Introduction

Microfinance is a development tool used to create access for the economically active poor to financial services at a sustainably affordable price. The issue of micro financing was hitherto understood only in terms of working capital. The availability of skilled Human Capital is fundamental to creating and sustaining the momentum of Financial System Strategy 2020 (FSS, 2020).There is an immediate need to enhance the skills of the current workforce in the medium to long term need and to develop a continuous pipeline of quality human capital for the Nigerian Financial Services Industry. This will depend heavily on the reformation of the collapsing Educational and Institutional structures in Nigeria and on the collaborative and competitive attitude that the existing players in the Financial Services industry decide to adopt. Human capital is the knowledge and know-how that can be converted into value. Human capital consists of know-how education, vocational qualifications, training, trading programs, union activity compensation plan and shares options scheme. Today, it is argued that these expenditures are incurred by an enterprise in order to get the benefit of the services of its manpower force and treat them as intangible asset to be capitalized. This is against the accounting principle of treating them completely of expenditure nature by writing them off against profit in the profit and loss account. The failure of professional accountants to treat human resources as assets just like physical and financial assets led to the emergence of Human Resources Accounting (HRA) – (Eddie and Atrill, 2002). There has been little debate in the literature on human resources accounting in the context of its significance when evaluating firm’s performance. Flamholtz (1971) defines Human Resources Accounting as the measurement and reporting of the cost and value of people in organization resources. For instance, efforts to make human capital acceptable as costs in organization have not been totally recognized. The human resources costs are usually written off to the profit and loss account and expenses in the books of the company rather than creating value for human capital and accounting for them in the balance sheet of the company as done in the case of physical assets like lands, machineries, equipments and financial assets like ordinary shares, treasury bills and debentures.

The issues of who is responsible for the effective use of all other resources in the business (Akindele, 2007) have been on the front burner. Human resources being the traditional name for human skills used in the organization over the years have remained less valued and recognized in the literature of the accounting professions. To bring value to human resources is to redescribe it as human capital. Human capital gives rise to Human Capital Assets whose value is significant to the organizations. Baker (2003) stated that, human capital asset (HCA) brings out the investment in human capital. How do will evaluate the value attributable to human capital? There has always been the problem of accounting for human capital value, which is conventionally being applied in reducing the profit of Micro-Finance Bank (MFB) and by implication; result is huge loss to organizations.

Human capital is the productive efforts of an organization’s workforce while performance is the employees’ performance that helps implements the firm’s strategy. Most firms have had to cut down the cost of human capital to ensure survival because huge human capital cost is always a threat to the survival of firms and also a threat to the liquidity of banks and other businesses. Organizations invest in human development, only for the human capital to leave the organization for greener pastures within a short period. The economic loss to such firm impact negatively and heavily on its performance, survival and growth. There is the problem of a onetime huge investment in human capital that brings MFB to long time loss if not treated adequately. These are issues that have been in existence and have to be addressed in this study. There is also the issue of concept compatibility through the practice of expending huge human capital cost and the growing idea of capitalizing human capital development as intangible asset. The incessant turnover of trained and talented personnel of the firm that could have been retained by organization in the balance sheet of firms cannot be overlooked. Accounting is seen to have two distinct stands: Management accounting, which seeks to meet the needs of business managers and financial accounting which seeks to meet the accounting needs of all the other users. Management accounting is the application of professional knowledge and skill in the preparation and presentation of accounting information so as to assist management in the formulation of policies and in planning and controlling the activities of business enterprise. The main users of financial information relating to business owners, customers, employees and their representatives, lenders, government, suppliers, investment analyst, competitors and community representatives.

Financial statement of a business provides a picture of the overall financial position and performance of the business. This is achieved through three major financial books of account which are rendered on a regular basis. These books are: cash movements over the period (The Cash flow Statement); the amount of wealth generated by the business over a particular period (The Profit and Loss Account); the accumulated wealth of the business at the end of a particular period (The balance sheet). Accounting is also based on a number of rules or conventions that have evolved over time in order to deal with the practical problems experienced by preparers and users rather than to reflect some theoretical ideal. Under the money measurement convention, accounting normally deals with only those items that are capable of being expressed in monetary terms. This is because money is a useful common denominator with which to express the wide variety of resources held by a business (Eddie and Atrill, 2002). However, not all such resources are capable of being measured in monetary terms and so will be excluded from the balance sheet. The money measurement convention, therefore, limits the scope of accounting reports. Some resources held by a business are not normally included in the balance sheet because they cannot be quantified in monetary terms and include quality of the workforce, the reputation of the business’s products, the location of the business, the relationships with customers and the quality of management. In the traditional accounting practice, the heavy amount incurred on the recruitment, placement, selection, training and development of the personnel is generally treated as expenditure and hence, it is debited to profit and loss account of the period during which such amount is incurred.

The hypothesis to be tested in null form state that: Human capital development value does not have significant and positive impact on the Microfinance banks’ performances. The focus of this study is microfinance banks in the four major divisions of Ogun State, Nigeria. Sixteen microfinance banks were investigated. The researcher reached out to shareholders and stake holders of the banks in focus and also covered the head offices of the affected banks that were not in Ogun State. This study is justified because of failure of professional accountants to treat human resources as an asset and reveals the non significant roles given to the managers of businesses. This study will also attract the attention of the academics and societies generally that the concept of human resources accounting should be an important issue to be treated as assets in the books of organization by reflecting them in the balance sheet. Some of the research questions to be answered in this study are: What is the effect of human capital development value (employees’ compensation in terms of salaries, wages) on the micro finance banks’ performances in Ogun State? What would be the effect of human capital development (staff training and development) on the financial statement of a firm? These questions are germane to this study in order to ascertain the contribution of Human capital to the performance of microfinance banks. This study is carried out by a case study of Microfinance banks in Ogun state in Nigeria to empirically provide insights into how human capital of Micro finance banks is reported in annual reports.The study is divided into five sections. Section one above presents the introduction. Section two reviews the existing literature. Section three shows methodology adopted for the study. Section four presents the data analysis and interpretation of results while Section five which is the last part deals with the finding, conclusion, and recommendations for policy decisions.

Literature Review

Likert (1967) argued that accountants have failed to deal with the human element in organizations as an asset and have consistently omitted it in corporate balance sheets as indicated by large difference between market values and book values of the owner equity in many corporations. He opined that managers take imprudent decisions due to lack of information about the form’s of human assets; irrespective of laudable vision and mission statements, the underlining purpose of the organization is to make profit.

