BA School of Business and Finance, University of Latvia, Riga, LV-1013, Latvia

Volume 2026,

Article ID 523128,

IBIMA Business Review,

12 pages,

DOI: https://doi.org/10.5171/2026.523128

Received date: 30 March 2026; Accepted date: 11 June 2026; Published date: 27 June 2026

Academic Editor: Dariusz Wielgorka

Cite this Article as:

Hao HE (2026)," Persistent Differences in Innovation Efficiency: Evidence from Chinese Listed Firms “, IBIMA Business Review, Vol. 2026 (2026), Article ID 523128, https://doi.org/10.5171/2026.523128

Innovation efficiency reflects a firm’s ability to transform innovation inputs into technological outputs. While prior studies have identified various determinants of innovation performance, little attention has been paid to whether differences in innovation efficiency persist over time due to stable firm-specific characteristics. This study addresses this gap by examining the structural persistence of innovation efficiency among Chinese listed firms. Using a panel dataset of Chinese A-share listed firms from 2012 to 2023, comprising 37,658 firm-year observations, innovation efficiency is estimated through Stochastic Frontier Analysis (SFA) based on a Cobb–Douglas innovation production function. The persistence of innovation efficiency is then assessed using an intraclass correlation coefficient (ICC) framework. The results indicate that the average innovation efficiency of Chinese listed firms is 0.787, with substantial variation across firms. More importantly, approximately 66.4% of the total variation in innovation efficiency can be attributed to firm-specific and time-invariant factors, providing strong evidence of structural persistence. Additional analyses show that firm size is positively associated with innovation efficiency, whereas financial leverage has a negative effect. In contrast, the effective tax rate does not exhibit a robust relationship with innovation efficiency after controlling for firm fixed effects. These findings suggest that long-term innovation efficiency is primarily shaped by persistent organizational capabilities and internal resources rather than short-term external factors. The study contributes to the literature on innovation efficiency and firm heterogeneity and offers policy implications for fostering sustainable innovation capacity.

Innovation is crucial for enterprise competitiveness and can promote economic development across the board of our country currently. But different companies have varying degrees of innovation output after converting the input factors of innovation; this degree is often called Innovation Efficiency. Taking into account the above situations, there may be various factors affecting the effectiveness of innovation and they are caused by different reasons (Dosi, 1988; Griliches, 1990-1994).

Most current research has focused on isolating different causes that affect innovation effectiveness under constrained resources or individual institutions thus far. Although this study offers important clues about the cause of innovation achievement; relative to this issue remains less explored – that is, if Innovation efficiency in general exhibits structural persistency through Time. In terms of innovation efficiency, it can be improved through improvements in organizational capabilities, management Models and learning Experiences (Barney, 1991; Cohen & Levinthal, 1990; Teece et al., 1997) to demonstrate relatively high persistence across a number of different enterprises over a certain period.

Based on this situation, this research explores the structure-induced long-run persistence of Innovation effectiveness by analysing a panel dataset containing Chinese-listed firms. Estimation of innovation efficiency employs stochastic frontier techniques to distinguish between non-innovator inefficiency and random error phenomena. This technique has become the routine method for firm-level efficiency evaluation since Aigner, et al. (1977) proposed it; Stochastic Frontier Analysis (SFA) (Meeusen & van den Broeck, 1977; Battese & Coelli, 1995; Coelli et al., 2005). Check whether the level of innovation kept in the long run and to which extent all firms innovate themselves are notable. Through record-keeping of stylised patterns of efficiency persistence, this paper helps improve our understanding of the structural changes in firm-level innovation performance, also provides policy suggestions for innovation policies related to research and development expenditures.

In terms of content contributions at present, this paper presents a certain form of Stylized Information on the stability of innovation-Efficiency through firm size panel data; Second, applying stochastic Frontier analysis to measure firms’ innovative efficiency under the context of China would provide an all-around assessment. The third one is that there is still a relationship between the Structure Role of firm-level capabilities in innovating outcomes according to previous studies at the long-term development difference level and advantages (Mueller, 1977; Wiggins & Ruefli, 2002; Patel & Pavitt, 1997).

