Natasha MUZALDIN1, Safawi ABDUL RAHMAN2, Shamsul Anuar SARIFUDIN3 And Muhamad Khairulnizam ZAINI4

1,2,4Faculty of Information Management, Universiti Teknologi MARA, Selangor Campus, 40150 Shah Alam, Selangor, Malaysia

3IZSTech Sdn Bhd, C-03-02, iTech Tower, Jalan Impact, 63000 Cyberjaya, Malaysia

Volume 2022,

Article ID 512221,

Journal of Mobile Technologies, Knowledge and Society,

16 pages,

DOI: 10.5171/2022.512221

Received date: 24 November 2020; Accepted date: 15 September 2021; Published date: 11 November 2022

Cite this Article as:

Natasha MUZALDIN, Safawi ABDUL RAHMAN, Shamsul Anuar SARIFUDIN And Muhamad Khairulnizam ZAINI (2022)," A Study on Behavioural Intention to Use Mobile Wallet with Special Reference to Citizens in Shah Alam, Selangor, Malaysia", Journal of Mobile Technologies, Knowledge and Society, Vol. 2022 (2022), Article ID 512221,DOI: 10.5171/2022.512221

Internet of Things (IoT) embraces Internet technologies supporting remote and mobile applications including Mobile Wallet (M-Wallet). The M-Wallet is an electronic wallet (e-wallet), a mean that is widely used for digital payment. While literature indicated that neighboring countries advanced in the adoption of M-Wallet for digital payment, Malaysia is considerably “infant” as this technology is not extensively used. As such, a study had been conducted to investigate the users’ behavioral intention and the determinant to adopt mobile wallets as digital payment platform in a selected locality in Malaysia. Built upon three basic constructs of Unified Theory of Acceptance and Use of Technology 2 (UTAUT 2) and previous relevant research models, a model of factors influencing behavioral intention on mobile wallet for this study was proposed. Adopting the convenience sampling technique, the online questionnaire had been administered to 384 respondents. The 327 returned questionnaires had been examined and the 315 valid questionnaires were brought into analysis. Both SPSS and SmartPLS were used for descriptive analysis, internal consistency reliability analysis, indicator reliability analysis, convergent validity analysis, discriminant validity analysis, coefficient of determination (R2) analysis, path coefficients analysis and hypotheses testing where appropriate. The results revealed that Hedonic Motivation is the strongest and most crucial factor influencing the intention to use mobile wallet. The Perceived Risk, Perceived Security and Perceived Trust have significant influence on behavioral intention on mobile wallet usage.

As information technology infrastructure becomes mature, businesses nowadays are conducted online and in a digital manner. Businesses adopt online payments methods such as Internet banking, electronic cards (debit and credit), mobile banking and also mobile payment such as mobile wallet (Sarika and Vasantha, 2019; Bezhovski, 2016; Wang et al., 2019; Pandy and Crowe, 2017). With such online payment facilities, businesses may reach users 24/7 without border.

The mobile wallet technology allows users to perform the transaction virtually and easily in both in-store and remote place (Liébana- Cabanillas et al., 2018). Since the first day of its establishment, mobile wallet technology has been widely used by people worldwide for digital payment. It is reported that countries like China and India (PwC Malaysia, 2018) have an extensive use of mobile wallet for performing online transaction and digital payment. The use of mobile wallet for making online payment is growing for its easy-to-use feature.

In Malaysia, a variety of mobile wallet types are available for the users. The four mobile wallet types are open, semi-open, semi-closed as well as a closed wallet (Kumar and Sharma, 2019; Rao, 2015). In Malaysia, despite the existence of providers of mobile wallets such as AEON wallet, Maybank Pay, Grabpay and Gift voucher (Farhan Gazi, 2020), the use of mobile payment is considerably new and is not frequently being applied (Yeow et al., 2017). People prefer former methods and are reluctant to exchange their credit or debit cards’ role with the use of mobile wallet in making payment (Aydin and Burnaz, 2019). The Star (2019) reported that only 8% of Malaysia citizens are currently using mobile wallet to make online payment whereas Muller (2020) stated that 67% of Malaysians conduct their transaction using credit card and online banking.

It is learnt from the reports that Malaysians prefer online transaction but less prefer to use mobile wallet. This issue is hypothesized to be related to the behaviour of the consumers. Triggered by this hypothesized issue, the study investigates users’ behavioural intention and the determinant in the adoption of mobile wallets as digital payment platform. The two research questions devised for the study are the main factors that determine behavioural intention towards mobile wallets among users, and the extent of effort expectancy, facilitation condition, hedonic motivation, perceived security, perceived risk and perceived trust, influence the use of mobile wallet behavioural intention.

The remaining sections of this paper are arranged as follows. The literature review comes to discuss the background that surrounds the issue tackled in the study. Section #3, i.e., the hypotheses development and research model justify the formulated hypotheses for the study. The methodology that the research adopts is justified in section #4. Next section presents the finding of the research and section #6 follows to discuss the finding. Section #7 concludes the paper.

Literature Review

Digital economy built upon digital computing technologies. Digital economy lets businesses transform into e-commerce and e-business. Digital economy stands as part of economic output that derived solely or primarily from digital technologies with a business model (Bukht and Heek, 2017). As digital economy grows rapidly since the beginning of this century, the way the business is conducted transforms significantly in which technological-based means are adopted in many business dimensions.

One of the business areas where computing technologies is widely adopted is payment system. In digital economy, the cash transactions were not preferred and the transaction is made using electronic money (Mohanad Faeq Ali et. al. 2019). The use of electronic payment system is the main strength of e-commerce and the most vital aspect of digital business (Bezhovski, 2016; Maurya, 2019). Due to advantages such as adequate payment infrastructure and practical use, electronic payment has become the preferred mean for making payment for goods and products purchased.

There are various methods of digital payment available for consumers to choose from. One of the earliest methods was debit/credit cards (Xiao, Hedman and Runnemark 2015). Currently, Internet banking system (Zheng et. al. 2009) is widely used. As mobile technology advances, the contactless cards and mobile payment (Chae and Hedman, 2015; Ozcan and Santos, 2014) are quickly adopted by consumers for the purpose of making payment. The variety of methods and instruments offers consumers with flexibility in enabling the electronic payment.

