1ESSEC of Tunis – Tunisia – LIGUE laboratory LR99ES24 and Dr. In Accounting – IAE of Nice-Univ. of Nice Sophia Antipolys, France

1Dr. In Accounting – ISCAE of Tunis – Univ. of Manouba, ISCAE, Campus Universitaire Manouba, 2010, Tunisia

1Professor of Accounting at ESSEC of Tunis, Tunis, Tunisia

2ESSEC of Tunis – Tunisia

Volume 2023,

Article ID 550358,

IBIMA Business Review,

20 pages,

DOI: https://doi.org/10.5171/2023.550358

Received date: 10 May 2023; Accepted date: 22 August 2023; Published date: 30 October 2023

Academic Editor: Jamila Oukharijane

Cite this Article as:

Wissal BEN LETAIFA and WISSAL BEN HADJ SALEM (2023)," The Digitalization of Accounting Firms: Survey Research from Tunisia", IBIMA Business Review, Vol. 2023 (2023), Article ID 550358, https://doi.org/10.5171/2023.550358

Research Motivation -The purpose of this paper is to analyze the impact of digitalization on accounting firms by focusing on the strategies implemented by heads of accounting firms to react to digitization and not be replaced. Our study also makes it possible to identify the main factors of resilience of client companies of accounting firms which helped them to overcome the covid crisis. In our knowledge, the Tunisian literature has never exposed these determinants with the use of content analysis in Tunisia. Design/Methodology –The investigation was conducted via a qualitative methodology through the content analysis of telephone survey and google forms surveys. Main Findings and Implications – The findings reveal that digitization represents a technological progress that has turned the accountant’s business worldwide in times of the covid crisis. It was a lifeline that helped clients/companies survive in order to overcome the covid crisis. However, the digitization of accounting firms has advantages and disadvantages. In sum, this paper tries to fill a gap in the corporate governance literature and provides meaningful information on the impact of digitization on the accountant’s business in the covid period.

“It is important today to study what new emerging forms of control are associated with the digitalization of organizations in order to determine their implications for behavior” (Ciampi and Berland, 2019). According to this quote, it appears that the concept of digitalization is not new. Its origins go back almost 30 years. In the 1990s, the progressive popularity of the personal computer (PC, or «personal computer»), and of course the Internet in companies, gave rise to this concept of «digitalization».

The 2000s marked a new connotation of this concept with the arrival of new tools such as smartphones and mobile Internet, which ensure communication and information sharing. In early 2010, with the impact of the global economic downturn, the digital transformation became a clear way to improve performance and ensure sustainability. All human organizations (companies, institutions, associations) are gradually becoming aware of the importance of this issue.

Starting in 2015, the SaaS software boom increases the importance of technology in every business line of the company; this is in particular the time of the explosion of collaborative tools that come to provide work to many customers (team communication, project management, co-editing of documents, electronic signature, etc.). As a result, digitalization appears to be a logical follow-up to technological change, and more particularly to the Internet and computing. It is in fact a tool that aims to transform traditional processes, objects, or professions through digital technologies in order to make them more efficient. This tool has transformed the reality of many professions.

Within accounting firms, for example, there has been talk about digitalization to (1) free up human time for higher value-added tasks, (2) place IT tools for lower value-added tasks, (3) modernize firms by making greater use of cloud applications, (4) adopt lean management, (5) use collaborative tools to increase productivity, (6) diversify offerings, and (7) digitize the offer through the development of a portal accessible to several users and for several purposes and needs.

Nevertheless, digitalization presents several challenges. First, the public accountant must not abandon his clients alone in the face of their decisions. The second challenge is for the public accountant to position himself as an administrative and financial director outside the company. The third issue is the hyper particularity of the services since several clients expect a specification of the relationship with their public accountant, directly related to the question: is it an assistance or aposteriori control? The fourth challenge is to connect firms to the practices of young employees through mobile access, automation technologies and other digital tools.

Moreover, the consequences of digitalization are numerous. Accountants are no longer required to perform a number of slow tasks that they had to perform upstream. Indeed, accountants, the company’s first partners, are also seeing their world evolve and must adapt to meet the demands and new issues of their clients. Of course, employees will not disappear from the firm. Their profession will simply adjust to the new needs of the clientele.

As accounting firms grow in an increasingly competitive world, the emergence of players from the digital world, audit assignments will be carried out by software that will identify risk areas, due diligence and material misstatement, and will be addressed directly to business leaders. That said, it is reassuring to think that digital will not exhale the human factor. Better still, the more digital is the present, the more important the staffwill be. The human being will then have to find a place where he is not in competition with the machine.

We believe that software is not a direct competitor of firms because it does not support the production of accounting statements without a human click point. The public accountant thus becomes a key subject of support for the business lines, and not only the finance department, with a location much closer to the consulting business lines. Taking all these points into account, our problem is to ask the following question: will the profession of the accountant and the accountant disappear with the digital transformation?

To address this issue, we will examine in a first section the theoretical background on the role of digitalization in the resilience of societies in times of crisis, and its impact on the profession of the accountant. Then, in a second section, we will discuss the literature review. In the third section, we will describe our methodology, before stating our results in the fourth section. The fifth section will be used to conclude and present our research limitations.

Theoretical Background on Digitization

Theoretical framework on the role of digitalization in the resilience of societies especially during the COVID-19 health crisis

Some companies are more reputed than others to survive crises. According to Calabro et al. (2021), family businesses are considered resilient businesses with a variety of tools to survive crises. In times of crisis, the management style adapts whether it is in family businesses or not by requiring all employees to stay at home and no longer carry out their professional activities naturally. Business leaders are no longer able to receive documents from their clients from hand to hand and the employees’ challenge was to know how to guide a person to live and work better in the health situation or by teleworking.

These impacts also affect accounting firms, which play a vital role in the operation and development of businesses. The challenge for accounting firms and auditors is that they are on the front line to help organizations and managers cope with the difficulties they face. The Statutory Auditor is therefore asked to estimate the degree of difficulty in order to respect the fundamental principle of business continuity and to take the necessary measures to manage the situation.

The relationship with business leaders has changed and turned to counseling and coaching. It was more a question of managing the stress of investors worried by the situation. The challenge was therefore to guarantee, but also to protect employees while making them available for effective monitoring in order to cope with the succession of decrees, and malfunctions.

The availability, agility, and adaptability to the situation supported the relational dimension between business leaders and accountants. It should be noted that digitalization has ensured remote working through the use of new digital tools, including the use of new accounting entry software. Thanks to these digital tools, time and productivity have been saved. Faced with urgent customer expectations, the accountant found himself faced with a sensitive demand that requires him to adapt and an ability to solve complex problems in a faster manner. As a result, the accountant has added value through his technical accounting and tax knowledge, but also through his awareness of the importance of these digital tools.

To do this, certain skills are necessary to work well with the digitized tool. In this sense, the accountant must know how to observe, prevent and explain the risks and the innovations observed in the market. He must explain to his collaborators the strategy to be adopted to face the threats of the next day. It must mobilize information as opportunities and build a team with a strong digital quotient.

The literature review on digitalization

The literature review reveals that some researchers have studied the impact of digitalization on business performance, such as Aral and Weill (2007), Chae et al. (2014) and Deltour et al.(2014). They found that business performance improves with digitalization.Other researchers have investigated the relationship between digitalization of banking services and business performance (Musabegovité etal.2021). The digitalization of e-services has also been studied by Kahveci and Wolfs (2018) in order to analyze the impact of bank digitalization on performance.

Let’s look at the digital tools offered by some accounting firms that are considered very useful to clients. It should be noted that various digital tools are offered by public accounting firms to initiate discussions with potential clients of the public accounting firm and are used to support clients online.

