2E.H.E. Europa University EurAKA, c/o Businesspark NWS AG, Zelgliweg 3, Itingen, Switzerland

Volume 2025,

Article ID 366602,

Journal of Organizational Management Studies,

12 pages,

DOI: doi.org/10.5171/2025.366602

Received date: 9 April 2025; Accepted date: 15 July 2025; Published date: 15 September 2025

Academic Editor: Ivana Dvorski Lackovic

Cite this Article as:

Dietmar Ernst and Nicole MAU (2025)," Simulation-based Valuation of German Mid-sized Firms: A Risk-oriented Alternative to Traditional CAPM Approaches”, The Journal of Organizational Management Studies, Vol. 2025 (2025), Article ID 366602, https://doi.org/10.5171/2025.366602

The valuation of small and medium-sized enterprises (SMEs) is a key task for corporate transactions, succession planning, capital raising and changes in the shareholder structure. In Germany, the valuation of small and medium-sized companies is mainly based on the IDW S 1 standard, which requires the use of the Capital Asset Pricing Model (CAPM) to derive the risks of a company from the capital markets. The CAPM itself is based on very restrictive assumptions that are not suitable for the valuation of SMEs. A notable gap in the literature exists in the development of valuation methods that directly incorporate company-specific risk data instead of relying on market-based proxies, especially in light of recent legal and regulatory changes (e.g., StaRUG, IDW PS 340) that now require SMEs to systematically document and manage risk. To address this issue, the study proposes a simulation-based valuation approach that uses Monte Carlo simulations to aggregate firm-specific risks from internal planning systems and derive risk-adjusted values for cash flows and cost of capital. The results show that simulation-based valuation is not only consistent with modern regulatory and legal requirements, but also provides a methodologically sound alternative to CAPM by providing risk-adjusted enterprise values that better reflect the realities and challenges of SME valuation.

Keywords: Simulation-Based Valuation, SME, CAPM

Introduction

The valuation of small and medium-sized enterprises (SME) is a task that has not yet been sufficiently addressed in academic discourse. Although the characteristics and the associated business practices of SMEs have been extensively researched, the question of how to include these special features in a business valuation has not yet been satisfactorily resolved. One reason for this is the dominance of capital market-oriented Anglo-Saxon valuation theory, which is primarily aimed at the valuation of large and listed companies. In conjunction with the neoclassical Capital Asset Pricing Model (CAPM) (Sharpe, 1964; Lintner, 1965; Mossin, 1966), which is based on perfect capital markets, a simple, transparent and comprehensible approach was developed that derives the risk of companies with the help of capital market data. With the help of the CAPM, which is essentially based on the findings of portfolio theory (Markowitz, 1952), the cost of equity for a company to be valued is determined for a benefit-maximizing, strictly rational and risk-averse investor who holds a perfectly diversified portfolio of companies. This valuation theory is now state of the art in Germany and is also used in the valuation of SME (Behringer, 2012; Ihlau and Duschau, 2019). This is justified by the lack of suitable valuation methods for SME and the lack of risk information about the SME to be valued. As a result, risk premiums for SME were applied to the CAPM values in valuation practice in order to obtain more realistic decision values (Ernst et al., 2012, p. 73 ff.). The fact that these approaches are methodologically incorrect is a major problem in the valuation of SME. In the meantime, however, the starting point for the valuation of SME has changed fundamentally.

Hier ist eine präzisere, wissenschaftlichere Fassung, die sich gut in einen akademischen Artikel einfügt:

—

Due to the regulatory changes introduced by Directive (EU) 2019/1023 and its transposition into German law through the Corporate Stabilization and Restructuring Act (StaRUG), as well as the related auditing standard IDW PS 340 (Romeike, 2019), enterprises are required to implement formal risk management and early warning systems. These provisions oblige firms to systematically identify, evaluate, and document material risks that could jeopardize their going-concern status.

Consequently, it can be reasonably assumed that even small and medium-sized enterprises (SMEs) maintain a structured and comprehensive risk information base. This risk data does not only serve compliance and reporting obligations but also provides a reliable foundation for risk-adjusted business valuations. Hence, the legal and regulatory framework has significantly enhanced both the availability and quality of risk-related information necessary for valuation purposes.

With simulation-based planning and valuation, a method has been developed that allows the risk information from the risk early warning system of SME to be processed and the imperfections of the markets to be taken into account in valuations.

