Joaquim LEITE1, Cecília CARMO2 and Gastão CORREIA3

1Unidade de Investigação Aplicada em Gestão (UNIAG) –

Instituto Politécnico de Bragança (IPB), Bragança, Portugal

2Research Unit on Governance, Competitiveness and Public Policies (GOVCOPP) –

Universidade de Aveiro (ISCA-UA), Aveiro, Portugal

3Instituto Politécnico de Bragança (IPB), Bragança, Portugal

Volume 2026,

Article ID 765158,

IBIMA Business Review,

10 pages,

DOI: https://doi.org/10.5171/2026.765158

Received date: 4 March 2026; Accepted date: 9 June 2026; Published date: 15 July 2026

Academic Editor: António Fernandes

Cite this Article as:

Joaquim LEITE, Cecília CARMO and Gastão CORREIA (2026)," Enhancing Efficiency in Urban Water Services: Applying the Balanced Scorecard to the Portuguese Municipal Company AEP “, IBIMA Business Review, Vol. 2026 (2026), Article ID 765158, https://doi.org/10.5171/2026.765158

This study explores how the Balanced Scorecard (BSC) can enhance strategic management practices aimed at minimizing treated water losses in a municipal water utility. Although operational efficiency has shown improvement, unbilled treated water remained notably high in 2020, exceeding 17% during distribution. This ongoing inefficiency underscores the importance of systematic, theory-informed approaches for sustainable performance enhancement. A mixed-methods design was employed, combining qualitative insights with quantitative data derived from financial statements and managerial forecasting tools. These inputs were synthesized into a strategic map aligned with the four BSC perspectives, enabling the effective translation of strategy into measurable objectives. Findings indicate that implementing the BSC strengthened organizational alignment, refined planning processes, and enhanced performance assessment. The framework also clarified the connections between financial outcomes and non-financial performance drivers. Particular attention was given to the learning and growth perspective, highlighting the crucial role of employee engagement in addressing inefficiencies. This focus supports improvements in internal processes, such as technological modernization and infrastructure upgrades, which contribute to stronger customer relationships and increased awareness of efficient water use. Overall, the study confirms the BSC as a valuable tool for strategic governance and evidence-based decision-making in the water utility sector.

Keywords: Balanced Scorecard (BSC), Resource Efficiency, Urban Water Utility Performance, Sustainability in Water Services.

Introduction

A Portuguese municipal company, Águas e Energias do Porto (AEP), posed the following real challenge to academic researchers: although the company has recorded several positive management indicators in recent years (until 2020), it has a percent-age of unbilled treated water (in recent years) at the level of supply to citizens of around 17% (Águas e Energia do Porto [AEP], 2020a, 2020b). This corresponds to a good quality of service according to the reference ranges of the regulator (Entidade Reguladora dos Serviços de Água e Resíduos [ERSAR], 2020). This result corresponds to an annual volume of 3,697,156 m3 of water, which is equivalent to a daily average of 10,129 m3.

This company has already been the subject of various academic studies in the field of management, including studies on the operationalization, implementation, and use of a Balanced Scorecard (BSC), considering the vision and strategy (Costa, 2015), without the specific objective of reducing the losses of water purchased but not sold to customers (unbilled water). Unbilled water is an efficiency indicator for managing entities because it represents the value of water that has been collected, treated, transported, stored, and distributed but not billed, and is made up of real losses, apparent losses, and unbilled authorized consumption (ERSAR, 2020). In this activity, upstream systems are those made up of a set of components upstream of the distribution network that connect the water medium to the downstream system. In turn, downstream systems are made up of a set of components that enable the water supply service to be provided to consumers. Systems can be integrated when the connection between the water environment and the consumer is provided by the same system.

The strategic indicators for monitoring the quality of the service provided to customers are based on three different subsystems (AEP, 2020a, 2020b; ERSAR, 2020): (1) indicators relating to the quality of the water and service perceived by customers; (2) indicators relating to the sustainability of the company, namely economic, financial, infrastructural, operational and human capacity; and (3) environmental sustainability indicators relating to the conservation of natural resources, in particular water resources.

