1Roseline O. OZEGBE, 1Farouk A. ADEDOKUN, 2Adewale D. OSINOWO and 1Toluwa C. OLADELE

1Department of Banking & Finance, University of Ibadan, Ibadan, Nigeria

2Dominion Trust (Investment) Bank Limited, Lagos, Nigeria

Volume 2025,

Article ID 713356,

Journal of Financial Studies and Research,

12 pages,

DOI: https://doi.org/10.5171/2025.713356

Received date: 23 September 2024; Accepted date: 13 December 2024; Published date: 3 January 2025

Academic Editor: Ajayi Emmanuel Olusuyi

Cite this Article as:

Roseline O. OZEGBE, Farouk A. ADEDOKUN, Adewale D. OSINOWO and Toluwa C. OLADELE (2025)," Does Stock Market Growth Translates to the Broader Economic Development? Annual Time-Series Data Insights from Nigeria ", Journal of Financial Studies & Research, Vol. 2025 (2025), Article ID 713356, https://doi.org/10.5171/2025.713356

Motivated by lingering incidence of relative economic underdevelopment of Nigerians, this research examined the influence of the growth of the Nigerian stock market on the improvement of individual Nigerians, beyond Gross Domestic Product (GDP) expansion. Employing annual time-series data from 2003-2022, the research examined how specific stock market indicators such as market capitalization, liquidity, and volatility influenced comprehensive development metrics encompassing real GDP per capita and Human Development Index (HDI). Multiple regression analyses (OLS) were adopted as the estimation technique. The findings showed that market capitalization positively and significantly impacted both the real GDP per capita and HDI. However, the effects of stock market liquidity were varied, showcasing an insignificant impact on real GDP per capita yet a significant negative impact on human development. Stock market volatility, on the other hand, showed insignificant implications on both real GDP per capita and human development. Consequently, the study concluded that market capitalization and liquidity are the major drivers of economic development in Nigeria. Therefore, the study recommended that deliberate measures should be put in place to further open the market and make it more attractive to investors because of its ability to improve the well-being of the citizens with appropriate regulatory oversight to curb negative effects.

Keywords: Human Development Index, Stock Market, Market Capitalisation and Liquidity, Real Gross Domestic Product per Capita.

Introduction

The capital market is an important component of the financial system of any country as it plays vital role in the mobilisation of long-term savings, allocating capital, creation of liquidity, diversification of risks, improved capital dissemination, information acquisition, and enhanced motivation for corporate control and promoting economic growth. To the extent of literature search, the positive relationship between capital accumulation and real economic growth has long been affirmed in economic theories (Barro, 1991; Mankiw et al., 1992; Romer, 1994; Anyanwu, 1998; Iyola, 2004; Chinwuba & Amos, 2011; Yadirichukwu & Chigbu, 2014; Christie, 2016). The capital market serves as a lubricant or driver that keeps the economy’s wheel turning towards growth and development because of its crucial role in not only mobilising long-term funds and directing them towards productive investment but also efficiently allocating these assets to projects that will provide the fund owners with the highest returns (Adeusi et al., 2013).

The Nigerian Stock Exchange (NSE) now Nigerian Exchange Group (following the demutualization of the NSE in 2021, the Nigerian Exchange (NGX) Group now has 3 subsidiaries: Nigerian Exchange Limited (NGX), the operating exchange; NGX Regulation (NGX RegCo), the independent regulation company; and NGX Real Estate (NGX RelCo)) has grown to become the fourth largest stock exchange in Africa (the top three leading exchanges being Johannesburg Stock Exchange (JSE) with USD1.077trillion and trailing behind in the second place is Casablanca Stock Exchange (MASI) with USD69.8billion and Botswana Stock Exchange (BSE) with USD52.5billion market capitalisation), though still small compared to various nations in Asia, Europe, North and South America in terms of market capitalisation (CBN, 2007).

