École Nationale de Commerce et de Gestion (ENCG) Tanger,

Université Abdelmalek Essaâdi, Tangier, Morocco

Volume 2025,

Article ID 829655,

Journal of North African Research in Business,

15 pages,

DOI: doi.org/10.5171/2025.829655

Received date: 25 June 2025; Accepted date: 2 September 2025; Published date: 11 November 2025

Cite this Article as:

Hafsa Rayouss and Rachid Mchich (2025), “ Crowdfunding in Morocco under Law 15-18 : A Descriptive Analysis of the Regulatory Framework and Early Developments ”, Journal of North African Research in Business, Vol. 2025 (2025), Article ID 829655, https://doi.org/10.5171/2025.829655

This study aims to identify the determinants of the success of crowdfunding campaigns in Morocco, in light of the new legal framework introduced by Law 15-18. By employing a descriptive analysis of 1,262 campaigns conducted between January 2023 and December 2024, enriched by a documentary study, the authors examine the influence of quality signals, social capital, and emergency situations on contributors’ trust. The results reveal that crisis contexts, such as earthquakes or medical appeals, act as catalysts for mobilization, significantly increasing success rates. The study proposes the first empirical mapping of crowdfunding in Morocco and formulates recommendations for investors, platform managers, and project holders to structure a more resilient and equitable ecosystem.

Keywords: Crowdfunding, legal framework, success of crowdfunding campaigns, quality signals

Introduction

In a world where access to financing represents a major challenge for entrepreneurs and innovative project holders, crowdfunding has emerged as a viable and revolutionary alternative. Since its emergence in the 2000s, this mode of financing has connected investors, project holders, and financial intermediaries. By appealing to a large number of people through online platforms, crowdfunding represents an exceptional opportunity to raise funds while bringing together a community around innovative and ambitious projects.

The rise of platforms such as Kickstarter, Indiegogo, or Ulule illustrates the validity and relevance of this model. In 2022, millions of projects were funded around the world, demonstrating the economic and social impact of this phenomenon. However, this rapid expansion raises several fundamental questions. What structural, relational, and contextual factors influence the success of crowdfunding campaigns in Morocco within the context of the new legal framework established by law 15-18?

The objective of this study is to provide a comprehensive overview of crowdfunding in Morocco, identify the determinants of campaign success, and assess the impact of emergency situations on fundraising performance. This study emerged following the recent adoption of Law 15-18, which establishes an innovative legal framework while leaving a zone of uncertainty regarding the effective operation of campaigns and the trust signals they generate among contributors. Consequently, we are questioning the structural, relational, and contextual elements that can shed light on the success or failure of crowdfunding campaigns in Morocco within the framework of this new legal regime. In order to answer this question, we conducted a descriptive analysis of 1,262 campaigns initiated between January 2023 and December 2024 on the three main approved platforms, accompanied by a documentary study of legislative texts as well as platform reports. The major contribution of our article lies in the presentation of the first empirical mapping of crowdfunding in Morocco, as well as in highlighting the catalytic effect of emergency situations (such as post-earthquake events and medical appeals) on the success of fundraising campaigns. Moreover, we provide operational recommendations aimed at public decision-makers, platform operators, and project leaders.

Foundations of Crowdfunding

Origins and definitions

Crowdfunding represents a digital transposition of ancestral collective practices, during which a group of people finances projects. As early as the 19th century, the Statue of Liberty and the Sagrada Familia were built through popular subscriptions, illustrating that the dynamics of collective contributions anticipated the Internet era. In Africa, the spirit of financial solidarity can be expressed through financial support systems such as citizen mobilization, which enabled the financing of the Hassan II Mosque in 1986.

At the international level, crowdfunding is referred to as “participatory financing.” However, in Morocco, in order to avoid any confusion with Islamic finance already named as such, Bank Al-Maghrib chose the term “collaborative financing” to designate this mode of financing.

The widespread adoption of Web 2.0, however, has significantly broadened the scope of these fundraising efforts: the term “crowdfunding” emerged in 2006, although pioneering initiatives, such as the fundraising orchestrated by fans of the band Marillion in 1997, had already validated this model (Agrawal et al., 2010). Crowdfunding is characterized as “a public call, primarily conducted via the Internet, to mobilize financial resources” (Schwienbacher and Larralde, 2012). It establishes a direct link between project holders and contributors, thereby enhancing online visibility, community engagement, and ultimately, the chances of commercial success (Bessière & Stéphany, 2017).

Theoretical Framework

Crowdfunding is based on various theoretical foundations that help explain its specific dynamics in comparison with traditional financing methods. The theory of information asymmetries, developed by Jensen and Meckling in 1976, highlights the informational imbalances existing between project holders and financiers. These imbalances are mitigated by the intermediation of digital platforms, which act as credibility filters. The signaling theory, developed by Spence in 1973, posits that project leaders emit quality signals, such as a prototype or a business plan, in order to reassure contributors. At the same time, the network effect and social dynamics (Katz & Shapiro, 1985) highlight the importance of initial contributions from a small circle to trigger a collective adhesion dynamic. The theory of extended rationality (Sen, 1977) emphasizes that contributors’ motivations sometimes go beyond economic interest, encompassing altruistic or prosocial considerations. Finally, the Schumpeterian perspective (Schumpeter, 1939) considers crowdfunding as an institutional innovation, capable of overcoming the inherent rigidities of the traditional banking system, supporting projects with high uncertainty, and establishing lasting community bonds between project holders and contributors who share common values.

