This research empirically studies the factors that influence the intention of SME owners and managers to adopt m-banking in rural Bangladesh. The study specifically focuses on business oriented m-banking, such as paying suppliers or receiving payments from customers, and on person-to-person use of m-banking. Although over the last ten years a wide spectrum of m-banking frameworks has emerged in various countries, very few research have focused on SMEs m-banking adoption and acceptance of the service. Another rationale for undertaking such a study is that m-banking has not yet been extended to rural Bangladesh. To fill the gap this research surveyed 550 SMEs owners/managers in four (4) rural villages. The survey indicates that poor banking facilities, cost, credibility, gender, education and SME business type are the main factors that significantly influence the intention to adopt m-banking. The analysis focuses on the three factors that have been largely overlooked in prior literature, that are banking satisfaction, m-banking advantages for SMEs, and SME business type. The study broadens our understanding of m-banking and provides insights into developing m-banking strategies in Bangladesh. This research will be of potential value in accelerating the development of m-banking in Bangladesh.

Keywords: M-banking framework, Virtual banking, Individual perception, Country studies

Introduction

Over the past two decades there has been a growing impetus worldwide towards the adoption of m-banking for the unbanked population. The small and medium enterprises (SMEs) are part of this unbanked sector, deprived of sophisticated banking facilities while playing a major economic role in the developing countries (Nichter & Goldmark 2009). SMEs in most countries, like their smallness always receive small support and favourable banking facility. Historically banking has been one of the major constraints for SMEs (Ardic et al. 2012, Beck & Demirgüç-Kunt 2006, Harvie 2004, Levy 1999). However, some research studies in other parts of the developing world have established m-banking as a suitable banking system for SMEs (Bångens & Söderberg 2011, Higgins et al. 2012, Kumar et al. 2011). Research studies suggest that the commercial banks can target SME owners as a user group since SMEs retail payment is surprisingly high (Bångens & Söderberg 2011). In spite of numerous studies on m-banking, which are largely conducted from the individual perspective, very few research provide insights into the adoption and acceptance of m-banking by SMEs. M-banking however is now at the centre of intense national interest in countries like South Africa, Kenya, Philippines and India etc. More recently, in Bangladesh, the central bank’s initiative to offer banking service to the unbanked population has sparked the m-banking implementation by various commercial banks such as Trust bank, Dutch Bangla Bank, BRAC bank etc. (Rahman 2012).

Despite the huge potential of m-banking in Bangladesh, not much research effort has been devoted in this area, by comparison with other countries. Moreover, m-banking providers consider Bangladesh as a market but they do not target it as a specific market. But Medhi et al. (2009) suggest that an unbanked market should to be targeted first and then answers should be given in relation to how m-banking could be adopted in that market. Another important criticism on the m-banking research in Bangladesh is that, to date all the attempts are too technology-led (Mousumi & Jamil 2010). The researches include business models but exclude social models. It is important to consider the technological, contextual and social perspectives on which m-banking adoption depends (Bankole 2011; Daud et al. 2011; Kadušić et al. 2011; Min et al. 2011; Yang 2011). M-banking services are still in their infancy, leaving a great deal of room for development. The availability of the service alone does not ensure that SMEs will adopt the service. Predicting SMEs’ intention is important. There is a need, therefore, to understand their acceptance of m-banking and to identify the drivers, inhibitors, risk, satisfaction and usability factors affecting Bangladeshi SME’s intentions to use m-banking. This information can improve the building of m-banking systems that SMEs want to use, and help discovering why potential SMEs avoid using the existing system. Failure to understand any one of the factors may result in failure to capitalize on the benefits of m-banking. For Bangladesh, the failure could be severe: a step backward.

To fill the current gap, this study investigates a customer perspective framework for rural SMEs in Bangladesh. The research is being undertaken at the right time as it is expected to support the national policies, such as Millennium Development Goal 2015 and the National IT Policy 2009 undertaken in Bangladesh. This research is significant to the SMEs, banks, MTOs in Bangladesh. It contributes greatly to the understanding of how to deliver financial services for rural SMEs in Bangladesh using m-banking.

Literature Review

With 75 million mobile phone users, 45% unbanked population, and 99% of the population within the mobile network (Bangladesh bank 2012; BRTC 2012; CIA 2012), Bangladesh has encouraged the banks, telecoms and the central bank to come forward in the introduction of m-banking. M-banking was first introduced as Short Message Service (SMS) banking by the private banks in Bangladesh. The early m-banking service had very limited functionality, such as viewing own account details, balance and mini statement. However, with the deregulation of policy on 29th November 2009, current m-banking services in Bangladesh offer cash-in, cash-out, fund transfer for merchant payment, salary disbursement and utility payments (Rahman 2012).