Since its first operation on June 5, 1961, the Nigerian Exchange Limited (NGX) has undergone technological and operational transformation that has impacted the macroeconomic landscape of the Nigerian economy. This is the operating exchange, NGX, which is a multi-asset exchange with 393 listed securities, comprising 151 listed companies (8 Premium Board, 133 Main Board, 7 Growth Board and 3 Asem companies, 157 Fixed Income Securities, including Green Bonds and Sukuk (106 FGN, 8 State and 43 Corporate Bonds, 12 Exchange Traded Products, 4 Index Futures and 69 Memorandum listings, as at September 12, 2024 (Nigerian Exchange Group). The total market capitalization increased over time, rising from $1.7billion in 1980 to $41.0billion in May 2024. This level of capitalisation could further increase tremendously in the aftermath of Nigeria signing the African Continental Free Trade Area (AfCFTA) agreement and concerted efforts put in place to improve the ease of doing business (Onwuka and Ozegbe, 2020).

New and established businesses have issued a variety of financial instruments to finance product development, new initiatives, or general corporate expansion. The market was instrumental to the actualization of significant national reforms such as monetary and fiscal policies, sectoral reforms, including the abolition of 80% of the oil subsidy in 1988, interest deregulation starting in August 1987, financial market reform, and public sector reforms which entail the full or partial privatisation and commercialisation of about 111 public owned enterprises in which the NGX was to play a key role during the offer for sale of the shares of the affected enterprises (Anyanwu, 1993; World Bank, 1994; Yesufu, 1996; Anyanwu et al., 1997). Again, the stock market was instrumental to the initial 25 banks that were able to meet the minimum capital requirement of ₦25 billion during the banking sector consolidation in 2005, and even in very recent times (Oyefusi & Mogbolu, 2003). Okereke-Onyiuke (2000) stated that the stock market’s easily accessible and cheap sources of capital continue to be essential to the economy’s long-term viability, in addition to several other benefits including no short repayment period because funds are retained for medium to long-term periods or in perpetuity, funds for state and local governments are without constraints, as well as ample time to repay debts, where applicable.

The intricate relationship between the stock market and its potential impact on economic development in Nigeria stands as a subject yet to be fully explored. Several studies (Edame & Okoro, 2013; Azubuike, 2017; Cynthia et al., 2021; Okoye & Nwisienyi, 2022) have analysed the impact of the stock market on Nigeria’s economic growth, typically using GDP as the key metric. However, economic development encompasses more than just GDP growth. Aspects such as human development, productivity, and standard of living are key indicators of a country’s economic development. The inadequacy of current studies to consider these broader economic development variables limits the holistic understanding of the impact of the Nigerian stock market. Nigeria, one of Africa’s largest economies, has experienced fluctuations in economic growth rates and faces significant challenges related to poverty alleviation, unemployment, and income inequality. While the stock market has the potential to address some of these challenges by providing a platform for businesses to raise funds for innovation, expansion and employment creation, its historical trajectory reveals a shortfall in effectively channelling such achievement towards empowering Nigerians (World Bank, 1994). In other words, despite the growth of the Nigerian stock market overtime, it does not seem to have translated into their well-being as the problem remains that Nigerians are still classified amongst the poorest in the world. The critical research gap becomes a lack of comprehensive investigation of the relationship between specific stock market indicators and comprehensive economic development metrics beyond aggregate economic growth (GDP) that impact the individual well-being.

Specifically, this study analysed the impact of market capitalisation, liquidity, and volatility on Human Development Index and real income per capita. The findings will provide a more holistic perspective on the role of the country’s stock market in driving multidimensional economic development. It will also inform policy decisions regarding financial market regulation, integration with global capital markets, and other stock exchange governance issues. Understanding these relationships can help accelerate progress towards key development objectives in Nigeria such as creation of productive employment and raising living standards.

