The Impact of Business Investment on Euronext Stock Returns: A Study of Companies Listed at Amsterdam, Brussels, Paris, and Lisbon Stock Exchanges between the Years 2017 and 2022

GOVCOPP – Research Unit on Governance, Competitiveness and Public Policies, DEGEIT – Department of Economics, Management, Industrial Engineering and Tourism, University of Aveiro, Campus Universitário de Santiago, 3810-193, Aveiro

Volume 2024,

Article ID 526234,

IBIMA Business Review,

9 pages,

DOI: https://doi.org/10.5171/2024.526234

Received date: 29 March 2024; Accepted date: 17 June 2024; Published date: 25 July 2024

Academic Editor: Jose Carlos Lopes

Cite this Article as:

Luís COSTA, Elisabete VIEIRA and Mara MADALENO (2024)," The Impact of Business Investment on Euronext Stock Returns: A Study of Companies Listed at Amsterdam, Brussels, Paris, and Lisbon Stock Exchanges between the Years 2017 and 2022", IBIMA Business Review, Vol. 2024 (2024), Article ID 526234, https://doi.org/10.5171/2024.526234

The objective of this work is to analyze the impact that the investment from companies has on a number of Euronext stock returns. For the analysis, we used the Generalized Method of Moments (GMM) to collect a sample of companies from the stock exchanges in Amsterdam, Brussels, Paris, and Lisbon, between 2017 and 2022. The results indicate that the investment generated by companies has a positive and significant impact on Euronext stock returns, therefore suggesting that managers from Euronext companies should employ a balanced investment strategy that incorporates both tangible and intangible assets, in order to enhance stock returns. This study can provide some guidance in decision-making for private and institutional investors investing in Euronext stocks. The originality of this article derives from the analysis of the impact that investment, divided between tangible and intangible assets, has on Euronext stocks returns. Finally, it is important to point out that the use of the GMM methodology allowed for the collection of robust results.

In financial markets, the analysis of the factors that influence stock returns is increasingly important for investors and, therefore, it is one of the most current and relevant subjects in financial theory and, at the same time, one of the oldest and most arousing interests of researchers. Theoretical literature highlights that, to make a conscious decision about buying or selling a stock, investors need to have in-depth knowledge of companies. This is because according to Song (2015), the information available on the stock market about companies is constantly reflected in their price. Costa (2022a) adds that the market price of stocks fluctuates according to the law of supply and demand. Therefore, in each transaction, the negotiated price jointly identifies the price each investor is willing to pay and the price at which each investor is available to sell.

From a business point of view, investment is a very important aspect in determining the ability of companies to remain resilient and, therefore, is an essential condition for their development. It is the investment that introduces facilities, equipment, and processes into organizations that incorporate the advancement of knowledge and that allow available resources to be used more productively (Alexandre et al., 2017). Additionally, the growing globalization and the industrial revolution 5.0 that is taking place today highlight the importance of investment by companies, requiring them, according to an evolutionary perspective, where only the most resilient resists, a continuous effort to improve at various levels, with emphasis on investment in its tangible and intangible assets. Only the combination of these factors allows companies to survive and prosper (Silva and Oliveira, 2020; Alexandre et al., 2021).

This article aims to analyze the impact of companies’ investment on the return on Euronext stocks. This investigation is of great importance because, as far as we know, there is still no study that analyzes this problem for the reality of Euronext. Furthermore, this research can help investors better understand how companies’ investment influences Euronext stock returns, so they can adjust their investment strategies and more accurately determine companies’ intrinsic value. Finally, this study is relevant for managers of Euronext companies, as it provides valuable clues about the efficient allocation of resources and the maximization of shareholder value.

The article is organized as follows: Point 2 reviews the literature on the impact of investment on stock returns; Point 3 presents the econometric methodology, data sources, sample definition, variables used and descriptive statistics; Point 4 presents the results of this study, and its analysis; Point 5 concludes this work.

