Department of Accountancy, University of Johannesburg, South Africa

Volume 2025,

Article ID 202801,

IBIMA Business Review,

13 pages,

DOI: https://doi.org/10.5171/2025.202801

Received date: 23 October 2024; Accepted date: 4 April 2025; Published date: 20 May 2025

Cite this Article as:

Mohammed Kayode AJAPE and Michael O. Adelowotan (2025)," Digital Accounting Practices and Financial Performance: Quantitative Research in Seven International Deposit Money Banks in Nigeria ", IBIMA Business Review, Vol. 2025 (2025), Article ID 202801, https://doi.org/10.5171/2025.202801

Although previous studies have explored the link between digitalisation and bank performance, the impact of these digital tools on deposit money banks in Nigeria remains debatable, especially regarding the components of digital accounting practices. This study examined the effect of digital accounting practices on the financial performance of deposit money banks (DMBs) in Nigeria. Specifically, the study investigated the impacts of data analytics, automated bookkeeping, machine learning, cloud-based accounting systems, and blockchain technology on Nigeria’s return on assets of DMBs. A survey design was employed. A stratified sampling method was adopted to select seven deposit money banks with international authorization. A self-administered questionnaire was used to collect data from a sample size of 396 employees, which was determined using the Taro Yamane formula. The data were analysed using both descriptive and linear regression methods using SPSS. The results of the analysis showed that data analytics, automated bookkeeping, machine learning, cloud-based accounting systems, and blockchain technology have a positive and statistically significant influence on financial performance (ROA). The study concluded that digital accounting practices significantly influenced the economic performance of licensed deposit money banks in Nigeria. The study recommended, among others, that DMBs should enhance their data analytics capabilities to improve financial performance further.

The Deposit Money Banks (DMBs) serve as a backbone for the Nigerian economy (Ngozi et al., 2023; Makinde, 2021; Pam, 2020). These banks provide essential financial services like savings mobilisation, financial inclusion promotion, and credit and financing provisions that can aid economic growth and development.

Digital accounting is now crucial in banking worldwide, including in Nigeria. Nigerian banks maintain performance through digital change and cost-saving (Moses-Ashike, 2018; Umoren & Olokoyo, 2020). They use digital systems to streamline work and meet regulations. Fintech has transformed banking, boosting customer service and efficiency (Okorie & Salami, 2019; Osamor, 2020). Digitalisation has changed how accounting functions are done (Coman, et al., 2022; Bhimani, 2020). Fijabi and Lasisi (2023) noted that this consists of several technologies which help in recording, analysing, and sharing financial data. They involve cloud-based software that ensures security, electronic payments, blockchain, and data analytics for secure deals and aids in real-time financial checks (Owolabi et al., 2023; Ogunsola, 2021).

Furthermore, digital accounting offers more efficiency and lowers costs for DMBs (Coman et al., 2022; Oladejo et al., 2020). This technology improves financial management accuracy and decision-making. Routine tasks like data entry and reporting are automated. This automation cuts errors and helps allocate resources better (Owolabi et al., 2023; Fijabi & Lasisi, 2023). Automation also frees employees to focus on strategy. Digitalisation increases transparency in financial reporting. Stakeholders access live financial data, building trust. Quick decisions are made possible with real-time data, while cloud storage ensures security (Ngwengeh, Messomo, & Mbu, 2021; Bhimani, 2021; Oladejo & Yinus, 2020).

However, digital accounting has its risks and challenges. These include cybersecurity threats, data privacy issues, and skill gaps (Gaya et al., 2022; Samuel & Grace, 2022; Odunayo et al., 2023), high investment in infrastructure and talent development (Amahalu et al., 2020; Mujiono, 2021).

Nigerian DMBs face many challenges in financial performance relating to inefficiencies and operational problems, and lack of transparency in financial reporting. This affects trust and decision-making by stakeholders (Akinbode et al.,2023; Audu, 2020). Many banks still use manual, outdated systems. These lead to transaction delays and errors (Samuel & Grace, 2022; Oladejo & Yinus, 2020). Limited data analytics adds to these problems. Banks fail to get insights into customer behaviour, and market trends fail to forecast trends and spot financial issues, weaken strategic planning, and reduce their competitive advantage (Dick, 2024; Samuel & Grace, 2022).

Studies have explored the link between digitalisation and bank performance (Odukwu et al., 2023; Owolabi et al., 2021; Okika & Udeh, 2019). However, the specific impact of these digital tools on deposit money banks in Nigeria remains debatable, especially regarding the components of digital accounting practices. This study provides empirical evidence on the impact of various digital accounting practices on financial performance metrics within Nigerian deposit money banks. Thus, the study prompted a rethink of the potential of using digital accounting tools, highlighted the importance of adopting more advanced technologies to enhance financial performance, and challenged the existing narrative that the Nigerian banking system is not effectively utilising advanced technologies.

Literature Review

Digital Accounting Practices

The evolution of technological innovations can be traced back to the invention of fundamental computing devices such as abacus, which has been used since at least 500 B.C. This technology opens fresh possibilities for digitalisation (Byrd & Ding, 2023; Haabazoka, 2018). The primary purpose of digital accounting is to enable organisations to analyse real-time data, make informed strategic decisions, and have interactive access to current information to aid sales promotions, marketing, and future planning (Nithya & Kiruthika, 2021; Rahman et al., 2023).