An economy driven by sustainability objectives is based on the trust that companies and their management control systems communicate to stakeholders (Backes and Traverso, 2022; López et al., 2025). The strategic goal that defines an organization’s direction always takes into accounts the organization’s mission (Santos, 2014). Given that resources are limited, organizations manage resources according to strategic objectives. In the strategy map, the objectives are linked to the financial and non-financial perspectives of the BSC through an understanding of cause-and-effect relationships (Leite et al., 2026a, 2026b). The indicators (measures) assess the level of achievement of the objectives, and it is useful to link them to time-bound and quantified targets against which action plans (initiatives) can be developed (Kaplan and Norton, 1996). Although an organization must always strive to achieve its objectives, they must be realistic if they are to be achieved (Santos, 2014).

The cause-effect relationships in the BSC define a logical chain in which intangible assets are converted into tangible value, always taking into account efficiency, efficacy and effectiveness (Santos, 2014; Silva et al., 2025). The strategy map makes it possible to understand and visualize these cause-effect relationships based on the interactions between objectives (Kaplan and Norton, 2004; Wilson et al., 2004). These causal relationships make it easier to analyze and correct certain aspects that have a negative impact, or to change an objective or indicator that is no longer as important to the organization.

The BSC is a management control tool that clarifies not only the organization’s strategy, but also the factors that influence performance (Piantoni et al., 2024; Silva et al., 2025]. The strategy map also aims to improve the quality of teamwork and communication (Kaplan and Norton, 2004). Strategy maps (cause-and-effect relationships), which include four different perspectives – the financial perspective, the customer perspective, the process perspective and the learning and growth perspective – allow managers to organize useful information considering the vision and strategy (Kaplan and Norton, 1996; Leite et al., 2026a, 2026b). Effective water resource management needs to integrate sustainability into organizations’ management control systems, which means recognizing its strategic relevance (Beusch et al., 2022).

In general, the literature on sustainability in the BSC distinguishes between the stages of design and implementation on the one hand and use and evolution on the other (Mio et al., 2022). Sustainability is a strategic option that creates business value and contributes to the appropriate use of natural resources (Frostenson et al., 2022). Management control systems guide strategic implementation by influencing organizational behavior and ensuring that activities are controlled (Osma et al., 2022). The need for continuous strategic reorganization is the focus of public sector managers (Bianchi and Montemaggiore, 2008).

As the main objective of public sector organizations is not financial performance (Fontes et al., 2022), the original BSC model can indirectly translate sustainability aspects or be adapted according to each specific situation (Bobe et al., 2017). In the public sector, the perspective of providing a service to citizens may be more relevant than the financial perspective. However, public companies also need to be transparent in their management of public resources and can use strategic management tools typically used by private companies to improve their performance (Northcott and Taulapapa, 2012).

Stakeholders (government, community, financiers, suppliers, others) are interested in the non-financial information generated by management control systems, particularly information related to sustainability, but the success of decisions will always depend on the ability of managers to make the best strategic choices (Krylov, 2025; Monteiro et al.,2022). The effective use of sustainability practices in management control systems, strategically integrating economic, social, and environmental factors, can enhance business performance and improve profitability indicators (Qiu et al., 2022).

Given the situation described in the previous paragraphs, there are several opportunities for improvement (AEP, 2020a, 2020b; ERSAR, 2020): (1) rehabilitation of pipes and collectors; (2) strengthening of measures to prevent flooding due to dam-age to pipes; (3) adequate training of human resources; (4) prevention of structural collapse of collectors; and (5) control of emergency discharges. In response, the company’s main strategy has focused on the detection of breaks and malfunctions in the water distribution network, through the daily work of active damage control teams and rapid intervention to repair the anomalies detected, as well as the rebuilding of the network (AEP, 2020a, 2020b).