To guide the reader, the article is structured as follows. First, an overview of the current state of SME valuation is given. It is explained that although the CAPM is currently regarded as the standard for the valuation of SME, valuation practice uses pragmatic solutions that attempt to overcome the weaknesses of the CAPM. However, these solutions are not alternatives to the CAPM, but merely modifications that cannot be justified from a scientific point of view. Simulation-based planning and valuation are presented as an innovative approach to the valuation of SME. The drivers that promote its use and the advantages of this approach compared to previous methods for valuing SME are discussed in detail.

Current state of research

Current status of the valuation of SME

The concept of simulation-based valuation of SME

Conclusion

Current State Of Research

The valuation of SME is a field of research that has primarily attracted attention in Europe (Marcello and Pozolli, 2019), but above all in German-speaking countries (Ihlau and Duschau, 2019; Behringer, 2012). This is certainly due to the fact that SMEs are of particular economic importance in German-speaking countries. Despite the high macroeconomic importance of SMEs and the challenges involved in their valuation, the topic has received little attention in valuation theory. One can get the impression that the topic has been exhausted and that few innovative approaches are used.

In particular, in the German context, business valuation theory is strongly influenced by the auditing profession. This profession is organized in the Institute of Public Auditors in Germany (IDW), which has formulated the principles for carrying out business valuations in Germany with IDW S 1 as amended in 2008 (IDW 2008). Although this standard is not legally binding, it is used as a reference in official valuation reports. IDW S 1 is based on international valuation standards, which in turn are heavily dominated by Anglo-American valuation theory. These are based on the principles of modern capital market theory, which, in line with the neoclassical school, assume perfect capital markets and primarily focus on the valuation of large, listed companies. In valuation theory, the risks of a company are derived from capital market data using the Capital Asset Pricing Model (CAPM). The scope of risk is captured by a risk-adjusted discount rate, which is derived from (historical) share returns using the Capital Asset Pricing Model (CAPM) via the beta factor. However, this schematic approach often does not include a quantitative risk analysis of the valuation object, as it is assumed that the risks are adequately taken into account by the described risk adjustment of the discount rate. This is often not the case for SMEs or personal companies in particular (Gleißner and Ihlau, 2012).

Numerous critiques have emerged that challenge the applicability of the CAPM to SMEs. Fama and French (Fama and French, 1992), Carhart (Carhart, 1997), Fama and French (Fama and French, 2015) and Azevedo, Kaserer and Campos (Azevedo et al., 2021) have developed multi-factor models that can explain stock market returns far better than the CAPM. All of these approaches are based on the common idea of explaining the level of risk of a company via the capital markets, but not via the actual risk potential in the company. The special features of SME are also not taken into account in these approaches.

Despite these limitations, the CAPM remains widely used in practice, leading to various pragmatic adaptations. In 2001, the FEE (now ACE – Accountancy Europe) published recommendations for the valuation of SME. IDW Practice Note 1/2014 (IDW 2014) specifies the requirements of IDW S1 with regard to SME. The Practice Note attempts to identify existing problem areas from the perspective of the profession and to provide guidance on a uniform approach to dealing with them. The fact that the CAPM is still being used to determine the cost of equity is to be viewed critically.

The American literature discusses various approaches that can be used to evaluate SME. Among these adaptations, one notable approach is the Total Beta method. The creation and naming of the total beta approach is closely related to the name Aswath Damodaran (2012). Damodaran assumes that the owners of SMEs have invested all their capital in the SMEs and recommends using total beta, which includes both systematic and unsystematic risks, instead of the beta factor which only includes systematic risks. The mathematical procedure consists of dividing the beta factor by the correlation coefficient. The total beta approach seems to describe the valuation situation of SME better, but still has the disadvantage of deriving the risks from the capital market and not from the company itself.

The second relevant approach is known as the “Modified CAPM” (MCAPM). The MCAPM (Damodaran, 2012) is based on the standard CAPM. The MCAPM adapts the standard model to better value SME companies by adding unsystematic risks, such as size risk and company-specific risk. This helps to capture the higher uncertainty and limited market data typically associated with SME, resulting in a more accurate cost of equity. This is supplemented by a small company premium and a company-specific adjustment (so-called “Specific Company Risk Premium”) for additional risk factors.