Literature Review and Hypotheses Development

According to Meggison et al. (2010), stock market capitalization refers to the total market value of all outstanding shares of companies listed on a stock exchange and it is a key metric popularly used to assess the size, depth, and development of a stock market. In principle, enhanced stock market capitalization has the potential to foster economic expansion through various channels identified in theoretical literature such as more funds mobilized for investment through facilitation of risk diversification (Levine 1991, 2001), more efficient allocation of capital to productive investments compared to individual savers by reducing information costs (Bencivenga et al., 1996), and ease of investors to divest and realize capital gains, which provides incentive for further investment (Obstfeld, 1994). However, some downsides have been associated with heightened market capitalization such as misallocation of investment towards speculative assets or short-term projects that do not enhance productivity (Morck et al. 2000), as well as stock prices probability of becoming more volatile and prone to bubbles as capitalization grows, thereby heightening macroeconomic instability (Bhide, 1993). The size and depth of a country’s stock market, often measured by market capitalization, have been linked to long-run economic growth in several studies. Jalloh (2015) employed a dynamic panel estimation technique to evaluate the relative influence of stock market capitalization on economic growth in 15 African countries. The study showed that increasing stock market capitalization by a marginal average of 10% causes significant growth in GDP per capita in the countries under investigation by an average of 5.4%.

Njemcevic (2016) studied the impact that the capital market of six transition countries in South-east Europe had on their economic growth employing a Panel-Corrected standard Error model on ten years data (2003-2012) with positive and significant impact of market capitalization ratio on economic growth.

In the Nigerian setting, Okoye and Nwisienyi (2022) adopted a time series multiple regression analysis and found that there is significant relationship between all share index (ASI), market value and market capitalization on GDP, in line with Kolapo and Adaramola (2012). Ugherughe and MaryAnn (2019) investigated the impact of stock market capitalization of three sub-Saharan African countries (Mauritius, South Africa & Nigeria) on broader development as determined by the UN Human Development Index (HDI) for 1997-2017. Their results indicated that while stock market capitalization was positive in the three countries and significant in Mauritius and South Africa, it was insignificant in Nigeria. The positive effect was opined to have been driven by greater capital accumulation and productivity growth from increased financial intermediation and investment funding through the stock market.

Also, Waya (2019) found that market capitalization had a positive but insignificant impact on economic growth in Nigeria in their time series analysis on data from 1999 to 2011 using the same analytical technique, and corroborates earlier study by Donwa and Odia (2010) for 1981-2008. Osamwonyi and Osaseri (2020) examined the economies of South Africa and Nigeria from 1995 to 2015 using panel estimating techniques along with the Granger causality test and ordinary least squares on quarterly data and found that the stock exchange does not lead to economic growth. The conflicting result was adduced to factors such as low market capitalization, small market size, few listed companies, low volume of transactions, low absorptive capitalization, and illiquidity at those earlier periods.

Consequently, the study hypothesizes that:

H01: Stock market capitalization has no effect on economic development in Nigeria.

Market liquidity refers to the ability of buyers and sellers of securities to transact efficiently, and is measured by the speed with which large purchases and sales can be executed at the relative transaction cost (Elliot, 2015). Higher liquidity has been observed to lower the cost of equity capital for firms, enabling easier raising of investment funds for productive projects (Amihud & Mendelson, 1986) and also incentivizing longer-term, higher-return, investments since it is easier for investors to exit positions (Bhide, 1993). Moreover, there are also indications that liquid markets improve the informational efficiency of stock prices through higher trading volumes (Holmström & Tirole, 1993) and also without price impact, facilitating portfolio diversification and risk sharing, but not without tendencies to incentivize speculative short-term trading that delinks prices from economic fundamentals (Rotheim, 1981; Holmström & Tirole, 1993). At very high levels, liquidity could support herd behaviour and stock market volatility (Brunnermeier & Pedersen, 2009).

Kolapo and Adaramola (2012) incorporated stock market liquidity and turnover ratios along with capitalization in their research and found mixed effects on Nigeria’s economic growth from 1986 to 2009. While market size remained positive, liquidity measures were insignificant or negatively related to real GDP per capita in close alignment with Njemcevic (2016) and Christie (2016). Similarly, Omankhanlen (2011) found an insignificant relationship between stock market turnover and economic growth from 1980 to 2009 once controlling for macroeconomic factors like inflation and money supply. The study of Ugherughe and MaryAnn (2019) on stock market indicators and whether they affect HDI in sub-Saharan countries also discovered that stock market liquidity affected South Africa and Mauritius significantly but not Nigeria. Similarly, Wilhelmson and Lidén (2020) investigated the impact of the stock market of 58 countries on their human development index and found out that there was no significant relationship between stock market liquidity and human development index. The authors speculated that volatility from speculators and short-term traders could be diluting the impact of liquidity on development.