Mobile wallet is one of the mobile payment instruments that is used for purchasing goods and services in an easier and more convenient manner. Mobile wallet originates from the digital wallet (Doan, 2014) in which it stores credit information on the cloud. Bosamia (2017) and Singh et al. (2017) stated that mobile wallet is a virtual wallet that exists in the smartphone where the money is stored in virtual form. Mobile wallet, as an application software on smartphone, serves as a digital container to store information like payment and loyalty cards, tickets, receipts and vouchers (GSMA 2012). With mobile wallet, cashless and/or cardless transaction can be established. Mobile wallet has both software and hardware and enables the use of credit or debit transaction with smartphones.

Mobile wallet is preferred by smartphone users for many reasons. It enables mobile users to be more accessible to financial services. It also allows the users to use their credit or debit cards virtually for financial transactions like paying bills, shopping, booking tickets, fund transfer and etc. (Singh et al., 2017). With pre-installed application or program and tap-to-pay procedures, mobile wallet enables fast monetary transaction for practical usage.

With respect to the extent of usage, literature indicates the classification for mobile wallet. Generally, mobile wallet is classified into four classes namely open, semi-open, semi-closed and closed wallets (Sardar, 2016; Rana 2017; Alaeddin et al., 2018). These four types can be either based on the ability to reload, connect with the bank or have the option where money can be withdrawn (Wadhera et al., 2017). The open wallet enables transactions at any in-store and online purchase. Examples of open wallet are PayPal and Maybank Pay (MAE wallet) (Oh, 2018; Farhan Gazi, 2020). The semi-closed wallet enables consumers to purchase goods and services from registered stores. Grabpay and Touch ‘n Go are examples for semi-closed wallet (Farhan Gazi, 2020; Chew, 2019; Birruntha, 2019). Lastly, the closed wallet is used exclusively for the purchases in the merchant’s premise or company such as Golden Screen Cinema and Gift vouchers (Alaeddin et al., 2017). More examples for closed, semi-closed, semi-opened and open wallets are available both in the published literature and Internet for references.

Studies on mobile wallet are extensive as the researchers studied mobile wallet from diverse perspectives. Far earlier, Shin (2009) validated a comprehensive model of consumer acceptance in the context of mobile payment. Amaroso and Magnier-Watanabe (2012) proposed a comprehensive model integrating eleven key consumer-related variables affecting the adoption of mobile wallet and identified the case of the successful adoption of mobile wallet in Japan. Seetharam et al (2017) investigated the key factors that influence the acceptance of mobile wallet in Singapore. Zhang et al, (2018) examined the factors that influence both the technology acceptance and actual usage aspects of mobile payment adoption from the perspective of the general systems theory. Chawla and Joshi (2019) examined the factors that influence a consumer’s attitude and intention to use mobile wallets using a sample representative of Indian users. In addition to this, Husnil et al (2019) had examined the factors of hedonic motivation and social influence on the intention to use e-money in Indonesia in which they found that both factors are crucial in accelerating the intention on e-money usage. Singh and Sinha (2020) measured merchants’ intention to use a mobile wallet technology. A latest one examines the effect of perceived risk, government support, and perceived usefulness on customers’ intention to use e-wallet during COVID-19 outbreak (Aji, Berakon and Md Husin, 2020). The huge studies on mobile wallets were reported in the literature reflecting a huge variety of related dimensions of mobile payment.

The studies reported above have been conducted in several countries including Malaysia. In Malaysia, the use of mobile wallets is growing as PwC Malaysia (2018) found that only 22% of people tend to adopt e-wallet services and most cases that use e-wallet are mainly in e-commerce. Therefore, it is acknowledged that if compared to Indonesia, e-wallet adoption in Malaysia is still in its infancy (Aji, Berakon, Md Husin 2020; PWC, 2018). Following Chwah et al. (2018), even though most people own smartphones and the mobile wallet has preliminary existed, the use of cash and card payment are still in a higher demand in making purchase especially in the physical store such as mall, groceries or stalls.

The less usage of mobile wallet facility to make payment compared to its neighbouring countries as reported invites a research effort. In establishing this research, the combination of perceived trust, perceived security and perceived risk with three constructs that initially exist in UTAUT2’s structure (effort expectancy, facilitating condition hedonic motivation) is made. The goal of the combination is to allow research that is comprehensive in nature with expectation to yield a strong justification in its finding.

Hypotheses Development and Research Model

The construct of hypotheses for the research reported in this paper is as follows.

Behavioural Intention

Behavioural intention is a degree in which an individual has conveyed a mindful plan regarding the decision of whether or not to perform a definite future behaviour (Venkatesh et al., 2012). Many studies have used this construct to study the intention towards adopting the technology for both mobile payment (Thakur and Srivastava, 2013; Phontanukitithaworn et al., 2015; Mehdi et al., 2018) and mobile wallet (Patel, 2016; Hanudin Amin, 2009; Kafsh, 2015; Singh et al., 2017). Behavioural intention is important in order to identify the users’ intention to use something new, since in Malaysia mobile wallet is considered new and still at the growing stage of usage as compared to other advanced countries. This is to measure the level of users’ intention to use mobile wallets as part of mobile payment in making the purchase to become easier and convenient.

Effort Expectancy

Venkatesh et al. (2003) defined effort expectancy as the level of easiness when using any related systems. Users will show more inclination to use the mobile wallet only if it is easy to be used. This is because if the system is using user-friendly technology, it can surely gain high acceptance, thus, being adopted by users as they will not feel any hassles or putting a lot of effort in using this mobile wallet (Park and Ohm, 2014). Recent studies by Megadewandanu et. al. (2016) and Singh et. al. (2019) have shown that effort expectancy has a significant or positive influence on the intention to use mobile wallet. This study proposes the following hypothesis for effort expectancy.