Related to the MCAPM is the “Build-up Method” (Pratt and Gabowsi, 2014). The concept of the build-up method is similar to that of the MCAPM. In contrast to the MCAPM, however, the build-up method uses only the general market risk instead of a company-specific beta factor, which means a beta factor of one. This means that all company-specific risk factors are included in the size discount and the specific company risk premium. The MCAPM, on the other hand, only reflects those company-specific risks that are not yet included in the beta factor. Industry-specific risks can also be included in the build-up method. The basis for measuring the individual premiums and discounts are empirical capital market studies such as those carried out by Duff & Phelps (Duff & Phelps et al., 2017). Numerous studies on quantification and empirical relevance have been conducted in the USA and Germany. Ihlau and Duschau (2019) provide a very good overview of the results. It can be seen from this that it is not possible to make general statements about SME-related risk premiums (Ernst et al., 2012). Furthermore, modifications to the CAPM should be rejected methodologically. The CAPM is a self-contained capital market model. The addition of the “size premium” destroys the premises and the equilibrium solution of the CAPM (Jonas, 2008). The application of a general “size premium” should therefore be rejected.

Due to the increasing recognition of imperfections in capital markets – such as information asymmetries, transaction costs, illiquidity, and behavioral biases – traditional valuation models based on the assumption of perfectly efficient markets have faced growing criticism. In response, valuation approaches have been developed in recent years that explicitly address these real-world conditions.

These approaches, on the one hand, derive a company’s risk exposure through a structuered and quantitative risk analysis, considering both systematic and unsystematic risks. On the other hand, they explicitly incorporate the consequences of market imperfections into the valuation process, for example by adjusting discount rates, expected cash flows, or cost-of-capital assumptions. By doing so, they aim to provide a more realistic and decision-useful assessment of enterprise value that better reflects the risk–return profile under actual market conditions.

These new approaches can be divided into two categories: investment theory valuation and simulation-based valuation. For more information, see Matschke and Brösel (2021), Hering (2021), Ernst (2022a), and Gleißner and Ernst (2019), as well as the literature cited therein. Simulation-based business valuation offers a good approach to taking into account the special features of the SME to be valued by means of a risk analysis and thus enabling a risk-adequate valuation. It also meets the legal requirements for an early risk identification system (StaRUG), the new auditing standards for early risk identification systems (IDW PS 340) and the new principles of proper corporate planning (GoP).

Current status of the valuation of SME

To better understand the implications for practical valuation, the following section outlines the current standard approaches applied in SME valuation.

CAPM as the standard for risk calculation

When valuing SME, the valuation standard S1 of the IDW is primarily used, which prescribes the CAPM (Gleißner (2014) provides a good overview of the discussion surrounding the CAPM) to determine the cost of equity. For large and listed companies, it may well make sense to derive the risk – measured as a beta factor – using capital market models. In the world of SME, the model assumptions of the CAPM are not fulfilled due to the special characteristics of SME. The consequence of this is that the entrepreneur not only bears the systematic risks (market risks) as in the CAPM, but also the unsystematic risks (company-specific risks). As the unsystematic risks are decisive for the success or failure of SME, they are of great importance. The assumption of a perfectly diversified portfolio in which all unsystematic risks can be eliminated means that the actual risks for SME are greatly underestimated. As a result, only some of the risks are priced in when calculating the cost of equity, which tends to lead to low costs of equity. Low equity costs then lead to high company values. This issue becomes evident during the sale of a medium-sized enterprise (Dreher and Ernst, 2021). CAPM-based valuation reports often yield company values that exceed what potential buyers are willing to pay. This is due to the fact that the buyer prices all risk into the purchase price in its valuation and offer. After all, the purpose of due diligence (risk analysis) when acquiring a company is to uncover all risks. It is obvious that these are then also taken into account in the purchase price offer.

Practical approaches to risk-adequate valuation in SME

As we have seen, a CAPM-based business valuation does not lead to any meaningful decision-making aids for SME. This problem is well recognized in SME valuation practice. Given these limitations, practitioners have adopted various workarounds to approximate more realistic cost of equity figures.

a) Fixed target return

It is possible to determine the cost of equity on the basis of a fixed return expectation of the owners if the equity providers or investors for whom the valuation is prepared have a specific return expectation for the company to be valued (see Ernst and Häcker, 2017, p. 554). Investment companies, for example, express return expectations, as they in turn have to offer their investors the prospect of a specific return target. For medium-sized companies, investment companies often set a minimum return of 15% p.a. after tax. A critical aspect of this approach is that the derivation of the cost of equity is not very transparent and comprehensible.

b) Derivation of the cost of capital from multiple-based prices

An investor often has specific purchase price expectations due to the parallel application of multiple methods and their transaction experience. If the corporate planning is accepted by both parties, the appropriate cost of equity can be derived from the purchase price expectations and the company’s cash flows, as a multiple is the reciprocal value of the cost of capital. The problem with this approach is that it mixes the “value” and “price” dimensions of a company, which is not permissible according to business valuation theory and the IDW S1 business valuation standard.

c) Premiums for SME-specific risks on the CAPM values

In order to be able to model realistic return expectations and capital costs for SME, SME-specific risks are added to the CAPM values in valuation models. This ensures that all valuation-relevant risks are included in the calculation of the cost of equity.

