Joberth VARGAS FIGUEROA, Melva LINARES GUERRERO, Sindulfo J. DIAZ ANGULO and Cristina V. MENDO CALLIRGOS

Universidad Privada del Norte

Volume 2023,

Article ID 239727,

IBIMA Business Review,

12 pages,

DOI: https://doi.org/10.5171/2023.239727

Received date: 23 May 2023; Accepted date: 26 July 2023; Published date: 11 September 2023

Cite this Article as:

Joberth VARGAS FIGUEROA, Melva LINARES GUERRERO and Sindulfo J. DIAZ ANGULO (2023)," The Deduction System as a Tax Compliance Strategy: A Peruvian Case", IBIMA Business Review, Vol. 2023 (2023), Article ID 239727, https://doi.org/10.5171/2023.239727

The research aimed to determine the relationship between the deduction system and tax compliance, showing a Peruvian case specifically in a service company; regarding the methodology used, it is: type of basic research, quantitative approach, non-experimental design and correlational descriptive level. On the other hand, the population was made up of 6 collaborators; the technique used was the survey and the instrument was the questionnaire developed under the Likert scale. Whose result showed a significance P value of 0.001 <0.05; the null hypothesis is rejected and the hypothesis of the researcher is accepted, therefore, the system of deductions is related to tax compliance, with a confidence level of 95%. In addition, the correlation coefficient is 0.971, indicating a strong positive relationship. Concluding that there is a strong positive relationship between the deduction system and tax compliance, thus allowing to increase the tax revenues of the state due to the fulfillment of its tax obligations of service companies.

Keywords: deductions, compliance, tax obligations

Introduction

Tax evasion is a latent problem that affects many countries in the world having an effect on tax collection, because without the revenues that taxes represent, it is not possible to finance State expenditures on goods and services to meet the needs of the population; this is exacerbated in developing countries because they are economies that have more than a third of informal economy (La Porta & Shleifer, 2008). For this reason, governments are concerned with avoiding unfair tax competition promoted by informality (Garín, et al. 2019).

There are several causes related to tax evasion, one of them is informality especially in developing countries; in Latin America (LA), according to estimates for the period 1991-2015, informality represented 38.81% of the Gross Domestic Product (GDP) (Medina & Schneider, 2017); while, in Peru, the results for the period 2007-2019 indicated that the informal sector represents around 62% according to sources from the National Institute of Statistics and Informatics (INEI, 2019).

Due to informality motivated in some way by the corruption of the rulers and the bureaucracy, many companies omit their income and this is negatively linked to the size of the company and the age of these (Pedroni, et al., 2022). In this way, tax evasion increases.

This shows the shortcomings and fragility of the tax administration of each country, in which they should improve their policies to reduce informality by allowing a higher percentage of collection (Páez and Domínguez, 2021). If we add to all this the limited tax morale of taxpayers, the collection is lower.

In Peru there is a large percentage of companies that operate in informality, evading taxes and failing to comply with tax obligations; according to the National Institute of Statistics and Informatics (INEI, 2022): “As of December 31, 2021, the number of active companies registered in the Central Directory of Companies and Establishments amounted to 2 million 981 thousand 98 companies, with a growth of 7.3% over the previous year” (p. 2). For these formal companies, among other mechanisms, the Tax Obligations Payment System or deduction system has been implemented to carry out an advanced collection of VAT; this allows them to have a fund of money in the Bank of the Nation that will serve them in the payment of their tax obligations, fines, among others, or withdraw the surplus money; however, the National Superintendence of Customs and Tax Administration (SUNAT, n.d.) shows statistical data according to the Annual Report of the year 2021 on the Tax collection of the Central Government for the sum of S / 139 947 million. These data reflect income such as collection of the account of deductions to the treasury, due to inconsistencies, deficiencies in the accounting and tax management of taxpayers.

A Cajamarca Services company located in northern Peru whose economic activity is the construction of other types of civil engineering works, being a provider of integral mining and construction services, is affected by the different tax obligations imposed in the country. Due to the fact that its business item is construction in mining companies, it affects the detraction system, both as a supplier and as an acquirer of services. This system has served to provide the company with a fund to be able to make the payment of its tax obligations; therefore, it seeks to investigate the relationship between the system of deductions and compliance with tax obligations.