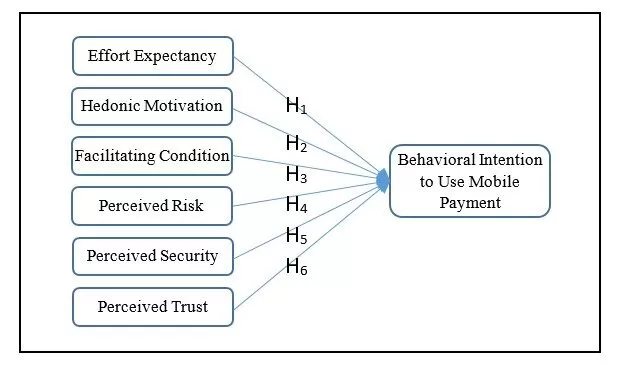

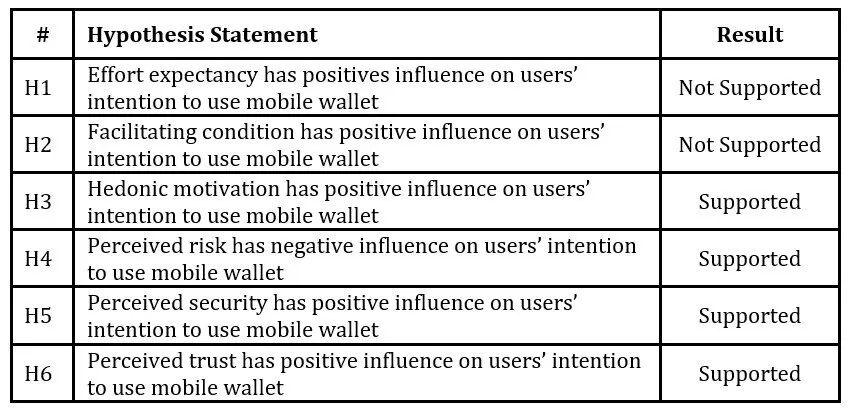

H1: Effort expectancy has positives influence on users’ intention to use mobile wallet

Facilitating Condition

According to Venkatesh et al. (2003), facilitating condition is the degree in which an individual knows and believes that both organizational and technical infrastructure exist to support them in using the system. When users have insight about technologies or a mobile wallet which is able to give them support in using the application, they will become more willing to use the mobile wallet and feel not afraid if they will misuse it. Previous studies found that facilitating condition has positive effect towards the behavioural intention in using mobile wallet (Chawla and Joshi, 2019; Megadewandanu et al., 2016; Patel, 2016; Madan and Yadav, 2016). In this study, the following hypothesis related to facilitating condition is proposed.

H2: Facilitating condition has positive influence on users’ intention to use mobile wallet

Hedonic Motivation

Venkatesh et al. (2012) define hedonic motivation as a feeling of excitement or pleasure which results from the use of technology. It is one of the important roles that is needed in order to identify whether users will accept and use it or not (Brown and Venkatesh, 2005). The technology will not be useful if users are not feeling interested or excited about the device. When they have an interest and feel excited, it will increase their intention to use mobile wallet. The studies by Megadewandanu et al. (2016) and Morosan and Defranco (2016) found that this determinant has a positive influence on behavioural intention to use mobile wallet. Relating to this determinant, this study hypothesises that;

H3: Hedonic motivation has positive influence on users’ intention to use mobile wallet

Perceived Risk

Risk can be defined as the uncertainty such as the severity of certain occasions as well as the consequences from the outcome of action conducted due to respect to human value (Aven and Renn, 2009). As the behavioural intention of the mobile wallet involves some degree of uncertainty, it is believed that perceived risk is fused as a direct determinant of behavioural intention to adopt the technologies. According to a study by Singh et al. (2019) and Madan and Yadav (2016), when perceived risk is decreasing, the intention to adopt a mobile wallet is increasing simultaneously. This study adopts perceived risk and constructs the following hypothesis.

H4: Perceived risk has negative influence on users’ intention to use mobile wallet

Perceived Security

Perceived security is defined as the level of confidence that the users have regarding the security system (Law, 2007). The mobile wallet had opened up many different and new risks on security such as the risk of smartphones which might be stolen, damaged or even lost (Chari, et al., 2001). When this happens, the security of information stored in the mobile wallet is crucial to be protected. Studies show that perceived security consists of a positive influence on behavioural intention to use a mobile wallet to make a purchase (Chawla and Joshi, 2019; Kafsh, 2015; Shin, 2009; Seetharaman et al., 2017). When the users are confident that mobile wallet is able to secure their personal data and information, many will be willing to use mobile wallet. On perceived security, the following hypothesis is proposed.

H5: Perceived security has positive influence on users’ intention to use mobile wallet

Perceived Trust

Trust refers to the concept of willingness to be taken from the actions of other persons or a third party (Redhwan Mohammed Abdullah Al-Amri et. al., 2016). The trust factor has been found to be useful and was included in previous studies related to mobile wallet (Shaw, 2014; Chawla and Joshi, 2019; Shin, 2009). Following Yan and Yang (2014), trust on mobile payment allows positive expectation regarding its system. When users doubt that this mobile wallet has a high security of their information, it will be difficult for them to increase their intention in using the mobile wallets. Studies by Chawla and Joshi (2014) show that trust really plays an important role in influencing the behavioural intention of mobile wallet in India. That is why, trust is important to be included in this study. In this study, the following hypothesis is proposed pertaining to trust.

H6: Perceived trust has positive influence on users’ intention to use mobile wallet

The six variables with their respective hypothesis are gathered into theoretical model depicted in Figure 1. It is noted that these main variables were adopted from previous studies (Venkatesh et al., 2012; Megadewandanu et al., 2016; Singh et al., 2019; Aydin and Sebnem Burnaz, 2016; Chawla and Joshi, 2019) for better understanding of the users’ behavioural intention on mobile wallet. It is expected that this model may help in clarifying the issue on users’ behavioural intention on the technology in this research context.

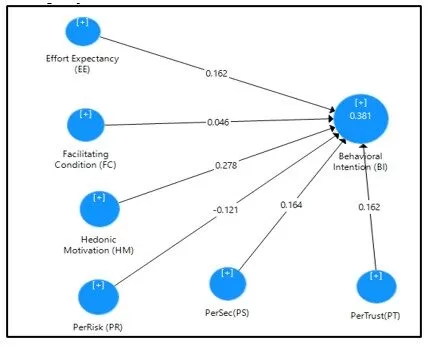

Fig 1. Theoretical Model for Behavioral Intention to Use Mobile Payment System

Methodology

This research adopts the quantitative approach in order to identify users’ behavioural intention on mobile wallet. The study setting was Shah Alam, the capital city of Selangor, Malaysia with 650,000 inhabitants (Shah Alam City Council, 2019). The research instrument was a questionnaire with eight (8) sections namely: Demographic Profile, Behaviour Intention, Effort Expectancy, Facilitating Condition, Hedonic Motivation, Perceived Risk, Perceived Security and Perceived Trust and five (5) scales of Likert measurement. Upon pilot testing, the questionnaire was administered online to 384 respondents following convenience (non-probability) sampling. A total of 327 questionnaires were returned and a set of 315 questionnaires were valid for analysis. Applying both SPSS Statistics Version 22 and also SmartPLS Version 3.0, the analysis techniques applied were descriptive, common method variance and structural equation modelling (SEM) with two steps modelling approach namely Confirmatory Factor Analysis (CFA) and structural model to examine the relationship between independent and dependent variables.

