1Alexandre SILVA, 1Sofia CARDIM and 2Joaquim LEITE

1Instituto Politécnico de Bragança (IPB), Bragança, Portugal

2UNIAG, Instituto Politécnico de Bragança (IPB), Bragança, Portugal

Volume 2025,

Article ID 372518,

Journal of Organizational Management Studies,

12 pages,

DOI: 10.5171/2025.372518

Received date: 23 June 2025; Accepted date: 30 July 2025; Published date: 30 September 2025

Academic Editor: Pedro Neves Rito

Cite this Article as:

Alexandre SILVA, Sofia CARDIM and Joaquim LEITE (2025)," A Portuguese Case Study on Performance Monitoring in Technology Transfer and Valorisation Centres Using the Balanced Scorecard Approach”, The Journal of Organizational Management Studies, Vol. 2025 (2025), Article ID 372518, https://doi.org/10.5171/2025.372518

Aligning strategic, operational, and technical priorities is critical for effective governance in Research and Development (R&D) organisations, especially those engaged in technology transfer and innovation. This article explores the development and application of the Balanced Scorecard (BSC) as a structured performance monitoring tool for a Portuguese Centre for the Valorisation and Transfer of Water Technology. Situated within the national network of technological interface centres, the research investigates how the BSC, supplemented by a strategic map, can support integrated management control by aligning organisational efforts with strategic goals. The study employs a qualitative case study methodology, with empirical data collected through three semi-structured interviews involving the centre’s CEO and two mid-level managers. The content analysis of interview transcripts enabled the identification of fourteen strategic objectives and their respective indicators, which were systematically mapped across the BSC’s four perspectives and interlinked through causal relationships. The results underscore the BSC’s potential to improve internal strategic coherence and monitoring capacity and to attend as a transferable framework for other public or private research centres facing similar challenges. The study offers both practical comprehensions for institutional management and conceptual contributions to the literature on performance management in the context of science, technology, and innovation.

Keywords: Management control, Balanced Scorecard (BSC), Water technology, Technology development and transfer centres.

Introduction

The structure of this study is organised into five sections. The first presents an introduction that theoretically frames the valorisation and transfer of water technology, management control and the BSC to support the research objective. The second section describes the methodology used. The following section presents the results, which include fourteen strategic objectives, organised by the four perspectives of the BSC, and the corresponding performance indicators. These strategic objectives were sequenced in a strategy map. The final two sections summarise a theoretical discussion and the conclusions.

Like other organisations, technology and science-based entities face the challenge of using management practices that link the institutional mission with measurable results. Strategic management control tools such as the Balanced Scorecard (BSC) have been gaining relevance in sectors for which they were not initially designed, such as non-profit organisations and research and development centres (Kaplan and Norton, 2001; Treinta et al., 2020). The Water Technology Development and Transfer Centre (WTDTC, fictitious name for confidentiality reasons) is a prime example of this type of organisation. The WTDTC, based in Portugal, is active in the water sector and its mission is to enhance scientific knowledge, transfer technology and provide specialised services. Promoting knowledge about water in different areas (human consumption, natural fresh water, natural spring and thermal mineral water, process water and swimming pool water) is the remit of this type of centre. The WTDTC’s organisational structure is marked by a hybrid nature, combining the characteristics of a public and private entity, a scientific mission and regional operations. These conditions make the organisation’s strategic management, defining priorities and monitoring results, exceptionally complex. This methodologically justifies using the case study method in a qualitative research paradigm (Otley et al., 2023).

Technology centres emerged in Portugal in the 1980s with the publication of Decree-Law no. 461/83 (1983) to support industrial development, to introduce innovation to markets, optimise natural resources and bring together public and private entities for technological advancement. Later, changes were made to the design and management philosophy of technology centres through Decree-Law no. 249/86 (1986), allowing these centres to be appropriately integrated into the national scientific research and technological development system. These changes were necessary to meet the requirements of Portugal’s accession to the then European Economic Community (EEC). However, there was a need to adjust the technology centres to the reality that was emerging, and, to simplify procedures, Decree-Law 312/95 (1995) was published, which imposed a reduction in public intervention in the management of these centres.