On the other hand, others (Tan & Shafi, 2021; Obiakor & Okwu, 2011; Riman et al., 2008) found evidence of positive and significant impact of market liquidity on economic growth per capita in Nigeria at different time horizons. Also, Febra et al. (2023) employed multiple regression analysis to study the effect of stock market liquidity on the economic development of 59 countries, using the Human Development Index as an indicator for economic development rather than GDP. The results suggested that more liquid stock markets promote lower cost of mobilising savings and therefore facilitate better, not only more, investments. Hence, the study hypothesizes that:

H02: Stock market liquidity has no effect on economic development in Nigeria.

Stock market volatility refers to fluctuations in stock prices and returns, reflecting the level of instability and risk in a stock market usually measured by the standard deviation or variance between returns from that same security or market index (the relative volatility of a particular stock to the market is its beta coefficient). A higher level of volatility signifies a greater degree of risk associated with the security in question. Several models suggest high volatility can impede growth. High volatility indicates greater uncertainty, which may deter risk-averse investors and firms from making productive investments (Levine & Zervos, 1998). Extreme volatility in the stock market produces instability in the capital market, destabilizes the value of currency, as well as hampers international trade and finance such that economic growth and stock market volatility are deemed inversely related where causality is found (Bhowmik, 2013). It also makes forecasting and planning more difficult for corporations (Bloom, 2014). In addition, volatility can amplify macroeconomic instability as households adjust consumption based on fluctuating wealth (Jeanne & Rose, 2002). Excessive volatility could also reflect speculative trading and bubbles detached from economic fundamentals (Brunnermeier & Oehmke, 2013).

Empirical evidence (Campbell et al., 2001; Okere and Ndugbu, 2015; Babatunde, 2013; Oko and Onyinye, 2019; Samuel et al., 2019) has established that excessive instability may impede economic growth and development of stock market. The effect on economic growth is mixed in that it is believed that while some volatility facilitates liquidity and trading, others have a negative effect indicating that some optimal level of volatility could be established. Thus, the study hypothesizes that:

H03: Stock market volatility has no effect on economic development in Nigeria.

Methodology

Model Specification

The model which specifies that economic development (proxied by real GDP per capita and Human Development Index (HDI)) is influenced by the stock market indicators (market capitalisation, turnover ratio, volatility of stock market index) is generally formulated as:

GDPPC = ƒ(X) = f (MCAP, TOR, VIX)

HDI = ƒ(X) = f (MCAP, TOR, VIX)

Specifically:

GDPPC = β0 + β1MCAP + β2TOR – β3VIX + ɛ eq. 1

HDI = β0 + β1MCAP + β2TOR – β3VIX+ ɛ eq. 2

Where;

GDPPC = Real Gross Domestic Product Per Capita

HDI = Human Development Index

MCAP = Market Capitalization

TOR = Turnover ratio (measuring market liquidity)

VIX = Volatility of Stock Price Index

ɛ = Stochastic error term within a confidence interval of 5%

β0 = Constant term

β1 – β3 = Coefficients of the independent variables

and β1, β2 & β3

Ex-post facto design was adopted, and annual time-series data were obtained for 20 years, 2003-2022. The data were sourced from the Nigerian Exchange (NGX) Group and the Securities and Exchange Commission (SEC), Nigeria’s National Bureau of Statistics (NBS), and the United Nations Development Programme (UNDP) reports.

Estimation Technique

The study presented descriptive metrics (mean, standard deviation, minimum and maximum values for all variables (real GDP per capita, HDI, market capitalization, turnover ratio and volatility index)). The Shapiro-Wilk test was conducted to check if the data followed a normal distribution. The analysis utilized ordinary least squares (OLS) regression to establish the relationship between the dependent variables (GDP per capita, HDI) and the independent variables (market capitalization, turnover ratio, volatility index). Heteroscedasticity (Breusch-Pagan test) was conducted to confirm the assumptions of the OLS regression.