Literature Review

The term investment can be defined as the allocation of financial resources, time, or effort to obtain a return in the future (Nugroho, 2020). Investment can be made by individuals, companies, and even governments, and is an essential practice to increase personal wealth, finance business projects, and promote economic growth. There are several types of investment, each with its level of risk and potential return. Choosing the appropriate investment depends on the financial objectives, risk tolerance, and time horizon of each investor (Soares et al., 2015).

From a business point of view, the investment can be real or financial. Financial investment refers to the allocation of resources into financial assets, such as stocks, bonds, bank deposits, and other financial instruments available on the market. This type of investment involves transactions in financial markets and focuses on the expectation of obtaining financial returns, such as dividends, interest, or capital gains (Nugroho, 2020). On the other hand, companies’ real investment involves the allocation of resources into tangible and intangible assets and is directly related to the functioning of the companies’ business model. According to Alexandre et al. (2017), this type of investment is essential for companies to expand and be competitive in the market in the long term and, therefore, it is the type of investment that will be the object of analysis in this investigation.

Iltas and Demirgunes (2020) state that tangible assets are physical assets of companies that are used in the production or completion of goods or services and that are expected to be used for more than one year. These assets are generally held by companies to support their core activities. Examples of tangible assets are land, buildings, vehicles, furniture, and other equipment. Iltas and Demirgunes (2020) indicate that companies with more tangible assets tend to finance themselves at a lower cost. This is because tangible assets can be used as collateral for loans, which reduces the risk perceived by creditors and positively influences stock returns.

On the other hand, Cardozo-Torres et al. (2021) indicate that intangible assets are identifiable non-monetary assets without physical substance. For the authors, examples of this type of asset include patents, brands, licenses, franchises, internally developed software, customers, and human capital. Mendez-Morales et al. (2024) state that this type of investment is a guarantee of the innovation capacity of any institution and, therefore, is increasingly important in the current business situation in which all activity is supported by IT management programs that certify the quality of all operational functioning.

Costa et al. (2021) state that all companies must invest to cover the amortization and depreciation they practice, that is, they must restore their capital to the productive level. When companies invest less than the amortization and depreciation they practice, they can cause high cash flows in the short term, but they can lose operational capacity in the medium and long term, which can channel them into an unsustainable situation (Eisenhardt and Martin, 2000). When a company decides to invest, it tends to allocate liquid resources to a specific tangible or intangible fixed asset with the prospect of generating a higher result than what it would obtain if it had not opted for the investment plan (Daum, 2003; Chen and Srinivasan, 2023).

Pinho et al. (2019) state that when a company announces a future action plan, such as the start of a new project, the share price can have a negative or positive reaction. Company management can watch the stock price reaction to see what market participants think of the plan. If the price falls, management may need to review its calculations and reconsider the decision made, as the market received the information as negative. Therefore, the stock market can help management get a second opinion on their investment decisions.

Therefore, understanding the impact of business investment on stock returns is complex and multifaceted. On the one hand, some studies indicate that investing can have a positive impact on stock returns. In this sense, Costa (2022a) analyzed the companies included in the Euro Stoxx 50 index between 2016 and 2019 using the panel data methodology. The results indicate that there is a positive causality between investment and stock returns. The author indicates that investors tend to value companies that reinvest their profits, due to the expectation created regarding the increase in their future cash flows. Similar results are presented by Miranda et al. (2013), Medrado et al. (2016), Magro et al. (2017) and Gomes et al. (2020) in Brazil; Alarussi and Gao (2023) in China; Balzer et al. (2020) in the United States; Haji and Ghazali (2018) in Spain and Pechlivanidis et al. (2022) in Greece.

By opposition, excessive or misdirected investments can lead to disappointing or even negative returns, with a consequent negative impact on stock returns. Thus, some studies indicate that companies that have surplus resources run the serious risk of wasting them on inefficient spending or unprofitable projects (Jensen, 1986; Richardson, 2006; Nekhili et al., 2016; Takamatsu and Lopes- Fávero; 2019).

Kim et al. (2016), Nugroho (2020) and Modena et al., (2020) also highlight that if companies do not adequately manage the life cycle of their investments, including the planning, implementation, and monitoring phase, this can lead to a waste of resources, excessive costs and low returns. Finally, it is important to indicate that there is also literature that states there is no statistically significant influence between investment and stock returns (Assagaf, 2016; Nugroho, 2020).

