Introduction and Literature Review

Given the importance of money in the course of any type of company is required to provide information about past movements of cash and cash equivalents of an entity by means of the cash flow statement. Information about the financial position, performance and changes in the financial position of the enterprise is useful to a wide range of users in making economic decisions. Users of financial statements include the present potential investors, employees, creditors, suppliers and other trade creditors. All are interested in the company’s statement regarding the company’s capacity to meet its obligations to pay cash and evaluation for future cash flows (cash – flow strategic), and cash flow analysis exposes its usefulness in this situation. In this article, we want to study the degree of harmonization of national regulations (OMFP 3055/2009) with international regulations (IAS 7) regarding cash flow policies. The results obtained contribute to the development of a set of globally accepted accounting standards and the development of the process of globalization of accounting. We studied the literature in the field and the topic of harmonisation and convergence is not a new one, but we did not identify studies regarding the degree of hamonisation between national and international regulations regarding cash flows.

Harmonisation has been defined by Samuels and Piper (1985) as “the attempt to bring together different systems. It is the process of blending and combining various practices into an orderly structure, which produces a synergistic result”. Why is harmonization important? Shil et al (2009) say that “this “harmonization” of accounting standards will help the world economy in the following ways: by facilitating international transactions and minimizing exchange costs by providing increasingly “perfect” information; by standardizing information to world-wide economic policy-makers; by improving financial markets’ information; and by improving government accountability”. Wang’s (2011) article investigates whether harmonization of accounting standards increases comparability between countries, using a difference-in-differences design for the introduction of International Financial Reporting Standards. His research shows that harmonization increases comparability, facilitating the international transfer of information.

Research Design and Methodology

In conducting this study, the researcher has proposed a conceptual and practical approach to harmonisation of standards, focusing on studies that emphasize the degree of similiude between national regulations and international standards, focusing on the level of harmonisation at a state level. The author aims to answer the question whether there is a convergence process between national regulations and international ones, related to cash flows, and if for London Stock Exchange there is harmonisation of regulations in companies on the capital market from UK. We used both qualitative and quantitative reasearch approach. Using qualitative method, we analysed and synthetised the results of our study, consulting materials in order to develop the article. For the quantitave part of our scientific research, we used Jaccard coefficients developed in 2005, Herfindahl Indexes (H index and E(H) index) developed by Van Tas in 1988. The author assumed that the synthesis results of these studies are essential for a better understanding of the harmonisation and convergence process, and this can form the basis for best practice in the application of cash flows accounting policies.

Accounting regulations

The sets of accounting regulations studied for the development of this article are IAS 7 “Statement of Cash Flows” used internationally and the Order of the Ministry of Public Finance no. 3055/2009 for approval of accounting regulations harmonized with European Directives and International Accounting Standards. A necessary component of a complete set of financial statements under IFRS is the statement of cash flows (cash flow statements) prepared under IAS 7 as a standalone tool, with the same importance as balance sheet, income statement, statement of changes of equity and explanatory notes. The importance of this component of financial statements is so great that in order to normalize it, a separate standard dealing with this statement was promulgated, namely IAS7.

IAS 7 “Cash Flow Statements” was issued in December 1992 by the International Accounting Standards Committee (IASC), replacing IAS 7 Statement of Changes in Financial Position published in October 1977. Following the terminology changes made by IAS 1 “Presentation of Financial Statements” in September 2007, the IASB changed the title of IAS 7 “Cash Flow Statements-” (Cash Flow Statements-) in the “-Cash Flow Statement-” (-Statement of Cash Flows-). IAS 7 became operative for financial statements covering the period from 1 January 1994. Romania’s preparation for accession to the European Union imposed the necessity of harmonizing Romanian accounting and financial statements with those used in EU countries and internationally. This process of harmonization is done in stages and involves first a legal framework specifying the new accounting regulations and reporting financial statements, and secondly, gradual implementation of new legislation on various categories of economic agents to the widespread application of these rules throughout the economy.

In Romania, the cash flow statement is regulated by the Ministry of Finance Order no. 3055/2009 which has two components:

– Accounting regulations compliant with Directive IV of the European Economic Community. These regulations provide the design and content of annual financial statements, accounting principles and rules for recognition, measurement, presentation and removal of elements in the annual financial statements, the rules for drawing up, approval, audit / verification, according the law, and publishing of annual financial statements, some rules on management accounting, chart of accounts and the content and function of accounting accounts in role since 01.01.2010. In addition, these guidelines establish rules for the organization and management of accounting and reporting according to the requirements of state institutions, for the use of all users.

– Accounting regulations compliant with Directive VII of the European Economic Community. These regulations prescribe the form and content of the consolidated annual financial statements and the rules for drawing up, approval, auditing and publication of consolidated annual financial statements.

According to paragraph 7 of the Framework for the Preparation and Presentation of Financial Statements issued by IASB, a component of the complete set of financial statements is the cash flow statement with the balance sheet, income statement, statement of changes in equity and notes to financial statements. A complete definition of the cash flow statement is reflected under IAS 7, in the contents of which are specified more both theoretical and practical aspects related to this subject: “Cash flows are inflows and outflows of cash and cash equivalents. Cash comprises cash and cash equivalents and deposits. Cash equivalents are short-term financial investments, highly liquid, which are convertible into known amounts of cash and which are subject to an insignificant risk of changes in value.” Among the major objectives of the cash flow statement is the assessment of the entity’s ability to develop liquidity, evaluation of entity’s solvency, determining liquidity needs and not least the determination of maturity of payments and the risk of future receipts. Information on the cash flows of an entity is useful to users of financial statements, as a basis for assessing the ability of the entity to generate cash and cash equivalents and the needs to utilize those cash flows. Economic decisions of beneficiaries require an evaluation of a company’s ability to provide cash and cash equivalents and the timing and safety of their occurrence. Some of the benefits of the users of cash flow statement are:

• Users can assess the changes in the structure of the net assets of an entity and the entity’s ability to influence the amount and timing of cash flows’ occurrence;

• Information provided by the cash flow statement for determining whether an entity can generate cash and cash equivalents, thus increasing the comparability of reporting the operating performance of different companies;

• History of Cash Flows examines the relationship between profitability of an entity and net cash flow.