Typology Of Crowdfunding Models

Crowdfunding encompasses a variety of practices and mechanisms, which are distinguished by the expectations of the contributors and the nature of the projects funded. The four main models identified are as follows:

Donation-based crowdfunding: Contributors provide funds without expecting any remuneration in return. This model can include donations without any reward (purely altruistic). (e.g., GoFundMe, Cotizi, JustGiving, KiwiCollect…)

Reward-based crowdfunding: Project leaders fund an initiative in exchange for a reward (prototype, goodies, exclusive access…). They receive neither shares nor refunds; it is a form of pre-sale and community engagement, ideal for innovative or technological projects. (e.g., Indiegogo, Kickstarter, Ulule…)

Lending-based crowdfunding: Contributors act as lenders. They anticipate a repayment, whether it is with interest or not. This model constitutes an alternative financing option to traditional bank loans, particularly suited for young businesses and small enterprises. (e.g., LendingClub, beehive…)

Equity crowdfunding: Investors provide funds to a company in exchange for shares or equity. This model, known as “crowdinvesting,” proves particularly suitable for young companies and businesses seeking venture capital financing. Each model has its own advantages and disadvantages, which vary depending on the profile of the contributors, the project leaders, and the financial objectives. (e.g., Seedrs, Wefunder…)

Operation of crowdfunding platforms

Main actors and key roles

The mechanism of crowdfunding platforms relies on the interaction of three main categories of participants: project holders, contributors, and the platform itself.

Crowdfunding involves the collaboration of three essential actors: first, the project holders, whether individuals, start-ups, or organizations, who must develop a clear concept, rely on quality elements such as videos or prototypes, and mobilize their network to attract support; next, the contributors, whose motivations can vary between seeking financial or material gains, the desire to have a social and cultural impact, as well as an interest in an innovative product, and who rely on credibility indicators and the initial support observed; finally, the platform, as a digital intermediary, is responsible for filtering projects to assess their feasibility, securing financial transactions, and monitoring the campaign after its completion to ensure the delivery of promised rewards or results.

Operational Process

The operation of crowdfunding platforms follows a structured process composed of several steps:

Submission of the project

The project leader presents their proposal to the platform, including a detailed description, a clear financial goal, a deadline, and possibly rewards. Some platforms conduct a preliminary assessment to verify the project’s viability (e.g., Kickstarter), while others opt for a more flexible approach (e.g., Indiegogo).

Fundraising campaign

Once the project has received approval, the campaign is launched online. It is based on two mechanisms:

The “all or nothing” system means that the funds are only released if the funding goal is fully met. This reduces risks for contributors and encourages project leaders to fully commit.

The “flexible” system implies that the funds collected are given to the project leader, regardless of whether the set goal is reached. This mechanism is frequently employed in the context of campaigns where every contribution matters (e.g., charitable initiatives).

Mobilization of social networks

Social media platforms are essential for the visibility and success of campaigns. These platforms maintain access to a broader audience and stimulate the viral effect, especially thanks to the initial participation of close ones such as family and friends.

Fundraising and fund management

Once the goal is reached, the funds are transferred to the beneficiary, after deducting the platform fees, which are generally between 5% and 10% of the amount collected.

Post-campaign

The project leader is responsible for the implementation of the project as well as the distribution of the rewards or benefits that were promised. Transparency, as well as regular communication with contributors, is crucial to maintaining trust and preventing disputes.

Economic Models of Platforms

Crowdfunding platforms are characterized by their economic models, which exert a significant influence on their functioning and strategies.

Compensation system

Commission on funds collected: the predominant model, with rates varying depending on the platform and the nature of the campaign (e.g., Kickstarter applies a 5% commission on the funds raised, in addition to bank transaction fees).

Subscriptions or fixed fees: some platforms charge registration or subscription fees to cover their operational costs (e.g., Patreon, which operates on a subscription model allowing users to fund content creators).

Additional service offerings

Many platforms offer value-added services, such as marketing tools, advice on structuring the campaign, or partnerships with experts to increase the credibility and success rate of the campaigns. (For example, lawyers or financial consultants).

Marketing tools: Advertising campaigns on social media, carefully optimized pages to attract investors.

Advice and support: Assistance in drafting a high-quality project presentation, organizing rewards, and setting a realistic funding goal.

Partnerships with experts: Collaboration with lawyers, financial consultants, or crowdfunding specialists to provide optimal support to entrepreneurs.

Specialization by sector or type of project

Some platforms focus on specific niches (e.g., Ulule for cultural and artistic projects, Seedrs for technology startups through equity crowdfunding, and GoFundMe for personal and humanitarian causes), allowing them to better meet the expectations of project leaders and contributors.

Factors for the Success of Campaigns

The success of a crowdfunding campaign relies on several key factors that influence contributor engagement and fund collection. First of all, the quality and clarity of the project are essential for the success of a campaign; its objective must be well-defined, with a polished presentation and attractive rewards that strengthen contributors’ trust. Next, mobilizing the personal network plays a crucial role, as strong initial support (family, friends) creates a signaling effect that encourages others to participate. Moreover, the financial goal and the duration of the campaign must be well-calibrated, as excessive ambitions or an overly long period can demotivate contributors. Moreover, the strategic use of social media is crucial to maximize the project’s visibility and maintain engagement. An explanatory video and attractive visuals increase attention and evoke an emotional connection with the audience, while the transparency and credibility of the project leader are reassuring elements for potential investors. The implementation of motivating rewards and appropriate incentives, such as exclusive products or early access, also helps attract more supporters. Finally, continuous campaign engagement, with regular updates, follow-ups, and dynamic interactions with the community, helps maintain enthusiasm and optimize the chances of success. By combining these elements, a crowdfunding campaign maximizes its chances of reaching and even exceeding its funding goal.