In the international arena, Cunalata (2018) concluded that: (…) it was possible to evidence the existence of failures in the records, in the declarations of the entity, as well as a lack of accounting, responsibilities and administrative policies that lead to the achievement of institutional objectives, generating waste of resources. On the other hand, the importance of compliance with the law or regulations in force in each country should be highlighted in order to ensure the correct fulfillment of tax obligations, as Ponce (2020) points out: “the proper management and correct application of laws can avoid retaliation by the Tax Administration because the analysis and fiscal application of tax planning must be carried out strictly to tax laws”. Finally, Córdova (2018) points out “these companies are affected with tax fines due to the lack of tax management, in addition, because they do not participate in training, they do not know about the tax benefits they would access if they comply with their tax obligations”.

Regarding the national background, Cuentas & Urquizo (2022) obtained as a result a correlation of 92.80% with a level of significance of 3.39% lower than the margin of error of 5.00%; this allowed them to conclude that “the system of detractions influences to a significant degree the substantial obligations in the cargo transport companies that have been subject to investigative treatment”. Similarly, Mescco (2019) obtained as a result that Pearson’s correlation is 0.015, which allowed us to conclude that “the deduction system affects tax compliance”. Also Cajahuaringa & Melgar (2020) obtained as a result a Pearson correlation with a significance level of less than 5%, showing that there is a 95% probability of its occurrence, which could allow the conclusion that “tax planning has a significant relationship with the system of deductions of exempt products”. These studies affirm what was mentioned by Chacón & Dimìnguez (2018), Panta (2018), Vilela & Yovera (2021) and Gardos (2017), who concluded that the Detraction System has a collection purpose acting as a mechanism for compliance with tax obligations.

Regarding the theoretical bases of the first variable of study, the System of deductions, commonly known as the System of Payment of Tax Obligations (SPOT) which according to SUNAT (2020) and Villazana (2019), is an administrative mechanism that contributes to tax collection and consists of the deduction (discount) made by the buyer or user of a good or service affected by the system, a percentage of the amount to be paid for these operations, to then deposit it in the Banco de la Nación, in the current account in the name of the seller or service provider, which, in turn, will use the said funds to make the payment of taxes, fines and payments on account, including their respective interests and the update that is made of the said tax debts in accordance with article 33 of the Tax Code.

The study variable – detraction system has the following dimensions; initially, the dimension of legality based on the principle of legality, which according to Támara (2020), is based on “the primacy of the law, a fact by which all legal bodies of Peru in their exercise of public power are limited to what is established by the constitution and the law, In this way, it does not admit other infractions or criminal sanctions that are not typified in the criminal law to be applied before an action that is considered as a crime”. Secondly, there is the dimension Account of deductions, as indicated by SUNAT (2022), so that “companies can make the deposit of the deductions they must open a current account in any of the agencies of the Banco de la Nación, in said account they will receive payment by their clients for the amounts deducted “.

The second variable of study is the Compliance with tax obligations, for Solórzano (2011) tax compliance “is related to fiscal morality that is constituted by a single variable called tolerance to fraud inscribed in the dimension of the values and internal motivations of the individual”. For the author Arana (2009):

Civic-tax education is fundamental as a mechanism to be able to implant in the consciousness of individuals the importance of tax compliance and ensure that it is voluntary, since in this way it would be part of the culture in society for the new generations, reducing the breach of tax obligations (p. 227).

As a first dimension, there is the tax obligation, which for Hernández (2017), is “the legal relationship between the creditor and the tax debtor, the debtor is obliged to give a benefit to the creditor ”, as for the tax obligations it is the relationship between the company that acts as a debtor and obliged to give a benefit to the state that acts as a creditor. The second dimension is tax management, for LA LEY (n.d.), “it is the ability to carry out an efficient accounting management within the company”; for Sánchez & Tarodo (2015), on the other hand, tax management “is considered as a mechanism to be able to administer taxes”, tax management is also responsible for directing the entire process of tax settlement, … From the quantification, determination and settlement of the tax debt, in addition, it is responsible for managing all documents related to tax debts with the Tax Administration.

Then, taking into account the background and theories that support the study, the following research problem has been formulated: What is the relationship between the deduction system and the fulfillment of the tax obligations of a service company Cajamarca – Peru? And, specifically, what is the relationship between the deduction system and the tax obligations of a service company Cajamarca – Peru?; What is the relationship between the deduction system and the tax management of a service company Cajamarca – Peru?; What is the relationship between legality and compliance with tax obligations of a service company Cajamarca – Peru?; What is the relationship between the fund of the deduction account and the fulfillment of the tax obligations of a service company Cajamarca – Peru?.