Technology interface centres play a strategic role in exploring new areas and adopting new emerging technologies, namely in the circular economy, energy efficiency and industry 4.0, contributing to the transformation and modernisation of the industrial sector (Recovery and Resilience Plan, 2021). With the publication of Order No. 8563/2019 (2019), the Ministry of Economy established the regulation that defines the process for recognising technology interface centres, reinforcing their importance in Portugal’s innovation ecosystem. Order No. 10252/2017 (2017) established the definition of technology development and transfer centres, which recognised 28 interface centres as infrastructures of the Portuguese research and innovation system. These centres promote technology transfer and innovation in companies through certification, production improvement, innovation support and training. The legal framework for the recognition, formalisation and operation of technology interface centres came about in 2019 with the publication of Decree-Law 63/2019 (2019), which introduced public policies to encourage innovation and technology transfer.

An integrated scientific approach is fundamental to ensuring water availability for future generations (Dias and Matos, 2023). In the face of climate change and increasing pressure from human activities, sustainable water management has become one of the most significant contemporary challenges. The implementation of innovative policies, the integration of modern technologies and the adoption of participatory practices are key to avoiding waste and preserving this resource.

The use of information, communication and electronic technologies, the Internet of Things (IoT), data science, among others, will enable the digital transformation process of the water sector to be energised, enhancing the value of both water and the entities involved (Mamede et al., 2023). Technology can boost the water sector’s digital transformation process, improving the value of both the water and the organisations involved, resulting in an industry that is stronger, more capable and closer to communities. The quality of accounting information systems positively influences organisational performance, an effect amplified by the dynamic analytical capabilities inherent in accounting (Varma et al., 2025). Furthermore, there is a significant relationship between these analytical capabilities and management control systems, which are central in guiding and improving organisational performance.

Management control is defined as a process by which managers influence members of the organisation to implement outlined strategies, ensuring that resources are obtained and used efficiently to achieve organisational objectives (Anthony and Govindarajan, 2007). Management control includes processes, tools and practices organisations use to achieve strategic and operational goals (Ferrolho, 2024). It also involves monitoring, evaluating, and adjusting activities and resources to achieve the desired results, going through the main elements that management control entails. These elements are planning, evaluation, monitoring and decision-making.

The BSC is an effective tool for aligning operational execution with the organisation’s strategic vision, allowing objectives to be monitored in multiple dimensions, including the financial one (Kaplan and Norton, 2004). This tool makes it possible to integrate innovation initiatives, stakeholder relations, and improved internal efficiency, critical factors in sustainably generating value. In addition, strengthening the capacity of applied research centres to provide specialised services is a fundamental vector for their economic viability and territorial impact (Silva and Costa, 2021). The use of the BSC in this framework contributes to results-oriented strategic management, with indicators that promote continuous performance and institutional autonomy.

The systemic approach promoted by the BSC makes it possible to guarantee strategic and operational coherence, reinforcing long-term viability (Kaplan and Norton, 2004). Adopting strategic control models such as the BSC can promote the integration of mission and results, provided it is adapted to the organisational context (Kumar et al., 2024). A BSC model that aligns a strategy between innovation and environmental responsibility (eco-innovation) can help companies reduce ecological impacts and promote sustainability, without compromising economic and financial growth (Guerra, 2023). Risk management and operating costs, product management and recycling strategies and greenhouse gas emissions are examples of environmental factors that are relevant for management control purposes (Wang et al., 2022).

The combined BSC and Enterprise Risk Management (ERM) can function as a hierarchical control infrastructure. The BSC acts as the visible predominant practice, while ERM seeks recognition. Despite this asymmetry, it is possible that ERM significantly influences the BSC itself, challenging the view that subsidiary practices merely follow guidelines imposed by a predominant practice (Huber et al., 2025). The potential offered by the BSC is not perceived equally enthusiastically by all those involved, and there may be differences between the point of view of its promoters and that of other employees (Gooneratne and Hoque, 2021). In other words, those responsible for promoting the BSC face challenges when trying to align the diverse interests and perceptions of the employees involved in its practical application in specific contexts.

Based on this theoretical framework, the following research question was posed: How can a BSC proposal be drawn up, complemented by a strategy map, for a research centre that promotes water technology transfer? This question arises from the need to use a tool to formalise strategic objectives, clarify priorities, define performance indicators and support decision-making.