Data Presentation and Analysis of Results

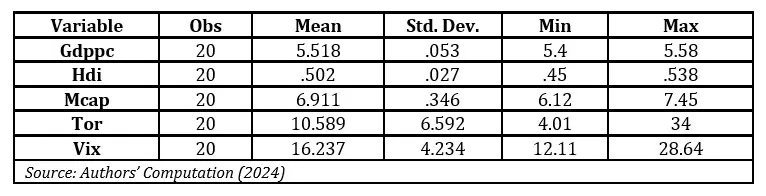

Table 1: Descriptive Statistics

Table 1 shows the mean of real GDP per capita (GDPPC) as 5.518 with a standard deviation of 0.053 suggesting that, on average, the income generated per person in Nigeria is relatively high which indicated a robust economy with significant wealth creation potential. The HDI mean of 0.502 suggested a moderate level of human well-being in Nigeria. The standard deviation suggests disparities in access to education, healthcare, and other essential services among different segments of the population. The mean market capitalization (MCAP) of 6.9 suggested a considerable size and value of listed companies in Nigeria’s stock market which could signify confidence among investors in the Nigerian economy and its growth prospects, though with tendencies towards disparities in the size and stability of different sectors within the economy based on the standard deviation. Market liquidity (TOR) and market volatility (VIX) means are equally presented as 10.589 and 16.237 respectively indicating high liquidity and volatility. The significant difference between the minimum and maximum values of the liquidity variable is an indication that, while some firms performed exceedingly well under the period under consideration, others recorded a significant decline in their performance. Similarly, the volatility variable showed significant minimum and maximum values suggesting that the market was highly volatile.

Regression Analyses

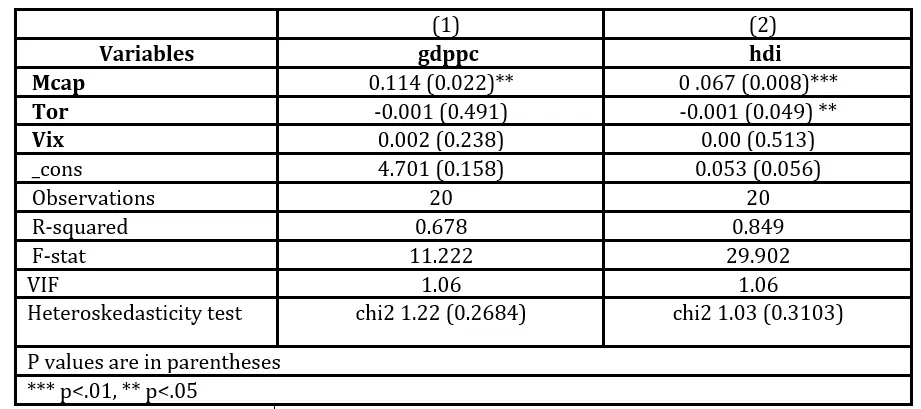

Table 2: Regression Results

Source: Authors’ Computation (2024)

Table 2 above shows results obtained from the estimation of equation 1 and 2 as earlier stated. The results obtained from the mean variance inflation factor (VIF) were conducted to test multicollinearity among the independent variables. For the variables not to suffer from multicollinearity problem, the rule of thumb specified VIF ≤ 10. Our VIF of 1.06 shows that the level of linearity among the independent variables is within the acceptable standard. Furthermore, the Breusch-Pagan test result showed significant p-values on the dependent variables indicating that the assumption of homoscedasticity of the pool OLS regression results has been violated and by implication validating the OLS estimates.

As indicated, MCap showed a positive and significant effect on real GDPpc [coef. = 0.114 (0.022)] and HDI [coef. = 0.067 (0.008)]. Market liquidity had a negative and insignificant impact on real GDPpc [coef. = -0.001 (0.491)] and also negative but significant effect on HDI [coef. = -0.001 (0.049)]. While market volatility exhibited insignificant impacts on real GDPpc [coef. = 0.002 (0.238) and HDI [coef.0.000 (0.513)].

