Introduction and Literature Review

Generally, the application of IAS/IFRS is a very complex process that can be due to the mandatory accounting regulations, the management’s initiative, the request of the shareholders or the need to have comparative information.

Accounting harmonization is tightly connected to the international accounting standardization and standards can be written in clear language and have the required documentation for the implementation with proper training.

Among the advantages of the international financial harmonization there is the trust inspired by the financial statements prepared according to the International Accounting Standards.

The international harmonization of accounting principles is a topic of rapidly increasing importance as the jet age brings the financial centres of the world within a few hours of each other, and improved means of data processing and of communication make the exchange of information almost instantaneous. Accountancy as the common language of business must keep up with this accelerated pace in order to maintain meaningful financial reporting (Barr, 1967).

According to Nobes and Parker (2008), ‘Harmonization’ is a process of increasing the compatibility of accounting practices by setting bounds to their degree of variation. ‘Harmony’ is the state where compatibility has been achieved. ‘Standardization’ appears to imply working towards a more rigid and narrow set of rules. ‘Harmonization’ and ‘standardization’ have often been used interchangeably. However, standardization implies a narrowing down to one policy for any accounting topic, whereas harmonization implies that differences could be allowed to remain as long as the users of financial statements have a means of getting similar information from different statements. Harmonization is most useful when it concerns similar users who receive information from companies in different countries. However there are some obstacles to harmonization such as the size of the present differences between the accounting practices of different countries, the lack of an international regulatory agency, the nationalism, the effect of ‘economic consequences’ on accounting standards.

Deegan (2009) provides theoretical explanations as to why, in the absence of efforts to globally harmonize or standardize accounting practices, accounting regulations and practices could be expected to vary between different countries. So, between countries there are various differences, such as differences in culture, religions as a subset of culture, legal systems, financing systems, taxation systems, the strength of the accounting profession and accidents of history, which will also influence the accounting systems.

On the other hand, Beke (2010) describes and summarizes how the harmonized international accounting system can promote business decisions and influence economic environment. According to this, the unified, harmonized accounting system will lead to new types of analysis and data, furthermore with the possible integration of new indicators from the business management of certain countries. He classified the accounting systems, and in his opinion this classification should contribute to an improved understanding of: the extent to which national accounting systems are similar to or different from each other, the pattern of development of individual national systems with respect to each other and their potential for change, the reasons why some national systems have a dominant influence while others do not. The reason for differences in accounting principles between certain nations could be that they vary in the level of economic development, in the legal system, in the taxation system, in the intensity of capital market, so as in the level of inflation, in the typical methods of financing an enterprise, in the shareholder background, finally in the political and cultural traits, factors that are influencing accounting harmonization. Accounting diversity causes a series of problems such as the preparation of consolidated financial statements by companies with foreign operations, assessing to foreign capital markets, comparability of financial statements, the lack of high-quality accounting information in some parts of the world.

There are several studies analyzing harmonization in different countries. The commitment by the European Union to mandate the use of IFRS for certain EU entities has generated a series of changes in global accounting that according to Gielen and Hegarty (2007) can only be described as revolutionary. They have shown, studying the case of nine EU Member States: Belgium, Denmark, Estonia, France, Germany, Luxembourg, Poland, The Netherlands, United Kingdom that strong statutory relationship between financial and tax accounting may have negative consequences, resulting in financial and/or tax accounting systems failing to achieve their objectives. However, a few additional considerations may help policymakers in evaluating the appropriate degree of relationship between tax and financial accounting given the circumstance of their Member State: the Member State’s current situation (historical/tradition and economic); the case for associating tax and financial accounting.

Vallisova and Dvorakova (2011) detected the main differences between the Czech accounting system and IAS/IFRS and recovered further way of Czech accounting harmonization according to accounting global trends. The System of IAS/IFRS is from the beginning the purely accounting system and a range of financial and tax accounting are strictly separated. That is no longer in the Czech Republic, where financial profit is used as the basis for tax calculating and Czech accounting law is closely linked to the tax system.

Wysłocka (2008) presents the progress of harmonization of regulations concerning accounting, especially in Poland and describes functions performed by the accounting in market economy: reporting, evidential, optimizing, control, analytical. A relevant obstacle on this way is a high level of severity of Polish tax law.