As a general objective, it is proposed: to determine the relationship between the system of deductions and the fulfillment of the tax obligations of a service company Cajamarca – Peru; and, specifically, to establish the relationship between the Detractions System and the tax obligations of a service company Cajamarca – Peru; to establish the relationship between the Detractions System and the tax management of a service company Cajamarca – Peru; to establish the relationship between the legality and compliance with tax obligations of a service company Cajamarca – Peru; to establish the relationship between the fund of the deduction account and the fulfillment of the tax obligations of a service company Cajamarca – Peru.

The general hypothesis is: there is a strong positive relationship between the deduction system and the fulfillment of the tax obligations of a service company Cajamarca – Peru; as specific hypotheses, there are the following: there is a positive relationship between the Detractions System and the tax obligations of a service company Cajamarca – Peru; there is a positive relationship between the Detractions System and the tax management of a service company Cajamarca – Peru; there is a strong positive relationship between the legality and compliance with tax obligations of a service company Cajamarca – Peru; and there is a positive relationship between the fund of the deduction account and the fulfillment of the tax obligations of a service company Cajamarca – Peru.

Materials And Methods

The focus of the research is quantitative, according to Guerrero & Guerrero (2014), “quantitative research consists of contrasting hypotheses from the probabilistic point of view and, if they are accepted and demonstrated in different circumstances, from them to elaborate general theories” (p. 48); in this research, it is sought to collect documentary information from the study company to be analyzed and explained.

By not manipulating or modifying the study variables, the design is non-experimental; according to Hernández et al. (2014), in a non-experimental study no situation is generated, but existing situations are observed, not intentionally caused by the researcher, in such research the independent variables occur and it is not possible to manipulate them, you do not have direct control over these variables nor can you influence them, because they have already happened, as well as their effects.

The time in which the research is developed is transversal taking information from the company only in a period of time. Liu and Tucker (as cited in Hernández et al., 2014) mention that in research, whose design is transitional or transversal, information is collected in a single moment, that is, in a unique time.

The level is descriptive – correlational; Hernández et al. (2014) affirm that descriptive research is the one that includes the description, registration, analysis and interpretation of the current nature, composition or processes of the phenomena. It is correlational; according to Hernández et al. (2014), this type of study seeks to know the degree of relationship between two or more variables by measuring each variable independently, and then quantifying and analyzing them in order to establish the relationship or association that exists between them.

According to Hernández et al. (2014), “a population is the set of all cases that agree with a series of specifications” (p. 174), which is why the study population is the workers of the service company who have theoretical, technical and practical knowledge of the Detractions System and on the Fulfillment of Tax Obligations, which are those who work within the area of Management, Administration and Accounting, adding a total of 6 workers.

Hernández et al. (2014) define the sample as “a subgroup of the population of interest on which data will be collected, and which has to be precisely defined and delimited beforehand, in addition to being representative of the population.” (p.173), therefore, in the present research an intentional non-probabilistic sampling was used because the sample is made up of the total elements of the population.

The method used is the Inductive-Deductive because from particular facts it goes to generalizations and vice versa. It is a means of reasoning by which individual facts are analyzed in order to determine the relationship of the most frequent phenomena when generalizing all the information. (Guerrero & Guerrero, 2014).

The technique, according to Guerrero & Guerrero (2014), can be considered as “a tool of the method, since it guides all the investigative activity, the type of techniques on which the researcher will rely depends on it” (p. 50). In this case, the survey technique was used; according to Baena (2014), it is the technique by which the researcher applies a questionnaire to the study sample in order to obtain the necessary data and information and develop the research.

The instrument used for the collection of information was the questionnaire which, according to Hernández et al. (2014), is an instrument used for data collection in quantitative research and consists of posing a set of questions that are congruent with each other and serve to measure the study variables.

The procedure followed was to apply the instrument, which had response options on a Likert scale with a rating of 1 to 5, was elaborated based on 20 questions divided into two parts, applied to the sample. The first part of the questionnaire consists of 10 questions that evaluate the dimension of the Detractions System, posing questions related to the dimensions of Legality and Account of detractions. The second part of the survey consists of 10 questions that evaluate the dimension of Tax Compliance, divided into 5 questions that evaluate the dimension of Tax Obligations and the remaining 5 questions evaluate the dimension of Tax Management.

The measurement scale for both questionnaires based on a Likert scale are: (1) strongly disagree, (2) partially disagree, (3) neither agree nor disagree, (4) partially agree and (5) strongly agree. With this, the validity and reliability of the instruments used to obtain information and data processing was determined, and the judgment of experts in the field was used. To analyze the information obtained through the questionnaire, the SPSS Program was used in version 24, which helped to capture the final results based on each study variable, additionally, the Excel program was used to organize the information.