Which SME-specific risks are used in practice? Among the many possible risks, the following are often named as SME-specific risks and taken into account by means of mark-ups (see Ihlau and Duschau 2019, p. 226 ff.; Ernst et al. 2012, p. 73 ff.):

Unsystematic risks: Unsystematic risks – unless a perfectly diversified portfolio exists – are often decisive for the value of the SME. Examples of transaction-related risks include a lack of company succession, potential bad debt losses, the loss of a major customer, dependencies on a supplier, contaminated company premises, ongoing legal proceedings, expiring patents, etc.

Fungibility surcharge (liquidity surcharge, mobility surcharge): The fungibility surcharge is intended to cover the risk that it is not possible to sell company shares at any time at a reasonable price and without high transaction costs due to the lack of a stock exchange listing for SME.

Surcharge for personal liability: A surcharge for the personal liability of the shareholder may be justified if the shareholder provides collateral from his private assets.

Package premium (control premium): Package premiums can be taken into account if a majority shareholding is acquired, as the acquirer then has the opportunity to actively influence the company’s business policy.

However, these pragmatic solutions introduce their own set of challenges, as outlined below.

Problems In Current Valuation Practice

As relevant as SME-specific risks are to valuation, quantifying them is difficult. The risks mentioned have very different dimensions, making it almost impossible to cast them into a common risk measure. In SME, there are often several SME risks that are relevant to valuation. We are therefore again dealing with a portfolio of risks whose combined effects must be taken into account in the modeling. This is because two risks that are manageable on their own can pose a threat to the company’s existence when combined. In practice, one helps oneself by calculating flat-rate premiums for the SME risks mentioned and simply adding them together, disregarding interactions. Although a modification of the CAPM to include SME risks is understandable from a practitioner’s perspective, it should be strictly rejected from a methodological point of view. The CAPM with its restrictive premises must either be accepted or rejected. Variations in between are not scientifically justifiable and are (rightly) not accepted in an official valuation report. This approach also contradicts IDW S.1. In light of the methodological shortcomings of CAPM-based and modified approaches, simulation-based valuation has emerged as a promising alternative.

The concept of simulation-based valuation of SME

As we have seen, the business valuation of SME is at a methodological impasse. Simulation-based business valuation could provide a way out.

Conception of the simulation-based evaluation

Simulation-based business planning and business valuation addresses the points of criticism of the valuation practice practiced to date by SME. Simulation-based valuation methods are DCF business valuation methods that are based on the quantification of future risks of the valuation object, aggregate the risks by means of simulation, calculate risk measures from this and use these as the basis for the business valuation.