The strategic management of companies – public sector, private sector and social or cooperative sector (Abrantes, 2019) – involves a set of planning, monitoring, and control tools, with a particular focus on useful and practical performance evaluation tools, which make it possible to solve management challenges. Among other valid alternatives, the BSC has become a useful tool for managers to make long-term decisions by organizing financial and non-financial information (Cheng et al., 2018; Cooper et al., 2017; Kaplan and Norton, 1996).

In this context, the aim of this study was to understand how and why to use the BSC as a management tool for the challenge of reducing the indicator of unbilled water in a public water supply company. Given this challenge for academic research, a case study was justified as a research method, supported by the theoretical framework of sustainability and the BSC, with the aim of organizing information in order to implement management alternatives as appropriate to the challenge in question.

The study is divided into three parts. It begins with a theoretical framework in the context of BSC and sustainability, highlighting the concepts inherent to water losses in municipal water companies. Next, it presents the scientific methodology chosen: a case study of the municipal company AEP. Finally, the results present four strategic objectives, one in each perspective of the BSC, culminating in a strategic map that translates the cause-effect relationships between these objectives. As this is also about the sustainable management of water, it was justified to complement the approach from a sustainability perspective.

Methodology

In line with the research question, the aim of this study is to understand how and why BSC can be used to reduce treated water losses in a municipal water distribution company. Therefore, a theoretical framework in the context of sustainability (Beusch et al., 2022; Frostenson et al., 2022; Monteiro et al., 2022) and BSC (Cheng et al., 2018; Cooper et al., 2017; Kaplan and Norton, 1996; Piantoni et al., 2024) is considered appropriate. The research method chosen was the holistic single descriptive case study because it is suitable for answering questions such as how and why (Yin, 2018). This holistic single case study method is widely used in qualitative research that seeks analytical interpretation in a concrete context rather than generating statistical generalizations (Parker, 2012).

AEP was the municipal company chosen for this academic research. The data were collected by analyzing documents from the following entities:

– Annual Report on Water and Waste Services in Portugal 2019 (ERSAR, 2020).

The analysis of these documents played a fundamental role in this work, as all the proposed objectives considered the follow-up work that AEP is doing to reduce un-billed water, taking into account sustainability and ongoing technological developments.

Results

This section of the findings begins with a brief overview of the company that is the subject of this study. It then proceeds to explain the four perspectives of the BSC, followed by the final strategy map showing the identified cause-and-effect relationships.

Presentation of the Company

AEP is a Portuguese municipal company founded in October 2006, whose share capital is wholly owned by the municipality of Porto, although it is legally, administratively, and financially autonomous (AEP, 2020a, 2020b). The company’s social objective is the integrated and sustainable management of the entire urban water cycle in the municipality of Porto, namely: (i) water distribution, (ii) wastewater collection and treatment, (iii) storm water drainage, (iv) management of watercourses (rivers and urban streams), (v) management of the seafront, and (vi) energy management and promotion of environmental education and sustainability.

With more than 158,000 customers, the vision of this municipal company is to be “an internationally recognized benchmark company in the management of the urban water cycle” (AEP, 2020a, 2020b). The company’s mission is to ensure the complete and effective management of the urban water cycle, creating economic and social value, focusing on the customer, developing good environmental management practices and internal motivation (AEP, 2020a, 2020b), taking into account its values: (1st) Sense of Public Service, (2nd) Fairness, (3rd) Sustainability, (4th) Transparency, (5th) Trust, (6th) Innovation and (7th) Excellence.

Due to the Covid-19 pandemic, sales and services decreased by 6.4% in 2020 (AEP, 2020a). Compared to the previous year, there was a 23.5% decrease in the volume of non-household customers due to the suspension or slowdown of trade. There was an increase of 4% in the household sector due to closures, teleworking, lay-off, and school closures. This had a negative impact on the financial perspective and, although it weighed on the company’s accounts, the volume of investment totaled 18.2 million euros.