Digital accounting tools often adopted by banks include the use of automated systems, Application Programming Interfaces (APIs), the Internet of Things (IoT), and others for data collection and processing (Laghari et al., 2022; Broby, 2021; Bhimani, 2020). In addition, banks now utilise digital channels like online banking platforms, mobile applications, and chatbots to provide convenient and accessible means for customers to perform transactions, access their account information and seek support (Laghari et al., 2022; Kaur et al., 2021). Also, there is consensus in the literature that banks now adopt Robotic Process Automation (RPA), blockchain technology, advanced encryption techniques, intrusion detection systems, multi-factor authentication, cloud computing, and AI-powered systems for keeping customers well-informed about their financial activities (Eswaran et al., 2022; Oino, 2019).

Components of Digital Accounting Practices

Data analytics includes several processes like prescriptive, predictive, diagnostic, and descriptive analysis, each explaining data differently (Shakya & Smys, 2021; Ali et al., 2020). In banking, data analytics is crucial for improving decisions and managing risks. Banks use predictive analytics to evaluate credit risk and predict defaults more accurately (Thomas et al., 2017; Ali et al., 2020). Data analytics helps in making better decisions by offering insights from large datasets while alsoenables data-driven strategies implementation. For example, banks use big data to refine investment strategies, make market trends and predict economic changes (Sun et al., 2018; Davenport & Ronanki, 2018).

Machine learning, or ML, is a branch of artificial intelligence where machines learn how to do something without being told how to do it. However, these systems work with data, make decisions, and cover different such processes with the least human interference (Kelleher, 2019; Beutel et al., 2019). Techniques in machine learning include reinforcement learning, semi-supervised learning, and supervised learning. In the banking industry, machine learning is used to prevent and detect fraudulent activities, thereby contributing to a higher level of security (Ngai et al., 2017; Sahin et al., 2020). Machine learning enhances customer experience and personalisation, and helps in understanding customer behaviour and transaction history (Choudhury & Kumari, 2020; Moreno et al., 2019).

Cloud computing provides accessible applications via the Internet from any location. With cloud storage, users of cloud computing software can access vast resources without limitations. This integration of cloud computing into accounting processes transforms information systems from isolated entities into powerful tools for gathering and analysing financial and non-financial data, enhancing organisational control (Lunga, 2021; Lambe & Ola, 2020). Users of cloud computing benefit from real-time accounting insights based on the provider’s expertise, including updates on evolving accounting standards (Lanz & Nearon, 2022; Polyviou et al., 2023).

Blockchain is a decentralized database technology invented by a user or a group of users using a pen name Satoshi Nakamoto in October 2008 to support Bitcoin purchases. The blockchain design has also been linked to Nakamoto’s protest of the global financial crisis 2008, whereby, through the banks’ agency of third-party intermediaries, the future of the international economic system was at stake (Sharma et al., 2022). Essentially, a blockchain is a series of blocks containing transactions. Cryptography secures these transactions with a chain of digital signatures. Each block groups transactions and links them to the previous block through consensus. This update is shared with all network users (Yi & Li, 2022; Sharma et al., 2022).

Financial Performance

Financial performance shows how well a business uses its assets. It measures how revenues are generated for investors. This includes benefits from shares and operations (Olayinka, 2022; Vibhakar et al., 2023). Stakeholders use it to judge a company’s strategies and operations (Godwin et al., 2020; Mishra & Kapil, 2018). Financial performance is usually checked yearly to compare similar firms in or across industries (Makinde, 2021; Pam, 2020). Key indicators like return on assets (ROA), return on equity (ROE), and net profit margin are common. ROA shows how well a company earns using its assets (Farouk & Hassan, 2018; Yusoff & Alhaji, 2017). Other performance measures include economic value added (EVA) and a balanced scorecard. EVA measures the value created beyond shareholders’ required return. It clarifies economic profit (Ilyas & Rafiq, 2019; Yıldız & Boz, 2021).

Theoretical Framework

This research is based on two key theories: the diffusion of innovation (DOI) theory by Rogers (1962) and the Technology Acceptance Model (TAM) by Davies (1989).

Diffusion of Innovations (DOI) Theory

DOI theory was created by Rogers in 1962. He introduced this idea in his work, “Diffusion of Innovations.” The theory explains how and why new ideas spread and describe the rate at which new technology moves through cultures. The theory has become essential for studying innovation in sociology, marketing, and IT (Rogers, 1962). The DOI theory shows key factors influencing digital accounting adoption. The theory suggests that banks consider advantages, compatibility, complexity, trialability, and observability.

Technology Acceptance Model

TAM was created by Fred Davis in 1989. Davis used TAM to explain and predict technology acceptance. TAM posited that two main factors drive technology acceptance. They are “perceived usefulness (PU)” and “perceived ease of use (PEOU).” These factors shape attitudes towards technology, affect the intention to use it, and lead to actual usage. Studies show that technology success depends on user acceptance (Rahi et al., 2019; Mansoori et al., 2020).

Integrating TAM helps to connect technology acceptance to efficiency, customer satisfaction, and financial results (Al-Okaily et al., 2020; Wamba et al., 2020).

Empirical Review

Data Analytics and Financial Performance

Al-Dmour et al. (2023) explored the factors affecting big data use in Jordanian banks. They built a framework using past studies and the Technology–Environment–Organisation (TOE) model. The study used a quantitative method. Data came from 235 senior and middle managers via online and paper questionnaires. Results showed banks’ use of big data is moderate, around 60%. The TOE model explained 61% of the variations in big data practices. Organisational factors were key predictors. Findings also revealed that big data use boosts bank performance.