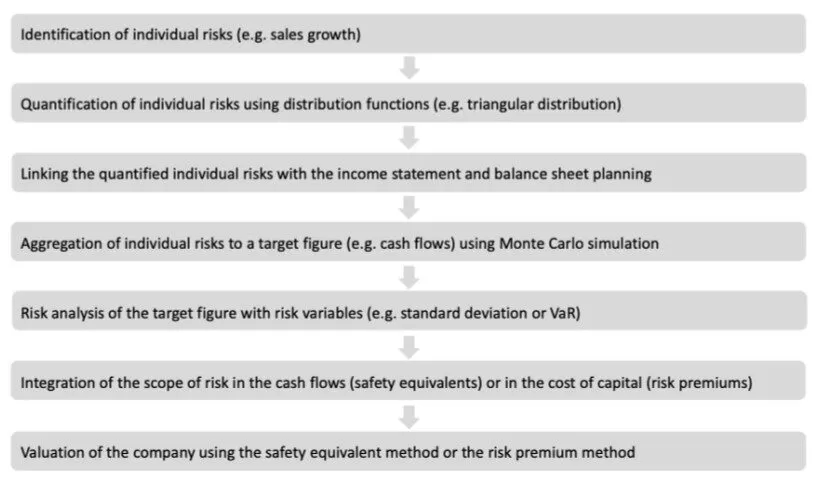

In these methods, the effects of the individual risks of the SME (taking correlations into account) are allocated to the corresponding items of the budgeted income statement and budgeted balance sheet as part of planning in line with expectations (Ernst and Häcker, 2024). The risk effects of the individual risks (e.g. sales fluctuations) are described by probability distributions (e.g. a triangular distribution, PERT distribution or normal distribution). Many thousands of future scenarios are run through in independent simulation runs as part of a Monte Carlo simulation (Gleißner, 2004, p. 355). The entirety of all simulation runs forms a representative sample of all possible risk-related future scenarios for the income statement and balance sheet. The target variables of the simulation are, for example, the cash flows. Aggregated frequency distributions can be determined from the determined realizations of the target figures. Based on the frequency distribution of the cash flows, risk measures can now be calculated which are based on the actual risk scope of the cash flows. The most frequently used risk measures are the standard deviation or the value at risk. Safety equivalents and risk-adequate capital costs can be derived from the results of the risk analysis. In the safety equivalent method, also known as the risk discount method, a risk discount is first deducted from the expected value of the cash flow in the numerator. The resulting certainty equivalents are then discounted at the risk-free interest rate to obtain the enterprise value. In the risk premium method, which is widely used in practice, the expected value of the cash flow without a risk discount is used in the numerator. This is then discounted using the risk-adjusted cost of capital from the risk analysis and the enterprise value is calculated. Figure 1 shows the process of simulation-based business planning and business valuation (see Ernst (2022b), p.99).

Fig. 1. Process of simulation-based corporate planning and business valuation

Drivers for the use of simulation-based evaluation

a) Legal emphasis on risk analysis and risk aggregation as part of business valuation

Companies are mandated by law to implement comprehensive risk management systems. An example of this is the Directive (EU) 2019/1023, which addresses the importance of appropriate risk management and requires the establishment of clear and transparent early warning and communication systems to identify risks that could threaten the viability of companies at an early stage (cf Article 3 of Directive (EU) 2019/1023). Auditors are required to review the company’s early risk detection system as part of their audit in accordance with IDW Audit Standard 340 (from 2020). Ultimately, this means that SME must have an early risk identification system in place, the findings of which must be taken into account in all business decisions made by the management. If this is not done, the management is personally liable.

b) Improved data situation for a risk analysis

The previous justification for risk analysis with a focus on (historical) capital market data, namely the lack of suitable alternatives, can no longer be accepted today. Due to the aforementioned laws and auditing standards, it can now be assumed that a great deal of information about the opportunities and threats (risks) of a company is available within the company and must be used as a basis for decisions.

c) Inability of traditional financial valuation methods based on perfect markets to take transformation effects into account

The term VUCA summarizes the challenges that companies have to face in an increasingly digitalized world. In management theory, the term stands for Volatility, Uncertainty, Complexity and Ambiguity (see also Kuznik 2016). The volatility of transformation unleashes enormous forces and is the catalyst for radical change. This is particularly true for SME. Transformation refers to the impact of disruptive technologies that bring new competitors into the market and threaten existing business models. These extreme events are associated with a high degree of parameter uncertainty and therefore pose particular problems for corporate planning, value-oriented corporate management and risk management.

These statements describe exactly the opposite of what is assumed in modern capital market theory as the premises of the model world and is considered suitable as a basis for decision-making. Due to their model assumptions, they cannot in any way take into account the phenomena typical in a transformation phase.

d) Errors and liability risk if the insolvency risk is ignored

The CAPM is based on the premise that there is a fixed investment universe to which neither a new investment can be added nor from which an investment can be removed. As a result, the insolvency of a company, with the associated interruption of the cash flow for the owners, is not envisaged. This means that the company is assumed to have an infinite lifespan. In the meantime, there are a large number of publications that address this issue and emphasize the importance of insolvency risk (see e.g. Gleißner, 2010; Saha and Malkiel, 2012; Friedrich, 2015; Lahmann et al., 2018). Today, there is no longer any doubt about the importance of insolvency risk and the need to include it in business valuation.

e) New valuation methods available (risk-value models – imperfect replication)

In the past, it was regularly argued that there was no alternative to the valuation theory of perfect markets based on financial theory. Based on the fundamental ideas of simulation-based valuation theory, innovative valuation methods have been developed in recent years that take into account the special features of imperfect capital markets and SME. This approach to simulation-based corporate planning and business valuation is presented in the next section.