Literature Review

Innovation Efficiency Measurement

Innovations Efficiency has become an important problem of the study on Firm’s Innovating performance. In general, this is referred to as a company’s ability to transform innovative inputs, including R&D expenditure of funds, people and so on, into innovative outcomes, Patent applications or other types of innovation. Several approaches to measuring how effectively a specific type of input transforms into observable innovation through observation have been proposed empirically so far; therefore, it is still one of the key topics addressed by research focusing on innovative activities and firm performance (Dosi, 1988; Griliches, 1990, 1994).

One commonly used approach is data envelopment analysis (DEA), which is a non-parametric method for evaluating relative efficiency by constructing an efficient frontier, in cooperation with Charnes, Cooper and Rhodes (1978)’s extended DEA framework within the scope of assessing economic entities at higher-efficiency levels among different Systems using this approach based on comparative performance evaluations between multiple units across various contexts, as it lacks functional dependence so far. There are deficiencies in the application of DEA that cannot solve statistical fluctuations; therefore, inefficient enterprises may be wrongly regarded as effective because of measurement errors or random disturbances in the data over time.

Another method is stochastic front-end analysis (SFA) which also takes into account both production technology differences in output levels at various scales due to uncertainty factors. Different from DEA, SFA includes a stochastic error term and can separate inefficiency from the random disturbance. In particular, the observation-based research on innovation may be affected by uncertainty in reporting, errors during issuance of reports, and subsequent alterations caused by external interference. Following these developments, subsequent works have expanded the application of the Stochastic Frontier Analysis method to panel data sets and inefficient behaviour models at a firm level in time-series studies. (Battese & Coelli, 1995) Nowadays, SFA has become one of the typical methods to evaluate productivity/efficiency expansively in a broad sense (Coelli et al., 2005; Kumbhakar and Lovell, 2000).

Based on many years of previous research into innovative outcome-researched input relationships within the field of innovation theory, Griliches (1990; 1994) argued that patents are essential signs of innovative behaviour due to their obviousness, but he admitted that there were shortcomings in the acquisition method and linkage issue among input-output problems was complex. According to Archibugi and Pianta’s views (1996), there are many kinds of innovations at various levels in the different fields. As shown in Table 4-3 of recent innovation outcomes statistics from the Oslo Manual (OECD/Eurostat, 2018), these new forms are an integrated multi-component system consisting of input factors, implementation processes, and end-effects.

Patent-based innovation efficiency indices serve as input-output indicators that capture both production-side information and the economic returns of firm-level innovation activities. Recent studies have shown that these indices also have economic relevance beyond the production process (see, e.g., Kong & Jiang, 2023). Therefore, the stochastic frontier approach, which assesses how close a firm operates to the innovation frontier, is well suited for estimating firm-level innovation efficiency.

Persistence in Firm Performance and Innovation Capability

Some related branches in the research explore how a firm’s performance changes over time. Research into early stages of the industrial economy revealed that there is usually an excess profit for enterprises across a long timeframe beyond competition effects; it has not completely evaporated. (Mueller, 1977). Building on this line of inquiry, Wiggins and Ruefli (2002) showed that some firms sustain superior performance for more than a decade, while others do not, highlighting the temporal dynamics of competitive advantage.

Long-term differences among firms may be explained by the resource-based view of the firm. Barney (1991) suggests that a company requires valuable, rare, inimitable, and non-substitutable resources to achieve sustained competitive advantage. Similarly, the absorptive capacity literature emphasises that firms differ systematically in their ability to recognise, assimilate, and exploit external knowledge (Cohen & Levinthal, 1990; Zahra & George, 2002).

Based on subsequent studies by other researchers on the definition of dynamic capabilities, Teece-Pisano-Shuen (1997) suggest that a company creates enduring comparative advantages by inheriting some fundamental elements from its original origin. In the latter stage, at this point where the external environment undergoes changes requiring new combinations, upgradings or restoration of internal resources, subsequently, some other scholars focus on dynamic capabilities forming a path through time and change in management methods or normalized skills accumulated within daily operations (Eisenhardt & Martin, 2000; Helfat & Peteraf, 2003). One party believes that enterprises possess technological strength due to developmental trends, and it has been strengthened through continuous innovation experiences; it is still influential to some extent.