Empirical research cites several limitations imposed by traditional accounting system in reporting human and intellectual capital. This includes the writing off of intellectual and human assets to expenses in the income statement. (Backhuijs et al., 1999, Lev et al., 1999) have demonstrated that it leads to systematic under valuation and relatively adverse liquidity of firms, These weaknesses are responsible for giving rise to part of the gap between market value and the net book value. Ronen (2001) opined that human capital refers to the productive capacities of human beings as income producing agent in the economy which also consists of wealth, skills and knowledge, which have economic value cited in (Imeokparia, 2009:139). Enterprises report human capital because it will improve the performance of the enterprise. Kaplan et al., (1992) and Kirkpatrick (1994) studies conducted on human capital showed that it would improve enterprise image in society; indicate social responsibility and ethical values to the outside world; improve marketing to present and potential customers; benchmark human resources management and development; attract and retain qualified labour force. Guest (1997) and Hartog (1999) argued that the identification of human capital does not in itself imply that it will be measured. Given the intangible nature of human capital and the difficulties in establishing reliable measuring techniques, indicators such as market value over booked value or costs of input over output activities at enterprise level have been used rather than actual measurement. Two different methods can be used to measure the input of human capital. For instance, non-economic measurement one of the methods; can be linked either to formal or real human capital. Formal human capital can be ascertained through education attainment, years of schooling and/or other indicators such as job positioning number of years in job positions, etc. This is primarily related to individual and society level. Real human capital can be measured directly at the individual level by means of interviews, test and/or examinations. Hillage and Morale (1996) submitted that economic measurement methods are related to the costs and benefits of acquiring, maintaining and developing human capital. This is related to all levels, individual, organization and society. This includes direct and indirect education and training costs, alternative costs as well as the returns to any given investment, be it time and/or money. The inability to come up with reliable and verifiable methods of measurement system is one of the challenges for reporting on human capital. For instance, the cost-effectiveness of the training may be so glaring that formal evaluation may be unnecessary.

Olsson (2001) examined the annual reports of the largest Swedish firms in the stock market. It was found that in 1998 none of the 18 companies reported more than 7% of human resources information in annual reports and they were deficient in the quality or the extent of the disclosure. Brennan (2001) cited in (Imeokparia, 2009:139) carried out a similar empirical study in Ireland using technology and people oriented firms. She analyzed annual reports of 11 public firms and 10 private firms. Her study showed that external capital is the most frequently reported category.

Okafor (2009) in her study on disclosure of human capital in the annual reports of firms in Nigeria, solicited for views of accountants both academic and in practice.

“She found that most accountants are in favour of HRA theories and practice in the country, but they are of the view that, HRA information should be presented as a separate report and as asset in the balance sheet so that financial statements without HRA Information shall be presented as a healthier manner. She advocated the use of staff costs methods of HRA valuation for inclusion in financial statements. The study also found that there number of difficulties in HRA which include; difficulty in quantifying human resource without bias, difficulty in establishing acceptable parameters for valuation, establishing basis for depreciating of human assets, high mobility from one job to other and agitation for salary increase can makes valuation”.

Kumshe (2012) in a Ph.D thesis titled ‘human resource accounting in Nigeria; an analysis of its practicability which aims at examining and assessing the applicability of Human Resource Accounting (HRA) in the financial statements of incorporated companies in Nigeria, utilized views from both administrative and management staff of the sample companies:

“The study established that, there is greater awareness among various categories of staff of HRA concepts but also agreed that HRA is not practiced by Nigeria companies. The study showed how HRA can enhance the completeness and quality of financial statements; also with HRA more information is made available to the investor to make more rational investment decisions, because HRA provides more information on the real value of companies”.

Mohammed and Aminu (2012) in his paper titled “human capital accounting: assessing possibilities for domestication of practice in Nigeria”; concluded that it is possible to domesticate HRA in Nigeria considering that, both professional and accounting standards are capable of accommodating HRA practices especially with the growth of service sector in the Nigeria economy and the manner in which convergence and harmonization of accounting practice grow stronger by the day. He argued for domestication of HRA practice in Nigeria through legislation and ensuring complete participation of all stakeholders. He advocated for an expansion of international accounting standard (38) on accounting for intangible assets to cover human resource or there should be a new standard developed to cater for HRA practice in Nigeria.

Patra, Khatik and Kolhe (2003) examined the correlation between the total human resources and personnel expenses for their fitness and impact on production. They found that HRA valuation was important for decision making in order to achieve the organization’s objectives and improve output. Sometimes it may be impossible to obtain the data necessary for a formal evaluation of training. Using content analysis of 100 companies selected by market capitalization, Imeokparia (2009) found that Nigeria companies are active in human resource and intellectual capital reporting. Most Nigerian companies report human resource and intellectual capital in the sundry section of the annual report such as the managing director’s report, chairman’s statement and value added statement. The study showed human resource accounting and intellectual capital information by line count and one-third by frequency count. A detailed exposition of human capital development practices in Singapore was undertaken by Lall (1999) and Kurvilla, Erickson and Hwang (2001). In Singapore the government has taken the initiative in human capital development, investing heavily in creating high-level skills to drive and upgrade the industrial structure. The tertiary education system was expanded and directed towards the needs of national industrial policy. The government emphasized specialization at the tertiary level, changing focus from social studies to technology and science oriented fields. To achieve this, the government exercised tight control of curriculum content and quality, and ensured its relevance to national industrial objectives.

To this end, the government extensively promoted employee training programs held outside the firm. The government set-up the Skill Development Fund in 1979, along with a Skill Development Levy, which collects a tax of 1 percent of payroll from employers to subsidize the training of low-paid workers. According to Lall (1999:36), this symbolized the “identification of technology-intensive and knowledge-intensive industrial structure and high value-added orientation as national objectives”. The government runs 2 national Universities, four polytechnics and numerous public or non-profit specialized institutions for a population of 4.5 million people. 41 percent of University graduates were in technical fields as at 1996. Polytechnics aim at meeting the strategic needs of mid-level technical and managerial skills, emphasizing engineering at every point.

Methodology

The study was carried out in Ogun State. The state was created in 1976 with the capital in Abeokuta. Ogun State is located in the South West of Nigeria with a population of Three million seven hundred and twenty eight thousand and ninety eight citizens (3,728,098), (National bureau of statistics 2006 national population census). This population is expected to have grown to (4,218,001) as at 2011, given the annual growth rate of twenty five percent (25%). The state has 20 Local Government Areas and is predominantly populated by the Yorubas with the Eguns in the minority. The state is broadly classified along four ethnic/ dialect nationalities namely: The Egbas, Ijebus, Remos and Yewas. The total population for this study consists of the forty eight (48) Micro Finance banks that are spread across the state. Ogun state one of the leading commercial centres in Nigeria was chosen for convenience because the researchers reside in Sango Ota, Ogun State. In order to achieve the research objective and ensures the collection of representative data, the state was divided into four, namely Egba, Ijebu Remo and Yewa Divisions. Structured questionnaires were used to elicit information from respondents. Four microfinance banks were sampled in each of the four divisions using judgmental sampling technique based on the possibility of being able to collect the required data from the chosen microfinance bank. The researcher however, ensured a wide geographical spread of the selected microfinance banks within each of the division to ensure collection of a representative sample. Most of the most of the Micro finance banks are located in the four divisions. A randomly selected sample size was taken from the population and this produced a total sample of 16 microfinance banks (33.3%) out of a total of 48 microfinance banks in the state cutting across the four divisions.