Advantages of the simulation-based evaluation of SME

The advantages of simulation-based corporate planning and business valuation address the weaknesses of CAPM-based business valuation and offer solutions for taking into account the risk situation in companies and the imperfections in markets.

a) Use of planning in line with expectations

Expected plan values are a necessary prerequisite for the application of the discounted earnings value or discounted cash flow method (see IDW 2008). An expected value expresses which characteristics of earnings or cash flow will occur “on average” in all possible future scenarios based on risk. Accordingly, a reconciliation to expected values is required for the simulation-based valuation.

b) Consideration of corporate risks in corporate planning

Another advantage of simulation-based corporate planning is that all significant relationships between plan values and risk values are considered and checked for plausibility when setting up the simulation model, i.e. integrated P&L, balance sheet and cash flow statement planning including the distribution functions of corporate risks. In a simulation-based valuation, Monte Carlo simulation is used to calculate future scenarios for the company, taking into account the dependencies of the planning items. A simulation-based valuation is based on a critically and systematically analyzed planning model in which existing dependencies and uncertain planning assumptions are systematically examined.

c) Consideration of the insolvency risk in the business valuation

The insolvency risk, which can be expressed by the insolvency costs and in particular the probability of insolvency, influences the amount and development over time of the expected values of the cash flows and also the cost of capital (see Gleißner, 2011, and Lahmann et al., 2018). The possibility of insolvency leads to a finite expected value for the duration of a company’s existence and, as a rule, a termination of payments to the owners, which must be taken into account when determining the company value. This consideration is virtually “automatic” in a simulation-based valuation. It is only necessary to define the conditions under which insolvency occurs. In particular, it is possible to determine the probability of scenarios occurring that lead to insolvency and thus the interruption of the cash flow. The effects of insolvency costs and the probability of insolvency are thus taken into account directly in the simulation when determining the expected values of the cash flows.

d) Derivation of a risk-adjusted discount rate (cost of capital rate) directly from the simulation results

A simulation-based valuation does not require independent and potentially inconsistent models for “numerator” and “denominator”. The value of a payment depends on (1) the expected value, (2) the timing and (3) the risk content of these cash flows. The risk content of the cash flows from the simulation can be expressed by a risk measure, such as the standard deviation or the value at risk of the cash flows. The risk measure can be converted directly into a suitable risk-adjusted discount rate (or a certainty equivalent) (for the basics of valuation with risk-value models and the “imperfect replication” method, see Dorfleitner and Gleißner, 2018; Dorfleitner, 2020). In contrast to the traditional “capital market-oriented” valuation, the cost of capital in a simulation-based valuation can be derived directly from the earnings risk as a result of risk analysis and risk aggregation instead of from historical fluctuations in share returns (as is usually the case with the CAPM beta factor).

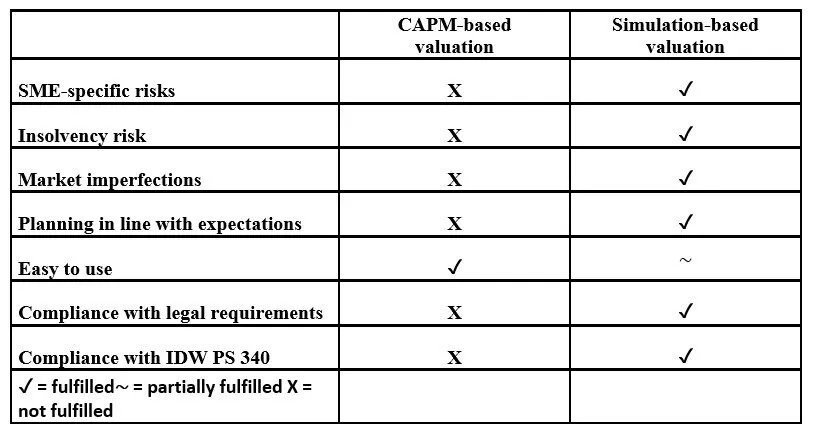

Table 1 summarizes the comparison between CAPM-based and simulation-based business valuation (see Ernst (2022b), p.104).

Table 1. Comparison between CAPM-based and simulation-based business valuation

Conclusion

The article shows that business valuation models based on modern capital market theory (in particular the CAPM) are not very suitable for the valuation of SME. This is due to restrictive model assumptions that do not take into account the special features of SME. They are therefore unable to provide decision-making aids for entrepreneurial action. Consequently, modifications to the CAPM have been developed in business valuation practice, but these contradict the assumptions of the CAPM and should therefore be rejected methodologically.

Due to current legislation and auditing standards as well as further developments in valuation theory, there are innovative approaches that overcome the previous limitations in the valuation of SME. Simulation-based valuation is a method of valuing an SME based on its given risk situation without having to derive the risk from a peer group of listed companies in a simplified manner. The StaRUG and IDW PS 340 mean that the risk data required for this are recorded and evaluated in the SME.

