UNIAG, Instituto Politécnico de Bragança (IPB), Bragança, Portugal

Volume 2025,

Article ID 599488,

Journal of Innovation Management in Small and Medium Enterprises,

9 pages,

DOI: 0.5171/2025.599488

Received date: 26 June 2025; Accepted date: 18 July 2025; Published date: 24 September 2025

Academic Editor: Kátia Lemos

Cite this Article as:

Joaquim LEITE, Joana FERNANDES and Ana FERNANDES (2025)," The Balanced Scorecard as a Strategic Cost Management Tool: Insights from a Portuguese Small and Medium Enterprise", Journal of Innovation Management in Small & Medium Enterprises Vol. 2025 (2025), Article ID 599488,

https://doi.org/10.5171/2025.599488

The Balanced Scorecard (BSC) is a strategic management framework that offers an integrated view of organizational performance, supporting managerial control and enhancing long-term competitiveness. While traditionally applied in large enterprises, its adaptation to smaller industrial firms is both relevant and viable, especially considering the operational challenges these firms face – such as limited resources and lack of formalized management systems. This study adopts a case study methodology focusing on a small industrial enterprise. Data collection involved interviews with the company’s manager, yielding both financial and non-financial information. Quantitative data were analyzed using Microsoft Excel, while qualitative insights were structured around the central research question. A strategy map was developed, featuring two strategic objectives per BSC perspective, along with associated indicators, targets, and initiatives. The findings emphasize the BSC’s value as a strategic planning and control tool in resource-constrained environments, contributing to improved decision-making. Moreover, the study adds to existing literature by demonstrating the practical relevance of the BSC in uncertain and economically challenging contexts.

Keywords: Performance measurement, Cost Management, Balanced Scorecard (BSC), Small and Medium Enterprise (SME), Case Study, Portugal.

Introduction

This paper is organized into five fundamental sections. The first corresponds to the introduction, where the theoretical framework of the Balanced Scorecard (BSC) is presented, highlighting its relevance to the research objectives. The second section presents the methodology adopted. The third section focuses on the presentation and analysis of the results obtained. Finally, the last two sections are dedicated to discussing the results in the light of the theoretical framework and presenting the study’s main conclusions.

Management accounting and control emerged with the industrial revolution and the appearance of large factories, and the evaluation of organizational performance was based exclusively on financial indicators (Blocher et al., 2019). This branch of accounting has followed the evolution of technology in production processes (Drury, 2018), becoming a powerful cost control tool, providing different spending information for the various needs of managers (Silva, 2016). The main objective of management control is to calculate, analyze and allocate industrial costs according to the criteria used in the company, in order to obtain relevant data for industrial management control (Caiado, 2011; Rajan and Datar, 2018). However, in recent decades, it has been shown that the incorporation of non-financial indicators provides a more comprehensive and informed view of organizational performance (Lonbani et al., 2015; Gupta and Salter, 2018).

The management of a company must make decisions by planning, controlling and selecting operations, and monitoring is necessary as the results develop (Major and Vieira, 2018). Managers must make decisions based on well-organized and well-founded information. All organizations need to have well-defined strategic expense management in order to be able to follow and achieve their objectives in the market, as this type of strategic management is seen as an evolution of cost management techniques (Silva, 2016). This tool monitors the company’s internal factors very dynamically, acting as a decision-making tool.

For a company’s management to be able to make decisions, the BSC tool needs to provide timely, real and quality information. To this end, management will have to carry out daily planning of expenses, classification and analysis of possible cost reductions or improvements in the production process, in an organized way that allows company managers to make the right decisions (Silva, 2016). Such decisions can involve company financing. Technical competence and the diversification of funding sources are key to increasing the effectiveness of sustainable financing, involving the definition of priorities through the BSC (Kurbanova et al., 2025). However, a context of uncertainty involves risk. For this reason, the BSC and enterprise risk management can function as a hierarchical control mechanism, with the BSC being the more predominant practice and enterprise risk management the more ancillary practice, but used for recognition and legitimization purposes (Huber et al., 2025). Even with this difference in purpose associated with both, enterprise risk management can influence the BSC itself.

