Ana Filipa M. ROQUE, Maria-Céu G. ALVES and Mário RAPOSO

NECE Research Center in Business Sciences, University of Beira Interior, Covilhã, Portugal

Volume 2019,

Article ID 437064,

IBIMA Business Review,

11 pages,

DOI: 10.5171/2019.437064

Received date: 19 February 2019; Accepted date: 30 April 2019; Published date: 19 June 2019

Cite this Article as:

Ana Filipa M. ROQUE, Maria-Céu G. ALVES and Mário RAPOSO (2019)," The Use of Management Accounting and Control Systems in the Internationalization Strategy: A Process Approach", IBIMA Business Review, Vol. 2019 (2019), Article ID 437064, DOI: 10.5171/2019.437064

The general objective of this study is to contribute to the understanding of the relationship between strategy and organizational structure, namely how the use of Management Accounting and Control Systems (MACS) contributes to the successful implementation of the internationalization strategy and consecutively to the improvement of the company’s performance.We conducted a single case study in a Portuguese company in the services sector using interview and desk research. The company’s internationalization model (IM) was characterized and studied through a process approach. Subsequently, the relationship between the MACS use and the implementation of the internationalization strategy were analyzed. Results suggest that MACS were not only instrumental to the implementation of the company’s internationalization strategy, but they also “shaped” it, and were “shaped” by it.

The study contributes to the MACS literature showing how the internationalization process and the MACS use fit to improve the company’s performance.

Keywords: Internationalization, Internationalization strategy, I-Model, Management Accounting and Control Systems.

Introduction

The internationalization is currently considered as one of the companies’ competitiveness factors and growth

strategies (Welford and Prescott, 1994). However, the adoption of this strategy is not simple (Fernández and Nieto, 2005). The current instability forces and constrains the companies to constantly adjust their activities in order to grow. In this process, there is a systematic adaptation between strategy and structure.

Chandler (1962) concluded that the companies’ structure was adjusted to their strategies, thus finding an intimate relationship between the strategy and the organizational structure. Therefore, it is perceptible that the structure depends on the contingencies of each organization at a given moment. Hence, there are variables that contribute to this, such as strategy, environment, and technology (Chandler, 1962). This fact leads several authors to assert that there is no single, universal technical structure of management control. It changes with the company’s internal and external characteristics (Otley, 1980; Chenhall, 2003).

The relationship between internationalization and MACS has been widely studied in the literature (Haldma and Lääts, 2002; Luther and Longden, 2001; Carenzo et al., 2011), however there is no reference to the relationship between a particular IM and the company’s MACS use during the development of the process.

Thus, with this paper, we try to answer the following questions: (1) How does the internationalization strategy imply (or not) changes in the MACS use? and (2) How does the company’s MACS use facilitate (or not) the implementation of the internationalization strategy?

A qualitative research study was developed, through an exploratory case study, in a Portuguese company in the service sector, in engineering and in consulting. This company represents a successful case of the implementation of an innovation-related IM (I-Model).

In terms of structure, after this introductory section, this study is composed by a literature review section. Next, the methodology is presented and the empirical study is analyzed. Finally, in a third section, we present the results’ analysis and discussion. We also present the study’s conclusions, its limitations and some lines for future research.

Literature Review

The internationalization process

The internationalization of a company consists in the extension of its strategies of products-markets to other countries, from which a total or partial replica of its operational chain results (Roque et al. 2018a; Roque et. al. 2019). Faced with ever-changing markets, the companies must necessarily adapt to their environment, in order to respond to the emerging challenges. The need for innovation at an organizational level has become permanent.

Murteira (1997) states that the degree of an organization’s innovation can be justified by three levels of behavior of the company: (1) the external level, including products and markets; (2) the internal level, namely; technological equipment and processes, human resources, organization and R&D, and (3) the level of systemic positioning, internationalization and trans-nationalization strategies, mergers, strategic alliances, joint ventures, etc. In this last level (the level of an organizational behavior of systemic positioning), the internationalization process of the I-Model company is seen as an innovation and underlies an incremental performance in the internationalization of the companies (Andersen, 1993; Rogers, 1962).