The success of crowdfunding campaigns depends on several elements:

Quality and clarity of the project: A clear objective, attractive rewards, and careful communication increase the chances of success.

Mobilization and engagement of the network: Projects with strong initial support (friends, family) are more likely to exceed their goals thanks to the signaling effect and group dynamics.

Duration and financial goal: Studies show that overly ambitious financial goals or excessively long campaign durations reduce the chances of success.

Strategic use of social media: The active use of platforms like Facebook, Twitter, and Instagram to promote the project is a key factor.

Crowdfunding platforms in Morocco

Currently, three crowdfunding platforms are officially regulated in Morocco by Bank Al-Maghrib and the AMMC. They operate within a legal framework ensuring transparency, transaction security, and contributor protection, while facilitating access to funding for innovative or solidarity-based projects. Akkan, the first approved SFC in 2024, adopts a dual model combining equity investment and collaborative lending, specializing in supporting socio-economic projects and enhancing value creators, with an “all or nothing” fundraising system. It targets SMEs, startups, and social projects, and benefits from a partnership with the Banque Centrale Populaire. Kiwi Collecte, founded in 2021, the first donation-based platform, supports projects with social impact in various fields (solidarity, health, education, culture…) and applies a “flexible” funding model. During its first campaign, it managed to raise an amount of 450,000 MAD and register a successful project. She collaborates with Attijariwafa Bank to secure the funds. Finally, Alif Crowd, operated by Alif Invest SA and approved by Bank Al Maghrib in 2024, offers donation and loan operations to innovative project holders, such as startups, very small and small enterprises (VSEs/SMEs), as well as associations according to the “all or nothing” principle, but has not yet started its activities. This Moroccan platform is currently in the launch phase and has not yet begun its operations.

The Moroccan Legal Framework

Official Bulletin of Law 15-18

Fundamental Principles

The Dahir No. 1-21-24 of 10 Rejeb 1442 (February 22, 2021) implementing Law No. 15-18 on crowdfunding established a new legal framework for crowdfunding in Morocco, also known as “crowdfunding.” This alternative financing method allows for the mobilization of financial resources from the public to support predetermined projects through specialized electronic platforms.

The main actors in crowdfunding are as follows:

SFC: Moroccan company managing one or more platforms.

PFC: online platform dedicated to crowdfunding.

Project holder: individual or entity benefiting from financial support.

Contributor: entity, whether physical or legal, providing funding to a project.

Angel investor: a qualified individual, possessing specific skills and resources.

The law allows for the financing of projects both in Morocco and abroad, provided that the rules related to currencies and local regulations are respected. It recognizes three types of financing:

Investment: giving money to become a shareholder.

The loan: lending money, with or without interest.

The donation: giving money without expecting anything in return.

The law specifies that the funds collected through crowdfunding do not fall under the scope of traditional banking laws:

The funds collected are not considered bank deposits within the meaning of the current regulations.

Loan operations carried out via crowdfunding platforms do not fall under the legal regime applicable to credit.

Investment operations are exempt from the obligations related to public fundraising.

Donations are not subject to the traditional legal framework governing charitable donations.

Donations in the form of waqf properties are expressly excluded from the scope of this legislation.

The operators of crowdfunding

The core of the crowdfunding mechanism relies on crowdfunding companies. These are Moroccan law companies, specially established to create, manage, and supervise crowdfunding platforms. Their role is essential to ensure the regularity and security of the operations carried out through these platforms.

Conditions for the creation and operation of crowdfunding companies

The law rigorously regulates the formation and operation of crowdfunding companies. The requirements aim to strengthen the reliability of the system:

SFCs must be established in the form of a public limited company or a limited liability company.

Their minimum share capital is set at 300,000 dirhams, fully paid up upon their creation.

They must establish their registered office within Moroccan territory.

Guarantees must be provided regarding internal organization, human and technical resources, as well as the performance of the information system.

Management of the executives

To ensure honest operation, the leaders of crowdfunding companies:

Must present a clean criminal and disciplinary record, with no convictions that could tarnish their morality, integrity, or reputation.

Must demonstrate professional skills in line with the requirements of collaborative financing.

Approval according to the nature of the operations

The exercise of the activity requires prior authorization, confirmed by the qualified authority depending on the type of operation:

Bank Al-Maghrib acts for platforms that offer loans or donations.

The AMMC is responsible for regulating platforms that offer investment operations.

Management regulations and additional obligations

Each crowdfunding company is required to draft a management regulation specific to each platform it manages. This document specifies:

The technical and legal mechanisms for the operation of the platform

Rules applicable to project holders and contributors;

The instruments for managing conflicts of interest and handling complaints.

Regulated complementary activities

In addition to their main mission, collaborative financing companies have the ability to authorize secondary activities, such as:

Support and advice to project holders before their publication on the platform;

The advertising of projects on external platforms;

The management of products for contributors, in accordance with the terms set by the regulations.

