilities should also be worked upon to easily capture citizens for complete tax assessment.

References

Abdul H., Zubauru U., & Abubakar B. (2021) Curbing Tax Evasion through Taxpayer Identification Number (TIN) in Niger State, Nigeria. Sriwijaya International Journal of Dynamic Economics and Business, 5(1) 1-16

Adeyemi, A., & Adeduro, A. (2020). INSIGHT: Tax Revenue Mobilization in Nigeria. Daily Tax Report : International, 1–6.

Akimov, , & Kadysheva, K. (2023). E-government as a tool for communication with young people: legal aspects.Journal of Law and Sustainable Development,11(1)1-11 https://doi.org/10.37497/sdgs.v11i1.272

Akinleye, G. T., Olaoye, F. O., & Ogunmakin, A. A. (2019). Effect of tax identification number on revenue generation in Southwest Nigeria. Journal of Accounting and Taxation, 11(9).

Aminu, A. M., Ibrahim, M. S., & Sulu-Gambari, M (2019). Impact Analysis of Petroleum Profit Tax and the Economic Growth in Nigerian: 1985-2019.

Asaolu, T. O., Olabisi, J., Akinbode S. O., and Alebiosu, O., N., (2018). Tax revenue and economic growth in Nigeria. Scholedge International Journal of Management & Development, 5(7), 72-85

Attamah, N. (2019). Determinants of Non-Tax Compliance in Nigeria: A Study of Enugu Metropolis. International Network Organization for Scientific Research, 5(1): 41-47, 2019.

Charles, U.J; Ekwe, M.C and Azubuike, J.U.B (2018). Federally Collected Tax Revenue and Economic Growth of Nigeria: A Time Series Analysis. International Accounting and Taxation Research Group, Faculty of Management Sciences, University of Benin, 24-38

Ebi, B. O., & Ayodele, O. (2017). Tax reforms and tax yield in Nigeria. International Journal of Economics and Financial Issues, 7(3), 768 – 778.

Ebifuro O, Mienye E, Odubo TV (2016). Application of GIS in Improving Tax Revenue from the Informal Sector in Bayelsa State, Nigeria. International Journal of Scientific and Research Publications 6(8):1-13.

Edewusi, D. G. & Ajayi, I.., E., 2019. “The Nexus between Tax Revenue and Economic Growth in Nigeria,” International Journal of Applied Economics, Finance and Accounting, Online Academic Press, vol. 4(2), pages 45-55.

Efanga, U. O., Umoh, E. A., & Jonah, A.E. (2019). Examination Of the Effectiveness of Taxpayer Identification Number (Tin) In Combating Tax Evasion in Nigeria (Case Study Of Akwa Ibom State Board Of Internal Revenue). International Journal of Management and Commerce Innovations,7(2), 469-483.

Ezugwu, C.I. and Agbaji, J. (2014). Assessment of the application of taxpayer identification number (TIN) on internally generated revenue in Kogi State. Mediterranean Journal of Social Science, 5(20), 38- 48’

Gurama, Z. U., Mansor, M., & Pantamee, A. A. (2015). Tax evasion and Nigeria tax system: an overview. Research Journal of Finance and Accounting, 6(8), 202-211.

Gylych, J. Samira, A. and Abdurrah, I (2016). The Impact of Tax Reforms and Economic

Growth of Nigeria. The Empirical Economics Letters 15(5):30-40

Haller, A.P. (2012) Concepts of Economic Growth and Development. Challenges of Crisis and of Knowledge. Economy Transdisciplinarity Cognition, 15, 66-71.

Herbert, W. E., Nwarogu, I. A., & Nwabueze, C. C. (2018). Tax reforms and Nigeria’s economic stability. International Journal of Applied Economics, Finance and Accounting, 3(2), 74-87.https://www.researchgate.net/publication/337552320_Tax_revenue_and_private_domestic_investment.

Iheduru, N. G., & Ajaero, O. O. (2018). Tax Identification Number and Non-Oil Revenue: A Comparative Analysis of Pre and Post Tin Adoption. International Journal of Accounting & Finance Review, 3(1).

Jocet, C.R.P. (2014). Taxpayer identification number (TIN): Its Development and Importance in Tax Administration. International Journal of Management Research, 2(4), 16-22

Kesavan, V., and Srinivasan, K. S. (2023) Present State and Future Directions of Digital Payments System: A Historical and Bibliographic Examination. International Journal of professional Business Review. 8(6)1-29

Kolade T. & Ajogbor P. (2019). Nigeria: Nigeria’s Unchanging Tax to GDP Ratio: An Instructive Appraisal. Mondaq.

Nwadialor, E. O., & Agbo, E. I. (2020). Increasing Tax-To-Gdp Ratios Of Sub Sahara-African Countries: Lessons From Advanced Economies. International Journal of Research in Management Fields, 4(1), 17-38.

Nwokoye , G.A, and R.A,Rolle(2015). Tax Reforms and Investment in Nigeria: An Empirical Examination. International Journalof Development and Management Review, 39-51 (3) (PDF) Tax revenue and private domestic investment. Available from: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwjLo6Goj-n-AhU8lP0HHbV2DMgQFnoECBUQAQ&url=https%3A%2F%2Fwww.ajol.info%2Findex.php%2Fijdmr%2Farticle%2Fview%2F120933%2F110373&usg=AOvVaw213DfBHsykQk-BkQKA6Tdd

Ogbodo, O. C., & Nweze, C. L. (2021) Effect Of Tax Revenue On Economic Development: Evidence From Nigeria. Research Journal of Management Practice| ISSN, 2782, 7674.

Okauru, Ifueko Omoigui (Ed.). 2012. A Comprehensive Tax History of Nigeria. Ibadan, Nigeria: Safari Books Limited.

Okpe, I. I. (2000). Personal income tax in Nigeria. Enugu: Ochumba Printing and Publishing Company

Olatunji, O.C., and Oludayo, A.J. (2018). Impact of Taxpayer identification number on revenue generation in Ekiti State. European Journal of Accounting, Auditing and Finance Research, 6(5), 35- 46.

Olagunju, O. O, Laguda, K. F, Megbon, O.M. (2020). Taxation, Economic Growth and Sustainable Productivity in Nigeria.

Oraka, A., Ogbodo, O., & Ezejiofor, R. (2017). Effect of Tertiary Education Tax Fund (TATFUND) in Management of Nigerian Tertiary Institutions.

Oriakhi, D.E., Ahuru, R.R. (2014), Impact of tax reform on federal revenue generation in Nigeria. Journal of Policy and Development Studies, 9(1), 157-9385.

Oshiobugie, O. B., & Akpokerere, O. E. (2019). Tax revenue and the Nigerian economy. International Journal of Academic Management Science Research, 3(2), 61-66

Salman, R. T., Akintayo, S., Kasum, A. S., & Bamigbade, D. (2019). Effects of taxpayers’ identification number on revenue generation in Lagos State, Nigeria.

Ugwuanyi, G. O. (2014). Taxation and Tertiary Education Enhancement in Nigeria: An Evaluation of the Education Tax Fund (ETF) Between 1999-2010. Journal of Economics and Sustainable Development, 5(6), 131-141.

Yahaya, H. & Bakare, A. (2018) Effect of petroleum profit tax and companies’ income tax on economic growth in Nigeria. Journal of Public Administration, Finance and Law, 1(1) https://www.jopafl.com/uploads/issue13/EFFECT_OF_PETROLEUM_PROFIT_TAX_AND_COMPANIES_INCOME_TAX_ON_ECONOMIC_GROWTH_IN_NIGERIA.pdf