In spite of the industry efforts to implement m-banking, not much research effort has been devoted to rural Bangladesh. Existing research efforts on m-banking in Bangladesh focused the customer and technology perspectives (Ahmed et al. 2011; Dewan & Dewan 2009; Mousumi & Jamil 2010). However, three problems are found with their customer perspective. Firstly, instead of using strong empirical evidence, the research studies are founded on a small number of participants. Secondly, a strong research tradition in m-banking worldwide shows that social factors have a powerful influence on m-banking adoption; but current research on m-banking in Bangladesh have not considered this socio-cultural approach. Moreover, the research studies have not considered any Information System (IS) adoption theories, but IS theories are important in explaining the adoption of IS. Furthermore these theories as have a relation to the individual’s preference and reaction (Goodhue & Thompson 1995). Thirdly, the m-banking research tends to under-estimate the true extent of customers’ intention to use the service by narrowing cognitive factors of human behavior. One research has attempted to predict young consumers’’ m-banking choice; but the research is city based, and rural settings (65% of the population) are ignored (Ahmed et al. 2011; Dewan & Dewan 2009). This research is one of the earliest attempts to examine m-banking in a rural Bangladesh setting.

M-banking has gained great interest in the research community worldwide as it is expected to have an impact in developing countries. Existing m-banking research mainly focus on advantages, adoption, design and technology. Scholars suggest that for developing countries, m-banking can reduce ‘walking many kilometres for the banking’ (Medhi et al 2009) and m-banking is a panacea for the poor (Aker & Mbiti 2010; Dunmcombe & Boateng 2009). M-banking has the potential to offer low cost virtual bank accounts to the large number of unbanked individuals worldwide (Bangens & Soderberg 2008; Dejan 2011; Dolan 2009; Medhi et al. 2009), to women living at the bottom of the society (Chavan et al. 2009), to the farmers (Kirui 2010) and to the SMEs (Bångens & Söderberg 2011). A recent study by Bångens and Söderberg (2011), reports that SMEs usage of m-banking is very high in Tanzania. Aker & Mbiti (2010) and Donner & Camilo (2008) suggest, m-banking thus have a correlation to the economic development. However, the most popular topic in m-banking research is the customer perspective that concentrates on adoption, acceptance and usage of m-banking (Brown et al. 2003).

Over the last ten years, a wide spectrum of m-banking frameworks has emerged in various countries. Frameworks are pivotal for the explanation of the factors and determinants of m-banking (Brown et al. 2003). They include consumer, technical, social, and security perspectives and apply Information Systems (IS) adoption theories to explain the individual’s preference and reaction. The most popular IS theories in m-banking research are the classic Diffusion of Innovations Theory (Roger 1995), Technology Acceptance Model (TAM) and the extended TAM (Davis 1989), the Theory of Planned Behaviour (TPB) (Taylor & Todd 1995) and the Unified Theory of Acceptance and Use of Technology (UTAUT) (Venkatesh et al. 2003). These theories concentrate on individual needs, user characteristics, and consumer behaviour and describe sociological factors (Donner 2008). Bankole and Cloete (2011), Daud et al. (2011) and Kadušić et al. (2011) have used IS theories in developing an m-banking framework. In some cases, the researchers extended the actual model or combined two models to explain the possible adoption and acceptance patterns (Tobbin 2009). However, Luarn and Lin (2005) identify volitional elements of TAM as a limitation and added two new constructs from TPB in addition to the factor perceived credibility.

The latest m-banking frameworks have more dimensions and variations of factors. For example, adoption is tested together with satisfaction (Jia-bao 2011), social cognitive factors (Ratten 2011), cost-benefit perception on adoption (Shen et al. 2010), trust transfer from online to M-banking (Wei 2011), usability comparisons between SMS banking and Interac¬tive Voice Response (IVR) (Peevers 2011). A most recent m-banking framework examines the individual’s entrepreneurial adoption decision to use m-banking (Ratten 2011). Some research also tests religious belief on m-banking adoption (Amin 2011).