All entities need cash, however different are their principal revenue-producing activities because otherwise companies cannot carry on their normal and consistent work, can not pay the obligations at maturity and fail to provide a strong return for investors. Therefore, IAS 7 requires all entities to prepare, in addition to other components of the annual financial statements, the cash flow statement. In the practical part of this study, one of the topics analyzed in all the companies studied is the type of cash flows. According to the classifications, there are three types of cash flows that may result from an entity’s activity: cash flows from operating activities, cash flows from investing activities and cash flows related to financing activities. Each entity is free to classify the operations carried out on the three categories mentioned above, based on the way that best suits its business. Operating activities are the main revenue-generating activities and other activities excluding the investment and financing ones. Investment activities reveal those operations that relate to the acquisition and disposal of fixed assets and other investments not included in cash equivalents. Financing activities are activities that involve changes in the value and structure of equity and in the entity’s loans. Very important is the fact that cash flows exclude cash movements between items that constitute cash or cash equivalents because these components are part of the cash management of an entity rather than part of its operating, investing and financing activities.

The second topic examined in the practical part of our study refers to the modality to report cash flows. Both within IAS 7 and under OMPF 3055/2009 are mentioned two methods of reporting cash flows, namely the direct method and the indirect method. The direct method is used to present the main classes of gross cash receipts and payments, such as proceeds from the sale of goods and services, cash payments to suppliers for goods and services, employees, etc. Companies are encouraged to report cash flows from operating activities obtained using the direct method, since it provides useful information in forecasting future cash flows and which is not disponible under the indirect method. For the direct method, information about major classes of gross cash receipts and payments can be obtained in two ways:

• When applying a treasory accounting, the cash flows from operations are derived from the accounting records of the company, by comparing proceeds with the payments from operations;

• When applying accrual accounting, operations’ streams are obtained from the profit and loss account by adjusting operating income and expenses during the period with changes of inventories, receivables and payables (variation of operating working capital) and any claims and liabilities related to investing or financing activities (change in non-operating working capital).

The formula for calculating cash flows from operating activities as determined by the direct method with the application of accrual accounting is:

FNE = VEI – CEP – ΔNFRE

Where: FNE = operating cash flows;

VEI = operating income receivable;

CEP = paying operating expenses;

ΔNFRE = change in working capital need of service.

ΔNFRE = (Closing balance – Starting balance) component elements of ΔNFRE.

The indirect method involves determining the net cash flow from operating activities by adjusting net profit or net loss with effects of changes in inventories, receivables and payables during the period, with non-cash items such as depreciation, provisions, deferred taxes, unrealized gains and losses from foreign currency, undistributed profits of associates and minority interests, as well as all other items for which the cash effects are cash flows from investing activities or financing activities. The formula for calculating operating cash flows determined by the indirect method is:

FNE = RNC – VC- VIF + CC + CIF – ΔNFRE

Where: FNE = operating cash flows;

RNC = net result sheet;

VC = income calculated;

VIF = income from investing and financing activities;

CC = cost calculated;

CIF = cost of investing and financing activities;

ΔNFRE = change in working capital need of service.

Although IAS 7 recommended the direct method, especially to meet the informational needs of investors who can make a better forecast for future cash flows, most companies prefer using the indirect method because the calculation method is closer to the format and accounting reports “discret” character, in situations where the publication of required cash flow statement with the direct method would not benefit the image of the entity. The third and fourth topic studied for the entities are related to flows of received and paid dividends, which should be disclosed separately. These will be classified in a consistent manner from period to period, being generated by operating, investing or financing activities.

Capital Market from which the Companies were Chosen

Companies whose financial statements have been studied are listed on the London Stock Exchange. London Stock Exchange is one of the major exchanges in Europe in terms of market capitalization of listed companies and the financial heart at a global level with about 3000 companies from over 70 countries admitted to trading on its markets. London Stock Exchange (LSE) is one of the oldest stock exchanges in the world, dating back to 1773. The Stock Exchange is declared to be the most international as it comes permanently to meet its customers’ new products and services, maintaining a leading position in terms of liquidity for European stocks. In 2007, the London Stock Exchange merged with the Italian Stock Exchange creating the London Stock Exchange Group.