Krejcie & Morgan (1970) in Amadi (2005) agrees with the sample as they proposed the population proportion of 0.05 as adequate to provide the maximum sample size required for generalization. A total of 350 questionnaires were distributed among the 16 selected banks cutting across the top executives, middle level managers, lower level workers; the directors and the shareholders of Microfinance banks in Ogun state. A total of 320 questionnaires were finally adjudged good enough for the purpose of analysis after evaluating the quality of responses of the respondents to the questionnaires. Secondary data were collected from already published works, collated figures and facts from Central Bank, financial journals, newspaper articles relating to micro finance banks, and annual reports of concerned micro finance banks and the internet. The validity for this research instrument was confirmed by subjecting the Questionnaire to expert review and constructive opinion. The experts selected included academics and professionals in the field. The reliability this research was confirmed by testing and retesting the questionnaires.

Measurement of Variable

The hypothesis and variable for this study is operationalized using simple linear regression model. The hypothesis to be tested in null form state that: Human capital development value does not have significant and positive impact on the Microfinance banks’ performances. Impact factor requires the use of regression analysis; relationship study requires the use of correlation while differences between variables in a study require the use of ANOVA.

Model: S = f (HCV) ……………………………………… Equation 1

HCV = Human Capital Value

S = b0 + bih + U ………………………………………. Equation 2

Where S = Survival (Gearing Ratio – D/E), D = debt, E = equity

G = b0 +b1W+ b2 T + b3A + U. ………………………………….Equation 3

Hence we will generate below the following:-

Log G = b0+b1 log W+ b2 logT + b3 logA + U ……………………Equation 4

Data Presentation, Analysis and Interpretation

The study employed both parametric and non-parametric technique. The parametric statistics enable the researcher to generalize the outcome of the research through the sample parameter. The Non-Parametric method include simple percentages, ratios and averages while the parametric statistic used the simple regression analysis for the purpose of generalizing the result obtained from the sixteen (16) microfinance banks used for the study.

Distribution of Respondents

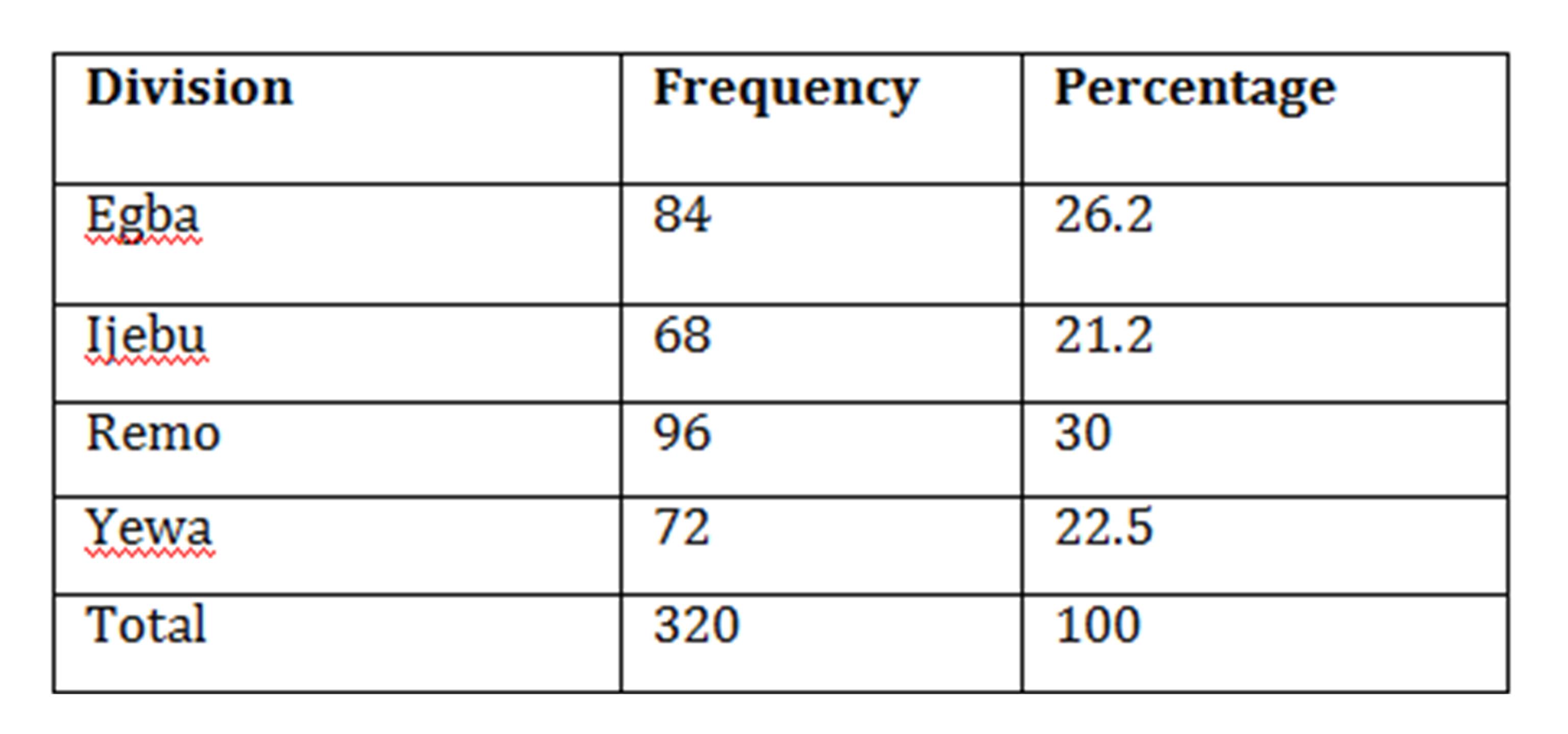

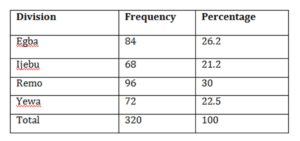

Table 4-1 presents the distribution of the respondents by divisions. Out of the 350 questionnaires administered 320 were selected for final analysis. This represents about 91.42 percent of the total questionnaire distributed. A total of 84 (26.2%) were from Egba, 68 (21.2%) from Ijebu, 96 (30.0%) from Remo and 72 (22.5%) from Yewa divisions of Ogun State.