Therefore, the trend of innovation output might also show periodicity. Companies can convert innovation input into output quickly and efficiently by using cutting-edge technology, excellent management methods, fast-product update speed, etc. On the contrary, those lacking innovation abilities will remain relatively underutilised. Reiteration of the concept that ability encompasses more than a single dimension from recent research into innovative capability is an integrated multi-dimensional system for enhancing organisational effectiveness and business performance. (Moreira et al., 2024)

Though extensive work in recent years has examined firm Performance Persistence, Technological Competence and Dynamic Capabilities, relatively little is known about how Innovation Efficiency behaves in this regard. Most previous studies have focused on the reason for an increase or decrease in how much a company’s innovative output leads to profit, and, at present, these factors may vary from one industry to another.

Research Gap

Extensive research has examined innovation efficiency, firm innovation capabilities, and performance persistence separately. To this day, there is no unified system of study in any field. Additionally, relatively fewer attention has been paid to whether the innovation-efficiency gap exists consistently over time and what causes it based on the structure of each company’s enterprise.

The problems in the background section concern academic research and policy implementation separately. Innovation efficiency shows relatively stable characteristics and is attributed to endowment structural factors of the enterprise; thus, it will not be influenced by short-term policy changes substantially. However, in terms of the main reasons affecting reduction in effect, policies’ responses are relatively fast. Thus, through examination of the structure-based persistence of innovation effectiveness, we can have a deeper understanding of how firms achieve their innovative outcomes from multiple perspectives for further studies on firm-specific characteristics and capability formation mechanisms in related literature (Mueller (1977); Barney, (1991); Wiggins & Ruefli, (2002)).

Therefore, this study contributes to other studies in two aspects through its results: Firstly, using panel data from Chinese-listed companies and applying stochastic frontier analysis to estimate firm-level innovation efficiency; Next, determining if there exists a Structure of Persistence in the Innovation Efficiency by Testing how Much This Difference Can Be Explained By Stable Firm-Level Factors. Thus, this paper connects efficiently with other studies on the relationship among firms’ longevity, innovativeness and dynamism to conduct further research. It also provides some empirical evidence on the positive economic impact of innovation efficiency at the firm level recently (Kong et al., 2023).

Data and Methodology

Data

This study selects panel data of Chinese A-share listed companies. Firm-level financial and innovation-related data are obtained from public databases. Based on the typical approach of innovation-efficiency research in academic papers, this paper will focus on enterprises with sufficient data sources for R&D inputs and outputs and will mainly use patent-based indices which are commonly used in empirical studies of innovations and productivity (Griliches (1990,1994); Archibugi & Pianta (1996); OECD/Eurostat (2018)).

Through several means, it has been confirmed that the data are reliable. First, observations with missing essential variables are excluded. Secondly, outliers have been eliminated to reduce their influence on the results. All the above steps were completed, and finally obtained a panel dataset containing numerous annual observations of observed public companies (Griliches, 1990, 1994; Kong et al., 2023).

The dataset contains firm-level information on R&D investment and innovation outputs (such as the number of patents). Following the approach of Griliches (1990, 1994) and Kong et al. (2023), I use this dataset to establish an innovation production function and estimate firm-level innovation efficiency.

Stochastic Frontier Analysis of Innovation Efficiency

This paper estimates firm-level innovation efficiency using a Stochastic Frontier Analysis (SFA) approach. Based on the traditional stochastic frontiers’ literature (Aigner et al., 1977; Meeusen & Van Den Broeck, 1977; Battese & Coelli, 1995), we specify a Cobb-Douglas innovativeness-production function with patent-output expressed as an aggregate of R&D investment, capital inputs and labour-inputs.

The stochastic frontier model can be expressed as follows:

where denotes the number of patent applications of firm i in year t;, , and represent R&D expenditure, capital input, and labor input, respectively, is a two-sided random error term capturing statistical noise, and ≥0 is a one-sided inefficiency term. Following the standard SFA framework, it is assumed that ,while , i.e., a half-normal distribution.

Firm-level innovation efficiency is calculated following the standard SFA literature (Coelli et al., 2005; Kumbhakar & Lovell, 2000) as:

where represents the technical efficiency of firm i in year t, and the efficiency score ranges from 0 to 1, where higher values indicate that firms operate closer to the innovation frontier and are more efficient in transforming innovation inputs into technological outputs.