Methodology

A qualitative approach was supported by the single case study method, as it is a particularised study in a single organisation, allowing for a detailed analysis of its particularities (Yin, 2017). The case study was the Water Technology Development and Transfer Centre (WTDTC), a technology interface centre. It is an entity dedicated to research and development, with an organisational structure characteristic of a private non-profit institution. The centre’s activities include those described below: (i) identifying and analysing business needs; (ii) boosting research and development activities for new technologies, processes and products; (iii) strengthening qualified employment and scientific employment; (iv) institutional collaboration between scientific organisations; (v) organising specialised technical and technological training; and (vi) cooperation with similar national and foreign institutions.

The following research question was formulated as a guide to this study: How can a BSC proposal be drawn up, complemented by a strategic map, for a research centre promoting water technology transfer? This question aims to meet the following objectives: (i) identify strategic objectives, (ii) define performance indicators to monitor each objective, and (iii) organise the objectives into a strategic map of cause/effect correlations.

Data were collected through semi-structured interviews. These interviews were conducted in the 2nd quarter of 2025 with the top executive director and two middle managers responsible for decisions. This technique is flexible in qualitative research, allowing free exploration of themes while ensuring consistency between interviews (Bryman, 2016; Otley et al., 2023). Interviews provide a privileged insight into the internal dynamics of organisations, making it possible to collect accurate and authentic data (Bowen, 2009; Yin, 2017).

Results

This section of the results begins by summarising the activities of the WTDTC case. This technology interface centre is subject to the supervision of the National Innovation Agency and the Foundation for Science and Technology (2023), which monitor the implementation of projects funded in research, development and innovation. In addition, the centre is bound by the sectoral legislation applicable to laboratory activity, scientific research, and the provision of technical services, namely accreditation, safety, and good laboratory practices. The diversification of clients and the increase in the number of analyses carried out are signs of the potential for expansion in this activity area. However, maintaining modest net results and dependence on public financial support reinforce the need to implement results-oriented strategic management.

In 2019, the centre’s net profit was negative, reflecting the initial phase of the organisation, with a reduced structure and still no income from providing services. However, since 2020, the centre has shown positive and growing net results. This growth is sustained above all by the significant increase in operating subsidies and the provision of services, which went from zero in 2019 to over €60,000 in 2023. As a result, the return on equity (ROE), which was negative in 2019, evolved positively until it reached more than 3% in 2023. This shows an organisation on a growth trend, with a funding base that is still heavily dependent on subsidies, but with positive signs of an increase in its activity. These characteristics justify and contextualise the BSC proposal as a tool for strategic planning and monitoring organisational performance, integrating the financial and non-financial perspectives.

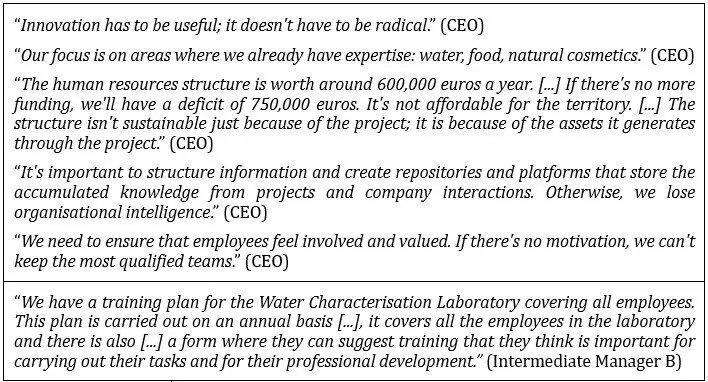

The data (text excerpts) relating to the financial, customer, internal processes and learning and growth perspectives are shown in Tables 1, 2, 3 and 4, respectively, indicating the role of the interviewees.