Innovation models view the internationalization as a process in which the steps are analogous to adopting a new product (Rogers, 1962). Each stage in the process is seen as an innovation for the company (Bilkey and Tesar, 1977, Cavusgil, 1980 and Reid, 1981), allowing contributing to its incremental development.

Some approaches to the I-Model gradually represent the various phases of the internationalization and they consider that the action of an external agent is an incentive to start the process. However, according to Andersen (1993), the interpretation of the differences about the internationalization process’ nature is only a semantic question. This author argues that this model is developed based on innovation in the business perspective. To Lin (2010), the different stages of the I-Model are related to the export rate, which, in turn, is proportional to the company’s turnover, and the company progresses in the process as turnover increases.

There are many models developed that compete for the I-Model classification, namely with regard to the companies’ involvement in the export process and in the perspective of adopting innovation.

In our study, we analysed the four most relevant innovation models in different phases of the process, such as Bilkey and Tesar (1977), Cavusgil (1980), Czinkota (1982) and Reid (1981), and also we highlight the study of Leonidou and Katsikeas (1996) which contributes in this area.

Analysing the different perspectives of the most relevant innovation models, we conclude that the internationalization decision is affected by different Push or Pull forces (Andersen, 1993).

To Bilkey and Tesar (1977) and Czinkota (1982), the model is divided into six phases. The company is not interested in exporting, in phase 1 and it only satisfies unsolicited orders. It is, however, partially interested in phase 2 which leads to the conclusion that there is a “push” or an external change mechanism that initiates the export decision. To Cavusgil (1980) and Reid (1981), the model is divided into five phases and the company is more interested in exports and it is more active during the early stages. In these models, there is a “pull” mechanism or an internal change that explains the transition to the next phases (Lin, 2010).

Leonidou and Katsikeas’ (1996) model allows characterizing, the companies’ exporting process in three phases: (1) pre-involvement, which assembles the companies that only sell domestically/nationally and which are not interested in exports, and also those that consider the possibility of exporting and those that have already developed this process and have since been interrupted; (2) initial involvement that gathers companies that export sporadically, and (3) advanced involvement, which involves companies that export regularly to various markets and which may have characteristics that commit them to a greater involvement in the internationalization.

Management Accounting and Control Systems use

The MACS is a structure that simultaneously contemplates an information network, in which the system collects, processes and communicates information and other types of relationships that discipline and influence behaviours’ (Roque et al, 2018 b).

A MACS’ dimensions’ approach is usually used in management accounting research, because it allows considering specific, more tangible aspects and, at the same time, more subjective, more intangible objectives which a macro perspective would not allow.

In this paper, we consider two of the most referenced dimensions in the MACS literature, namely; the diagnostic and interactive uses of MACS (Cf. p. e. Agbejule, 2006; Ahrens and Chapman, 2004; Ballvé, 2006; Bisbe and Otley, 2004; Hartmann and Vaassen, 2003; Henri, 2006; Naranjo-Gil and Álvarez-Dardet, 2006; Naranjo-Gil and Hartmann, 2006, 2007; Roberts, 2003; Sjoblom, 2003; Thorén and Brown, 2004), grouped into a category named the style of use of the MACS (Novas et al., 2017).

Some authors (Agbejule, 2006; Bisbe and Otley, 2004; Henri, 2006) argue that there is a complementarity between the various system’s dimensions. In the case of the information use, an association is detected between the “diagnostic” and the “interactive” dimensions.

These dynamics, according to Simons (1991, 1995), allow managing the organizational tensions that derive from the users’ interests, either from the “diagnostic” type dimension information associated to a more traditional role, or from the one that derives from a system with a more “interactive” role associated to more active systems.