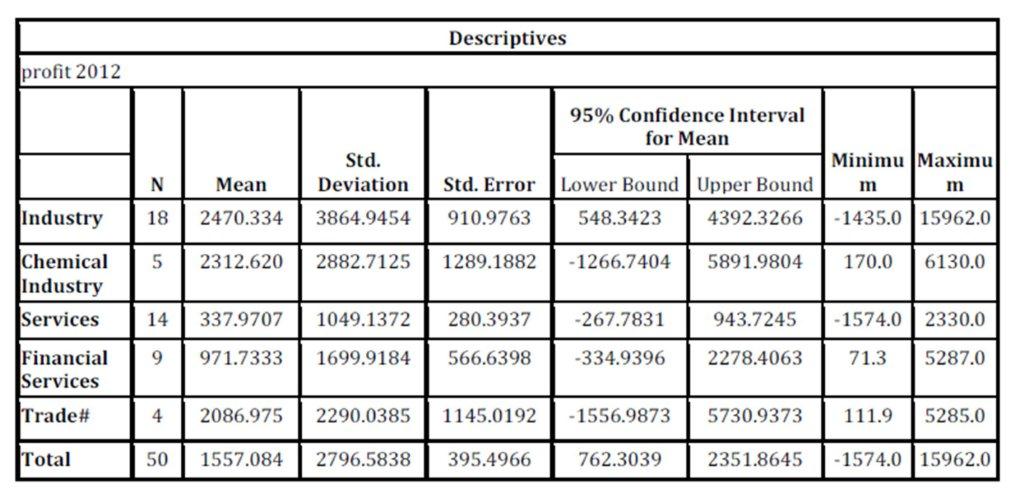

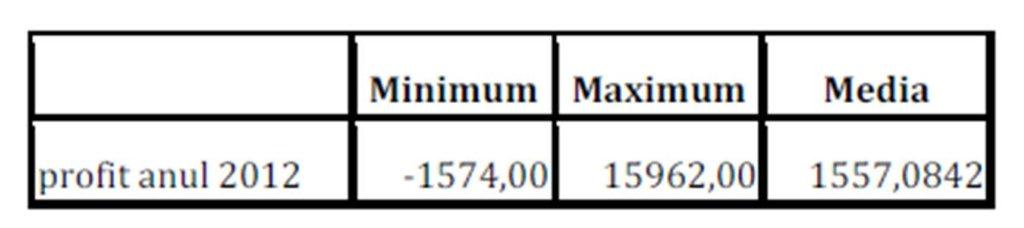

Table 1: Profit 2012 for the entities studied ( descriptive)

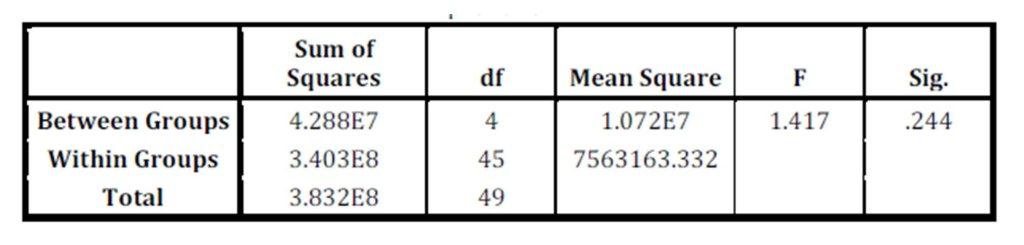

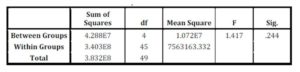

Table 2: Profit 2012 for the entities studies (ANOVA) profit 2012

The 50 companies were selected from the 100 entities belonging to the FTSE 100 index. This index is the index of 100 blue chip companies with the largest market capitalization on the London Stock Exchange, which have a total market capitalization amounting to 81% of the UK stock market. A blue chip is a label used for public companies considered the most robust, the most efficient and the most stable on the market. Usually blue chip companies sell products and services well known and widely accepted and have as the main feature positive financial performance also in difficult times, which helps to strengthen the reputation of strong company capable of development. Among the criteria taken into account in the appointment of blue chip companies include: capitalization, liquidity, performance, quality of ownership and management, market position and the work done. For example, on the capital market in Romania, Romanian Bank for Development companies and Petrom are considered blue chips.

The largest returns were recorded for the entities studied (fig.2) in the industry sector, followed by the commercial sector and the lowest profits in the services sector. In the third column of table 1, averages for each sector profits are calculated. In the ANOVA (table 2), we checked whether the activity has a significant influence on the profits made. To have a more comprehensive study on companies and the industry related, we analyzed the collected data using SPSS.

Entities covered in the project can be classified in relation to the field of activity:

• 8% commercial activity profile

• 36% activity profile in the industry

• 10% activity profile in chemical

• 28 % services

• 18% financial services.

Since the probability of being wrong when rejecting the null hypothesis is 0.244> 0.05 results that the null hypothesis is accepted, so the sector does not affect profit.