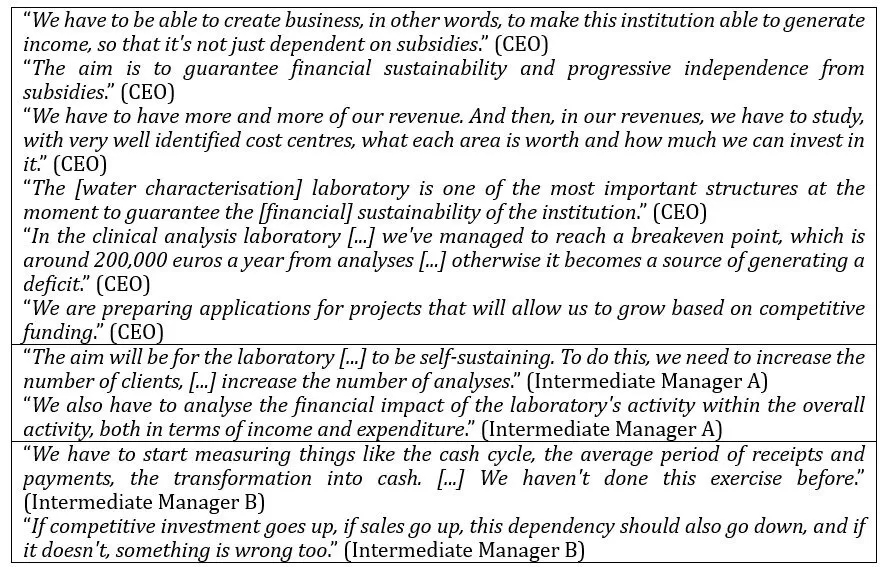

Table 1: Excerpts from the interviews that support the objectives: financial perspective

Source: Authors’ own elaboration

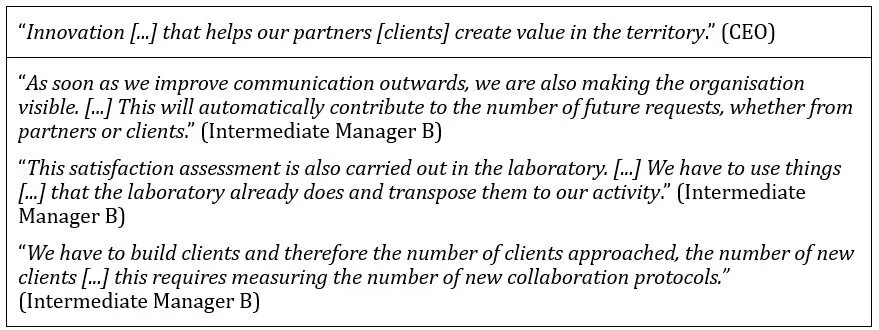

Table 2: Excerpts from the interviews that support the objectives: customer perspective

Source: Authors’ own elaboration

Table 3: Excerpts from the interviews that support the objectives: internal processes perspective

Source: Authors’ own elaboration

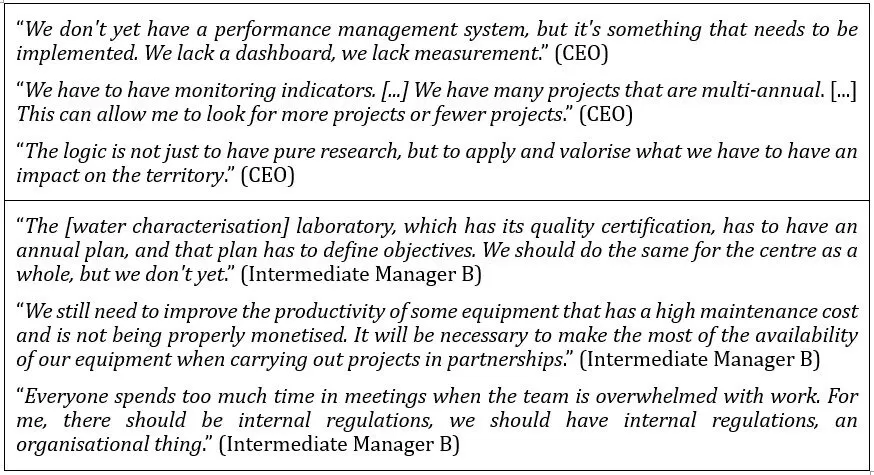

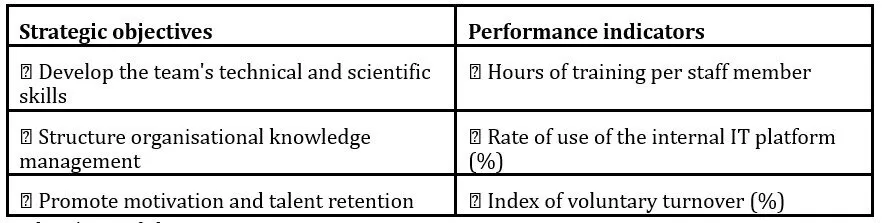

Table 4: Excerpts from the interviews that support the objectives: learning and growth perspective