Major changes in the structure of the crowdfunding company

Ultimately, any major change in the structure or control of a crowdfunding company (e.g., a merger, a change of principal shareholder, or a change in legal form) requires obtaining a new approval. This requirement aims to maintain a high level of vigilance and compliance.

Crowdfunding Operations

Each category has its own rules, but some universal principles apply to all:

Annual fundraising amount: 10 million dirhams per project, with an overall cap of 20 million.

Limitation of individual contributions, except for qualified investors (business angels).

A project can be broadcast exclusively on only one platform at a time.

Maximum collection period: 6 months.

It is imperative that a written contract be established between the project holder and the contributor, whether on paper or electronic medium, in accordance with the standard clauses defined by regulatory means.

The project leader is required to submit an explanatory note including the following elements: objectives, schedule, risks, as well as the terms of use or reimbursement of funds.

For investment projects, it is necessary to conduct a feasibility study. For donations, it is necessary to obtain administrative authorization for amounts exceeding 500,000 dirhams.

Control and Supervision

The evolution of crowdfunding, as an innovative method for collecting savings in favor of economic, social, or cultural projects, requires the establishment of a strict oversight framework ensuring the transparency and security of transactions.

Dual supervisory authority

Law No. 15-18 establishes strict oversight, led by Bank Al-Maghrib and the AMMC, to ensure the transparency and safety of collaborative financing. This distinction allows each organization to act according to its capabilities and area of expertise, while ensuring comprehensive coverage of the sector.

Control modalities

The regulatory authorities (Bank Al-Maghrib and the AMMC) have extended powers to ensure the control of SFCs. They are authorized to:

Conduct document checks both remotely and on-site,

Require the provision of any relevant document or information,

Ensure compliance with the regulation on the management of crowdfunding platforms and current legal obligations.

In return, the SFCs must keep all documents required for the audit and provide them to the competent authorities.

Statutory Auditor: a complementary role

Each SFC is required to appoint an independent statutory auditor for a renewable period of three years. This professional is tasked with:

Verifying the financial statements of the SFC;

Ensuring that management complies with legal standards.

Preparing annual reports submitted to the competent authority;

In case of irregularity or suspicion of fraud, the commissioner is obliged to inform the supervisory authority without delay.

Injunctions and corrective sanctions

If the regulatory authority detects a serious anomaly, such as insufficient reliability of the information system or the absence of adequate internal control, it is entitled to order the SFC to rectify the situation within a specified timeframe.

If the SFC does not comply with this directive, the authority could impose stricter sanctions, including the possibility of revoking its license, which amounts to a prohibition on conducting its activities.

Objectives of the control

This supervision system aims at three main objectives:

Protecting contributors by ensuring access to trustworthy information and the security of their funds;

Ensuring the legitimacy of projects by verifying the identity, moral integrity, and solidity of project leaders;

Ensuring the sustainability of the sector by preventing systemic risks, fraud, and unfair practices.

Financial Provisions

Law No. 15-18 establishes a financial framework aimed at ensuring the sustainability of Financing Companies and strengthening their accountability within the supervisory system.

Payment of an annual fee

Starting from the fifth year following the issuance of their license, the SFCs are required to pay an annual commission to the competent authority (Bank Al Maghrib or the Moroccan Capital Market Authority), calculated on the collected funds, not exceeding 0.3%, in order to finance regulatory and supervisory missions.

Payment method

The legislation stipulates that the SFCs must comply with a maximum period of three months following the closure of their fiscal year to pay the annual fee required by the supervisory authority.

In case of non-compliance with this deadline, a late penalty of up to 2% per month or fraction of a month will be applied, which constitutes an incentive mechanism aimed at ensuring financial rigor and avoiding recurring delays.

Sanctions

The entire set of sanctions provided by Law No. 15-18 represents a vital element in the control of collaborative financing. It aims to ensure transparency, the rigor of participants, and the protection of those who contribute. Here is how this system is structured:

Prevention of deviations: the legislation aims to rigorously regulate the activities of SFCs to prevent erroneous practices, significant shortcomings, or information deficiencies.

Disciplinary sanctions: Maghreb or the AMMC, these measures include warnings, reprimands, or the suspension of executives in case of non-compliance with legal obligations (publication delays, absence of reports, etc.).

Monetary sanctions: Administrative sanctions of up to 50,000 dirhams are considered in cases of technical or formal irregularities (absence of legal mentions or professional membership declaration).

Criminal sanctions: The most severe situations, such as the illegal exercise of a crowdfunding activity or the fraudulent use of an approved name, can result in penalties of up to three years in prison and a fine of one million dirhams.

Recidivism: Any recidivism results in a doubling of the penalties incurred, which reinforces the deterrent effect of the legal framework.

Purpose of the system: Beyond the sanction, the objective is to maintain public trust, ensure the credibility of the field, and establish a balanced and safe regulatory framework.

Transitional and Final Provisions

The transitional and final provisions of Law No. 15-18 aim to regulate the gradual implementation of the new crowdfunding regulations, while ensuring a smooth transition for the participants involved. It is presented as follows:

Immediate entry into force: The law comes into effect upon its publication in the Official Bulletin, thus making prior approval mandatory for any platform, whether already existing or in the process of being created.