Given the above, we propose our first research hypothesis.

H1: Increased investment has a positive impact on Euronext stock returns.

Additionally, based on studies by Iltas and Demirgunes (2020) and Alarussi and Gao (2023), we will reinforce the analysis by examining investment in isolation, more precisely, at the level of tangible assets and intangible assets, so we propose to investigate hypothesis 2 and 3.

H2: Increased investment in tangible assets has a positive impact on Euronext stock returns.

H3: Increased investment in intangible assets has a positive impact on Euronext stock returns.

Data, Variables, Methodology

Sample

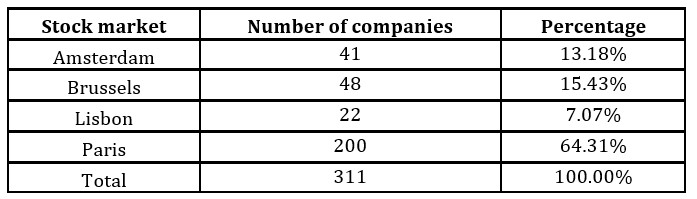

In this work, we analyzed a total of 311 non-financial companies quoted on the Amsterdam, Brussels, Lisbon, and Paris stock exchanges, between the years 2017 and 2022. Table 1 distributes the sample by stock exchange.

Table 1: Sample distribution regarding location

As happened in the study by Costa et al. (2024), in this investigation we took company data from The Wall Street Journal website and macroeconomic data from Eurostat.

Variables used

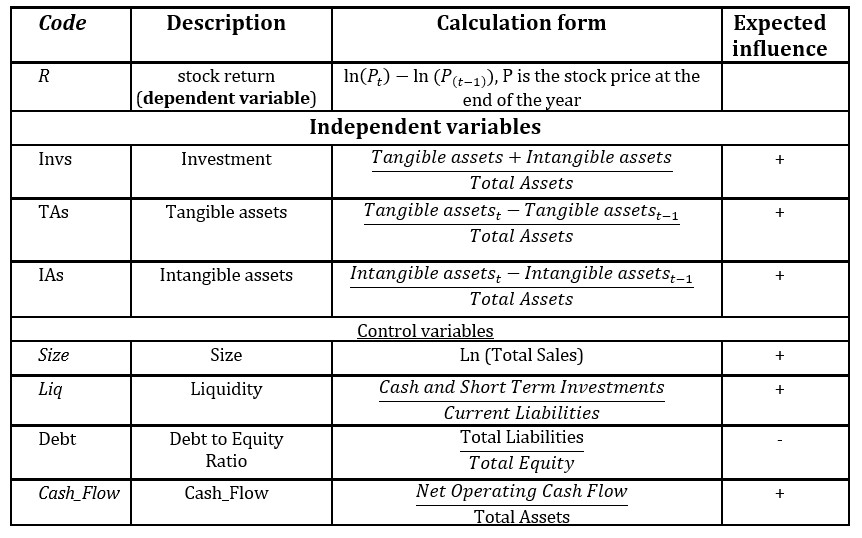

In this work we use the annual return on shares as the dependent variable. To answer the research questions, we used 3 independent variables that identify companies’ investment.

The literature states that to guarantee the robustness and precision of the analyses, we must use indicators that control the size, liquidity, debt, and cash flow of companies (Ribeiro and Quesado, 2017; Nguyen et al., 2019; Vieira et al., 2019; Sausan et al., 2020; Phuong, 2020; Costa et al., 2021; Costa, 2022b; Fernandes and Costa, 2023). Table 2 presents the dependent variable, the independent variables, the calculation method, and the expected influence signal.

Table 2: Presentation of the dependent variable and independent variables

Methodology

In this work, we use the GMM methodology, which allows us to combine time series and cross-sections in a single model. This methodology allows for controlling the heterogeneity present in companies and allows the use of more observations, which leads to an increase in the number of degrees of freedom and reduces collinearity between independent variables (Neves et al., 2018). Furthermore, this methodology allows to correct the endogeneity that occurs when independent variables are correlated with the error terms of the regression models (Khan, 2023).