Source: Authors’ own elaboration

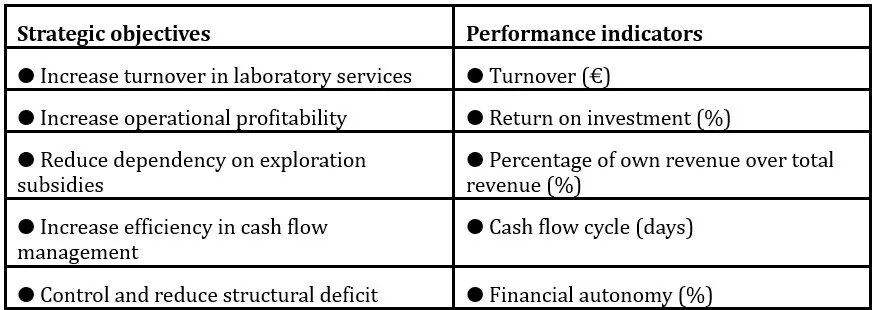

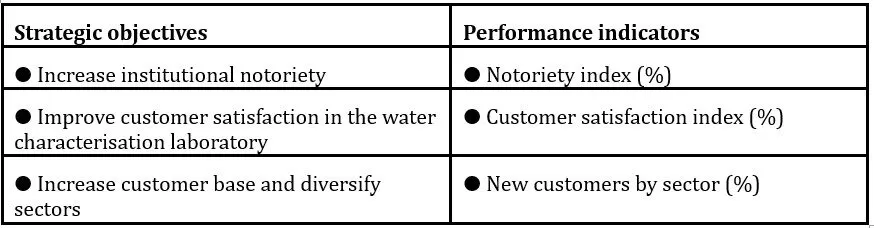

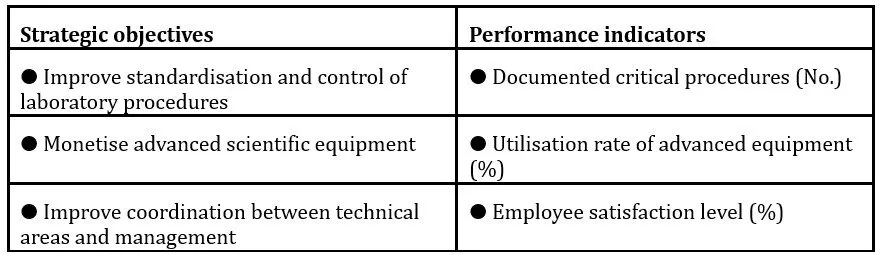

The data presented in the four tables above allowed to identify the corresponding strategic objectives, associating them with management indicators (measures) and also organising them into the four perspectives of the BSC (see Tables 5, 6, 7 and 8).