Simulation-based business valuations can be used to determine risk-adequate company values for succession issues or SME transactions, for example, which serve as a basis for purchase price negotiations. This was previously not possible with CAPM-based business valuations, which is why M&A practice relies almost exclusively on multiple methods to determine the purchase price of SME. Although these reflect the current prices of SME, they do not provide any information on the risk-adequate equivalent value an investor receives for the purchase price.

Simulation-based corporate planning and business valuation represent a paradigm shift in the valuation of SME. It would be desirable for the IDW to deviate from the paradigm of perfect capital markets in its standards for the valuation of SME and recognize that the valuation of SME requires methods that capture the special features of SME in the derivation of risk. The scientific community should be required to provide methods for integrating SME risk information into corporate planning. Furthermore, simulation-based models are needed that are based on the familiar DCF approaches and are designed in such a way that they can be understood by decision-makers despite their increased complexity. Ernst’s model (2022a) shows that this can be achieved. This model should be adapted to the specific characteristics of SME and the added value that simulation-based corporate planning and valuations create compared to the approaches used to date should be demonstrated.

Finally, it should be noted that the implementation of simulation-based corporate planning and evaluation depends heavily on the willingness of SME owners and managers to engage with this innovative approach. Especially in SME, there is a lack of awareness among SME owners and managers to deal intensively with risk management issues. In addition, there is also a lack of qualified personnel in SME who are able to carry out simulation-based business planning and assessments. As legislation, auditing standards and the new principles of proper business planning require an intensive examination of risks and their effects, SME owners and managers should see risk management issues in conjunction with simulation-based planning and evaluation less as an additional burden and more as an opportunity. The opportunities lie in increasing the stability of their SME, reducing costs in the event of damage and losses, improving the SME’s rating, reducing the cost of capital and increasing the value of the company.

References

Azevedo, V., Kaserer, Ch. and Campos, L. M. S. (2021) ‘Investor Sentiment and the Time-varying Sustainability Premium,’ Journal of Asset Management 22, 600-621.

Behringer, S. (2012) Unternehmensbewertung der Mittel- und Kleinbetriebe, 5th edition, Berlin: Erich Schmidt Verlag.

Carhart, M. M. (1997) ‚On Persistence in Mutual Fund Performance,‘ Journal of Finance, 52 (1), 57-82.

Damodaran, A. (2012) Investment Valuation: Tools and Techniques for Determining the Value of Any Asset, 3rd ed., Hoboken, NJ: Wiley.

Dorfleitner, G. and Gleißner, W. (2018) ‘Valuing Streams of Risky Cash Flows with Risk-value Models,’ Journal of Risk, 20 (3), 1-27.

Dreher, M. and Ernst, D. (2021) Mergers & Acquisitions, Understanding M&A Processes for Large- and Medium-Sized Companies, Cham: Springer.

Duff & Phelps et al (2017) Valuation handbook – U.S. guide to cost of capital, New Jersey: Willey.

Ernst, D. (2022a) ‘Simulation-Based Business Valuation: Methodical Implementation in the Valuation Practice,’ Journal of Risk and Financial Management, 15, 1-17.

Ernst, D. (2022b) ‘Bewertung von KMU: Simulationsbasierte Unternehmensplanung und Unternehmensbewertung,’ Zeitschrift für KMU und Entrepreneurship, 70 (2), 91-108.Ernst, D. and Häcker, J. (2017) Financial Modeling: An Introductory Guide to Excel and VBA Applications in Finance, London: Palgrave Macmillan.

Ernst, D. and Häcker, J. (2024) Corporate Risk M: A Case Study on Risk Evaluation, Cham: Springer.

European Parliament Directive 2019/1023/eu of the european parliament and of the council of 20 june 2019 on preventive restructuring frameworks, on discharge of debt and disqualifications, and on measures to increase the efficiency of procedures concerning restructuring, insolvency and discharge of debt, and amending directive (eu) 2017/1132 (directive on restructuring and insolvency). Official Journal of the European Union 18, pp. 18 – 55.

Fama, E. F. and French, K. R. (1992) ‘Section of Expected Stock Returns,’ The Journal of Finance, 47 (2), 427-465.

Fama, E.-F. and French, K.-R. (2015) ‘A five-factor asset pricing model,’ Journal of Financial Economics, 116 (1), 1-22.

Friedrich, T. (2015) Unternehmensbewertung bei Insolvenzrisiko, Peter Lang: Frankfurt am Main.