Result and Discussion

The result of statistical analysis using SPSS Version 22 and SmartPLS Version 3.0 includes the brief demographic profiles, internal consistency reliability, indicator reliability, convergent validity, discriminant validity, coefficient of determination (R2), path coefficients and hypotheses testing.

Demographic Profiles

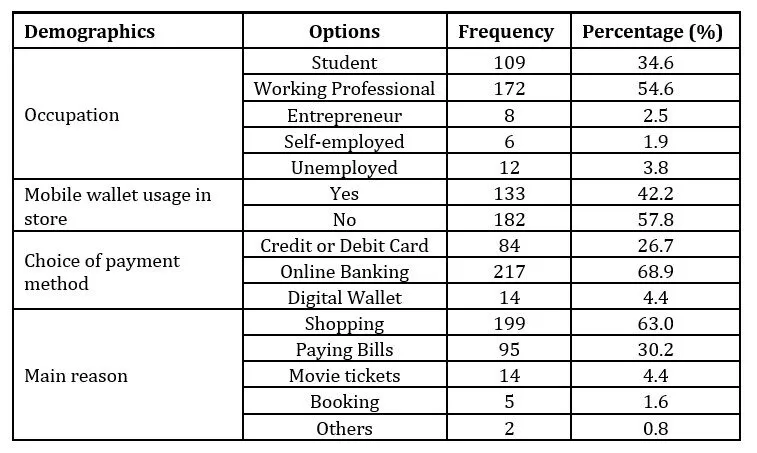

Table 1 shows the simplified and brief characteristics of the respondents on mobile wallet. The survey had been responded by working professional (54.6%), student (34.6%), entrepreneur (2.5%), unemployed citizen (3.8%) and self-employed personnel (1.9%). With regard to mobile wallet usage, it is found that 182 (57.8%) respondents have never used mobile wallet to make payment and the remaining 133 (42.2%) used it in store. On the choice of payment method, the descriptive analysis indicated that respondents less prefer mobile wallet or digital wallet as only 14 (4.4%) of respondents opted this option. The online banking is at higher preference among respondents with 68.9% (217), while the use of credit/debit card for payment is preferred by 84 (26.7%) respondents. On the reason for using mobile wallet, respondents intended to use it mostly for shopping (199:63%), paying bills (95:30.2%), movie tickets (14:4.4%), booking for services and products (5:1.6%) and other purposes (2:0.8%).

Table 1: Demographic Result

Internal Consistency Reliability

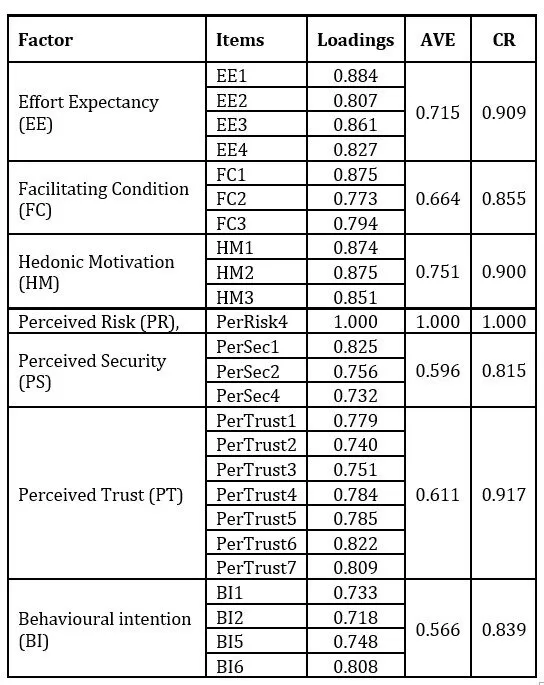

For testing the reliability and validity of the model used in the study, Confirmatory Factor Analysis (CFA) was used using SmartPLS software. All constructs under Effort Expectancy (EE), Facilitating Condition (FC), Hedonic Motivation (HM), Perceived Risk (PR), Perceived Security (PS), Perceived Trust (PT) and Behavioural intention (BI) were included. As depicted in Table 2, the measurement model was considered reliable as all item loadings (FC4, PerRisk1, PerRisk2, PerRIsk3, PerSec3, BI3 and BI4) below the arbitrary value of 0.7 were excluded. As for Average Variance Extracted (AVE) of each available construct was found to have acceptable range from 0.566 to 1.000 in which the value gained is more than the recommended AVE value that is 0.5. Lastly, the Composite Reliability (CR) of the study was also found to be in good range from 0.839 until 1.000.