The result of market capitalization aligned with the findings of Kolapo and Adaramola (2012); Jalloh (2015); Njemcevic (2016); Ugherughe and MaryAnn (2019); Tan and Shafi (2021) that market capitalisation is a significant driver of real GDP per capita and HDI as measures of economic development. The study, therefore, negated the hypothesis that market capitalisation does not impact economic development.

Stock market liquidity, however, did not present a consistent result as it showed significant effect only on quality of life as measured by the HDI. This inconsistency in the result could be attributed to the fact that high liquidity could lead to higher volatility that can endanger expected positive returns leading to losses that can impact negatively on the well-being of Nigerians. The finding is consistent with those of Brunnermeier and Pedersen (2009) and Febra et al., (2023), and did not align with our hypothesis that stock market liquidity does not impact human development.

Furthermore, the volatility indicator showed an insignificant result, indicating that stock market volatility is not a driver of economic development in Nigeria. This finding aligned with the study hypothesis that stock market volatility does not impact economic development in Nigeria. This further corroborated the findings of Nzomo and Dombou-Tagne (2017); Guo (2002); and Wang (2010).

Conclusion and Policy Recommendations

Motivated by the challenges in the Nigerian economy, this study examined the effect stock market performance has on Nigeria economic development. Based on the findings, the study concluded that market capitalisation is a major driver of Nigeria economic development. The study inferred further that stock market liquidity has the capacity to further improve Nigeria economic development. Consequently, the study recommended that deliberate measures should be put in place to further open the stock market and make it more attractive to investors because of its ability to improve economic development. Furthermore, while stock market liquidity has been seen to be very important to the development of the economy, measures should be put in place by relevant authorities to ensure that the liquidity position is not abused by unscrupulous entities to the detriment of economic development.

References

Adeusi, S. O. and Azeez, B. A. (2013). ‘Impact of capital market development on the Nigerian economy: A post-SAP analysis.’ Journal of Economics and Behavioral Studies, 5(1), 1-7.

Amihud, Y. and Mendelson, H. (1986). ‘Liquidity and stock returns,’ Financial Analysts Journal, 42(3), 43-48.

Anyanwu, J.C, Oyefusi S.A, Oaikhenan, H. and Dimowa, F.A. (1997). Structure of the Nigerian Economy (1960 – 1997). Onitsha, JOANEE Educational Publishers Ltd., Nigeria.

Anyanwu, J. C. (1998). ‘Stock market development and economic growth in Nigeria,’ Vision, 2(1), 33-38.

Anyanwu, J.C. (1993). Monetary Economic Theory, Policy and Institutions. Uyo, Hybrid Publishers Limited., Nigeria.

Azubuike, A. (2017). ‘Impact of the Nigerian Stock Exchange on economic growth,’ MPRA Paper No. 75984, posted 4/1/2017; downloaded 12/1/2017 https://mpra.ub.unimuenchen.de /75984/

Babatunde, O. A. (2013). ‘Stock market volatility and economic growth in Nigeria (1980-2010),’ International Review of Management and Business Research, 2(1), 201-209.

Barro, R. J. (1991). ‘Economic growth in a cross section of countries,’ The quarterly journal of economics, 106(2), 407-443.

Bencivenga, V. R., Smith, B. D. and Starr, R. M. (1996). ‘Equity markets, transactions costs, and capital accumulation: An illustration,’ The World Bank Economic Review, 10(2), 241-265.

Bhide, A. (1993). ‘The hidden costs of stock market liquidity,’ Journal of Financial Economics, 34(1), 31-51.

Bhowmik, D. (2013). ‘Stock market volatility: An evaluation,’ International Journal of Scientific and Research Publications, 3(10), 1-17.

Bloom, N. (2014). ‘Fluctuations in uncertainty,’ Journal of Economic Perspectives, 28(2), 153-176.

Brunnermeier, M. K., and Oehmke, M. (2013). ‘Bubbles, financial crises, and systemic risk,’ Handbook of the Economics of Finance, 2, Part B, 1221-1288.

Brunnermeier, M. K., and Pedersen, L. H. (2009). ‘Market liquidity and funding liquidity,’ The Review of Financial Studies, 22(6), 2201-2238.