As happened in the investigation by Costa et al. (2024), we use the first differences to leave the variables stationary and thus obtain more robust estimates.

Descriptive Statistics

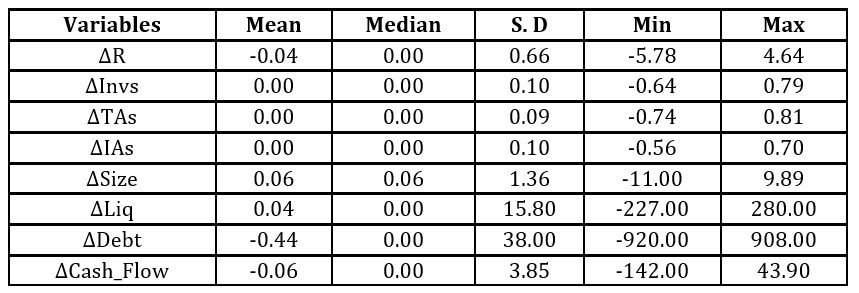

Table 3 presents the descriptive statistics of the variables analysed in the study.

Table 3: Descriptive statistics of the variables

The Debt variable is the one with the highest standard deviation, which indicates that it is the variable with the greatest dispersion with respect to the mean.

Econometric Analysis

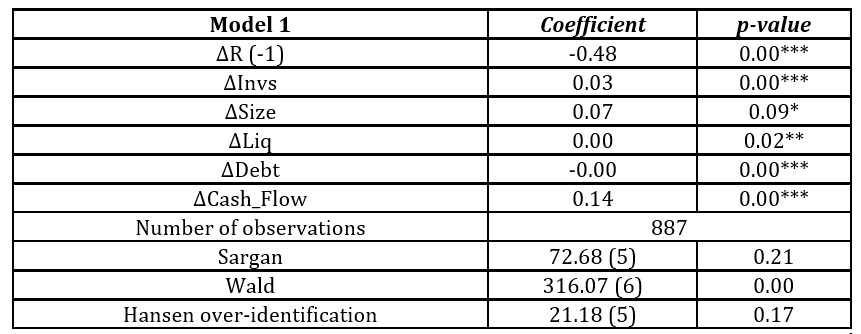

Table 4 shows the results obtained in Model 1 using the two-stages GMM methodology.

Table 4: Model 1 results

Notes: The Sargan, Wald and Hansen tests allow us to conclude that the econometric model is valid. Variables are defined in Table 2. T statistics; *** significance level of 1%, ** significance level of 5%, * significance level of 10%.

Model 1 results indicate that the investment has a positive and statistically significant effect on Euronext stock returns. Therefore, this study corroborates the research by Silva and Oliveira (2020) and suggests that an increase in the level of investment can create investors’ expectations of an increase in companies’ future cash flows. This fact can attract investors interested in obtaining the benefits of future growth, which can increase demand for companies’ stocks and increase their market value. Given the above, we validate H1.

Firm size has a positive and statistically significant causality with Euronext stock returns. This evidence is in line with the study by Ribeiro and Quesado (2017) and suggests that larger companies tend to benefit from economies of scale and, therefore, tend to present higher returns. Moreover, the liquidity and debt ratios are statistically significant. These results are in line with Nguyen et al. (2019) and Fernandes and Costa (2023), suggesting that companies tend to present higher returns as they find it easier to fulfill their short, medium, and long-term responsibilities.

Likewise, the results suggest that companies’ ability to generate liquid assets, assessed through the control cash flow variable, has a positive and statistically significant effect on stock returns. The value of the coefficient allows us to identify that investors attach great importance to companies’ ability to generate revenue through their operational activity.

To strengthen these results, below we present model 2 which decomposes companies’ investment in relation to tangible and intangible assets.