Creation of the ASFC: The law establishes a unique professional association, called the Association of Collaborative Financing Companies (ASFC), to which all licensed SFCs are required to adhere.

Organized governance: A general assembly of the SFC must be convened within two years to proceed with the election of the president and the board of the ASFC, thus establishing the foundations of collective regulation of the sector.

Purposes of the transitional measures: The objective is to facilitate a gradual adaptation to the new rules, while preventing interruptions in activity or situations of non-compliance, and promoting the organization of the sector around a legitimate professional representation.

Scope of the measure: The intention expressed by the legislator to reconcile innovation and legal security, while promoting the emergence of a collaborative, stable, and regulated financial ecosystem.

AMMC Guide – Crowdfunding

This guide helps investors understand the fundamentals of crowdfunding and provides them with accessible tools to analyze projects, assess risks, and engage in a crowdfunding operation in an informed manner.

Financial Terms

Dividend: potential income from a capital investment.

Interest rate: compensation for a loan.

Liquidity: ease of reselling an asset without significant loss of value.

Regulatory Concepts:

Approval: administrative authorization required to operate a platform.

Presentation note: document describing a project, required to evaluate it before contribution.

Angel investor: an experienced contributor who benefits from a special status.

Choice of platform:

Necessity to choose a PFC duly approved by the AMMC for investments or by Bank Al-Maghrib for loans and donations.

Importance of reading and understanding the general terms of use (GTU) of the platforms.

Project Analysis:

In-depth analysis of the submitted projects: objectives, responsible parties, projected budget, timeline, and risk identification.

Analysis of the past performance of projects funded on the platform.

Investment Strategies:

Diversification of investments to minimize overall risk.

Selection of projects based on their alignment with the investor’s risk profile.

Consideration of risks:

Risks associated with the non-implementation of the project (delays, abandonment, defaults).

Risk of non-repayment of capital or interest (particularly in the context of loan models).

Liquidity risk: absence of a secondary market for the acquired securities.

Risk of zero or insufficient returns, as well as capital loss.

Regulatory Framework

Necessity for SFCs to provide clear information to contributors regarding the inherent risks of each category of financing.

Right of recourse in case of platform or issuer failure.

Methodology

The study is based on an in-depth descriptive analysis of 1,262 campaigns launched between January 2023 and December 2024, representing a cumulative funding request of 142 million dirham. The criterion for success chosen corresponds to achieving the fundraising goal at 100%. The data used comes from the Crowdfunding Barometer in Morocco 2023-2024, developed by the Happy Smala innovation lab. This barometer includes campaigns from local and international platforms, supporting Moroccan projects with either a profit or non-profit aim, with particular attention given to campaigns initiated in the post-earthquake context.

Results and Discussion

State of crowdfunding in Morocco

The 2023-2024 barometer, designed by the Happy Smala Innovation Lab, presents an overview of crowdfunding in Morocco, encompassing all campaigns conducted on a range of both local and international platforms. These campaigns provide support to Moroccan projects, whether for profit or not, with particular attention to post-earthquake campaigns. By highlighting its solidarity dimension and identifying the obstacles to its development outside of emergency situations.

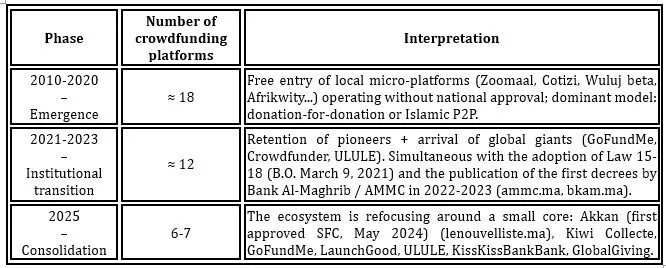

Table 1: Evolution of crowdfunding platforms (Happy Smala)

This table presents a comparative analysis of crowdfunding platforms, both local and international, that have contributed to the financing of Moroccan projects during the year 2023–2024. This ranking is based on the total amount collected by each platform.

Weight of international platforms: Foreign platforms largely dominate in terms of the volume of funds collected. GoFundMe stands out very clearly, with over 80 million dirhams collected, which alone represents more than 60% of the total volume observed. It is followed by GlobalGiving (nearly 21 million MAD) and LaunchGood, which are also international platforms specializing in solidarity fundraising.

Positioning of Moroccan platforms: Kiwi Collecte and Akkan represent the main local Moroccan platforms shown in the graph. Their share in the total volume of funds raised remains modest.

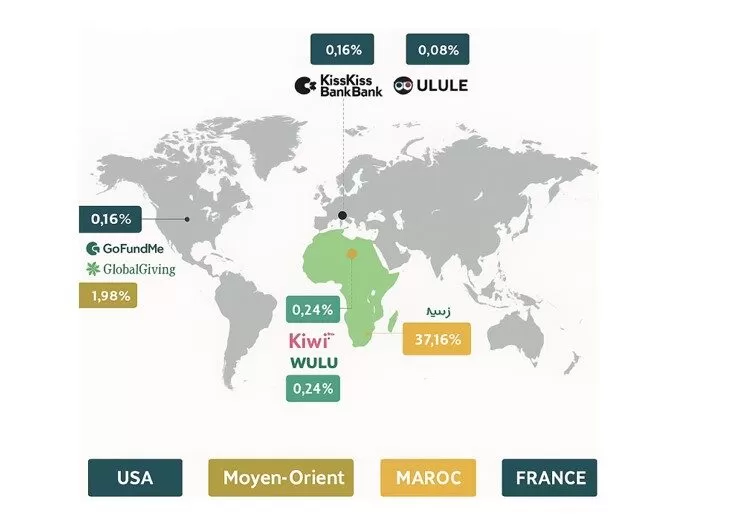

Fig 1. Mapping of crowdfunding platforms (Happy Smala)