Despite the fact that m-banking frameworks have been developed using data from different countries (Bankole & Cloete 2011; Laukkanen & Pedro 2012), research indicates that m-banking frameworks are highly contextual. Factors have varied effects in different regional contexts. Amin et al. (2008) report that perceived ease is an m-banking factor in Malaysia, while Daud et al. (2011) find no significant relationship. There is therefore a need, to understand the adoption drivers, motivators and the factors of the users in each specific country.

Research Question and Hypothesis Development

The research will provide an answer to the question: what factors influence the intention of rural SMEs in Bangladesh to adopt an m-banking service? To answer the question this paper reports on a survey among rural SMEs in Bangladesh. The questionnaire was administered in a face-to-face setting to understand the mindset of the people and to overcome any literacy difficulties.

Hypothesis Development

This research is established on the premises of IDT, TPB, TAM, and the m-banking framework by Luarn and Lin (2005). The paper considers the factors reported in several related works, such as factors of perceived usefulness, perceived ease of use, perceived credibility, perceived risk, cost and demographics. However, the research also contributes to the body of knowledge by introducing three new factors which impact on on the intention to adopt m-banking, namely banking satisfaction, m-banking advantages for SMEs, and SME business type. These factors are rarely mentioned in prior studies.

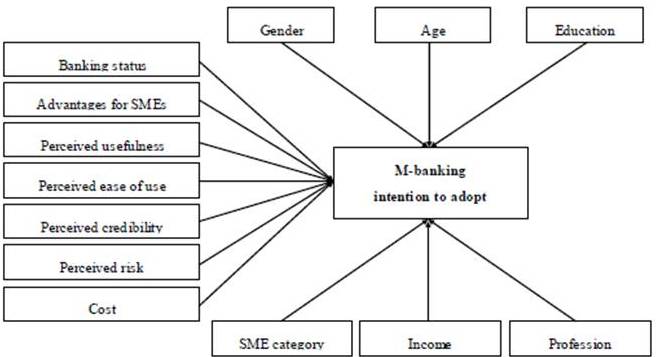

The factors which were considered in this study and the hypotheses which relate to them are listed as follows and summarized in Figure 1:

Figure 1.M-Banking Framework Based on the Hypotheses

Banking Status

M-banking is growing fastest and furthest in developing countries as traditional bricks-and-mortar banking excludes the poor and rural citizens in these countries. In m-banking research this variable is not often considered, except by Bångens and Söderberg (2011) and Brown et al. (2003). In Bangladesh rural SMEs are deprived of any banking facilities. This can be a reason for the uptake of m-banking in Bangladesh. The research thus includes a hypothesis:

H1: Poor banking facilities for SME owners/managers will lead to a higher intention to adopt m-banking

Relative Advantages for SMEs

Taylor and Todd (1995) define relative advantage as the extent of benefits the service offers over previous ways of performing the same task. Previous studies suggest that m-banking offers additional value, such as location-free access, real-time banking, ubiquitous purchase etc. (Brown et al. 2003; Tobbin 2009; Riquelme & Rios 2010; Jia-bao 2011). For rural SMEs, m-banking can offer easy payment, effective management and convenient banking. This forms the basis for the following hypothesis:

H2: The greater the perceived advantages of using m-banking for SMEs, the more likely that it will be adopted

Perceived Usefulness

Usefulness is the ability to enhance performance using a particular system (Davis 1989). Perceived usefulness has a significant effect on m-banking adoption (Daud et al. 2011; Luarn and Lin 2005; Min et al. 2011; Tobbin 2009). Rural SMEs will use the service if the users find it useful in saving banking time, increasing productivity, or enhancing effectiveness. The research presents a hypothesis:

H3: Higher perceived usefulness of m-banking will lead SME owners/managers to higher intention to adopt.

Perceived Credibility

Perceived credibility refers to the security and privacy concerns of the users. New users of an electronic system may have concerns with the unsanctioned intrusions or outflows of personal information, fear of the lack of security and unnecessary intrusion by the system (Daud et al. 2011; Luarn and Lin 2005). Online transactions are new in Bangladesh, so it is important to know SME owners/managers’ concerns about divulging banking information online. Hence the research posits:

H4: Perceived credibility of SME owners/managers will have a positive effect on intention to adopt m-banking

Perceived Ease of Use

To capitalize on the benefits of m-banking, it has to offer easy use of the system. Davis (1989) defines ease of use as the degree to which a person believes that using a particular system would be effortless. In m-banking, empirical results illustrate that perceived ease of use is related to the intention of acceptance of m-banking in non-users (Luarn & Lin 2005; Lin 2011; Min et al. 2011). This research includes the hypothesis:

H5: Perceived ease of use of m-banking will have a positive effect on the intention to adopt m-banking in rural SMEs.