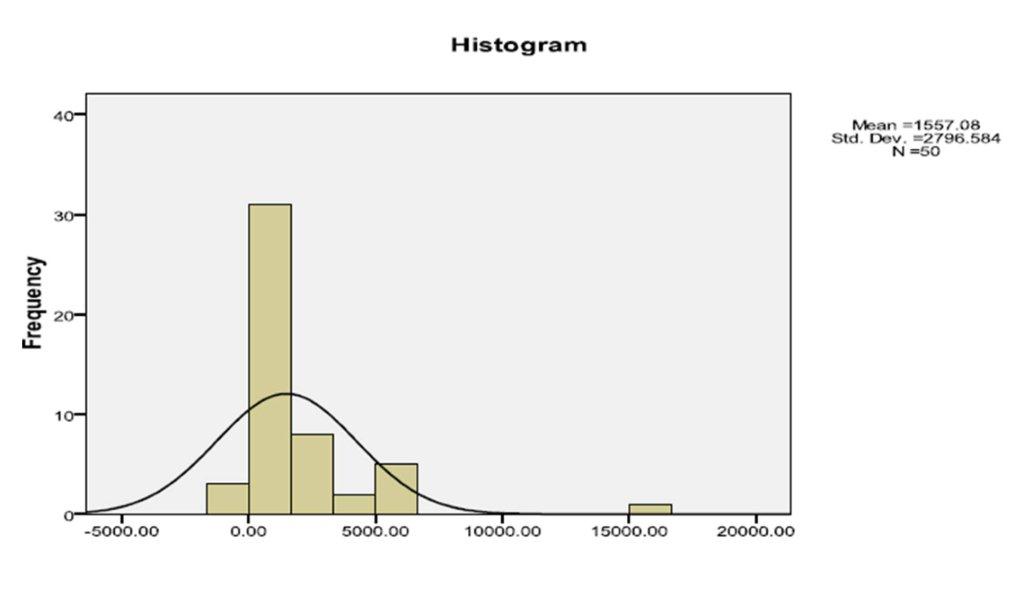

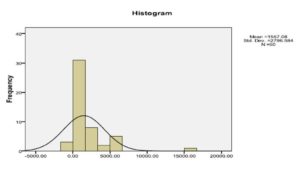

Figure 1: Entities studied – profit for 2012 Histogram

The distribution histogram allows the visualization of the variable, being used to determine whether the distribution is normal by comparing the histogram of the variable with the chart of Gauss curve. According to the chart (fig.1), we can see that the distribution of profit does not approach the normal distribution law.

Figure no : Reporting methods used for cash flows

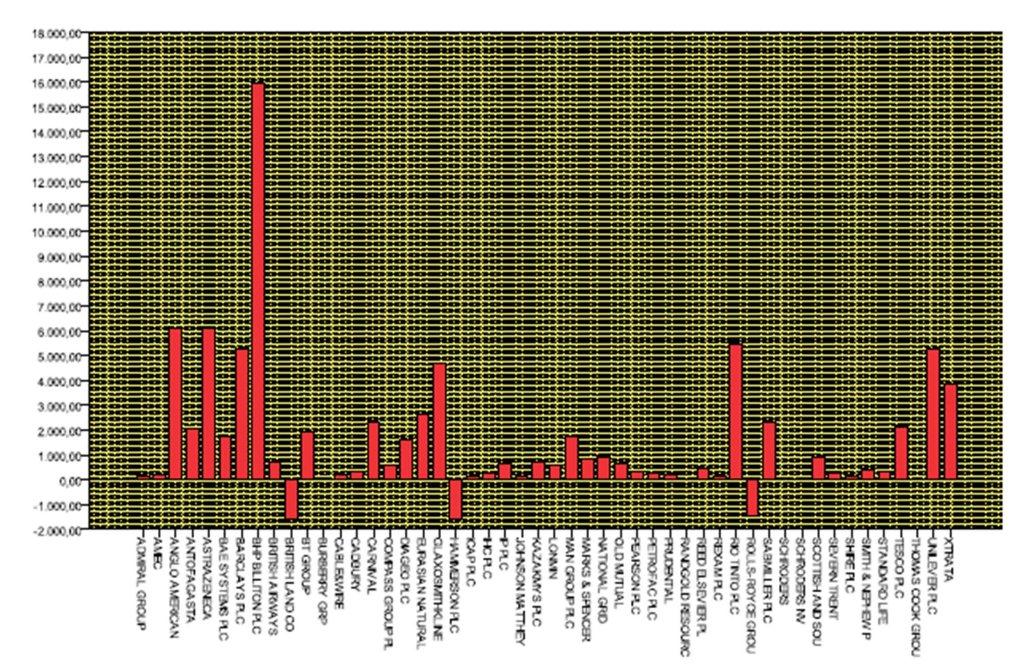

Figure 2: Entities studied – net profit for 2012

Table 3: Profit 2012 –minimum, maximum, media

As it can be seen, the minimum recorded was £ -1.574 billion by the entity Hammerson PLC and the maximum £ 15.962 billion registered by the entity BHP Billiton PLC.