Results

The results obtained from the research carried out on the system of deductions and compliance with tax obligations of a service company Cajamarca – Peru, developed based on the objectives set.

First, the normality test was developed to establish the correlation test to be used as shown below:

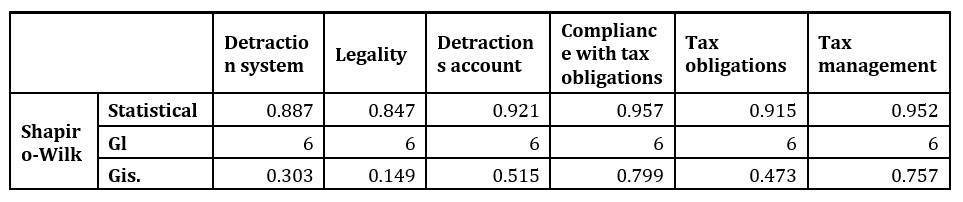

Table 1: Normality test

According to Table 1, using the Shapiro Wilk normality test for samples smaller than 50 individuals, that the significance in all the data of the variables and dimensions, is greater than 0.05, indicating that there is normal distribution, therefore, the Pearson Correlation parametric test will be used.

General Hypothesis Test

HI There is a high positive relationship between the deduction system and the fulfillment of the tax obligations of a service company Cajamarca – Peru. H0 There is no significant and positive relationship between the deduction system and the fulfillment of the tax obligations of a service company Cajamarca – Peru.

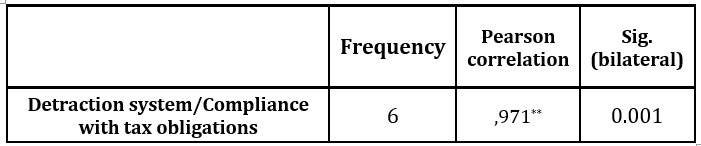

Table 2: Relationship between the deduction system and compliance with tax obligations of a service company Cajamarca – Peru.

Note. **. The correlation is significant at the 0.01 (bilateral) level.

According to Table 2, there is a significance P value of 0.001 <0.05; the null hypothesis is rejected and the hypothesis of the researcher is accepted, therefore, the system of deductions is related to the fulfillment of the tax obligations of a Service company, with a confidence level of 95%. In addition, the correlation coefficient is 0.971, indicating a strong positive relationship.

+Specific Hypothesis 1

HE1: There is a positive relationship between the deduction system and the tax liability dimension of a service company Cajamarca – Peru. H01: There is no positive relationship between the deduction system and the tax liability dimension of a service company Cajamarca – Peru.

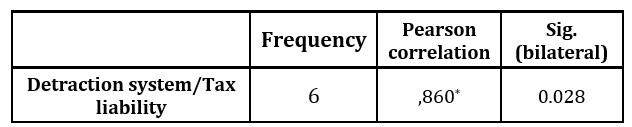

Table 3: Relationship between the deduction system and the tax liability dimension of a service company Cajamarca – Peru

Note.*. The correlation is significant at the level 0.05 (bilateral).

Table 3 shows a significance P value of 0.028 <0.05; the null hypothesis is rejected and the hypothesis of the researcher is accepted, therefore, the system of deductions is related to the dimension tax obligation of a company of Services Cajamarca – Peru, with a confidence level of 95%. In addition, the correlation coefficient is 0.860, indicating a strong positive relationship.

Specific Hypothesis 2

HE2: There is a significant and positive relationship between the deduction system and the tax management dimension of a service company Cajamarca – Peru. H02: There is no significant and positive relationship between the deduction system and the tax management dimension of a service company Cajamarca – Peru.

Table 4: Relationship between the deduction system and the tax management dimension of a service company Cajamarca – Peru

Note. **. The correlation is significant at the 0.01 (bilateral) level.

According to Table 4, a significance P value of 0.001 <0.05 is observed; the null hypothesis is rejected and the hypothesis of the researcher is accepted, therefore, the system of deductions is related to the tax management of a company of Services Cajamarca – Peru, with a confidence level of 95%. In addition, the correlation coefficient is 0.971, indicating a strong positive relationship.

Specific Hypothesis 3

HE3: There is a significant and positive relationship between the legality dimension and compliance with tax obligations of a service company Cajamarca – Peru. H02: There is no significant and positive relationship between the legality dimension and compliance with the tax obligations of a company of Services Cajamarca – Peru.