Perceived Risk

Risk is at the centre of all banking transactions. Risk is defined as a consumer’s belief about potential uncertainty (Tobbin 2009). Customer perceptions of uncertainty in the areas of finance, performance, privacy and time are barriers to m-banking (Anus et al 2011; Brown et al 2003). Risk may have the most significant negative impact if the users do not have prior experience of electronic transactions (Tobbin 2009). The hypothesis is presented below:

H6: SME owners/managers’ greater perceived risk of m-banking will have a negative impact on the intention to adopt.

Perceived Cost

In m-banking, there are some costs associated with the service, such as traffic billing, commission charges and flat fees. The price has an effect on the motivation to accept or reject the service but also perceptions of price are important for customers who have not yet tried the service (Luarn & Lin 2005; Yao & Zhong 2011). Therefore, a hypothesis is included:

H7: Perceived financial cost will have a negative effect on m-banking intention to adopt for SME owners and manager.

Demographic and Socioeconomic Factors

Some researchers have predicted that m-banking adoption is related to an individual’s demographic status, such as gender, age and education, and to socioeconomic factors (Laukkanen & Cruz 2012). The followings are hypotheses based on these factors:

H8: Gender of the SME owners/managers will have an effect on m-banking adoption. H9: Age will have an effect on m-banking adoption. H10: Level of education will have an effect on m-banking intention to adopt. H11: Occupation will have an effect on m-banking intention to adopt. H12: SME owner or manager’s income will have an effect on intention to adopt m-banking. H13: Business type of the SME will have an effect on the intention of the owners to adopt m-banking.

Research Methodology

This research is descriptive and was conducted using a quantitative method. A survey was administered to rural SMEs in Bangladesh. In this research, m-banking is defined as performing balance checks, account transactions, payments, transfers, etc. using a mobile phone. M-banking can be either for existing banking customers or for the new unbanked customers. The research focused on small and medium enterprises in the rural Bangladesh having assets of Taka (Bangladeshi currency) 15 million to 200 million and/ or a maximum 150 employees. The dependent variable is the intention to adopt m-banking. Traditionally intention is measured using a Likert scale, but the intention can also be measured dichotomously (Ajzen & Fishbein 1969). In this research the dependent variable has three possible outcomes: intention, indecisive and no-intention. The intention category has expressed to use m-banking service as soon as the service becomes available to them and the no-intention category has no intention to use the service at the moment. Selection of Villages and Survey Participants

The survey was conducted in four villages in the Ganbandha district of the Rajshahi division of Bangladesh. The villages provide a microcosm of rural Bangladesh. Like other villages, agriculture provides the main source of livelihood. SMEs provide the second source of income (Davis et al. 2010). But in the none-harvest session and in the time of drought or flood when agriculture is not possible, SMEs are the only option of livelihood in these villages. Like the country as a whole, the villages are predominantly Muslim with a Hindu minority (Schendel 2009). The villages are not close to any big cities, approximately 20-30 kilometres from the district headquarter. So the urban influence has little effect on the villages. The district is considered among the poorest in Bangladesh. Though there are several government bank branches, private commercial banks (PCB) do not consider these villages viable for business as PCBs are heavily skewed in favour of wealthy and urban centres. Till to date no commercial bank has opened a branch in any of these villages. But in Bangladesh, PCBs have gained significant success in poverty alleviation and economic development. Bangladesh Bank also disburses loan through PCBs. However, these are some reasons for selecting these villages.

SME owners/managers who had a mobile phone or had an intention to buy a mobile phone were included in the survey. The research undertook a purposeful selection of SME owners/managers that provided a balanced and representative sample. SMEs were heterogeneous in terms of type and size. Some participants had a bank account while the rest were from the cash economy. Some were educated, some semi-educated and some uneducated. Both male and female participants were included. The research surveyed 550 SMEs owners and managers. The large sample size makes the result strong and significant.

Developing and Pre-Testing the Questionnaire

This research used a survey which was administered to SMEs within rural villages in Bangladesh. The researcher prepared an initial survey questionnaire based on the hypotheses. The survey questionnaire was then pre-tested by a group of IT professionals, bank officers and Telco officials. The participants were given the questionnaire in both English and Bangla. The pre-testing helped the researcher to gauge the clarity of questions, to understand whether the instrument was capturing the desired phenomena and to verify if any important variable was not being omitted. Feedback served as a basis for correcting, refining and enhancing the survey questionnaire. Changes were made and several iterations were conducted.