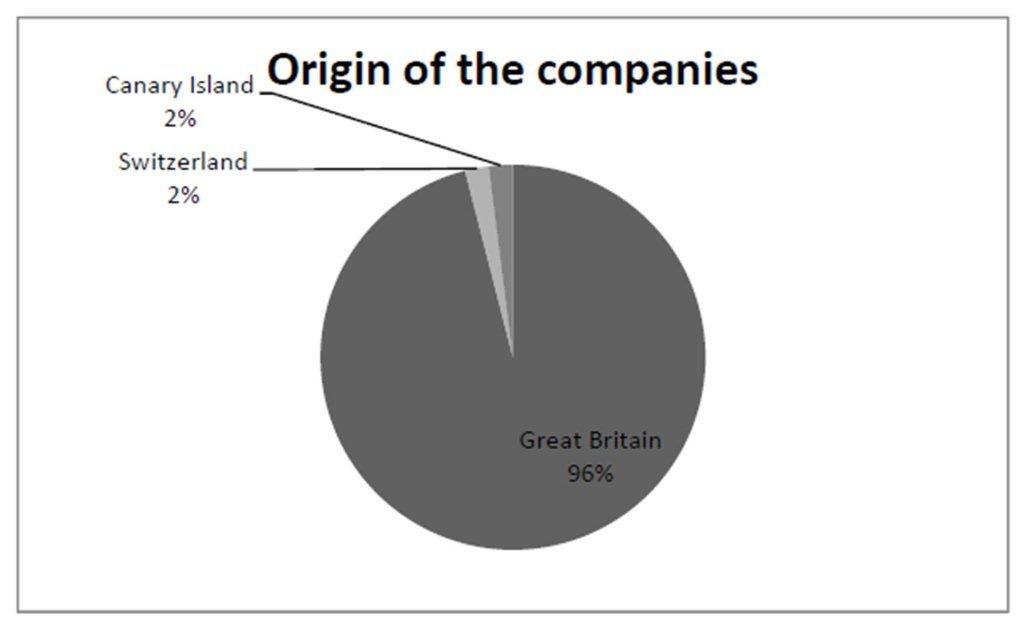

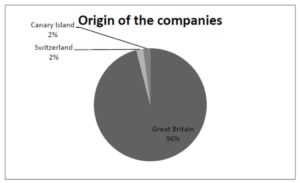

Figure 3 : Origin of the studied companies

Analysing the studied companies (fig.3), we observe that 96% of companies listed on the London Stock Exchange come from Britain and 4% are from outside Switzerland or the Canary Islands.

Results and Discussions

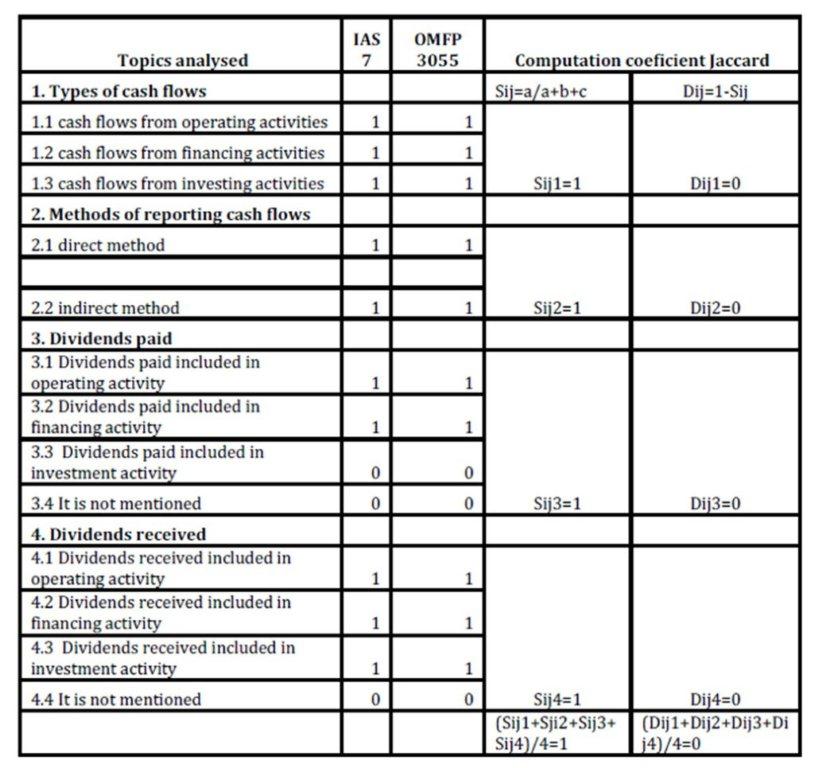

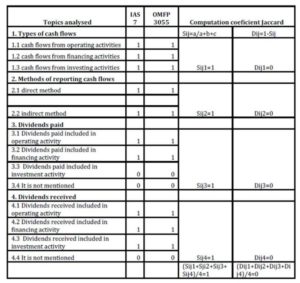

Jaccard Coefficients

Fontes A. Rodriguez uses for the first time Jaccard coefficients as a tool to measure the degree of formal harmonization in his book Measuring Convergence of National Accounting Standards with International Financial Reporting Standards in 2005. Jaccard coefficients measure the changes in the degree of harmonization of the Romanian national accounting (OMFP 3055) and International Accounting Standards (IAS / IFRS).

Table 4 : Degree of convergence between Romanian and International referentials

As resulted from our calculations, there is a maximum degree of similarity between the two regulations.