These tools are different from traditional communication services such as phone calls and emails. They are materialized by chats for real-time communication with potential customers. This communication is considered very user-friendly and is particularly appreciated by users.

Various other accounting software are available online and are used by clients and accountants to update remotely accessible accounting. Simply connect via the Internet, either by smartphone, PC or tablet to update the accounting database securely. This action allows the accountant to focus on his audit mission and on more complex tasks.

These software-experts in accounting are available in order to digitize all documents in paper format, allow an electronic archiving of all the accounting and tax documentation of the client company. In this way, they facilitate the search and update and file any document by any data subject. Other software programs, such as CRM, improve the communication between the accountant and his client by transmitting information that makes it possible to optimize time and manage several clients at the same time.

Digitalization has a strong impact on the accountant’s profession. It is seen as an opportunity as these firms have to adapt to digital change by acquiring the latest technologies and updating software to automate tasks and save time that was previously very highly notorious. The use of robotics and artificial intelligence are replacing manual and mostly repetitive accounting activities. In this way, there is more opportunity for accountants who have more time to focus on tasks with higher added value.

Digitalization allows the restructuring of audit engagements. Indeed, for accounting engagements, accountants adopt software packages (professional software), better organize audit engagements, and eliminate accounting breakdowns that are already embedded in this software or through the use of new, more digitized tools such as extranet. Digitalization improves the efficiency and effectiveness of audit services. The use of high-performance digital tools provides the auditor with the speed with which his assignments are carried out and the efficient organization of his work files through their electronic filing, which allows him to refer to them without wasting time. The use of software facilitates the control and the electronic work allows reaching competitive execution times.

Advisory activities are organized on the web, as are publication and communication on the Internet. The accountant can communicate with his clients by text, videos, animated presentations, webcasts. It can even make use of tele-tax reporting and ensure continuous training via the web. In this way, all accounting and consulting activities migrate to the web. The accountant must choose his employees according to their knowledge and their accounting as well as digital skills. The latter are monitored on the basis of the achievement of objectives and not on the achievement of the work. It is the employees who set their working methods to achieve the overall objective of the audit engagement. They can work from home by choosing flexible working hours since work organization is digitalized. Employees can choose to become independent and not remain employees of the accounting firm all the time. They can enjoy their free time and work with several clients by negotiating high compensation with their clients. The time savings generated by digital tools can even reduce fixed costs and be efficient.

Research Methodology

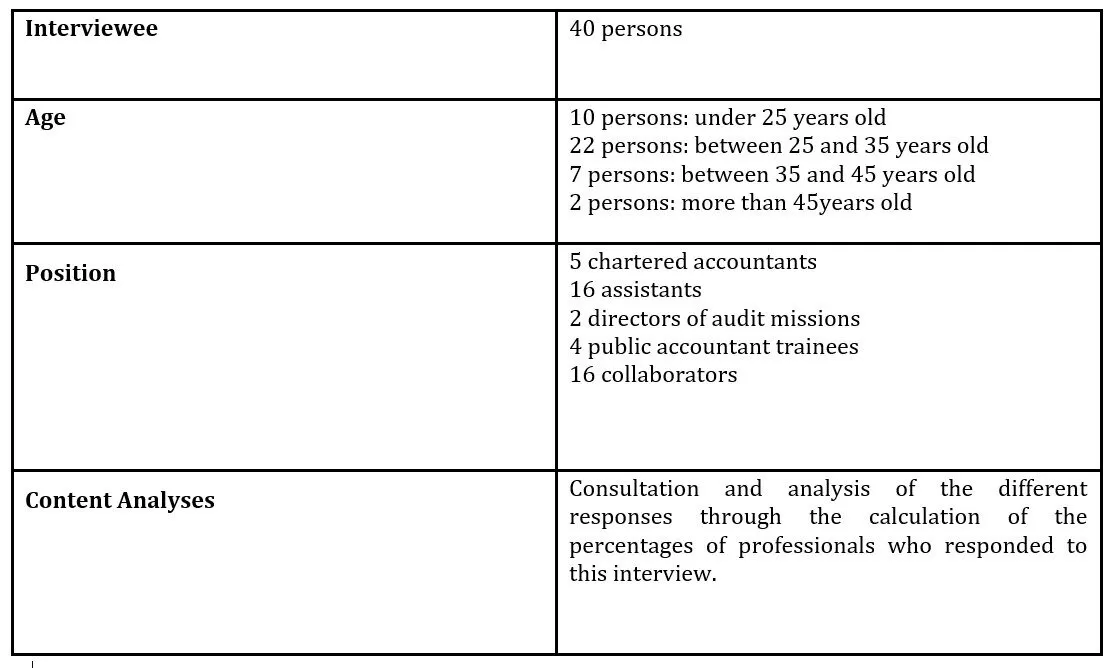

Presentation of the telephone survey

Sample

In this study, the author used a telephone survey of 25 accountants from different regions of Tunisia. This survey made it possible to listen to the various opinions of these accounting professionals about the importance of digital tools and the impact of digitalization within accounting firms. So, they were led by questionnaire with six questions and each telephone interview lasted about half an hour. We add that questions are made with regard to the literature in digitalization and resilience of SME.

Questionnaires

In our work, we do not ask the question “will the profession of the accountant disappear with the digital transformation?” but we focused on what adds the digital transformation to the accountant business. We received 25 responses to the following questions:

1/ What is your position within the firm?

2/ In your opinion, is the accounting profession part of a process of digital transformation?

3/ Do you think that the digitalization of the accounting profession is an element that improves the development of employees?

4/ Do you think the accounting transition process is conducive to improving the accounting environment?

5/ Are you able to spend a budget to start training on the use of software?

6/What are some of the challenges you may encounter in using new software?

Statistical Tools

We build our results by means of representative diagrams which allow bettering the displaying of our results. We have used descriptive statistics for our empirical work.

Results

Results of the direct survey of respondents

We will present the results of the qualitative study that was produced by the five questions in the survey conducted directly with respondents

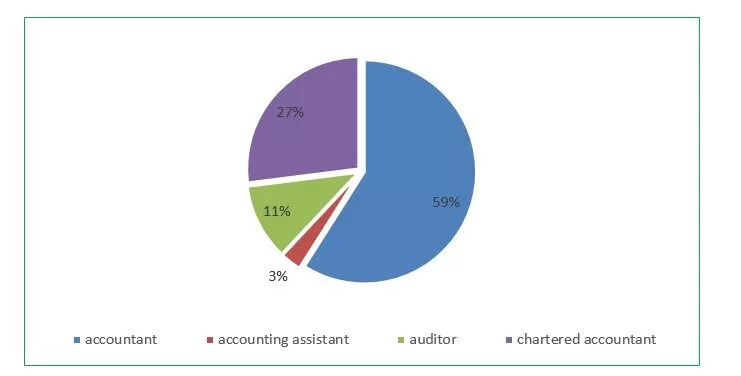

What is your position within the firm?

3% of the respondents interviewed in the firms through this survey are accounting assistants, 11% of the respondents are auditors, 27% of the respondents are chartered accountants and 59% of the respondents are accountants.