Albu et al (2011) investigates the inter-play between institutions, routines and politics in the Romanian context and highlights the complexity of accounting change in an emerging country. According to them, differences in the way IFRS will be applied in Romania and in other countries will remain, because of the environmental factors affecting the accounting system such as the characteristics of a code-law country, a dominant position of the State and a reduced importance of the accounting profession.

The benefits of harmonization

The harmony is desired since it brings in more benefits and this mystery has shown all its clues. Each regulatory change had an important role in this process. The professional accountant has a dual role to play in relation to the set of alternatives that resulted after a number of changes to both accounting regulations and accounting standards.

The decision of adopting the IAS/IFRS should be based on a thorough investigation regarding related costs and benefits and whether this decision was justified from a cost-benefit point of view.

Is it important to ensure that investors or managers take the proper decisions? Of course it is and factors in the situation that may trigger biases that the decision makers have need to be thoroughly analyzed.

The auditors rely only to a certain extent on the honesty of directors and no amount of regulation is necessarily going to ensure that dishonest people are going to be honest.

The application of IAS/IFRS can be due to the mandatory accounting regulations, the management’s initiative, the request of the shareholders or the need to have comparative information.

Switching to IAS/IFRS can also generate costs related to training of personnel, double reporting, consulting services or even adjustment of computer information system, but the advantages of harmonization are multiple.

These costs should have been budgeted for even though the change of the relevant legislation would have been made fast.

All in all, the implementation of IAS/IFRS reporting offers a number of advantages:

-it offers relevant information to investors and therefore is an appropriate accounting system for listed companies

-it permits the access to the foreign financing market

-when in the process of decision making, the managers are offered a good information resource.

It is important to look at accounting harmonization as improvement and assess the accounting benefits in terms of whether new accounting practices satisfy better the interests of the users of economic information, and present the information in an understandable and fair way.

Different people may have different views regarding international accounting, which depend on the accounting practices used in the past and the construction of the concept of professionalism. Investigating the evolution and history of accounting brings into our attention the limits of harmonization.

In order to demonstrate the importance of harmonization, but also its limits we have distributed a questionnaire to a sample of professionals, which determines their position regarding the benefits of harmonization. The respondents completed and returned 20 surveys, based on which we performed an analysis of results using a scale from 1 to 5 (1 – totally disagree, 2 – disagree, 3 – neither agree nor disagree, 4 – agree, 5 – totally agree). The primary purpose of the study was to determine the degree of importance associated with the process of harmonization.

The questions based on which the results were analyzed are the following:

- Does the new projects related to the changes in the accounting policies have a contribution to the enhancement of accounting harmonization?

- Does the consistent application of accounting policies contribute to the true and fair view of the financial position and the performance results of an entity?

- Can the process of harmonization lead to a development of the techniques and practices of creative accounting?

- Are the needs of regulators limiting the process of harmonization?

- Can the accountants improve the process of harmonization by actively presenting comparative analysis between the situation before and after harmonization?

The results of the questionnaire are presented below:

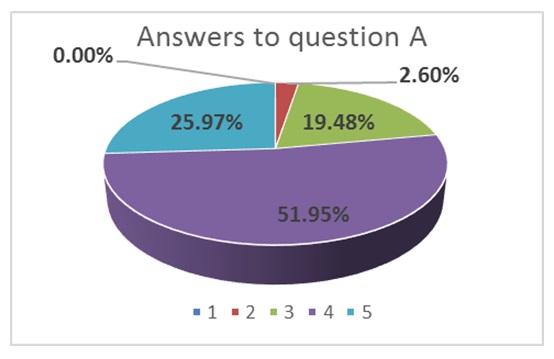

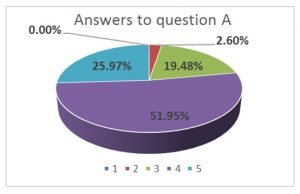

Fig.1: The results for question A (based on the answers received related to the

changes in the accounting policies);

Source: own analysis

51.95% of the interviewed professionals believe that new projects related to the changes in the accounting policies have a contribution to the enhancement of accounting harmonization, while only 2.6% are reluctant to these due to the flexibility involved in and the chances of making the wrong decision.