H Index

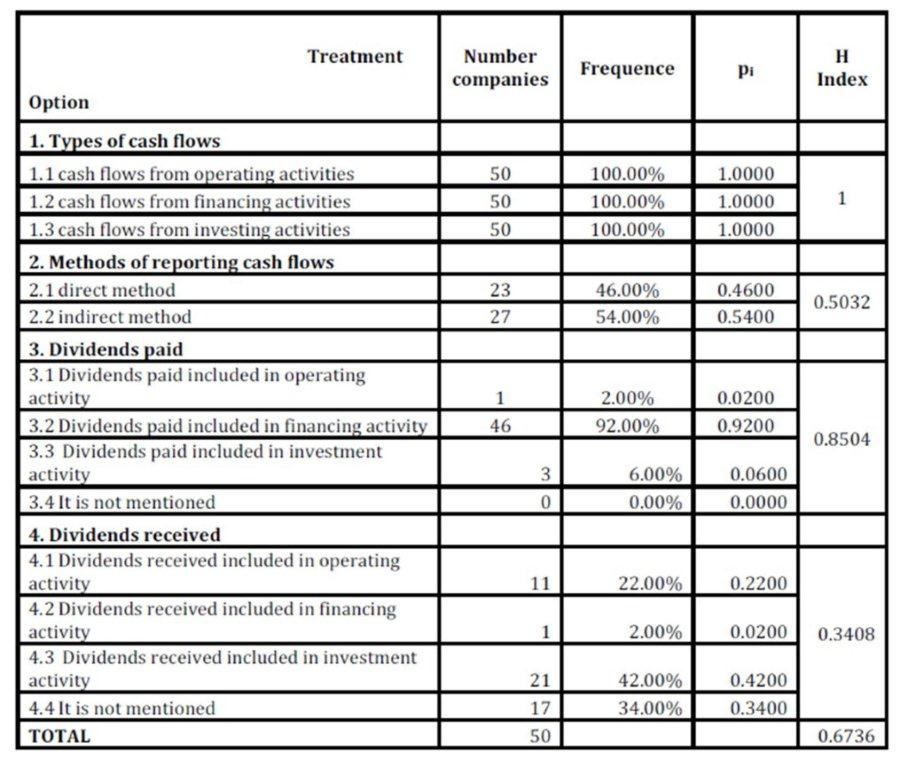

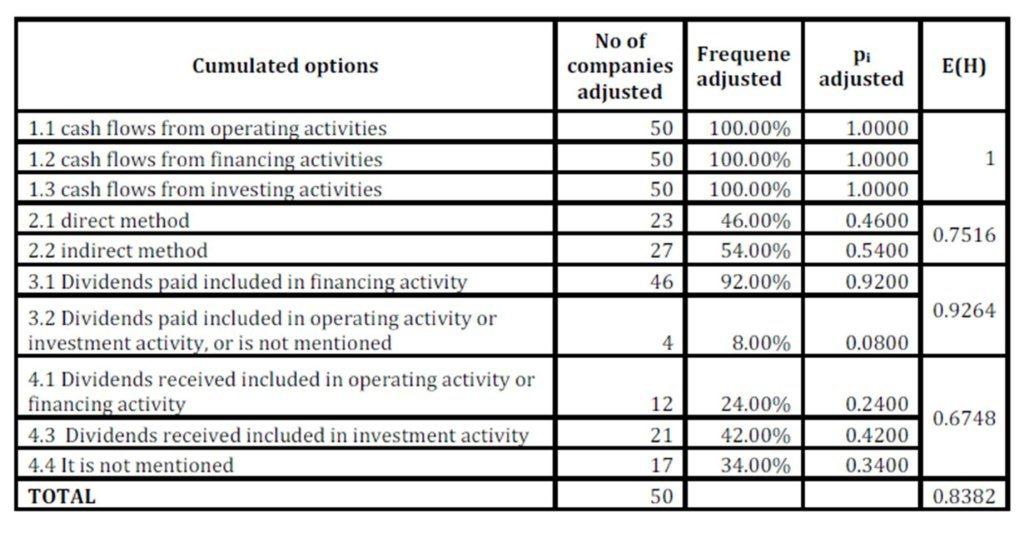

This indicator was developed by Tas van in 1988 to measure the degree of harmonization at a state level. This indicator is used when considering a sample of entities, measuring the compatibility of accounting practices. Starting from the idea that the degree of harmonisation depends not only on the number of alternative accounting methods used, but also on the degree to which each method is used in practice, Mustata (2008) afirms that H Index (Herfindahl Index) is actually a statistical tool of measuring the concentration degree. It is recommended that this indicator to be applied when the accounting methods used implies a concentration around a limited number of alternatives.

E ( H ) measures with H Index the compatibility of accounting practices. For this indicator to be relevant, the minimum number of subjects which choose a certain accounting option shall be five.

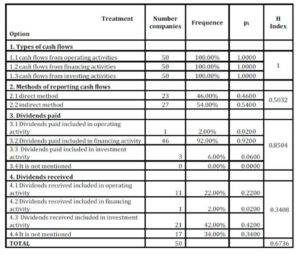

Table 5: H Index computation

H Index was computed for each problem and subproblem studied. Depending on the values obtained, it can be observed the degree of approximation at 3 levels: low, medium and high.

SPSS analysis

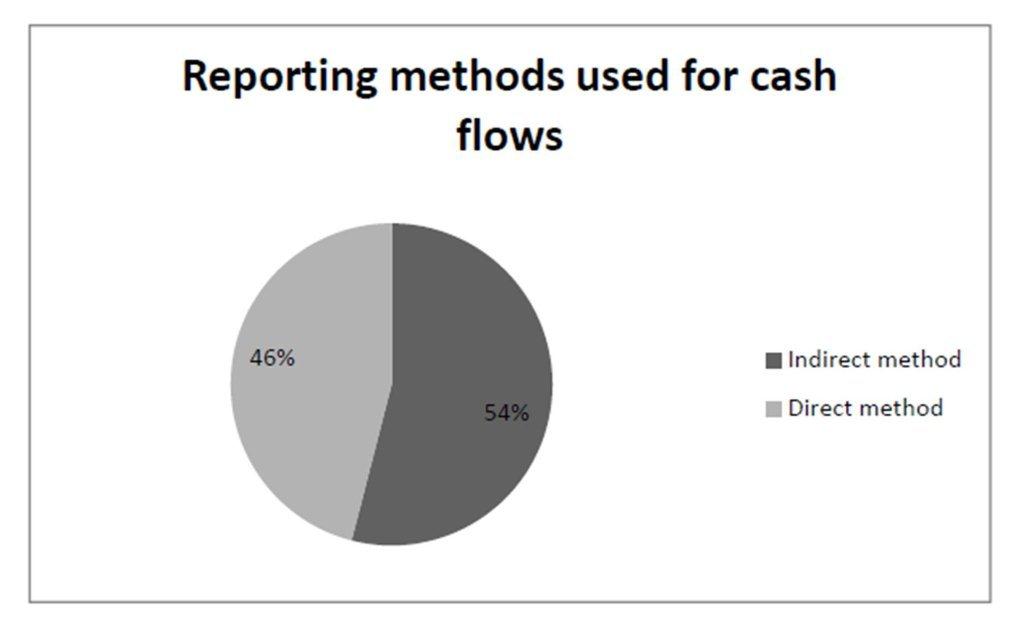

Methods of reporting cash flows that can be applied by entities under IAS 7 are classified as follows:

• direct method of reporting cash flows

• indirect method of reporting cash flows.