Thus, it is natural that, as the MACS’ use evolves from a “diagnostic” type to a combination of both or only to an “interactive” system, the dynamics generated by the contradictory, but complementary, elements inherent to each of the dimensions’ increases (Naranjo-Gil and Hartmann, 2006; Tuomela, 2005; Henri 2006).

The systems in which the style of information use is “diagnostic” are formal systems that the managers use to control results and correct deviations from the established performance objectives. These are limited systems, regarding the search for innovative solutions and the identification of opportunities, once the attentions are essentially addressed to the performance variables (Simons, 1995). These are systems characterized by the ability to evaluate processes’ outputs, by the existence of measures that exist to allow for comparison and corrective measures to deviations which will equate it with the traditional definition of management control (Simons, 1991). Success factors are simply defined, and involvement is simply implicit in an already deliberate strategy (Pešalj, et al., 2018).

The “interactive” type systems are systems that foster innovation, learning and the search for new solutions which triggers the emergence of new strategies, as their participants interact and respond to emerging opportunities and threats (Novas et al., 2017). These are less restricted, more superficial and, at the same time, more informal control systems. The control is focused on communication and cooperation, which allows information to flow and fosters debate and dialogue within the organization itself, thus forming the fundamental mechanisms for knowledge creation and integration (Agbejule, 2006). In these systems, the manager reports the system’s use personally, regularly and frequently to his subordinates. It is used to define regular meeting schedules of interconnection with direct subordinates and others in order to review data and the action plan’s results (Simons, 1991).

The relationship betweenMACS (use) and the I-Model

The relationship between the internationalization and the MACS use is systematically adapted, since we assume, similarly to several authors (Samson et al., 1991; Simons, 1987, 1990; Henri 2006), that the strategy changes and conditions the organizations’ structure, namely; the MACS (Chandler, 1962).

This structure adaptation to the strategy is easily understood in models based on innovation, such as the I-Model where the simple export process is, as we have seen, considered an innovative process (Rogers, 1962; Andersen, 1993).

Gomez-Conde et al. (2013) studied the internationalization’s direct effect, mediating effect and moderating effect on the relationship between the MACS’ interactive use and innovation. Despite the direct and positive relationships between the internationalization degree and innovation, the authors failed to demonstrate the mediating or moderating effects of internationalization in the relationship between the MACS and innovation. However, the authors found statistically significant relationships when the sample is disaggregated according to the internationalization degree. The authors argue that a less interactive use can jeopardize innovation;

“In highly internationalized companies, it may occur that too high an internationalization degree is reached that it may be excessive or inadequate and may create dysfunctions. The results suggest that the less interactive use of the MCSs can contribute to reducing the risk of internationalization, but will consequently mitigate the positive effect that the interactive use of the MCSs could have on the Commitment to Innovation.” (Gomez-Conde et al., 2013, p. 62)

One of this work’s great contributions is the conclusion they have reached, since the MACSs’ interactive use is not necessarily the only source of information and motivation that leads companies to a greater commitment to innovation. The impact of the MACSs’ interactive use varies according to the internationalization level the company is at.

Hence, the I-Model supports itself in a MACS that includes a dynamic style of information use (Simons, 1995), the diagnostic and interactive type that enables to make comparisons and take corrective measures to reduce deviations, as well as in systems that allow communication and cooperation in order to let information flow and develop knowledge (Simons 1991, 1995), essential for the development of IM, such as I-Model.