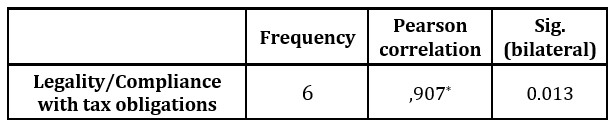

Table 5: Relationship between the legality dimension and compliance with tax obligations of a service company Cajamarca – Peru.

Note. *. The correlation is significant at the level 0.05 (bilateral).

According to Table 5, a significance P value of 0.013 <0.05 is observed; the null hypothesis is rejected and the hypothesis of the researcher is accepted, therefore, the legality dimension is related to the fulfillment of the tax obligations of a company of Services Cajamarca – Peru, with a confidence level of 95%. In addition, the correlation coefficient is 0.907, indicating a strong positive relationship.

Specific Hypothesis 4

HE4: There is a significant and positive relationship between the dimension account of deductions and the fulfillment of the tax obligations of a company of Services Cajamarca – Peru. HE4: There is no significant and positive relationship between the dimension account of deductions and the fulfillment of the tax obligations of a company of Services Cajamarca – Peru.

Table 6: Relationship between the dimension account of deductions and compliance with the tax obligations of a company of Services Cajamarca – Peru.

Note. **. The correlation is significant at the 0.01 (bilateral) level.

Table 6 shows a significance P value of 0.005 <0.05; the null hypothesis is rejected and the hypothesis of the researcher is accepted, therefore, the dimension account of detractions is related to the fulfillment of the tax obligations of a company of Services Cajamarca – Peru, with a confidence level of 95%. In addition, the correlation coefficient is 0.942, indicating a strong positive relationship.

Discussion

The research was based on the interest in determining the relationship of the deduction system as a strategy in the fulfillment of tax obligations in a company from Cajamarca, Peru. For which the general hypothesis has been corroborated thanks to the contrast of the specific hypotheses that in the following paragraphs expose the results obtained and compare with the related research background.

In relation to the general hypothesis, the Pearson test was used and a correlation coefficient of 0.971 was obtained; indicating a strong positive relationship between the deduction system and the fulfillment of the tax obligations of a service company, this indicates that the detractions system ensures compliance with tax obligations in said company. Likewise, in terms of its significance it showed a 0.001, showing a significant relationship, since the P value of 0.001 <0.05. These results are consistent with those obtained by Mescco (2019), who concluded that the deduction system affects tax compliance. Similarly , Quiroz (2019) concluded that the deduction system is related to the tax collection of accounting service companies. Additionally, Chacón & Leticia (2018), concluded that the Detraction System serves as an effective mechanism for tax compliance.

In relation to specific hypothesis 1: there is a positive relationship between the Detractions System and the tax obligations of a service company Cajamarca – Peru. Using the Pearson test, a correlation coefficient of 0.860 was obtained and a P value of 0.028 <0.05 was evidenced; indicating a strong positive relationship between the variables, therefore, the deduction system is related to the tax obligation dimension of a service company, in the same way, it coincides with the research of Panta (2018), who concluded that the level of compliance with tax obligations in relation to the deduction system is acceptable, Since 72.45% of the total tax obligations generated in the year under study have been canceled with the funds generated in the deduction account, evidencing that the deduction system serves to ensure the payment of taxes by companies. Additionally, the results are related to Cuentas & Urquizo (2022), who concluded that the deduction system significantly influences substantial obligations.

In the specific hypothesis 2: there is a positive relationship between the Detractions System and the tax management of a service company Cajamarca – Peru. Using Pearson’s test, a correlation coefficient of 0.971 was obtained; a significance P value of 0.001 <0.05; Being the strength of strong positive correlation, therefore, the system of deductions is related to the tax management of the company. This is related to what was pointed out by Cajahuaringa & Melgar (2020), who conclude that tax planning has a significant relationship with the deduction system, this because through tax planning tax management can be given and in effect efficiently manage the taxes assigned to the company.

In relation to the specific hypothesis 3: there is a strong positive relationship between the legality and compliance with the tax obligations of a service company Cajamarca – Peru. Using the Pearson test, a correlation coefficient of 0.907 was obtained, with a significance P value of 0.013 <0.05; Being the strength of positive correlation strong, therefore, the legality dimension is related to the fulfillment of the tax obligations of the service company. The study is related to what Ponce (2020) pointed out, who concluded that with the proper management and correct application of laws, retaliation by the tax administration can be avoided because the analysis and fiscal application of tax planning must be carried out strictly to tax laws.