Table 5: WTDTC objectives and indicators: financial perspective

Source: Authors’ own elaboration

Table 6: WTDTC objectives and indicators: customer perspective

Source: Authors’ own elaboration

Table 7: WTDTC objectives and indicators: internal process perspective

Source: Authors’ own elaboration

Table 8: WTDTC objectives and indicators: learning and growth perspective

Source: Authors’ own elaboration

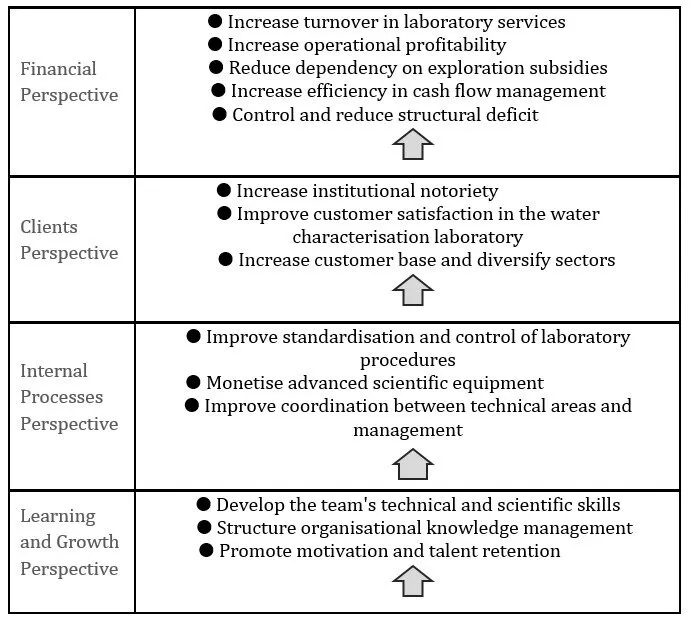

The four Tables above define an indicator (performance measure) capable of monitoring each strategic objective within the BSC model, organised according to the four classic perspectives of this management tool: financial, customers, internal processes and learning and growth. To better visualise the cause-effect relationships between the economic and non-financial strategic objectives, according to the BSC perspectives, a strategic map was drawn for the technology interface centre under study (see Figure 1)

Figure 1: WTDTC strategy map in BSC perspectives

Source: Authors’ own elaboration

The primary purpose of the strategic map shown in Figure 1 is to clarify the logical link between the strategic objectives and the four perspectives, making it possible to see how the results of each BSC perspective are reflected at higher levels. In this specific case, given the dependence of objectives within the same perspective, it was considered that the various objectives interact with each other, and it is sufficient to present the cause-effect relationship between all the strategic goals of each perspective and not between each objective individually. This way, the map communicates the strategy coherently and execution-oriented, aligning efforts and resources around a common purpose.

The perspective of learning and growth is the basis of organisational training. Developing the team’s technical and scientific skills promotes the enhancement and specialisation of human resources, an essential factor in guaranteeing the quality of services. At the same time, structuring organisational knowledge management ensures the retention of technical knowledge and internal dissemination, boosting synergies and innovation. These two objectives, combined to promote motivation and retain talent, strengthen the organisation’s human and cultural base, creating the necessary conditions for practical innovation, learning and growth processes.

The achievement of learning and growth objectives directly influences the internal processes perspective. The increased qualification and motivation of the team means that the standardisation and control of laboratory procedures can be improved, guaranteeing consistency and technical rigour. At the same time, accumulated knowledge and installed capacity make it possible to make the most of cutting-edge scientific equipment, exploiting the institution’s full technological potential. In turn, the coordination between technical and administrative areas, reflected in the objective of improving coordination between technical and administrative areas, helps to reduce inefficiencies and speed up the organisational response.

The performance of internal processes can strengthen the organisation’s ability to create value for its stakeholders, impacting the objectives of the customer perspective. Recognition of good practices and technical excellence helps increase institutional awareness, essential for strengthening the organisation’s position in the scientific and business ecosystem. A more effective and personalised service offering can enhance the satisfaction of the water characterisation laboratory’s customers, promoting customer and partner loyalty. The growing reputation and perceived quality make increasing the client base and diversifying sectors easier, allowing the technological interface centre to expand its activities.

Finally, achieving the objectives relating to clients directly supports the goals of the financial perspective, materialising the organisation’s strategy. Greater demand from and loyalty to clients make it possible to increase the provision of laboratory services, which in turn contributes to improving operating profitability. The growing generation of its revenue makes it possible to reduce dependence on operating subsidies, promoting greater operational financial independence from external funding sources. At the same time, efficiency and planning gains support increased efficiency in treasury management, budgetary control and the structural deficit reduction. Therefore, this linking of causes and effects between strategic objectives confirms that the strategy aimed at economic and financial results depends not on an isolated factor, but on the alignment between people, processes and the market.

Discussions

This research has made it possible to carry out an in-depth analysis of the organization’s internal constraints, making it possible to outline a strategic model that is coherent with its institutional mission and specific framework. The use of the BSC as a strategic management tool enables coherent integration between strategic and operational objectives (Kaplan and Norton, 2004). This alignment capacity becomes even more relevant when, by being adjusted to the specific context of the organization, the BSC can serve as a link between the institutional mission and the results achieved (Kumar et al., 2024). In hybrid organizational structures, which simultaneously incorporate characteristics of public and private entities, as well as a scientific vocation combined with regionally-based intervention, additional challenges arise in formulating strategy, defining priorities and monitoring results. From a methodological point of view, these specificities support the choice of a case study as an appropriate research strategy within a qualitative paradigm (Otley et al., 2023).