Table 2: Item Loading, AVE and CR

Discriminant Validity

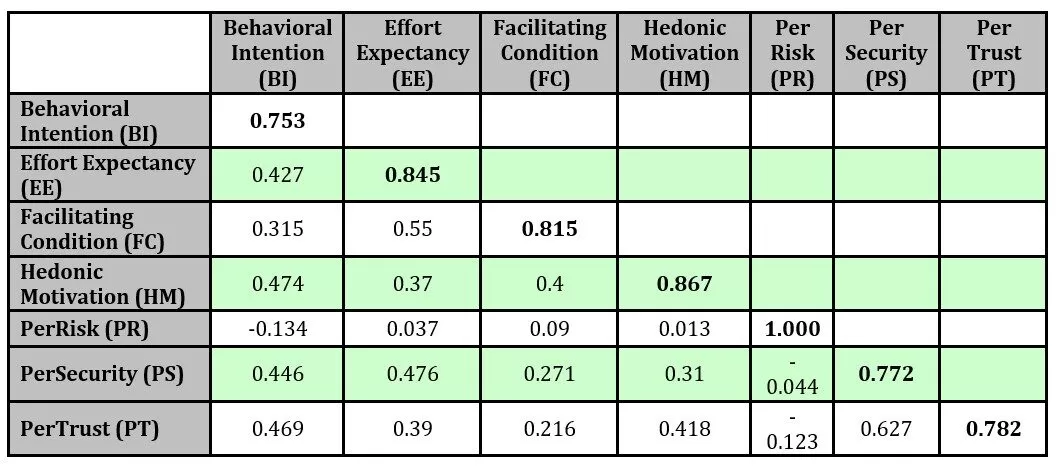

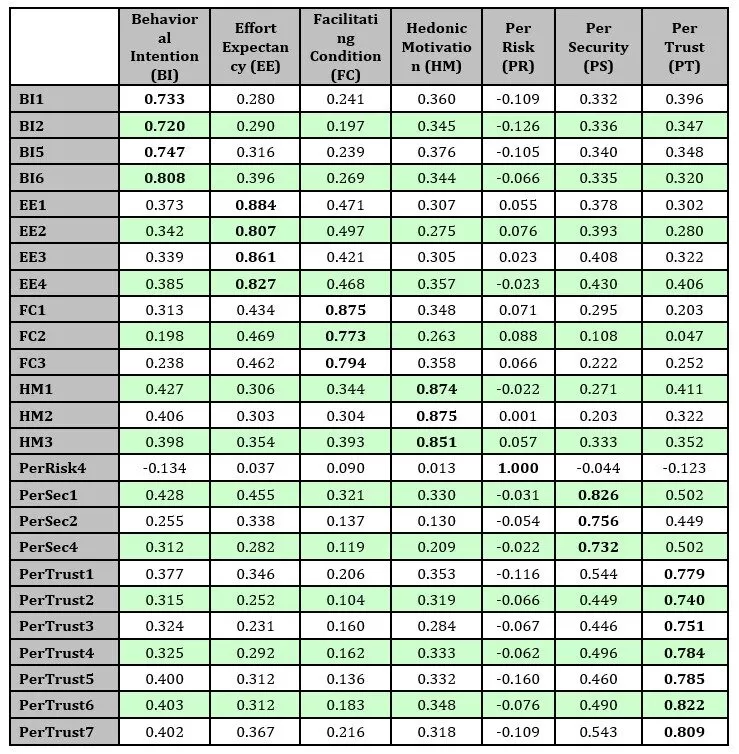

The assessment of discriminant validity is established upon two well-known measures i.e., Fornell and Larcker’s criterion (1981) and cross loading. As for the first assessment, each AVE construct is generated and processed using SmartPLS built in algorithm. In Table 4, the bold element represents the square root of AVE results and the non-bold represents the inter-correlation value between each construct. It is noted that all the square root of AVE elements is higher than the other element construct. It implies that the result gained for discriminant validity meets the Fornell and Larker’s criterion.

Table 4: Inter-correlation Matrix (Fornell and Larker’s criterion)

Once the first assessment is established, the following assessment examines the indicators’ loading of all construct correlations. The result for cross loadings is also produced from SmartPLS algorithm process. Table 5 shows the result of cross loading that exists between the construct and indicators. Identical to Fornell and Larcker’s criterion, the indicators’ loading must have higher value against their respective intended variables as compared to other variables. As indicated in Table 5, the loading of each block is higher than any other block within the same rows and columns. Therefore, this output confirms the cross-loading measurement. Both reliability and validity tests that have been conducted on the measurement model achieve the satisfactory level. The result from the tests confirmed the indicators’ validity to be used in the structural model.

Table 5: Cross Loading Output by Smart PLS

Coefficient of Determination (R2)

The R2 value indicates that the amount of variance that is contained in the dependent variable is required to be explained by the independent variables. It implies that, when R2 has a larger value, it will increase the predictive ability of structural model. SmartPLS’s algorithm is used to obtain the R2 value in this study. The SmartPLS’s bootstrapping is used to help in generating the t-statistic as well as path coefficient value of the model. The bootstrapping had generated 500 samples from 315 cases. The result of structural model is presented in Figure 2 in which it displays Effort Expectancy, Facilitating Condition, Hedonic Motivation, Perceived Risk, Perceived Security and Perceived Trust, which are able to explain 38.1% of the variance in Behavioural Intention. The value of 0.381 makes the R2 for this study as average.

Figure 2: Result of Structural Model from SmartPLS’s Bootstrapping

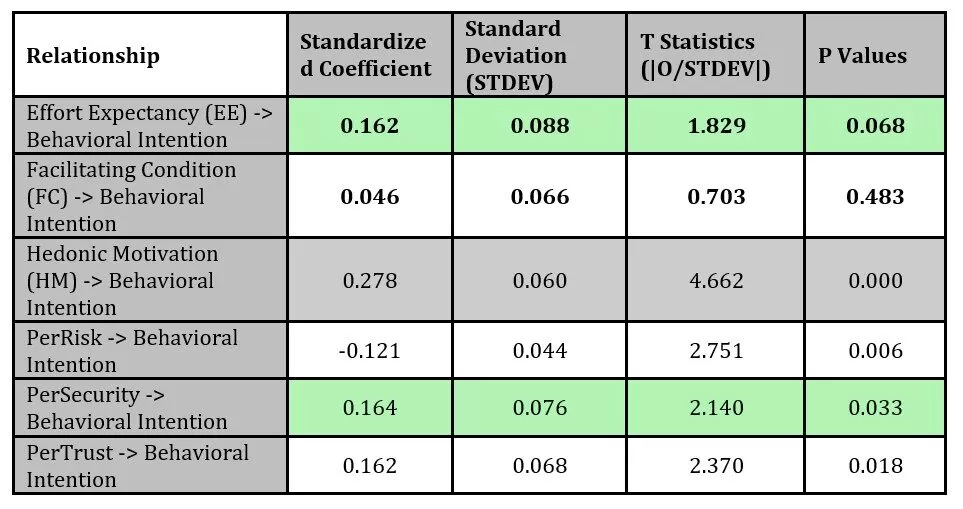

Path Coefficients

For the structural model used in this study, each path that connects six latent variables represents its own hypothesis. Therefore, based on the analysis on the structural model, it gives the researcher the ability to confirm or disconfirm each hypothesis made as well as to gain insight about the strength of the relationship that has existed between both dependent and independent variables in this study. Using the output gained from SmartPLS algorithm and bootstrapping, the relationship between independent and dependent variables as well as their significant value were examined. Table 6 shows the path coefficient, t-statistics and significance levels for all hypothesis path used. The result of the hypotheses testing is discussed in the next subsection.

Table 6: Path Coefficient

Hypotheses Testing

Assessment of path coefficient, t-statistics and significant levels is critical to reject or accept the proposed hypotheses. As indicated in Table 6, it is learnt that Behavioural Intention is influenced directly by Hedonic Motivation (β=278, t=4.662, p<0.05), Perceived Risk (β=-0.121, t=2.751, p<0.05), Perceived Security (β=164, t=2.140, p<0.05) and Perceived Trust (β=162, t=2.370, p<0.05). As a result, hypotheses H3, H4, H5 and H6 are supported. Among these four variables, Hedonic Motivation is found to be the most crucial and significant factor in influencing the behavioural intention on mobile wallet in the context of this study. Behavioural intention is not influenced directly by Effort Expectancy (β=0.144, t=1.829) and Facilitating Condition (β=0.047, t=0.703) since the p-value is more than 0.05 while t value is less than 1.967. The insignificant p-value and t value lead to rejection of hypothesis H1 and H2.