Methodology

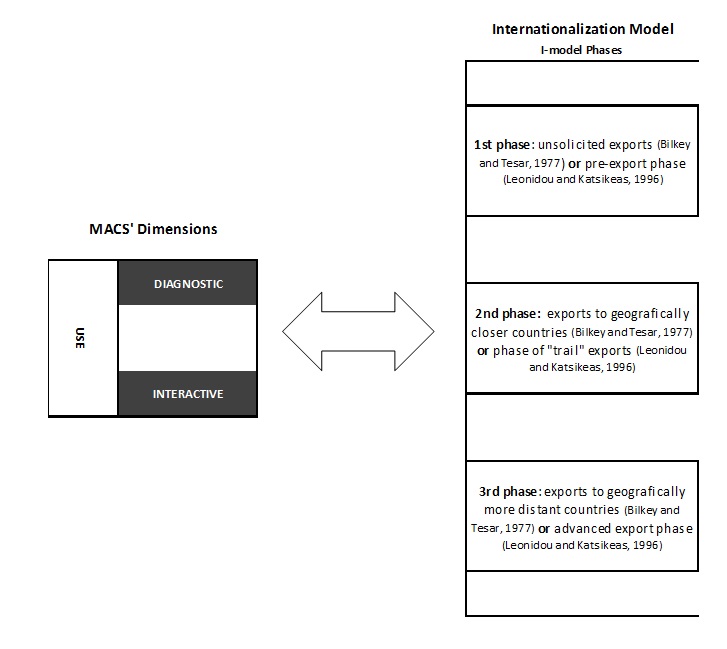

In order to examine the relationship between the model adopted in the internationalization process and the MACS use, and similarly to other studies (Simons, 1990; Archer and Otley, 1991; Francisco and Alves, 2012) a case study was developed in a Portuguese company in the services sector. Our research questions, how does the internationalization strategy imply (or not) changes in the MACS use?, and how does the company’s MACS use facilitates (or not) the implementation of the internationalization strategy?, which call for a qualitative approach. According to Yin (2014), when it comes to “why” or “how” questions, conducting a case study is the most appropriate research method. The proposed research model is presented in figure 1

Two MACS use dimensions (interactive use and diagnostic use) were analysed. These dimensions were related to the I-Model characteristics and to the different phases of evolution of the model, as proposed by Bilkey and Tesar (1977) and by Leonidou and Katsikeas (1996).

We assume that the I-Model must be supported by a “diagnostic” use of the MACS in the initial stage of the process development (phase 1), and by a more interactive use in the subsequent phases (phases 2 and 3).

Figure 1: Research Model

Source: Own

The company studied develops its activity in the construction industry and civil engineering sector, namely engineering projects elaboration, and was selected by convenience, due to its participation in the “IX Symposium COTEC Europe”, on February 10, 2017. This company assumed that the commitment to the internationalization of its services was based on innovation, which simultaneously boosted its performance and organizational growth.

Hence, we have sought to understand how the IM influences and/or is influenced by the MACS use. To this end, and similar to other studies (Naor et al., 2015; Pellinen et al., 2016) a qualitative research work was developed, embodied in a single case study (Yin, 1993, 2014). The data collection was performed through a semi-structured interview to the company’s CEO (responsible person for the process), with questions that were adapted from other studies (Burns et al., 2002; Major et al., 2010; Novas et al., 2017).

The information was also interpreted and triangulated, based on documentary analysis of information provided by the company. The interview and other data collection took place between September and December 2017.

Empirical Analysis

Company’s Description

Procifisc – Engineering and Consulting, Lda (http://www.procifisc.pt/) is a Portuguese Company that develops their activity, since 2007 in the sector of engineering, architectural and consulting services. It has 3 non-subsidiary companies, that is, companies from the same economic group, where there is no account consolidation.

Research, development and innovation are the company’s biggest bets to ensure a sustained growth, based on the creation of new products and services that are increasingly adapted to the market’s evolution which allows characterizing the internationalization process as a process of “adoption of innovation”, as suggested by the I-Model.

Analysis of results

Procifisc Internationalization Model

The Procifisc internationalization process started in 2012, due to a need for the company’s expansion and growth. Procifisc CEO compares its work with what “the Portuguese navigators did 500 years ago”, justifying that the uncertainty leads to the knowledge discovery and development.

There was an adaptation to the innovation potential, regarding responsiveness and the creation of new services that were scarce in the market (Cunha and Verhallen, 1998). The process is assumed as an innovation for the company and it allows its incremental development, as suggested by Bilkey and Teaser (1977), Cavulgil (1980) and Reid (1981). It is, thus, latent to verify that the model adopted by the company is the I-Model.