Estimation procedure

The stochastic frontier model is estimated using maximum likelihood estimation (MLE), which jointly estimates the parameters of the production function and the variance components of the error terms. Specifically, the composed error term is decomposed into a two-sided random noise component () and a one-sided non-negative inefficiency component ().

The variance parametersand are estimated, and the ratio is used to assess the relative importance of inefficiency relative to random noise, where λ captures the contribution of inefficiency relative to statistical noise.

A likelihood ratio (LR) test of the null hypothesis

is conducted to verify the presence of inefficiency effects, where the null implies the absence of inefficiency.

The firm-level innovation-efficiency score is obtained through the expected value of the inefficiency component given a composite of error terms; this follows the conventional specification for SFA. (Jondrow et al., 1982)

Persistence of Innovation Efficiency

This section tests whether innovation efficiency exhibits structural persistence, i.e., how much of its variation is explained by firm-specific structural factors. Based on such an interpretation in other scholars’ works concerning durable between-firm differences, it is considered to be evidence of significant structural heterogeneity (Mueller, 1977; Wiggins & Ruefli, 2002).

Specifically, we estimate a random effects model in this way:

where denotes the innovation efficiency of firm i in year t,is the constant term, represents the firm-specific effect capturing time-invariant characteristics, is the idiosyncratic error term.

Evaluation criterion for the persistence of innovation-efficiency is to use ICC, which is given by:

where denotes the variance of firm-specific effects, denotes the variance of the idiosyncratic error term.

A higher value of (ρ) indicates that a larger share of the variation in innovation efficiency is explained by persistent firm-level characteristics rather than short-term fluctuations.

Empirical Results

Descriptive Statistics

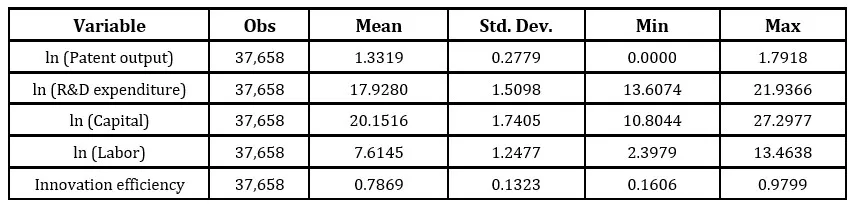

Table 1 displays the descriptive statistics for the primary explanatory variables employed in the stochastic frontier model. Based on these results, the variation in the effect of companies’ innovations is quite large; therefore, the productivity changes after transformational investments vary among different companies. Average Level of Innovative Efficiency: 0.787; The Individual Scores Rang from 0.161 to 0.980, which indicates certain Variability. Most companies are relatively close to the frontier of innovation; however, a few have considerably low level of performance.

Table 1: Descriptive statistics of the SFA sample

Notes: Innovation efficiency is estimated using stochastic frontier analysis (SFA). The sample consists of Chinese A-share listed firms during the period 2012–2023. Source: Author’s own composition.

In addition to R&D expenditures, capitals and labourers, there is also substantial variation within enterprises, indicating different resource-endowments and innovation-investment methods for the Chinese-listed companies under examination.

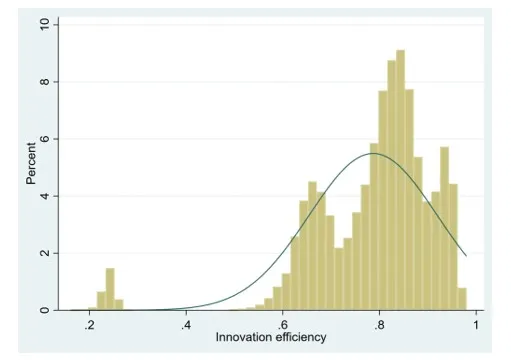

Fig 1. Distribution of innovation efficiency

Most companies are in an efficient operation level between 0.75 and 0.9; relatively few are at a low-efficiency or high-cost end.