ThePilotStudy

A pilot survey was conducted on in August 2011 in the business union office of a village namely Lakxipur to test the survey instrument in terms of its wording, the sequence of questions and the layout of the questions. It also allowed the researcher to gain familiarity with the participants. In this research 28 participants were invited to do the pilot study. They were given the questionnaires in Bangla; 18 participants returned them without any problem, which represents a rate of 71%. The respondents identified problems with the wording of the questionnaire, which resulted in further changes, as well as the participants’ unfamiliarity with the Likert-scale system.

Final Survey Instruments and the Scale of Measurement

The final survey was in the native language and had four sections: current banking status, mobile phone usage, the perception of m-banking factors and the demographic questions. Participants had to tick the appropriate answer/s for three sections (banking, mobile phone and demographic), but the participants’ perceptions of m-banking factors were collected using a five-point Likert-type scale. The demographic questions for this research were placed at the end as it was considered better to keep participants’ minds on the purpose of the survey at the beginning. There was no technical jargon or difficult words in the questions, and closed ended questions were used. This helped the respondents to make their decision quickly when answering. In each question, a space was given in case the participant had something to add in their own word.

The Survey Process

The survey was conducted in two phases. In the first phase, the educated SMEs who had shown strong interest in the research and had a previous understanding of surveys were identified. The researcher gathered 5-10 participants and briefed them about the procedures. This gave an opportunity for any questions from the participants to be answered to establish clarity. In the second phase, the participants comprised the uneducated/semi-educated or less enthusiastic SME owners/managers, and female entrepreneurs. The researcher visited their shops and workplaces and administered the survey. The shortage of time, unawareness of the research process, personal issues and illiteracy were identified as some reasons that inhibited them to participate in the survey in the first phase. In the situation where the participants had no reading and writing ability, the researcher asked the questions orally and recorded the answers.

Research Result

The survey data were analysed by statistical software SPSS version 17. Descriptive statistics are represented by frequency, percentages and cross-tabulations.

Demographic Data

The gender distribution indicates that males (86%, compared to 13% female) were dominant in the survey (Table 1). Among the participants, 26-30 years age group (27%) was the highest and 51+ group (9%) was the lowest. Only 34% participants had below primary education level and 36% had gone to high school. The participants covered a heterogeneous selection of SMEs. According to income, 251 participants earned below 5000 Taka, equivalent to AU$ 60 per month. Among the survey participants 90% owned a mobile phone and 6.6% users did not own any mobile phone but used other’s mobile phone.

The banking status (Table 1) reveals that 16% of the survey participants were unbanked and lived on the cash economy. Another 17% did not have any business account and used a personal bank account for business purposes. With their banking arrangements, 44% participants were dissatisfied, 40% satisfied and 15% did not comment on their banking.

It is encouraging that 47.6% of the survey participants already know about m-banking. This is due to the huge advertising campaign of m-banking providers in Bangladesh. The statistics of intention to adopt of m-banking is also impressive. Among the 547 accepted responses, 66% participants (N=363) were intentional, 30% participants (N=163) were indecisive and only 4% (N=21) were no-intention customers regarding their potential use of m-banking.