Fig 1. % Survey results of firm positions

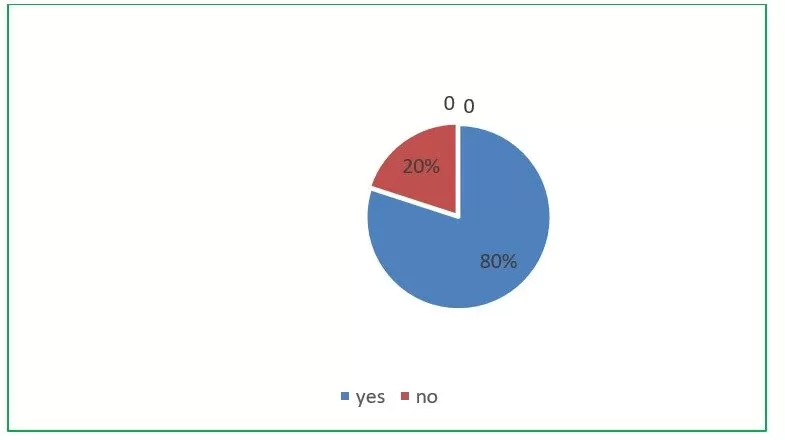

In your opinion, is the accounting profession part of a digital transformation process?

The results show that 20% of the respondents in this survey believe that the accounting profession isn’t part of a digital transformation, unlike 80% of those interviewed who really think so.

Fig 2. Professional opinion on the digital transformation of the accounting profession

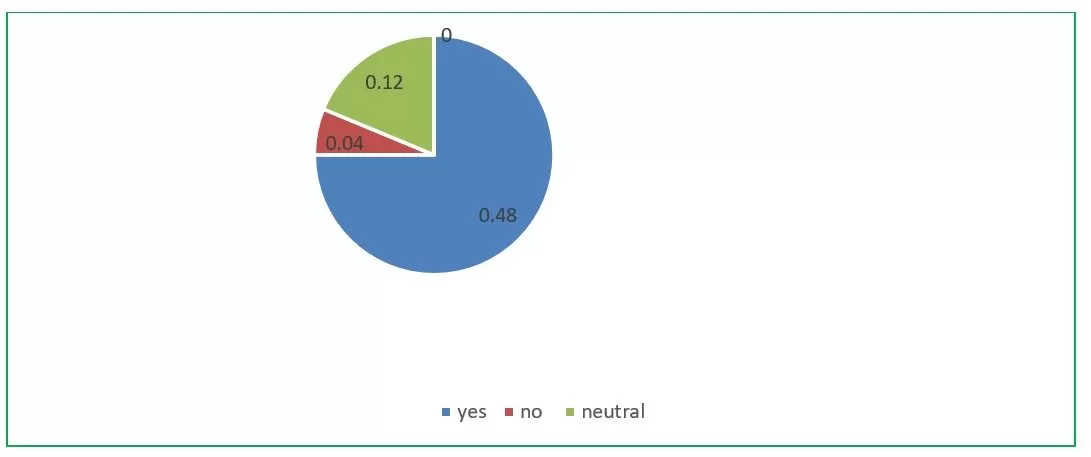

Do you think that the digitalization of the accounting profession is an element that improves the development of employees?

The results show that 4% of the respondents think that the digitalization of the accounting profession doesn’t improve the development of employees within accounting firms, while 12% of the respondents do not think so and 48% are neutral towards this observation.

Fig 3. The opinions of professionals regarding digitalisation as a factor that improves employee savings

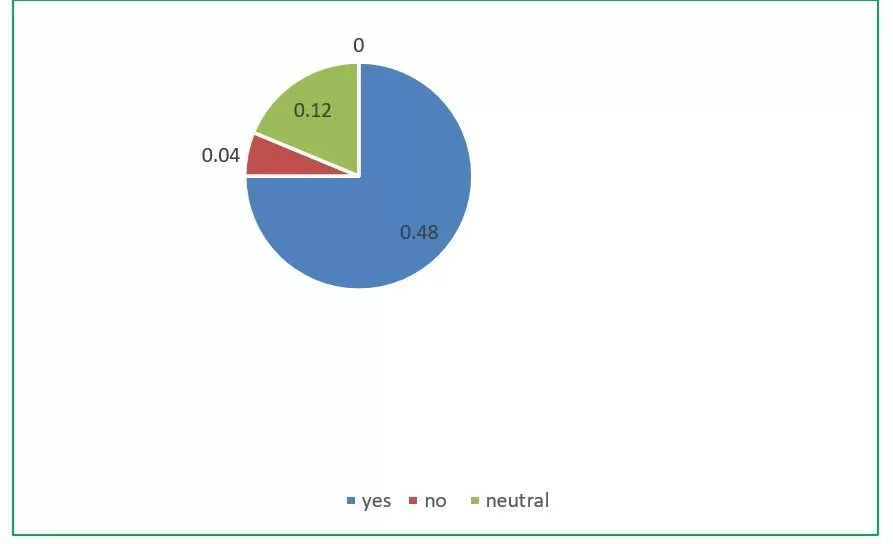

Do you think the accounting transition process is conducive to improving the accounting environment?

The results show that 4% of the respondents believe that the accounting transition process does not improve the accounting environment, while 48% of the respondents think that the accounting transition process improves the accounting environment and 12% are neutral towards this observation.

Fig 4. The opinions of professionals regarding digitalization as a factor that improves accounting environment

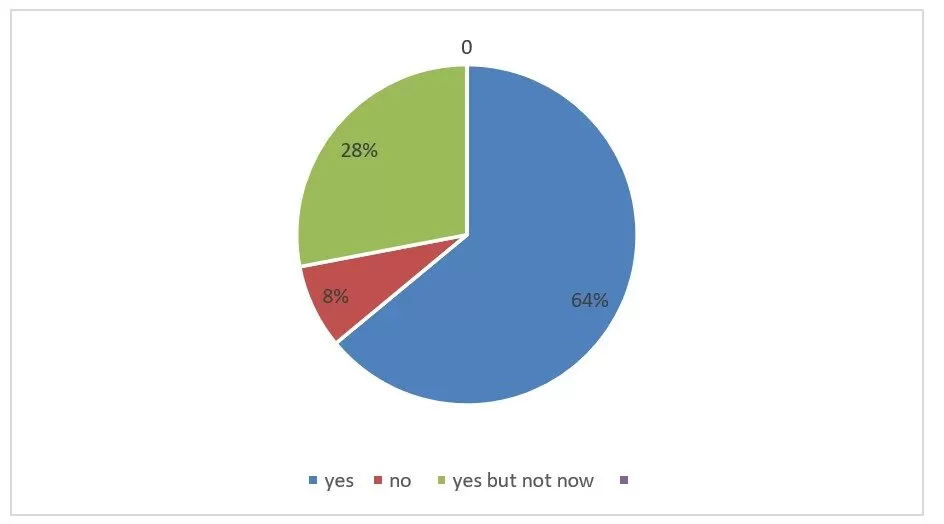

If so, are you able to spend a budget to start training on the use of software?

The results show that for the 48% who answered positively the previous question, 8% are not willing to spend a budget to do training on the use of software, 28% are in favor of training on the use of software but not now and 64% of these respondents reply that they are able to spend a budget to start training on the use of software.

Fig 5. Professional opinions on the budget for training on the use of new software

Presentation of Google Forms Survey Results

Questionnaire Format

The survey was conducted using a questionnaire containing 16 questions. It was built on the basis of theoretical study and literature review. We employed the same methodology of the content analysis of Oussi et al.(2019).

Sample

The survey focuses on the perception of accountants regarding the adoption of the digitalization and their impact within accounting firms. As a result, our questionnaire is sent to a sample of professionals in the accounting field which are always with all novelty and development enriched from the theoretical as well as practical point of view.

The questionnaire was released electronically. Some people did not respond to our questionnaire, which significantly reduced the sample size and the subsequent reliability of the results.

Statistical Tools

We present our results by means of representative diagrams and histograms that will allow better visualization of the results. In addition, we have used the descriptive statistical tool for our empirical work.

Analysis of the results obtained

Our survey is based on 40 questionnaires received from Tunisian interviewees. We describe briefly the age andthe position for the interviewees and the method employed.

Results are presented below for every question.