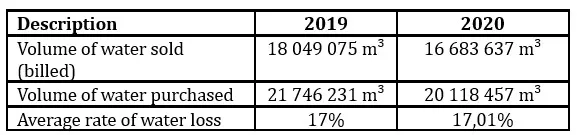

Table 1 illustrates the level of water losses (in m³) by comparing the volume of water purchased from Águas do Douro e Paiva company (the water supplier) with the volume of water sold and billed to end users in 2019 and 2020.

Table 1: Average rate of unbilled water loss

Source: Authors’ own elaboration based on AEP (2020a, 2020b)

The persistence of the average level of losses in recent years, which has always been higher than 17%, makes the target of reducing this average to 15% realistic and even ambitious. With the aim of reducing unbilled water, this municipal company has created a program with a series of internal strategies and targets for 2019 to 2021, with the main objective of achieving an overall figure of 15% for this index by the end of 2022 (AEP, 2020a, 2020b).

In order to achieve this target of 15% in the average rate of (unbilled) water losses, the company’s action program was based on the following pillars (AEP, 2020a, 2020b): (1) Reinforcement of teams specialized in the active and rapid detection of leaks and faults using acoustic loggers and reduction of the time taken to carry out these interventions; (2) Renovation and replacement of equipment (pipes, pressure valves, meters, calipers); (3) Optimization of consumption calculation models; (4) Execution of contracts for the replacement of the supply network and definition of 70 new water pressure measuring points; and (5) Reinforcement of operations to check zero and high consumption meters.

It was in this context that the assessment of financial and non-financial performance through a strategic management tool such as the BSC, enhanced by the implementation of a new business intelligence system in the company, was called into question. Thus, in 2020, the main activities carried out by the company were aimed at the following (AEP, 2020a, 2020b): (1st) Reviewing performance indicators and redefining targets; (2nd) Monitoring the company’s monthly performance by evaluating management indicators, analyzing results, and producing management reports; (3rd) Automating data collection to calculate indicators; and (4th) Creating new daily indicators to monitor performance.

Financial Perspective

In 2019, an investment of 3.9 million euros was made, covering the replacement of 27 kilometers of pipelines, 1,913 house connections and 190 hydrants (AEP, 2020a, 2020b). With a view to improving the sustainability of the infrastructure and reducing unbilled water, the company awarded two new contracts for the replacement of pipe-lines during the period in question, for a value of approximately 1.5 million euros. It also launched a program to reduce unbilled water, including a set of internal strategies with targets for the period 2019 to 2021, with the aim of reducing these losses to 15% by the end of 2022. Table 2 summarizes the objective, indicator, target, and initiative.

Table 2: Financial perspective for the municipal company AEP

Source: Authors’ own elaboration based on AEP (2020a, 2020b)

By reducing losses due to water not being billed to customers, the company aims to increase its financial income, which must also compensate for upstream investments in the long term. By managing the non-financial perspectives (customers, internal processes and learning and growth), this desired financial performance will be a con-sequence.

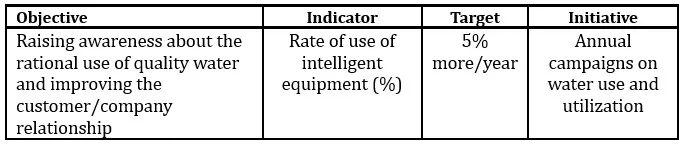

Customer Perspective

All the company’s activities are focused on meeting customers’ needs and exceeding their expectations whenever possible (AEP, 2020a). The Customer Management Unit is responsible for liaising with all customers, regardless of the service provided, man-aging the various communication channels, and dealing with requests for information and complaints. For continuous improvement, this Customer Management Unit is developing a project aimed at ensuring accurate billing of services and customer satisfaction, including:

(1) streamlining communication channels; (2) standardizing the flow of customer requests; (3) updating customer data; and (4) increasing billing based on actual readings (AEP, 2020a).

For the future, the company plans to:

(1) increase the number of customers using electronic billing and direct debit; (2) increase the number of customers registered with the digital meter and the app; (3) maintain the volume of actual readings and the level of quality; (4) reduce the number of complaints; and (5) focus processes on improving results (AEP, 2020a). Table 3 summarizes the objective, indicator, target, and initiative.