Campbell, J.Y., Lettau, M., Malkiel, B.G. and Xu, Y. (2001). ‘Have individual stocks become more volatile? An empirical exploration of idiosyncratic risk,’ Journal of Finance 56, 1, 1-43.

Central Bank of Nigeria (2007). Capital market dynamics in Nigeria: Structure, transaction cost and efficiency, 1980-2006.

Chinwuba, O., and Amos, O. A. (2011). ‘Stimulating economic development through the capital market: The Nigeria experience,’ Journal of Research in National Development, 9 (2).

Christie, D. İ. K. E. (2016). ‘Stock market efficiency promotes economic development: Empirical evidence from Africa,’ International Journal of Economics and Financial Issues, 6(3), 1287-1298.

Cynthia, U. G., Chinedum, N. N. and Ikechi, K. S. (2021). ‘Effects of capital market development on the economic growth of Nigeria,’ International Journal of Innovation and Economic Development, 7(2), 30-46.

Donwa, P. and Odia, J. (2010). ‘An empirical analysis of the impact of the Nigerian capital market on her socio-economic development,’ Journal of Social Sciences, 24(2), 135-142.

Edame, G. E. and Okoro, U. (2013). ‘The impact of capital market and economic growth in Nigeria,’ Public Policy and Administration Research, 3(9), 7-15.

Elliott, D. J. (2015). Market liquidity: A primer. Economic studies bulletin, The Brookings Institution, 1-13.

Febra, L., Fernandes, M. E. and Silva, T. (2023). ‘Stock market liquidity impact on economic development,’ Rethinking Management and Economics in the New 20’s Springer Proceedings in Business and Economics, 2023, p. 99-117). Singapore.

Guo, H. (2002). ‘Stock market returns, volatility, and future output,’ Federal Reserve Bank of St. Louis Review, 84, 75-86.

Holmström, B. and Tirole, J. (1993). ‘Market liquidity and performance monitoring,’ Journal of Political economy, 101(4), 678-709.

Iyiola, M.A. (2004). Macroeconomics: Theory and Policy. Mindex Publishing Revised edition, Nigeria.

Jalloh, M. (2015). ‘Does stock market capitalization influence economic growth in Africa? Evidence from panel data,’ Applied Economics and Finance, 2(1), 91-101.

Jeanne, O. and Rose, A. K. (2002). ‘Noise trading and exchange rate regimes,’ The Quarterly Journal of Economics, 117(2), 537-569.

Kolapo, F. T. and Adaramola, A. O. (2012). The impact of the Nigerian capital market on economic growth (1990-2010). International Journal of Developing Societies, 1 (1), 11-19.

Levine, R. (1991). Stock markets, growth, and tax policy. The Journal of Finance, 46(4), 1445-1465.

Levine, R. (2001). International financial liberalization and economic growth. Review of International Economics, 9(4), 688-702.

Levine, R. and Zervos, S. (1998). ‘Banks, stock markets and economic growth,’ American Economic Review, 37 (3), 537-558.

Mankiw, N. G., Romer, D. and Weil, D. N. (1992). ‘A contribution to the empirics of economic growth,’ The quarterly journal of economics, 107(2), 407-437.

Megginson, W. L., Smart, S. B. and Graham, J. R. (2010). Financial Management. Cengage Learning.

Morck, R., Yeung, B. and Yu, W. (2000). ‘The information content of stock markets: why do emerging markets have synchronous stock price movements?’ Journal of Financial Economics, 58(1-2), 215-260.

Nigerian Stock Exchange (NSE) Fact Book for 2004 –2022. Lagos: The Nigerian Stock Exchange, https://com

Njemcevic, F. (2016). ‘Capital market and economic growth in transition countries: Evidence from South East Europe. Proceedings of 8th International Conference of the School of Economics and Business, University of Sarajevo, School of Economics and Business Trg oslobodjenja–Alija Izetbegovic 1, Sarajevo, Bosnia and Herzegovina, Vol. 48, p. 146, October.

Nzomo, T.J. and Dombou-Tagne, D. R. (2017). ‘Stock markets, volatility and economic growth: evidence from Cameroon, Ivory Coast and Nigeria,’ Panorama Economico, 12(24), 145-175.