Frontier Estimation of Innovation Efficiency

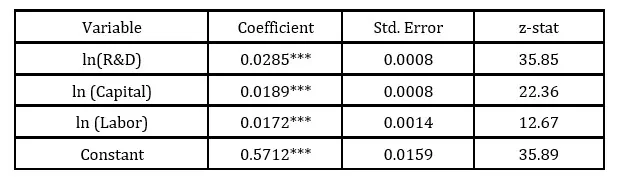

Table 2: Stochastic frontier estimation of innovation production

Notes: *** p < 0.01. The stochastic frontier follows a Cobb–Douglas innovation production function where patent output is explained by R&D input, capital, and labor. Source: Author’s own composition.

Table 2 shows the estimation results of the stochastic frontier innovation-production function. All the coefficients for R&D investment, capital and labour input are positive and have a statistically significant effect on the quantity of innovative outputs by companies.

Among them, R&D investment has a higher coefficient than others and is therefore the main factor promoting innovation results. From the above results, according to some other researchers’ conclusions, it is inferred that a company requires continuous substantial investments in knowledge during its innovation process and increases its R&D scale to promote development.

In addition, the variance parameters, that were obtained to identify how poorly managed some companies were, were used. The likelihood ratio test significantly rejects the null hypothesis of no inefficiency (p<0.001) to demonstrate that a stochastic frontier model is suitable for this study. Observing that firms have substantial differences in converting innovation inputs into outputs, the problem of efficiency-differentiation among these companies is now recognised.

Structural Persistence of Innovation Efficiency

Whether the phenomenon of innovation efficiency’s persistency depends on how much it is attributed to individual firms’ structural characteristics, the ICC value is 0.664, meaning about 66.4 per cent of the total change in innovation efficiency can be attributed to differences among companies; the rest is caused by changes in individual enterprises over time.

The above results provide sufficient evidence for the structural nature of innovation efficiency; thus, firm-specific differences in innovation performance mainly stem from long-standing characteristics and not immediate fluctuations.

According to theory research, in terms of firm-specific resources, organisational routine and accumulated knowledge have different impacts on a company’s long-term performance through the resource-based view, dynamic capabilities model and others. (Barney, 1991; Wiggins & Ruefli, 2002; Helfat & Peteraf, 2003)

Firm-Level Structural Effects

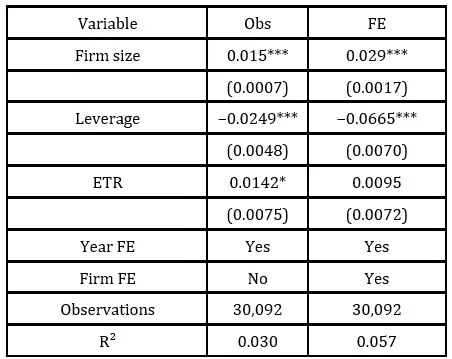

Table 3: Determinants of innovation efficiency

Notes:Standard errors are reported in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.10. Source: Author’s own composition.

Table 3 shows the estimation results of the influencing factors of innovative effectiveness. Using the collected data to conclude via a positively significant effect test, there has been an increase in innovative output as per unit of investment for large-scale firms. In this way, it can be observed that large companies have certain advantages; however, due to the limitations of their own conditions or business scale, they are constrained by finance in carrying out innovation activities and thus affecting the allocation effect of resources for such purposes. This suggests, from higher proportion of indebtedness for innovation activities may limit the ability to adapt flexibly; therefore, there are some uncertain issues with ETR as well. Although it is marginally significant at the baseline level, its significance disappears after controlling for firm-fixed effects; therefore, there is no systemic effect of tax-relevant factors on the variability of firms’ innovation-efficiency levels.

Therefore, according to this research conclusion, under the overall impact on innovation performance, structural characteristics associated with resource-endowment levels and finance are relatively more substantial compared with policies implemented through short-term regulation. Based on previous studies, it can be seen from this study as well that firms’ own abilities are crucial factors affecting long-term innovation capacity over time.

Discussion

There exists a strong persistence in the Structure of Innovation among firms based on comprehensive analyses across all cases. Thus, there are no significant differences among enterprises in terms of the transformation capability of their innovation input factors; rather, it is more related to inherent factors over a longer period.

Another cause of this may be a well-established technological foundation. Companies with higher investment in R&D can develop more advanced technologies to improve the efficiency of their own innovative activities, and expand absorptive capacity, thereby maintaining a stable and high level of innovation performance. This finding is consistent with previous research showing that accumulated knowledge and experience contribute positively to operational outcomes (Cohen & Levinthal, 1990; Patel & Pavitt, 1997).