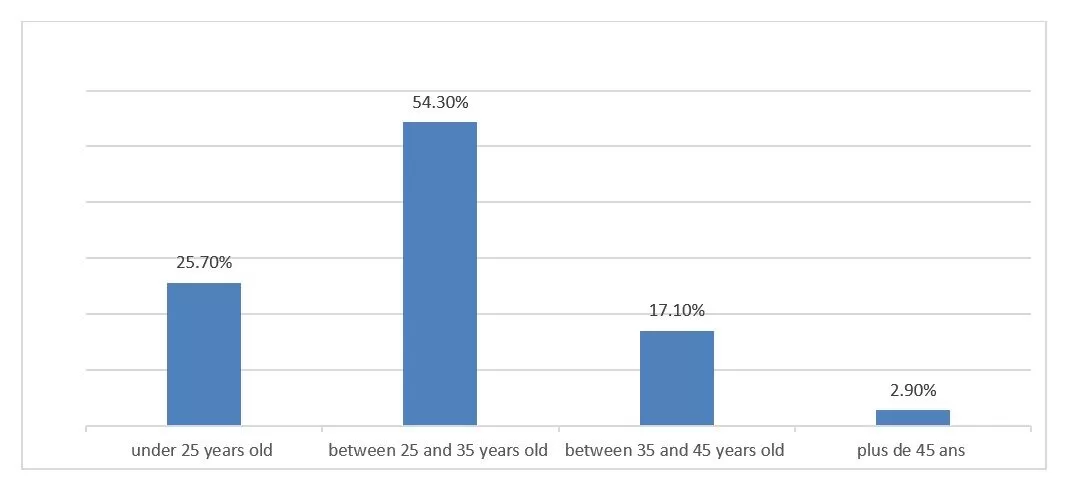

How old are you?

It appears that 25.7% of the respondents are under 25, 54.3% are in the 25-35 age group, 17.10% are in the 35-45 age group and 4.5% are over 45.

Fig 6. Age intervals of professionals

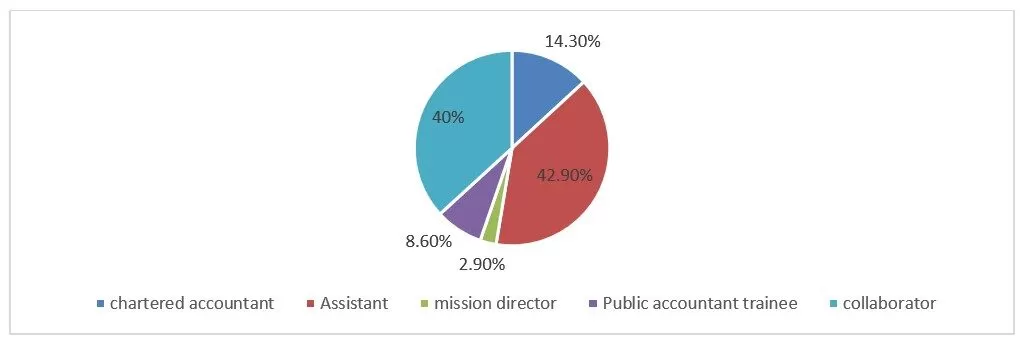

What is your position within your firm?

Concerning the positions occupied by respondents, the results show that 42.9% of the respondents are assistants, 40% of the respondents are collaborators, 14.3% of the respondents are chartered accountants, 8.6% of the respondents are public accountant trainees and 2.9% of the respondents are directors of audit missions.

Fig 7. Percentage (%) of positions held

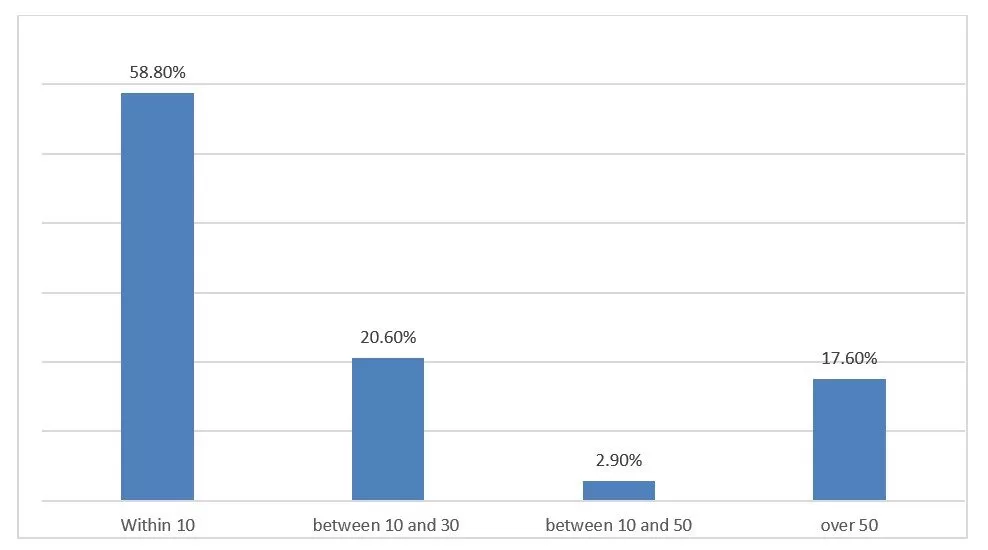

How many employees does your practice have?

Concerning the percentages of employees employed by respondents, the results show that 17,6% of the respondents are employees in firms with more than 50 employees, 2.9% of the respondents are employees in firms with between 10 and 50 employees, 20.6% of the respondents are employees in firms with between 10 and 30 employees and 58.8% of the respondents are employees in firms with fewer than 10 employees.

Fig 8. Percentage (%) of employees in firms

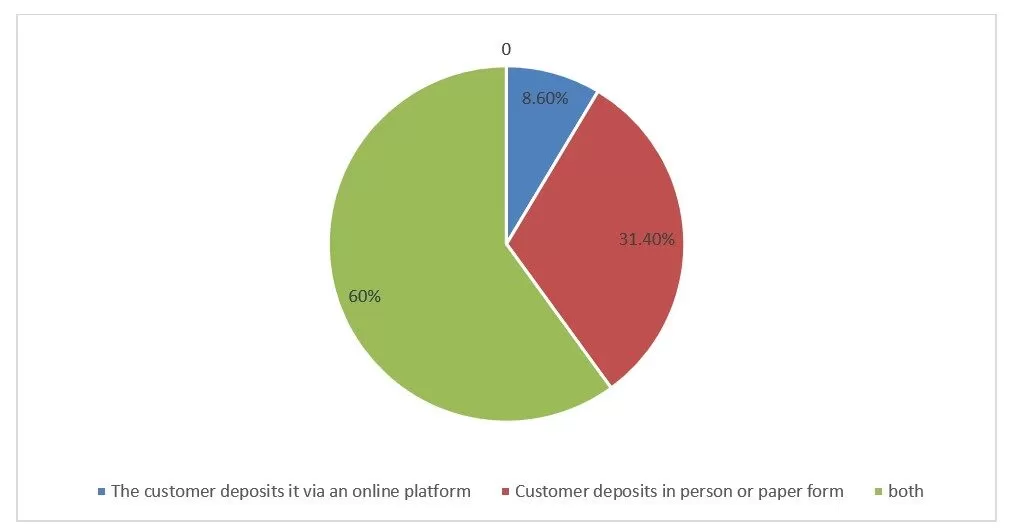

How do you restore your clients’ accounting?

Regarding the accounting deposit percentages by clients, the results show that 60% of the respondents file their accounts both on paper and on the online platform of accounting firms that audit them, 31% of the respondents file their accounting on paper with the accounting firms that audit them, while 8.6% deposit their accounting on the online platform.