Omoge, Gala, and Horky (2022) explored how AI-enabled CRM systems and the usage of technology affect consumer buying behaviour in Nigeria. They also looked at technology outages, which have not been widely studied. The study involved 400 customers from ten banks who were surveyed face-to-face. Findings indicate that technology use positively affects customer satisfaction and service quality. However, service quality did not directly impact buying behaviour. The research also found that technology downtime moderates the relationship between customer satisfaction, purchase intentions, and technology use in banking.

Automated Bookkeeping and Financial Performance

Srbinoska and Donovska (2023) surveyed 30 Macedonian firms to assess digitalisation in accounting. They found most firms adopted ERP technology, but AI was less common due to its innovative nature. Both AI and ERP are still in the early stages of implementation. Improvements noted were better reporting, decision-making, resource use, and faster processing.

Adeyemo and Okoronkwo (2024) studied how Artificial Intelligence (AI) affects bank operations in Lagos State, Nigeria. They identified AI technologies used by banks and their impact on the efficiency of five banks. The study surveyed 450 employees from these banks. Results showed that fraud detection, automation, and deep learning significantly improved efficiency. Chatbots had a positive but minor effect. The study concluded that AI improves bank operations in Nigeria. They recommend using AI—especially fraud detection, automation, and deep learning for better efficiency.

Machine Learning and Financial Performance

Tuteja et al. (2023) created a machine learning (ML) model to classify banks as low- or high-performers. They focused on non-performing assets (NPA) in Indian public sector banks (PSBs) from 2015 to 2020. They used unsupervised K-means clustering to form groups and the classification and regression tree (CART) for predictions. The model achieved a prediction accuracy of 0.9375, sensitivity of 0.8571, and specificity of 0.9600.

Atiku and Obagbuwa (2021) used eight machine-learning algorithms to predict bank performance in Nigeria based on human resources outcomes. They employed Python software with machine learning libraries. Results showed that human resources outcomes are vital for organisational performance. The models achieved accuracy rates between 74% and 81%.

Cloud-Based Accounting System and Financial Performance

Ahmad et al. (2024) assessed cloud-based accounting adoption and its impact in Jordan. They used a descriptive research design in Amman. They sampled 120 business administrators using purposive sampling. A questionnaire was the primary tool, validated for accuracy and language. Reliability was high at 0.84, according to Cronbach’s Alpha. Data were analysed using regression with a significance level of 0.05. The study found that cloud accounting speeds up task completion and improves information accuracy in real time.

Owolabi et al. (2023) studied how cloud accounting impacts financial reporting in Nigerian banks. Surveying IT staff from 10 banks, they found cloud accounting improved the relevance and accuracy of financial information. The study concluded that cloud accounting benefits financial reporting through cost savings, data security, and better access.

Blockchain Technology and Financial Performance

Gaya et al. (2022) studied digital banking’s impact on Kenyan banks’ financial performance. They looked at how banks are moving to digital platforms. They used both cross-sectional and longitudinal research methods. Data were taken from financial reports from 2019 to 2022. Mobile banking, agency banking, and online banking improved financial performance. However, ATM banking had a negative effect. They recommended that banks in Kenya focus more on mobile, agency, and online banking. ATM banking should be used cautiously due to its negative impact.

Odukwu et al. (2023) explored how digital accounting affects Nigerian banks’ financial performance. They used data from the annual reports of nine banks and found that blockchain technology (BCT) and cloud accounting (CLA) positively impacted return on assets (ROA). The study showed that digital accounting practices improved financial performance.

Research Method

The research design adopted in this study is the survey design, commonly used in business and management research (Bryman & Bell, 2016). The survey method facilitated gathering information on respondents’ characteristics, beliefs, and opinions (Creswell & Creswell, 2018).

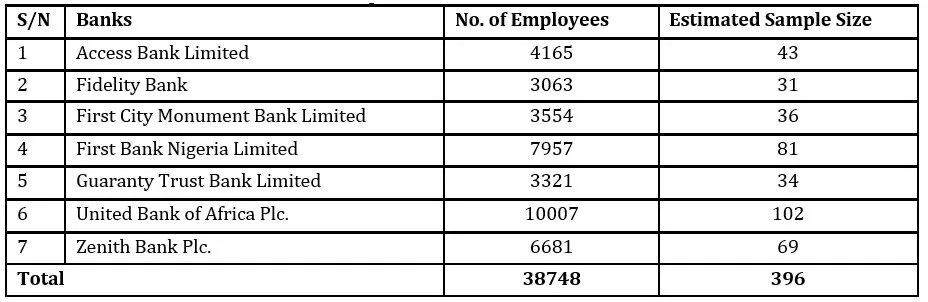

Following the studies by Oladejo and Yinus (2020), Elegunde and Shotunde (2020), and Adeyemo and Okoronkwo (2024), the target population for this study is the deposit money banks licensed with international authorisation. These banks are Access Bank Limited, Fidelity Bank Plc., First City Monument Bank Limited, First Bank Nigeria Limited, Guaranty Trust Bank Limited, United Bank of Africa Plc., and Zenith Bank Plc. These banks were selected because they already have an international authorisation, which means they are already exposed to advanced technological capabilities. They also have the resources to adopt and implement digital accounting practices to enhance performance (Kama & Adigwe, 2020; Adeniran & Adediran, 2019). In addition, these banks play essential roles in the Nigerian economy and have the infrastructure to implement and benefit from advanced digital accounting technologies (CBN, 2021). The total number of employees of the seven banks is 38748, as presented in Table 1 (see Appendix 1). Using Taro Yamane’s (1967) formula based on the total population size, 396 employees were selected. The distribution of this 396 to each of the seven DMBs is also contained in Table 1 (see Appendix 1).