The results show that operational tools have been designed to support decision-making by integrating financial and non-financial data (Kaplan and Norton, 2004). Faced with a research activity on the valorization and transfer of water technology, the proposed BSC allows for a strategic alignment between innovation and environmental responsibility – or eco-innovation – underpinning measures to reduce environmental impacts that simultaneously promote sustainability and economic and financial growth (Guerra, 2023). In this context, environmental factors such as risk management and operating costs, the life cycle of products, recycling strategies and the control of greenhouse gas emissions are particularly relevant for management control purposes (Wang et al., 2022). The application of the BSC challenges the traditional view that subsidiary practices are limited to replicating guidelines imposed by dominant models, proving adaptable to different organizational realities (Huber et al., 2025). However, the potential of the BSC is not universally recognized among all members of the organization, and there are often differences between the perspective of its promoters and that of other employees (Gooneratne and Hoque, 2021).

The construction of a BSC allows for the definition of key strategic objectives, duly distributed across the original model’s four perspectives and accompanied by the respective performance indicators (Kaplan and Norton, 2004). This fits in with the concept of management control, understood as a process by which managers guide the members of the organization to achieve the strategies outlined, ensuring efficient use of resources (Anthony and Govindarajan, 2007). In this sense, management control involves an articulated set of processes, tools and practices aimed at guaranteeing the effective execution of strategic and operational objectives (Ferrolho, 2024), and is essential for transforming the BSC’s objectives into measurable results.

Conclusions

This study aimed to propose a BSC, including a strategy map, adapted to the reality of a non-profit organisation with a scientific and technological mission. The research enabled an in-depth understanding of the organisation’s internal challenges, designing a strategic model consistent with its mission and context, and developing practical tools to support management based on financial and non-financial information. Using a qualitative approach based on data collected through semi-structured interviews, it was possible to map out the organisation’s needs and priorities.

The construction of the BSC made it possible to formalise 14 strategic objectives, distributed across the model’s four perspectives, and their respective performance indicators. The potential contributions of this study include adapting the BSC to the context of a technology interface centre, introducing a culture of planning and management control and strengthening institutional alignment around a clear strategic vision.

The study has some limitations, namely the lack of structured historical data in certain areas and the fact that they have not yet been implemented in practice. The study of a single case, using a single source of data, and a single strategic planning and management instrument can also be considered a limitation of this study. Consequently, as suggestions for future research, several directions can be identified. Firstly, the practical implementation of the proposed BSC and strategy map will be investigated to identify barriers, limitations, skills, and digital media for recording and sharing information, focusing on systematising operational and performance data. Secondly, it would also be pertinent to compare actual and planned targets, identify possible initiatives, and extend the use of the BSC to other areas and projects at the technology interface centre to understand the potential of integrated management. Finally, research multiple cases, triangulate data, use strategic management tools other than the BSC and use alternative research methodologies, namely the quantitative research paradigm.

References

Anthony, R. N. and Govindarajan, V. (2007), ‘Management control systems, 12th, McGraw-Hill.

Bowen, G. A. (2009), ‘Document analysis as a qualitative research method,’ Qualitative Research Journal, 9 (2), 27– https://doi.org/10.3316/QRJ0902027

Bryman, A. (2016), ‘Social Research methods,’ Oxford University Press.

Decreto-Lei n.º 461/83, Diário da República (Portugal), 300 (I Série), 4164(11) –4164(15) (30 de dezembro de 1983). https://files.diariodarepublica.pt/1s/1983/12/30001/00110015.pdf

Decreto-Lei n.º 249/86, Diário da República (Portugal), 194 (I Série), 2156–2162 (25 de agosto de 1986). https://files.diariodarepublica.pt/1s/1986/08/19400/21562162.pdf

Decreto-Lei n.º 312/95, Diário da República (Portugal), 272 (I Série-A), 7270–7273 (24 de novembro de 1995). https://files.diariodarepublica.pt /1s/1995/11/272a00/72707273.pdf

Despacho n.º 10252/2017, Diário da República (Portugal), 227 (II Série), 26597-26599 (24 de novembro de 2017). https://files.diariodarepublica.pt/2s/2017/11/227000000/2659726599.pdf

Despacho n.º 8563/2019, Diário da República (Portugal), 186 (II Série – Parte C), 56–61 (27 de setembro de 2019). https://files.diariodarepublica.pt/2s/2019/09/186000000/0005600061.pdf

Decreto-Lei n.º 63/2019, Diário da República (Portugal), 94 (I Série), 2466–2475 (16 de maio de 2019). https://files.diariodarepublica.pt/1s/1995/11/272a00/72707273.pdf

Dias, R. and Matos, F. (2023), ‘Impactos das mudanças climáticas nos recursos hídricos: Desafios e implicações para a humanidade),’ Revista Sociedade Científica, 6(1), 1571–1603. https://doi.org/10.61411/rsc100003

Ferrolho, J. C. (2024), ‘Planeamento e Controlo de Gestão: Uma visão estratégica empresarial,’ 1.ª ed., Rei dos Livros.