Interpretation

Moroccan projects are primarily supported by the GoFundMe (59.47%) and LaunchGood (37.16%) platforms, due to their high visibility as well as their cultural or religious affinity. Local platforms such as Wuluj (0.24%) and Kiwi (0.08%) remain marginal, reflecting an ecosystem that is still poorly structured. Similarly, KissKissBankBank (0.16%) and Ulule (0.08%) are struggling to establish themselves due to a lack of community anchoring. This selection of platforms reflects a process of legitimization and trust on a transnational scale.

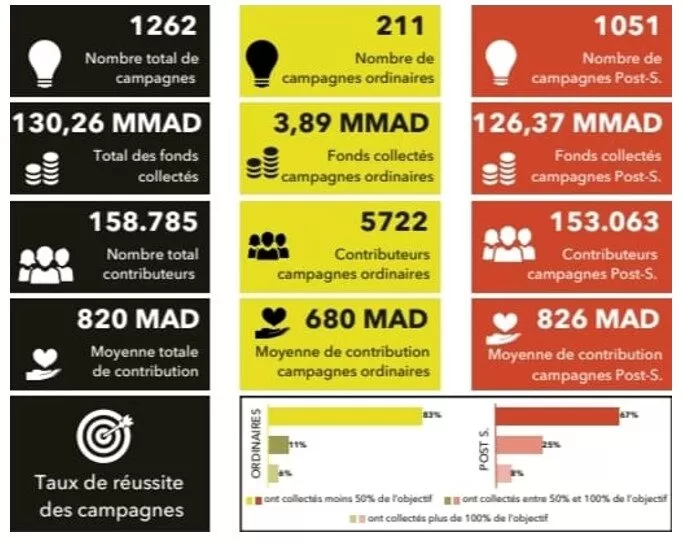

Fig 2. Comparison of pre- and post-earthquake performances (Happy Smala)

Interpretation:

Out of a total of 1262 crowdfunding campaigns, the campaigns initiated following the earthquake represent the most significant share of contributions, amounting to 126.37 million MAD, and mobilize a total of 153,063 contributors. Their success rate is high (67% exceeded their goal).

For ordinary campaigns, the rate is only 4%, with 83% failing to reach half of the set target. The average contribution is also higher for post-earthquake campaigns (826 MAD compared to 680 MAD). These discrepancies illustrate that the success of a campaign is closely linked to the emotional context as well as the perceived urgency.

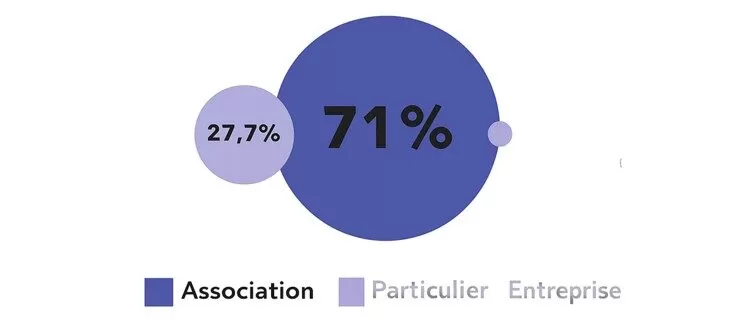

Fig 3. Typology of Crowdfunding Project Holders 2023–2024 (Happy Smala)

Interpretation:

This graph illustrates that 71% of campaigns are supported by associations, while 27.7% are supported by individuals, with companies being virtually absent. It also highlights that individuals frequently turn to associations to raise funds. This illustrates the predominance of the associative fabric in the field of crowdfunding in Morocco, which is frequently used as a trusted interface to ensure the security of transfers.

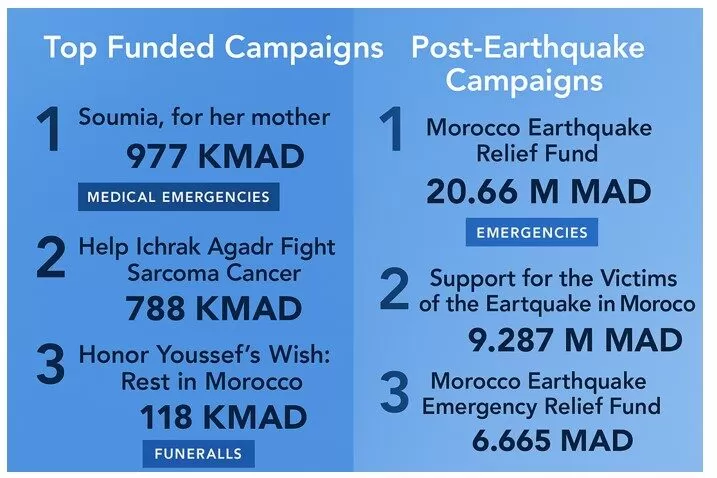

Fig 4. Comparative evolution of ordinary and post-earthquake campaigns (Happy Smala)

Interpretation:

The three ordinary campaigns receiving the most funding all involved medical emergencies or funeral expenses, with “Soumia for her mother” (977K MAD) in first position and “Ichrak Agadr Cancer” (788K MAD). This highlights the great receptiveness of donors toward individual and humanitarian causes.