Table 1: Demographic Data

Factors

Frequency

Percent

Gender

Male

478

86.9

Female

72

13.1

Age

>=18

10

1.8

19-25

120

21.8

26-30

149

27.1

31-35

95

17.3

36-40

60

10.9

41-50

64

11.6

51+

49

8.9

Occupation

Manager or employee

64

11.6

Owner

486

88.4

Education

Below Primary

186

33.8

SSC

188

34.2

HSC

133

24.2

College/University

40

7.3

Earnings in Taka

>= 5000

251

45.6

5001 to 10000

212

38.5

10001 to 20000

70

12.7

20001 to 40000

14

2.5

40001+

1

.2

Mobile phone ownership

Yes I have a mobile phone

494

89.8

No, but I use others mobile phone

36

6.5

No, But I wish to buy a mobile phone

12

2.2

No, cause I cannot afford a mobile Phone

3

.5

I do not wish to buy mobile phone

2

.4

Other

3

.5

Banking

Unbanked

115

15.4%

Owner’s personal account is used in business

87

11.7%

Bank with government bank

158

21.2%

Bank with private bank

65

8.7%

Bank with post office

7

0.9%

Bank with NGO

311

41.7%

Other type of accounts

3

0.4%

Comments on banking

Dissatisfied

241

43.8

Don’t know

84

15.3

Satisfied

221

40.1

Hypothesis Testing

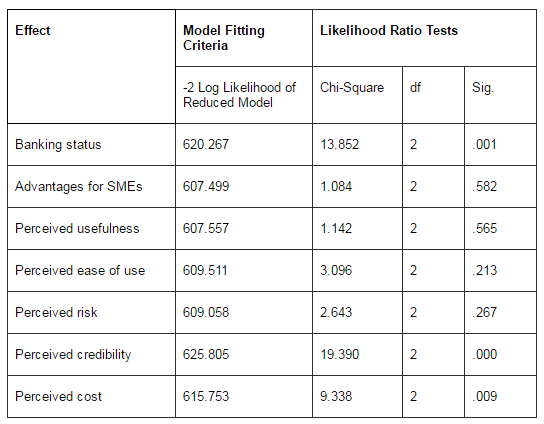

Multinominal Logistic Regression (MLR) was used in the analysis since the dependent variable is a trichotomous variable (intentional, indecisive and no-intention customers. MLR is a statistical technique that can be applied to situations involving more than two choices in a criterion variable. Mathematically, MNL analysis estimates the log-odds ratio to compare levels of the criterion variable.

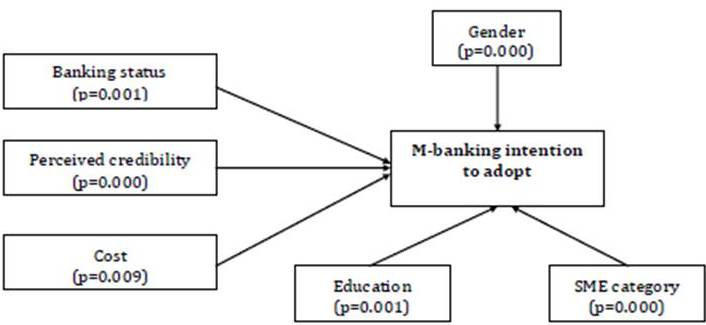

The presence of a relationship between dependent and independent factors is based on the statistical significance of the final model chi-square. In this analysis (Table 3), the distribution reveals that the probability of the model chi-square (66.974) was 0.000, less than the level of significance of 0.05 (i.e. p<0.05). Thus the result suggests a statistically significant relationship between independent factors, banking satisfaction (p=0. 001<0.05), perceived credibility (p=0. 000<0.05) and cost (p=0. 009<0.05) and the dependent variable.

Table 2: M-Banking Variables Testing Using Multinominal Logistic Regression

The proportional by chance accuracy rate is computed by squaring and summing the marginal percentages in each group (0.038² + 0.298² + 0.663² = 0.529). The proportional by chance accuracy criteria is 65.5% (1.24 x 52.9% = 65.5%). The classification accuracy rate is 68.6% which is greater than the proportional by chance accuracy criteria of 65.5%. The criterion for classification accuracy is satisfied.

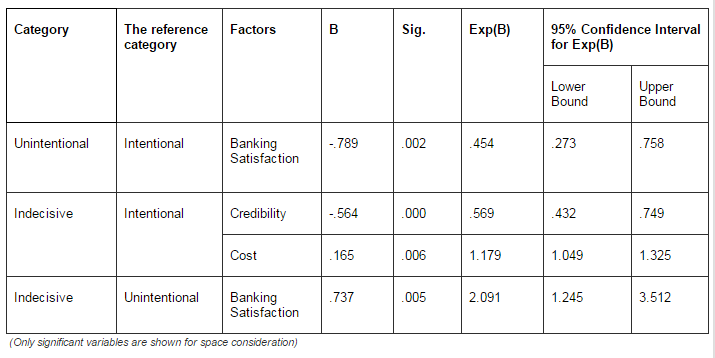

Table 3, parameter Estimates of MLR compares the effect of each variable on three groups, intentional, indecisive and no-intention customers. The independent variable banking satisfaction is significant in distinguishing the no-intention customers and intentional category (0.002 < 0.05). A one-unit increase in the variable banking satisfaction is associated with a 0.789 decrease in the relative log odds of being in no-intention customers versus intentional. Banking satisfaction also plays a role in segmenting the no-intention customers and indecisive category (0.005<0.05).