Table 3: Customer perspective for the municipal company AEP

Source: Authors’ own elaboration based on AEP (2020a)

The main objective set by the company is to meet the needs of customers and exceed their expectations whenever possible, with the strategic aim of raising awareness of the rational use of quality water and improving the customer/company relationship. Increasing the number of bills based on real values will have a positive impact on both the company and the consumer, as real readings avoid errors due to poor consumption estimation. It can also help to detect water leaks (visible or not), which can reduce water losses in the network.

Internal Process Perspective

Also close to the customer is the company’s Operations Management Unit, which is responsible for daily service requests from customers and emergencies such as bursts, flooding, water shortages, low pressure, and blocked collectors (AEP, 2020a). The water supply area has a budget of 19.3% for the modernization and replacement of pipes and meters, which could reduce real losses and increase the reliability of the system. This will have a positive impact not only financially, but also in terms of the company’s image with customers, i.e. there is an interdependence between non-financial and financial performance indicators. Table 4 summarizes the objective, indicator, target, and initiative.

Table 4: Internal process perspective for the municipal company AEP

Source: Authors’ own elaboration based on AEP (2020a)

The installation of new meters and the modernization of pipelines contribute to the automation of processes, the reorganization of work routines, an improvement in the productivity of teams and a reduction in the loss of water resources. During 2020, 2,187 meters were installed, thus surpassing the number of meters installed the previous year and the target of 1,720 meters, which corresponds to an increase of 12.5% (AEP, 2020a). With a focus on reorganizing work routines and improving team productivity, the company’s Call Centre was analyzed which, because of the Covid-19 pandemic crisis, saw an increase in membership of 28.9% (AEP, 2020a).

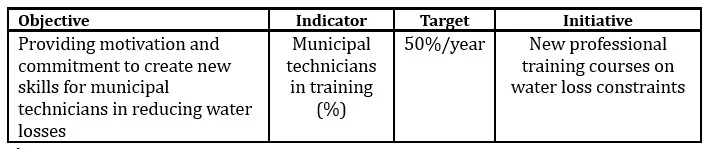

Learning and Growth Perspective

The company’s Human Resources department is responsible for managing its people and promoting best practices in people management and leadership (AEP, 2020a). The company has launched a project called “People, Culture and Organization” with the aim of developing an integrated people management model based on three pillars (AEP, 2020a): (1) Corporate Project, which includes the mission, values, and strategy; (2) Management System, which consists of models and tools; and (3) Leadership, which consists of performance models. The objectives of this project are based on motivation and demand, improving cooperation and vertical communication, and promoting employee participation, which leads to the creation of ideas, commitment, and a sense of responsibility.

Given the size and growth of the company, it was essential to modernize and up-date the available IT tools (new business intelligence system) for human resources management (AEP, 2020a). The Human Resources department supports decision-making and ensures good administrative and legal practices, consciously and safely managing employees, promoting correctness and fairness in recruitment and selection, salary processing based on biometric data, contract management, health, hygiene and safety at work, training management and performance evaluation. The company maintains occupational medicine as a priority area of intervention in its human resources policy, valuing the workplace as the place of choice for primary prevention of occupational risks, health protection and access to health services. Workplaces are safe and provide employees with motivation and commitment. In this context, the objective, indicator, target, and initiative are summarized in Table 5.

Table 5: Learning and growth perspective for the municipal company AEP

Source: Authors’ own elaboration based on AEP (2020a)

The company is committed to continuous employee professional development and satisfaction. In fact, training is essential to improve the skills of the workforce, which has a significant impact on the quality of the company’s services. For example, in the case of telemetry meters, it is necessary for workers who are unfamiliar with this new equipment to receive training to improve their performance and safety. Investing in professional training valorizes the company’s existing know-how and helps to develop talent.