Fundação para a Ciência e a Tecnologia. (2023), ‘Normas de execução de projetos I&D,’ https://www.fct.pt

Gooneratne, T. N. and Hoque, Z. (2021), ‘The fate of the balanced scorecard: Alternative problematization and competing networks,’ Qualitative Research in Accounting and Management, 18(2), 255–281. https://doi.org/10.1108/QRAM-03-2020-0028

Guerra, J. B., Schneider, J., Lima, M. A., Peixoto, M. G., Barbosa, S. B., Neiva, S.S., Birch, R., Jesus, M. A., Junges, I. and Dutra, A. R. (2023), ‘Balanced scorecard e eco-inovação no setor industrial: Um mapa estratégico para a inovação ambiental,’ Business Strategy and the Environment, 32, 4266–4281. https://doi.org/10.1002/bse.3364

Huber, C., Kraus, K. and Meidell, A. (2025), ‘Integrating the balanced scorecard and enterprise risk management: Exploring the dynamics between management control anchor practices and subsidiary practices,’ Management Accounting Research, 66, 100924. https://doi.org/10.1016/j.mar.2024.100924

Kaplan, R. S. and Norton, D. P. (2001), ‘The strategy-focused organisation: How balanced scorecard companies thrive in the new business environment,’ Harvard Business School Press.

Kaplan, R. S. and Norton, D. P. (2004). Strategy maps: Converting intangible assets into tangible outcomes. Harvard Business Press.

Kumar, S., Lim, W. M., Sureka, R., Nguyen, N. P. and Kumar, N. (2024), ‘Balanced scorecard: Trends, developments, and future directions,’ Review of Managerial Science, 18(8), 2397–2439. https://doi.org/10.1007/s11846-023-00700-6

Mamede, H., Neves, J. C., Martins, J., Gonçalves, R. and Branco, F. (2023), ‘A prototype for an intelligent water management system for household use,’ Sensores, 23(9), 4493. https://doi.org/10.3390/s23094493

Ministério das Finanças. (2023), ‘Portal das Finanças: Legislação fiscal e contributiva,’ https://www.portaldasfinancas.gov.pt

Otley, D., Peda, P. and Pfister, J. A. (2023), ‘A methodological framework for theoretical explanation in performance management and management control systems research,’ Qualitative Research in Accounting & Management, 20(2), 201– https://doi.org/10.1108/QRAM-10-2021-0193

Programa de Recuperação e Resiliência. (22 de abril, 2021). PRR. https://recuperarportugal.gov.pt/wp-content/uploads/2024/04/PRR.pdf

Silva, M. and Costa, R. (2021), ‘Sustentabilidade financeira em instituições de ciência e tecnologia: Contributos da prestação de serviços especializados,’ Revista Portuguesa de Gestão e Inovação, 5(2), 33–48.

Treinta, F., Moura, L., Cestari, J. M., Lima, E., Deschamps, F., Costa, S. and Leite, L. (2020), ‘Design and implementation factors for performance measurement in non-profit organizations: A literature review,’ Frontiers in Psychology, 11, 1799. https://doi.org/10.3389/fpsyg.2020.01799

Varma, A., Sharma, A. and Khan, A. (2025), ‘Accounting-analytic capabilities’ impact on management controls and performance,’ Journal of computer information systems, 1–16. https://doi.org/10.1080/08874417.2024.2441770

Yin, (2017), ‘Case study research: Design and methods,’ 7th ed., Sage Publications.

Wang, J.-S., Liu, C.-H. and Chen, Y.-T. (2022), ‘Green sustainability balanced scorecard: Evidence from the Taiwan liquefied natural gas industry,’ Environmental Technology & Innovation, 28, 102862. https://doi.org/10.1016/j.eti.2022.102862