Fig 9. Percentage (%) the establishment of customer accounts

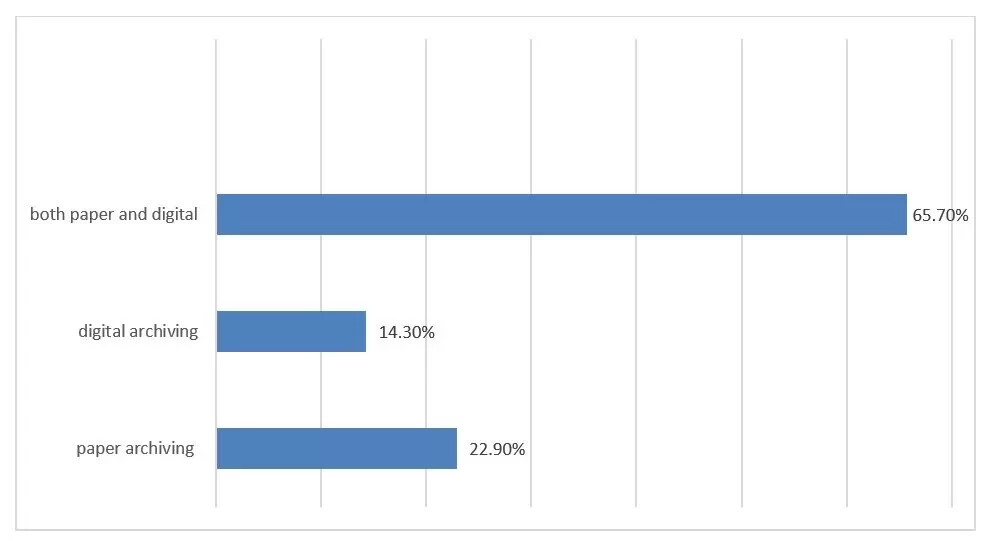

How do you archive accounting documents?

Concerning the archiving of accounts filed by clients, the results show that 65.70% of the responding clients archive their accounts in paper and online, compared to 22.9% who archive in paper only, and 14.3% of the responding clients that digitally archive their accounts.

Fig 10. Archiving of accounting documents

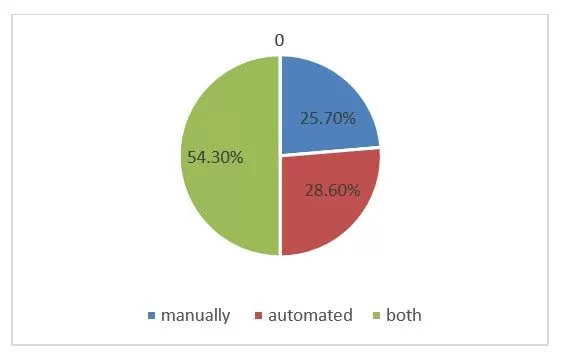

How do you perform your accounting production?

Regarding the production of accounting documents filed by clients, the results show that 54.30% of the responding clients produce their accounts both manually and via software, against 28.6% of the responding clients who produce automated accounting, and 25.70% of the respondents who produce their accounting manually.

Fig 11. Accounting production

If your accounting production is automated, what digital tools have you adopted?

The respondents’ answers show that the software used by clients of accounting firms are: Sage model import and export, Cielcompta, ERP, MC office de télé déclaration fiscale, Isi compta, Sharepoint and Ciel future and soft.

How do these digital tools help you in your daily work?

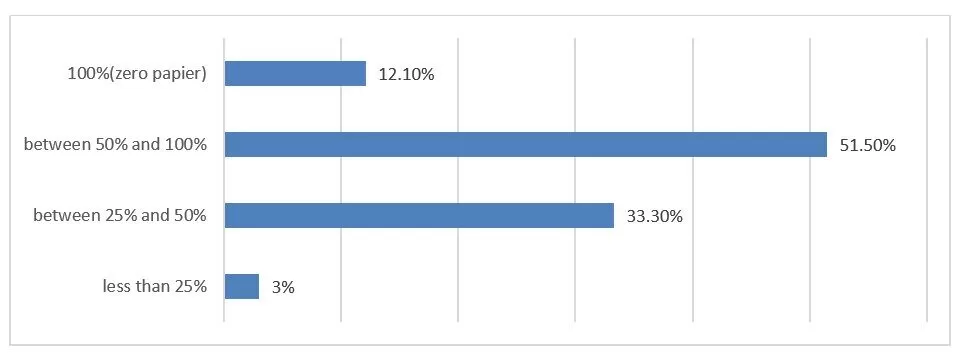

The results show that 12.10% of the respondents use accounting documents in digital format only (i.e., 0 paper), 51.50% of the respondents use digital tools between 50% and 100% in their daily work, 33.30% of the clients use digital tools between 25% and 50% in their daily work, and 3% of the respondents use digital tools less than 25% intheir daily work.

Fig 12. The opinions of professionals regarding the importance of digital tools in their daily work

Can you and your clients remotely access your firm’s IT resources?

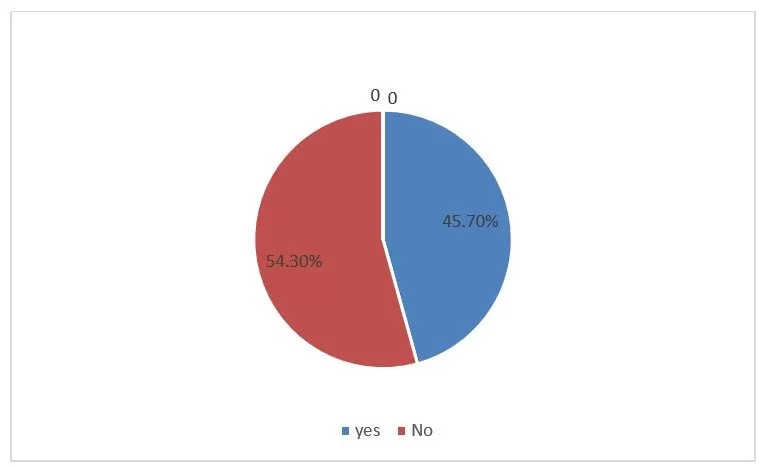

The results show that 54.3% of the respondents cannot remotely access the IT resources of the accounting firm for lack of digital tools against 45.7% who confirm being able to access the firm’s IT resources.

Fig 13. Remote access to the firm’s IT resources

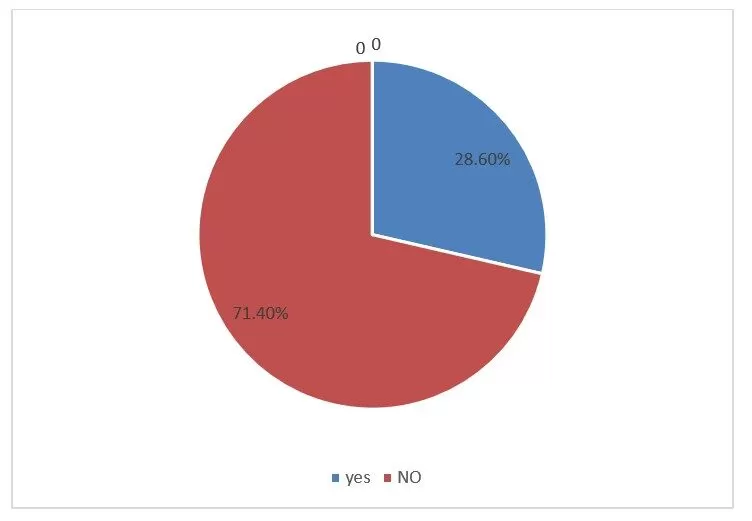

Have you taken any training on the use of digital tools?