Finally, with respect to specific hypothesis 4: there is a positive relationship between the fund of the deduction account and the fulfillment of the tax obligations of a service company Cajamarca – Peru. Using the Pearson test, a correlation coefficient of 0.942 and a significance P value of 0.005 <0.05 were obtained; Indicating a strong positive relationship, therefore, the dimension account of deductions is related to the fulfillment of the tax obligations of the service company. This is related to the results obtained by Romero (2021), who concludes that accounting service companies affected by withholding can use the withheld balance for the payment of their taxes, evidencing the use of advanced collection systems.

Conclusion

In relation to the general objective, it is concluded that there is a strong positive relationship between the Detractions System and the Fulfillment of Tax Obligations of a company from Cajamarca -Peru. Because the Pearson correlation reached a value of 0.971; a P value of 0.001 <0.05. Which means that thanks to the system of deductions it is possible to comply with tax obligations within the company.

In relation to the specific objective one concludes that, there is a strong positive relationship between the system of deductions and tax obligations. Because the Pearson correlation reached a value of 0.860; a significance P value of 0.028 <0.05. This means that the deduction system was implemented as an advance collection mechanism to cover the payment of tax obligations in the service company, thus facilitating timely compliance with them.

In relation to specific objective two, it is concluded that there is a strong positive relationship between the deduction system and the tax management of a service company in Cajamarca, Peru. Because the Pearson correlation reached a value of 0.971; and a P value of 0.001 <0.05. Which means that the deduction system is a tool that can be used in tax management within the company for efficient management in the payment of taxes.

In relation to specific objective three, it is concluded that there is a strong positive relationship between the legality and compliance with the tax obligations of a service company from Cajamarca-Peru. Because the Pearson correlation reached a value of 0.907; a P value of 0.013 <0.05. Which means that legality is the basis on which we work to be able to comply with tax obligations in accordance with the laws and regulations in force in the country.

In relation to specific objective four, it is concluded that there is a strong positive relationship between the deduction account and compliance with the tax obligations of a service company from Cajamarca-Peru. Because the Pearson correlation reached a value of 0.942; a P value of 0.005 <0.05. which means that the deduction account turns out to be indispensable to be able to manage the payment of taxes and comply with tax obligations, because it is a current bank account regulated by the State and that does not generate expenses of any kind to the company in such a way that the full amount of the deposit is channeled into the payment of tax obligations.

References

Arana, S. (2009). Factors that affect the voluntary fulfillment of tax obligations . In S. Arana, Factors that affect voluntary compliance with tax obligations (p. 227). Madrid: DUKINSON.

Cajahuaringa, J., & Melgar, J. (2020), Tax planning and its relationship in the system of deductions of exempt products of the company Mitawi Zu E.I.R.L. located in the district of La Victoria, 2019. Unpublished thesis. Peru: Universidad Autónoma del Perú. Institutional repository. https://repositorio.autonoma.edu.pe/bitstream/handle/20.500.13067/1080/Cajahuaringa%20Toledo%2c%20Jan%20Paul%3b%20Melgar%20Barrios%2c%20Julio%20Jose.pdf?sequence=1&isAllowed=y

Chamber of Commerce of Lima. (2022), Penalties for tax infractions imposed by sunat. [online] available at < https://lacamara.pe/sanciones-por-infracciones-tributarias-que-impone-sunat/#:~:text=Tipos%20de%20sanciones,Multas> [accessed: 07 March 2022].

Chacón, P., & Domínguez, H. (2018), The system of deductions of the igv – spot as a mechanism for tax compliance in the graphic company Yafra S.A.C. district La Victoria – Lima, year 2016. Unpublished thesis. Peru: Universidad Privada del Norte. Institutional repository.https://repositorio.upn.edu.pe/bitstream/handle/11537/14338/Chac%c3%b3n%20Mu%c3%b1oz%2c%20Patricia%20Marlene.pdf?sequence=5&isAllowed=y

Córdova, M. (2018), Tax effects of the renova plan in the urban transport sector of Guayaquil 2013 – 2015. Unpublished thesis. Ecuador: University of Guayaquil. Institutional repository. http://repositorio.ug.edu.ec/bitstream/redug/37146/1/Proyecto%20Johana%20corregido%20%281%29%20%281%29%20%281%29.pdf