The research instrument for this research study was a self-administered questionnaire developed on a five-point Likert scale ranging from strongly agree (5) to strongly disagree (1). The internal consistency method (Cronbach Alpha) was employed to test reliability, and each variable had a coefficient value above 0.6. The study’s dependent and independent variables were measured on a five-point Likert scale following the studies of Igbekoyi et al. (2023) and Ajayi and Akinrinola (2023).

Using the SPSS software, multiple linear regression analysis was conducted to isolate the impact of the independent variable (digital accounting practices) on the dependent variable (financial performance measured as return on asset, ROA). The multiple regression model adopted for the study is as follows:

Where:

β0 and β1 – β5 represent the Intercept and regression parameters; μ is the error term; DA, AB, ML, CAS, and BLT represent data analytics, automated bookkeeping, machine learning, cloud-based accounting systems and blockchain technology.

Data Analysis and Results

Analysis was done based on 379 responses received out of the expected 396 responses. This response represents 95.7% of the total expected responses, which is significantly valid and credible for this analysis.

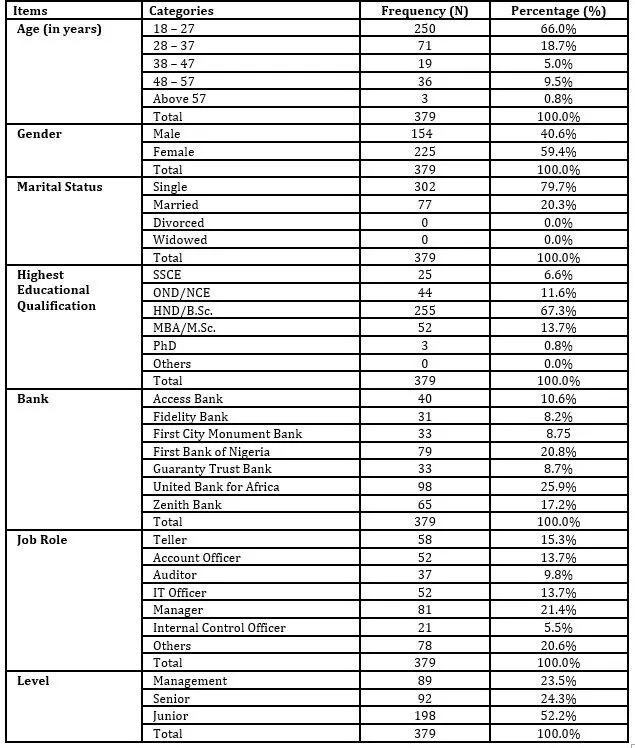

Table 2 contains the demographic information of our respondents. The majority of the respondents, 66.0% of the sample aged 18 to 27 years, suggest that the participants are likely to be relatively new to the workforce and possibly more adaptable to digital accounting practices. Those aged 28 to 37 make up 18.7%, and the numbers decrease significantly in older age groups. Only a tiny percentage of respondents are above 48 years old. This indicates that our study mainly reflects the views of younger bank employees.

Table 2: Socio-Demographic Distribution of the Respondents

Source: Field Survey (2024)

There are more female respondents (59.4%) than male respondents (40.6%). Most respondents are single (79.7%), while only 20.3% are married. A large portion of the respondents, 67.3%, hold HND/B.Sc. Degree while 13.7% hold MBA/M.Sc. Degree. This suggests that respondents have the knowledge and skills to understand and implement digital accounting practices effectively. The respondents come from various banks, with the most prominent groups being the United Bank for Africa (25.9%), First Bank of Nigeria (20.8%), and Zenith Bank (17.2%). This variety ensures that the study captures a broad perspective across different financial institutions. Participants hold diverse job roles, with the largest groups being Managers (21.4%), Tellers (15.3%), and Account Officers (13.7%). 20.6% of the respondents were from other departments that were not listed.

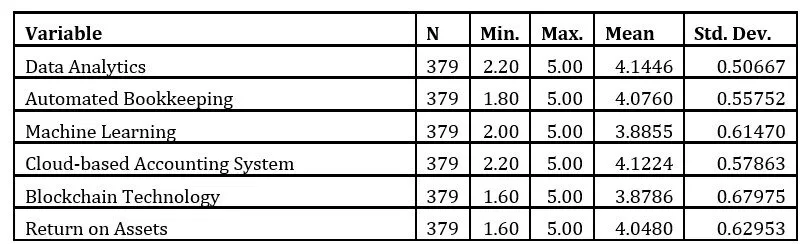

Table 3: Descriptive Statistics of the Study’s Variables

Source: Computed by the Authors (2024)

Results in Table 3 revealed that, on a five-point scale, responses from the respondents tend toward agreement with statements on each variable of the study. Data analytics recorded the highest mean value of 4.14; this is closely followed by cloud-based accounting system (4.12), automated bookkeeping (4.07), and return on assets (4.05). Machine learning and blockchain technology recorded average scores of 3.89 and 3.88, respectively.