Table 4-1: Distribution of Respondents by Divisions

Source: Field Survey, 2012

Distributions by Respondents Category

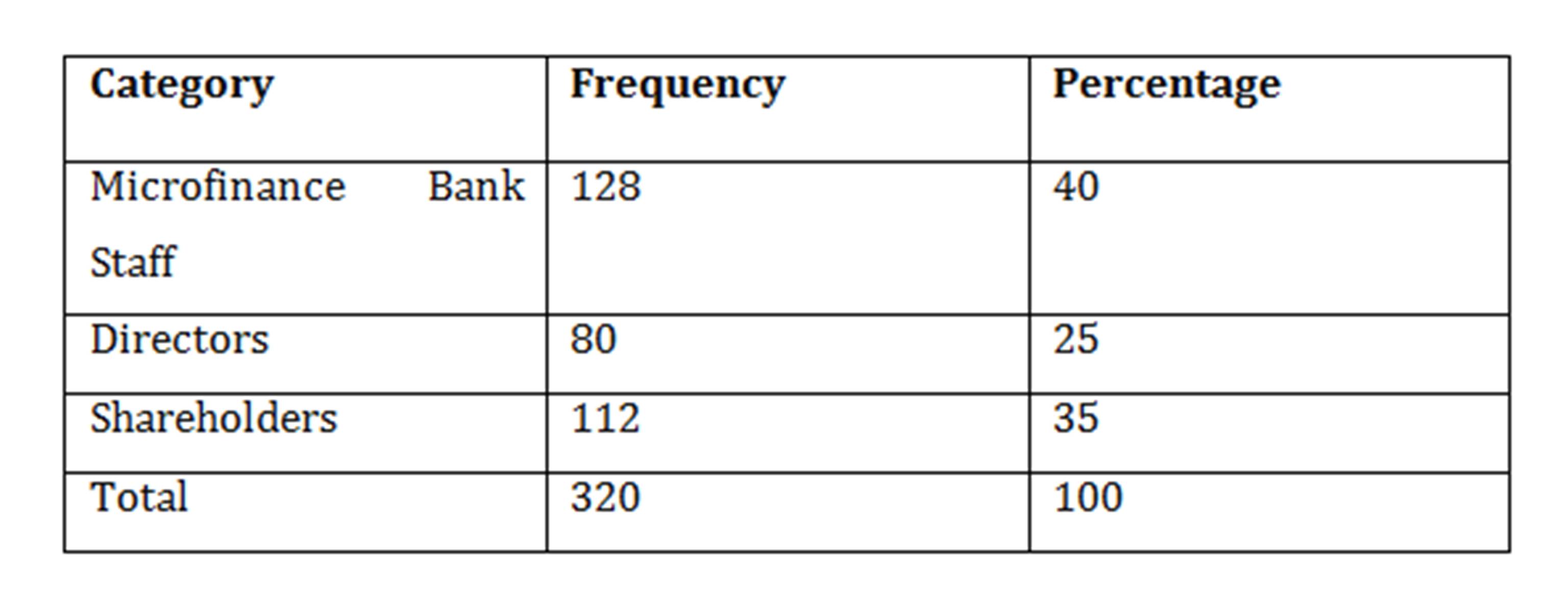

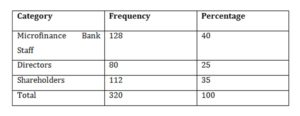

Table 4-2 shows the distribution of the different categories of the respondents used in the survey. The table shows that 128 (40%) were microfinance bank staff, 80(25%) were directors of microfinance bank while 112 (35%) were microfinance bank shareholders. This shows that information was elicited from both high and low staff.