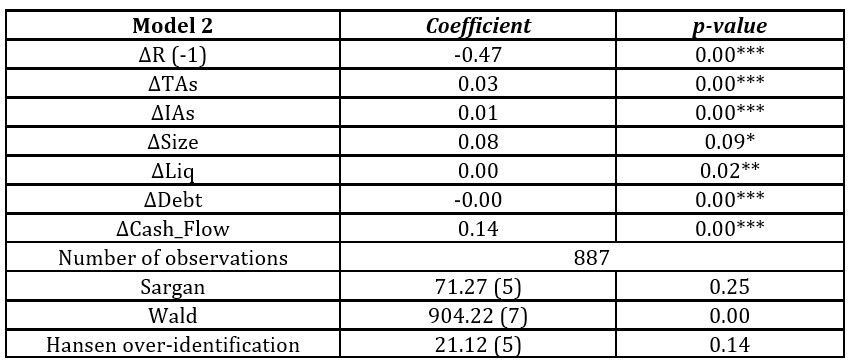

Table 5: Model 2 results

Notes: The Sargan, Wald and Hansen tests allow us to conclude that the econometric model is valid. Variables are defined in Table 2. T statistics; *** significance level of 1%, ** significance level of 5%, * significance level of 10%.

The results of Model 2 demonstrate that tangible assets and intangible assets have a positive and statistically significant impact on Euronext stock returns. These data corroborate the studies by Iltas and Demirgunes (2020) and Alarussi and Gao (2023) and allow us to validate H2 and H3.

This conclusion indicates that managers of Euronext companies should seek to have a balanced investment strategy that incorporates tangible and intangible assets to maximize stock returns. This holistic approach recognizes that synergies between these two types of assets can provide a lasting competitive advantage for companies.

Finally, we have that Model 2 validates the results presented in Model 1, regarding size, liquidity, debt, and cash flow.

Conclusion

This investigation sought to understand the impact that investment by Euronext companies has on their stock returns. To this end, companies that are part of the Amsterdam, Brussels, Lisbon, and Paris stock exchanges were analyzed. The results of this analysis revealed that investment, whether in tangible or intangible assets, has a positive and statistically significant effect on Euronext stock returns. This finding indicates that managers of Euronext companies must seek to invest to cover the amortization and depreciation they carry out, that is, they must restore the companies’ capital to the productive level. Likewise, companies must have an ambidextrous investment strategy that incorporates both tangible and intangible assets.

These results offer valuable insights into the relationship between corporate investment and Euronext stock returns and can help investors adjust their investment strategies. On the other hand, managers of companies listed on Euronext can benefit from these results by developing more efficient investment strategies that aim to maximize shareholder value. By recognizing the importance of tangible and intangible assets, managers can direct resources more effectively, capitalizing on synergies between these assets and strengthening the companies’ competitive position in the market.

Finally, it is important to note that the present study remains incomplete because it focused only on Euronext companies. Future research could explore more stock exchanges to assess whether these results would remain valid.

References

Alarussi, A. S., and Gao, X. (2023), ‘Determinants of profitability in Chinese companies.’ International Journal of Emerging Markets, 18(10), 4232-4251, doi: 1108/IJOEM-04-2021-0539.

Alexandre, F., Bação, P. M., Carreira, C., Cerejeira, J., Loureiro, G., Martins, A. M., and Portela, M. (2017), ‘Investimento empresarial e o crescimento da economia portuguesa.’ Fundação Calouste Gulbenkian.

Alexandre, F., Jalles, J., Martins, J., Brinca, P., Sequeira, T., Montelius, L., and Santos, C. (2021). ‘Do made in ao created in: um novo paradigma para a economia portuguesa.’ Fundação Francisco Manuel dos Santos.

Assagaf, A. (2016), ‘Effect of Investment Opportunity Set (Ios), level of leverage and return to return stock market company in Indonesia Stock Exchange.’ Efect of investment opportunity set, level of leverage and ROA to return stock market company in Indonesia stock exchange, 14(3), 1625-1644.

Balzer, R., Užík, M., and Glova, J. (2020), ‘Managing growth opportunities in the digital era–an empiric perspective of value creation.’ Polish Journal of Management Studies, 21, doi: 17512/pjms.2020.21.2.07.