Obiakor, R. T. and Okwu, A. T. (2011). Empirical Analysis of Impact of Capital Market Development on Nigeria’s Economic Growth (1981–2008). DLSU Business & Economics Review, 20, 79-96.

Obstfeld, M. (1994). ‘Evaluating risky consumption paths: The role of intertemporal substitutability.’ European economic review, 38(7), 1471-1486.

Okere, P. and Ndugbu, M. (2015). ‘Macroeconomic variables and savings mobilization in Nigeria,’ International Journal for Innovation, Education and Research. 3, 105-116. 10.31686/ijier.vol3.iss1.304.

Okereke-Onyiuke, N. (2000). Stock market financing options for public projects in Nigeria,’ The Nigerian stock exchange fact book, 41-49.

Oko, O. P. and Onyinye, A. F. (2019). ‘Impact Of capital market on economic growth in Nigeria (1990-2019). Proceedings of 8th Annual International Academic Conference on Accounting and Finance, P. 322, Nigeria.

Omankhanlen, A. E. (2011). ‘The effect of exchange rate and inflation on foreign direct investment and its relationship with economic growth in Nigeria,’ Economics and Applied Informatics, 2011, 1, 5-16.

Onwuka, I.O. and Ozegbe, R.O. (2020). ‘African continental free trade area agreement: Does the facts support the benefits for Nigeria? International Business Research; 13 (7). URL: http s ://doi.org/ ibr.v1 3 n 7 p 2 3 6.

Osamwonyi, I. and Osaseri, G. (2020). ‘A causality study of stock market development and economic growth in Nigeria and Brics. Acta Universitatis Danubius. Administratio, 12(1).

Oyefusi, S. A. and Mogbolu, R. O. (2003). Nigeria and the structural adjustment programme. Nigeria Economy Structure, Growth and Development, Mindex publishing, Benin city, 387-402.

Riman, H. B., Esso, I. E. and Eyo, E. (2008). ‘Stock market performance and economic growth in Nigeria, A causality investigation,’ Global Journal of Social Sciences, 7(2), 85-91.

Romer, P. M. (1994). ‘The Origins of Endogenous Growth,’ Journal of Economic Perspectives. 9(1), 3-22.

Rotheim, R. J. (1981). Keynes’ monetary theory of value (1933). Journal of Post Keynesian Economics, 3(4), 568-585.

Samuel, U. E., Abner, I. P., Inim, V. and Ndubuaku, V. (2019). ‚Monthly stock market volatility on economic growth in Nigeria,’ International Journal of Mechanical Engineering and Technology, 10(10), 131-144.

Tan, Y. L. and Shafi, R. M. (2021). ‘Capital market and economic growth in Malaysia: the role of ṣukūk and other sub-components,’ ISRA International Journal of Islamic Finance, 13(1), 102-117.

Ugherughe, J. E. and MaryAnn, N. I. (2019). ‘Stock market indicators and human development index in Sub-Saharan Africa: The case of Mauritius, Nigeria and South Africa (1997–2017),’ Journal of Finance and Marketing, 3 (3): 28-39.

Wang, X. (2010). ‘The Relationship between stock market volatility and macroeconomic volatility: Evidence from China,’ International Research Journal of Finance and Economics, ISSN 1450-2887, 49, Euro Journals Publishing, Inc.

Waya, A. F. (2019). ‘Nigerian economy under democratic rule and the impact of capital market on its growth,’ Port Harcourt Journal of History and Diplomatic Studies, 6)4), 265-278.

Wilhelmson, L. and Lidén, J. (2020). ‘The stock market and human development,’ Lund University, School of Economics and Management, Unpublished bachelor thesis.

World Bank (1994). Adjustment in Africa: Lessons from Country Case Studies, Washington D.C, The World Bank.

Yadirichukwu, E. and Chigbu, E. E. (2014). ‘The impact of capital market on economic growth: the Nigerian perspective,’ International Journal of Development and Sustainability, 3(4), 838-864.

Yesufu, T. M. (1996). ‘The Nigerian economy: Growth without development,’ Benin Social Sciences Series for Africa, University of Benin, pp. 89-110.