The characteristics of the respondents, such as age, educational level, and job role, could influence this response. Since most of the respondents are young adults and are highly educated, they are usually more open to and involved in innovative practices. Moreover, those in managerial or senior roles also seem to have a better understanding of the strategic importance of innovation, are more open to new ways of simplifying complex financial processes and are more likely to be more conversant with the implications digital accounting practices have for financial performance.

Test of Hypothesis

The central null hypothesis of the study was tested using the questionnaire statements on data analytics, automated bookkeeping, machine learning, cloud-based accounting systems, blockchain technology, and return on assets. The results are presented in Tables 4 and 5.

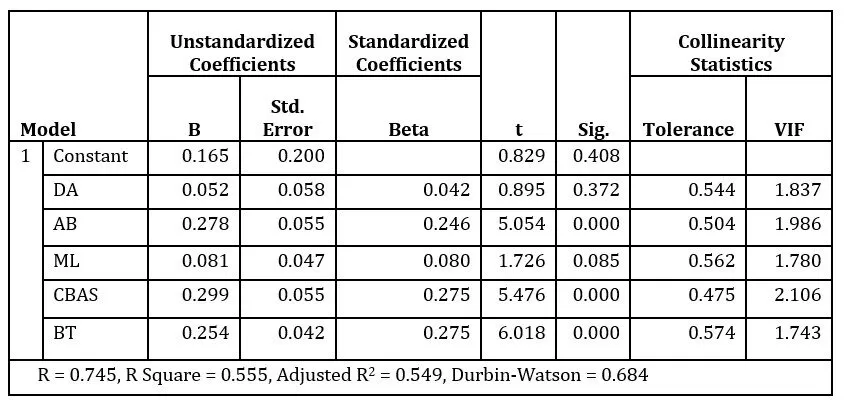

Table 4: Multiple Regression Results

Source: Computed by the Authors (2024)

Table 5 presents the combined effects of the independent variables on the return on assets (ROA). The R-value is about 75%, indicating the level of relationship between the five independent variables and ROA, the dependent variable. The adjusted R2 is about 55%, which shows the extent to which the independent variables could explain the variations in ROA. The collinearity statistics revealed that VIF statistics for the variables were far below 10, and tolerance statistics were well above 0.2. This outcome suggests no problem of multicollinearity among the predictor variables. Further, data analytics and machine learning do not significantly impact ROA (p> 0.05), whereas automated bookkeeping, cloud-based accounting systems, and blockchain technology significantly affect ROA.

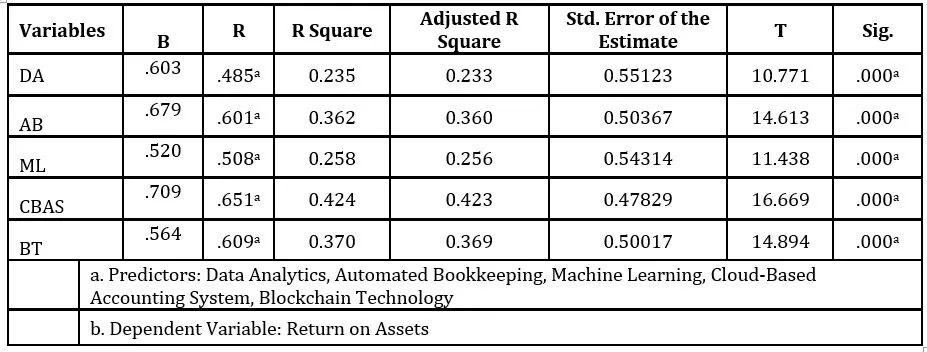

Table 5: Individual Regression Results

Source: Computed by the Authors (2024)

Table 5 shows results when each predictor variable is regressed against the outcome variable. The results revealed that each of data analytics, automated bookkeeping, machine learning, cloud-based accounting systems, and blockchain technology has a positive and statistically significant impact on ROA (t = 10.771, 14.613, 11.438, 16.669, 14.894; p < 0.05). The R statistics for each variable reveal a considerable association with ROA. The coefficient of determination (R2) shows that each variable could explain the changes in ROA.

Discussion of Findings

The result of the central hypothesis showed that digital accounting practices have a positive and statistically significant impact on ROA. Previous empirical studies in developed and other developing economies and Nigeria echo this same result. For instance, Al-Dmour et al. (2023) and Igbekoyi et al. (2023) found that data analytics positively impact bank financial performance, improve operational efficiency, enhance financial stability, and improve the efficacy of accounting practices. Srbinoska and Donovska (2023) and Adeyemo and Okoronkwo (2024) found that automated bookkeeping and robotic process automation (RPA) have been shown to improve process efficiency, reduce error rates, lead to more accurate and timely financial reporting, and improve operational efficiency in Nigerian banks, which translates into better financial performance outcomes.

Regarding machine learning, Atiku and Obagbuwa (2021) and Petropoulos et al. (2023) found that these techniques offer high precision in predicting credit ratings and loan eligibility, aid operational efficiency, and potentially enhance financial performance metrics. Cloud-based accounting systems have also enhanced task completion and resource efficiency, improved performance expectancy and decision quality, and enhanced overall financial outcomes through better data management and decision-making (Ahmad et al.2024; Akai et al. 2023). Lastly, the significant positive effect of blockchain technology on ROA is supported by the findings of Odukwu et al. (2023) and Gaya et al. (2022), which show that blockchain technology enhances efficiency and reduces costs.