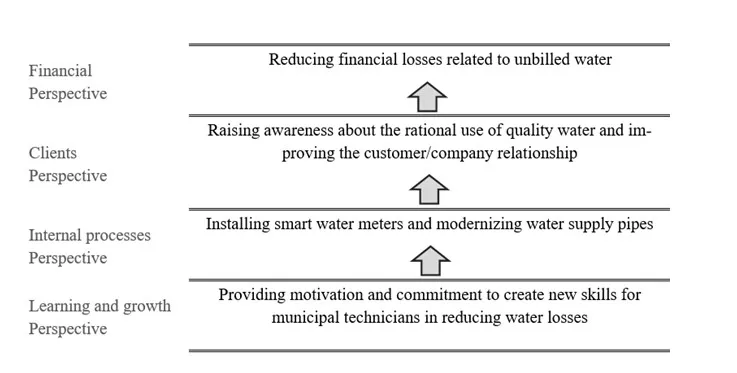

Strategic map

After presenting and justifying the company’s strategic objectives in the previous sections, a strategic map has been drawn in Figure 1 to help visualize the cause-and-effect relationships between each objective in each perspective of the BSC for AEP.

Figure 1. Cause-effect relationships for the municipal company AEP

According to Figure 1, the motivation and commitment of the municipal technicians to the large amount of water that is purchased but not billed, implying losses, is the basic objective of the learning and growth perspective. This objective has an impact on the necessary installation of new and modern equipment in terms of internal processes, with a direct consequence on the improvement of the company’s relationship with its customers, raising awareness of the correct use of quality water. Finally, it has a financial impact on revenue by reducing losses due to water purchased but not billed to customers.

Discussion and Conclusion

According to the results of this research, the management planning and control of companies shows causal relationships between strategic, financial, and non-financial objectives, without necessarily referring explicitly to the BSC tool or any other. However, by organizing each objective, indicator, target, and initiative into the four perspectives of the BSC, it becomes clearer how this tool can help to distinguish between financial and non-financial information and clarify causal relationships that support decision-making (Cheng et al., 2018; Cooper et al., 2017; Kaplan and Norton, 1996). Clarifying the factors that affect performance enhances the potential of the BSC as a strategic tool in organizations (Fontes et al., 2022; Piantoni et al., 2024), both in the design and implementation phases (Mio et al., 2022).

The need for efficiency in the proper management of water resources is also linked to the need to integrate sustainability aspects into management planning and control systems, thus demonstrating their strategic relevance (Beusch et al., 2022). In this way, sustainability management creates business value and reflects strategic choices that contribute to the best use of natural resources (Frostenson et al., 2022), directly influencing organizational behavior (Osma et al., 2022). The potential for continuous strategic reorganization through BSC is relevant in both the private and public sectors (Bianchi and Montemaggiore, 2008), including the sector of water supply to citizens. Indeed, the quest to improve corporate profitability indicators benefits from the efficient adoption of sustainability practices based on economic, social, and environmental factors (Backes and Traverso, 2022; Qiu et al., 2022).

This case study focused on a municipal water distribution company, AEP, with the challenge of understanding how to reduce treated water losses with the support of the BSC. Therefore, sustainability and BSC were the appropriate theoretical framework for this academic research. Relevant documentary data were collected from the water distribution company, as well as from the company that produces this water and the public regulator of the sector. It was possible to clarify the strategic objectives and establish a cause-effect relationship (strategy map) in order to achieve a final financial objective: To increase the financial revenues associated with the reduction of the unbilled water tariff in a Portuguese municipal water company.

As this is a case study of a single company, the results should not be used to standardize planning and control systems in water companies, as it is only an analysis of a single organization. As a result, the conclusions are limited to the company analyzed, as the organizational culture and the resources available are factors that could influence the results of the study in other companies and other sectors of activity.

For future research, it is suggested that other water distribution organizations be studied, using the BSC as a management tool and comparing organizations to understand which aspects differ between them and which aspects lead to better results. A different research methodology is also suggested, namely quantitative research as an alternative to the case study, as well as studying other strategic challenges/goals from a BSC perspective or even another theoretical framework.