Table 4.14: Hypothesis results

Findings

Based on the result produced from statistical analysis and discussion that follows, it is learnt that Hedonic Motivation is a critical factor influencing the behavioural intention to use mobile wallet by its solid merit. Other three factors i.e., Perceived Risk, Perceived Trust, and Perceived Security accompanied Hedonic Motivation as crucial in influencing behavioural intention on mobile wallet. This finding is aligned with Wong and Mo (2019), Madan and Yadav (2016), Fatimah et al (2019), Megadewandanu et al., (2016), Verkijika (2018) and Patil, Dwivedi and Rana (2017) and Sardar (2016) where they earlier found that Hedonic Motivation, Perceived Risk, Perceived Security and Perceived Trust as crucial factors for people’s intention to use mobile wallet. Among the four variables, this study found that Hedonic Motivation stands as the strongest and most significant factor. This finding matches Fadzil’s (2017) study which had produced similar finding. Both Fadzil (2017) and this study are conducted in Malaysia. Therefore, up to this point of time, it can be reasoned that Malaysian people take HM as a critical factor for their engagement in mobile wallet. The implication would be that service provider shall increase the entertainment in mobile wallet application to make it more appealing. Not only that, it is also crucial to make sure a high security is provided in the mobile wallet, thus, minimizing any potential risk. The service provider also might need to increase and build close relationship with consumers in order to increase their trust.

As hypothesized, Hedonic Motivation, Perceived Security and Perceived Trust have positive influence on behavioural intention, while Perceived Risk has negative influence on behavioural intention to adopt mobile wallet. The result affirmed these four hypotheses. As a result, it is learnt that when all these first three factors increase, the users’ intention to use mobile wallet would also increase. And, when the perceived risk decreases, the intention is increasing. As for Effort Expectancy and Facilitating Condition, the result of the study contrasts with Singh et al. (2019), Dong (2018), Morosan and Defranco (2016), Patel (2009) and Slade et al. (2013) in which they found a significant relationship between these two variables and behavioural intention to use mobile wallet. In response to this discrepancy, it might be said that users will have high intention to use mobile wallet when the level of Hedonic Motivation, Perceived Security, and Trust is high due to its significant and positive relationship, and low Perceived Risk as it has negative influence on the intention to use mobile wallet.

Conclusion and Future Research

This research aims at determining the state of consumers’ intention to use mobile wallet as previous literature informed that, in Malaysia, the level and rate of mobile usage is at infancy. Being triggered from this issue, this study attempts to examine the determinants or factors that may influence the adoption of mobile wallet service. The theoretical framework consisting of six determinants (Behavioural Intention, Effort Expectancy, Facilitating Condition, Hedonic Motivation, Perceived Risk, Perceived Security, Perceived Trust) gathered from established literature was proposed. Upon the analysis, it is found that Hedonic Motivation, Perceived Risk, Perceived Security and Perceived Trust are the main factors that positively affect users’ behavioural intention on mobile wallet with Hedonic Motivation as the strongest predictor. The other two predictors i.e., Effort Expectancy and Facilitating Condition have negative affect and are thus rejected as they are insignificant predictors.

Despite the fact that the intended objectives had been achieved, this study has some limitations in its locality and sampling in particular. Enhancement in future research can be made in the locality to include wider areas or all capitals in Malaysia at once or individually. Definitely this will involve larger sampling. By remaining all variables in the proposed model, another potential research on this topic would be examination of the intention of different groups of citizens such as M40 and T20 in adopting the mobile wallet facility. The individual research effort can be accumulated to allow the pattern analysis of consumers’ intention to use mobile wallet in Malaysia.

Acknowledgement

We would like to express our special thanks to IZSTech (M) Sdn Bhd (1394190-M) for the financial support in the publication of this paper.

References

Alaeddin, O., Altounjy, R., Zalina Zainudin and Fakarudin Kamarudin. (2018), ‘From Physical to Digital: Investigating Consumer Behaviour of Switching to Mobile Wallet,’ Polish Journal of Management Studies. 17(2), 18-30. https://doi.org/10.17512/pjms.2018.17.2.02

Amoroso, D. L. and Magnier-Watanabe, R. (2012), ‘Building a Research Model for Mobile Wallet Consumer Adoption: The Case of Mobile Suica in Japan,’ Journal of Theoretical and Applied Electronic Commerce Research, 7(1), 94-110.

Ang, G. W. (2010), ‘A Study on the Determinants of Behavioral Intention Towards using Mobile Banking Services in Malaysia’. [Thesis Dissertation]. University of Malaya.

Aven, T. and Renn, O. (2009), ‘On Risk Defined as an Event Where the Outcome is Uncertain,’ Journal of Risk Research, 12(1), 1-11.

Aydın, G. and Burnaz, S. (2016), ‘Adoption of Mobile Payment Systems: A Study on Mobile Wallets,’ Journal of Business, Economics and Finance, 5(1), 73-02.

Bezhovski, Z. (2016), ‘The Future of The Mobile Payment as Electronic Payment System,’ European Journal of Business and Management, 8(8), 127-132.

Birruntha, S. (2019). ‘The best e-wallets in Malaysia, as ranked by users,’ The Malaysian Reserve. [Online], [Retrieved April 27, 2020], https://themalaysianreserve.com/2019/10/29/the-best-e-wallets-in-malaysia-as-ranked-by-users/

Bosamia, M. P. (2018), ‘Mobile Wallet Payments Recent Potential Threats and Vulnerabilities With its Possible Security Measures,’ International Journal of Computer Sciences and Engineering, 7(1), 810-817.

Brown, S. A. and Venkatesh, V. (2005), ‘Model of Adoption of Technology in Households: A Baseline Model Test and Extension Incorporating Household Life Cycle,’ MIS quarterly, 29(3).

Bukht, R. and Heeks, R. (2017), Defining, conceptualising and measuring the digital economy. development informatics: Working paper series, Centre for Development Informatics Global Development Institute, SEED, UK.

Carr, M. (2008), ‘Mobile payment systems and services: an introduction, 10,’ Venture Woods. [Online], [Retrieved July, 2019], http://venturewoods.org/wp-content/uploads/2008/06/mobile-payment-systems-and-services.pdf

Chae, J. S. U. and Hedman, J. (2015), ‘Business Models for NFC Based Mobile Payments,’ Journal of Business Models, 3 (1), 29-48.