Within this framework, Kaplan and Norton (2018) developed the BSC, a strategic management model that makes it possible to articulate organizational objectives with the information relevant to their pursuit, and which has been widely adopted and studied in the specialized literature. This management tool is a strategic performance evaluation system (Kaplan and Norton, 1996). According to Neves (2011), the BSC is a strategic management model that translates the organization’s vision and strategy into objectives, indicators, targets and initiatives organized into four distinct perspectives: financial, customer, internal processes and, finally, learning and growth.

Given the recognized effectiveness of the BSC in the strategic management of large companies in different international contexts, its adaptation to small industrial companies is not only pertinent, but also feasible. These entities, due to their smaller structure and limited resources, tend to lack management systems guided by a strategic vision, thus compromising the effectiveness of the planning and control of their activity. Such a vision can integrate aspects of sustainability, namely the concept of Sustainability BSC (SBSC), already recurring in the literature in recent years, reflecting an integration of the Sustainability Development Goals into the original BSC, incorporating environmental, social and economic sustainability factors (Quesado, 2025). Both models (original BSC and SBSC) have enormous potential for monitoring performance and supporting decision-making, but both require constant updating and adaptation to meet the challenges of each specific organization (Li, 2024). This demonstrates the difficulty these models have in integrating increasingly dynamic and real-time determinants, making it necessary to use the flexibility the models contain in order to quickly make them more agile.

Based on the theoretical framework set out above, the following research question was formulated: how can a BSC proposal be drawn up for a small industrial company in a specific context? This problem arises from the need to implement strategic management tools capable of generating structured and relevant information, which is essential for managing and controlling costs in small industrial businesses.

Methodology

This work seeks to explore how to develop a BSC proposal in a small industrial company in a concrete context, in order to be used as a decision support tool. The theoretical basis is supported by management control (Drury, 2018; Major and Vieira, 2018), particularly the BSC (Huber et al., 2025; Kaplan and Norton, 2018; Kurbanova et al., 2025; Quesado, 2025). The data analyzed were obtained from internal company documents and through a semi-structured interview with the company manager. The data were processed using content analysis, focusing on the research question.

The methodological approach adopted was the single case study (Yin, 2017), a choice consistent with the holistic nature of the phenomenon under analysis and widely recognized in the literature on management control in specific organizational contexts. This type of qualitative methodology allows for an in-depth analysis of questions that arise in the form of “how”, and is especially pertinent for research where contextual complexity conditions management practices (Spanò et al., 2020). Qualitative approaches, through the case study method, in public and private entities, have been widely used in a variety of research into the design (proposals), implementation and use of the BSC, not only in terms of economic and financial results, but also in terms of political and social factors (Barros, 2025).

Results

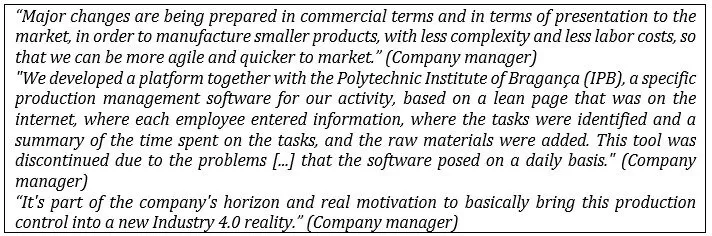

In order to draw up the strategy map, it is essential to understand the control mechanisms currently in place at the company. According to the manager, production cost control is carried out using Excel sheets, in which, at the end of each product, the costs of raw materials and labor are recorded. Although efforts have been made to create automated tools, these initiatives were later discontinued due to recurring errors and the lack of effective monitoring. Thus, current management is still based on a manual process, susceptible to inaccuracies and dependent on the operational rigor of employees.