Table 4-2: Distributions by Respondents Category

Source: Field Survey, 2012

Socio-Demographic Characteristics of the Respondents

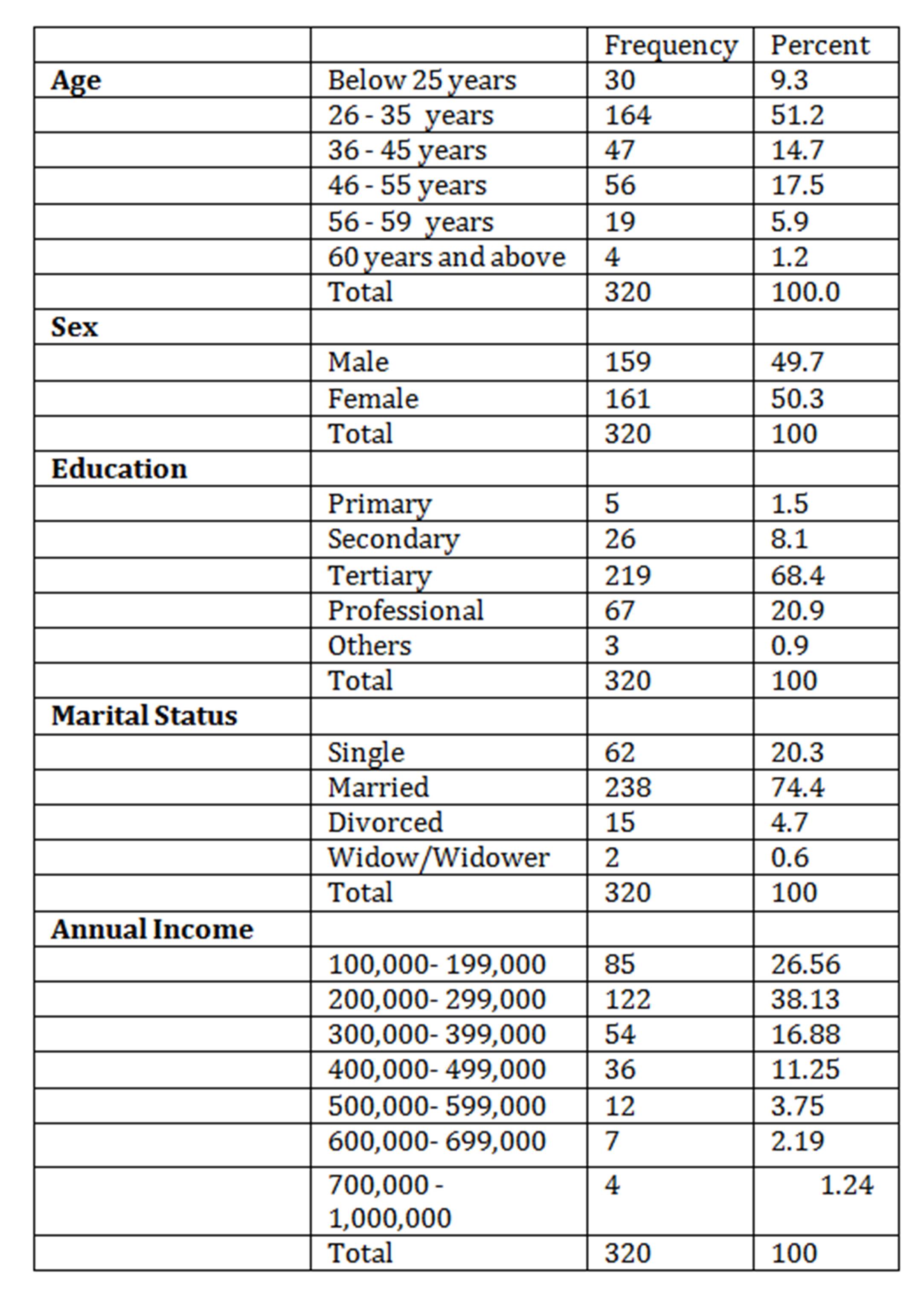

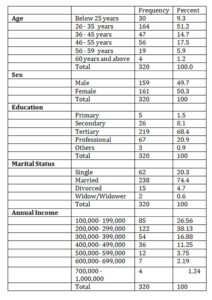

The results in Table 4-3 show the socio-demographic characteristics of the respondents. The variables provided in the table below gives an insights into the background of the respondents which is assumed to have influence on their opinions and perception of human resource accounting issues and performance of the organization. Their age distribution shows that 30 (9.3%) of the respondents were below 25 years of age, 164 (51.2%) between 26 — 35 years, 47 (14.7%) between 36 — 45 years, 56 (17.5%) between 46 — 55 years, 19 (5.9%) between 56 — 59 years and 4 (1.2%) were 60 years and above. This indicates that majority of the respondents were between the age of 26 – 35 years old. The distribution of the respondents by gender according to the table shows that 144 (45.0%) of the respondents were male while 161 (50.3%) were females. This shows an equitable gender distribution of respondents to the study. The distribution of respondents by educational qualifications indicates that 5 (15%) were educated up to Primary School, 26 (8.1%) up to Secondary school, 219 (68.4%) were graduates, 67 (20.9%) had Professional Qualifications and 3 (0.9%) had other qualifications. The table also presents the distribution of respondents by marital status. From the table 4-3, it can be seen that 62 (19.4%) of the respondents were single, 238 (74.4%) were married, 15 (4.7%) divorced and 2 (0.6%) are widow/widower.

Table 4-3: Respondents’ Distribution by Socio-Demographic Variables

Source: Field Survey, 2012

General Appraisal of Human capital Accounting and MFBs Performance

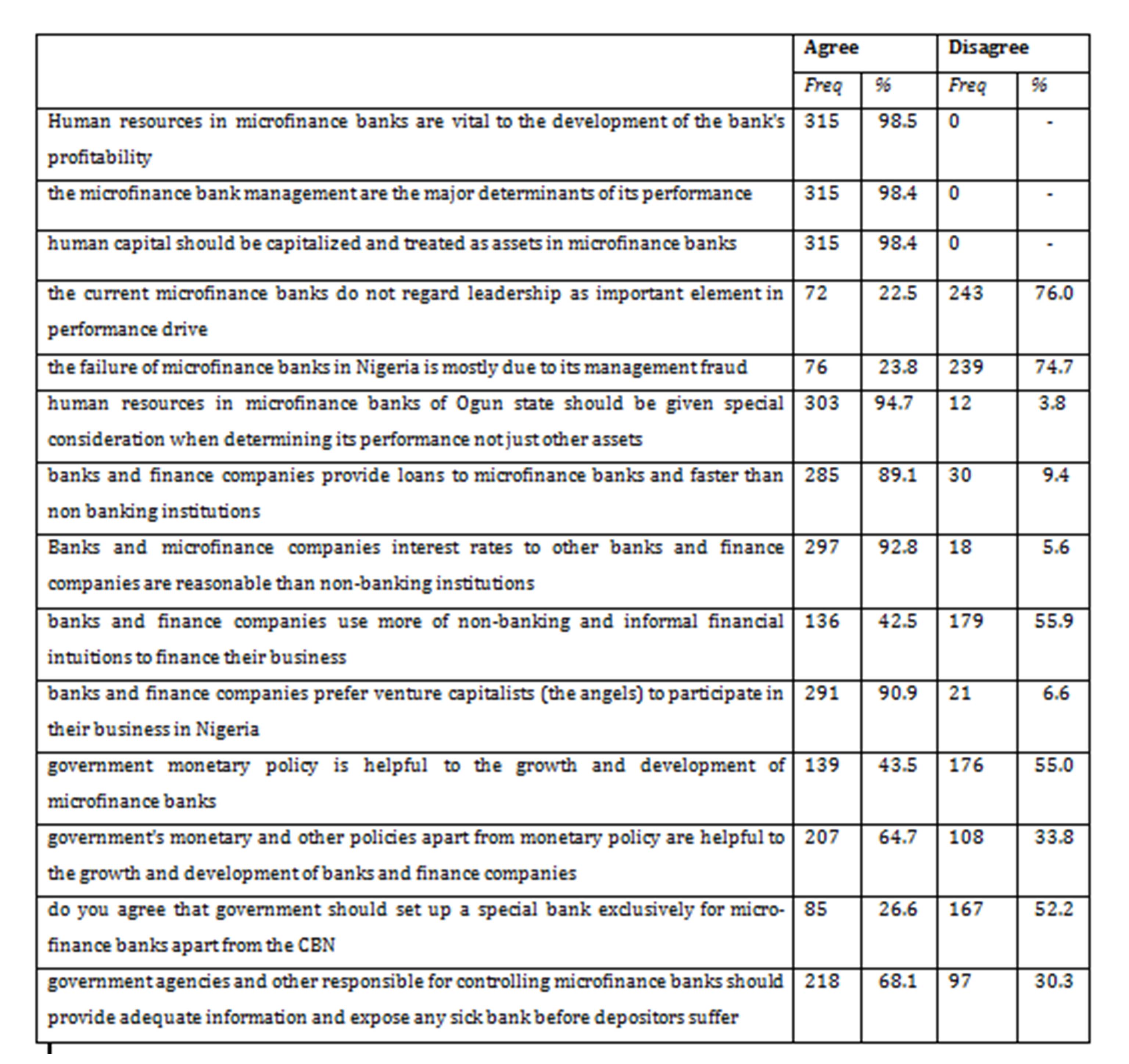

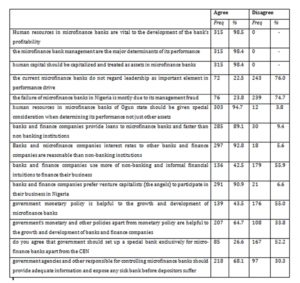

Table 4-4 below presents the general appraisal of the human capital accounting and other general matters on MFBs performance. The table shows that the 98.5% respondents agreed that human resources in microfinance banks are vital to the development of the bank’s profitability, 98.4% of respondents confirmed that the microfinance bank management are the major determinants of its performance and 98.4% of the respondents agreed that human capital should be capitalized and treated as assets in microfinance banks. 94.7% respondents agreed that human resources in microfinance banks of Ogun state should be given special consideration when determining its performance. From the study 92.8% agreed that Banks and microfinance companies interest rates are reasonable than non-banking financial institutions; 90.9% agreed that banks and finance companies prefer venture capitalists (the angels) to participate in their business in Nigeria; 64.7 % agreed that governments monetary are helpful to the growth and development of banks and finance companies while 68.1% confirmed that government agencies and other responsible for controlling microfinance banks should provide adequate information and expose any financial unhealthy bank before depositors suffer.

Table 4-4: General Appraisal of Human capital Accounting and MFBs Performance

Source: Field Survey, 2012

The result shows that 76% disagreed that the current microfinance banks do not regard leadership as important element in performance while 74.7% confirmed that the failure of microfinance banks in Nigeria is mostly due to its management fraud.