Chari, S., Kermani, P., Smith, S. and Tassiulas, L. (2001), ‘Security Issues in M—commerce: A Usage—Based Taxonomy,’ In E-commerce agents. 264-282. Springer, Berlin, Heidelberg.

Chawla, D. and Joshi, H. (2019), ‘Consumer Attitude and Intention to Adopt Mobile Wallet in India – An Empirical Study,’ International Journal of Bank Marketing, 37(7), 1590-1618. https://doi.org/10.1108/IJBM-09-2018-0256

Chew, J. (2019), ‘Which e-wallet app do Malaysians use frequently?. iPrice. [Online], [Retrieved April 27, 2020], https://iprice.my/trends/insights/best-ewallet-malaysia/

Creswell, J. (2014), Research Design: Qualitative, Quantitative, and Mixed Method Approach. (4th), SAGE Publication, California.

Davis, F. (1989), ‘Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology,’ MIS Quarterly, 13(3), 319–340.

Dewan, S. and Chen, L. (2005), ‘Mobile Payment Adoption in the US,’ Journal of Information Privacy and Security, 1(2), 4–28.

Doan, N. (2014), ‘Consumer Adoption in Mobile Wallet: A Study of Consumers in Finland,’. [Thesis dissertation]. The Turku University of Applied Sciences.

Dong, X. (2018), ‘Performance Expectancy, Effort Expectancy, Social Influence, Facilitating Conditions, and Relative Advantage Affecting The Chinese Customers’ Decision to Use Mobile Payment in Bangkok,’. [Dissertation]. The Graduate School of Bangkok University. http://dspace.bu.ac.th/bitstream/123456789/3779/1/Dong2.pdf

Fadzil, F. (2017), ‘A study on factors affecting the behavioral intention to use mobile apps in Malaysia,’ SSRN Electronic Journal.[Online], [Retrieved May 12, 2020], https://doi.org/2139/ssrn.3090753

Farhan Gazi. (2020), ‘What is an e-wallet and how is it different from a credit card?,’iMoney. [Online], [Retrieved April 27, 2020], https://www.imoney.my/articles/choosing-e-wallet

Fishbein, M. and Ajzen, I. (1975), Belief, Attitude, Intention, And Behavior: An Introduction to Theory and Research, Reading, MA: Addison-Wesley.

Gupta, V. (2017), ‘A Study on Consumer Adoption of Mobile Wallet,’ International Journal of Trade and Commerce II ARTC, 6(1), 57–70.

Hanudin Amin. (2009), ‘Mobile Wallet Acceptance in Sabah: An Empirical Analysis,’ Labuan Buletin of International Business & Finance, 7, 33-52. http://ssrn.com/abstract=1866816

Hendy Mustiko Aji, Izra Berakon and Maizaitulaidawati Md Husin/ (2020), ‘COVID-19 and E-wallet Usage Intention: A Multigroup Analysis Between Indonesia and Malaysia,’ Cogent Business & Management, 7(1). https://doi.org/1080/23311975.2020.1804181

Husnil Khatimah, Susanto, P. and Nor Liza Abdullah. (2019), ‘Hedonic Motivation and Social Influence on Behavioral Intention of E-Money: The Role of Payment Habit as a Mediator,’ International Journal of Entrepreneurship, 23(1), [Online], [Retrieved December 21, 2020], https://www.abacademies.org/articles/hedonic-motivation-and-social-influence-on-behavioral-intention-of-emoney-the-role-of-payment-habit-as-a-mediator-8006.html

Kafsh, S. Z. (2015), ‘Developing consumer adoption model on mobile wallet in Canada,’. [Thesis dissertation]. Master of Science in Electronic Business Technologies, Ottawa, Canada, 2015.

Kline, R. B. (2010), ‘Principles and Practice of Structural Equation Modeling. (3rd), Gilford Press, New York.

Kumar, D. and Sharma, U. (2019), ‘Design E-wallet As a Centralized e-Wallet,’ International Journal of Engineering and Advanced Technology (IJEAT), 9(2), 1993-1999. https://doi.org/10.35940/ijeat.B2684.129219

Law, K. (2007), ‘Impact of perceived security on consumer trust in online banking,’. [Doctoral dissertation], University of Technology, Auckland .

Liébana-Cabanillas, F., Marinkovic, V., Luna, I. R. and Kalinic, Z. (2018), ‘Predicting the Determinants of Mobile Payment Acceptance: a Hybrid SEM-Neural Network Approach,’ Technological Forecasting & Social Change, 129, 117-130. https://doi.org/10.1016/j.techfore.2017.12.015

Madan, K. and Yadav, R. (2016), ‘Behavioural Intention to Adopt Mobile Wallet: A Developing Country Perspective,’ Journal of Indian Business Research, 8(3), 227-244. https://doi.org/10.1108/JIBR-10-2015-0112

Maurya, P. (2019). ‘Cashless Economy and Digitalization,’ Proceedings of 10th International Conference on Digital Strategies for Organizational Success. 1-6. http://dx.doi.org/10.2139/ssrn.3309307

Megadewandanu, S., Suyoto and (2016), ‘Exploring Mobile Wallet Adoption in Indonesia using Utaut2: An Approach From Consumer Perspective,’ Paper presented on 2nd International Conference on Science and Technology-Computer (ICST), Yogyakarta, Indonesia.

Mehdi, H., Mollik, A. T., Johns, R. and Muhammad Sabbir Rahman. (2018), ‘M-payment Adoption for Bottom of Pyramid Segment: An Empirical Investigation,’ International Journal of Bank Marketing, 37(1), 362-381. https://doi.org/ 10.1108/IJBM-01-2018-0013

Ming, L. Y. and Yin, L. T. (2017), ‘The College Students’ Behavior Intention of using Mobile Payments in Taiwan: An Exploratory Research. Proceedings of IASTEM International Conference, 2nd – 3rd January 2001, Singapore.

Mohammad, A. (2008), ‘The development of e-payments and challenges in Malaysia,’ The Seacen Centre. [Online], [Retrieved Jun 11, 2020], https://www.seacen.org/GUI/pdf/publications/research_proj/…/Chap5.pdf.

Mohanad Faeq Ali, Norharyati Harum, Nur Azman Abu, Mohammed Saad Talib, Mohamed Doheir and Mohammed Nasser Al-Mhiqani. (2019), ‘Impact of Cashless Society on The Economic Growth in Malaysia,’ Religación, 4(17), 769-777.