The way of entry and establishment used by the company in the international market was initially through sporadic exports and through the establishment of companies in the host country at a later stage (Bilkey and Tesar, 1977, and Leonidou and Katsikeas, 1996).

After this first analysis, we find that on the basis of the characterization of the I-Model presented by Andersen (1993), the process was developed after 5 years of the company’s activity pre-exports phase and the whole process is based on a behavioural theory that stems from an incremental form.

The process was facilitated by the host countries’ contact and linguistic proximity, which, as we have previously seen, constituted a criterion for ranking the international markets. This confirms and characterizes the I-Model’s second phase, that is, the phase in which the process’ design and development begins, in an active way, to geographically and culturally closer countries.

Currently, Procifisc has three legally established companies abroad: Angola (since 2014), Sao Tome (since 2013) and Brazil (since 2014). It exports to Mexico, Spain, the Dominican Republic (since 2015) and to Mozambique and Timor (since 2016). The future was projected to the foreign markets, namely; Africa and South America.

The international scenario and the current situation favour cooperation between people and companies aiming the exploration of all the means and paths to business success and the internationalization process development.

The description of the internationalization strategy once again corroborates the I-Model characterization; namely the third stage of the process development, according to Bilkey and Tesar (1977) and Leonidou and Katsikeas (1996) where exports are progressively assumed to geographically more distant countries and an advanced export phase is reached.

Evolution of the Procifisc’s Management Accounting Control Systems

In order to characterize Procifisc’s MACS use during the IP, we questioned the interviewee about the main changes in the Management Control during the last years. The CEO noted that “to keep up with the company’s growth, it was necessary to create a cohesive and trustworthy structure for the management body to draw the necessary conclusions for the decision-making at all levels of the business. The management, accounting and control of everything are possible, as long as there is a system that reports the various situations, whether financial or not. The dialogue, the meetings and analysis are also fundamental.”

The CEO believes that the MACS use provides useful information to support decisions and define strategy. It allows guiding the management for the investment or not.

The accounting system in international companies is controlled locally; however, it lacks weekly reporting to the CEO. The system works, as well as a qualitative control mechanism (Pinzón et al., 2011), with two different dimensions, one side of interaction through meetings and contacts with intermediaries and, another side, of diagnosis, with reports analysis. These conclusions are similar to those of Ramirez- Garcia et al. (2013), a system that allows measuring results and controlling deviations (Simons, 1995).

The relationship between Procifisc I-Model and MACS use

The relation between the defined strategy and the system use is, therefore, registered and validated. The style of use of information is more objective, more synthetic and interactive.

Through Procifisc’s constant concern to continually detect the global market’s needs and to accurately identify the customers’ requirements and expectations, the company has been extending its activities scope to international markets. This company began its process, after 5 years of activity, based on the sporadic export of its services. Only later did it consolidate this process through the companies’ opening in the international market.

Analysing all the historical evolution and the subsequent internationalization process evolution, we conclude that the adopted model uses the information reported by the MACS through a diagnostic approach, fundamentally in the first phase, and the beginning of the development of the second stage of the process. That is, at the stage of unsolicited exports (Bilkey and Tesar, 1977) or pre-exports stage (Leonidou and Katsikeas, 1996) and in the phase of exports to geographically closer countries (Bilkey and Tesar, 1977) or phase of export “trail” (Leonidou and Katsikeas, 1996). In the second phase, there is a complementarity between the various system dimensions (diagnostic and interactive), similarly to that advocated by several authors (Agbejule, 2006; Bisbe and Otley, 2004; Henri, 2006). In these phases, the MACS supports and is used to control the achievement of results and to correct deviations from the previously established performance objectives and it allows, or not, the evolution to subsequent phases. It should be noted that reports are analyzed for this purpose.