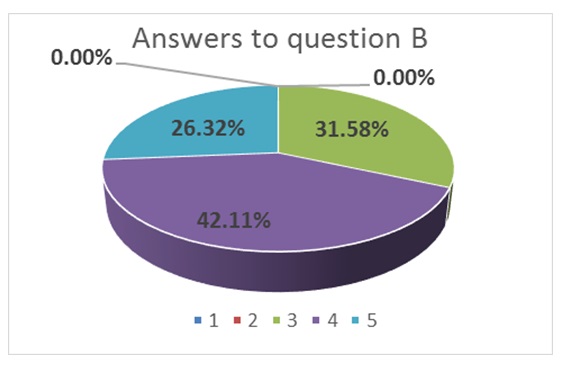

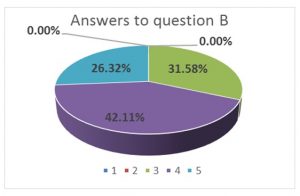

Fig.2: The results for question B (based on the answers received related to the consistent application of accounting policies)

Source: own analysis

68.42% of the subjects agree the consistent application of accounting policies contributes to the true and fair view of the financial position and the performance results of an entity. This result might have a positive impact, since it can contribute to building proper measures to manage the suitable accounting policies in order to reflect the true achieved performance and not a fictional one.

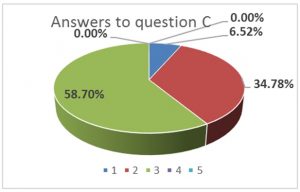

Fig.3: The results for question C (based on the answers received related to the process of harmonization)

Source: own analysis

58.7% of the questioned professionals neither agree nor disagree with the fact that the process of harmonization could lead to a development of the techniques and practices of creative accounting, while 34.78% of the subjects disagree with this fact since the financial statements prepared in accordance with the local generally accepted accounting rules modified after harmonization proved to reflect the true and fair view of the financial statements.

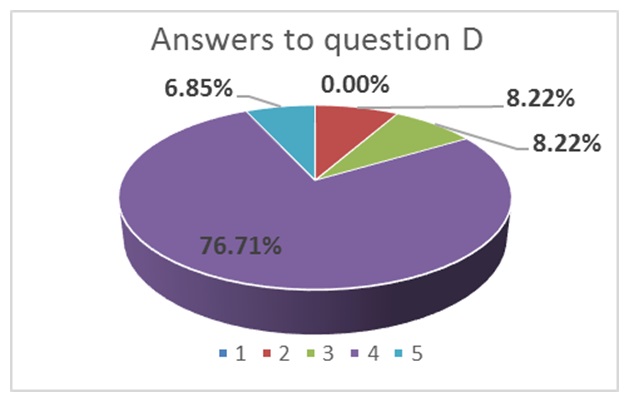

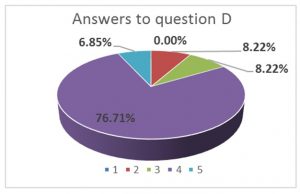

Fig.4: The results for question D (based on the answers received related to the limits of the process of harmonization)

Source: own analysis

84.56% of the subjects agree with the fact that the needs of regulators are limiting the process of harmonization since the primary needs to be satisfied are those of the financial information users.

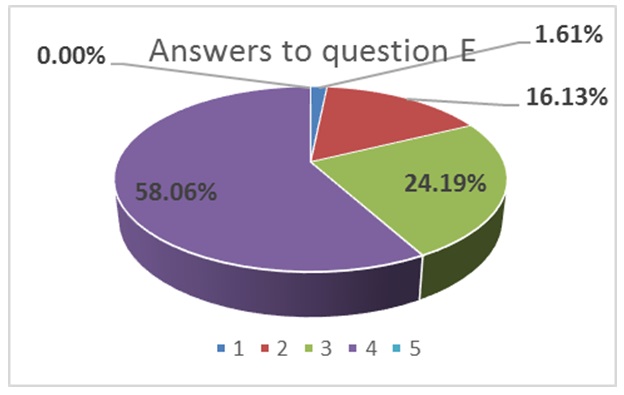

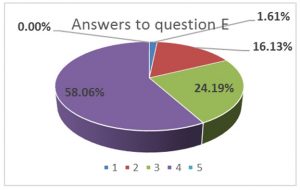

Fig.5: The results for question E (based on the answers received related to the improvements of the process of harmonization)

Source: own analysis

From the answers received from the respondents, most of the professionals believe that they play a very significant role in the process of harmonization by actively presenting comparative analysis between the situation before and after harmonization.