Morosan, C. and DeFranco, A. (2016), ‘It’s About Time: Revisiting Utaut2 to Examine Consumers’ Intentions to Use NFC Mobile Payments in Hotels,’ International Journal of Hospitality Management, 53, 17–29.

Muller, J. (2020), ‘Leading e-commerce payment methods in Malaysia 2019,’ [Online], [Retrieved May 22, 2020], https://www.statista.com/statistics/895540/e-commerce-payment-methods-malaysia/

Oh, A. (2018), ‘The e-wallet infinity war in Malaysia – Everything you need to know about e-wallet starts here..…’ [Online], [Retrieved April 27, 2020], https://www.ecinsider.my/2018/12/malaysia-ewallet-battle-landscape-analysis.html

Ozcan, P. and Santos, F. M. (2014), ‘The market that never was: turf wars and failed alliances in mobile payments,’ Online Library. [Online], [Retrieved July 23, 2020], https://onlinelibrary.wiley.com/doi/abs/10.1002/smj.2292

Pandy, S. M. and Crowe, M. (2017), ‘Choosing a Mobile Wallet: The Consumer Perspective,’ Federal Reserve Bank of Boston, 1-23.

Park, E. and Ohm, J. (2014), ‘Factors Influencing Users’ Employment Of Mobile Map Services,’ Telematics and Informatics, 31(2), 253-265.

Patel, V. V. (2016), ‘Young Consumers’ Intention to Use Mobile Wallet Services: An Empirical Investigation Using UTAUT Model. In Nirma International Conference on Management (NICOM), Institute of Management, Nirma University.

Rana, S. S. (2017), ‘A Study of Preference Towards The Mobile Wallets among The University Students in Lucknow City,’ Scholedge International Journal of Management & Development, 4(6), 46-57. https://doi.org/ 10.19085/journal.sijmd040601

Rao, R. S. V. (2015), ‘E- wallet – a ‘pay’volution,’ Paper presented on 2015 at One Day National Seminar on Business Dynamics – A Paradigm Shift in Policies for Sustainability, St Mary’s College, Hyderabad

Redhwan Mohammed Abdulllah Al-Amri, Nurazean Maarop, Yazriwati Yahya, Sya Azmeela Shariff, Ganthan Narayana Samy and Azizul Azizan. (2016), ‘Factors Influencing NFC Mobile Wallet Proximity Payment Adoption From the Human and Security Perspective’ In Proceeding of the First International Conference on ICT for Transformation.

Sardar, R., Dr. (2016), ‘Preference Towards Mobile Wallets among Urban Population of Jalgaon City,’ Journal of Management (JOM), 3(2), 1-11. http://www.iaeme.com/jom/-

Sarika, P. and Vasantha, S. (2019), ‘Impact of Mobile Wallets on Cashless Transaction,’ International Journal of Recent Technology and Engineering (IJRTE), 7(6S5), 1164-1170.

Seetharaman, A. Kumar, K. N., Palaniappan, S. and Weber, G. (2017). ‘Factors Influencing Behavioural Intention to Use The Mobile Wallet in Singapore,’ Journal of Applied Economics and Business Research (JAEBR), 7(2). 116-136.

Shaw, N. (2014), ‘The Mediating Influence of Trust in The Adoption of the Mobile Wallet,’ Journal of Retailing and Consumer Services, 21, 449–459. http://dx.doi.org/10.1016/j.jretconser.2014.03.008

Shin, D. H. (2009), ‘Towards an Understanding of the Consumer Acceptance of Mobile Wallet,’ Computers in Human Behavior, 25, 1343–1354. https://doi.org/10.1016/j.chb.2009.06.001

Singh, N. and Sinha, N. (2019), ‘How Perceived Trust Mediates Merchant’s Intention to Use a Mobile Wallet Technology,’ Journal of Retailing and Consumer Services, 52, 1-13. https://doi.org/10.1016/j.jretconser.2019.101894

Thakur, R. and Srivastava, M. (2014). Adoption Readiness, Personal Innovativeness, Perceived Risk and Usage Intention Across Customer Groups for Mobile Payment Services in India,’ Internet Research, 24(3), 369–392.

The Star. (2019), ‘E-wallet users to get RM30,’ The Star News. [Online], [Retrieved April 24, 2020], https://www.thestar.com.my/news/nation/2019/10/12/e-wallet-users-to-get-rm30

Venkatesh, V., Thong, J. Y. L. and Xu, X. (2012), ‘Consumer Acceptance and Use of Information Technology: Extending The Unified Theory of Acceptance and Use of Technology,’ Forthcoming in MIS Quarterly, 36(1), 157-178.

Verkijika, S. F. (2018), ‘Factors influencing the Adoption of Mobile Commerce Applications in Cameroon.,’ Telematics and Informatics, 35(6), 1665–1674. doi:10.1016/j.tele.2018.04.012

Wadhera, T., Dabas, R. and Malhotra, P. (2017), ‘Adoption of M-wallet: A Way Ahead,’ International Journal of Engineering and Management Research (IJEMR), 7(4).

Wang, W. H. and Mo, W. Y. (2019), ‘A Study of Consumer Intention of Mobile Payment in Hong Kong, Based on Perceived Risk, Perceived Trust, Perceived Security and Technological Acceptance Model,’ Journal of Advanced Management Science, 7(2), 33-38. doi: 10.18178/joams.7.2.33-38

Xiao, X., Hedman, J. and Runnemark, E. (2015), ‘Use of Payment Technology: A Perspective Based on Theory of Consumption Value,’ ECIS 2015 Research-in-Progress Papers. Paper 40.

Yan, H and Yang, Z. (2014), ‘An Empirical Examination of User Adoption Mobile Payment.,’ International Conference on Management of e-Commerce and e-Government, Shanghai, 156-162, doi: 10.1109/ICMeCG.2014.40.

Yeow, O. M., Haliyana Khalid and Nadarajah, D. (2017), ‘Millennials’ Perception on Mobile Payment Services in Malaysia. Proceedings of the 4th Information Systems International Conference 2017, ISICO 2017, 6-8 November 2017, Bali, Indonesia.

Zhang, Y., Sun, J., Yang, Z. and Wang, Y. (2018), ‘What Makes People Actually Embrace or Shun Mobile Payment: A Cross-Culture Study,’ Mobile Information Systems, 2018.

Zheng Q., Han Y., Li S., Dong J., Yan L. and Qin J. (2009), Payment Technologies for E-commerce. In: Zheng Q. (eds) Introduction to E-commerce. Springer, Berlin, Heidelberg. https://doi.org/10.1007/978-3-540-49645-8_3