Regarding post-seismic campaigns, the top three collected significantly higher amounts, particularly the “Morocco Earthquake Relief Fund” with 20.66 MMAD, followed by “Support for Earthquake Victims” (9.29 MMAD) and the “Emergency Relief Fund” (6.67 MMAD). These data attest that the emotional context, the magnitude of the crisis, as well as the media virality exert a predominant influence in the mobilization of funds.

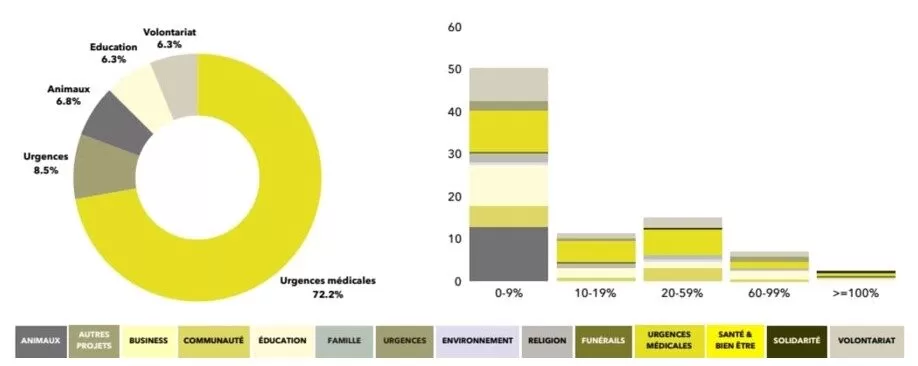

Fig 5. Distribution of projects according to the targeted impact and the success of the collections (Happy Smala)

Interpretation:

The examination of the thematic distribution of funded projects highlights a significant concentration of crowdfunding campaigns around medical emergencies, which represent more than 70% of all analyzed projects. The other categories, such as non-medical emergencies, animal protection, education, and volunteering, appear in a much more marginal manner. However, despite this strong mobilization in favor of medical causes, the majority of campaigns do not reach 10% of their funding goal.

The campaigns that manage to raise between 60 and 99% of the targeted funds are few in number, while those that reach or exceed the set goal remain exceptional. These data reveal a tension between the high demand for funding for critical situations and the persistent difficulty in mobilizing the necessary resources. They thus highlight the structural limitations of the model, while questioning the effectiveness of the platforms in their ability to concretely support project leaders, particularly in an emergency context.

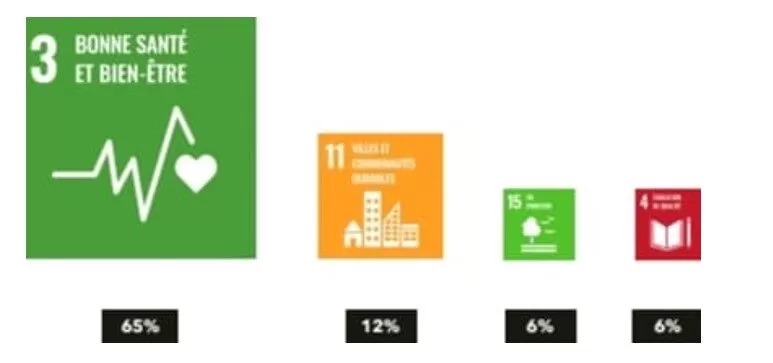

Fig 6. Distribution of campaigns by sustainable Development Goals (Happy Smala)

Interpretation:

This graph shows a strong concentration of crowdfunding campaigns around SDG 3, related to health and well-being, which represents 65% of the projects. This reflects a priority given to urgent health needs. SDG 11, related to sustainable cities and communities, follows with 12%, particularly in connection with post-earthquake reconstruction. SDG 15 (life on land) and SDG 4 (quality education), each at 6%, are underrepresented, highlighting a thematic imbalance. This observation highlights the need to diversify campaigns to better integrate all the sustainable development goals.

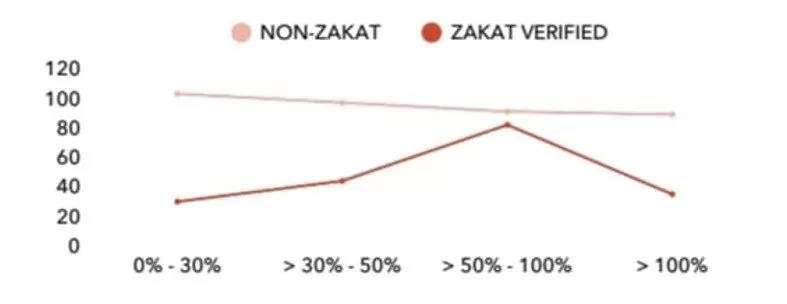

Fig7. Link between “Zakat verified” certification and campaign success (Happy Smala)

Interpretation: This graph shows that campaigns verified as eligible for Zakat perform better than others: they more often reach between 50% and 100% of their target. On the other hand, non-Zakat campaigns mostly remain below 50%. This suggests that the mention “Verified Zakat” reinforces donors’ trust and improves the chances of success, without necessarily leading to exceeding the goals.