Organisational routines and management Practices are another possible reason. Firms have built an efficient system of innovation management; there are reasonable incentive policies, good coordination between research and production departments in practice. Organisations keep their level of performance superior or inferior continuously across periods in relation to others’. According to the resource-based view and dynamic capability perspective, it helps explain that firm-specific routines and capabilities can enhance a company’s long-run competitiveness gap (Barney, 1991; Teece et al., 1997; Helfat & Peteraf, 2003).

Based on policies, it can be seen that short-term policy adjustments are less effective in enhancing innovation efficiency. Therefore, the policy will aim to enhance companies’ capabilities for continuous long-term innovations and expand their sources of knowledge, improve organisational capacity building, and optimize resource allocation efficiency. It can be inferred from this that the reason for the non-significant impact of tax-relevant factors on innovation efficiency empirically is because policies that are applied to companies gradually change their fundamental level of ability.

Conclusion

Examining whether Innovation Efficiency shows Structural Persistence at the Firm Level Based on Panel Data of Chinese Listed Companies, a stochastic frontier analysis (SFA) approach was used for estimating firm-level innovation-efficiency levels and measuring the degree of variation that is influenced by persistent factors specific to each enterprise.

It shows that each company has its own degree of innovation effectiveness to some extent; however, a large proportion originates from uncontrollable factors for the specific companies. Therefore, based on empirical observation at present, the effects generated by innovation changes between firms vary inversely with the underlying strength differences prior to these changes.

Firm Size positively affects the efficiency of innovation. Further analysis shows that The Impact Leverage negatively affects this relation. The effect of tax-related factors has been relatively weak, indicating that policies may be less effective in promoting Innovation Efficiency within a short time frame.

In summary, it shows a need for an enhancement in the capability of innovation performance overall. From the policy aspect, it indicates that enhancing firms’ innovation efficiency needs long-term effort in improving technical strength, organisational mechanisms and resource utilisation efficiency; it does not need only short-term policies’ intervention.

There is a deficiency in the above research. Furthermore, the perspective of studying how individual companies’ institutions affect their own innovation Performance in different Environments under various future research Directions can also be considered.

References

Aigner, D. J., Lovell, C. A. K. and Schmidt, P. (1977) ‘Formulation and estimation of stochastic frontier production function models,’ Journal of Econometrics, 6(1), 21–37.

Altuzarra, A. (2024) ‘Innovation persistence and firm growth: Do they go hand in hand?’ Journal of the Knowledge Economy, 15, 18590–18616.

Antonelli, C., Crespi, F. and Scellato, G. (2012) ‘Inside innovation persistence: New evidence from Italian micro-data,’ Structural Change and Economic Dynamics, 23(4), 341–353.

Barney, J. (1991) ‘Firm resources and sustained competitive advantage,’ Journal of Management, 17(1), 99–120.

Battese, G. E. and Coelli, T. J. (1995) ‘A model for technical inefficiency effects in a stochastic frontier production function for panel data,’ Empirical Economics, 20(2), 325–332.

Cefis, E. and Orsenigo, L. (2001) ‘The persistence of innovative activities: A cross-countries and cross-sectors comparative analysis,’ Research Policy, 30(7), 1139–1158.

Charnes, A., Cooper, W. W. and Rhodes, E. (1978) ‘Measuring the efficiency of decision-making units,’ European Journal of Operational Research, 2(6), 429–444.

Coelli, T. J., Rao, D. S. P., O’Donnell, C. J. and Battese, G. E. (2005) An introduction to efficiency and productivity analysis (2nd ed.), Springer.

Cohen, W. M. and Levinthal, D. A. (1990) ‘Absorptive capacity: A new perspective on learning and innovation,’ Administrative Science Quarterly, 35(1), 128–152.

Cui, X., Wang, C., Liao, J., Fang, Z. and Cheng, F. (2021) ‘Economic policy uncertainty exposure and corporate innovation investment: Evidence from China,’ Pacific-Basin Finance Journal, 67, 101533.