Conclusion and Recommendations

This study examined the effect of digital accounting practices on the financial performance of licensed deposit money banks in Nigeria. Specifically, the study investigated the impact of data analytics, automated bookkeeping, machine learning, cloud-based accounting systems, and blockchain technology on the financial performance of deposit money banks in Nigeria. These digital accounting practices significantly affected key performance metrics, measured by the return on assets of deposit money banks in Nigeria. This underscores the transformative potential of digital accounting in enhancing the financial performance of deposit money banks in Nigeria.

The study recommended that deposit money banks in Nigeria should enhance employees’ capabilities in implementing and optimizing digital accounting tools to achieve enhanced trust in banking operations and improve financial performance.

References

Adeyemo, F. S., & Okoronkwo, G. (2024). Artificial intelligence and operational efficiency of deposit money banks in Lagos State, Nigeria. In Technology management and the challenges of sustainable development: A Festschrift for Professor Matthew Olugbenga Ilori (pp. 4–15).

Akai, N. D., Ibok, N., & Akinninyi, P. E. (2023). Cloud accounting and the quality of financial reports of selected banks in Nigeria.European Journal of Accounting, Auditing and Finance Research, 11(9), 18–42.

Akinbode, F. A., Omoba, O. O., Okewale, J. A., & Adedeji, S. B. (2023). International financial reporting standards (IFRS) disclosure and financial performance of deposit money banks (DMBS) in Nigeria.Journal of Management Science and Entrepreneurship.

Al-Dmour, H., Saad, N., Basheer Amin, E., Al-Dmour, R., & Al-Dmour, A. (2023). The influence of the practices of big data analytics applications on bank performance: Filed study.VINE Journal of Information and Knowledge Management Systems, 53(1), 119–141. https://doi.org/10.1108/VJIKMS-09-2021-0200

Ali, Q., Salman, A., Yaacob, H., Zaini, Z., & Abdullah, R. (2020). Does big data analytics enhance sustainability and financial performance?The case of ASEAN banks.The Journal of Asian Finance, Economics and Business, 7(7), 1–13. https://doi.org/10.13106/jafeb.2020.vol7.no7.001

Al-Okaily, M., Al-Okaily, A., Al-Kasasbeh, M., Al-Kasasbeh, R., & Gharaibeh, M. (2020). Digital transformation and financial performance of small and medium enterprises: An empirical study in Jordan.Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 124. https://doi.org/10.3390/joitmc6040124

Amahalu, N. (2020). Effect of e-accounting systems on financial performance of quoted deposit money banks in Anambra State. Available at SSRN 3704503. https://doi.org/10.2139/ssrn.3704503

Atiku, S. O., & Obagbuwa, I. C. (2021). Machine learning classification techniques for detecting the impact of human resources outcomes on commercial banks’ performance.Applied Computational Intelligence and Soft Computing, 2021(1), 7747907. https://doi.org/10.1155/2021/7747907

Audu, S. I. (2020). National transparency and the performance of the financial market in Nigeria.International Journal of Business and Finance Management Research, 8(1), 10–14.

Beutel, J., List, S., & von Schweinitz, G. (2019). Does machine learning help us predict banking crises?Journal of Financial Stability, 45, 100693. https://doi.org/10.1016/j.jfs.2019.100693

Bhimani, A. (2020). Digital data and management accounting: Why we need to rethink research methods.Journal of Management Control, 31(1), 9–23. https://doi.org/10.1007/s00187-020-00302-7

Bhimani, A. (2021). Accounting disrupted: How digitalisation is changing finance. John Wiley & Sons. https://doi.org/10.1002/9781119780608

Broby, D. (2021). Financial technology and the future of banking.Financial Innovation, 7(1), 1–19. https://doi.org/10.1186/s40854-021-00248-8

Byrd, G. T., & Ding, Y. (2023). Quantum computing: Progress and innovation.Computer, 56(1), 20–29. https://doi.org/10.1109/MC.2022.3204715

Choudhury, N., & Kumari, P. (2020). Role of machine learning in banking industry.International Journal of Management, 11(9), 8–14. https://doi.org/10.34218/IJM.11.9.2020.002

Coman, D. M., Ionescu, C. A., Duică, A., Coman, M. D., Uzlau, M. C., Stanescu, S. G., & State, V. (2022). Digitisation of accounting: The premise of the paradigm shifts of the role of the professional accountant.Applied Sciences, 12(7), 3359. https://doi.org/10.3390/app12073359

Creswell, J. W., & Creswell, J. D. (2018). Research design: Qualitative, quantitative, and mixed methods approach.

Davenport, T. H., & Ronanki, R. (2018). Artificial intelligence for the real world.Harvard Business Review, 96(1), 108–116.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology.MIS Quarterly, 13(3), 319–340. https://doi.org/10.2307/249008

Elegunde, A. F., & Shotunde, O. I. (2020). Effects of artificial intelligence on business performance in the banking industry: A study of access bank plc and united bank for Africa-UBA.IOSR Journal of Business and Management (IOSR-JBM) Ser. IV, 22(5), 41–49.

Eswaran, S., Rani, V., Ramakrishnan, J., & Selvakumar, S. (2022). An enhanced network intrusion detection system for malicious crawler detection and security event correlations in ubiquitous banking infrastructure.International Journal of Pervasive Computing and Communications, 18(1), 59–78. https://doi.org/10.1108/IJPCC-08-2021-0208

Fijabi, L. K., & Lasisi, O. R. (2023). Accounting practices in a digitalised world: Nigerian prospective.African Journal of Accounting and Financial Research, 6(1), 63–82.