Testing of Hypothesis

The hypothesis in this study investigated the influence of managerial expertise on the survival of MFBs. This was evaluated by testing the hypothesis that: Managerial expertise does not have any significant effects on the microfinance banks’ survival factors

S = f (HCDV) Equation…………………….. 4.5

Investment in human capital development value is linearly decomposed into: Salaries (S) and Managerial expertise (M). The dependent variable, SV (Survival) has been proxied by the growth in turnover, implying the ability of the business to continue to generate business gives an assurance for its continued existence and survival. The estimated regression line is presented in equation ………………………………………….4.6

SV = 1.514 + 0.182S + 0.165M 4.6

(41.014) (3.349)* (3.033)* Adj. R2 = 0.058

Note: t-values in parentheses; *: significant at 1 percent level; F-value: 10.746 (sig: 000)

The result presented in equation 4.6 indicates that investment in human assets through salary payments has a positive and significant influence on survival of microfinance banks. This is brought about by the fact that payment of good salary is motivational which propels employees to strive harder to generate income for the firm since their own individual survival is also dependent on the survival of the bank. On the other hand; investment in training and development of managerial expertise also has significant and positive effect on the survival of MFBs in Ogun State.

The adjusted R2 is 0.058, implying that human capital development contributes about 5.08% to the continued survival of MFBs. The study therefore reject the null hypothesis that human capital value has no tangible effects on the microfinance banks’ survival factors and accept the alternative. This confirms studies of Kumshe (2012) and Mohammed and Aminu (2012) that capitalization of human resource need to be recognize in human resource accounting.

Microfinance Bank and Reporting of Expenses on Human Capital Expenditure

The study carried out a content analysis of the annual reports and financial statements of the sampled MFBs. The content analysis can be summarized under the following headings.

Staff Training

All the MFBs reported that:

- Their banks recognized human resources as the most important assets of the organization.

- Staff is allowed to attend seminars and courses especially those organized by Central Bank of Nigeria (CBN) and other Training Institutions

- The distribution of training attendance cut across all cadres of staff- managing directors, Company Secretary, Internal Auditors, other Senior staff and Junior staff

- In-house courses were also organized for staff especially the junior staff.

However, none of the Microfinance Bank (MFBs) reported on the actual amount expended on staff training and development.

Staff Salary and Staff Strength

(i) The average expenditure on staff salaries and wages the MFBs was N11, 045, 453 per annum for the period covered.

(ii) The average staff strength was eighteen (18). It therefore implies that an average MFB in Ogun State invested an average of N613, 636.28 per employee in terms of salaries and wages.

Financial Performance of Microfinance Banks in Ogun State

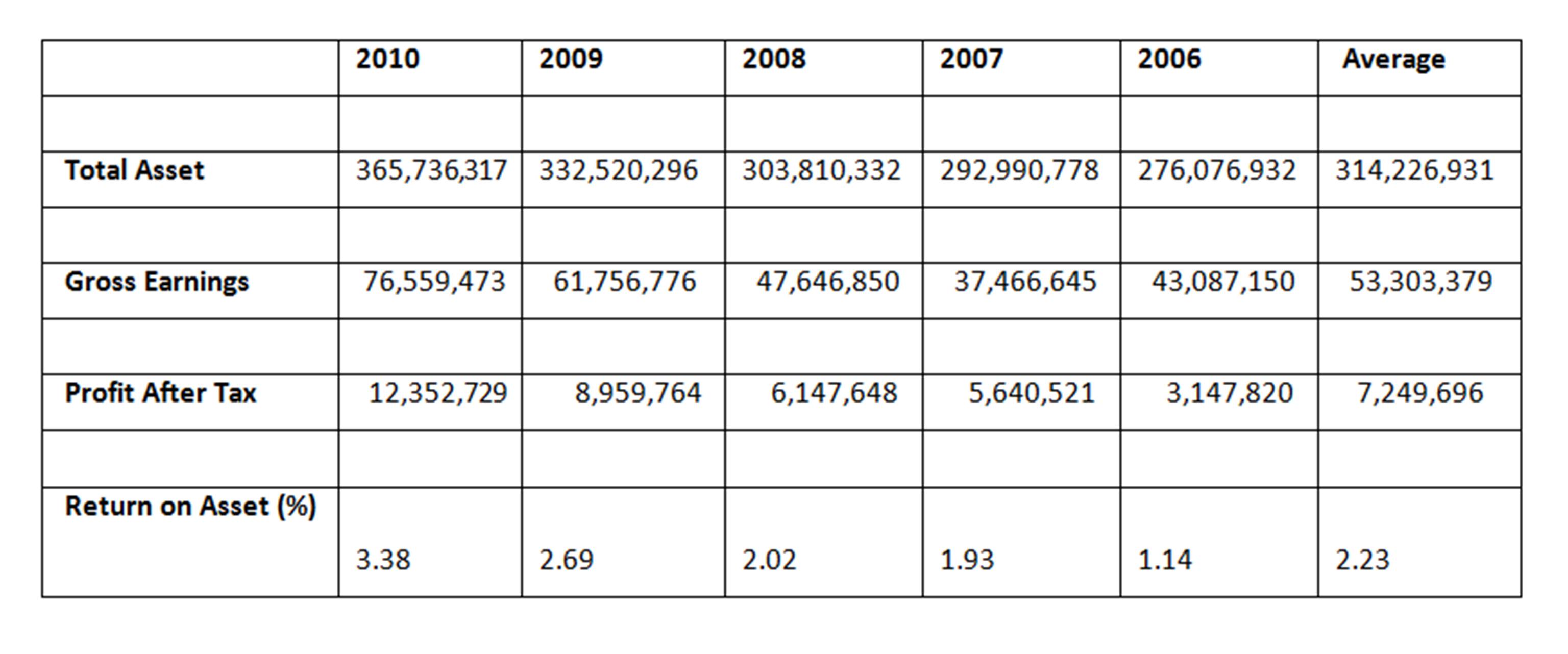

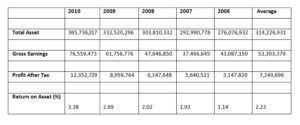

Table 4-6 presents the average financial performance of the microfinance banks whose staff was included in the survey. The analysis was based on the summary of the average total assets, gross earnings, and profit after tax and return on assets of the MFBs.

Average Total Assets

The result shows that the MFBs had consistently shown improvements in terms of their yearly average performances from 2006 to 2010. The total assets of the MFBs have improved from N276.08 million in 2006 to N365.74 million in 2010 with an annual average of N314.33 million. This suggests growth of 32.48% over the five- year period in the banks’ total assets.

Average Gross Earnings

The average total earnings /turnover of the MFBs had also improved consistently. The average gross earnings grew from N43.08 million in 2006 to 76.56 million in 2010. This indicates a growth rate of 77.68% over the five-year period. The average gross earnings of the MFBs was N53.30 million.