Table 3: Hypothesis Testing by Comparison Using Multinominal Logistic Regression

The independent factors credibility (p=0.000) and cost (p=0.006) are found differentiating the indecisive and intentional category. The parameter estimates also inform that each unit increase in credibility, the odds of being in the group of indecisive decreased by 25% (0.749 — 1.0 = -0.251). For each unit increases in cost, the odds of being in the indecisive group increased by 32.5% (1.325—1.0 = 0.325). This indicates that survey respondents who perceive m-banking is costly are more likely in the indecisive group, rather than in the intentional group.

Non-parametric techniques such as Chi-square test are ideal when the dependent (Intention to adopt m-banking) and the independent factors (gender, age, level of education, occupation, income and SME category) are both categorical. In this research the Chi-square test results suggest that the age (p=0.656), occupation (p=0.228) and income (p=0.731) have no effect on the intention. But gender (0.000), education (0.001) and SME category (p=0.000) have a significant effect on the intention. It is found using SPSS crosstab that participants running a small tea stall, tobacco shop or Riksaw (tricycle) puller show a lower intention to adopt m-banking.

Evaluation of the Model

To assess the soundness and the effectiveness of the model the researcher conducted the overall model evaluation, statistical test of individual predictors and goodness-of fit statistics. The details are as below:

Overall Model Evaluation:

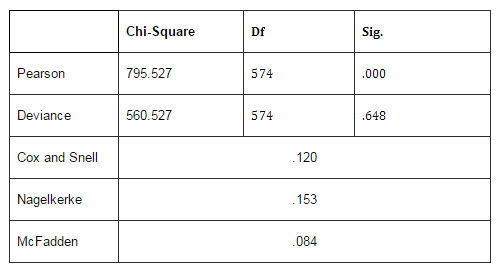

A logistic regression model is expected to provide better fit to the data if it improves over the intercept-only model. Intercept only model is also called null model with having no predictors. Intercept only model serves as a god baseline because it contains no predictors (Peng et al. 2002). In this research the likelihood ratio chi-square of 66974 with a p-value<0.000 indicates that the model as a whole fits significantly better than an empty model (model with no predictors).

Goodness of Fit

Goodness-of fit statistics assess the fit of a logistic model against the actual outcome (Peng et al. 2002). In this research the goodness-of fit is measured by one inferential and two descriptive measures. To assess the goodness of fit of all variables in the model, Person chi-square was obtained. Person chi-square is significant as p<0.000. The pseudo R square statistics was measured by Cox & Snell and Negelkerke R. Cox & Snell is 0.120 and Negelkerke R is 0.153 (table 4). The number indicates a modest improvement in fit over the baseline model.

Table 4: Goodness-of Fit and Pseudo R-Square

Discussion

The survey results help us to broaden our understanding of m-banking in Bangladesh. First of all, this survey demonstrates that mobile phones are the technology of choice of the SME owners/managers. Mobile phone ownership is much higher than private ownership of home phones or computers in the surveyed area. Only 7 participants were found to have access to a computer. Also their income indicates that buying a computer is costly for them. So m-banking has a greater chance to include rural and poor citizens. An important finding regarding their mobile phone usage is that interoperability of m-banking between the mobile networks is important as multiple SIM usage is common.

Figure 2. M-Banking Framework Based on Accepted Hypotheses.

The age distribution indicates that a wide range of age categories are engaged in SME business in rural Bangladesh. This implies that m-banking providers have a chance to offer the service to all ages. Moreover, the chi-square test reveals that age is not a factor in the intention to adopt m-banking. However, gender and education are two identified demographic factors that are associated with m-banking adoption. Laukkanen and Cruz (2012) and Riquelme and Rios (2010) also have identified the effect of gender on m-banking adoption.

Moreover, this research shows an alarming issue that unbanked and dissatisfied banking customers do not have the intention of adopting the service. M-banking providers have to think how they can make this service attractive to the no-intention customers. In m-banking, education has two aspects: firstly illiterate people find the service unsuitable from a literacy standpoint and, secondly, people from a lower educational background may not understand the usefulness of banking. Thus, besides SMS, voice recognition based m-banking might be suitable for uneducated customers.