Gaya, F., Omoro, N., & Kinyua, H. W. (2022). Digital banking and financial performance of listed commercial banks in Kenya.African Development Finance Journal, 4(3), 169–197.

Godwin, J., Kent, P., & Stewart, J. (2020). Corporate governance mechanisms and corporate performance.Accounting Research Journal, 33(1), 129–143. https://doi.org/10.1108/ARJ-08-2017-0137

Haabazoka, L. (2019). A study of the effects of technological innovations on the performance of commercial banks in developing countries: A case of the Zambian banking industry. In The future of the global financial system: Downfall or harmony 6 (pp. 1246–1260). Springer International Publishing. https://doi.org/10.1007/978-3-030-12453-3_129

Igbekoyi, O. E., Oke, O. E., Awotomilusi, N. S., & Dagunduro, M. E. (2023). Assessment of big data and efficacy of accounting practice in Nigeria.Asian Journal of Economics, Finance and Management, 297–312.

Ilyas, M., & Rafiq, M. (2019). Economic value added or accounting earnings? What explains market value in Pakistan?International Journal of Economics and Finance, 11(2), 103–110. https://doi.org/10.5539/ijef.v11n2p103

Kaur, S. J., Ali, L., Hassan, M. K., & Al-Emran, M. (2021). Adoption of digital banking channels in an emerging economy: Exploring the role of in-branch efforts. Journal of Financial Services Marketing, 26, 107–121. https://doi.org/10.1057/s41264-020-00077-8

Kelleher, J. D. (2019). Deep learning. MIT Press. https://mitpress.mit.edu/9780262537551/deep-learning/

Laghari, A. A., Wu, K., Laghari, R. A., Ali, M., & Khan, A. A. (2022). A review and state of art of Internet of Things (IoT). Archives of Computational Methods in Engineering, 29, 1395–1413. https://doi.org/10.1007/s11831-020-09531-w

Lambe, I., & Ola, M. H. (2020). Effect of loan loss provision on revenue recognition of deposit money banks (DMBs) in Nigeria. Binghan International Journal of Accounting and Finance (BIJAF), 1-13.

Lanz, J., & Nearon, B. (2022). Risk impacts of SaaS cloud computing. CPA Journal, 92.

Lunga, D. (2021). Benefits and challenges of cloud-based enterprise resource planning (ERP): A case of Bank of Abyssinia (Doctoral dissertation, St. Mary’s University).

Makinde, M. S. (2021). Board characteristics, asset quality and financial performance of deposit money banks in Nigeria (master’s thesis, Kwara State University (Nigeria)).

Mansoori, A., Mohammadi, S., Taheri, A., & Niknejad, N. (2020). The role of perceived ease of use and perceived usefulness in acceptance of mobile health applications. Journal of Advanced Pharmaceutical Technology & Research, 11(3), 87–91. https://doi.org/10.4103/japtr.JAPTR_173_20

Mishra, C. S., & Kapil, S. (2018). Effect of ownership structure and board structure on firm value: Evidence from India. Corporate Governance: The International Journal of Business in Society, 18(5), 781–803. https://doi.org/10.1108/CG-03-2018-0110

Moreno, A., Redondo, T., & Rodríguez, M. B. (2019). The role of machine learning in customer experience management. Journal of Business Research, 104, 623–630. https://doi.org/10.1016/j.jbusres.2018.11.040

Mujiono, M. N. (2021). The shifting role of accountants in the era of digital disruption. International Journal of Multidisciplinary: Applied Business and Education Research, 2(11), 1259–1274.

Ngai, E. W., Hu, Y., Wong, Y. H., Chen, Y., & Sun, X. (2017). The application of data mining techniques in financial fraud detection: A classification framework and an academic review of literature. Decision Support Systems, 50(3), 559–569. https://doi.org/10.1016/j.dss.2010.08.006

Ngozi, O. J., Chukwudi, O. K., & George, A. A. (2023). Banks diversification and return on assets of deposit money banks in Nigeria. International Journal of Advanced Academic Research, 9(9), 86–104.

Ngwengeh, B., Messomo, E., & Mbu, S. (2021). The influence of digital financial services on the financial performance of commercial banks in Cameroon. European Scientific Journal ESJ, 17, 1857–7881. https://doi.org/10.19044/esj.2021.v17n30p26

Odukw, V. C., Eke, P., Nwankwo, C., & Stanley, M. O. (2023). Digital accounting practices and financial performance of licensed deposit money banks in Nigeria. Journal of Production, Operations Management and Economics (JPOME), 3(02), 32–41. https://doi.org/10.55529/jpome.32.32.41

Odunayo, J., Akintoye, R. I., Aguguom, T. A., Sanyaolu, A. W., Omobowale, A., & Osunusi, K. A. (2023). Digital disruption of accounting information and quality of financial reporting of listed money deposit banks in Nigeria. International Journal of Applied Economics, Finance and Accounting, 17(2), 337–352.

Ogunsola, E. A. E. (2021). Effect of cloud accounting on the financial reporting quality of SMEs in Nigeria.

Oino, I. (2019). Do disclosure and transparency affect the bank’s financial performance? Corporate Governance: The International Journal of Business in Society, 19(6), 1344–1361. https://doi.org/10.1108/CG-09-2018-0289

Okika, C. E., & Udeh, F. N. (2019). Electronic accounting and bank operations: Evidence from quoted deposit money banks in Nigeria. Journal of Global Accounting, 6(1), 88–103.