Analyzing the model’s evolution, we verify that it is supported in a MACS of interactive use, in the most active phases of the process, namely in phases 2 and 3, that is, when developing exports, either to countries geographically closer or more distant, or in the advanced export phase (Bilkey and Tesar, 1977; Leonidou and Katsikeas, 1996). According to the CEO, the MACS “provides daily information, which facilitates the control and it allows verifying the report’s information and aiding in our decisions.”

At this stage, although the company is controlled locally, the CEO analyzes the weekly information report which is sent to him in a formal way, which facilitates the CEO’s control and allows, as Simons (1991) suggests, setting agendas of regular meetings for the interconnection with direct subordinates and others, in order to review data and the action plan’s results.

“In practical terms, we choose to continue, discontinue or simply give up the internationalization process, in a given market, through the results we obtain whether they are financial or non-financial, and this basis is given by the information analysis that is reported by the MACS.” (CEO). After this analysis, we conclude that there is a strong relationship between the MACS use and the IM (strategy).

Conclusions, Implications and Lines for Future Research

The IM followed by the company fit the models presented by Bilkey and Tesar (1977) and by Leonidou and Katsikeas (1996), which allows us to conclude that the model adopted by the company is the I-Model.

Procifisc adapts its MACS’ use as the internationalization process evolves. The MACS use facilitates the internationalization strategy’s implementation, which reveals that it contributes to the company’s permanence and development in international markets.

In phase 1 of the IM, I-Model, the use of the MACS is more traditional, the information is used for diagnostic purposes. This result is based on the fact that the system, at an early stage, does not have as many information reporting abilities because the need is simply little stimulated by the process. In the following phases, there is a complementarity between the various MACS dimensions (diagnostic and interactive).

Being aware of the limitations of this study, due to the fact that it is limited to a case study, which makes it impossible to generalize the conclusions, we propose this study’s replication in other companies and with another dimensions of MACS, and replicate it through a quantitative approach to internationalized Portuguese companies.

Acknowledgements

The authors would like to thank the funding obtained through the FCT – Foundation for Science and Technology under the project UID / GES / 04630/2019.

Agbejule, A. (2006). How task uncertainty and diagnostic use of MAS determine the relationship between interactive use of MAS and organizational performance. Presented in the AAA 2007Management Accounting Section (MAS) Meeting, July, Available at SSRN: https://ssrn.com/abstract=920644 or http://dx.doi.org/10.2139/ssrn.920644

Ahrens, T., Chapman, C. (2004). Accounting for flexibility and efficiency: a field study of management control systems in a restaurant chain. Contemporary Accounting Research, 21(2), 271-301.

Andersen, O. (1993). On the internationalization process of firms: A critical analysis. Journal of International Business Studies, 24 (2), 209 – 228.

Archer, S., Otley, D. (1991). Strategy, Structure, Planning and Control Systems and Performance Evaluation Rumenco Ltd. Management Accounting Research, 2(4), 263-303.

Ballvé, A. (2006). Creando conocimiento en las organizaciones con el Cuadro de Mando Integral y el Tablero de Control. Revista Contabilidad y Dirección, 3 (1), 13-38.

Bilkey, W., Tesar, G., (1977). The export behavior of smaller sized Wisconsin manufacturing Journal of International Business Studies, 8 (1), 93-98.

Bisbe, J., Otley D. (2004). The effects of the interactive use of management control systems on product innovation. Accounting, Organizations & Society, 29 (8), 709-737.

Burns, J., Ezzamel, M., Scapens, R. (2002). The Challenge of Management Accounting Change: Behavioural and Cultural Aspects of Change Management. London: CIMA.

Carenzo, P., Broccardo, L., Truant E., Vola, P. (2011). Influence of Internationalization on Management Accounting Tools: evidences from Italian Firms. Economia Aziendale Online, 2 (1), 157-173.

Cavusgil, S. (1984). Differences among exporting firms based on their degree of internationalization. Journal of Business Research, 12 (99), 195-208.