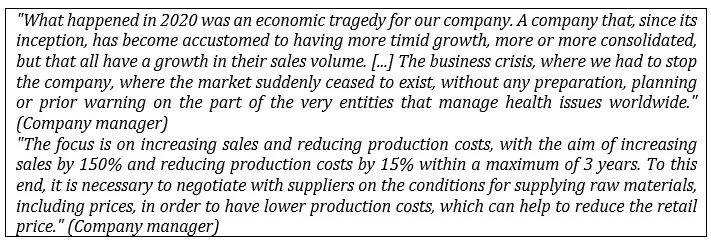

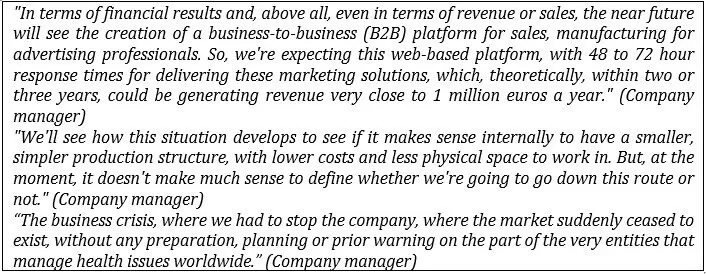

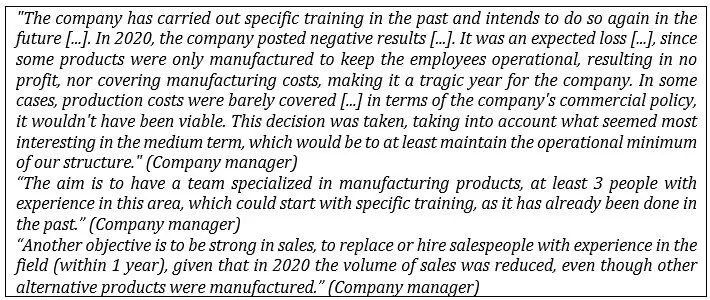

With regard to employee training, recruitment, motivation and individual team skills, it’s important to note that in the past the company implemented a specific training course for its activity. This investment in training is now intended to be repeated in the future, with a view to strengthening employees’ technical and motivational skills. The year 2020 was notable for the company’s negative results, a loss that the manager had anticipated. The production of certain products was only intended to keep the team operational, without generating any profit margin or even helping to cover manufacturing costs.

The strategic map developed reflects, in an integrated way, the cause-effect relationships between short-term initiatives and medium-term strategic objectives. This tool was built using the accounting information provided and based on the perspectives outlined in the interview with the company manager.

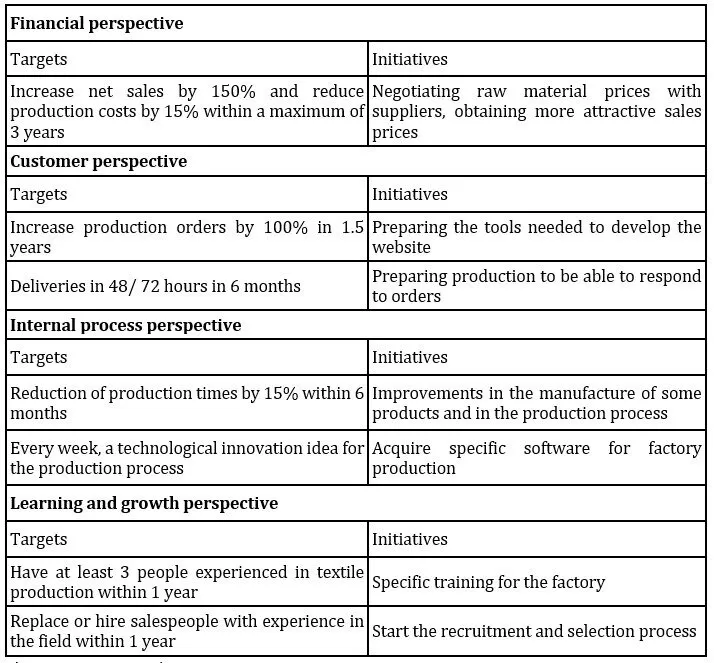

Tables 1, 2, 3 and 4 summarize the information from the interview with the company manager regarding the financial, customer, internal processes and learning and growth perspectives, respectively.