Oladejo, M. O., & Yinus, S. O. (2020). Electronic accounting practices: An effective means for financial reporting quality in Nigeria deposit money banks. International Journal of Managerial Studies and Research, 8(3), 13–26. https://doi.org/10.20431/2349-0349.0803003

Oladejo, M. O., Yinus, S. O., & Aina-David, O. A. (2020). Implementation of accounting technology and financial reporting quality of quoted deposit money banks in Nigeria. International Journal of Managerial Studies and Research, 8(2), 13–21. https://doi.org/10.20431/2349-0349.0802003

Olayinka, A. A. (2022). Financial statement analysis as a tool for investment decisions and assessment of companies’ performance. International Journal of Financial, Accounting, and Management, 4(1), 49–66. https://doi.org/10.35912/ijfam.v4i1.325

Omoge, A. P., Gala, P., & Horky, A. (2022). Disruptive technology and AI in the banking industry of an emerging market. International Journal of Bank Marketing, 40(6), 1217–1247. https://doi.org/10.1108/IJBM-03-2021-0112

Owolabi, S., Oyegoke, K. S., & Olalere, M. (2023). Cloud accounting and financial reporting quality of deposit money banks (DMBS) in Nigeria. International Journal of Management Studies and Social Science Research, 5(4), 98-110. https://doi.org/10.56293/IJMSSSR.2022.4666

Pam, B. (2020). Effect of cashless policy on the financial performance of selected deposit money banks (DMBs) in Nigeria. Bingham International Journal of Accounting and Finance (BIJAF), 304–319.

Petropoulos, A., Siakoulis, V., Stavroulakis, E., & Vlachogiannakis, N. E. (2020). Predicting bank insolvencies using machine learning techniques. International Journal of Forecasting, 36(3), 1092–1113. https://doi.org/10.1016/j.ijforecast.2019.12.006

Polyviou, A., Pouloudi, N., & Venters, W. (2023). Cloud computing adoption decision-making process: A sensemaking analysis. Information Technology & People. https://doi.org/10.1108/ITP-06-2022-0449

Rahi, S., Ghani, M. A., & Ngah, A. H. (2019). Integration of unified theory of acceptance and use of technology in internet banking adoption setting: Evidence from Pakistan. Technology in Society, 58, https://doi.org/10.1016/j.techsoc.2019.01.003

Rahman, M., Ming, T. H., Baigh, T. A., & Sarker, M. (2023). Adoption of artificial intelligence in banking services: An empirical analysis. International Journal of Emerging Markets, 18(10), 4270–4300. https://doi.org/10.1108/IJOEM-09-2021-1379

Rogers, E. M. (1983). Diffusion of innovations (3rd). New York: The Free Press.

Sahin, Y. G., Bulkan, S., & Duman, E. (2020). A cost-sensitive decision tree approach for fraud detection. Journal of Financial Crime, 27(1), 251–265. https://doi.org/10.1108/JFC-03-2019-0029

Samuel, D., & Grace, O. (2022). Information technology control and fraud risk detection in deposit money banks (DMBs) in Nigeria. Journal of Financial Crime, 27(1), 273–284. https://doi.org/10.1108/JFC-03-2019-0029

Shakya, S., & Smys, S. (2021). Big data analytics for improved risk management and customer segregation in banking applications. Journal of IoT in Social, Mobile, Analytics, and Cloud, 3(3), 235-249.

Sharma, D. K., Gupta, A., & Gupta, T. (2022). Development of Blockchain-Based Cryptocurrency. In Applications of Blockchain and Big IoT Systems(pp. 341-371). Apple Academic Press.

Sun, Z., Sun, L., & Strang, K. D. (2018). Big data analytics services for enhancing business intelligence. Journal of Computer Information Systems, 58(2), 162-169.

Thomas, L. Crook, J., & Edelman, D. (2017). Credit Scoring and Its Applications (2nd). Society for Industrial and Applied Mathematics (SIAM). https://epubs.siam.org/doi/epdf/10.1137/1.9781611974560.fm.

Vibhakar, N. N., Tripathi, K. K., Johari, S., & Jha, K. N. (2023). Identification of significant financial performance indicators for the Indian construction companies. International Journal of Construction Management, 23(1), 13-23. https://doi.org/10.1080/15623599.2020.1844856

Wamba, S. F., Akter, S., Edwards, A., Chopin, G., & Gnanzou, D. (2020). How ‘big data’ can make big impact: Findings from a systematic review and a longitudinal case study. International Journal of Production Economics, 165, 234-246.

Wamba-Taguimdje, S. L., Wamba, S. F., Kamdjoug, J. R. K., & Wanko, C. E. T. (2020). Influence of artificial intelligence (AI) on firm performance: The business value of AI-based transformation projects. Business Process Management Journal, 26(7), 1893-1924.

Yıldız, M. S., & Boz, H. (2021). The impact of economic value added on shareholder value in emerging markets. Borsa Istanbul Review, 21(4), 367-376.

Yusoff, W. F. W., & Alhaji, I. A. (2017). Corporate governance and firm performance: Evidence from Malaysia. International Journal of Economics and Financial Issues, 7(4), 1-6.

Appendix 1

Table 1: Population and Sample of Study

Source: Employees analysis in the latest annual report (2023) of each bank