Cavusgil, S. (1980). On the internationalization process of firms. European Research, 8 (6), 273-281.

Chandler, A. (1962). Strategy and structure: chapters in the history of the industrial enterprise. Cambridge: M.I.T. Press

Chenhall, R. (2003). Management control systems design within its organizational context: findings from contingency-based research and directions for the future. Accounting, Organizations and Society, 28(1), 127–168.

Cunha, M., Verhallen, T. (1998). Organizational innovation: An overview of topics, models and research directions. Comportamento Organizacional e Gestão, 4(2), 5-33.

Czinkota, M. (1982). Export Management. New York: Praeger Publishers.

Fernández, Z., Nieto, M. (2005). Internationalization Strategy of Small and Medium-Sized Family Businesses: Some Influential Factors. Family Business Review, 18 (1), 77-89.

Francisco, L., Alves, M. (2012), Accounting Information and Performance Measurement in a Nonprofit Organization, in A. Davila, M.J. Epstein, J. Manzoni (ed.) Performance Measurement and Management Control: Global Issues (Studies in Managerial and Financial Accounting, 25, Emerald Group Publishing Limited, 465 – 487

Gomez-Conde, J., Lopez-Valeiras E., Ripoll-Feliú,V., Gonzalez-Sanches, M. (2013). El efecto mediador y moderador de la internacionalizacion en la relacion entre los sistemas de control de géstion y el compromiso com la innovación. Revista de Contabilidad, 16 (1), 53-65.

Haldma T., Lääts, K., (2002), Contingencies influencing the management accounting practices of Estonian manufacturing companies. Management Accounting Research, 13 (1), 379-400.

Hartmann, F., Vaassen E. (2003). The Changing Role of Management Accounting and Control Systems. in BHIMANI, Alnoor (ed.), Management Accounting in the Digital Economy, Oxford University Press, Oxford, 112-132.

Henri, J. (2006). Management control systems and strategy: a resource-based perspective. Accounting, Organizations and Society, 31 (6), 529–558.

Leonidou L., Katsikeas C. (1996). The export development process: An integrative review of empirical models. Journal of International Business Studies, 27 (3), 517–551.

Lin S. (2010). Internationalization of the SME: Towards an integrative approach of resources and competences. 1er Colloque Franco-Tchèque: “Trends in International Business”, 117-135.

Luther R., Longden S. (2001). Management ac-counting in companies adapting to structural change and volatility in transition economies: a South African study. Management Accounting Research, 12 (1), 299-320.

Major, M., Pinto, J., Vicente, C. (2010). Estudo da Mudança nas Práticas de Controlo de Gestão em Portugal. Portuguese Journal of Accounting and Management, 10 (1), 9-42.

Murteira, J. (1997). Modelos de fronteira bilateral: uma aplicação ao mercado de trabalho em Portugal. Actas da 5ª Conferência Cemapre, ISEG, Universidade Técnica de Lisboa.

Naor, M., Bernardes, E., Druehl, C., Shiftan, Y. (2015). Overcoming barriers to adoption of environmentally-friendly innovations through design and strategy: learning from the failure of an electric vehicle infrastructure firm. International Journal of Operations & Production Management, 35 (1), 26-59.

Naranjo-Gil, D., Álvarez-Dardet C. (2006). El uso del sistema contable de gestión en la implantación de la estrategia: Análisis del ajuste contingente. Revista Española de Financiación y Contabilidad, 35 (128), 157-179.

Naranjo-Gil, D., Hartmann F. (2007). Management Accounting Systems, top management team heterogeneity and strategic change. Accounting, Organizations and Society, 32 (7/8), 735-756.

Naranjo-Gil, D., Hartmann, F. (2006). How Top Management Teams Use Management Accounting Systems to Implement Strategy. Journal of Management Accounting Research, 18 (1), 21-53.

Novas, J., Alves, M., Sousa, A. (2017). The role of management accounting systems in the development of intellectual capital. Journal of Intellectual Capital, 18 (2), 286 – 315.