58.06% of the questioned people believe that these analyses have a contribution to the enhancement of accounting harmonization, while 24.19% neither agree nor disagree with this statement.

Tax implications upon the process of harmonization

The accounting harmonization process begins to reduce the differences between the accounting information provided by the companies from different countries. A cause for the differences between the countries is the tax system, and the degree of connection between the accounting and taxation.

There are countries that apply an Anglo-Saxon system for the accounting practices, which is characterised by a high degree of disconnection between the accounting and taxation and countries that apply a European-Continental System which is characterised by a close connection between accounting and taxation.

Keeping separate tax and accounting records is in accordance with the financial needs of the companies and the link between tax and financial reporting rules can be used in favour of the company in order to create book-tax conformity.

Our research is concentrated on the impact of accounting harmonization and since taxation refers to fiscal policies in different context, situation and sector, its implications have to be measured accordingly.

It is impossible to split accounting from taxation because each one has an influence over the other and the interconnection has to be maintained.

The context in which the impact will be measured is Romanian legislation, which according to its accounting history started from European-Continental influences and finished at the moment by applying for a part of the companies the Anglo-Saxon influences. The professional judgment is important in applying both the accounting and taxation rules.

Conclusion

The process of harmonization can help in the construction of a better quality financial reporting system. The main findings focus on the important role each professional can have by following the opportunity to apply the stable, suitable accounting policies and by performing a thorough analysis that could assist investors and decision makers. The results reveal the fact that more than a half of the professionals questioned agree that the true and fair view of the financial position of a company is influenced by the consistent application of accounting policies, therefore this is a proof that the professionals are aware that they have an important role in building and managing the suitable accounting policies. Also, more than a half of the subjects believe that by presenting comparative analysis between the situation before and after harmonization, this will improve the process of harmonization. In this way their role in the process of harmonization is also important. The fact that the majority of the subjects believe that the needs of regulators are limiting the process of harmonization shows that they are aware that besides the fact that their role is important in the process of harmonization, this role is limited by the regulators. This limitation can influence the accounting policies, if we are looking from the point of view of the techniques and practices of creative accounting, which can be developed by some professionals. Therefore, more than a half of the questioned professionals neither agree nor disagree with the fact that the process of harmonization could lead to a development of the techniques and practices of creative accounting.

We can conclude that the increase in the relevance of the financial information will be more consistent after the harmonization process is complete and the IFRS adoption is realized worldwide.

If the accounting harmonization is successfully completed, there is a need to analyze what the taxation harmonization will imply in the future. We will further analyse the answers separately between auditors and accountants, by increasing the sample and aiming to obtain sufficient and appropriate evidence in order to sustain that the harmonization process will be complete once all the related parties act accordingly and work together in accomplishing this. Furthermore, regulation alone will not produce uniform financial reports because the requirements are much more complex since the reality is complex and different for each company in place.

References

- Albu, N., Albu, C.N., Bunea, S., Calu, D.A., Gîrbină, M.M. (2011), “A story about IAS/IFRS implementation in Romania: An institutional and structuration theory perspective”, Journal of Accounting in Emerging Economies, Vol. 1, No.1, 2011, pp 76-100

Google Scholar

- Barr A. (1967), The international Harmonization of Accounting Principles, 9th International Congress of Accountants from Paris, pp 1-21

- Beke J. (2010), International Accounting Harmonization: Evidence from Europe, International Business and Management, Vol. 1, No. 1, pp. 48-61

Google Scholar

- Deegan C. (2009), Financial Accounting Theory, McGraw-Hill

- Gielen F., Hegarty J. (2007), An accounting and taxation conundrum – A pan-european perspective on tax accounting implications of IFRS adoption, The World Bank Centre for Financial Reporting Reform, 2007

- Nobes C., Parker R. (2008), Comparative international accounting, 10th edition, Prentice Hall, London

Google Scholar

- Vallisova L., Dvorakova L. (2011), Development and evaluation of accounting harmonization processes in the Czech Republic with international accounting standards/international financial reporting standards, Annals of DAAAM for 2011 & Proceedings of the 22nd International DAAAM Symposium, Vol. 22, No. 1, pp 951-952

Google Scholar

- Wysłocka E. (2008), Harmonization and standardization of the accounting and its functions, Univ. Apulensis Ser. Oeconomica, vol. 1, no. 10