Analyzing the entities studied, it was observed that 54% of the entities apply the indirect method of reporting cash flows and 46% of them use the direct method (-fig. 4).

Table 6: E(H) Index computation

Figure 4: Reporting methods used for cash flows

Entities included in the project can be classified as:

• 2% of entities classified the dividends paid as cash flow from operating activities

• 6% of the entities classified the dividends paid as cash flow from financing activities

• 92% of entities classified flow dividends paid as cash flow from investment activities.

Analyzing the classification of dividends received in cash flows, the entities included in the project can be classified as:

• 22% of entities included dividends received into the cash flow from operating activities

• 2% of entities included dividends received into the cash flow from financing activities

• 40% of entities included dividends received into the cash flow from investment activities

• 36% of the entities do not specify in cash flow the dividends received.

With respect to dividends paid employment in the cash flow statement, we can conclude that:

• most entities include dividends paid on the cash flow statement in the financial activities, most entities being from industry sector, being 17 in number, with one exception;

• the entities that include dividends paid on the cash flow statement in the investment activities, provide financial services and trade.

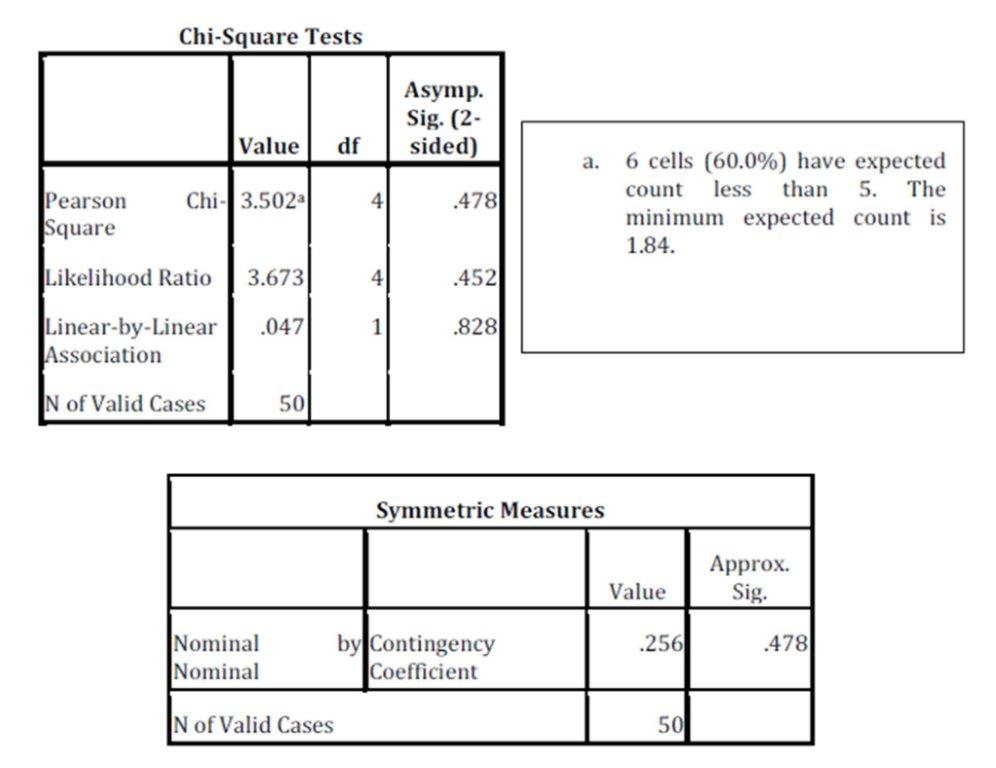

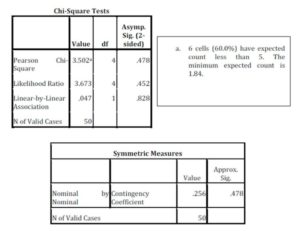

To verify the association between the two variables, the method of representating the cash flows and sector of activity, we used χ2 test. The χ2 test reveals the existence of association, and to find out the bond strength, we analysed the contingency coefficient. Pearson’s coefficient is 3.502 (≠ 0) and the probability of accepting the null hypothesis (Sig) is 0.478> 0.05 which indicates the existence of relationship between the two variables (table 7).

Table 7: Contingency coefficient computation

Contingency coefficient values are belonging to the interval [0, 1). If the coefficient’s value is closer to 1, the level of the association is higher. In this case, the coefficient is 0.256 which shows a medium link between the method used and the sector of activity.