Cui, X., Wang, C., Sensoy, A., Liao, J. and Xie, X. (2023) ‘Economic policy uncertainty and green innovation: Evidence from China,’ Economic Modelling, 118, 106104.

Eisenhardt, K. M. and Martin, J. A. (2000) ‘Dynamic capabilities: What are they?’ Strategic Management Journal, 21(10–11), 1105–1121.

Geroski, P. A., Van Reenen, J. and Walters, C. F. (1997) ‘How persistently do firms innovate?’ Research Policy, 26(1), 33–48.

Griliches, Z. (1990) ‘Patent statistics as economic indicators: A survey,’ Journal of Economic Literature, 28(4), 1661–1707.

Griliches, Z. (1994) ‘Productivity, R&D, and the data constraint,’ American Economic Review, 84(1), 1–23.

Hall, B. H., Jaffe, A. and Trajtenberg, M. (2005) ‘Market value and patent citations,’ RAND Journal of Economics, 36(1), 16–38.

Helfat, C. E. and Peteraf, M. A. (2003) ‘The dynamic resource-based view: Capability lifecycles,’ Strategic Management Journal, 24(10), 997–1010.

Hirshleifer, D., Hsu, P.-H. and Li, D. (2013) ‘Innovative efficiency and stock returns,’ Journal of Financial Economics, 107(3), 632–654.

Howell, A. (2016) ‘Firm R&D, innovation and easing financial constraints in China: Does corporate tax reform matter?’ Research Policy, 45(10), 1996–2007.

Ipinnaiye, O., Lenihan, H., Mulligan, K., Doran, J. and Roper, S. (2025) ‘Innovation success in small and larger firms: Does persistence and diversity in R&D matter when building a unique knowledge base?’ The Journal of Technology Transfer. Advance online publication.

Kong, D., Yang, Y. and Wang, Q. (2023) ‘Innovative efficiency and firm value: Evidence from China,’ Finance Research Letters, 52, 103557.

Kumbhakar, S. C. and Lovell, C. A. K. (2000) Stochastic frontier analysis, Cambridge University Press.

Li, C., Xu, Y., Zheng, H., Wang, Z., Han, H. and Zeng, L. (2023) ‘Artificial intelligence, resource reallocation, and corporate innovation efficiency: Evidence from China’s listed companies,’ Resources Policy, 81, 103324.

Meeusen, W. and van den Broeck, J. (1977) ‘Efficiency estimation from Cobb-Douglas production functions with composed error,’ International Economic Review, 18(2), 435–444.

Moreira, A., Navaia, E. and Ribau, C. (2024) ‘Innovation capabilities and their dimensions: A systematic literature review,’ European Journal of Innovation Management, 27(3), 901–930.

Mueller, D. C. (1977) ‘The persistence of profits above the norm,’ Economica, 44(176), 369–380.

OECD/Eurostat (2018) Oslo manual 2018: Guidelines for collecting, reporting and using data on innovation (4th ed.), OECD Publishing.

Patel, P. and Pavitt, K. (1997) ‘The technological competencies of the world’s largest firms: Complex and path-dependent, but not much variety,’ Research Policy, 26(2), 141–156.

Peters, B. (2009) ‘Persistence of innovation: Stylised facts and panel data evidence,’ The Journal of Technology Transfer, 34(2), 226–243.

Qiu, L., Yu, R., Hu, F., Zhou, H. and Hu, H. (2023) ‘How can China’s medical manufacturing listed firms improve their technological innovation efficiency?’ Technological Forecasting and Social Change, 194, 122684.

Raymond, W., Mohnen, P., Palm, F. and van der Loeff, S. S. (2010) ‘Persistence of innovation in Dutch manufacturing: Is it spurious?’ The Review of Economics and Statistics, 92(3), 495–504.

Teece, D. J., Pisano, G. and Shuen, A. (1997) ‘Dynamic capabilities and strategic management,’ Strategic Management Journal, 18(7), 509–533.

Wiggins, R. R. and Ruefli, T. W. (2002) ‘Sustained competitive advantage: Temporal dynamics and the incidence and persistence of superior economic performance,’ Organization Science, 13(1), 81–105.

Xu, X. and Sun, M. (2025) ‘The impact of firm internationalisation on innovation persistence,’ European Journal of Innovation Management. Advance online publication.