Table 4-5: Average Financial Performance of Microfinance Banks (2006- 2010)

Source: Annual Reports of 16 MFBs (2010)

Return on Assets (ROA)

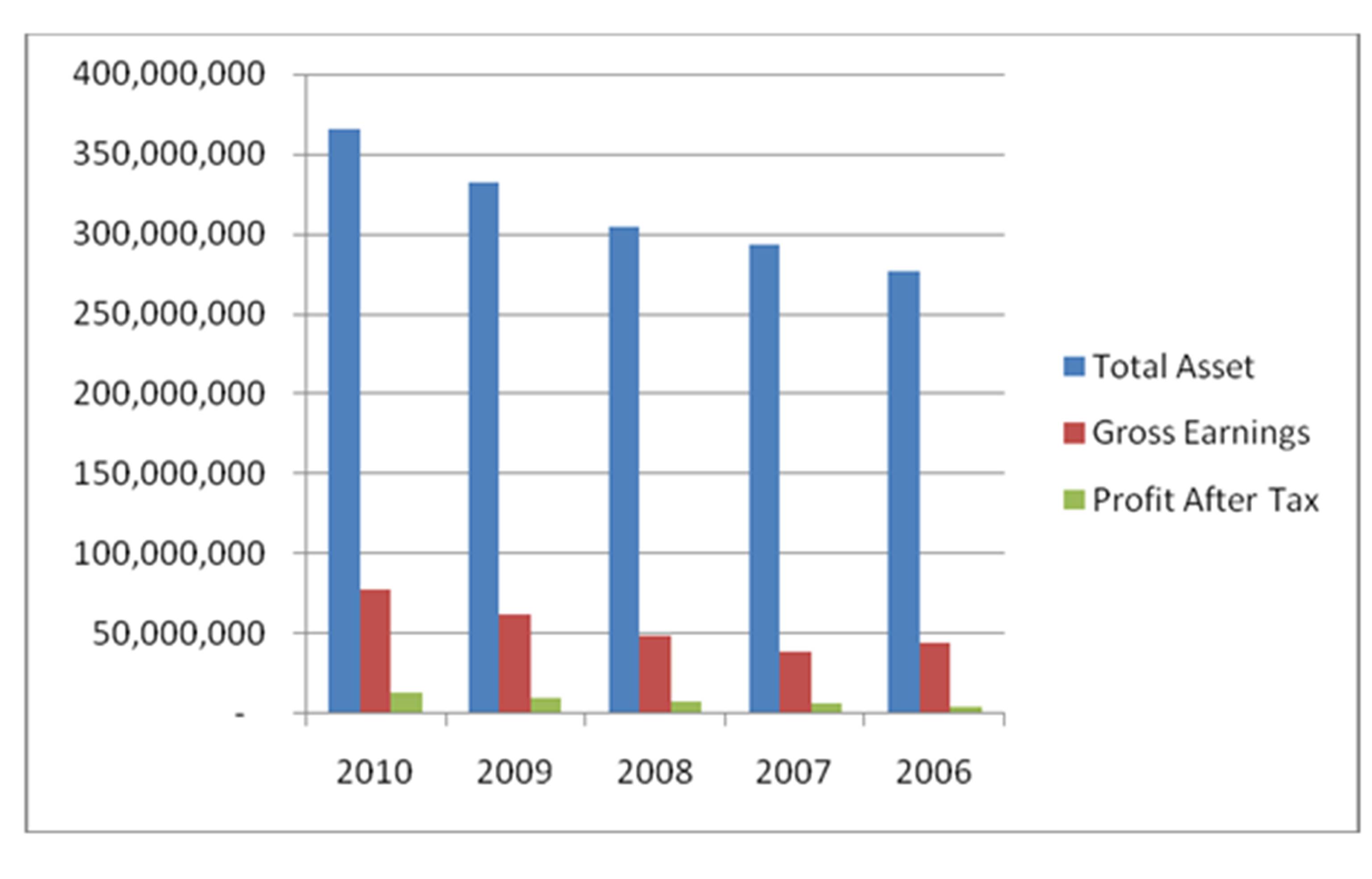

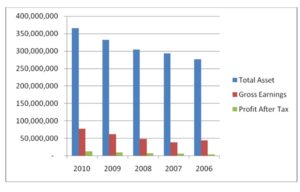

The result also shows that the MFBs have been run profitably over the years. The return on assets has been steadily on the upward trend. The return on asset was 1.14% in 2006 and grew to 3.38 as at 2010. The annual return on asset of the banks was 2.23 % on average. The MBFs have performed fairly well over the years. They have grown steadily in terms of asset base, profits and average return. The total asset, gross earnings and profit after tax is represented on chart 1 below:

Chart 1: MFBs Average total assets, Gross earnings and Profit after tax

Source: Annual Reports of MFBs

Conclusion, Findings and Recommendations

Conclusion

The study has shown that firms should ensure proper accounting for investment in human assets while such expenditures should be capitalized rather than written off to profit and loss accounts. Human capital value development, contributes significantly to the overall performance and survival of Microfinance banks in Ogun State. The failure of professional accountants to treat human resources as assets just like physical and financial assets led to the emergence of Human Resources Accounting (HRA). (Eddie and Peter, 2002). Human Resources Accounting advocates the measurement and reporting of the cost and value of people and their capitalization in organization resources rather than writing them off to profit and loss account. The value of human resource component of all organizations are treated in the conventional financial statement by writing off expenditures on human capital development to the profit and loss account rather than being capitalized and shown in the balance sheet.

Findings

- The study revealed that the majority of employees, directors and shareholders 219(68.4%) have tertiary education and majority (51.2%) aged between 26 and 35 years. The majority 122 (38.13%) have annual salary of N200, 000 – N300, 000. Majority – 69 (66.83%) of the microfinance bank workers and directors have attended one form of training or the other in recent time.

- The study revealed that majority 315 (98.5%) confirmed human resource team is vital to the overall performance of MFBs. It was also revealed 314 (98.4%) that human resources expenditures should be capitalized and treated as assets. 313 (98.4%) of the respondents revealed that the management of MFBs is the major determinants of MFBs performance in Ogun State. The MFBs expended an average of N613, 636.28 per annum, per staff as salaries and wages. The average staff strength was eighteen.

- While the MFBs reported on their staff training activities, they have failed to reveal the amount expended on staff training and development.

- The study also shows that human capital development has positive and significant impact on overall performance of MFBs in Ogun State and answers the research question in section one of the study. Specifically, employees’ compensation in terms of salaries, wages and staff training and development has positive and significant impact on the survival and overall performance of MFBs in Ogun State.

Recommendations

- The accounting profession all over the globe should create a framework in the balance sheet to recognize treatment of human resources and appropriate value to be attached based on the inherent qualities of human capital.

- Recognizing human capital in financial statement would show accuracy in profit declaration.

- The study recommends that firms can significantly improve on their performance by investing in their employees and seeing the payment of salaries and training cost as investment expenditures for the development of human asset towards enhancing the productivity of human asset. Human capital expenditures should be perceived as investment costs that can be capitalized and included in the balance sheet rather mere operational cost to be written off to the profit and loss account.