Table 1: Excerpts from the interview that support the objectives: financial perspective

Source: Authors’ own elaboration

Table 2: Excerpts from the interviews that support the objectives: customer perspective

Source: Authors’ own elaboration

Table 3: Excerpts from the interviews that support the objectives: internal processes perspective

Source: Authors’ own elaboration

Table 4: Excerpts from the interviews that support the objectives: learning and growth perspective

Source: Authors’ own elaboration

Analysis of the data systematized in the four tables presented above made it possible to identify the relevant strategic objectives for the company. Performance indicators, targets and initiatives to be implemented were associated with each of these objectives. These objectives and respective indicators were structured according to the four perspectives of the BSC, as detailed in Tables 5, 6, 7 and 8. This organization aims to ensure an integrated view of the strategy, facilitating continuous monitoring and alignment between operational execution and the company’s strategic objectives.

Table 5: Objectives and indicators: financial perspective

Source: Authors’ own elaboration

Table 6: Objectives and indicators: customer perspective

Source: Authors’ own elaboration

Table 7: Objectives and indicators: internal process perspective

Source: Authors’ own elaboration

Table 8: Objectives and indicators: learning and growth perspective

Source: Authors’ own elaboration

Table 9: Targets and Initiatives for the Strategy Map

Source: Authors’ own elaboration

The tables above made it possible to identify and associate each strategic objective with a performance indicator suitable for monitoring it in the context of the BSC. The objectives and respective indicators were organized according to the four classic perspectives of this strategic management model: financial, customers,

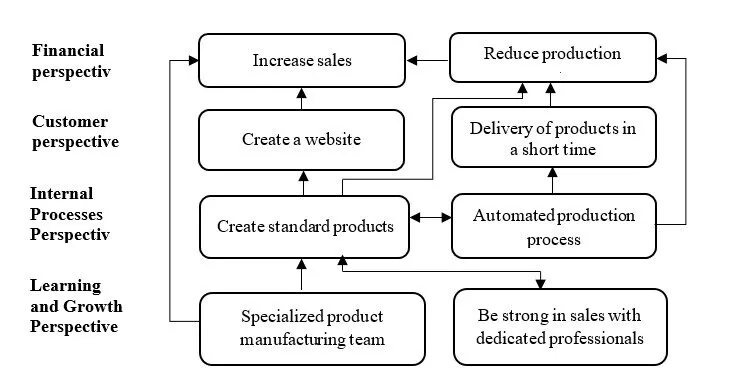

internal processes, and learning and growth. In order to represent the cause-effect relationships between the financial and non-financial objectives in a clear and integrated way, a specific strategy map was drawn up for a small industrial company, as shown in Figure 1.

Figure 1: Strategy map in BSC perspectives

Source: Authors’ own elaboration

The main objectives of the financial perspective are to increase sales by 150% and reduce production costs by 15% over a three-year period. Achieving these goals requires negotiating the supply conditions for raw materials, namely price levels, in order to reduce production costs and help reduce the retail price. This strategy could also boost sales growth, in line with the efforts outlined from a customer perspective. The results obtained, although lower than intended, were what was expected given the pandemic context, and the goals set from this perspective are geared towards a sustained recovery in a more favorable context.

From the customers’ perspective, the first objective is to create a digital business-to-business (B2B) platform, which will allow customer companies to customize the products they want and view the final product in real time. This initiative aims to double the number of production orders within 18 months. In addition, the second objective is to deliver products within 48 to 72 hours of the order being placed, a target to be achieved within six months. Achieving this goal requires production to be able to respond effectively, which means adapting human resources to the requirements of demand.