Cuentas, M., & Urquizo, N. (2022), Detractions and Tax Compliance System in Cargo Transport Companies in the District of San Juan de Lurigancho, Lima 2017-2018. Unpublished thesis. Peru: Universidad Peruana los Andes. Institution Repository. https://repositorio.upla.edu.pe/bitstream/handle/20.500.12848/3845/T037_44421706_T.pdf?sequence=1&isAllowed=y

Cunalata, R. (2018), Analysis and evaluation of the management and tax compliance of the company “Almacenes León”, Riobamba Canton, Chimborazo province, period 2015 – 2016. Unpublished thesis. Peru: Escuela Superior Politécnica de Chimborazo. Institutional repository. http://dspace.espoch.edu.ec/bitstream/123456789/9878/1/82T00908.pdf

Effio, F., & Mamani, Y. (2019), Detractions, retentions and perceptions analysis and practical application. Lima: Pacífico Editores SAC.

Lucas Garín, A., Tijmes-IHL, J., Salassa Boix, R. and Sommer, C. (2019) A dialogue between global trade governance and international environmental and tax policies, Derecho PUCP, (83), pp. 387 – 414. doi: 10.18800/derechopucp.201902.013.

Government of Peru (2022), Detractions. Plataforma Digital Única del Estado Peruano [online] < available at: https://www.gob.pe/701-detracciones> [accessed: 23 April 2022].

Guerrero, G., & Guerrero, M. (2014), Research Methodology. ed. Mexico: Grupo Editorial Patria.

Gutierrez, M. (2017), Detractions system and the sanctions regime and its impact on the management of the heavy cargo transport company Claro de Luna E.I.R.L Huancayo, 2016. Unpublished thesis. Peru: Universidad Católica Los Ángeles Chimbote. Institutional repository.https://repositorio.uladech.edu.pe/bitstream/handle/20.500.13032/3673/DETRACCIONES_SANCIONES_GUTIERREZ_SARMIENTO_MARICRUZ.pdf?sequence=1&isAllowed=y

Heras, W. (2019), Tax culture as a factor in the tax compliance of the merchants of the San Antonio de Cajamarca Shopping Center 2018. Unpublished thesis. Peru. National University of Cajamarca. Institutional repository. https://repositorio.unc.edu.pe/bitstream/handle/20.500.14074/3590/TESIS%20WILMER%20YONY%20HERAS%20BUSTAMANTE.pdf?sequence=1&isAllowed=y

National Institute of Statistics and Informatics. (2022), Business Demography in Peru – IV quarter 2021. Reports and Publications: https://www.gob.pe/institucion/inei/informes-publicaciones/2978908-demografia-empresarial-en-el-peru-iv-trimestre-2021

THE LAW. (n.d.), Tax Management. Legal Guides [Blog]. Available in https://guiasjuridicas.wolterskluwer.es/Content/Documento.aspx?params=H4sIAAAAAAAEAMtMSbF1jTAAASMTA1MDtbLUouLM_DxbIwMDS0NDA1OQQGZapUt-ckhlQaptWmJOcSoAc19A4DUAAAA=WKE [Accessed: 05 March 2023].

La Porta, R., & Shleifer, A. (2008), The Unofficial Economy and Economic Development. Brookings Papers on Economic Activity, otoño, 275-352.

Llamoctanta, J. (2021), System of deductions of the general sales tax and compliance with tax obligations in construction companies, of the district of Cajamarca, period 2020. Unpublished thesis. Peru: National University of Cajamarca.

Mescco, E. (2019), The detractions system and its impact on tax compliance of the company Ecoil S.A.C. of the district of Lurín in 2018. Unpublished thesis. Peru: Universidad Autónoma del Perú. Institutional Repository. https://repositorio.autonoma.edu.pe/bitstream/handle/20.500.13067/946/Mescco%20Castro%2c%20Elizabeth.pdf?sequence=3&isAllowed=y

Research Methodology. (2014). In G. Baena. Mexico: Grupo Editorial Patria.

Mosqueira, G., & Chávez, J. (2022), IGV detractions system and its impact on the liquidity and profitability of the company Mahadi S.A.C. Cajamarca 2020. Unpublished thesis. Peru: Universidad Privada Antonio Guillermo Urrelo. Institutional repository. http://repositorio.upagu.edu.pe/bitstream/handle/UPAGU/2454/Tesis%20SISTEMA%20DE%20DETRACCIONES%20DEL%20IGV%20Y%20SU%20INCIDENCIA%20EN%20LA%20LIQUIDEZ%20Y%20RENTABILIDAD%20DE%20LA%20EMPRESA%20MAHADI%20S.A.C.%20CAJAMARCA%202020.pdf?sequence=1&isAllowed=y