- This study recommends for domestication of Human Capital Accounting practice in Nigeria through legislation and ensuring complete participation of all stakeholders as this will help in strengthening investment and related decision, also international accounting standard (38) on accounting for intangible assets should be expanded to cover human resource or a new standard be develop to cater for Human resource practice in Micro finance banks and by extension enterprises in Nigeria.

References

- Akindele R.I, (2007): Fundamentals of Human Resources: Nigeria, Cedar Production, Ile-Ife. ISBN-978-38468-8-4. pp. 379-385.

- Amadi, V.L; (2005): “An Investigation into the Role of Private Sector in Nigeria Higher Institution: A Study of the University of Abuja”, International Journal of Research in Education, Vol.2, No1 & 2

- American Accounting Association (1970): A statement of Basic Accounting Theory: Evanston, LIL: AAA, revised pp. 35.

- Asaolu T. O. & Nasar M.L. (2007): Essentials of Management Accounting and Financial Management. Nigeria: Cedar Production Ltd., Ile-Ife.

- Backhuijs, J.B (1999): Reporting on intangible assets, OECD Symposium on Measuring and Reporting of Intellectual Capital, Amsterdam (June 9 -11)

- Baker, G.M.N.(2003) “The feasibility and Utility of HRA” California: Managing Review, Summer 1794, 1733.

- Dobija, M.(1998): “How to place Human Resources into the Balance Sheet”, Journal of

- International Business and Cultural Studies.

- Eddie Maclaney and Atrill, Peter (2002): Accounting — An Introduction, England Pearson Education Limited, Edinburg Gate Harlow Essex, pp. 140-143

- Federal Government of Nigeria (2003): National Bureau of statistics.

- Flamholtz, E.G. (1971): “A model for human resource valuation: A stochastic process with

- service rewards”, The Accounting Review, pp.253-67.

- Flamholtz, E.G. (1999): Human Resource Accounting: Advances, Concepts, Methods and Applications, Boston, MA: Kluwer Academic Publishers.

- Flamholtz, E.G., Bullen, M.L., & Hua, W. (2002): “Human Resource Accounting: A historical perspective and future implications”, Management Decision, 40 (10), pp.947-54.

Publisher – Google scholar

- Flamholtz, E.G., Bullen, M.L., & Hua, W. (2003): “Measuring the ROI of management development: An application of the stochastic rewards valuation model”, Journal of Human Resource Costing and Accounting, 7 (1-2), pp.21-40.

Publisher – Google Scholar

- Flamholtz, E. G , Kannan-Narasimhan, R., & Bullen, M.L.(2004): “Human Resource Accounting today: Contributions, controversies and conclusions”, Journal of Human Resource Costing & Accounting, 8 (2), pp.23-37.

- Guest, D.E (1997): “Human resource management and performance: A review and research agenda” International Journal of Human Resources Management, 8(3).

Publisher – Google Scholar

- Hartog, Joop (1999): “Behind the Veil of human capital”, in OECD Observer, No. 215 — Jan/Feb 1999

- Hillage, J. and Moralee, J. (1996): “The Return on Investors”, ies Report 314, Brighton, the

- United Kingdom.

- Imeokparia, L.A (2009): “Human Resource Accounting and Intellectual Capital Reporting in Developing Countries: An Empirical Study of Nigeria”, Journal of Management and Entrepreneur, Rosefet Academic Publication, Vol.2, No.1 p.1

- Kaplan, R. and Norton, D (1992): “The Balance Sheet Scorecard — Measures that drive Performance”, Harvard Business Review, Vol.70, No.1.

- Kirkpatrick, D.H (1994): Evaluating training programs, The Four Levels, San Francisco

- Koontz H. O’Donnel and Weihrich H. (1980): Management 7th Edition, New York: McGraw

- Krejcie, R. V; & Morgan, D.W. (1970): “Determining Sample Size for Research Activities”, Educational and Psychological Measurement, 30, 607-610.

- Kumshe, A.M (2012): Human Resources Accounting in Nigeria: An analysis of its practicability, A Ph.D thesis submitted to Postgraduate School Usman Danfodiyo University, Sokoto, Nigeria.

- Kuruvilla, S; Erickson, C.L and Hwang (2001): An assessment of the Singapore Skills Development System: Does It Constitute a Viable Model for Other Developing Nation, Articles & Chapters; Paper 214

- Lall, S.(1999):“Competing with Labour: Skills and Competitiveness in Developing Countries, Developing Policies Department, International Labour Office, Discussion Paper 31

- Lev, B., & Schwartz, A. (1999, January): “The use of the Economic Concept of Human Capital in Financial Statements”, Accounting Review, pp.103-112.

- Likert, R. M. (1967): “The Human Organization: Its Management and Value”, (New York: McGraw-Hill Book Company. Journal of International Business and Cultural Studies.

- Mohammed, Musa Kirfi and Aminu Abdullahi (2012): “Human Capital Accounting: Assessing Possibilities for Domestication of Practice in Nigeria”, Research Journal of Finance and Accounting, Vol. 3, No.10, p.1

- Okafor, G.O (2009): “Disclosure of Human Capital in the Annual Reports of Firms: The Nigerian Accountant’s View”, Certfied National Accountant, July-September

- Olsson, B. (1999): “Measuring personnel through human resource accounting reports: A procedure for management of learning. The hospital sector in Northwest Stockholm”, Journal of Human Resource Costing and Accounting, 4 (1), pp.49-56.

Publisher – Google Scholar

- Olsson, B. (2001: “Annual reporting practices: information about human resources in corporate annual reports in major Swedish companies”, Journal of Human Resource Costing and Accounting, 5 (1).

Publisher – Google Scholar

- Patra R., Khatik, S.K., & Kolhe, M. (2003): Human resource accounting policies and practices: A case study of Bharat Heavy Electricals Limited, Phopal, India”, International Journal of Human Resources Development and Management, 3 (4), pp.285.

Publisher – Google Scholar

- Schwarz, J.L., & Murphy, R. E. (2008): “Human capital metrics: An approach to teaching using data and metrics to design and evaluate management practices”, Journal of Management Education 32 (2), pp.164.

Publisher – Google Scholar

- Tang, T. (2005): “Human Resource Replacement Cost Measures and Usefulness”, Cost engineering, 47(8), pp.70.

- Wagner, C.G (2007): “Valuing a company’s innovators”, The Futurist,41 (5),7

- Weber, M. (1947): The Theory of Social and Economic Organization, New York, and Oxford University Press.

- Wood .F. (1987): Business Accounting I. London: W.C.2E 9AN Pitman Publishing, 128 Long Acre.

- Yesufu, T.M. (2000): The Human Factor in National Development, University of Benin Press and Spectrum Books Ltd.

- hrfolks.com. “Valuation of Human Capital”, JBIMSRetrieved from http://www.sec.gov/rules/proposed/2008/33-8982.pdf. Journal of International Business and Cultural Studies.