Discussion and conclusion

The discussion reveals three major insights. First, the emergency context acts as a catalyst: 67% of the campaigns launched after the earthquake on September 8, 2023, reach or exceed their goal, compared to 4% for ordinary fundraising, confirming that collective emotion reduces information asymmetries and increases donors’ ex ante trust (Mollick, 2014; Kuppuswamy & Bayus, 2017). Secondly, the near-hegemony of platforms such as GoFundMe and LaunchGood (97% of the funds) shows that project leaders rely on the reputation of international platforms, which serves as due diligence in a regulatory environment still under construction, thus extending the analysis of Belleflamme et al. (2015). Finally, the “Zakat verified” certification significantly increases the likelihood of reaching the critical threshold of 50 to 100% of the goal, illustrating the relevance of signaling theory in an Islamic context (Spence, 1973). Optimal performance thus relies on three levers: an average duration of about 80 days, religious labeling as a guarantee of probity, and a clear financial objective, contradicting the classic principle of “small is beautiful” (Schwienbacher & Larralde, 2012).

In this context, Law 15-18 and its implementing decrees now provide a legal framework, but the ecosystem is still dominated by foreign platforms and ad-hoc mobilizations. To establish lasting local trust, national platforms must strengthen their cybersecurity, forge solid banking partnerships, and aim for an upgrade in their services. In parallel, optimizing the usual campaigns requires project leaders to professionalize themselves through training in digital storytelling, community management, and the development of post-funding reporting. Finally, the implementation of incentive mechanisms such as tax breaks or partial guarantees could broaden the base of domestic contributors and reduce dependence on international platforms.

The study, however, presents several limitations: a limited time horizon, a sample focused on donations, and the absence of post-collection evaluation. Longitudinal studies, the integration of psychometric variables related to digital trust, and international comparisons are necessary to confirm these results and transform the solidarity reflex into a sustainable mechanism for financing innovation and territorial development. The research conducted by Dardour, Abdoune and Bentebbaa (2018) corroborates this trend, highlighting the importance of project presentation, team reputation, and digital communication. A close collaboration between regulators, researchers, platforms, and project holders will be crucial to support and diversify sectors towards maturity, ensure the financial integrity of collections, and maximize the social impact of each dirham invested.

In summary, the emergence of a resilient and equitable Moroccan crowdfunding ecosystem will require evolving regulation, sustained financial education efforts, and transparency tools to establish lasting trust between contributors and project holders.

References

Afrique IT News (2024) ‘Akkan opens the door to crowdfunding in Morocco.’ Afrique IT News, 28 May. Available at: https://www.afriqueitnews.com (Accessed 17 May 2025).

Autorité Marocaine du Marché des Capitaux (AMMC) (2022) Investor guide: Understanding collaborative financing – Crowdfunding. 9th edn. Rabat: AMMC. Available at: https://www.ammc.ma (Accessed 1 June 2025).

Bessière, V. and Stéphany, É. (2014) ‘Le financement par crowdfunding : quelles spécificités pour l’évaluation des entreprises ?’ Revue Française de Gestion, 242, 149–161. https://doi.org/10.3166/RFG.242.149-161

Bessière, V. and Stéphany, É. (2017) Crowdfunding: Foundations and practices. Brussels: De Boeck Supérieur.

Dardour, A., Abdoune, R. and Bentebbaa, S. (2018) ‘Determinants of successful fundraising via crowdfunding platforms: The case of startups.’ Revue Internationale des Petites et Moyennes Entreprises, 31(2), 57–78. https://doi.org/10.3917/mav.105.0081

Happy Smala (2024) Barometer of crowdfunding in Morocco 2023–2024. Casablanca: Happy Smala. Available at: https://www.happysmala.com/impact-together (Accessed 26 July 2025).

Jensen, M.C. and Meckling, W.H. (1976) ‘Theory of the firm: Managerial behavior, agency costs and ownership structure.’ Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

Katz, M.L. and Shapiro, C. (1985) ‘Network externalities, competition, and compatibility.’ American Economic Review, 75(3), 424–440. https://doi.org/10.2307/1814809

Kuppuswamy, V. and Bayus, B.L. (2017) ‘Does my contribution to your crowdfunding project matter?’ Journal of Business Venturing, 32(1), 72–89. https://doi.org/10.1016/j.jbusvent.2016.10.004

Loi n° 15-18 relative au financement collaboratif (2021) Bulletin Officiel du Royaume du Maroc, n°7014, 19 août.

Moussavou, J. (2017) ‘Information asymmetries and crowdfunding: The case of entrepreneurial project financing.’ Revue Française de Gestion, 268, 62–76. https://doi.org/10.3166/rfg.2017.00176

Schumpeter, J.A. (1939) Business cycles: A theoretical, historical, and statistical analysis of the capitalist process. Vols. 1–2. New York: McGraw-Hill.

Sen, A. (1977) ‘Rational fools: A critique of the behavioral foundations of economic theory.’ Philosophy & Public Affairs, 6(4), 317–344. https://doi.org/10.2307/2264946

Tian, Z., Guan, L. and Shi, M. (2018) ‘The key factors of successful internet crowdfunding projects: An empirical study based on different platforms.’ In: Proceedings of the 2018 International Conference on Industrial Economics System and Industrial Security Engineering (IEEISE). https://doi.org/10.1109/ICIEEM.2018.8758887