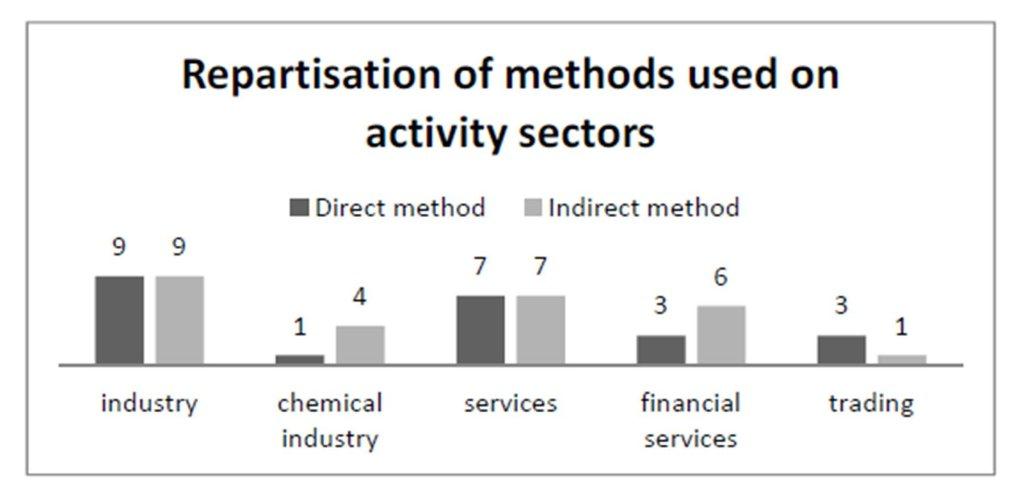

The graphic below shows the repartisation of the two methods on activity sectors:

Figure 5 : Repartisation of methods used on activity sectors

Conclusions

Harmonisation will reduce differences between countries and will highlight the comparability between companies all over the world. Concerns in the area of measuring accounting harmonization, national or international, is a normal state of affairs, the results obtained may contribute to the desire for the existence of a set of globally accepted accounting standards or the development of the globalization of accounting. Effects that amplify the harmonization of national accounting system in comparison with the two accounting referentials – European Directives and IAS/IFRS- are evident in the adoption of the new Order no. 3055/2009.

In the study conducted, the values obtained for the coefficients Jaccard, in the comparison of the Romanian accounting regulations and IAS 7 for all issues analyzed are Sij = 1 and Dij = 0. It results that between the two sets of accounting standards analyzed, there is a maximum degree of similarity, the two sets of standards dealing the same with the four problems analyzed. Following the SPSS analysis of the issues studied, it can be observed that there is a link of mean intensity between the method of reporting the cash flows and the sector of activity. The ANOVA analysis has shown that there are no links between the company’s profit and the sector of activity. Graphs made using SPSS give us a better perspective on the situations studied and the various links that may occur between them. Analyzing the compatibility of accounting practices for the fifty companies, we use two indicators H Index and E ( H ). Values obtained for H Index indicator, in the four issues considered are: H Index ( types of cash flows ) = 1 , H Index ( method of reporting cash flows ) = 0.5032 , H Index (dividends payable ) = 0.8504 H Index ( dividends received ) = 0.3408 , H global Index = 0.6736. Regarding cash flows, all 50 companies recorded three types of cash flows ( operating, financing, investing), so H Index ( types of cash flows ) recorded maximum values. H Index (methods of reporting cash flows ) recorded average values, 46 % of companies applying the direct method, the remaining 54 % using the indirect method. H index (dividends paid) records a high degree, the harmonization between accounting practices of the firms is at a high level. Around 92 % of the companies paid dividends and included them in the financing activities, 2% dividends paid included in operating activities and the remaining 6 % dividends paid included in investing activities. Under IAS 7, companies may not include dividends paid in investment activities. However, 6% of the analyzed companies include dividends paid within this category.

Regarding the dividends received is noted that 11 companies register the dividends received in operating activities, one firm in financing activities, 21 firms in investment activity and the remaining 17 firms (34% of sample representing 50 companies) do not mention the accounting politicy in respect of dividends received. H Index (dividends received) recorded averages, given the fact that for 34% of firms the received dividend policy is not mentioned. H Global Index’s value is an average one, the degree of compatibility for the issues analyzed in the sample being an average one. Globally, the indicator E ( H )’s value is 0.8382, the level of harmonization globally in terms of the four accounting policies analysis is high. Referring to the types of cash flows, the value of this indicator is maxim. Indicator E ( H ) for the reporting methods of cash flows records an average value, 54% of companies adopting the indirect method. In respect of dividends paid, the degree of compatibility is great, the value of E ( H ) = 0.9264, 92% of the 50 companies recording paid dividends in the financing activities, the remaining 8% included dividends paid in operating activities or investment activities. The value of indicator E ( H ) on the issue of dividends received is average, 24 % of firms using dividends received included in operating activities or financing ones, 42% included dividends received in investment activities, the remaining 34 % of companies do not specify any information in connection with the dividends received.

(adsbygoogle = window.adsbygoogle || []).push({});

References

1. Buiga, A. (2009) Statistică inferenţială. Aplicaţii în SPSS, ed.Todesco, Cluj Napoca.

2. International Accounting Standards Board (2007) , International Accounting Standards (IFRSs.).

3. Mustaţă, R. (2008) Measurement systems for harmonization and diversity in accounting- between necessity and spontaneity, Casa Cărţii de Ştiinţă Publishing, Cluj-Napoca.

4. Order of the Romanian Ministry of Public Finance 3055 (2009), published in Romanian Official Gazette no. 766, November 10.

5. Samuels, J., Piper, A. (1985) Accounting: A Survey, Hardcover, p.56-57.

6. Shil, C., Das, B. and Pramanik, A.K. (2009) Harmonisation of Accounting Standards through Internationalisation, International Business Research Journal, vol.2, no.2, April, p.195.

Google Scholar

7. Wang, C. (2011) Accounting Standards Harmonization and Financial Statement Comparability: Evidence from Transnational Information Transfer, Working paper, The Wharton School, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1754199.