The main objective of internal processes is to create standard products, taking into account the characteristics of the products. Over a period of six months, the aim is to reduce production times by around 15% by improving the manufacturing of certain products and the production process. However, another objective is to automate the production process which, according to the company manager, is a complex process, since the products are made to measure. If the previous objective from this perspective is achieved, it will be easier to do so by controlling production times and

calculating costs directly through specific production software.

Finally, from the perspective of learning and growth, the goal is to have a team specialized in manufacturing products, at least 3 people experienced in this area, who can start with specific training. Another objective is to be strong in sales, replacing or hiring salespeople with experience in the field (within 1 year), given that in the period under review the volume of sales was low, even though other alternative products were manufactured.

Discussions

Drawing up a strategy map based on the BSC, incorporating two strategic objectives per perspective and the respective indicators, targets and initiatives, reinforces the applicability of this model in small industrial companies. The results show the potential of the BSC as a tool for integrating relevant information for strategic management, especially in contexts marked by high uncertainty and economic and financial restrictions. As advocated by Kaplan and Norton (2018), the BSC makes it possible to align organizational strategy with operational objectives, making the company’s value creation logic visible. In the case under study, this logic materializes in the articulation between short-term objectives (such as cost reduction) and medium- and long-term goals (such as strengthening competitive capacity). The relevance of this alignment is widely recognized in the literature, which highlights the importance of the BSC in translating strategy into concrete action (Kaplan & Norton, 1996; Neves, 2011).

The applicability of the BSC in unstable environments, such as those faced during and after the pandemic, also demonstrates its usefulness as a strategic control and decision support tool. As Silva (2016) and Kurbanova et al. (2025) state, access to timely and reliable information, as well as the ability to plan and classify expenses, are fundamental for making sustainable financial decisions, especially in companies with limited resources. Integrating the BSC with complementary practices, such as corporate risk management, extends its reach even further, acting as a hierarchical control mechanism, where the BSC predominates as a strategy structuring system, and risk management works as a complement to legitimize critical decisions (Huber et al., 2025). This study therefore reinforces the practical usefulness of the BSC not only as a planning tool, but also as a means of legitimizing management in the face of risk and alternative financing scenarios.

In addition, the results obtained in this study suggest that the adoption of the BSC in small industrial companies can help to overcome weaknesses typical of the absence of a structured strategic vision. As Quesado (2025) and Li (2024) point out, both the traditional BSC model and its sustainable versions (SBSC) show great potential for adapting to different contexts, as long as they are continuously updated and adjusted to the specific dynamics of each organization. The integration of sustainability dimensions – economic, environmental and social – is increasingly valued, which reinforces the need for more agile strategic management models that are sensitive to external demands. In this sense, the results of this study contribute to the academic debate by demonstrating, on an empirical basis, the feasibility of implementing the BSC in small organizational structures, even in adverse environments, highlighting its value as a tool for resilience and strategic development.

Conclusions

This research used the case study method in a small industrial company to assess how the use of the BSC tool can support strategic cost management decisions, by drawing up the company’s strategy map. The study made it possible to understand how the company’s planning and cost control is carried out and how management tools help in strategic decision-making. An integrated management system allows the organization to function smoothly. At the company, it is not yet possible to carry out rigorous cost control, and the management believes that it needs software to evaluate and control spending. Through a strategic map according to the BSC, it is hoped to achieve strategic objectives and significant improvements in financial and non-financial management indicators, in a context of economic and financial instability.

The fact that this study is a qualitative investigation applied to a single company, in an adverse context, very much focused on production costs, can be pointed to as the main limitation of this work. Another limitation was the fact that only one of the company’s managers was interviewed. For future scientific research on the subject covered in this study, we suggest comparing the results obtained before implementing the BSC strategy map with those after implementation. Finally, a more comprehensive study is recommended, comparing the company’s situation with other industries in the same sector.