The results show that 28,6% of the respondents took training on the use of digital technology, compared to 71.40% who did not take training on the use of digital tools.

Fig 14. The opinion of professionals regarding the follow-up of training on the use of the digitalization

If so, approximately how many times and what was the specific subject of these trainings?

The 71.40% of the respondents to the previous question confirmed that they had taken at least 3 training courses on the use of digital tools in their work and that they focused on the use of software internal to the accounting firm.

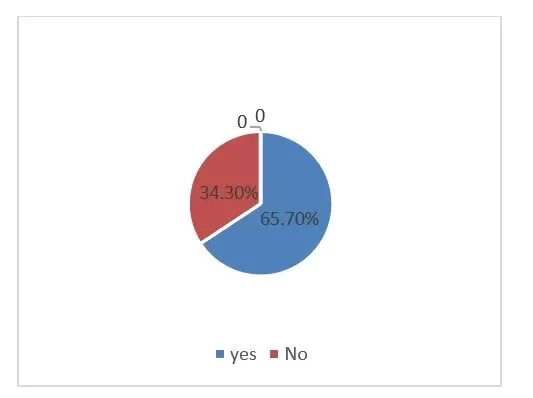

Does your practice use social media to communicate with its clients?

The results show that 65.7% of the respondents use social networks in their daily lives compared to 34.3% who do not.

Fig 15. The use of social networks

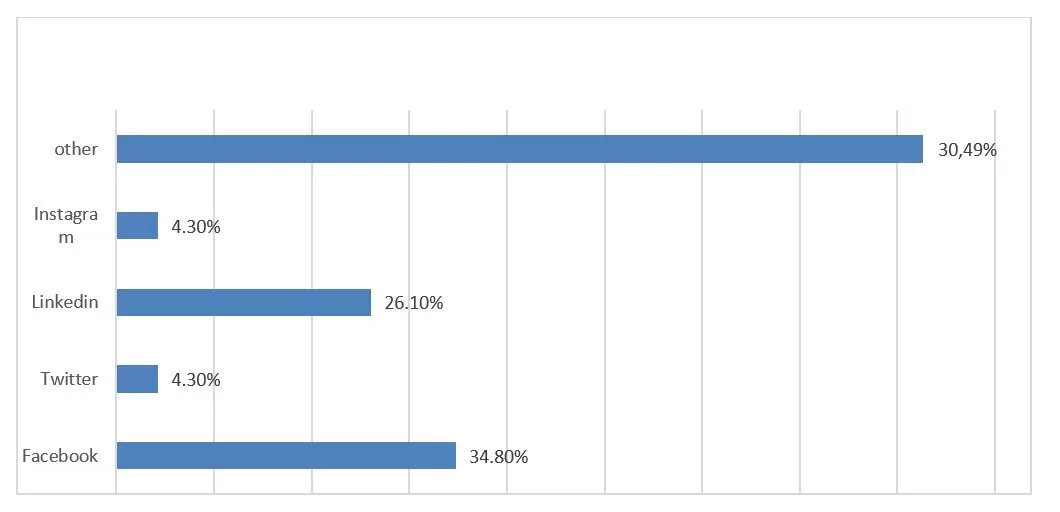

If so, what social network do they use?

Our survey results show that 34.8% of the respondents use Facebook, compared to 26.10% who use LinkedIn, 4.3% of the respondents use Twitter and 3.40% of the respondents follow Instagram.

Fig 16. Rate of use of social networks

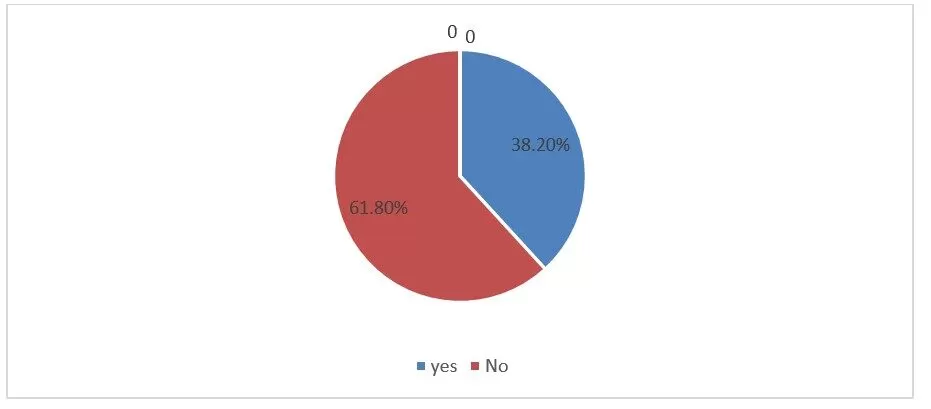

Are there any digital functions in your practice? (Example: digital consultant, web developer, etc.)?

The results show that 38.20% of the respondents confirm that there are public servants in the digital field in accounting firms (such as digital consultants, web developers, computer engineers, digital developers and web masters, etc.) where they work, while 61.80% deny it.

Fig 17. The functions related to the digitalization

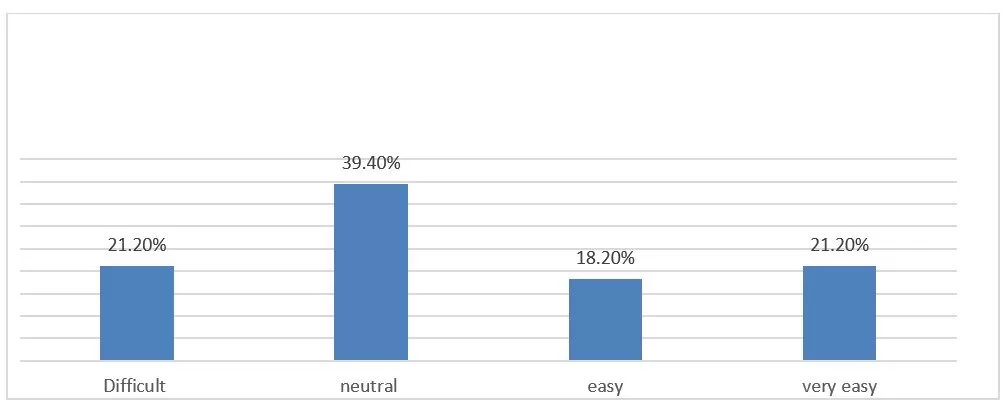

How do you welcome the use of the ization in your office?

The results show that 21.20% of the responding professionals believe that the use of the digitalization in accounting firms is difficult. 39.40% of the respondents find that the use of the digitalization in law firms is neutral. 18.2% of the respondents think that using the digitalization is easy, while 21.2% think that using the digitalization is very easy.

Fig 18. The functions related to the digitalization

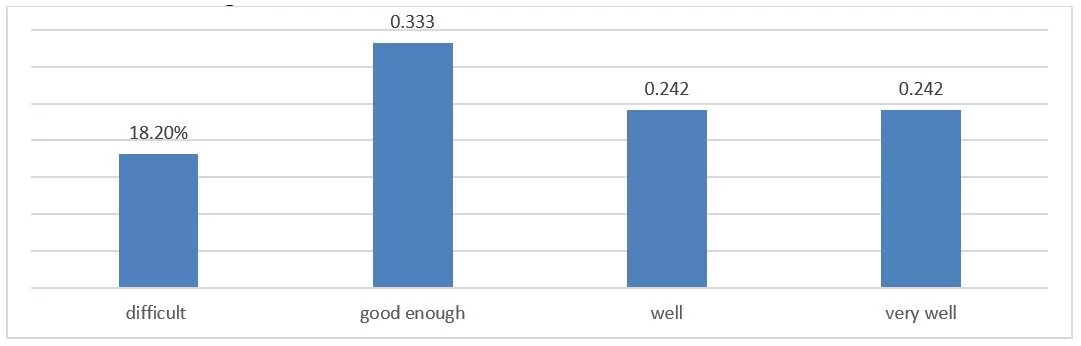

In your opinion, what is your clients’ reaction to digitalization in your accounting practice within the firm?