Panta, J. (2018), Analysis of the detractions system and its impact on compliance with the tax obligations of the company Piuramaq S.R.L, Piura 2016. Unpublished thesis. Peru: Universidad Alas Peruanas. Institutional repository. https://repositorio.uap.edu.pe/xmlui/bitstream/handle/20.500.12990/6360/Tesis_an%c3%a1lisis_Sistema.detracciones_cumplimiento.ObligacionesTributarias_emp._PIURAMAQ%20SRL_Piura.pdf?sequence=1&isAllowed=y

Vernazza Páez, Álvaro A., & Prado Domínguez, A. J. (2021) «Estimation of the tax gap for Colombia: proactive measures for its reduction», Economic Research, 80(317), pp. 58–81. doi: 10.22201/fe.01851667p.2021.317.78421.

Ponce, D. ( 2020), Tax planning for compliance with tax obligations in the commercial distributor bastidas Villacís Basvimart Cia Ltda. period 2020. Unpublished thesis. Ecuador: National University of Chimborazo. Institutional repository. http://dspace.unach.edu.ec/bitstream/51000/7007/3/TRABAJO%20DE%20TITULACI%c3%93N%20DAYANA%20DANIELA%20PONCE%20QUI%c3%91%c3%93NEZ-CPA.pdf

Quiroz, V. ( 2019), Detraction system and tax collection in accounting service provision companies, Comas – 2019. Unpublished thesis. Peru: César Vallejo University. Institutional Repository. https://repositorio.ucv.edu.pe/handle/20.500.12692/46846

Ramos, J., & Mendoza, L. (2018), The system of detractions of the igv and the effect on the liquidity of the company of Transportes y Negocios Alarcón Vega S.A.C. period 2014 – 2016. Unpublished thesis. Peru: Universidad Privada Antonio Guillermo Urrelo. Institutional repositotio. http://repositorio.upagu.edu.pe/bitstream/handle/UPAGU/740/Cont0061.pdf?sequence=1&isAllowed=y

Romero, S. (2021), Effects of the application of the Tax Regime for Microenterprises, designated as withholding agents within the regulatory framework of the Internal Tax Regime Law, Chapter I Art. 97.16. Unpublished thesis. Ecuador: Polytechnic University of Salesiana. Institutional repository. https://dspace.ups.edu.ec/bitstream/123456789/20997/1/TTQ438

National Superintendence of Customs and Tax Administration. (2022), Opening of account of detractions. VAT Detractions Regime [online] available in < https://orientacion.sunat.gob.pe/opeartividad-detracciones> [accessed: 15 March 2023].

National Superintendence of Customs and Tax Administration. (2022), Institutional Memory. MEMORIA 2021 [online] available in <https://www.sunat.gob.pe/cuentassunat/planestrategico/memoria/memoria2021.pdf> [accessed: 05 April 2023].

Superintendencia Nacional de Aduanas y Administración Tributaria (n.d.), Institutional Memory. National Superintendence of Customs and Tax Administration [online] available at < https://www.sunat.gob.pe/cuentassunat/planestrategico/memoria/memoria2021.pdf> [accessed: 10 April 2023].

National Superintendence of Customs and Tax Administration. (n.d.), Electronic Notifications [online] available at <https://orientacion.sunat.gob.pe/6620-09-notificaciones-electronicas-empresas> [accessed: 10 April 2023].

Támara, T. (2020), The principle of legality as a minimum requirement of legitimation of the criminal power of the State. Official Journal of the Judiciary [online] available at <https://revistas.pj.gob.pe/revista/index.php/ropj/article/view/267> [accessed: 12 January 2023].

Pedroni, F. V., Briozzo, A., & Pesce, G. (2022) «Microeconomic determinants of corporate tax evasion in emerging economies: the case of Argentina», Journal of Quantitative Methods for Economics and Business, 34, pp. 83–117. DOI: 10.46661/RevmetodosCuanteConempresa.5277.

Vilela, K., & Yovera, M. ( 2021), Detractions System and its Incidence on the Tax Obligations of Vehicle Maintenance Companies, Carabayllo – 2021. Unpublished thesis. Peru: César Vallejo University. Institutional repository. https://repositorio.ucv.edu.pe/bitstream/handle/20.500.12692/82796/Vilela_AKN-Yovera_SMDR-SD.pdf?sequence=1&isAllowed=y

Villazana, S. (2019). Regime of Detractions. In S. Villazana, Régimen de Detracciones (p. 16). Lima : Legal Gase.