Gleißner, W. (2004) ‚Die Aggregation von Risiken im Kontext der Unternehmensplanung,‘ Zeitschrift für Controlling & Management, 5, 350-359.

Gleißner, W. (2010) ‚Unternehmenswert, Rating und Risiko,‘ WPg, 63 (14), 735-743.

Gleißner, W. (2011) ‚Risikoanalyse und Replikation für Unternehmensbewertung und wertorientierte Unternehmenssteuerung,‘ WiSt, 11, 345-352.

Gleißner, W. (2014) ‚Kapitalmarktorientierte Unternehmensbewertung: Erkenntnisse der empirischen Kapitalmarktforschung und alternative Bewertungsmethoden,‘ Corporate finance: Finanzierung, Kapitalmarkt, Bewertung, Mergers & Acquisitions, 5 (4), 151-167.

Gleißner, W. (2021) Risikomanagement für KMU – Krisenfrüherkennung nach StaRUG, Merkblatt Nr. 1955, DWS Steuerberater Medien GmbH: Berlin.

Gleißner, W. and Ernst, D. (2019) ‘Company Valuation as Result of Risk Analysis: Replication Approach as an Alternative to the CAPM, Business Valuation OIV Journal, 1 (1), 3-18.

Gleißner, W. and Ihlau, S. (2012) ‚Die Berücksichtigung von Risiken von nicht börsennotierten Unternehmen und KMU im Kontext der Unternehmensbewertung,‘ Corporate finance / Biz., 3 (6), 312-318.

Hering, Th. (2021) Unternehmensbewertung, 4th ed., De Gruyter Oldenbourg: Munich.

IDW (2008) IDW S 1 as amended in 2008: Grundsätze zur Durchführung von Unternehmensbewertungen.

IDW (2014) IDW Praxishinweis 1/2014: Besonderheiten bei der Ermittlung eines objektivierten Unternehmenswerts kleiner und mittelgroßer Unternehmen.

Ihlau, S. and Duschau, H. (2019) Besonderheiten bei der Bewertung von KMU, 2nd ed. Wiesbaden: Springer Gabler.

Jonas, M. (2008) ‚Besonderheiten der Unternehmensbewertung bei kleinen und mittleren Unternehmen,‘ WPg (Sonderheft), 61, 117-122.

Kuznik, Th. (2016) Risk Management in a VUCA World: Practical Guidelines Based on the Example of a Multinational Retail Group, in: Mack, O. et al. (eds.) Managing in a VUCA World, Springer, 77-95.

Lahmann, A., Schreiter, M., Schwetzler, B. (2018) ‚Der Einfluss von Insolvenz, Kapitalstruktur und Fremdkapitalfälligkeit auf den Unternehmenswert,‘ Schmalenbachs Zeitschrift für betriebswirtschaftliche Forschung: ZfbF, 70 (1/2), 1-51.

Lintner, J. (1965) ‘The Valuation of Risky Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets,’ Review of Economics and Statistics, 47, 13-37.

Marcello, R. and Pozolli, M. (2019) ‘Critical issues when valuing small businesses,’ Business Valuation OIV Journal, 1 (1), 47-56.

Markowitz, H. M. (1952) ‘Portfolio selection,’ Journal of Finance, 7 (1), 77-91.

Matschke, M. J. and Brösel, G. (2021) Business Valuation, UVK Verlag: Munich.

Mossin, J. (1966) ‘Equilibrium in a Capital Asset Market,’ Econometrica, 34, 768-783.

Pratt, S. and R. Grabowsi, (2014) Cost of capital: Applications and examples, 5th Edition, Hoboken: Wiley.

Romeike, F. (2019) Neufassung des IDW Prüfungsstandards 340 (PS 340) – Risikoaggregation wird zur Pflicht, Besonderheiten der Unternehmensbewertung bei kleinen und mittleren Unternehmen Besonderheiten der Unternehmensbewertung bei kleinen und mittleren Unternehmen [Online], [Retrieved April 04, 2005], https://www.risknet.de/themen/risknews/risikoaggregation-wird-zur-pflicht/

Rossi, M. (2016) ‘The capital asset pricing model: a critical literature review,’ Global Business and Economics Review, 5, 604-617.

Saha, A. and Malkiel, B. G. (2012) ‘DCF Valuation with Cash Flow Cessation Risk,’ Journal of Applied Finance, 22 (1), 175-185.

Sharpe, W. F. (1964) ‘Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk, Journal of Finance, 19, 425-442.