Acknowledgment

This work was supported by national funds through FCT – Fundação para a Ciência e Tecnologia, I.P. under the project UNIAG UID/04752/2025 (DOI 10.54499/UID/04752/2025)

This work was financially supported by the UID/04058/2025 Research Unit on Governance, Competitiveness and Public Policies (GOVCOPP), funded by national funds through FCT – Fundação para a Ciência e a Tecnologia.

References

Abrantes, R. L. (2019), ‘Aplicação da metodologia do balanced scorecard numa empresa municipal [Master’s project in Management, ISCTE – Instituto Universitário de Lisboa. ISCTE Repository],’ http://hdl.handle.net/10071/18808 (accessed: March, 2021)

Águas e Energia do Porto. (2020a), ‘Instrumentos de Gestão Previsional,’ https://www.aguasdoporto.pt/files/uploads/cms/1608305824-V0UyqneCB3.pdf (accessed: April, 2021)

Águas e Energia do Porto. (2020b), ‘Relatório de Contas 2019,’ https://www.aguasdoporto.pt/files/uploads/cms/1601390002-afhQ9HE722.pdf (accessed: March, 2021)

Backes, J. and Traverso, M. (2022), ‘Life cycle sustainability assessment as a metrics towards SDGs agenda 2030,’ Current Opinion in Green and Sustainable Chemistry, 38, 100683. https://doi.org/10.1016/j.cogsc.2022.100683

Beusch, P., Frisk, J., Rosén, M. and Dilla, W. (2022), ‘Management control for sustainability: Towards integrated systems,’ Management Accounting Research, 54(March), 100777. https://doi.org/10.1016/j.mar.2021.100777

Bianchi, C. and Montemaggiore, G. (2008), ‘Enhancing strategy design and planning in public utilities through “dynamic” balanced scorecards: Insights from a project in a city water company,’ System Dynamics Review, 24(2), 175-213. https://doi:10.1002/sdr.395

Bobe, B. J., Mihret, D. G. and Obo, D. D. (2017), ‘Public-sector reforms and balanced scorecard adoption: An Ethiopian case study,’ Accounting, Auditing & Accountability Journal, 30(6), 1230-1256. https://doi:10.1108/AAAJ-03-2016-2484.

Cheng, M., Humphreys, K. and Zhang, Y. (2018), ‘The interplay between strategic risk profiles and presentation format on manager’s strategic judgments using the balanced scorecard,’ Accounting, Organizations and Society, 70, 92-105. https://doi.org/10.1016/j.aos.2018.05.009

Cooper, D., Ezzamel, M. and Qu, S. (2017), ‘Popularizing a management accounting idea: The case of the balanced scorecard,’ Contemporary Accounting Research, 34(2), 991-1025. https://doi.org/10.1111/1911-3846.12299

Costa, G. (2015), ‘A operacionalização, implementação e utilização de um Balanced Scorecard numa Empresa Pública de Serviços: O caso da Águas do Porto [Master’s dissertation in Economics and Business Administration, Faculty of Economics, University of Porto],’ https://repositorio-aberto.up.pt/handle/10216/80475 (accessed: February, 2021)

Entidade Reguladora dos Serviços de Água e Resíduos (2020), ‘Relatório Anual dos Serviços de Águas e Resíduos em Portugal (RASARP 2019) – Caraterização do Setor de Águas e Resíduos (Volume 1),’ http://www.ersar.pt/pt/site-publicacoes/Paginas/edicoes-anuais-do-RASARP.aspx#BookID=4729 (accessed: March, 2021)

Fontes, C., Leite, J. and Fernandes, P. O. (2022), Structural Autonomy and Management Performance: An Influence Reinforced in the Particular Context of Portuguese Public Secondary Schools,’ Administrative Sciences, 12(4), 172. https://doi.org/10.3390/admsci12040172

Frostenson, M., Helin, S. and Arbin, K. (2022), ‘Organizational sustainability identity: Constructing oneself as sustainable,’ Scandinavian Journal of Management, 38(3), 101229. https://doi.org/10.1016/j.scaman.2022.101229

Kaplan, R. and Norton, D. (1996), ‘The Balanced Scorecard: Translating strategy into action,’ Harvard Business School Press.