Current banking satisfaction reveals that 48% survey participants are unhappy with their banking. Therefore, m-banking could be an alternative channel for them. M-banking, can thus improve the SME environment by providing a sophisticated banking facility. Kumar et al. (2011) and Bångens & Söderberg (2011) also made a similar suggestion. However, the income statistics from this research inform us that SME owners/managers need low cost, even possibly no cost accounts, to take advantage of small savings and micro credit opportunities. Rural SMEs managers/employees are also reticent to divulge banking information online. Therefore, proper education and training should be given to reduce the effect.

A significant number of survey participants already knew about the service. A higher rate of awareness obviously will facilitate m-banking adoption. Mobile phone ownership among rural SMEs managers and owners informs us that they adopt a technology if the technology has a use and is affordable to buy and maintain. Therefore, if m-banking can be useful, it is sure to attract the unbanked and dissatisfied banking SME owners/managers.

Conclusion

M-banking is still in its infancy in Bangladesh. M-banking is not on the visible horizon. This empirical research is an effort to navigate through the landscape. This research examines the influence of m-banking factors on the intention to adopt the service by rural SME owners/managers. The research presents poor banking satisfaction (p=0.001), credibility (p=0.000), cost (0.009), gender (p=0.000), education (0.001) and the business type of the SME (0.000) as significant factors.

However, this research does not claim that the factors presented in this research are the only determinants of m-banking adoption in Bangladesh. The data was collected from four villages, thus the research may not represent the whole of Bangladesh. The study was conducted only on the SMEs at a particular point in time; thus a longitudinal study or research with a different population may provide more insights into user behaviour. Moreover, the factors are only from a customer perspective. In future, m-banking research should integrate the consumer view with factors derived from mobile technology providers, banking organizations and regulatory perspectives.

However, the merit of the research lies in presenting, for the first time, an m-banking framework for rural Bangladesh that includes customer perspective factors. Moreover, for the first time, this research considers ICT adoption in the SMEs, the second source of income in the country. Compared to other m-banking acceptance research, this research is based on larger numbers of participants and findings are from a controlled face-to-face survey. The contribution is significant, a step forward in m-banking research in Bangladesh. It also has important implications in providing useful insights into human behavioural and motivational factors which affect attitudes towards the adoption of m-banking in developing countries.

Appendix A: Extract from Survey Questionnaire

Participant’s Mobile Phone and Banking Information

1. Do you have a mobile phone

A. Yes

B. No, but I use others phone

C. No, but I intend to get one

D. No, I have no intention in owning one

2. The following best describe banking status of the SME

Unbanked

Owner’s personal account is used in business

Bank with government bank

Bank with private bank

Bank with post office

Bank with NGO

Other type of accounts

3. Which mobile network does your mobile phone belong to?

A. Grameen Phone

B. Bangla Link

C. Robi

D. Warid

E. City Cell

F. TeleTalk

4. Before tonight, have you heard that you can do your banking using your mobile phone?

A. Yes

B. No

Banking Status of the SME and the Owners/Managers

The following best describe banking status of the SME A. Very unhappy

B. Unhappy

C. No comments

D. Happy

E. Very Happy

The following best describe banking status of the SME owner/manager

A. Very unhappy

B. Unhappy

C. No comments

D. Happy

E. Very Happy

M-banking Advantages for SMEs

M-banking is advantageous for my business banking.

Using m-banking would make it easier for me to conduct business banking.

M-banking will allow me to manage my business more efficiently.

M-banking is more convenient than traditional banking.

I can pay to my city based whole seller by using mobile banking more effectively.

Perceived Usefulness

I think an m-banking service is very in useful.

I think m-banking services improve my performance.

I think m-banking services enhance my effectiveness.

I think mobile banking services increase my productivity by saving times.

I think I can save my time by using m-banking services.

I think I can save my money by using m-banking services. Perceived Ease of Use

I think mobile banking services are user-friendly.

M-banking doesn’t need a lot of mental effort to use the service.

Learning how to use m-banking is easy for me.

It would be easy for me to become skilful at using m-banking without getting customer support.

I think that I can learn how to use m-banking services easily without getting vocational training.

Perceived Credibility

Using m-banking would not divulge my personal information.

I think that online transaction through mobile phone will create unexpected problems.

Perceived Risk

I think that online transaction through mobile phone is risky.

I don’t feel safe in online transaction through mobile phone.

I think that online transaction through mobile phone is not confidential.

Cost

I think it is expensive for me to buy a mobile banking enabled mobile phone.

I think it is expensive for me to access mobile banking services.

I think the transaction fee in mobile banking services is expensive for me.

Intention to Use Mobile Banking Service

If mobile banking is available, what would have done?