Cardozo-Torres, V., Méndez-Morales, A., and Herrera, M. M. (2021), ‘La inversión en marcas y su relación con los resultados empresariales.’ Suma de Negocios, 12(27), 161-171, doi: 14349/sumneg/2021.V12.N27.A07.

Chen, W., and Srinivasan, S. (2023), ‘Going digital: Implications for firm value and performance.’ Review of Accounting Studies, 1-47.

Costa, L. M. (2022a), ‘Determinants of Annual Abnormal Yields of Stocks belonging to the Euro stoxx 50 Index.’ European Journal of Applied Business and Management, 8(2).

Costa, L. M. (2022b), ‘The impact of productivity on Euronext stock returns.’ European Journal of Applied Business and Management, 8(4).

Costa, L., Ribeiro, A., and Machado, C. (2021), ‘Determinantes do preço de mercado das ações: evidência empírica para o PSI 20.’ Revista Gestin, 22, 41-53.

Costa, L., Vieira, E., Madaleno, M. (2024), ‘Does Googling Impact Euronext Stock Returns?’ IBIMA Business Review, 2024, 963956, doi: 5171/2024.963956.

Daum, J. H. (2003), ‘Intangible assets and value creation.’ John Wiley and Sons.

Eisenhardt, K. M., and Martin, J. A. (2000), ‘Dynamic capabilities: what are they?’ Strategic management journal, 21(10‐11), 1105-1121, doi: 1002/1097-0266.

Fernandes, L., and Costa, L. M. (2023), ‘The impact of the sports and financial performance of European football clubs on their share prices.’ European Journal of Applied Business and Management, 9(4), doi: 58869/EJABM9(4)/04.

Gomes, H. B., de Castro Gonçalves, T. J., and de Lima Tavares, A. (2020), ‘Intangibilidade e o valor da empresa: uma análise do mercado acionário brasileiro.’ Revista Catarinense da Ciência Contábil, (19), 1.

Haji, A. A., and Mohd Ghazali, N. A. (2018), ‘The role of intangible assets and liabilities in firm performance: empirical evidence.’ Journal of Applied Accounting Research, 19(1), 42-59, doi: 1108/JAAR-12-2015-0108.

Iltas, Y., and Demirgunes, K. (2020), ‘Asset tangibility and financial performance: A time series evidence.’ Ahi Evran Üniversitesi Sosyal Bilimler Enstitüsü Dergisi, 6(2), 345-364, doi: 31592/aeusbed.731079.

Jensen, M. C. (1986), ‘Agency costs of free cash flow, corporate finance, and takeovers.’ The American economic review, 76(2), 323-329.

Khan, S. (2023), ‘The impacts of Sukuk on financial inclusion in selected Sukuk markets: an empirical investigation based on generalized method of moments (GMM) analysis.’ International Journal of Social Economics, 50(8), 1153-1168, doi: 1108/IJSE-06-2022-0424.

Kim, H. H., Maurer, R., and Mitchell, O. S. (2016), ‘Time is money: Rational life cycle inertia and the delegation of investment management.’ Journal of financial economics, 121(2), 427-447, doi: 1016/j.jfineco.2016.03.008.

Magro, C. B. D., Silva, A. D., Padilha, D., and Klann, R. C. (2017), ‘Relevância dos ativos intangíveis em empresas de alta e baixa tecnologia.’ Nova Economia, 27, 609-640, doi: 1590/0103-6351/3214.

Medrado, F., Cella, G., Pereira, J. V., and Dantas, J. A. (2016), ‘Relação entre o nível de intangibilidade dos ativos e o valor de mercado das empresas.’ Revista de Contabilidade e Organizações, 10(28), 32-44, doi: 11606/rco.v10i28.119480.

Mendez-Morales, A., Anzola-Morales, C., Ruiz-Acosta, L. E., and Camargo-Mayorga, D. A. (2024), ‘Intangible assets and their effects on business performance: an analysis for Colombian companies.’ Revista Galega de Economía, 33(1), doi: 15304/rge.33.1.9138.