Otley D. (1980). The contingency theory of management accounting: achievement and progress. Accounting Organizations and Society, 5 (4), 413-428.

Pellinen, J., Teittinen, H., Järvenpää, M. (2016). Performance measurement system in the situation of simultaneous vertical and horizontal integration. International Journal of Operations and Production Management, 36 (10), 1182-1200.

Pešalj, B., Pavlov, A., Micheli, P. (2018). The use of management control and performance measurement systems in SMEs: A levers of control perspective. International Journal of Operations & Production Management, 38 (11), 2169-2191,

Pinzón, P., Vázquez, J., Elorza, M., Espejo, C. (2011). Sistemas de Control para la Gestión de los Canales de Exportación Independientes: un Análisis Exploratorio sobre su Diseño y Uso. Spanish Accounting Review, 14 (2), 115-146.

Ramírez García, C., Vélez-Elorzab M.., Álvarez-Dardet-Espejoa M. (2013). ¿Cómo controlan los franquiciadores españoles a sus franquiciados? Spanish Accounting Review, 16 (1), 1-10.

Reid S. (1981). The decision maker and export entry and expansion. Journal of International Business Studies 12(2), 101-112.

Roberts, H. (2003). Management Accounting and the Knowledge Production Process, in BHIMANI, Alnoor (ed.), Management Accounting in the Digital Economy, Oxford University Press, Oxford, 260-283.

Rogers, E. (1962). Diffusion of Innovations. New York: Free Pres.

Roque, A., Alves M., Raposo M. (2019). Internationalisation strategy: main models and approaches, IBIMA Business Review, (2019).

Roque, A., Alves, M, Raposo, M. (2018 a). Internationalization Strategy: Main Models and Approaches. Vision 2020: Sustainable Economic Development and Application of Innovation Management from Regional expansion to Global Growth. 32nd International Business Information Management Association Conference (IBIMA), 15-16 November 2018, Seville, Spain

Roque, A., Alves, M, Raposo, M. (2018 b). Management Accounting and Control Systems and Strategy: A Theoretical Framework for Future Researches. Vision 2020: Sustainable Economic Development and Application of Innovation Management from Regional expansion to Global Growth. 32nd International Business Information Management Association Conference (IBIMA), 15-16 November 2018, Seville, Spain

Samson, D., Langfield- Smith, K., McBride, P. (1991). The Alignment of Management Accounting with Manufacturing Priorities: A Strategic Perspective. The Australian Accounting Review, 1(1), 29-40.

Simons, R. (1987). Accounting control systems and business strategy: An empirical analysis. Accounting, Organizations and Society, 12 (4), 357-374.

Simons, R. (1990). The role of management control systems in creating competitive advantage: new perspectives. Accounting, Organizations and Society, 15 (1/2), 127-143.

Simons, R. (1991). Strategic Orientation and Top Management Attention to Control Systems. Strategic ManagementJournal, 12 (1), 49-62.

Simons, R. (1995). Levers of control: how managers use innovative control systems to drive strategic renewal. Boston: Harvard Business School Press.

Sjoblom, L. (2003). Management Accounting in the New Economy. In Bhimani A. (ed.), Management Accounting in the Digital Economy. Oxford University Press, Oxford, 185-201.

Thorén, K., Brown T. (2004). Development of Management Control Systems in Fast-Growing Small Firms. In NCSB 2004 Conference – 13th Nordic Conference on Small Business Research.

Tuomela, T. (2005). The interplay of different levers of control: A case study of introducing a new performance measurement system. Management Accounting Research, 16 (4), 293-320.

Welford, R., Prescott, K. (1994). European Business – An Issue-Based Approach. 2nd Edition, Pitman Publishing, London.

Yin, R. (1993). Applications of case study research. Beverly Hills, CA: Sage Publishing.

Yin, R. (2014). Case study research. London: Sage Publications Inc.