The results show that 18.20% of the responding clients believe that the use of the digitalization in accounting firms is difficult. 33.30% of the respondents find that the use of the digitalization within firms is quite difficult. 24.2% of the respondents think that the use of the digitalization is very easy, while 24.2% think that the use of the digitalizaion is very easy. Nobody thinks that the profession of the accountant and the accountant will disappear with the digital transformation.

Fig 19. Customer’s reaction to the digitalization of accounting practices

Discussion

Digitization is a concept that consists of using the Internet to improve the use of accounting documents, their backup, and which allows remote access to the client’s accounts for the accountant and the client. These advantages make it possible to maintain the client-accountant relationship and their loyalty. We will discuss some points above.

Our study made by qualitative surveys reveals that the use of software is difficult for some respondents because they aren’t enough formed to use them. But we think that covid crisis has accelerated the use of digital services in order to maintain the client-auditor relationship.

Some workers had taken many hours to be able to perform with digital services. Also, archiving documents in the cloud is more facilitated with digitalization, especially in the era of geopolitical and economic instability, and this advantage could be very attractive to save the planet. The use of automatic services can also be helpful for the taxation files.

Study Limitation

We think that digitalization moderates the relations between clients and auditors, but also auditors and their collaborators. However, this study is limited by the number of respondents and could be enriched by other questions to be generalized.

Conclusion

Digitalization offers many advantages. We saw that digital tools have implemented a more efficient IT system, which can contribute to anticipating changes in the legal environment in order to update the system and help to better master the computer tools and accounting standards by users. However, the ability of competitors to digitize is faced with the fact that technology is always evolving. It requires heavy investment (purchase of hardware and software, staff training, maintenance, etc.); and there is always vulnerability to viruses, and risk of data loss.

In sum, although digitalization has a positive impact on accounting and audit practices, accounting assistants and employees face difficulties, which may be due to a lack of knowledge and skills.In order for the staff of the firm to understand the evolution of the technology and better understand the new digitized tools, they must participate in trainings and seminars presenting these different tools.

Finally, it is true that accounting and audit firms have made significant progress year over year. However, an additional effort should be made to optimize the development of online services, especially since the country is still far from full digitalization.

Note: The first version of this paper was presented in French at the TICEFA conference 5-7 may 2023, Hammamet, Tunisia. Then, an English version of this research was accepted in virtual presentation at 41st IBIMA conference June, 2023, Granada, Spain.

References

Agarwal, R. and Dhar, V. (2014). ‘Big Data, Data Science, and Analytics: The Opportunity and Challenge for IS Research,’Information Systems Research 25(3), 443– 448.

Al-Khazali and Zoubi H.(2005), ‘Empirical Testing Of Different Alternative Proxy Measures For Firm Size’, The Journal of Applied Business Research 21(3), 1-12.

Baltagi, B. H. (2005) ‘Econometric analysis of panel data‘. John Wiley and Sons Ltd, England, 3, 135–181.

Bharadwaj, A., El-Sawy, O., Pavlou, P. A., and Venkatraman, N. (2013). ‘Digital Business Strategy: Toward A Next Generation of Insights’. Management Information Systems Quarterly, 37(2),471–482.

Brynjolfsson, E. and McAfee, A. (2014). ‘The Second Machine Age: Work, Progress and Prosperity in a Time of Brilliant Technologies’. W. W. Norton & Company. DOI https://psycnet.apa.org/record/2014-07087-000.

Bughin,J and VanZeebroeck,N.(2017),’Thebestresponsetodigitaldisruption’. MIT SLoan Management Review, 58, 80–86.

Bughin,J.,Catlin,T.,Hall,B., andVanZeebroeck, N.(2017),’ImprovingYourDigital Intelligence’. MIT SLoan Management Review, 58(4), 80-86.

Charitou,A ,Clubb,C.and Andreou,A. (2001). ‘TheEffectofEarningsPermanence, Growth,andFirmSize ontheUsefulness ofCashFlowsandEarningsin Explaining Security Returns: Empirical Evidence for the UK’. Journal of Business Finance & Accounting, 28(5), 563–594.

Chae, H.C., Koh, C.E.and Prybutok, V.R. (2014). ‘Information Technology Capability and Firm Performance: Contradictory Findings and Their Possible Causes,’MIS Quarterly, 38(1), 305-325.

Calabro, A., Hermann, F., Minichilli, A. and J. Suess-Rees (2021). ‘Business families in times of crisis: the backbone of family firm resilience and continuity’. Journal of Family Business and Strategy. 12(2), 100-442.

C. Ho, E.K.Chang and V. R. Prybutok. (2014). ‘Information Technology Capability and Firm Performance’. MIS Quarterly. 38(1), 305-326.

Clemons, E. K. (2008). ‘How Information Changes Consumer Behavior and How Consumer Behavior Determines Corporate Strategy’. Journal of Management Information Systems, 25(2), 13–40.

Cüneyt, D.(2015) ‘The Impacts of Robotics, Artificial Intelligence On Business and Economics‘, World Conference on Technology, Innovation and Entrepreneurship, Elsevier,DOI 1016/j.sbspro.2015.06.134.

Dehning, B., Richardson, VJ, and Zmud, RW, (2003), ‘The Value Relevance of Announcements of Transformational Information Technology Investments’. MIS Quarterly, 27(4), 637–656.

Deltour, F. and LethiaisV. (2014). ‘L’innovation en PME et son accompagnement par les TIC : quels effets sur la performance ?,’Systèmes d’Information et Management 19(2),1-14.

Dutta, A., Lee, H., and Yasai-Arkedani, M. (2014). ‘Digital systems and competitive responsiveness: The dynamics of it business value’. Information and Management, 51, 762–773.

Dutta, S. and Biren, B. (2001). ‘Business Transformation on the Internet’, European Management Journal 19(5), 449-

Eun, HK.and Park, MJ. (2017),’Critical Factors on Firm’s Digital Transformation Capacity: Empirical Evidence from Korea,’International Journal of Applied Engineering Research 12(22),12585-12596.

Eyu, K. and Wolfs,B. (2018). ‘Digital banking impact on Turkish deposit banks performance’. Banks and Bank Systems13(3), 48-57.

Fitzgerald, M., Kruschwitz, N., Bonnet, D., and Welch, M. (2013), ‘Embracing Digital Technology. A New Strategic Imperative’. MIT Sloan Management Review55(2), 1-12.

Granados, N and Gupta, A. (2013),’Transparency strategy: competing with information in a digital world,’MIS Quarterly, 37(2), 637–642.

Haverkort,B.R.andZimmermann,A.(2017),’SmartIndustry:HowICTWillChange the Game’. IEEE Internet Computing, 21(1).8–10.

Haverkort,B.R. and Zimmermann,A.(2017), ‘SmartIndustry:HowICTWillChange the Game’. IEEE Internet Computing, 21(1), 8–10.

Hays, C. L. (2004). ‘What wal-mart knows about customers’ habit”s. The New York Times

Hsiao, C. (2003),’Analysis of Panel Data’. Cambridge University Press, Cambridge.

Tolboom I.(2016).’The impact of digital transformation: A survey based research to explore the effects of digital transformation on organizations’. Delft University of Technology

Nwankpa J.K. and Roumani Y. (2016),’IT Capability and Digital Transformation: A Firm Performance Perspective’, Thirty Seventh International Conference on Information Systems. Las consulaion 18/07/2023 on URL https://core.ac.uk/download/pdf/301370499.pdf.