Miranda, K. F., de Vasconcelos, A. C., da Silva Filho, J. C. L., dos Santos, J. G. C., and Maia, A. B. G. R. (2013), ‘Ativos intangíveis, grau de inovação e o desempenho das empresas brasileiras de grupos setoriais inovativos.’ Revista Gestão Organizacional, 6(1), 4-17, doi: 22277/rgo.v6i1.1823.

Modena, J. L., Sibim, M. C., Scarpin, J. E., and Barros, C. M. E. (2020), ‘A influência da representatividade dos ativos intangíveis sobre o retorno das ações quando do anúncio de revisão do rating soberano do Brasil para grau especulativo.’ Revista de Contabilidade do Mestrado em Ciências Contábeis da UERJ, 24(1), 74-89.

Nekhili, M., Amar, I. F. B., Chtioui, T., and Lakhal, F. (2016), ‘Free cash flow and earnings management: The moderating role of governance and ownership.’ The Journal of Applied Business Research, 32(1), 255-268.

Neves, M. E. D., Sousa, M., and Barbosa, C. (2018), ‘Determinantes da rendibilidade das ações: um estudo de empresas cotadas na Euronext Lisbon,’ Portuguese Journal of Finance, Management and Accounting, 4 (7).

Nguyen, C. P., Schinckus, C., and Nguyen, T. V. H. (2019), ‘Google search and stock returns in emerging markets.’ Borsa Istanbul Review, 19(4), 288-296, doi: 1016/j.bir.2019.07.001.

Nugroho, B. Y. (2020), ‘The effect of book to market ratio, profitability, and investment on stock return.’ International Journal of Economics and Management Studies, 7(6), 102-107.

Pechlivanidis, E., Ginoglou, D., and Barmpoutis, P. (2022), ‘Can intangible assets predict future performance? A deep learning approach.’ International Journal of Accounting and Information Management, 30(1), 61-72, doi: 1108/IJAIM-06-2021-0124.

Phuong, L. (2020), ‘Investor sentiment by psychological line index and stock return.’ Accounting, 6(7), 1259-1264, doi: 5267/j.ac.2020.8.026.

Pinho, C., Valente, R., Madaleno, M., and Vieira, E. (2019), Risco Financeiro-Medida e Gestão, 2ª Edição, Edições Sílabo.

Richardson, S. (2006), ‘Over-investment of free cash flow.’ Review of accounting studies, 11, 159-189, doi: 1007/s11142-006-9012-1.

Sausan, F. R., Korawijayanti, L., and Ciptaningtias, A. F. (2020), ‘The effect of return on asset (ROA), debt to equity ratio (DER), earning per share (EPS), total asset turnover (TATO) and exchange rate on stock return of property and real estate companies at Indonesia stock exchange period 2012-2017.’ Ilomata International Journal of Tax and Accounting, 1(2), 103-114, doi: 52728/ijtc.v1i2.66.

Silva, R., and Oliveira, C. (2020), ‘The influence of innovation in tangible and intangible resource allocation: A qualitative multi case study.’ Sustainability, 12(12), 4989, doi: 3390/su12124989.

Soares, M. I., Moreira, J. A. C., Pinho, C., and Couto, J. (2015), Investment Decisions: Financial Analysis of Projects (4th ed).

Ribeiro, A., and Quesado, P. (2017), ‘Fatores Explicativos da Rendibilidade Anormal Anual das Ações.’ European Journal of Applied Business and Management.

Song, L. (2015), ‘Accounting disclosure, stock price synchronicity and stock crash risk: An emerging-market perspective.’ International Journal of Accounting and Information Management, 23(4), 349-363, doi: 1108/IJAIM-02-2015-0007.

Takamatsu, R. T., and Lopes-Fávero, L. P. (2019), ‘Financial indicators, informational environment of emerging markets and stock returns.’ RAUSP Management Journal, 54, 253-268, doi: 1108/RAUSP-10-2018-0102.

Vieira, E. S., Neves, M. E., and Dias, A. G. (2019), ‘Determinants of Portuguese firms’ financial performance: panel data evidence,’ International Journal of Productivity and Performance Management, 68 (7), 1323-1342, doi: 1108/IJPPM-06-2018-0210.