Kaplan, R. S. and Norton, D. P. (2004), ‘Strategy Maps: Converting Intangible Assets into Tangible Outcomes,’ Harvard Business School Press.

Krylov, S. (2025), ‘Integrated business analysis as a result of the development of the concept of a balanced scorecard,’ Discover Sustainability, 6, 106. https://doi.org/10.1007/s43621-024-00758-6

Leite, J., Carmo, C. and Anes, H. (2026a), ‘ Integrating sustainability, balanced score-card and accounting information systems: A case in the automotive components industry,’ Lecture Notes in Networks and Systems, 1747, LNNS, 394–403. https://doi.org/10.1007/978-3-032-12879-9_36

Leite, J., Carmo, C. and Almeida, D. (2026b), ‘Non-Governmental Organizations and innovation in the fish productive chain: Combining the lenses of the sustainability balanced scorecard and information systems,’ Lecture Notes in Networks and Systems, 1747, LNNS, 370–381. https://doi.org/10.1007/978-3-032-12879-9_34

López, J. M., Fernández, A. G. and Valderrama, T. G. (2025), ‘A comprehensive dynamic balanced scorecard approach for the blue economy,’ Journal of Environmental Management, 391, 126367. https://doi.org/10.1016/j.jenvman.2025.126367

Mio, C., Costantini, A. and Panfilo, S. (2022), ‘Performance measurement tools for sustainable business: A systematic literature review on the sustainability balanced scorecard use,’ Corporate Social Responsibility and Environmental Management, 29(2), 367–384. https://doi.org/10.1002/csr.2206

Monteiro, A., Vale, J., Leite, E., Lis, M. and Kurowska-Pysz, J. (2022), ‘The impact of information systems and non-financial information on company success,’ International Journal of Accounting Information Systems, 45, 100557. https://doi.org/10.1016/j.accinf.2022.100557

Northcott, D. and Taulapapa, T. M. (2012), ‘Using the balanced scorecard to manage performance in public sector organizations,’ International Journal of Public Sector Management, 25(3), 166-191. https//doi.org/10.1108/09513551211224234

Osma, B, Gomez-Conde, J. and Lopez-Valeiras, E. (2022), ‘Management control systems and real earning management: Effects on firm performance,’ Management Accounting Research, 55(June), 100781. https://doi.org/10.1016/j.mar.2021.100781

Parker, L. (2012), ‘Qualitative management accounting research: Assessing deliverables and relevance,’ Critical Perspectives on Accounting, 23(1), 54–70. https://doi.org/10.1016/ j.cpa.2011.06.002

Piantoni, G., Dell’Agostino, L., Arena, M. and Azzone, G. (2024), ‘Assessing shared value in innovation ecosystems: A new perspective of scorecard,’ International Journal of Productivity and Performance Management, 73(11), 190–212. https://doi.org/10.1108/IJPPM-02-2023-0067

Qiu, F., Hua, N., Liang, P. and Dow, K. (2022), ‘Measuring management accounting practices using textual analysis,’ Management Accounting Research, 100818. https://doi.org/10.1016/j.mar.2022.100818

Santos, L. F. (2014), ‘Balanced scorecard: Contributos para a Implementação na Administração Local,’ https://comum.rcaap.pt/handle/10400.26/8602 (accessed: May, 2021)

Silva, A., Cardim, S. and Leite, J. (2025), ‘A Portuguese case study on performance monitoring in technology transfer and valorisation centres using the balanced score-card approach,’ The Journal of Organizational Management Studies, Vol. 2025, Article ID 372518. https://doi.org/10.5171/2025.372518

Yin, R. (2018), ‘Case Study Research and Applications: Design and Methods,’ 6th ed., Sage.

Wilson, C., Hagarty, D. and Gauthier, J. (2004), ‘Results using the balanced scorecard in the public sector,’ Journal of Corporate Real Estate, 6(1), 53-64. https://doi.org/10.1108/14630010410812234