References

Barros, R. S. (2025), ‘Research on the balanced scorecard for government entities: A literature review,’ Journal of Public Budgeting, Accounting and Financial Management, 37(3), 415–440. https://doi.org/10.1108/JPBAFM 10 2022 0162

Blocher, J., Stout, E., Juras, E. and Smith, S. (2019), ‘Cost management: A strategic emphasis,’ 8th ed., McGraw-Hill Education.

Caiado, C. (2011), ‘Contabilidade analítica e de gestão,’ 6th ed., Áreas Editora.

Drury, C. (2018), ‘Management and cost accounting,’ 10th ed., Cengage Learning EMEA.

Gupta, G. and Salter, S. (2018), ‘The balanced scorecard beyond adoption,’ Journal of International Accounting Research, 17(3), 115–134. https://doi.org/10.2308/jiar-52093

Huber, C., Kraus, K. and Meidell, A. (2025), ‘Integrating the balanced scorecard and enterprise risk management: Exploring the dynamics between management control anchor practices and subsidiary practices,’ Management Accounting Research, 66, 100924. https://doi.org/10.1016/j.mar.2024.100924

Kaplan, R. and Norton, D. (2018), ‘Mapas estratégicos: Convertendo ativos intangíveis em resultados tangíveis,’ 1st ed., Alta Books.

Kaplan, R. and Norton, D. (1996), ‘The Balanced Scorecard: Translating strategy into action,’ HBS Press.

Kurbanova, K. A., Nurmagambetova, A. Z., Nurgaliyeva, A. M., Dinçer, H., Yüksel, S. and Sigayev, Y. A. (2025), ‘Balanced Scorecard Based Project Priorities of Sustainable Energy Financing Via Artificial Intelligence Enhanced Hybrid Quantum Decision Making Modeling,’ Studia Universitatis “Vasile Goldis” Arad – Economics Series, 35(2), 113–139. https://doi.org/10.2478/sues-2025-0010

Li, W. (2024), ‘Effectiveness of the Balanced Scorecard in Enhancing Firm Performance,’ Journal of Human Resource Development, 7(1), 44–50. https://doi.org/10.23977/jhrd.2025.070107

Lonbani, M., Sofian, S. and Baroto, B., (2015), ‘Linking balanced scorecard measures to SME’s business strategy: Addressing the moderating role of financial resources,’ International Journal of Research, 3(12), 9299. https://doi.org/10.29121/granthaalayah.v3.i12.2015.2893

Major, M. J. and Vieira, R. (2018), ‘Contabilidade e controlo de gestão,’ 2nd ed., Escolar Editora.

Neves, F. (2011), ‘O Balanced Scorecard como instrumento de alinhamento estratégico nas organizações,’ [Tese de Doutoramento, Instituto Universitário de Lisboa] Repositório do Instituto Universitário de Lisboa. https://repositorio.iscte-iul.pt/handle/10071/3361 (accessed: June 12, 2021)

Quesado, P., Costa Oliveira, H. and Silva, R. (2025), ‘Integrating sustainability goals into the balanced scorecard: a bibliometric analysis of the sustainability balanced scorecard,‘ Measuring Business Excellence, 29(2), 352-367. https://doi.org/10.1108/MBE-09-2024-0139

Rajan, M. and Datar, S. (2018), ‘Horngren’s cost accounting: A managerial emphasis,’ 16th ed., Pearson.

Silva, M. L. (2016), ‘Mapeamento de técnicas de controlo de gestão nas 500 maiores empresas Portuguesas: aplicação de Target Costing,’ [Dissertação de mestrado, Instituto Superior de Economia e Gestão] Repositório da Universidade de Lisboa. http:// hdl.handle.net /10400.5/12681 (accessed: July 22, 2021)

Spanò, R., Caldarelli, A., Ferri, L. and Maffei, M. (2020), ‘Context, culture and control: A case study on accounting change in an Italian regional health service,’ Journal of Management and Governance, 24(1), 229-272. https://doi.org/10.1007/s10997-019-09458-0

Yin, R. (2017), ‘Case study research and applications: Design and methods,’ 6th ed. Sage Publications.