Wroblewski J. (2018).’Digitalization and firm performance are digitally mature firms outperforming their peers?,’Lund University School of Economics and Management.

Kane, GC, Palmer, D., Phillips, AN and Kiron, D. (2015),’Is your business ready for a digital future’,MIT Sloan Management Review, 56, 37–44.

Kauffman, RJ, Li, Tand Heck, EV, (2010),’Business Network-Based Value Creation in Electronic Commerce’,International Journal of Electronic Commerce, 15(1), 113–144.

Kurniawati, K, Shanks, G and Bekmamedova, N. (2013),’The Business Impact of Social Media Analytics’. The 21st European Conference on Information Systems.

LaValle, S, Lesser, E, Shockley, R, Hopkins, M S and Kruschwitz, N. (2011),’Big Data, Analytics and the Path From Insights to Value’. MIT Sloan Management Review, 52,21–31.

Leclercq-Vandelannoitte, A. (2015). ‘Managing BYOD: how do organizations incorporate user driven IT innovations?,‘Information Technology and People, 28(1), 2–33.

Li, ‘Digital Technologies and the Changing Business Models in Creative Industries’. (2015).In 48th Hawaii International Conference on System Sciences 5.

Loebbecke, C. and Picot, A. (2015),’Reflections on societal and business model transformationarising from digitization and big data analytics: A researchagenda’. Journal of Strategic Information Systems, 24, 149–157.

Lucas, HC, Agarwal, R, Clemons, EK, El Sawy, OA and Weber, B. (2013). ‘Impactful research on transformational information technology: an opportunity to inform new audiences’. MIS Quarterly 37(2), 371–382

McAfee, A and Brynjolfsson, E. (2008), ‘Investing in the IT that makes a competitive difference’. Harvard Business Review, 99–107.

Musabegovité I., MustafaO., Dukovic S.and JovanovicS.(2019),’Influence of financial technology (fintech) on financial industry’. Ekonomika Poljoprivrede,66(4), 1003-1021.

Oussi A.A., Klibi M.F. and I. Ouertani. (2019). ‘Audit committee role: formal rituals or effective oversight process’, Managerial Auditing Journal, 34(6), 673-695.

Piccinini, E., Gregory, R., and Kolbe, L. (2015),’Changes in the Producer-Consumer RelationshipTowards Digital Transformation’. 12th international conference on Wirtshaftinformatik, 1634–1648.

Rishika, R., Kumar, A., Janakiraman, R., and Bezawada, R. (2013). ‘The Effect of Customers’ Social Media Participation on Customer Visit Frequency and Profitability: An Empirical Investigation’. Information Systems Research, 24(1), 108–127.

Sarah E.Stief, Anne Theresa Eidhoff, Markus Voeth (2016), ‘Transform To Succeed: An Empirical Analysis of Digital Transformation in Firms’, International Journal of Economics and Management Engeneering, 10(6), 1833-1843.

Schoemaker, P. J. and Tetlock, P. E. (2017), ‘Building a more intelligent enterprise’. MIT Sloan Management Review, 58, 28–37.

Siddiqui ,A, Abbas, S, and S. Alkatheri (2019).’A Comparative Study of Big Data Frameworks’. International Journal of Computer Science and Information Security, 66-73.

Siddiqui,A and Qureshi,R. (2017),’Big Data In Banking: Opportunities And Challenges Post Demonetisation in India,Journal of Computer Engineering,33-39.

Smith, H., and McKeen, J. (2008),’Developments in practice: Social computing: How should it be managed? ‘Communications of the Association for Information Systems, 23(1),409-418..

Stolterman, E. and Croon Forst, A. (2006),’Information technology and the good life’. Information Systems Research: Relevant Theory and Informed Practice (p. 744). Springer US

Tolboom Irik, (2016),’The impact of digital transformation: A survey based research to explore the effects of digital transformation on organizations,’ Delft University of Technology.

von Blixen-Finecke, L., Byström, E. E., and Eriksson, A. (2017). ‘Digital leaders in Sweden 2018’. BearingPoint Research, 4–59.

Weill, P. and Woerner, S. L. (2015), ‘Thriving in an increasingly digital ecosystem’. MITSloan Management Review, 56. 27–34.

Weill, P. and Woerner, S. L. (2018). ‘Is Your Company Ready for a Digital Future?,’MIT Sloan Management Review, 59(2),21–25.

Weill,P.and Ross, W. (2005),’IT Governance: How Top Performers Manage IT Decision Rights for Superior Results’,International Journal of Electronic Government Research, 63-67.

Westerman, G. (2017) ‘Your Company Doesn’t Need a Digital Strategy,‘MIT SLoan Management Review.DOI https://shop.sloanreview.mit.edu/store/your-company-doesnt-need-a-digital-strategy

Westerman, G. and Bonnet, D. (2015),’Revamping your business through digital transformation’. MIT Sloan Management Review.Spring, 2–5.

Westerman, G., Calmejane, C. et Bonnet, D. (2011),’Digital Transformation: A Roadmap for Billion-Dollar Organizations,’ MIT Center for Digital Business, 1–68.

Westerman, G., Calméjane, C., Bonnet, D., Ferraris, P., and McAfee, A. (2011). ‘Digital transformation: A roadmap for billion-dollar organisations,’ MIT Center for Digital Business and Capgemini Consulting, 5–62.

Westerman, G., Tannou, M., Bonnet, D., Ferraris, P., and McAfee, A. (2012), ‘The Digital Advantage: How digital leaders outperform their peers in every industry,’ MIT Center for Digital Business and Capgemini Consulting, 2–21.

Zammuto,R.F.,Griffith,T.L.,Majchrzak,A.,Dougherty,D.J.,andFaraj,S.(2007), ‘Informationtechnology and the changing fabric of organization, ‘, Organization Science 18,749–762.

Zhu, F., and Zhang, X. M. (2010), ‘ Impact of Online Consumer Reviews on Sales: The Moderating Role of Product and Consumer Characteristics’. Journal of Marketing, 74(2), 133–148.

Annex 1

Telephone survey

1/What is your position within the firm?

2/ In your opinion, is the accounting profession part of a digital transformation process?

3/Do you think that the digitalization of the accounting profession is an element that improves the development of employees?

4/ Do you think the accounting transition process is conducive to improving the accounting environment?

5/ If so, are you able to spend a budget to start training on the use of software?

Annex 2

Survey by google forms

1/How old are you?

Under 25 years

Between 25 and 35 years

Between 35 and 45 years

Over 45 years

2/What is your position within your firm?

Public accountant

Assistant

Mission director

Public accountant trainee

Collaborator

3/How many employees does your firm have?

Less than 10

Between 10 and 30

Between 30 and 50

More than 50

4/How do you re-establish your clients’ accounting?

Customer deposits in person in paper form

The customer deposits it via an online platform

Both

5/How do you archive?

Paper archiving

Digital archiving

Both

6/How do you produce your accounting?

Manually

Automated

Both

7/If your accounting production is automated, what digital tools have you adopted?

8/How do these digital tools help you in your daily work?

Less than 25%

Between 25 and 50%

Between 50 and 100%

100% (zero paper)

9/Can you and your clients remotely access your firm’s IT resources?

Yes

No

10/Have you taken any training on the use of digital?

11/If yes, approximately how many times and what was the specific topic of these trainings?

12/Does your firm use social media to communicate with its clients?

13/If yes, which

Facebook

Twitter

LinkedIn

Instagram

Other

14/Does the digital functions in your practice apply? (Example: digital consultant, web developer, etc.)

Yes

No

15/If yes, which ones?

16/How do you welcome the use of digital in your office?

17/In your opinion, what is your clients’ reaction to digitalization in your practice?